Embed Size (px)

Citation preview

Multinationals and Transition

Business Strategies, Technologyand Transformation in Central

and Eastern Europe

Julia Manea and Robert Pearce

Multinationals and Transition

Also by Robert Pearce

GLOBALISING RESEARCH AND DEVELOPMENT (with Satwinder Singh)

INTERNATIONAL ASPECTS OF UK ECONOMIC ACTIVITIES (with Peter J. Buckley)

GLOBAL COMPETITION AND TECHNOLOGY

MULTINATIONALS, TECHNOLOGY AND NATIONAL COMPETITIVENESS (withMarina Papanastassiou)

PROFITABILITY AND PERFORMANCE OF THE WORLD’S LARGEST INDUSTRIALCOMPANIES (with John H. Dunning)

THE GROWTH AND EVOLUTION OF THE MULTINATIONAL ENTERPRISE

THE INTERNATIONALISATION OF RESEARCH AND DEVELOPMENT BY MULTINATIONAL ENTERPRISES

THE TECHNOLOGICAL COMPETITIVENESS OF JAPANESE MULTINATIONALS(with Marina Papanastassiou)

THE WORLD’S LARGEST INDUSTRIAL ENTERPRISES (with John H. Dunning)

US INDUSTRY IN THE UK (with John H. Dunning)

Multinationals and Transition Business Strategies, Technology and Transformation in Central and Eastern Europe

Julia Manea and Robert Pearce

© Julia Manea and Robert Pearce 2004

All rights reserved. No reproduction, copy or transmission of this publication may be made without written permission.

No paragraph of this publication may be reproduced, copied or transmitted save with written permission or in accordance with the provisions of the Copyright, Designs and Patents Act 1988, or under the terms of any licence permitting limited copying issued by the Copyright Licensing Agency, 90 Tottenham Court Road, London W1T 4LP.

Any person who does any unauthorized act in relation to this publication may be liable to criminal prosecution and civil claims for damages.

The authors have asserted their rights to be identified as the authors of this work in accordance with the Copyright, Designs and Patents Act 1988.

First published 2004 by PALGRAVE MACMILLAN Houndmills, Basingstoke, Hampshire RG21 6XS and 175 Fifth Avenue, New York, N.Y. 10010 Companies and representatives throughout the world

PALGRAVE MACMILLAN is the global academic imprint of the Palgrave Macmillan division of St. Martin’s Press, LLC and of Palgrave Macmillan Ltd. Macmillan® is a registered trademark in the United States, United Kingdom and other countries. Palgrave is a registered trademark in the European Union and other countries.

ISBN 0–333–96874–3

This book is printed on paper suitable for recycling and made from fully managed and sustained forest sources.

A catalogue record for this book is available from the British Library.

Library of Congress Cataloging-in-Publication Data Manea, Julia.

Multinationals and transition : business strategies, technology and transformation in Central and Eastern Europe / Julia Manea and Robert Pearce.

p. cm.Includes bibliographical references and index.ISBN 0–333–96874–3 (cloth : alk. paper)1. International business enterprises—Europe, Central. 2. International business enterprises—Europe, Eastern. 3. Business planning—Europe, Central. 4. Business planning—Europe, Eastern. 5. Investments, Foreign—Europe, Central. 6. Investments, Foreign—Europe, Eastern. I. Pearce, Robert D., 1943– II. Title.HD2755.5.M354 2004338.8′8843—dc22 2003065252

10 9 8 7 6 5 4 3 2 1 13 12 11 10 09 08 07 06 05 04

Printed and bound in Great Britain by Antony Rowe Ltd, Chippenham and Eastbourne

v

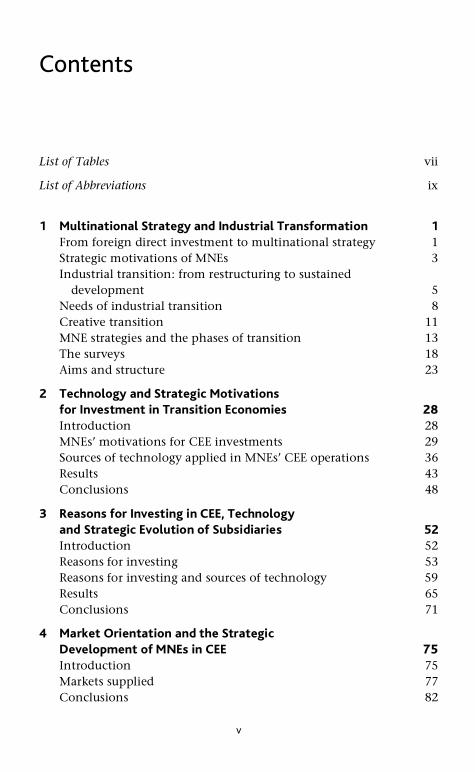

Contents

List of Tables vii

List of Abbreviations ix

1 Multinational Strategy and Industrial Transformation 1 From foreign direct investment to multinational strategy 1 Strategic motivations of MNEs 3 Industrial transition: from restructuring to sustained

development 5 Needs of industrial transition 8 Creative transition 11 MNE strategies and the phases of transition 13 The surveys 18 Aims and structure 23

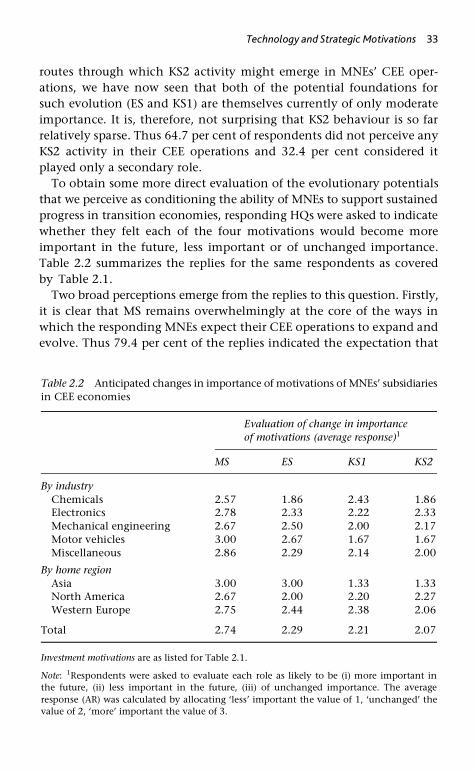

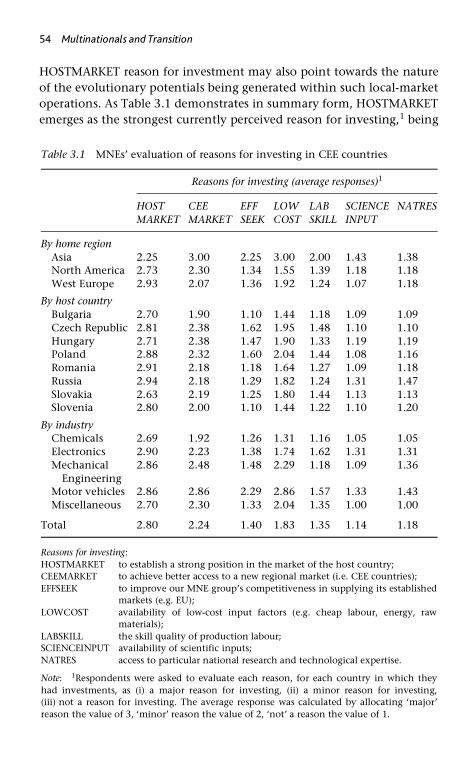

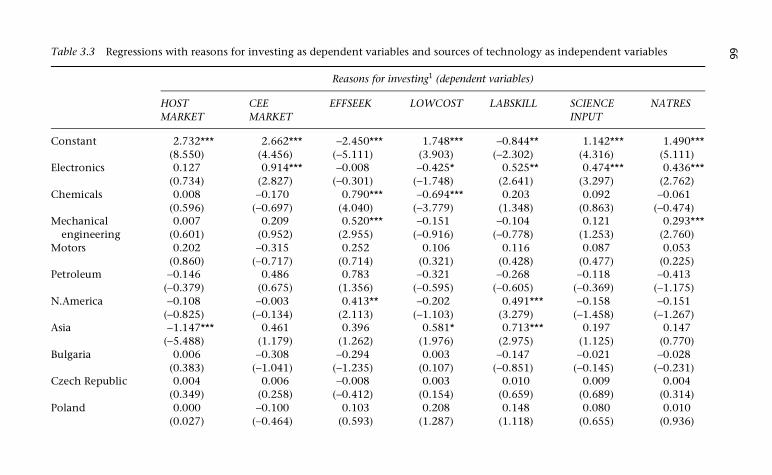

2 Technology and Strategic Motivations for Investment in Transition Economies 2828Introduction 28 MNEs’ motivations for CEE investments 29 Sources of technology applied in MNEs’ CEE operations 36 Results 43 Conclusions 48

3 Reasons for Investing in CEE, Technology and Strategic Evolution of Subsidiaries 52 Introduction 52 Reasons for investing 53 Reasons for investing and sources of technology 59 Results 65 Conclusions 71

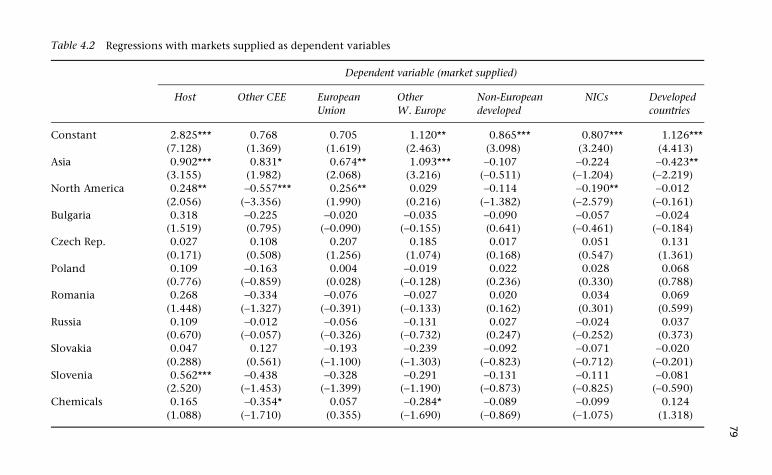

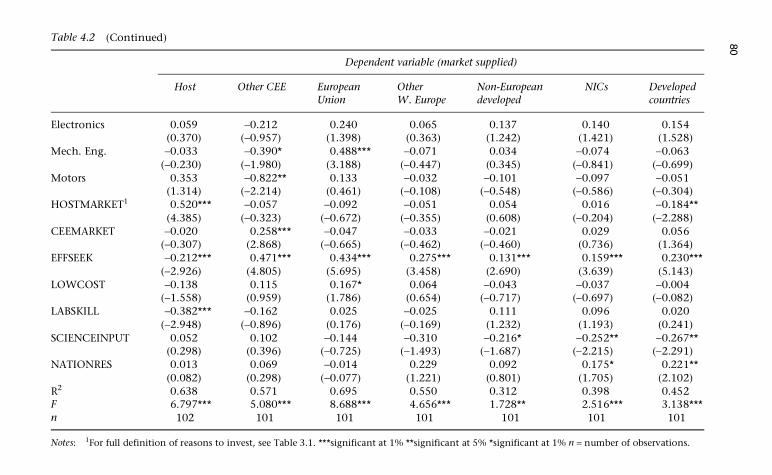

4 Market Orientation and the Strategic Development of MNEs in CEE 7575 Introduction 75 Markets supplied 77 Conclusions 82

vi Contents

5 Strategies of MNEs’ Subsidiaries in Romania 8585 Introduction 85 Classification of subsidiaries 86 Reasons for investing in Romania 87 Strategic roles of subsidiaries in Romania 90 Markets supplied by subsidiaries 93 Types of products produced 95 Sources of technology used by subsidiaries 99 Conclusions 102 Appendix: process of classification of subsidiaries 104

6 MNEs’ R&D and the Technological Transition in CEE 108108 Introduction 108 Knowledge capabilities in transition economies: a resource

and a constraint 109 Incomplete and distorted national innovation systems

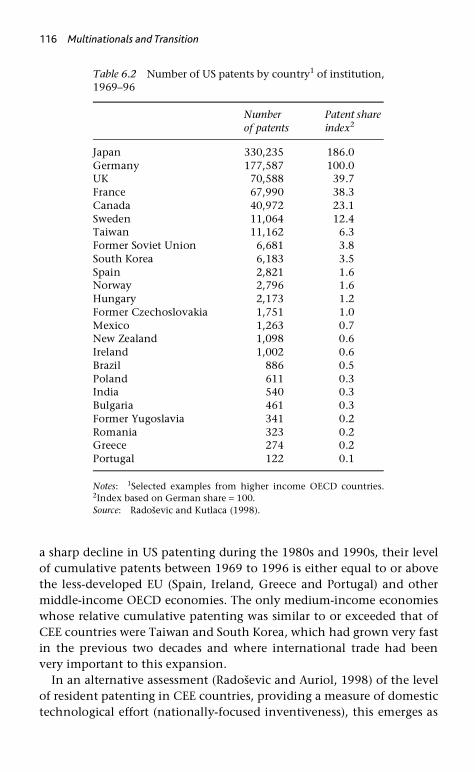

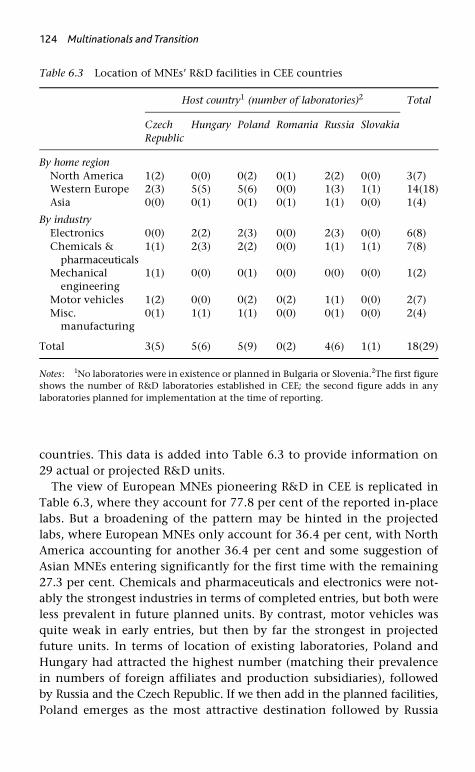

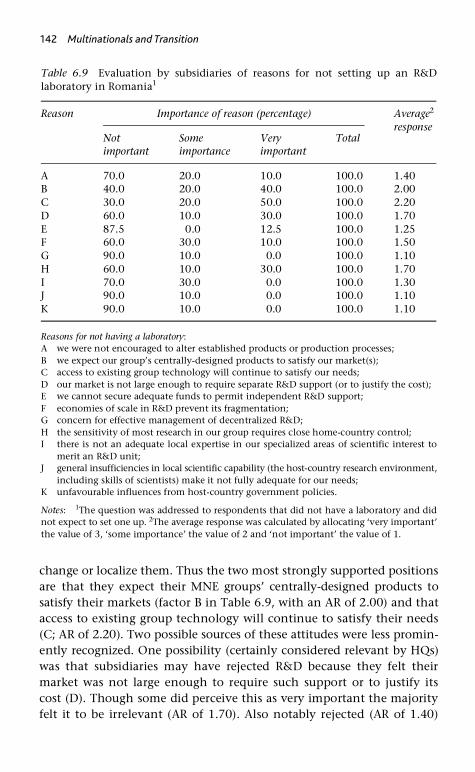

in transition economies 111 A brief assessment of the NSIs of CEE 114 MNE as a technology catalyst in transition economies 118 R&D strategy of MNEs and NSIs of transition economies 120 MNEs’ R&D in CEE 123 MNEs’ R&D in Romania 138 Conclusions 146

7 Input Supply Linkages of MNE Subsidiaries in CEE: Dependence or Development? 151151 Introduction 151 Foreign-owned firms, local input linkages and economic

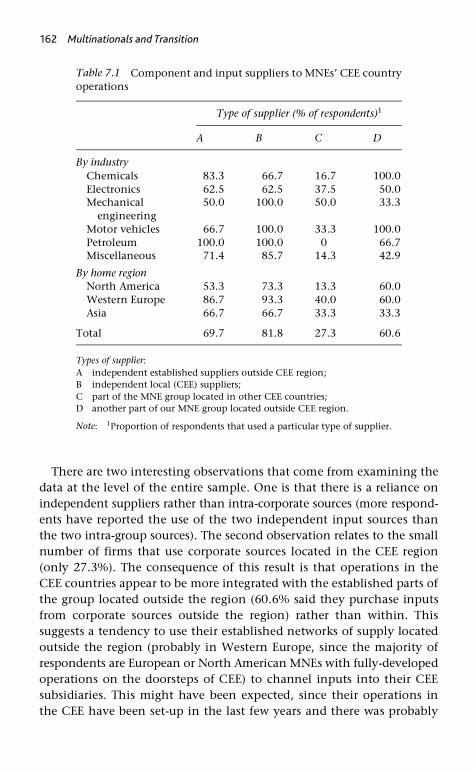

development: the debate 152 Sources of inputs used by MNE subsidiaries in CEE 161 Subsidiary-level influences on MNEs’ purchasing

patterns in CEE 165 Sources of inputs used by MNE subsidiaries in Romania 172 Conclusions 176

8 Conclusions 180180

Bibliography 187

Index 194

vii

List of Tables

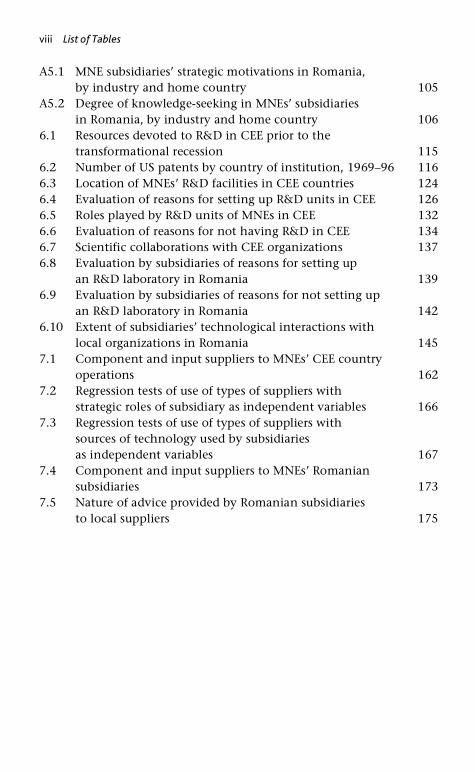

1.1 Population surveyed and response 19 1.2 Characteristics of responding HQs by home region

and industry 20 1.3 Location of MNEs’ CEE subsidiaries 21 1.4 Structure of respondents to Romanian subsidiary

survey, by home country and industry 232.1 Evaluation of the motivations of MNEs’ subsidiaries

in CEE economies 29 2.2 Anticipated changes in importance of motivations

of MNEs’ subsidiaries in CEE economies 332.3 Anticipated changes in importance of motivations

of MNEs’ subsidiaries in CEE economies by current strength of efficiency-seeking 35

2.4 Evaluation of technologies used in MNE subsidiaries in CEE economies 38

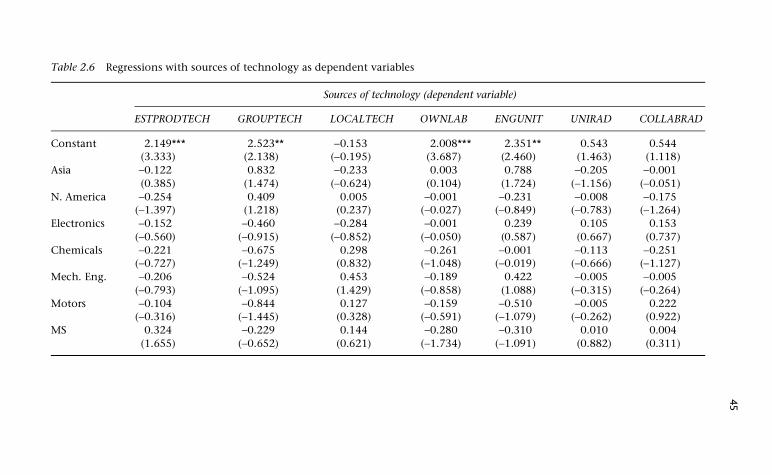

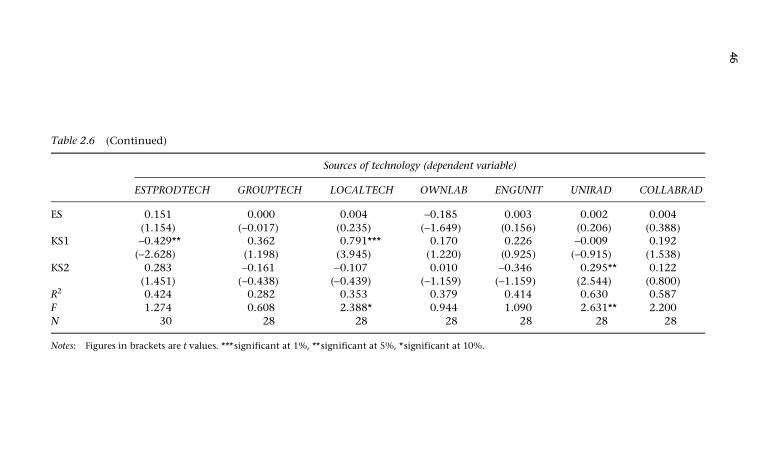

2.5 Summary of predicted relationships 44 2.6 Regressions with sources of technology as dependent

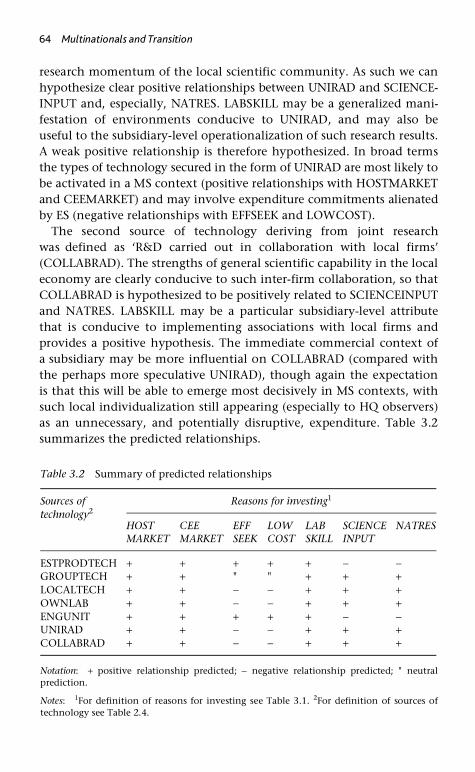

variables 45 3.1 MNEs’ evaluation of reasons for investing in CEE countries 54 3.2 Summary of predicted relationships 64 3.3 Regressions with reasons for investing as dependent

variables and sources of technology as independent variables 66

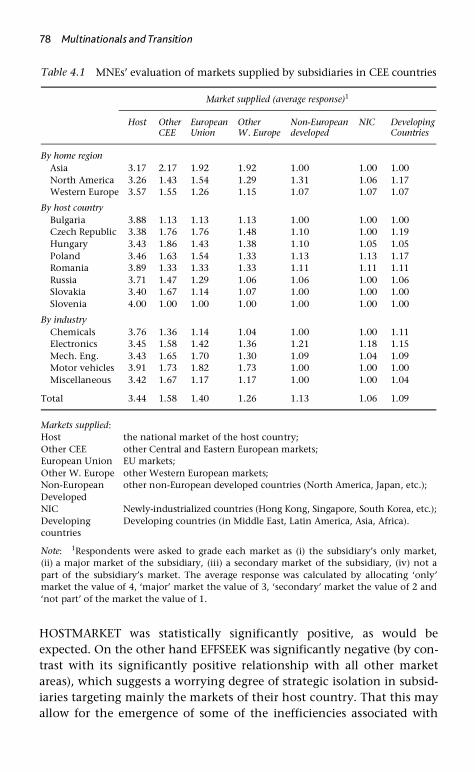

4.1 MNEs’ evaluation of markets supplied by subsidiaries in CEE countries 78

4.2 Regressions with markets supplied as dependent variables 79 5.1 Classification of MNEs’ subsidiaries in Romania 86 5.2 Subsidiaries’ evaluation of reasons for their investment

in Romania 88 5.3 Strategic position of subsidiaries in Romania in their

MNE group’s operations 91 5.4 Importance of markets supplied by subsidiaries

in Romania 93 5.5 Types of products produced in subsidiaries in Romania 96 5.6 Relative importance of sources of technology used

by subsidiaries in Romania 100

viii List of Tables

A5.1 MNE subsidiaries’ strategic motivations in Romania, by industry and home country 105

A5.2 Degree of knowledge-seeking in MNEs’ subsidiaries in Romania, by industry and home country 106

6.1 Resources devoted to R&D in CEE prior to the transformational recession 115

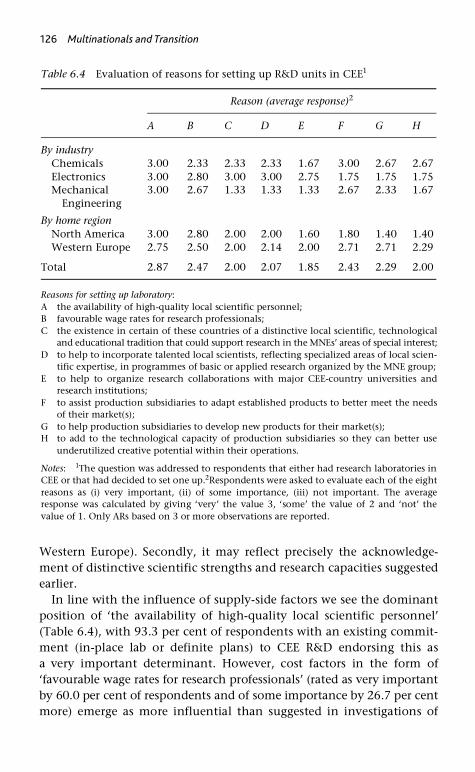

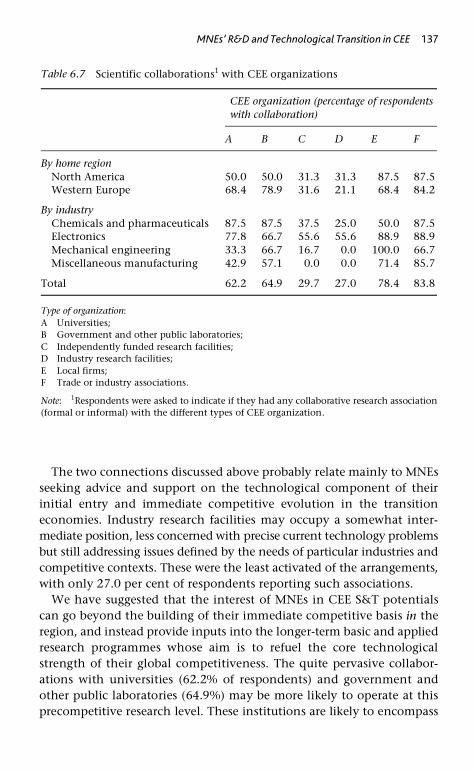

6.2 Number of US patents by country of institution, 1969–96 116 6.3 Location of MNEs’ R&D facilities in CEE countries 124 6.4 Evaluation of reasons for setting up R&D units in CEE 126 6.5 Roles played by R&D units of MNEs in CEE 132 6.6 Evaluation of reasons for not having R&D in CEE 134 6.7 Scientific collaborations with CEE organizations 137 6.8 Evaluation by subsidiaries of reasons for setting up

an R&D laboratory in Romania 139 6.9 Evaluation by subsidiaries of reasons for not setting up

an R&D laboratory in Romania 142 6.10 Extent of subsidiaries’ technological interactions with

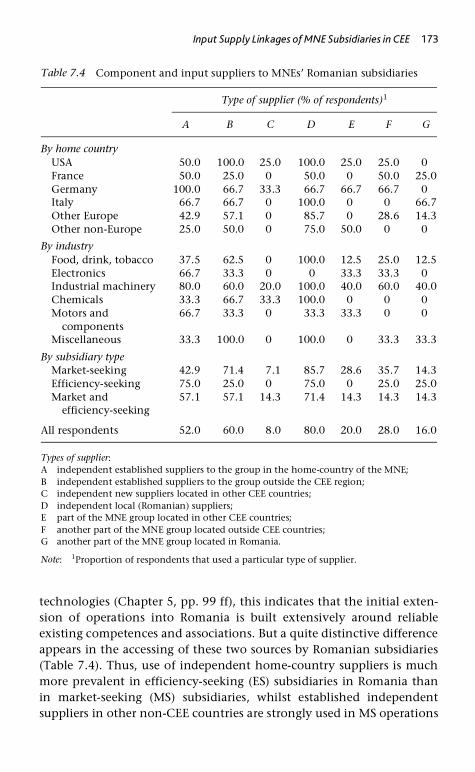

local organizations in Romania 145 7.1 Component and input suppliers to MNEs’ CEE country

operations 162 7.2 Regression tests of use of types of suppliers with

strategic roles of subsidiary as independent variables 166 7.3 Regression tests of use of types of suppliers with

sources of technology used by subsidiaries as independent variables 167

7.4 Component and input suppliers to MNEs’ Romanian subsidiaries 173

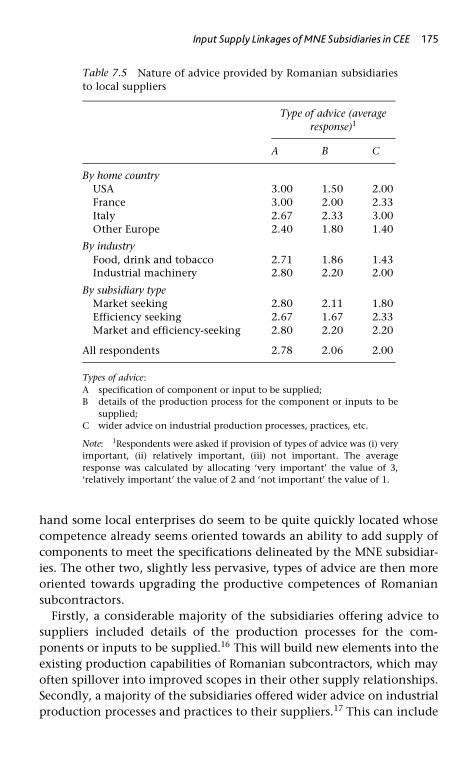

7.5 Nature of advice provided by Romanian subsidiaries to local suppliers 175

ix

List of Abbreviations

AR average response CEE Central and Eastern Europe ES efficiency-seeking FDI foreign direct investment GNP gross national product IIL internationally interdependant laboratories KS knowledge-seeking LA location advantage LIL locally-integrated laboratories MNE multinational enterprise MS market-seeking NIC newly industrializing country NSI national system of innovation OA ownership advantage OPT outward-processing trade R&D research and development S&T science and technology SL support laboratories SME small and medium-sized enterprise

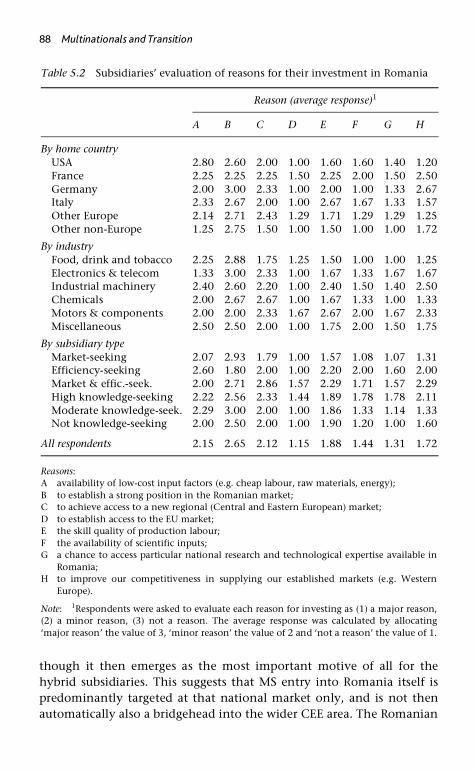

To Maria and Gheorghe Manea

1

1Multinational Strategy and Industrial Transformation

From foreign direct investment to multinational strategy

That ‘the role of foreign direct investment in aiding the regeneration ofthe shattered economies of East and Central Europe’ (Buckley, 1996)was an important early perception of the debate following the collapseof authoritarian centrally-planned regimes is well-understood. Indeeddocumentation and analyses of foreign direct investment (FDI) contrib-uted significantly to the preliminary elaboration of these concerns. Weargue here, however, that (mirroring the crucial refocusing of analyticalcontext pioneered by Hymer [1960/1976]) the relevance of FDI flowsto the processes at issue can only be fully comprehended through anunderstanding of the strengths and motivations of the agents responsiblefor them, that is multinational enterprises (MNEs). The strategic rolesplayed by MNEs’ operations in transition economies are here viewed ascentral to the nature of their contribution to the industrial restructuringnecessary in these countries. The increasingly heterogeneous nature ofthe globalized activity of MNEs emphasizes the range of these potentialroles, and therefore the crucial importance to host countries of the typesof operations they can attract.

An analogy with Hymer’s perception of the need to move from macro-level analysis of FDI to a micro-level approach to understanding MNEscan be instructive here. It has been noted (Dunning and Rugman, 1985;Yamin, 2000; Cantwell, 2000) that Hymer’s work in the late 1950sprovided two key pointers to the ways in which thought about theMNE evolved. Firstly, he pointed to the need for what became known asownership advantages (OAs) (Dunning, 1977, 1993) as a source of inter-national competitiveness. The ways in which MNEs exploit their existingOAs internationally has been a key facet of the manner in which they

2 Multinationals and Transition

have implemented global strategies. However, recently emerging per-ceptions of the widening strategic perspectives in MNEs also emphasizeincreasingly important aspects of these companies’ approach to theincorporation of internationalized elements in the ways they generatenew sources of competitive advantage (that is, OAs). Central to our viewof how MNEs involve themselves with transition economies is thatentry based on application of standardized existing OAs can creativelyevolve into the localized technological and innovation processes thatregenerate OAs.

Secondly, Hymer was concerned with the competitive (or marketstructure) implications of companies’ overseas production operations,suggesting that these could support international collusive (suppressionof competition) arrangements between leading global players. Thoughthis view has been effectively adopted in parts of the literature, otherapproaches now emphasize MNEs’ global strategies as ways of articulat-ing genuine worldwide competition between leading firms in majorindustries.1 Our analysis essentially adopts the latter view by assessingmajor MNEs’ movement into, and then evolving strategic progress in,Central and Eastern European (CEE) economies as a carefully articulateddevelopment that is intended to fit coherently with wider competitiveconcerns of the group.

Elsewhere we have suggested (Manea and Pearce, 1997) that the quitesubstantial number of early acts of FDI into CEE transition economies2

embody a distinctive dichotomy. Many of these investments are thoseof small or medium-sized enterprises (SMEs), often from countries withlittle heritage of overseas investment. Learning processes are key to theseSMEs’ investments; certainly to acquire new sources of commercialknowledge, but also to begin the generation of skills in the process ofgeographical expansion itself. The second type of investment representslarger subsidiaries of well-established MNEs, with the suggestion that thesehave an objective or role that is logically planned to support the initialstrategic expansion of these groups into emergent environments that are,nevertheless, already perceived as significant elements in their globalcompetitive situation. It is the nature and implications of the strategicimperatives of these subsidiaries that provide the core arguments andinvestigations of this book.

Firstly, the CEE subsidiaries may work with their MNEs’ establishedtechnology (as a crucial OA), seeking to improve its application to groupneeds. One version of this is a market-seeking (or expanding) motivation,that aims to supply the local CEE market area with existing products moreeffectively than might have been feasible through trade. Alternatively,

Multinational Strategy and Industrial Transformation 3

low-cost local inputs (Dunning’s location advantages [LA]) might inducean efficiency-seeking role in which the CEE country provides an exportplatform for supply of Western Europe and, perhaps, wider markets.Beyond these means of extending current competitive scopes, however,our viewpoint perceives a second, currently more tentative but poten-tially more valuable (for both CEE economies and MNEs) objective forMNEs’ CEE operations. This knowledge-seeking behaviour aims to useskill- and technology-based local attributes (creative LAs) to support theemergence of higher-value-added product development (and evenscientific) activity in MNE subsidiaries in CEE. As will be amplified sub-sequently (Chapter 6), the premise here is that a notable commitment toscience and technology under communist central planning led to a stockof knowledge and expertise that rarely (especially in high-technologysectors) fuelled effective commercial achievement. Entrepreneurial-drivenMNE subsidiaries may be able to pick up some of this underrealizedpotential quite quickly, enriching their group’s scope (helping regenerateor extend OAs) and activating local knowledge attributes as part of therepositioning processes of CEE economies

Strategic motivations of MNEs

We have indicated that it is through the particular priorities of differentstrategic motivations, activated at the level of their individual subsidiaries’operations, that MNEs can address specific needs of the industrial tran-sition process and, vitally, have the scope to become embedded in itthrough shared developmental aims and procedures. Here we introducethe categorization adopted in more detail. The important perception andexpression of such differential strategic priorities in MNEs’ expansionemerge in the earlier articulation of Behrman (1984), elaborated andextended by Dunning (1993).

The first of these motivations, market-seeking (MS), represents theextension of an MNE’s production and distribution activity into a newcountry or region. This has the primary motive of securing an effectivedevelopment of the local market for the most successful of the group’sexisting products. Though these goods may have been previously suppliedthrough trade, a more active commitment is now expected to be desired.The objective in the opening up and marketization of CEE economiesis thus to be actively locally-responsive in terms of adapting productsand/or processes to local circumstances and generally securing early-mover experience of conditions in these new market spaces. This maymean that some intuitive creative dynamism emerges from the, at least

4 Multinationals and Transition

low-level and informal, localized learning processes involved. The keyattractive factor for MS is the current status (size and average incomelevels) and, especially in CEE countries, the growth potential of localmarkets.

In the second motivation, efficiency-seeking (ES), MNEs relocate theproduction of established goods to, in our case, CEE economies to improvenetwork supply effectiveness. This seeks to improve the cost-efficiency ofsupply, with the goods then being (mainly) exported back to the markets(Western Europe in particular) where they have an already establishedhigh level of demand which is, however, perceived as now needing to beactively defended. Whilst MS complements existing production capacity(and thereby secures market extension), ES substitutes for parts of it (insupply of existing markets). This probably makes such ES-oriented supplyexpansion much more contentious (than MS) intra-group, especiallywhere existing Western European subsidiaries are more mature andtherefore more adept in terms of intra-group politics and bargaining.

In its pure form, ES behaviour provides no natural impulsion towardsany dynamic generation of individualized local creative capabilities.Firstly, there is no scope for product adaptation, since the motivation isto supply mature goods to markets where their characteristics are alreadywell-accepted. Secondly, the immediate ability of the local economy toattract this role derives from the supply of standardized cost-effectiveinputs. Thirdly, the cost-driven core of ES behaviour does not provideroom for any knowledge-generating overhead expenditures that do notdirectly relate to support of the short-term supply role.

The third imperative, knowledge-seeking (KS), does then reflect theacknowledgement in the contemporary MNE of a need to use dispersedfacilities (subsidiaries and/or scientific laboratories or research collabor-ations) to support the longer-term regenerative dimensions of strategiccompetitiveness (Pearce, 1999a; Papanastassiou and Pearce, 1999). Thusat its broader level KS means the pursuit by MNEs of new technologicalcapabilities, scientific capacity (research facilities) and creative expertise(for example dimensions of tacit knowledge) from particular host coun-tries, in order to extend the overall competences (product range and coretechnology) of the group. As investigated here, in the context of earlyMNE involvement with the transition economies, KS is treated as mani-fest in localized product development. In our subsequent analysis thisis specified in two forms which, initially, were seen as evolutionarypossibilities originating in the initial modes of behaviour (MS and ES).

Firstly, KS1 involves developing products in a particular CEE subsidiaryto target the market of that host country and other CEE markets. Thus

Multinational Strategy and Industrial Transformation 5

KS1 represents a logical extension and deepening of the MS role, andmight emerge as a way of building on, and formalizing the value of,those locally-responsive learning processes that we suggest may emergewith MS. In turn, KS2 involves developing products in a particular CEEsubsidiary to target the MNE’s long-established market areas outside theCEE. Intuitively, by analogy, this represents an extension and deepeningof the ES role. However, we then suggest two rather different routesthrough which KS2 activity may emerge.

Firstly, KS2 may indeed derive from ES subsidiaries using their grow-ing familiarity with MNEs’ supply networks and intra-group political/bargaining processes, in order to claim permission to extend theircapabilities to encompass product development activity targeting theirgroups’ wider markets. To do this they will probably need to have per-ceived some quite distinctive potential that is based on local knowledgeor research capacity, and which can plausibly be advocated as ultimatelylikely to extend the group’s product range in logical and valuable ways.

Secondly, KS2 may emerge through a widening of the markets madeavailable to successful KS1 product development. Thus goods that haveasserted their originality in CEE markets (with no a priori officially-mandated aim of supplying other markets of the MNE) may be sub-sequently perceived as revealing new characteristics that are in factquite radical and high-potential extensions of the group product range.Permission may then be granted to initiate supply to markets outside CEE.

Whatever their origins, KS2 products are likely to be quite distinctiveextensions of the MNE product range, and thus are less likely to challengethe immediate supply interests of extant Western European subsidiaries.This may, therefore, be politically (intra-group) a quite viable means ofgenerating dynamic potentials into CEE operations. In fact it may bethat, given the right host-country support (in terms of commitment totechnology, science, education, training), KS2 may also be the moreviable (compared to ES) means of orienting CEE supply capabilitiestowards an MNE group’s wider market areas.

Industrial transition: from restructuring to sustained development

The analytical core of this investigation is the potential for dynamic inter-dependencies between processes of industrial change in CEE transitioneconomies and the various dimensions of competitive strategic develop-ment in contemporary MNEs. To facilitate this we discern two distinctphases in the industrial development of CEE economies following the

6 Multinationals and Transition

abandonment of central planning and state ownership of industry.The first of these relates to the positioning of industry during the periodof fundamental restructuring of institutional, political and economicstructures.

The industrial sectors inherited from the centrally-planned era arelikely to be inefficient and unbalanced, so that the priority is to movetowards a logical, competitive and balanced set of industries that havebeen upgraded around genuine sources of comparative advantage. Thusthe inherited industrial structure that needs to be addressed in the firstphase of restructuring is likely to include some industries that have notrue or sustainable basis for competitiveness, which emerged andsurvived as the result of bargaining and negotiation within political andbureaucratic (and not effectively economic) structures. The potentialcorollary of this is that the industrial sector will have left seriouslyunderdeveloped (again due to malign and distorting elements of bar-gaining processes) other industries that would have reflected genuinesources of competitiveness. Finally, many of those industries that doexist (rightly or wrongly according to the structural balance criteria ofthe previous points) at the entry to phase one will have been ineffectuallydeveloped in terms of realizing their potential efficiency. This couldreflect a generalized lack of competitive pressures and fear of risk-takingin the earlier institutional environment.

Much of the early discussion of the potential value of Western inwardinvestment to CEE economies’ industrial transition saw this predomin-antly in terms of ‘gap-filling’. Thus the FDI package of new investmentin transition economies was expected to bring flows of capital, appropriatetechnology, managerial practices, entrepreneurial drive and internationalmarket access. These would then target the operationalization of theimmediate sources of static comparative advantage available in CEEcountries. This, by activation of competitive forces, then helps to securethe emergence of the more appropriate and balanced industrial sectorthat is needed. Though analytically helpful as far as it goes, this scenariois limited in two ways. Firstly, the view of the strategically heterogeneousMNE that we adopt very clearly allows for initial entry that is not only(or even mainly) ES-motivated (as assumed), and a wider range of aims,benefits and costs need to be allowed for. Secondly, the ‘gap-filling’approach is much less effective in allowing for dynamic response tochanges in local conditions, and this too is capable of more efficientelaboration within the compatible evolution of MNEs.

Whatever the policy basis, and the institutions involved, it is expectedthat the industrial transformation of phase one ends with a sector

Multinational Strategy and Industrial Transformation 7

characterized by a population of firms that can compete fairly in com-petitive market structures. This then points towards the rather differentnature of the second phase. Thus the industries and firms that emergefrom the first phase have asserted their initial competitive status throughthe possession of firm-level capability that can be applied to availableeconomy-wide resources (for example labour, energy, raw materials) inorder to achieve particular strategic aims. Now they need to address theissues of building the sustainability of their position by generating oracquiring new and revitalized competitive competences and movinginto more orderly processes of evolutionary growth and development.The central aim of phase two is, therefore, the continuous upgrading ofcompetitiveness within those industries that were able to assert theirposition during phase one.

Thus as the transition economies move away from the processes ofrestructuring and into the pursuit of sustainable development, theemphasis turns from activating underutilized sources of static compar-ative advantage towards the deepening and enhancement of inputs inthe form of the generation of created/dynamic comparative advantage.From the point of view of MNEs, this means crucial changes away fromthose conditions that attracted their initial entry. Local inputs becomehigher quality and more distinctive, but also more expensive. If MNEscannot, or are unwilling to, change the basis of their operations theywill exit these economies. Such footloose behaviour is a real possibilityif, as was expected to have often been the case, the local factors thatattracted initial entry were standardized homogenous inputs. Thesewould have no distinctive characteristics, that might embed the opera-tions locally, and so are likely to be equally readily available in otherrival economies.

But the nature of the contemporary MNE as a dynamic differentiatednetwork can provide the basis for the detection of a more positive second-phase potential. The potential for evolution to KS motivations expresslyallows for the co-option of MNEs’ CEE operations as a key developmen-tal force in securing the orderly progress of local economies into theirsustainable phase-two growth. The competitive mechanisms withinMNEs now provide an openness to subsidiaries in particular countriesupgrading their operations, in ways that reflect and respond to emerg-ing capabilities in these local economies. This is expected to contribute,in a logical and coherent way, to the extension of the knowledge capacityand product range of the group (Taggart, 1999; Birkinshaw and Hood,1998). From this derives the potential for a mutually-supportive dynamictechnology-based interface between the developmental needs of MNE

8 Multinationals and Transition

groups and the deepening of knowledge, skill and science potentials ofindividual countries.

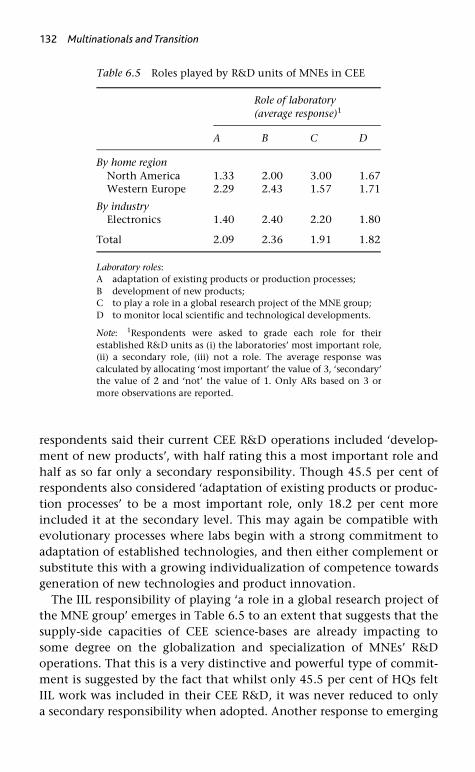

Needs of industrial transition

Within the broadly defined aims of the two phases of transition we candistinguish three specific (interdependent but analytically differentiable)objectives which have particular resonances with the investigation ofMNEs’ participation in the CEE economies.

It is routinely expected that key elements of the repositioning ofCEE economies, with decisive implications for the competitive natureof industry, can come under the heading of internationalization. We cangenerally suggest two aspects of the ways in which the transition pro-cess is expected to potentially benefit from new degrees and forms ofeconomic openness.

Firstly, through improved access to international markets for the transferof production-supporting resources: capital, technology, managementskills, marketing expertise and so on. That is, international access to themeans of enhancing supply scope. Secondly, through the opening-upof new trade potentials, with emphasis given to the various benefitsderiving from increased exporting opportunities. That is, international-ized routes to the effective operationalization of new and existing supplyscope.

The nature of our investigation (focusing on strategic behaviour ofcapacities once established) does not facilitate systematic elaboration ofpoints relating to the first issue, but some intuitive observations may beoffered. The benefits of new inflows of capital, technology and so on(that is, the elements of a traditional FDI package) may be perceived asof most decisive potential value in phase one (before the local economymoves towards its own generation of these resources). But also in phaseone the ability of local enterprise to organize acquisition of these factorsthrough arms-length markets, and to assimilate them effectively whereacquired, must be considered to be innately limited. Thus internalizedtransfer and application of these factors within the expansion processof MNEs into the CEE economies is a logical (and efficient) shortcut.

As phase two develops, the possibility of externalized (market-based)acquisition of these factors to strengthen emerging competitiveness ofmore mature local enterprises becomes more viable. The earlier MNE-organized transfer of the FDI package becomes relatively less necessaryto the widening of transition economies’ scope. This reinforces a themeof our analysis; that in phase two the key issue for local economies is

Multinational Strategy and Industrial Transformation 9

rather more to deepen the creative contribution of MNEs that entered inphase one than to too strongly target new entrants.

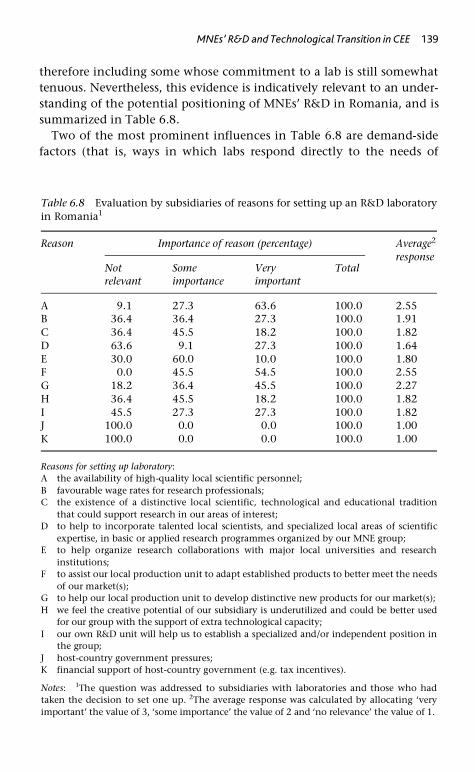

On the second aspect of internationalization (trade performance), ourearlier discussion (and the detailed analysis of subsequent chapters)discerns crucial evolution in the basis of export capability with the move-ment between phases of the transition process. Phase one is normallyexpected to target entry into international markets based on price com-petitive exports that represent factor-proportions trade (by activatingunderutilized sources of static comparative advantage). Internationalcompetitiveness remains the decisive arbiter of phase-two performance,but with an increasing aim to move the basis of exporting towards creative(knowledge- and skill-oriented) dynamic comparative advantage.

But, alongside this perceived need to position themselves much moreemphatically and decisively in terms of the international economy,CEE countries will also seek to very promptly address the need for newdimensions of marketization within their local economies. Thus, in manyeconomies undergoing transition from planning to market forces, acrucial early element is likely to involve quite fundamental reformula-tion of the relationship between consumers and local enterprise. Here itis central to the move towards the norms of market capitalism thatconsumers quickly learn that their discretionary demand patterns canincreasingly determine what is supplied to them and the standards ofquality targeted. This involves an opening-up to the mechanisms ofchoice, and of consumers’ response to firms’ newly-enriched procedures(advertising, packaging, promotions, sharpened distribution practices)for influencing their behaviour. Firms then need the complementaryunderstanding of the new consequences of consumers’ withdrawal ofdemand for their goods and, therefore, the need to address more pro-actively the quality and marketing of existing products.

Once the fundamentals of the marketing interface between customersand firms are established as normal routines of economic behaviour,the aims of effective marketization would be expected to deepen. Asfirms begin to address the essential competitive priority of extendingand developing their product range, consumers’ perceptions of lacunaein current supply scopes can become increasingly manifest as inputs intolocalized innovation processes. Where this creative level of marketizationemerges effectively in a transition economy the competitive benefitscan take two forms. In the direct sense the customer-base that initiallyexpresses the unmet wants receives an improvement in welfare throughan expansion of supply to precisely encompass these tastes. Indirectly,where the new products turn out to have characteristics that make them

10 Multinationals and Transition

relevant to wider markets (elsewhere in the CEE region or elsewhere inEurope), the internationally-competitive scope of industry grows towardshigher-value-added forms of exports.

Finally, it would normally be expected that the early stages of transitionwould need to yield very significant improvements in productiveefficiency. Thus most characterizations of industry under state ownershipand central planning assume vast levels of inefficiency, reflecting thepresence of various distorting influences and the absence of those com-petitive forces that require and impel optimized performance. Indeedso pervasive is this aim of efficiency that, though we discern it here asa separate objective, its pursuit is also seen to correlate closely withother facets of our analysis.

The pursuit of improved allocative efficiency is thus subsumed withinthe very nature of our perception of phase-one restructuring. Here innatelyhigh-cost industries are no longer provided with the safety net of plan-ning support, and competitive forces instead propel the industry structuretowards sectors that can embody genuine forms of static comparativeadvantage. The increased openness (internationalization) of the economiesprovides scope for the emergence of export-oriented industrial sectors,whose competitiveness increasingly derives from the realization ofeconomies of scale (at levels rarely available in pre-transition situations).In addition, it would be expected that the various new dimensions ofcompetitive pressure would work to decisively eliminate the X-inefficiencylikely to have been endemic in the organization and management ofpre-transition enterprises.

In terms of the issues and perspectives raised in our subsequentanalysis, the key efficiency concern of phase two is to sustain the com-petitive effectiveness of the supply of current goods and services, withoutsuch cost-based forces precluding adequate commitment of resourcesto forward-looking evolutionary and developmental activities. It cancertainly be argued that the balance between short-termist concerns withlow-cost production flexibility and immediate profitability, and medium-and longer-term investment in competitive deepening (commitment toaspects of an effective and well-balanced national system of innovation,for example), is a key factor in discriminating between different levels(and forms) of industrial and economic success in the long-establisheddeveloped market economies. Thus the ability to effectively encompassboth of these potentially competing priorities (almost seen as anti-pathetical ideologies in some current debates) into the sustainablecompetitive progress that needs to follow the initial stage of institutionaland industrial change is a crucial element in a broad view of efficiency.

Multinational Strategy and Industrial Transformation 11

Creative transition

We can now investigate, more systematically than previously, the waysin which particular motivations and strategic developments in MNEs canrelate to the needs of CEE host countries in their industrial restructuringand sustained development. These perceptions can then provide the basisfor the intuitive hypotheses of analysis of survey data in subsequentchapters. This exposition has two elements. Firstly, we elaborate herethe concept of creative transition as a process of MNE subsidiary develop-ment that has strong resonances with CEE evolution from phase one tophase two in industrial change, and in the next section we interposethe strategic aims of MNEs with the more specific needs of CEEs’industrialization.

As already indicated, we argue that at the core of the ability of subsid-iaries in CEE economies to upgrade their activity, in ways that are sym-biotic with host-country transformation and development, is the scopethat is made available to them, in the modern MNE, to reconfigure thetechnological bases of their operations. In essence they seek to gothrough a creative transition (Papanastassiou and Pearce, 1994, 1999) inwhich dependence on mature and standardized technologies of theirMNE is replaced by locally-generated knowledge and capabilities. Thesethen provide them with strongly individualized competences that canunderpin a claim to a distinctive position in the group’s wider pro-grammes for competitive regeneration.

Thus MNEs are expected to have initiated their CEE operations throughthe MS and/or ES modes of operation, and will be likely to have securedtheir effective entry around the use of those strong and familiar grouptechnologies that are already embodied in the successful products throughwhich the subsidiaries establish their bridgehead in these unfamiliarmarkets and productive environments. At this stage the new subsidiaries’motivations relate to the extension of the effectiveness with whichtheir MNEs utilize their already proven sources of competitiveness,either through widening of market scope (MS) or enhanced productiveefficiency (ES). However, strategic competitiveness (Pearce, 1999a) inMNEs requires continual upgrading of technological capabilities, withinnovation persistently revitalizing the product range and prevokingreconfigurations of production networks. If CEE subsidiaries remainsubmissively dependent on the inheritance of new products and tech-nologies that have been derived elsewhere in the group, the possibilityemerges that their capabilities (reflecting the local resource base, whichshould itself be changing due to the process of development) will move

12 Multinationals and Transition

out of line with those now required. If this occurs their survival withinthese (MS or ES) modes of operation is systematically compromised.

The alternative, enshrined here in the product-development KSmotivations, is for CEE subsidiaries to pursue participation within theknowledge-related evolutionary competitive processes of their MNE groups.Securing this route of escape from undue dependence on establishedMNE technology involves the co-option by subsidiaries of various typesof local knowledge and scientific capability in order to generate thoseunique competences that can be exercised through creative interdepend-ence with wider programmes (Pearce, 1999b). This defines the processof creative transition as one where the status of the subsidiary movesfrom responsiveness to the local market or the cost competitiveness ofstandardized local inputs (both activated mainly around establishedgroup technology), to a position that increasingly reflects its ability toassert individualized capabilities that build on the internalization andactivation of distinctive local technology and tacit knowledge. Overall,subsidiaries seek to generate a flexibility and diversity in their techno-logical base that can embed them into the developmental processes ofboth their MNE group and their host countries.

It is suggested here that the potential may have existed for MNE sub-sidiaries in CEE economies to move towards an effective KS motivationwith unusual alacrity. The normal expectation is that processes of routineand orderly development in most countries (what we consider to be phase-two conditions for the transition economies) will involve reinvestmentin science, education and training, which can then be supported andactivated by the KS needs of MNEs. In CEE this can be manifest in MNEs’establishment of in-house R&D laboratories (staffed by well-trained localscientists whose capacities may reflect distinctive elements of the localtechnological heritage), or through collaboration with local universitylaboratories (where, again, MNEs may benefit from accessing elementsof a unique technological tradition). Though policies supporting thisresearch- and education-based dimension are clearly desirable in CEEeconomies, it may be that they can often build on a certain scope for‘short-cuts’ that may be especially amenable to activation by MNEs.

This relates to the view that under the previous communist regimesthere had been a strong commitment to pure scientific research, and tothe generation of certain industrial skills. However, due to the lack of acommercial incentive structure and risk-aversion, this had not becomeadequately reflected in product innovation or competitive production.As just noted, the persistence of elements of this research output in thelocal CEE scientific community may provide a particular short-cut

Multinational Strategy and Industrial Transformation 13

potential to those R&D activities (in-house laboratory or collaborativeresearch) that would be a normal element of KS activity. Another facetof these possibilities is that those technologies that did emerge commer-cially in CEE enterprises under central planning had not been developedto their full competitive capacity, so that their adoption and reapplicationby MNEs may provide a basis for a more complete realization of theirpotential. In a similar fashion, skills (tacit knowledge) of local engineersmay help to individualize the competences of MNE subsidiaries, therebybecoming themselves of greater value in the process.

MNE strategies and the phases of transition

At the centre of our investigation are the potential dynamic inter-dependencies between the evolving needs and capacities of CEE econo-mies and the multifaceted aspects of the ways in which contemporaryMNEs apply globalised approaches to reinforcement of their strategiccompetitiveness. We can now review the ways in which this developmen-tal interface between MNEs and transition economies might eventuate,through the expectations and commitments of both parties regarding thethree strategic motivations of MNEs.

Market-seeking (MS)

From the point of view of the contemporary MNE, the presence of MSoperations in their entry to (phase-one) CEE economies would be likelyto have very case-specific motivations. Most current interpretations ofthe strategic evolution of MNEs within the increasing openness inthe wider global economy (Pearce, 2001) perceive the replacement ofmultidomestic approaches (Porter, 1986), which had used a portfolio ofseparate MS subsidiaries to supply isolated national markets, by integratednetworks of subsidiaries playing specialized export-oriented roles reflect-ing productive (ES) and/or creative (KS) capacities of host countries.Nevertheless, in the initial process of adding the restructuring CEEeconomies to their global competitive environment, MNEs may findspecific values for MS-type subsidiaries. However clear may be the intuitiveprojection of latent supply potentials in emerging transition economies,the most immediately plausible source of expanded profitability may bethe greatly enhanced access to their markets. In the relatively unstructuredinstitutional and market conditions of early transition, along with widerdimensions of endemic political and economic uncertainty, MNEs maysee unmet CEE market needs as a more secure basis for profit growththan unrealized supply potentials.

14 Multinationals and Transition

Central to this essentially bounded rationality decision process forMS entry is a severe lack of knowledge of economic conditions in CEEeconomies and a limited basis for informed a priori evaluation of risks tobe faced by early MNE operations. In this context, strategically-isolatedtargeting of local markets limits possible spillover damage to othergroup operations, of a type that would result from the failure of part ofan integrated supply network to fulfil its role. These perspectives thenexpand the rationale of MS beyond the mere augmentation of immediateprofitability, by indicating a very pertinent learning role. The degree ofembeddedness of MS activity provides a context for operative experienceof the local production, market, regulatory, institutional and politicalenvironment. An impetus to understand and evaluate the implicationsof these aspects of CEE conditions, beyond merely their direct impact oninitial MS activity, can build the information basis for a more optimizedview of the evolution of these operations.

The previous arguments suggest that whilst MS is no longer a naturalmode of behaviour within MNEs’ mature international networks, it canplay a crucial role in building the basis for eventually bringing newlyemergent economies into such developed global strategies. As CEE econ-omies acquire the institutional stability and orderly economic progressof phase two, and as MNEs’ operations are fully positioned to evaluateand react to these conditions, the basis emerges for refocused subsidiaryresponsibilities. In fact MS may prove to be a crucial but, in itself, tran-sitional mode of subsidiary behaviour. Thus the expectation is that MSwould be relatively less prevalent in MNEs’ CEE operations as phase twoprogresses and appears more securely founded. This should reflect boththe transition of early-mover subsidiaries from MS to other roles, and thewillingness of late entrants to use access to better information on a moremature environment to bypass MS and integrate CEE operations intowider strategies ab initio.

Clearly we would expect marketization to be the one of our selectedphase-one CEE needs that is most effectively activated by MS operationsin MNE subsidiaries. When MNEs seek to build a competitive bridge-head in the unformulated and unfamiliar CEE economic environmentthey are likely to base this around products with a well-established marketrecord. Central to this are likely to be effective and well-understoodmarketing practices that have already proved to be internationallytransferable and applicable. The use of these practices within early MSactivity offers new dimensions of market behaviour in CEE economies,and their assimilation by local customers is therefore a crucial elementin the movement of these countries towards the expected norms of

Multinational Strategy and Industrial Transformation 15

competitive markets. Subsequently it is then an important implicationof the possible repositioning of initially MS subsidiaries towards morespecialized export-oriented supply roles that this also draws the localmarket into a more internationalized position. Thus, just as increasingparts of MNE subsidiaries’ output are now exported, so increasingamounts of the goods sold in a CEE economy by these companies areimported from elsewhere in the group. So any improvement in market-ing practices relating to these goods that are applied within the MNEcan still be implemented in the CEE. This, however, is routine evolutioncompared to the step-change in marketization secured by phase-one MSactivity.

It is quite likely that the modern and successful technologies andcompetitive practices transferred by MNEs to initiate MS supply willraise the overall levels of productive efficiency in host CEE economies.However, aspects of this mode of operation may nevertheless constrainthe degree to which this happens. With the structure of MS productiondetermined by the pattern of local demand, the standard manufacturingtechniques applied may then be inappropriate in terms of local inputavailabilities (factor proportions) and induce cost inefficiencies insupply. The market power gained by the MNEs’ competitive advantages(notably product originality and quality here) allows acceptable levelsof profitability despite any such sub-optimality in use of existing pro-duction techniques. This permissive factor may generalize into morewidespread X-inefficiencies in organization and management. Finally,the constraint of supply to a specified and limited market area (the hostcountry alone in pure-MS behaviour) may deny the full realization ofeconomies of scale. Of these points both the probable failure of MS toactivate sources of available comparative advantage and/or to securefull use of economies of scale, explicitly correlate to its denial of the aimof internationalization through an opening-up to the competitive forcesof trade.

Efficiency-seeking (ES)

Efficiency-seeking expansion into the CEE economies fits more naturally(than market-seeking) with the expectations of the dominant strategicimperatives of contemporary MNEs. It is expected that one crucial concernof globally-competing enterprises is to optimize the effectiveness of anintegrated internationalized supply network, so as to allow cost-efficientproduction of mature price-competitive goods. Newly-emergent accessto low unit-cost inputs (labour at various skill levels, perhaps energy,raw materials, component parts) in the transition economies of CEE would

16 Multinationals and Transition

then induce MNEs to relocate parts of their supply networks into thesecountries. This was often seen as feasible very early in the opening-up ofthese transition economies because, it was assumed, many of the MNEmanufacturing technologies that were likely to benefit from low-costCEE inputs were also mature and standardized, and thus easy to transferto, and assimilate in, a new production environment. The fate of ESoperations as a host country develops significantly (here as CEE countriesenter phase two) is more ambiguous. As host-country real wages andother factor rewards rise (due to higher skill capacities and productivitylevels), MNEs could still retain an ES commitment by moving moretechnically-complex higher-value-added parts of their existing supplyneeds to these locations. The innate logic of this is, however, we argue,that eventually the level of sophistication of an economy will becomesuch that MNEs replace the ES motivation with knowledge-seeking.Then the supply of established goods is superseded by the developmentof new products.

In line with the above we would expect the ES behaviour of MNEsto be of most decisive relevance to CEE economies during phase one oftheir transition process. At this stage MNEs’ strategic behaviour supportsrestructuring by drawing sources of static comparative advantage intointernationally-competitive sectors, often by drawing them out ofineffectual use in those now declining uncompetitive industries thatwere artificially supported by central planning. The natural export-orientation of ES subsidiaries makes a very significant contribution tothe internationalization of CEE economies, and does so in ways that reflectmajor efficiency benefits through improved resource-allocation effectsand full access to economies of scale. In addition, the primary competitiveenvironment of an ES subsidiary can be seen to be that of its parentgroup’s supply network, which allows full scrutiny of its relative efficiency(that is, compared to other subsidiaries that could use the same technol-ogies and produce the same goods) in a way that is likely to eliminateany substantial degrees of X-inefficiency. The group-oriented nature ofES supply, of course, precludes any contribution to marketization of thehost economy.

As suggested earlier, it is possible to perceive ES behaviour continuinglogically into the orderly development of phase two. Thus the transferof increasingly advanced MNE technologies to produce more complexand valuable parts of an existing product range is routinely compatiblewith sustainable development and concomitant upgrading of host-countrycapacities. Nevertheless, two warnings can be expressed against over-commitment to this approach to MNEs’ operations. Firstly, it is dangerous

Multinational Strategy and Industrial Transformation 17

and unnecessary to oppose wage (and other input-cost) increases on thegrounds that ES MNEs will react negatively to them (with the risk offootloose withdrawal). Increased real rewards are the defining benefitof development and, we argue, need not alienate MNEs’ commitmentto an economy. Secondly, perpetual reliance on upgraded ES roles in MNEs’operations is, in effect, to accept an unnecessarily prolonged status oftechnological dependency. The most severe manifestation of this wouldbe the denial of the activation of these creative local capacities thatcould underpin MNEs’ KS support for localized innovation.

Knowledge-seeking (KS)

Though MNEs are certainly expected to retain a decisive commitmentto the cost-efficient supply of those goods that are already central totheir immediate profitability, the strategic diversity of the modernheterarchy (Hedlund, 1986) also encompasses globalized perspectiveson the medium- and long-term renewal of the fundamental sources oftheir competitiveness. The internationalized approaches to regeneratingthese bases of competitiveness we categorize under the broad heading ofknowledge-seeking. Two distinctive, but frequently highly interdepend-ent, aspects of broadly-defined KS enter strongly into our investigation.Firstly, the growing propensity of MNEs to activate decentralizedapproaches to R&D, through dispersed networks of laboratories that seekto play particular roles in these companies’ competitive regeneration.Secondly, in the refocusing of approaches to innovation to allow for theemergence of product development responsibilities in any part of theglobal network.

In our application of the categorization of strategic motivations toMNEs’ CEE activities, it is the product-development facet of KS thattakes the initial frontline position, with aspects of R&D strategy thenplaying distinctive supporting roles in the analysis. One aim of thisproduct development may be to extend the local (CEE region) competi-tiveness initiated in MS entry. Here it may be perceived (in the earlylearning processes of MS) that these regional markets are quite idio-syncratically different from those with which the MNE is familiar, andthat such distinctiveness is likely to persist, at least into the medium term.This, in turn, may suggest the benefits from extending the first-moverMS advantages of early entry from adaptation of existing goods towardsdevelopment of new goods for these markets (our KS1). Alternatively,probably where the source of the new product idea originates mainlyfrom locally-derived technological bases, the innovation may be seen,from the start, as a potentially quite radical extension of the MNEs’

18 Multinationals and Transition

overall product range so that its target market would immediately extendoutside the CEE region (KS2). Finally, an ad hoc hybrid mode may occurwhere goods only aiming to expand competitiveness within the CEEregion may emerge as being sufficiently radical to secure a place in MNEs’wider supply profiles.

From the point of view of the transition economies, the inculcationof the KS motivation can be seen as being at the core of the impulsionfrom the phase-one activation into competitiveness of standardizedeconomy-wide inputs, to the phase-two generation of firm-based sourcesof sustainable development that derive from their selective internalizationof creative capacities emerging in the local economy. Here MNE involve-ment has the potential to add a strong and unique stimulus to thegeneration and application of localized sources of dynamic comparativeadvantage in CEE, through the provision of complementary creativeattributes and perceptions and immediate access to the challenges ofcompetitive growth in international markets. This emphasizes thatKS-driven product development moves the internationalization of theseeconomies on from cost-driven supply of mature goods to dynamictechnology-based exports reflecting original scopes. Though this, tosome degree, breaks the direct link between internationalization andefficiency implied in ES exporting, the need routinely faced by globally-competing enterprises to maximize monopoly returns in the early lifeof new goods still implies pressure for cost-effective supply. Finally,much CEE-based innovation by MNEs (decisively that which targetscompetitiveness in the countries) extends the process of marketization toone in which customers secure access to means of expressing theirunmet wants (rather than merely experiencing new means by whichexisting goods are offered to them).

The surveys

Two surveys were carried out in order to secure MNEs’ viewpoints onattitudes to their initial strategic expansion into the CEE transitioneconomies, the forms in which these early aims were being operational-ized, and aspects of discerned potential for evolution and deepening ofthese commitments. Thus one obviously influential set of perspectiveswere sought through a survey of MNE HQs positioned to define andarticulate these companies’ CEE entry and strategic evolution. This datawas collected through a postal questionnaire sent to the global orregional headquarters of 408 leading manufacturing and resource-basedMNEs.

Multinational Strategy and Industrial Transformation 19

The population of firms surveyed was derived from the Fortune listingof the largest global corporations published in August 1996. Since thispublication had, by that date, started to combine industrial and servicecorporations into one listing of the world’s biggest businesses, when weextracted only the firms whose main activity was in the manufacturingor resource-based sectors the relevant population emerged as only 207such industrial enterprises. This population, we considered, was likelyto prove too small for the analysis envisaged. Therefore, in order toincrease the number of potential respondents, we went back to theclosest date ( July 1994) when Fortune provided the full separate listingof the world’s 500 largest industrial companies. By selecting only thefirms that did not appear in the combined 1996 ranking we deriveda further 201 industrial corporations relevant to our objectives. Addingthem to the initial 207 firms provided our final population of 408.

Thus a total of 408 questionnaires were sent in the Autumn of 1997to the corporate headquarters of these companies. This was followed bya reminder letter (and second copy of the questionnaire) mailed in early1998. Useable replies were received from 50 of these parent multi-national companies3 (Table 1.1), of which 39 confirmed that they haveinvestments in the CEE region, with the remaining 11 (which eitherexported to the region or were considering it for future involvement)

Table 1.1 Population surveyed and response

Notes: 1These replies were excluded from the final sample because they provided very littleand/or inconsistent information. 2These firms replied by declining to take part in the surveyfor various reasons. The two most important reasons given were (1) the corporation hadinsufficient experience in the region to be in a position to answer the questions meaning-fully (17 cases); (2) as a matter of corporate policy not to participate in surveys, as a result ofthe number of requests received for such information (17 cases). Only three companiesexpressed an unwillingness to answer on grounds of concern over confidentiality or com-mercial sensitivity of information. Seven indicated other reasons for not being able to com-plete the questionnaire.

Parent country of MNE

Number of firms in population

Number of respondents

Excluded inconsistent replies1

Firms expressing inability to participate2

W. Europe 122 21 2 27 N. America 154 19 2 6 Asia 119 10 3 8 Others 13 0 0 3

Total 408 50 7 44

20 Multinationals and Transition

replying to questions relating to their general evaluation of aspects oftransition economies, reasons why they have not invested and theirfuture approach to the region. Of the 39 respondents with operativeaffiliates in the CEE economies, 28 undertook manufacturing activitiesin at least one country amongst the eight surveyed. The other 11 hadsubsidiaries which carried out other significant parts of the manufacturingsector value-added chain (marketing, distribution, resource exploration,component procurement, strategic planning offices).

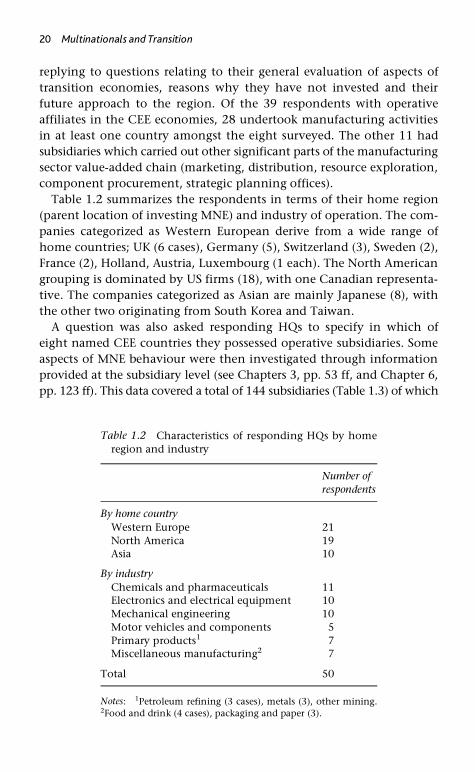

Table 1.2 summarizes the respondents in terms of their home region(parent location of investing MNE) and industry of operation. The com-panies categorized as Western European derive from a wide range ofhome countries; UK (6 cases), Germany (5), Switzerland (3), Sweden (2),France (2), Holland, Austria, Luxembourg (1 each). The North Americangrouping is dominated by US firms (18), with one Canadian representa-tive. The companies categorized as Asian are mainly Japanese (8), withthe other two originating from South Korea and Taiwan.

A question was also asked responding HQs to specify in which ofeight named CEE countries they possessed operative subsidiaries. Someaspects of MNE behaviour were then investigated through informationprovided at the subsidiary level (see Chapters 3, pp. 53 ff, and Chapter 6,pp. 123 ff). This data covered a total of 144 subsidiaries (Table 1.3) of which

Table 1.2 Characteristics of responding HQs by homeregion and industry

Notes: 1Petroleum refining (3 cases), metals (3), other mining.2Food and drink (4 cases), packaging and paper (3).

Number of respondents

By home countryWestern Europe 21 North America 19 Asia 10

By industryChemicals and pharmaceuticals 11 Electronics and electrical equipment 10 Mechanical engineering 10 Motor vehicles and components 5 Primary products1 7 Miscellaneous manufacturing2 7

Total 50

Multinational Strategy and Industrial Transformation 21

75 currently represented production operations, with the remainder cov-ering other elements of these companies’ strategic needs and/or buildingentry into the emerging markets (marketing and distribution, raw mater-ial sourcing, subcontractor development, regional planning offices,testing and clinical trials, computer-based systems and applications).

The second survey addressed the strategic positioning of MNEs’ CEEoperations directly, through a questionnaire sent to established subsidi-aries in Romania. The population of subsidiaries surveyed was derivedfrom the Romanian Development Agency listing (April 1996) of the

Table 1.3 Location of MNEs’ CEE subsidiaries1

(a) By home country

(b) By industry

Note: 1The first number represents the total number of subsidiaries, and the figures inbrackets gives the number of production operations.

Host country

Home country/region Total

N. America W. Europe Asia

Bulgaria 5(0) 7(3) 0 12(3) Czech Rep. 12(5) 10(8) 2(1) 24(15) Hungary 8(2) 12(10) 4(3) 24(14) Poland 11(6) 13(11) 2(1) 26(18) Romania 5(0) 5(3) 1(1) 11(4) Russia 11(5) 8(5) 1(1) 20(11)Slovakia 6(0) 9(7) 2(1) 17(8) Slovenia 5(0) 5(2) 0 10(2)

Total 63(18) 69(49) 12(8) 144(75)

Host country

Industry Total

Electrical Chemicals Mech. eng.

Motors Primary Miscel.

Bulgaria 4(1) 4(0) 1(1) 0 1(0) 2(1) 12(3) Czech Rep. 4(1) 5(2) 6(6) 4(3) 1(0) 4(2) 24(14)Hungary 7(4) 6(4) 3(2) 2(1) 1(0) 5(4) 24(15)Poland 7(4) 6(4) 4(4) 2(1) 1(0) 6(5) 26(18)Romania 4(1) 4(1) 1(1) 1(1) 0 1(0) 11(4) Russia 5(3) 5(2) 4(3) 1(1) 3(1) 2(1) 20(11)Slovakia 6(2) 5(2) 2(2) 1(0) 0 3(2) 17(8) Slovenia 4(1) 3(0) 1(1) 0 0 2(0) 10(2)

Total 41(17) 38(15) 22(20) 11(7) 7(1) 25(15) 144(75)

22 Multinationals and Transition

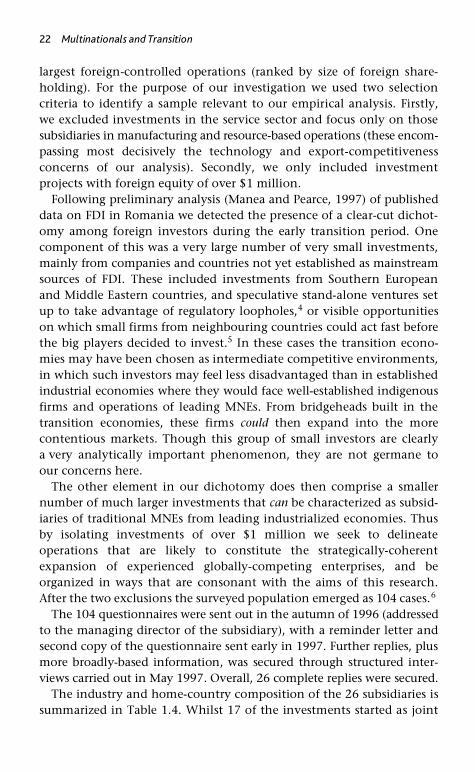

largest foreign-controlled operations (ranked by size of foreign share-holding). For the purpose of our investigation we used two selectioncriteria to identify a sample relevant to our empirical analysis. Firstly,we excluded investments in the service sector and focus only on thosesubsidiaries in manufacturing and resource-based operations (these encom-passing most decisively the technology and export-competitivenessconcerns of our analysis). Secondly, we only included investmentprojects with foreign equity of over $1 million.

Following preliminary analysis (Manea and Pearce, 1997) of publisheddata on FDI in Romania we detected the presence of a clear-cut dichot-omy among foreign investors during the early transition period. Onecomponent of this was a very large number of very small investments,mainly from companies and countries not yet established as mainstreamsources of FDI. These included investments from Southern Europeanand Middle Eastern countries, and speculative stand-alone ventures setup to take advantage of regulatory loopholes,4 or visible opportunitieson which small firms from neighbouring countries could act fast beforethe big players decided to invest.5 In these cases the transition econo-mies may have been chosen as intermediate competitive environments,in which such investors may feel less disadvantaged than in establishedindustrial economies where they would face well-established indigenousfirms and operations of leading MNEs. From bridgeheads built in thetransition economies, these firms could then expand into the morecontentious markets. Though this group of small investors are clearlya very analytically important phenomenon, they are not germane toour concerns here.

The other element in our dichotomy does then comprise a smallernumber of much larger investments that can be characterized as subsid-iaries of traditional MNEs from leading industrialized economies. Thusby isolating investments of over $1 million we seek to delineateoperations that are likely to constitute the strategically-coherentexpansion of experienced globally-competing enterprises, and beorganized in ways that are consonant with the aims of this research.After the two exclusions the surveyed population emerged as 104 cases.6

The 104 questionnaires were sent out in the autumn of 1996 (addressedto the managing director of the subsidiary), with a reminder letter andsecond copy of the questionnaire sent early in 1997. Further replies, plusmore broadly-based information, was secured through structured inter-views carried out in May 1997. Overall, 26 complete replies were secured.

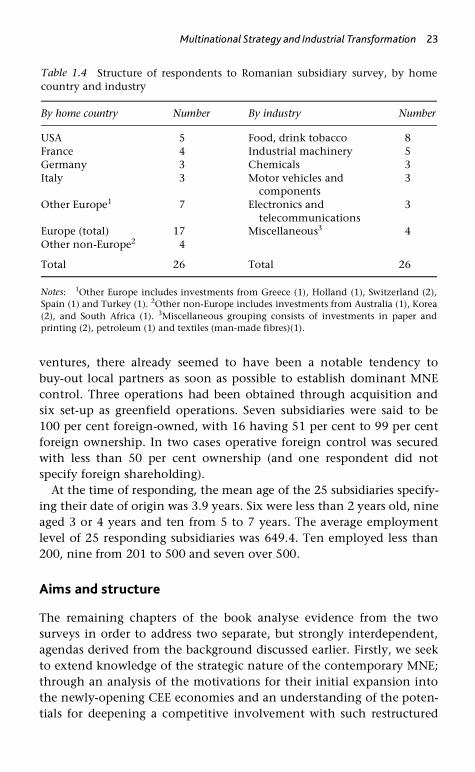

The industry and home-country composition of the 26 subsidiaries issummarized in Table 1.4. Whilst 17 of the investments started as joint

Multinational Strategy and Industrial Transformation 23

ventures, there already seemed to have been a notable tendency tobuy-out local partners as soon as possible to establish dominant MNEcontrol. Three operations had been obtained through acquisition andsix set-up as greenfield operations. Seven subsidiaries were said to be100 per cent foreign-owned, with 16 having 51 per cent to 99 per centforeign ownership. In two cases operative foreign control was securedwith less than 50 per cent ownership (and one respondent did notspecify foreign shareholding).

At the time of responding, the mean age of the 25 subsidiaries specify-ing their date of origin was 3.9 years. Six were less than 2 years old, nineaged 3 or 4 years and ten from 5 to 7 years. The average employmentlevel of 25 responding subsidiaries was 649.4. Ten employed less than200, nine from 201 to 500 and seven over 500.

Aims and structure

The remaining chapters of the book analyse evidence from the twosurveys in order to address two separate, but strongly interdependent,agendas derived from the background discussed earlier. Firstly, we seekto extend knowledge of the strategic nature of the contemporary MNE;through an analysis of the motivations for their initial expansion intothe newly-opening CEE economies and an understanding of the poten-tials for deepening a competitive involvement with such restructured

Table 1.4 Structure of respondents to Romanian subsidiary survey, by homecountry and industry

Notes: 1Other Europe includes investments from Greece (1), Holland (1), Switzerland (2),Spain (1) and Turkey (1). 2Other non-Europe includes investments from Australia (1), Korea(2), and South Africa (1). 3Miscellaneous grouping consists of investments in paper andprinting (2), petroleum (1) and textiles (man-made fibres)(1).

By home country Number By industry Number

USA 5 Food, drink tobacco 8 France 4 Industrial machinery 5 Germany 3 Chemicals 3 Italy 3 Motor vehicles and

components 3

Other Europe1 7 Electronics and telecommunications

3

Europe (total) 17 Miscellaneous3 4 Other non-Europe2 4

Total 26 Total 26

24 Multinationals and Transition

environments and for embedding such operations into wider MNE-groupcontexts and needs. Secondly, we seek to indicate how the strategicpriorities and opportunities pursued by MNEs can support (or compromise)specific objectives and needs of CEE economies, as they initially restruc-ture their industrial sectors and then seek to build the basis for moreorderly sustained development. Another pervasive analytical theme, verymuch at the interface of these two agendas, is the technological scopeof MNEs’ CEE operations. A central strand of this relates to the potentialfor the processes of competitive development within these subsidiariesto help revitalize and activate latent scientific, technological and tacitcapabilities inherited by transition economies from the centrally-planned era.

In the next chapter we firstly review evidence from the HQ survey onthe prevalence (and evolutionary potentials) of the four strategic moti-vations in MNEs’ early CEE operations. This chapter also assesses thetechnological positioning of subsidiaries, through an evaluation ofthe use of seven possible sources. These sources encompass existingtechnologies of the MNE group (the process of technology transfer),established host-country technologies that are adopted (and perhapsadapted) for use by CEE subsidiaries, and knowledge that is generatedand activated locally at the subsidiary level (through in-house R&D orcontractual arrangements with local institutions).

We then introduce the first of several regressions (see also Chapter 3,pp. 59 ff; Chapter 4, pp. 77 ff; and Chapter 7, pp. 165 ff), here testing rela-tionships between strategic motivations and types of technology used.7

As with many of these tests, the overall strength of the individualregressions tends to be rather weak. Two predictable factors are likely tocontribute to this. Firstly, the size and nature of the survey-baseddatasets. Secondly, that it is inherent to our theorizing that MNEs’operations in CEE are part of processes of change and evolution. Thus,whilst we sometimes (Chapter 2, pp. 36 ff; Chapter 3, pp. 59 ff) generateformal hypotheses for the relationships tested that reflect coherentstrategic behaviour of the forms suggested, these may also be weakenedstatistically by the presence of secondary forces for change (that are alsologically implied within our analytical foundations). Therefore we donot expect (or indeed intend) individual regressions to decisively proveparticular relationships. Rather, it is our aim to look for indicativepatterns (guided, where relevant, by the sets of hypotheses outlined)within groups of regressions. On this basis we believe that the sets ofregressions reported do allow us to draw out speculative, but logical,interpretations of MNE behaviour in CEE that can combine both clear

Multinational Strategy and Industrial Transformation 25

motivations for initial establishment and endogenous forces for com-petitive evolution.

The core of Chapter 3 is an evaluation and assessment of the relevanceof seven reasons for investing in the transition economies (includingevidence for the eight separate countries). Three of these reasons can beconsidered as demand-side factors, in that they reflect variants of theMS/ES motivations for investment (that is, how MNEs expect to benefitfrom CEE operations). The other four are then supply-side factors in thesense that they represent ways in which particular host-country charac-teristics provide the basis for activation of MNE operations with differentmotivations. Once again regressions (pp. 59 ff) test relationships betweenreasons for investment and the sources of technology used.

A key discriminating factor between different motivations or reasonsfor MNE investment in CEE is that of the geographical markets targeted.Chapter 4 reports evidence on the importance of seven market areas toMNEs’ CEE subsidiaries. Regression tests (pp. 77 ff) relate these marketsto the reasons for investing.

Chapter 5 encompasses the most substantial part of the analysis ofthe 26 replies to the Romanian subsidiary survey. Treating these repliesas mini case-studies, we firstly categorize each subsidiary as either market-seeking (MS), efficiency-seeking (ES) or as a ‘hybrid’ encompassingstrong elements of both MS and ES. We also classify each subsidiaryby the degree of knowledge-seeking (pp. 87 ff). The remaining sectionsreview evidence on reasons for investing, strategic roles, markets supplied,the types of products produced, and sources of technology used. Togain some impressions as to how these detailed characteristics relateto the broad strategic objectives and evolutionary potentials of MNEoperations, they are evaluated (when appropriate and relevant) interms of subsidiary-type (MS/ES/hybrid) and degree of commitment toknowledge-seeking.

The role of technology in our analysis is as the essential core of dynamicprocesses, decisively manifest in the strategic repositioning of subsidiaries.Here the process of creative transition involves subsidiaries moving frombeing dependent users of existing technologies to increasingly autono-mous generators of new technologies and competitive competences.As the lynchpin of the essentially localized component of this we seesubsidiary-driven R&D (either in-house laboratories or collaborations),that would reflect strong capabilities and knowledge in the host-countryscience base. In the early sections of Chapter 6 we develop aspects of thisargument, documenting the view of a strong, but distorted, scientificand technological heritage in the economies that are emerging from

26 Multinationals and Transition

centralized planning into a process of industrial transformation andcompetitive transition. Later in Chapter 6 we discuss the ways in whichapproaches to R&D in the modern MNE have the scope to address thepotentials remaining in post-transition CEE science bases. Both oursurveys investigated in detail the extent, nature and motivation of MNEs’R&D operations in CEE economies. Also, since we anticipated that inthe initial stages of establishing their competitive presence in CEE manyMNEs would not have included R&D as part of their early functionalscope, both surveys included questions relating to reasons for so farresisting the implementation of laboratories. Thus the detailed analysisin Chapter 6 (pp. 118–46) attempts to draw out an overview of MNEs’attitudes to the potentials of CEE science and technology for their ownneeds and programmes.

Another potential for MNEs’ CEE operations to provide spillovers intodevelopment of the competitive fabric of these economies lies in theirlinkages with local input suppliers. Aspects of the debate about suchpotentials are discussed in the early part of Chapter 7. HQ survey dataare then presented on the range of input suppliers used by their CEEsubsidiaries. Similar evidence on the suppliers used by subsidiaries inRomania then follow, with a discussion of aspects of their knowledgetransfer to their local (Romanian) suppliers.

Notes

1 The literature on the presence of (mostly) competitive oligopoly interactionin expansion patterns of MNEs (Knickerbocker, 1973; Flowers, 1976; Graham,1978) provided a stimulus to this line of argument.

2 Romania in the analysis cited here. 3 Many delegated the task to those regional or European offices that were respons-

ible for investments in the CEE countries. 4 For example, the very favourable early FDI legislation (i.e. the FDI law enacted

in 1991), in order to attract foreign investment, offered very generous fiscaland trade incentives without specifying any conditions (e.g. capital invested,employment levels, exports) at a time when there were still many restraintson domestic investors. This led to many projects being registered as being withforeign capital participation in order to enjoy the facilities offered to foreigninvestors.

5 Hunya (1996) notes a similar phenomenon with Austrian investment inHungary, observing that these were activities that ‘had not expanded inter-nationally before the opening-up of CEECs. Companies with little interna-tional experience grasped the opportunity for market penetration providedby Hungarian privatisation’. Also it has been remarked (e.g. Anton, 1996;Gogou et al., 1997) that there is a substantial participation of Greek compan-ies in CEECs (compared to their relatively underdeveloped position as inter-

Multinational Strategy and Industrial Transformation 27

national investors), with a particular focus on neighbouring countries such asAlbania, Bulgaria, Romania and the former Yugoslavia.

6 After excluding investments of below $1 million the population was 271 firms.Removing non-manufacturing/primary-product operations reduced theoperative population to 104 cases.

7 The econometric techniques used in the reported tests are OLS regressions.While in theory PROBIT analysis is often considered to provide a more accurateestimation of probability values in the case of qualitative variables, which isessentially useful for accurate prediction purposes, here the OLS method waspreferred because it provides a clearer picture of the factors that are of interestto this investigation. These include predominantly the detection of the natureof particular relationships between various aspects of subsidiary behaviour,the sign of these relations and their degree of significance. In some casesPROBIT and LOGIT tests were also run and these provided very similar resultswhich would have given precisely the same interpretation as offered here.For relevant discussion see Casson, Pearce and Singh (1991, p. 214).

28

2 Technology and Strategic Motivations for Investment in Transition Economies

Introduction