Embed Size (px)

Citation preview

Report No. 32416-MZ

MozambiqueAgricultural Development StrategyStimulating Smallholder Agricultural Growth February 23, 2006

AFTS1Agriculture, Environment, and Social Development Unit Country Department 2Africa Region

______________________________________________________

Document of the World Bank

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

ii

iii

CURRENCY EQUIVALENTS

Currency Unit = Metical (Mt), plural = MeticaisUS$1.00 = Mt 24,792.3 (exchange rate effective February 22, 2006)

FISCAL YEAR

January 1 to December 31

WEIGHTS AND MEASURES

Metric System

Vice President: Gobind NankaniCountry Director: Michael BaxterSector Manager: Richard ScobeyTask Team Leader: Jeeva Perumalpillai-Essex

iv

ABBREVIATIONS AND ACRONYMS

ADMARC Malawi Agricultural Development and Marketing CorporationADE Direct Assistance for Schools (Apoio Directo às Escolas)AGOA Africa Growth and Opportunity ActANE National Road Administration (Administração Nacional das Estradas)ASCA Accumulating Savings and Credit AssociationsAP National Early Warning System (Aviso Previo)ASE Social Action Fund (Acção Social Escolar)CAP Agricultural Census (Censo Agro-Pecuário)CCCP Communal Credit Fund (Caixa Comunitária de Crédito e Poupança)CEF Centre for Forestry Research (Centro de Experimentação Florestal)CFA Agricultural Training CenterCIF Cost, Insurance and FreightCGAP Consultative Group to Assist the PoorCGIAR Consultative Group on International Agricultural ResearchCLUSA Cooperative League of the United States of AmericaCOMESA Common Market for Eastern and Southern AfricaDFID Department for International Development (of the UK)DHS Demographic Health SurveyDINA National Directorate of Agriculture (Direcção Nacional de Agricultura)DINAP Nacional Livestock DirectorateDNA National Directorate of Water (Direcção Nacional de Águas)DNDR National Directorate of Rural DevelopmentDRC Domestic Resource CostsEFAFTI Education for All Fast Track Initiative ENACOMO Empresa Nacional de ComercializacãoENS National Seed CompanyESSP Education Sector Strategic PlanEU European UnionFAO Food and Agriculture Organisation of the United NationsFARE Fundo de Apoio a Reabilitação de EconomiaFDI Foreign Direct InvestmentFFA Agricultural Development Fund (Fundo de Fomento Agrário)FFHA Fundo de Fomento da Hidráulica AgrícolaFFP Fund for the Promotion of Fishing (Fundo de Fomento Pesqueiro)FFPI Fund for the Promotion of Small Industries (Fundo de Fomento da Pequena

Indústria)FOB Free on BoardFRA Food Reserve AgencyFTLRP Fast Track Land Reform ProgramGAPI Office for Assistance to Small Industries (Gabinete de Apoio à Pequena

Indústria)GDP Gross Domestic ProductGIS Geographic Information SystemsGOM Government of MozambiqueGPPE Gabinete de Promoção de Pequenas Empresas

v

IAM Mozambique Cotton InstituteIAF National Household Survey (Inquérito ao Agregado Familar sobre

Orçamento Familiar)ICM Mozambique Cereals InstituteICRISAT International Crops Research Institute for the Semi-Arid TropicsIDA International Development AssociationIFAD International Fund for Agricultural DevelopmentIIAM Institute of Agrarian Research of MozambiqueIIVM Mozambican Institute for Vetenary Research INCAJU Institute for the Promotion of Cashew (Instituto de Fomento de Caju)INDER Rural Development InstituteINIA National Agricultural Research Institute (Instituto Nacional de Investigação

Agrária)INIVE National Institute for Veterinarian Research (Instituto Nacional de

Investigação Veterinária)IPA National Institute for Animal Production (Instituto de Produção Animal)IRAM Institut de Recherches et d’Applications de Méthodes de DéveloppementJVC Joint Venture CompaniesKRII Japanese Aid ProgramLOLE Law on Local State Entities (Lei dos Orgãos do Estado)MADER Ministry of Agriculture and Rural Development (Ministério de Agricultura e

Desenvolvimento Rural)MASIP Malawi Agricultural Sector Investment ProgramMINAG Ministry of AgricultureMISAU Ministry of Health (Ministério de Saude)MFI Micro-Finance InstitutionMMF Mozambique Microfinance FacilityMSE Micro and small-sized enterprisesMt MeticaisNDV Newcastle Disease VaccineNHS National Health ServicesNRE Natural Resource ExtractionOECD Organisation for Economic Co-operation and DevelopmentORT Oral Rehydration TherapyPA Prime-agePAAO Plano Anual de Actividades e OrçamentoPARPA Action Plan for the Reduction of Absolute Poverty (Programa de Acção para

a Redução de Pobreza Absoluta)PCR Poupança e Credito RotativoPNS National Seed ProgramPROAGRI Agriculture Sector Public Expenditure ProgramPRSC Poverty Reduction Support CreditRGE Rural Group Enterprise Development ProgrammeRNF Rural Non-farmROCS Roads and Coastal Shipping ProgramsRWSS Rural Water Supply and Sanitation

vi

SADC South African Development CommunitySDC Swiss Agency for Development CorporationSEMOC Sementes de MoçambiqueSIMA Agricultural Market Information SystemSOCREMO Sociedade de Credito de MoçambiqueSPS Sanitary and Phytosanitary StandardsTIA Agricultural household survey (Trabalho de Inquérito Agrícola ao Sector

Familiar)TIP Targeted Input ProgramT&V Training and VisitUEM University of Eduardo MondlaneUNDP United Nations Development ProgrammeWFP United Nations World Food ProgrammeWTO World Trade Organization

vii

ACKNOWLEDGEMENTS

We would like to acknowledge the wide range of inputs, comments and suggestions during the course of this strategy. It was undertaken by a World Bank team to provide strategic guidance for the future development of Mozambique’s agriculture sector.

The strategy was led by Jeeva Perumalpillai-Essex and included Josef Loening, Daniel Liborio da Cruz Sousa, Eduardo da Sousa (AFTS1) and Isabelle Tsakok (consultant). Overall guidance was provided by Michael Baxter, Country Director Mozambique, AFCO2, and Richard Scobey, Sector Manager, AFTS1. Assistance with communication, budget management and arranging of meetings was provided by Caroline Guazzo (AFTS1) and Luísa Matsinhe (AFCO2). Seth Beckerman (consultant) edited the final draft of this document. The strategy benefited from contributions from Peter Moll (AFTP1), Louise Fox (AFTPM), Katleen van den Broeck (AFTPM), Elena Bardasi (AFTPM), Asmara Achcar (WBIHD), Alexander Lotsch (DEC) as well as David Mather, Duncan Boughton, Tom Walker and Rui Benfica (Michigan State University). The background papers were funded by the Belgium Poverty Reduction Partnership, Norwegian and Danish Trust Funds. Peer reviewers were Louise Cord (PRMPR) and Sushma Ganguly (ARD).

The strategy also benefited from valuable comments from the Government of Mozambique and many of the donors in Maputo from the workshop that was held in September 26, 2006.

viii

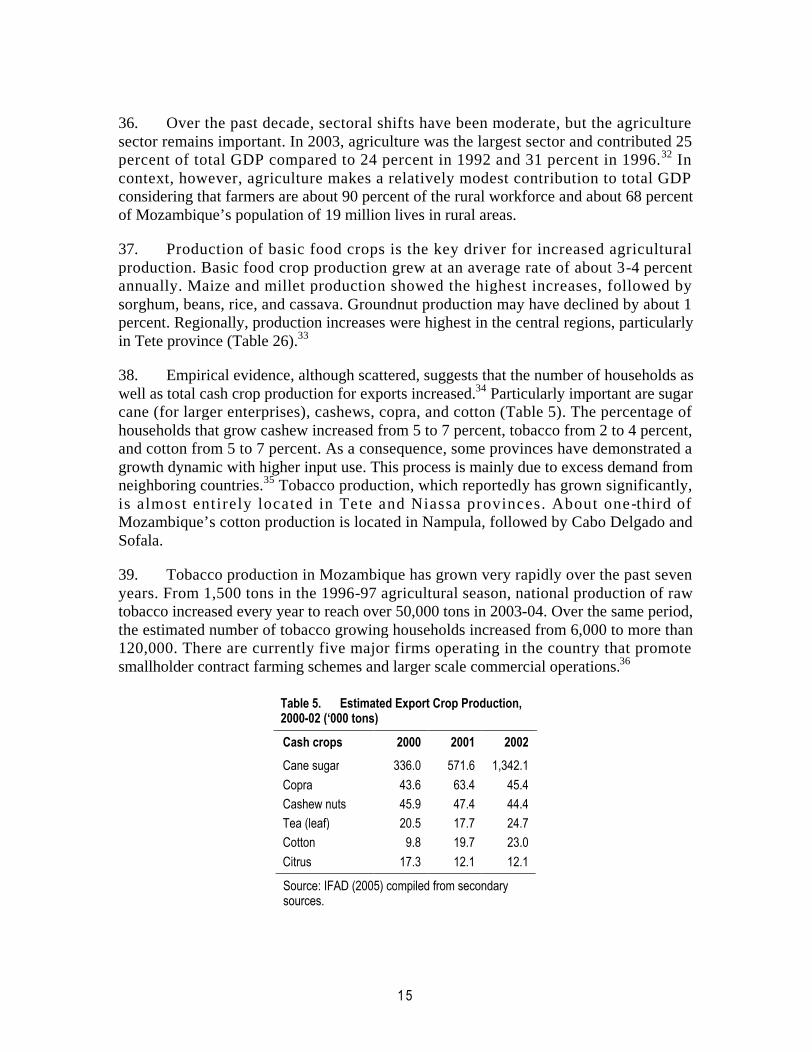

ContentsExecutive Summary......................................................................................................... xiii

Extensive Agricultural Growth Has Reduced Rural Poverty....................................... xiiiFuture Growth Requires Action ................................................................................. xivOverall Conducive Policy Environment .......................................................................xvHigh Costs of Business and Non-transparent Public Expenditures ...............................xvMain Structural Challenges: Infrastructure, Markets, and Institutions ........................ xviAgricultural Strategy: A Two-pronged Approach to Promote Growth....................... xviiSupportive Environment and Reduced Vulnerability: Cross-cutting Issues............... xviiiGovernment, Donors, and Civil Society Need to Think Together............................... xix

1. Past Decade of Agriculture and Poverty in Rural Mozambique .............................. 1Mozambique’s Agricultural Sector ............................................................................... 3

Dominance of Smallholder Agriculture................................................................. 3Livelihood in a Risky Environment ...................................................................... 4Regional Variation of Crop Production................................................................. 5Food Crops, Cash Crops, and Livestock ............................................................... 6Effects of Three Decades of War on Commercial Farming ................................. 11

Determinants of Agricultural Growth.......................................................................... 13Rapid Growth in Agriculture .............................................................................. 13Extensive Cultivation Is the Main Source of Agricultural Growth....................... 16Stagnant Land and Labor Productivity................................................................ 22

Decline of Rural Poverty ............................................................................................ 22Rural Poverty Declined but Remains Widespread............................................... 23Agricultural Growth Is the Main Determinant to Reducing Rural Poverty........... 23Further Determinants of Rural Poverty ............................................................... 25Moderate Increase in Rural Inequality ................................................................ 25

Non-farm Economy and Rural Labor Markets ............................................................ 27Rising Importance of the Non-farm Sector.......................................................... 27Strong Performance of the Rural Non-farm Sector in the North and Center ........ 28Sources of Rural Income Growth........................................................................ 28Determinants of Rural Non-farm Income............................................................ 30

2. Enabling the Rural Environment............................................................................. 35Natural Resource Endowment..................................................................................... 37

Land Abundance and Major Conflicts................................................................. 38Managing Water, Irrigation Investments, and Forest Resources .......................... 39Strong Environmental Regulatory Institutions Are Necessary............................. 40

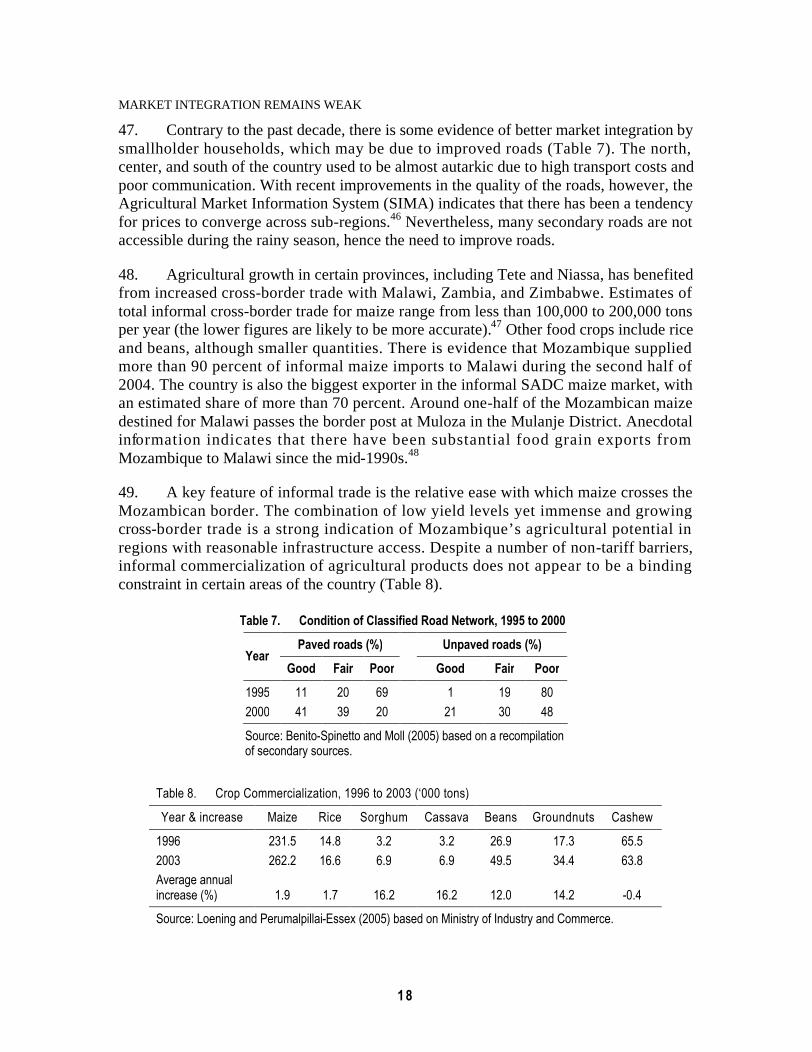

Macroeconomic Environment..................................................................................... 41Positive Record of Inflation, Trade, and Exchange Rates .................................... 41Significant Weaknesses in Public Expenditures .................................................. 42

Structural Factors and Institutions............................................................................... 46Weak Rural Infrastructure .................................................................................. 46Rural Labor and HIV/AIDS................................................................................ 47Insufficient Use and Adoption of Agricultural Technologies............................... 48Lack of Rural Finance ........................................................................................ 49

ix

Price Policy and Marketing Environment in Agriculture..................................... 50Major Institutional Challenges: Decentralization ................................................ 52

Vulnerability and Risk................................................................................................ 53

3. Strategy to Promote Growth of Smallholder Agriculture....................................... 55Necessary Conditions ................................................................................................. 55

Maintaining a Stable and Supportive Macro and Sector Framework ................... 55Good Governance............................................................................................... 57Control of HIV/AIDS ......................................................................................... 57

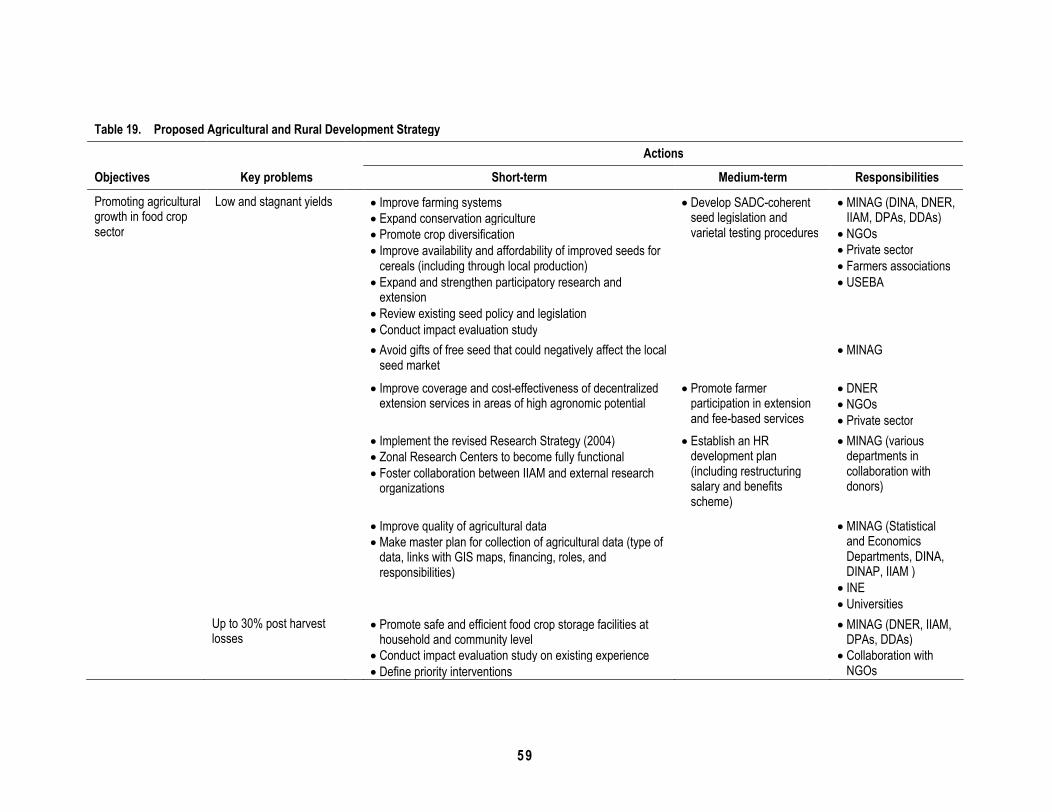

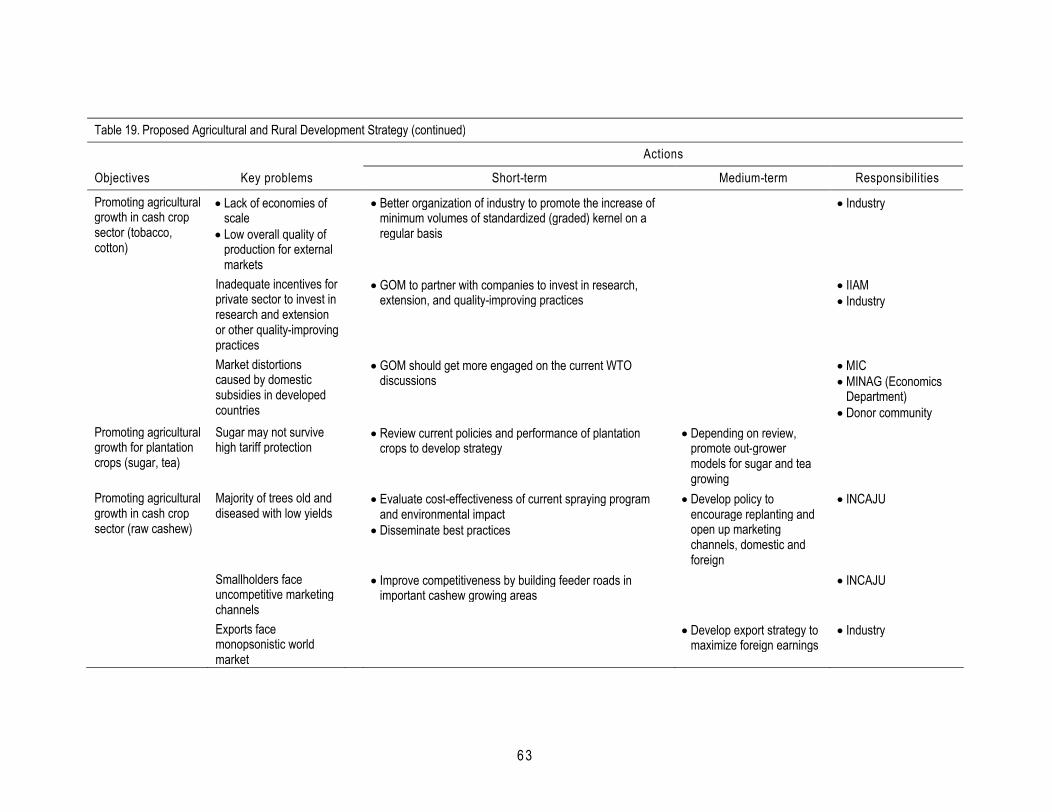

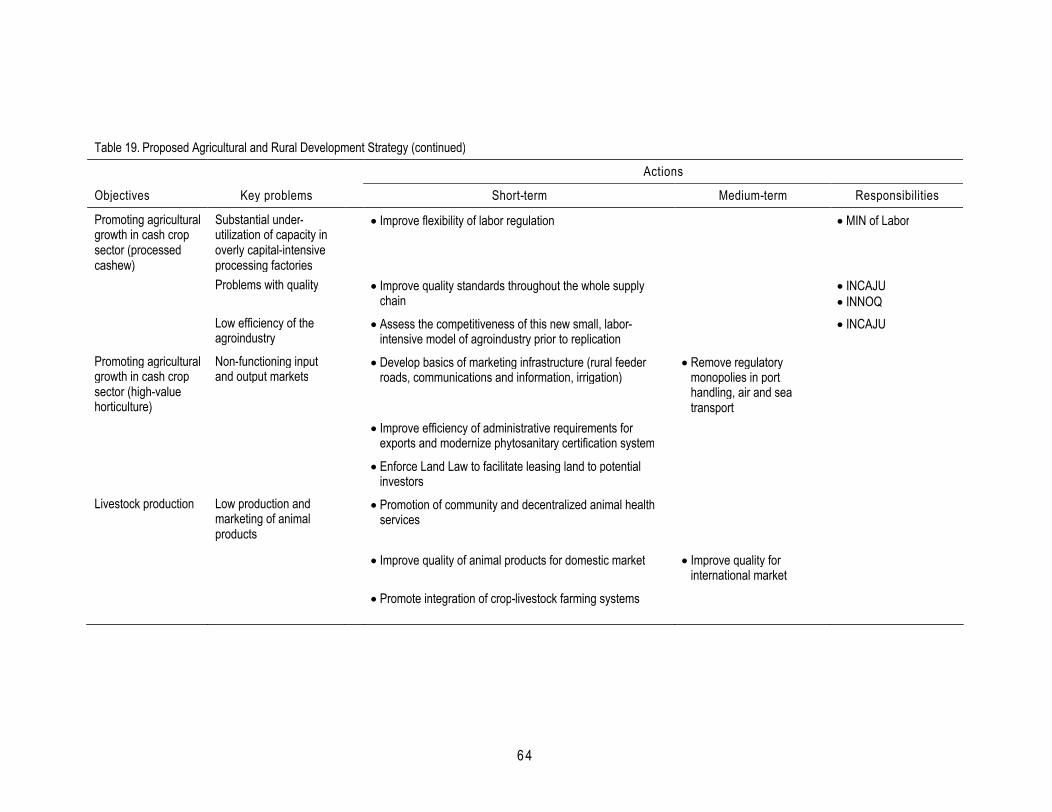

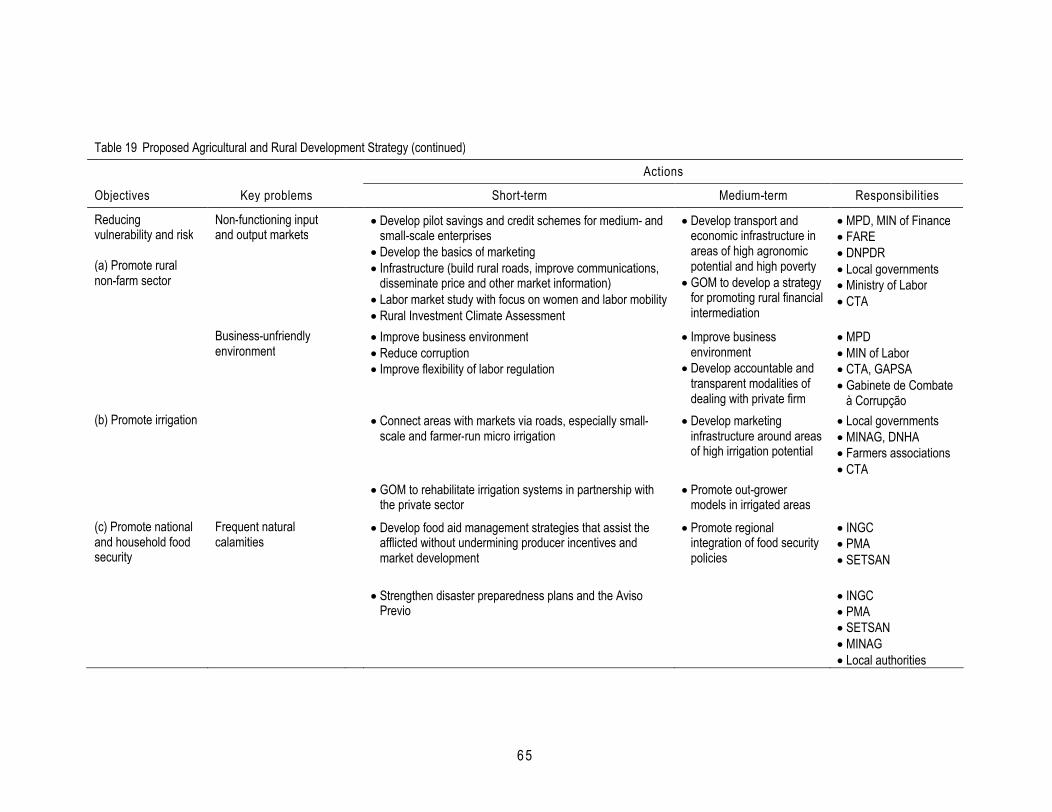

Two-pronged Strategy ................................................................................................ 58Priorities for the Food and Cash Crop Sectors: Basic Infrastructure ................... 58Strategy for Growth of Food Crops: Develop Rural Markets............................... 67Other Recommendations..................................................................................... 67Strategy for Growth in Cash Crops: Development of Out-grower/Contract Farming Schemes ............................................................................................................. 70Other recommendations...................................................................................... 71

Recommendations for Cash Crops .............................................................................. 73Sugar and Tea..................................................................................................... 73Cashew Nuts ...................................................................................................... 73Horticulture Crops.............................................................................................. 73Livestock............................................................................................................ 74

Reducing Vulnerability and Risks............................................................................... 75Food Security ............................................................................................................. 76

4. Implementation of the Strategy................................................................................ 77Enabling Environment ................................................................................................ 77

Macroeconomic Framework ............................................................................... 77Rural Infrastructure ............................................................................................ 77Other Rural Services........................................................................................... 78Policies............................................................................................................... 78Agricultural Statistics ......................................................................................... 79Public Expenditures............................................................................................ 79Research and Extension...................................................................................... 79

Institutions.................................................................................................................. 80Rural Producer Organizations............................................................................. 80Local Government.............................................................................................. 80

Role of Private Sector................................................................................................. 81Role of Donors ........................................................................................................... 81

References ........................................................................................................................129

Notes.................................................................................................................................137

Appendices1. Challenges to Measuring Agricultural Production in Mozambique............................. 832. Regression Analyses.................................................................................................. 853. Statistical Tables ....................................................................................................... 914. Agroclimatic Regions and Farming Systems.............................................................. 99

x

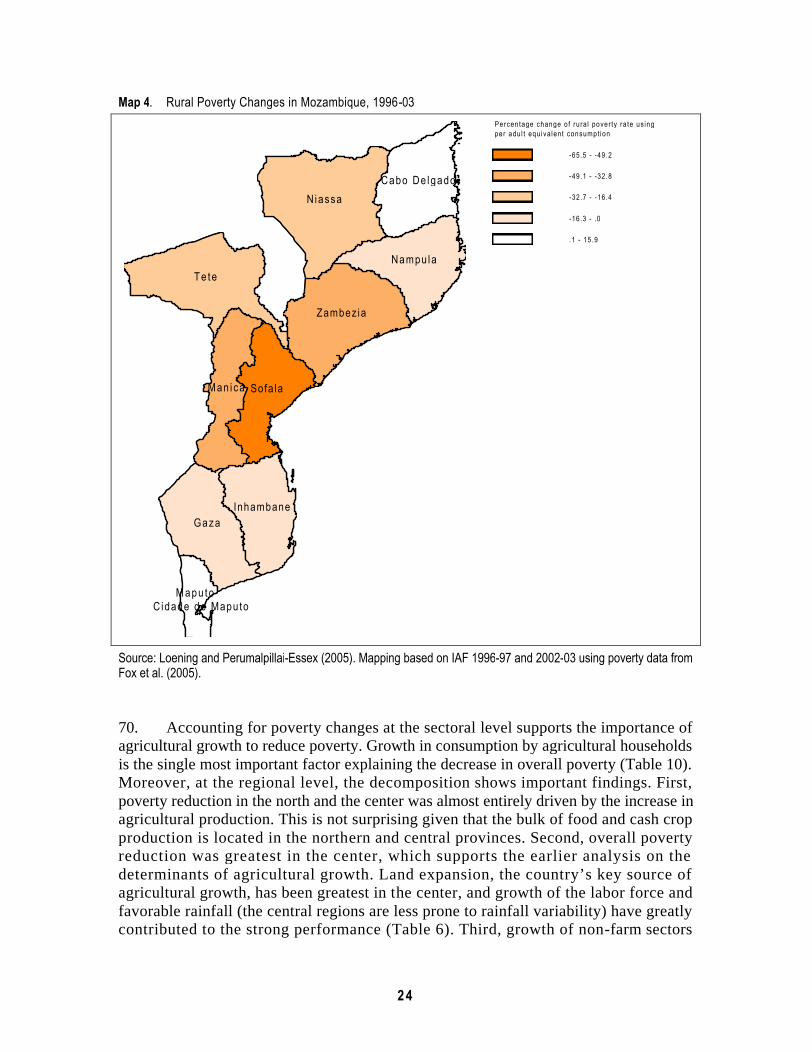

5. The Significance of Extension ..................................................................................1036. Effects of Neighboring Countries on Mozambique Agriculture.................................1077. HIV/AIDS and Agriculture.......................................................................................1138. Comparative Advantage of Major Cash Crops in Mozambique.................................1179. Horticultural Export Sector.......................................................................................12310. Public and Donor Sector Initiatives to Develop Rural Finance in Mozambique.........127

FiguresFigure 1. Maize Yields in Mozambique and Neighboring Countries, 1962-03 .................. 2Figure 2. Growth of Agricultural GDP, 1992-03 ............................................................. 14Figure 3. Maize Production, 1993-03 ............................................................................. 14Figure 4. Main Source of Land Acquisition, 2000 ........................................................... 17Figure 5. Impact of Extension on Crop Production by Income Quintile, 2002.................. 21Figure 6. Correlation of Food Crop Production and Poverty ........................................... 26Figure 7. Rural Growth Incidence Curve, 1996-03 .......................................................... 27Figure 8. Rural Household Income Sources, 2002 .......................................................... 31Figure 9. Rural Households Income Sources, 2002 ......................................................... 31Figure 10. Growth of Rural Household Income, 1996-02 ................................................. 32Figure 11. Total and Foreign Investments in Agriculture, 1998-04 ................................... 43Figure 12. Evolution of Crop Yields (from surveys), 1994-03 .......................................... 93Figure 13. Evolution of Mozambique Crop Yields (from Aviso Previo), 1993-01 ............ 93Figure 14. Rural Household Conditions Compared With Previous Year, 2004 .................104Figure 15. Responses to Prime-Age Adult Chronic Illness by Gender, 1999-02................113Figure 16. Responses to Prime-Age Adult Death from Illness by Region, 1999-02...........114

TablesTable 1. Estimated Actual and Potential Crop Yields ....................................................... 2Table 2. Basic Characteristics of the Agriculture Sector, 2000 and 2003 .......................... 4Table 3. Agroecological Conditions and Regional Crop Production Patterns.................... 6Table 4. Livestock in Mozambique, 1994-2003.............................................................. 10Table 5. Estimated Export Crop Production, 2000-02 .................................................... 15Table 6. Average Annual Growth Rates for Land, Labor, and Rainfall, 1993-03 ............ 17Table 7. Condition of Classified Road Network, 1995 to 2000....................................... 18Table 8. Crop Commercialization, 1996 to 2003 ........................................................... 18Table 9. Source of Extension Service by Poverty Quintile, 2002 ................................... 21Table 10. Decomposition of Poverty Change by Sector, 1996-03..................................... 26Table 11. Indices of Rural Inequality, 1996-97 and 2002-03 ............................................ 27Table 12. Rural Employment by Sector and Gender, 1996-97 and 2002-03...................... 29Table 13. Rural Employment by Type of Labor, 1996-97 and 2002-03 ............................ 29Table 14. Relative Consumption of Rural Household Head by Main Activity, 1996-97

and 2002-03 ..................................................................................................... 29Table 15. Relative Consumption of Household Head by Region, 1996-97 and 2002-03 ... 30Table 16. Natural Resource Extraction Activities of Rural Households, 2000 .................. 32

xi

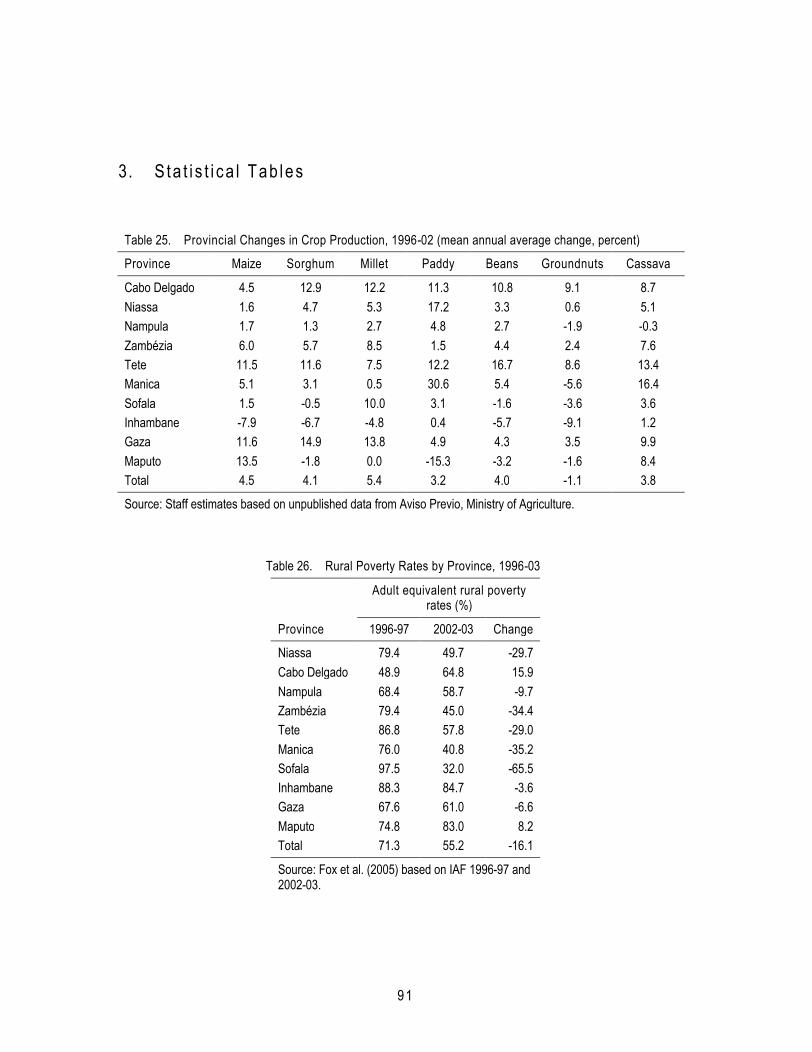

Table 17. A Scorecard for the Enabling Environment in 2005.......................................... 36Table 18. Government Expenditures by Selected Priority Sectors, 1998-04...................... 44Table 19. Proposed Agricultural and Rural Development Strategy................................... 59Table 20. Determinants of Smallholder Maize Production, 1993-01................................. 85Table 21. Determinants of Rural Crop Income, 2002 ....................................................... 86Table 22. Determinants of Rural Self-Employment Income, 2002.................................... 87Table 23. Determinants of Rural Wage Income, 2002 ...................................................... 88Table 24. Determinants of Rural Consumption, 2003....................................................... 89Table 25. Provincial Changes in Crop Production, 1996-02 ............................................ 91Table 26. Rural Poverty Rates by Province, 1996-03 ....................................................... 91Table 27. Mozambique Household Assets, Crop Diversification, and Agricultural Input

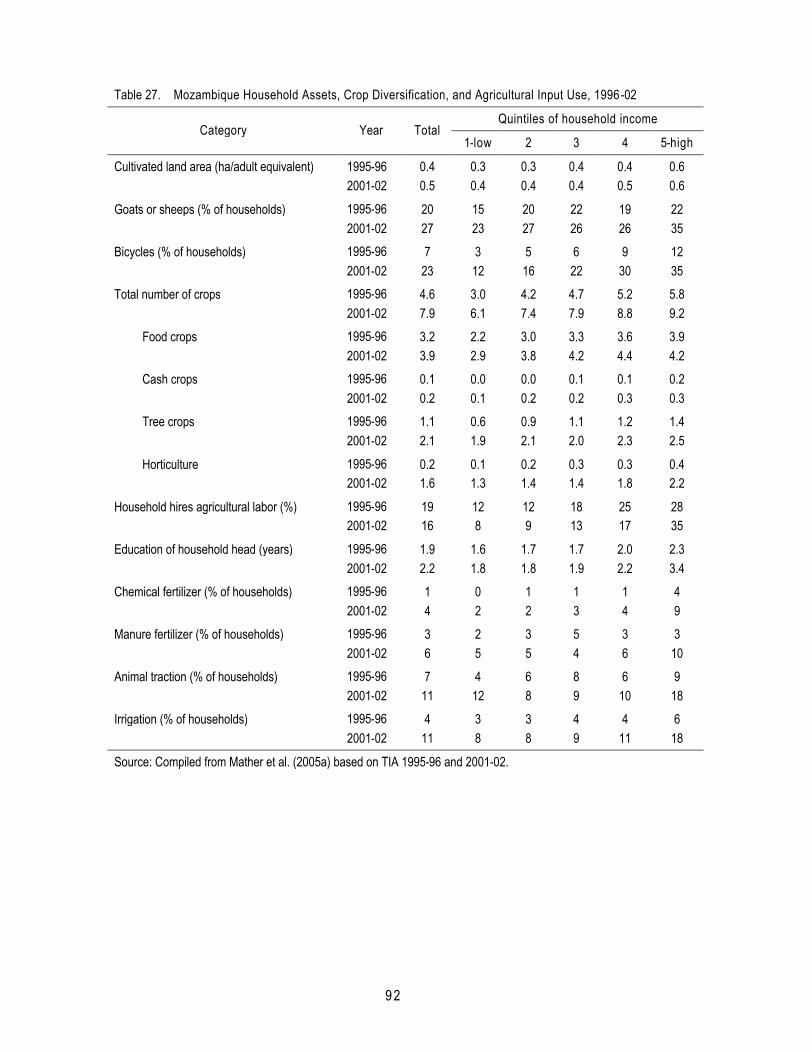

Use, 1996-02.................................................................................................... 92Table 28. Key Characteristics of the Mozambique Agricultural Sector, 2000-03.............. 94Table 29. Food Crop Production for Small- and Medium-size Farms by Province, 2003 .. 96Table 30. Cash Crop Production for Small- and Medium-size Farms by Province, 2003 . 96Table 31. Number of Livestock by Province, 2003........................................................... 96Table 32. Sole Crops of Basic Foods, 2000...................................................................... 97Table 33. Unmixed Area by Main Cash Crops, 2000 ....................................................... 97Table 34. Number of Holdings and Unmixed Areas, Selected Horticultural Crops, 2000 . 98Table 35. Main Agroecological Zones and Farming Systems in Mozambique.................100Table 36. Use of Agricultural Techniques by Availability of Extension Advice, 2004.....105Table 37. Summary of Profitability Analysis for Major Cash Crops, 2004-05 .................120

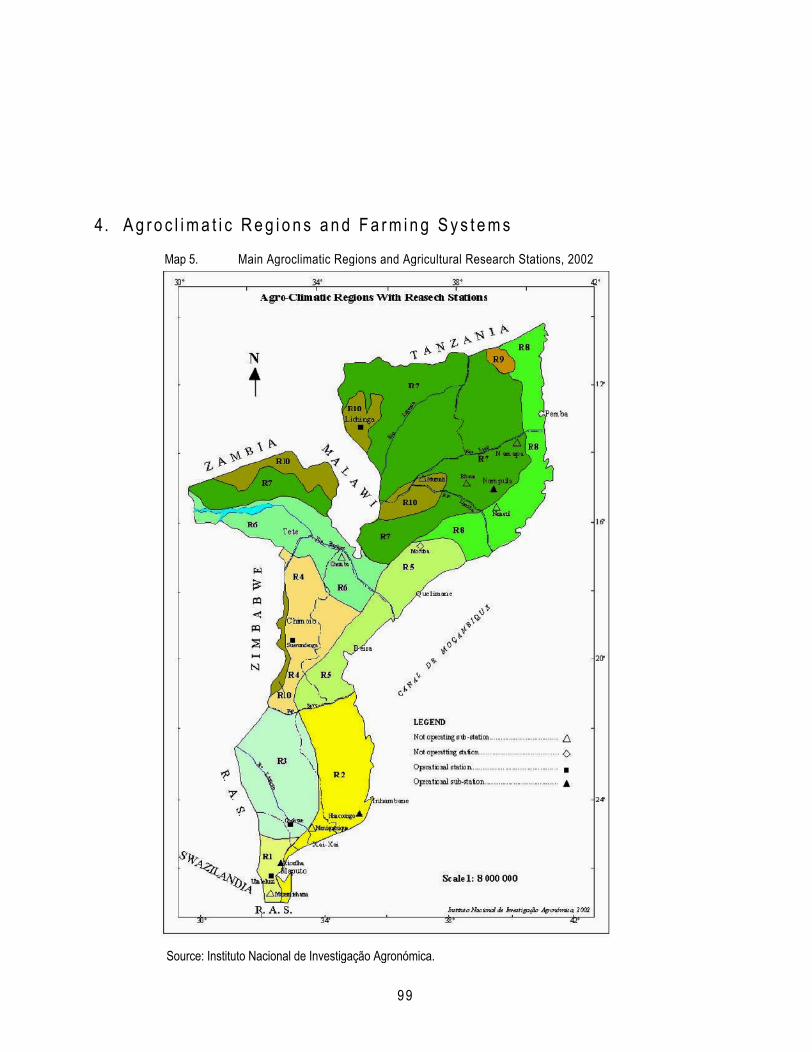

MapsMap 1. Major Food Crops and Rural Poverty in Mozambique, 2003................................. 7Map 2. Major Cash Crops and Rural Poverty in Mozambique, 2003................................. 9Map 3. Cattle Population and Rural Poverty in Mozambique, 2003 ................................ 12Map 4. Rural Poverty Changes in Mozambique, 1996-03 ............................................... 24Map 5. Main Agroclimatic Regions and Agricultural Research Stations, 2002................ 99

BoxesBox 1. Basic Provisions of the 1997 Land Law.............................................................. 38Box 2. Non-tariff Trade Barriers with Neighboring Countries........................................ 42Box 3. Agricultural and Rural Expenditures in Mozambique: Positive but Limited

Impacts............................................................................................................... 45Box 4. Impacts of Extension in Mozambique................................................................. 49Box 5. Why Credit Markets Function Poorly in Mozambique ........................................ 50Box 6. Main Types of Rural Producer Organizations in Mozambique ............................ 54

xii

xiii

Executive Summary

Extensive Agricultural Growth Has Reduced Rural Povertyi. Rural poverty has declined substantially over the last decade as the agriculture sector has shown remarkable improvements. Over 70 percent of the 19 million Mozambicans live in rural areas, with nearly 40 percent in the northern and central regions. The sector is dominated by 3.2 million smallholder families. The majority of smallholders grow food crops, and about 16 percent also participate in cotton and tobacco out-grower schemes. While overall annual agricultural growth has averaged 6 percent, increases in the food and cash crop sectors led to an impressive reduction in rural poverty over the period 1996 to 2003 — the rural poverty headcount decreased from 69 percent in 1996 to 54 percent in 2003. The largest decline was in the central region, followed by the north.

ii. The agriculture sector grew primarily through area expansion and an increase in the labor force, with a large increase in cultivated area in the central region. From 1992 to 2001, cultivated area expanded at 3.3 percent annually. The labor force grew at about 1.7 percent annually, which approximates rural population growth of 1.9 percent. After the 1992 peace accords, the increased rural labor force was primarily returned migrants. Basic food crop production was the key driver for growth, but cash crop production was

Key Messages of Mozambique’s Agricultural Development Strategy

Extensive agricultural growth has been the key factor in reducing rural poverty, however, current patterns of growth are unsustainable and future growth requires close attention.

Poor rural infrastructure and markets are major constraints for agricultural growth, thus for food crops, the strategy highlights the importance of rural markets.

For cash crops, the strategy emphasizes promotion of contract farming arrangements.

For both food and cash crops, this strategy focuses on crops that are among the most important and for which data or background analysis was readily available.

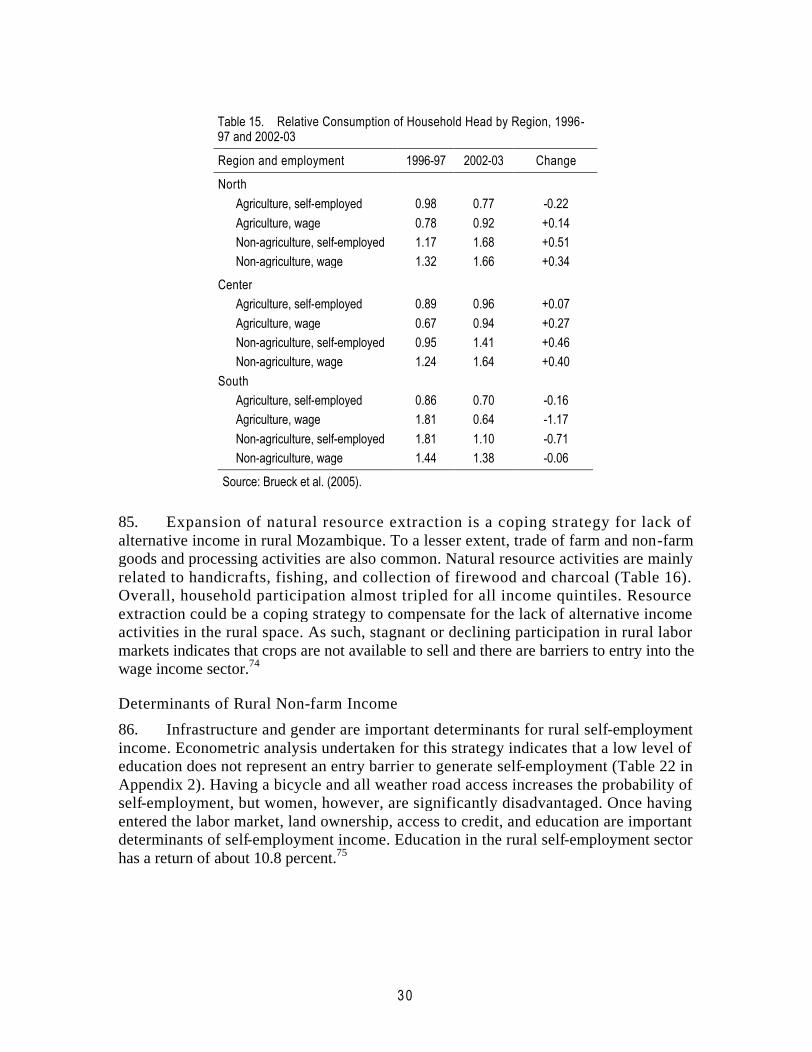

Basic infrastructure, such as rural roads and irrigation, and a number of factors related to the enabling environment, including malaria and HIV/AIDS, are important cross-cutting issues.

While the overall policy environment is considered to be more or less conducive to growth, the overall business environment, transparency of public expenditures, and donor coordination in the rural sector should be improved.

Finally, attention should be given to better monitor and evaluate the impact of agricultural and rural investments. In this regard, there is a need to significantly improve the statistical system of the sector.

This strategy is intended to cover a time horizon of five years, and is largely based on a synthesis of existing literature.

xiv

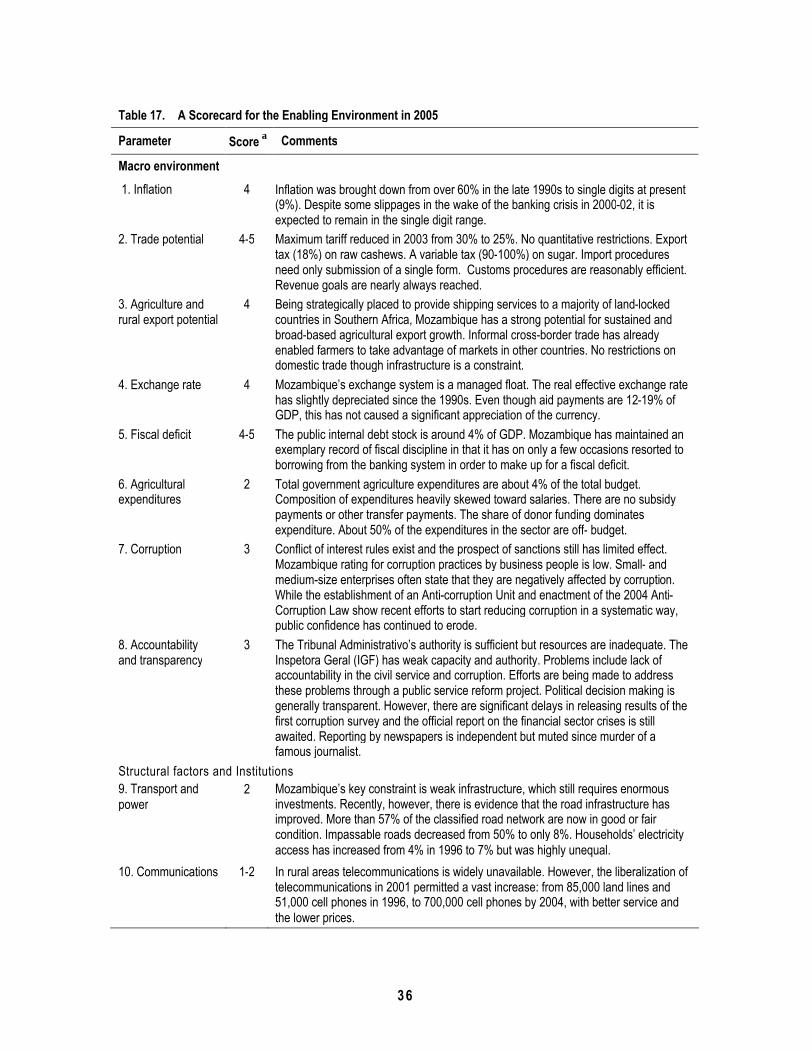

also important and is promoted mainly through out-grower schemes in northern and central Mozambique. However, access to and use of improved crop technologies remains limited, crop yields are stagnant, and thus rural incomes are also likely to stagnate. Other important findings include:

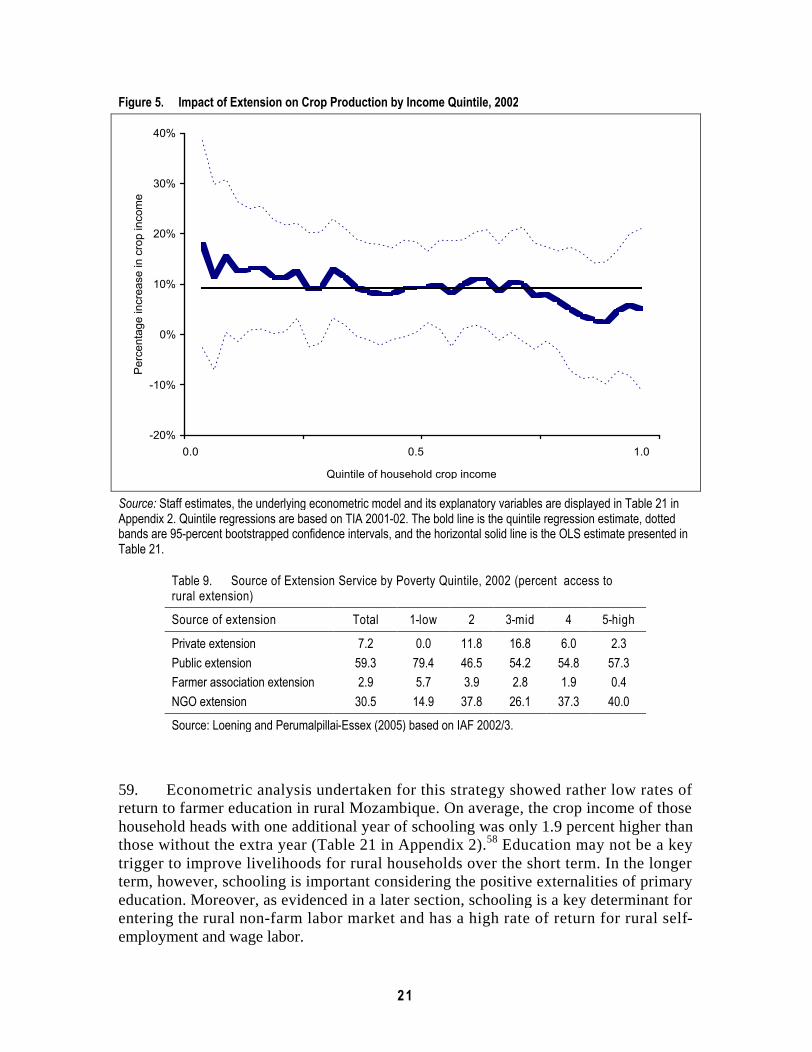

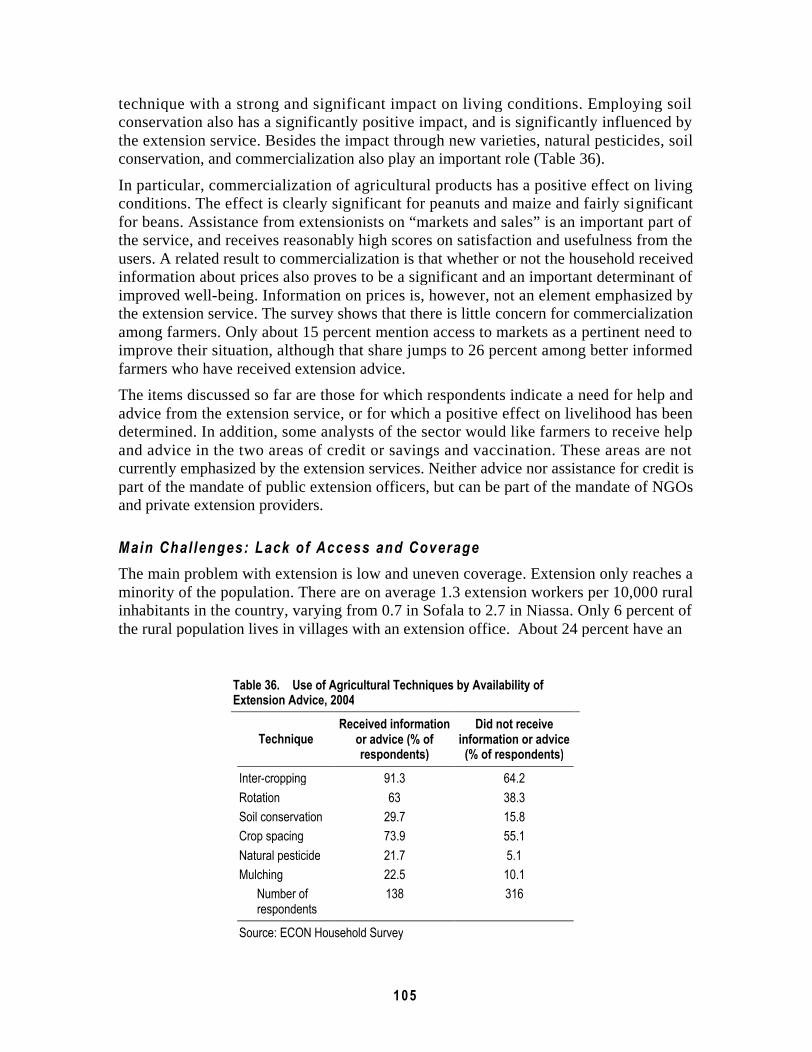

Extension significantly affects crop production but farmer education level does not affect adoption of technology nor income. Extension services have limited coverage but where such services are available, farmer income from crops has risen by 8 percent. Extension services provided by NGOs are more effective, however, public extension systems better address the rural poor. Extension messages have focused on use of improved seed and planting techniques. Educational level does not seem to significantly affect agricultural production —on average, one additional year of schooling is associated with only 1.9 percent increase in crop income.

There is evidence that crop diversification is a coping mechanism. From 1995 to 2003, the mean number of crops almost doubled from five to nine per household across all income groups, especially with food crops. This is not surprising where smallholders practice rainfed agriculture. Crop diversification does not seem to have affected income, however, which may be an issue of quality and quantity at the farm household level.

Market integration and cross-border trade are becoming crucial. With the improved infrastructure since peace was established, markets are more integrated and prices are more stable. There is increased cross-border trade with Malawi, Zambia, and Zimbabwe, with estimated total informal trade in maize over 100,000 tons. Mozambique supplies more than 90 percent of the trade to Malawi. There is increasing evidence that other food grain crops, such as sorghum and beans, are also traded.

The effects from neighboring countries are positive and important. Because north-south infrastructure is underdeveloped, a large part of trade is east-west. Zimbabwean farmers grow tobacco and other high-value export crops across the border in Mozambique as a result of the tumultuous political situation in their own country. Heavily subsidized inputs from Malawi and Zambia also find their way to Mozambique. The land-locked countries are also heavily dependent on Mozambican ports, hence the country earns substantial sums from the transit of freight.

Future Growth Requires Actioniii. The current sources of agricultural growth are not sustainable. Without close attention to the use and adoption of improved agricultural technologies, production growth may slow and rural poverty will remain widespread. Over the past decade, improved agricultural technologies have played only a minor role. For example, smallholder households that use fertilizer, animal traction, or small-scale irrigation increased to about 7 percent from a low of 4 percent. A limited number of smallholders use drought-resistant varieties or have access to improved seeds. The highest- and the lowest-income quintiles were more likely to adopt new technologies compared to middle-

xv

income groups. Among determinants of crop income, use of improved technologies, especially fertilizer, significantly affects income.

iv. Although constraints exist, Mozambique possesses the fundamentals to realize its considerable agricultural potential. The country is endowed with natural resources, including numerous fertile agroecological zones, but only about 10 percent of its 36 million arable hectares are cultivated. Mozambique has 104 river basins, 20 million hectares of forests, and a long coast line with three major ports. The current government is committed to rural growth and development, however, the potential can only be achieved through public-private partnerships in which the Government provides an enabling environment and the private sector assumes the risks and reaches out to rural areas.

Overall Conducive Policy Environmentv. The enabling macroeconomic environment is generally positive but with some constraining factors. Since the 1992 peace agreement the country has maintained positive macroeconomic growth, with an annual growth exceeding 9 percent since 1997. Mozambique has been supported by substantial foreign aid that contributes 15 percent of GDP, compared to the African average of 4 percent of GDP. Inflation has been reduced to single digits from a high of about 70 percent in the mid-1990s. A key constraint to investments, however, is the high cost of capital, with an average lending rate over 30 percent and credit for smallholders almost non-existent.

vi. Conditions are suitable to expand trade. The exchange rate is a managed float and hence there is no evidence that it is overvalued and works against exports. Additionally, the trade framework has been more liberal since the early 1990s, and Mozambique is working closely with SADC on free trade agreements. The trade-weighted average tariff is 9 percent, one of the lowest in the continent. Agriculture inputs such as fertilizer and agrochemicals, are not subject to any tariff.

High Costs of Business and Non-transparent Public Expendituresvii. The high cost of business development negatively affects private sector investments. Although the macro framework is positive, doing business in the country is a major challenge. Not only are procedures cumbersome, it also takes valuable time to obtain licenses and navigate other processes. Corruption and informal payments to government officials are cited as major deterrents, and in addition, the judicial system is not conducive to settling disputes fairly and quickly. Labor laws are also archaic and require modernization — hiring and firing processes are drawn out and it is not easy to hire foreign workers.

viii. Spending in the social sector has increased. About 65 percent of the budget is allocated to lending in the education, health, agriculture, water supply, and sanitation sectors, of which 50 percent is for education and health. Enrollment in primary education has increased, but retention is an issue, perhaps because of quality and capacity of the

xvi

teaching staff. Health indicators have improved but there is still much progress to be made — malaria and HIV (prevalence rate of 13 percent) are major problems, nearly 50 percent of rural children are malnourished, and as with the education sector, distance and poor infrastructure are major constraints to accessing services.

ix. The total annual budget for the agriculture sector is only about 4 percent of the total national budget, a problem that is compounded because funds are not provided on time or at critical times during the growing season. Fifty percent of agriculture expenditures are off-budget, hence it is difficult to assess efficacy of various activities. The total invested in rural areas from other sectors is not known because expenditures are not disaggregated. The Mozambican economy continues to be centralized with funds disbursed from central ministries.

Main Structural Challenges: Infrastructure, Markets, and Institutionsx. Constraints to agricultural growth are numerous. The 17-year conflict destroyed the basic infrastructure and institutions that were created during the colonial period. Rebuilding roads and bridges is now a priority and a necessary condition for any growth in the agriculture sector. The vast terrain and scattered and sparse population makes it all the more critical to ensure rural connectivity, but per capita investment costs are considerable and would have to be borne by the Government. The dismantling of state-owned organizations that provided agricultural inputs and bought and marketed production has created a vacuum. In its infancy, the private sector has yet to find it cost effective and profitable to reach out to rural areas.

Poor roads and markets and unexploited irrigation potential are key constraints to agricultural development. Despite recent investments in roads, the density of the road network is the lowest in southern Africa (32 kilometers per square kilometer), which to some extent is due the size of the country and difficulty in building and maintaining roads. With a sparse population, the unit costs of serving rural areas are high. Although building roads is essential for rural development, a major concern is the positive correlation between transport routes and transmission and prevalence of HIV/AIDS. Other key infrastructure such as power and telecommunications are also very poorly developed, especially in rural areas, as is irrigation, another key factor for agriculture. Total irrigated area is only about 3 percent of its potential.

Institutions in Mozambique are weak, lack capacity, and were largely shaped by its history. The war, colonialism, and socialism dictated the types of institutions and their thinking — during the socialist era, colonial farms became state farms, parastatals were established to supply inputs and market outputs, and smallholders were considered constraints to modernizing agriculture. Today, the Ministry of Agriculture formulates policies and regulations, and the private sector supplies inputs and markets. A major issue for many public sector entities is the lack of trained personnel. Colonial Mozambique did not train an adequate number of people and after the war many who were trained left the country. Today this deficit is a major constraint so that the country continues to rely on outside

xvii

technical assistance. Additionally, low salaries in government departments do not attract and retain skilled and qualified staff.

Agricultural Strategy: A Two-pronged Approach to Promote Growthxi. A boost to the agricultural economy is critical to ensure growth of the rural sector. Any strategy must promote sustained production and productivity for smallholders who depend on agriculture, thus improving their livelihood and reducing vulnerability and risk. The transformation of agriculture from low-productivity subsistence to high-productivity commercial is long-term, and the current strategy involves short-term activities to lay a foundation for a long-term transformation. Such growth should be highly productive and environmentally sustainable, along with strengthening the cash crop sector by promotion of out-grower schemes.

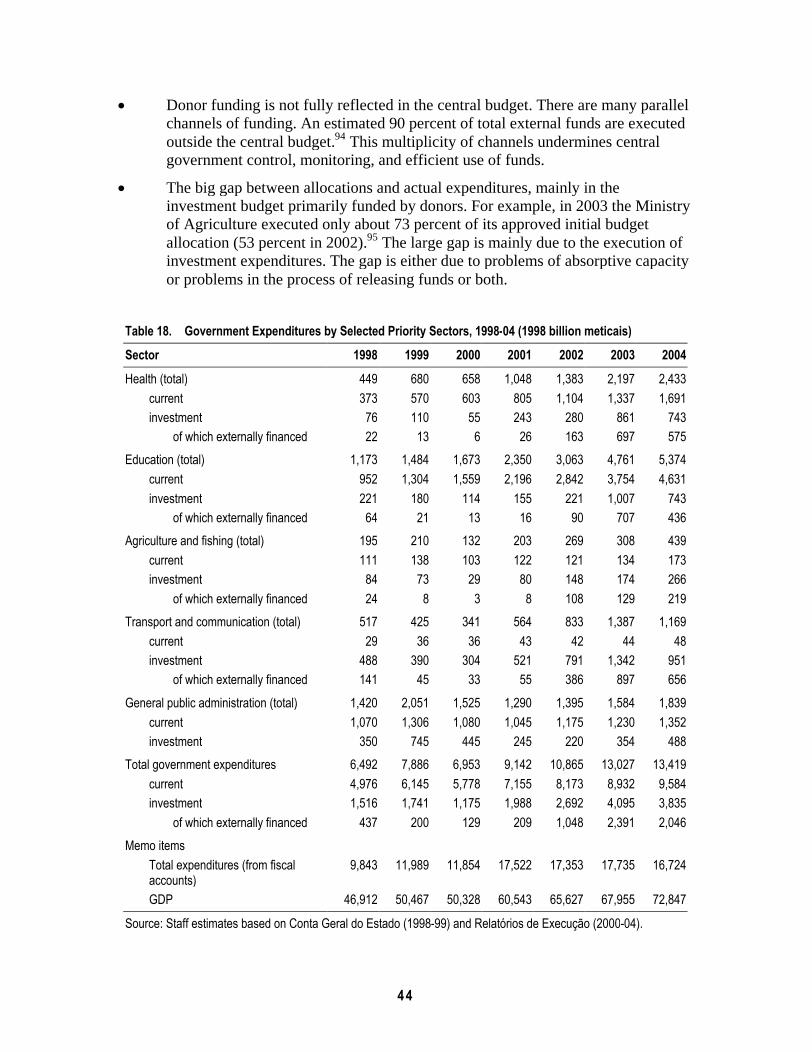

xii. A two-pronged strategy is required in the agriculture sector to promote growth in the rural sector. Given the subsistence nature of smallholder agriculture and emerging out-grower schemes, two elements are required. For the smallholder whose efforts produce food grains and other products for the domestic market, enhancing productivity is critical. For the growing number of smallholders who participate in out-grower schemes, strengthening their power to bargain for better farm-gate prices and improve industries that add value are essential.

The food crop sector currently dominates and will for years in the future. Yield increases are required through the use of improved seed and other inputs such as fertilizer and irrigation. Public sector activities such as research and extension services must be demand-driven and reach out to farmers. Given that most farmers are women, extension staff should reach out to this group and ensure that appropriate technology is gender-oriented.

The cash crop sector, already an important source of income growth, has substantial potential. Depending on the crop, there is a need to develop expertise and mechanisms to balance the interests of out-growers, companies, and the institutional environment. For example, out-growers need fair prices, companies do not want to be undermined by side-selling, and both groups need the results of research and extension to keep a competitive edge. Farmers need to organize into producer organizations so that they have the power to negotiate with companies. Companies need to feel the confidence to invest, and it is important that competitors with very short-term agendas do not undermine their efforts. Side selling is a major issue, and building a long-term relationship will need additional efforts.

Cashew, an important smallholder cash crop, needs to be revitalized. Given the age and diseased nature of most trees, structural characteristics of domestic and foreign markets, and the past controversial liberalization, experience should be reviewed. Replanting is important and farmers need the power to negotiate prices with processors and export marketers.

Horticultural exports have been a major source of export-led growth in many developing countries, and Mozambique has the potential for further

xviii

development of this sector. Especially in the central region, there are opportunities to cultivate high-value vegetable crops and flowers for export to Europe. Zimbabwe farmers are already investing in Mozambique because of the political situation in their own country. The public sector can support such endeavors to develop the quality standards required for higher income markets. There is also a need for a better marketing infrastructure essential to integrate smallholders in this high-value chain.

Productivity of the livestock sector is undermined by disease, high mortality, and inadequate feed. One essential support element is to deliver more widespread extension services, including those addressed specifically to women who tend small livestock and men who tend cattle. Currently they are neglected by an extension system that assists only cattle owners. As with crop cultivation, different types of livestock are demarcated along gender lines.

Supportive Environment and Reduced Vulnerability: Cross-cutting Issuesxiii. One necessary condition is that the overall macroeconomic framework and other sectoral investments must remain stable, including reducing the fiscal deficit and controlling inflation. Greater accountability and transparency to reduce corruption are critical to improving the business environment. Although education does not seem to be highly correlated with increasing agricultural income at a subsistence level, as the sector becomes more sophisticated, the capacity of farmers to absorb new technologies becomes important. Similarly, the health system must respond to the needs of poor smallholders, especially in dealing with HIV/AIDS. A short-term agricultural strategy that would build on the Government’s PROAGRI II strategy should include these cross-cutting elements:

BASIC INFRASTRUCTURE DEVELOPMENT. Any development of the agriculture sector requires development of good roads. The current cost of transportation is a major constraint. Additionally, markets need to include storage facilities and function well. This will also increase participation by the private sector in the rural economy.

EXPANDED USE OF IRRIGATION. Irrigation helps to diversify income and reduce risk. In addition to improving management of existing irrigation infrastructure, new irrigation systems for smallholders — from small dams to groundwater —will mitigate vulnerability from unpredictable rainfall. Irrigation infrastructure must be considered as a public good given that investments are high.

IMPROVED MANAGEMENT OF PUBLIC EXPENDITURES. As the Government embarks on a medium-term financial framework, one critical aspect is to include all expenditures in rural areas within the budgeting framework. This requires that all off-budget expenditures be identified and brought into the budget system.

PROMOTION OF A GOOD BUSINESS ENVIRONMENT. Such promotion requires (i) reducing corruption, (ii) reducing the cost to register a business, (iii) facilitating dispute settlement mechanisms, (iv) easing the application of regulations, (v) expediting payment of refunds by the Government, (vi) maintaining flexible labor regulations, and (vii) facilitating access to land.

xix

xiv. Reducing vulnerability and risks requires diversifying income sources from primary agriculture to wage income in rural non-farm areas. Such diversification includes improving the flexibility of labor markets, developing marketing infrastructure, improving market access, and improving the business environment through good governance. Reducing vulnerability also requires helping to curb the HIV/AIDS epidemic. Households need practical help to deal with labor shortages and nutritional deficiencies. A multisectoral approach to counter this epidemic is urgently needed.

xv. Food security is still a concern for rural households given Mozambique’s vulnerability to the vagaries of climate. The Government should continue to ensure that its food aid policy does not undermine domestic production incentives while instituting monitoring mechanisms that enable it and donors to respond quickly during emergencies.

Government, Donors, and Civil Society Need to Think Togetherxvi. Coordination requires multiple stakeholders — the Government, beneficiaries, the private sector, NGOs, and donors. Because unit investment costs are high to develop infrastructure, it is appropriate for the public sector to provide such services, including roads, railways, and surface irrigation facilities. The private sector should sell inputs and buy outputs. One deterrent for the private sector to be actively involved in selling inputs is that transaction costs are high to reach all farmers. Input distribution and produce marketing costs would be lower if farmers organized into rural producer organizations so they can participate in bulk buying and group marketing schemes.

THE GOVERNMENT NEEDS TO BE CLOSER TO THE PEOPLE. Given that the country is so large, decentralization becomes an important objective. The Government is committed to a decentralization framework and is working toward it, however, the strategy is still at a nascent stage. Together with strengthening government at the provincial and district levels it is important to empower communities and community-based organizations so they ensure that local governments are accountable and transparent.

CIVIL SOCIETY AND NGOs ARE IMPORTANT STAKEHOLDERS. To ensure that services are delivered to grassroots smallholders, civil society and NGOs must be closely

Limits of this Strategy

The fiscal implications of this strategy are not addressed. Such an analysis is beyond the scope of the document and would require more transparent documentation of public expenditures in the agriculture sector.

Natural resource management is only partially addressed because it is already included in the 2005 CEM (World Bank, 2005e) and its background papers.

Labor is obviously a vital issue in an agricultural development strategy, and the health of the population is a major component of that issue. Malaria is a key problem in the Mozambican health sector, and many believe it is a larger threat to rural health than HIV/AIDS. In this strategy, however, malaria is only partially addressed because the Bank expects to tackle this disease in the upcoming Country Assistance Strategy (CAS).

xx

aligned with agricultural development programs. At the district and provincial levels they should be involved in identifying and planning development programs. Government administration cannot be everywhere and hence in such a large country it is all the more important for these organizations to be involved. Local NGOs need to be strengthened so that when international organizations depart the capacity exists to mobilize communities, ensure that people are heard, and hold the Government accountable.

CURRENT DONOR PROGRAMS ARE NOT WELL COORDINATED. For the agriculture sector, the Ministry of Agriculture must inventory all activities and establish how and in what way donor programs complement its own programs. Additionally, the donor community must play an important role in providing long-term financing to the public sector. The stability of donor support is also an important factor.

DONORS NEED TO ENSURE FUNDING. Given that the Mozambican budget is funded primarily by external resources, the donor role is critical. Donors need to think together — not so much for their own interests as much as for the interests of the country. Programs should be jointly developed with the Government and communities, and should not compete with other donors. A truly empowered Government is one that can tell donors what it wants financed and where it wants the money to be invested with “government in the driver’s seat.”

1

1. Past Decade of Agriculture and Poverty in Rural Mozambique

1. Mozambique’s agricultural sector has shown remarkable progress in the recent past, with rural poverty declining by 16 percentage points from 1996-97 to 2002-03. Increased smallholder agricultural production was a fundamental part of this impressive achievement, and rural inequality increased only slightly because the decline in poverty was broad-based. The non-farm economy* also performed strongly, including small businesses and increased self-employment related to extracting natural resources, as well as increased wage labor opportunities. These factors contributed to reducing rural poverty for the upper income quintiles, however, despite substantial growth of the agricultural and rural non-farm sectors, poverty remains widespread.

2. Current patterns of agricultural growth are not sustainable and rural incomes face a substantial risk of stagnating. Over the past decade, agricultural growth was almost entirely driven by farming more land with a larger rural labor force, with few technological improvements. Improved agricultural technologies played only a minor role. Access to and use of improved crop technologies remains very limited, and there is evidence that crop yields are stagnant. If appropriate action is not taken, agricultural growth will slow and rural poverty will remain widespread.

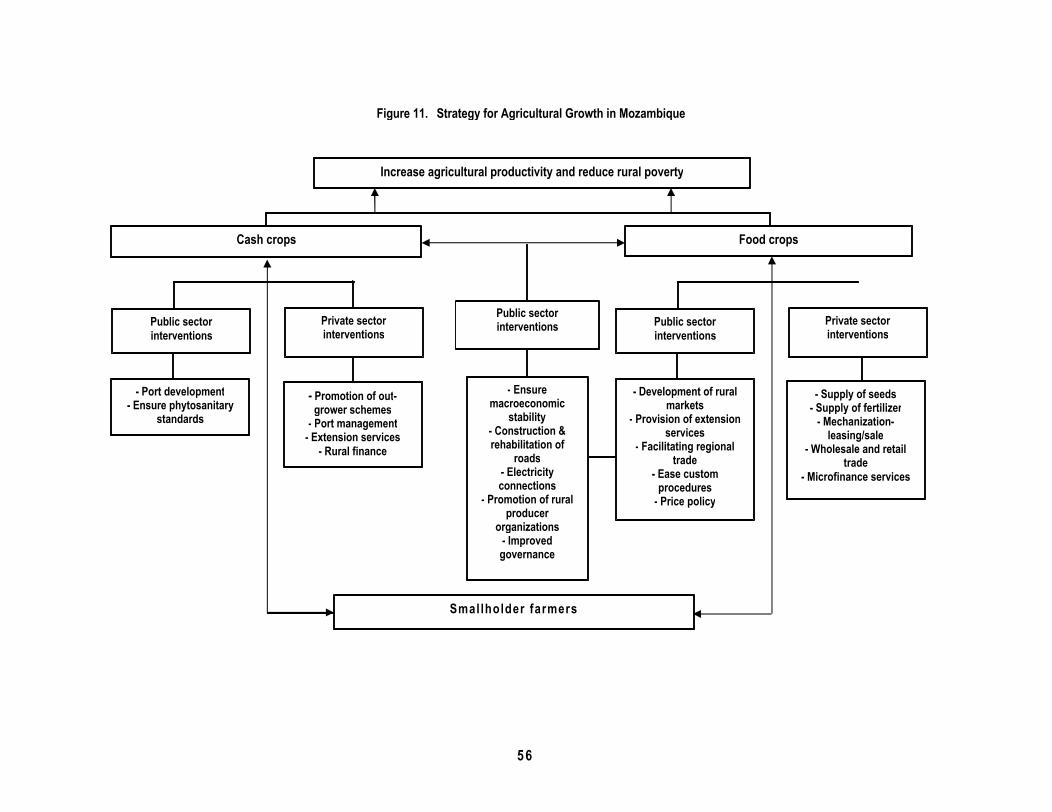

3. In the medium term, incomes can only improve with higher land and labor productivity, and future growth particularly depends on adaptation of new agricultural technologies. These include more and better extension services; adoption of best practices; introduction of new seed varieties, increased use of fertilizer, animal traction, and irrigation; and construction of more roads. Development input and output markets are critical because farmers have little incentive to improve yields if they cannot sell what they produce. In the non-farm sectors, primary education and measures to increase labor market access for women are important, as well as establishing marketing links to the local economy and neighboring countries. Finally, adoption of higher-value crops is crucial.

*In this strategy, rural non-farm activities occur outside of owner-operated farms. The non-farm sector thus includes wage labor on farms. Agriculture includes all primary production of food and cash crops, however, it excludes food processing, agricultural services, and other primary sectors such as mining or quarrying although they may take place on the farm.

2

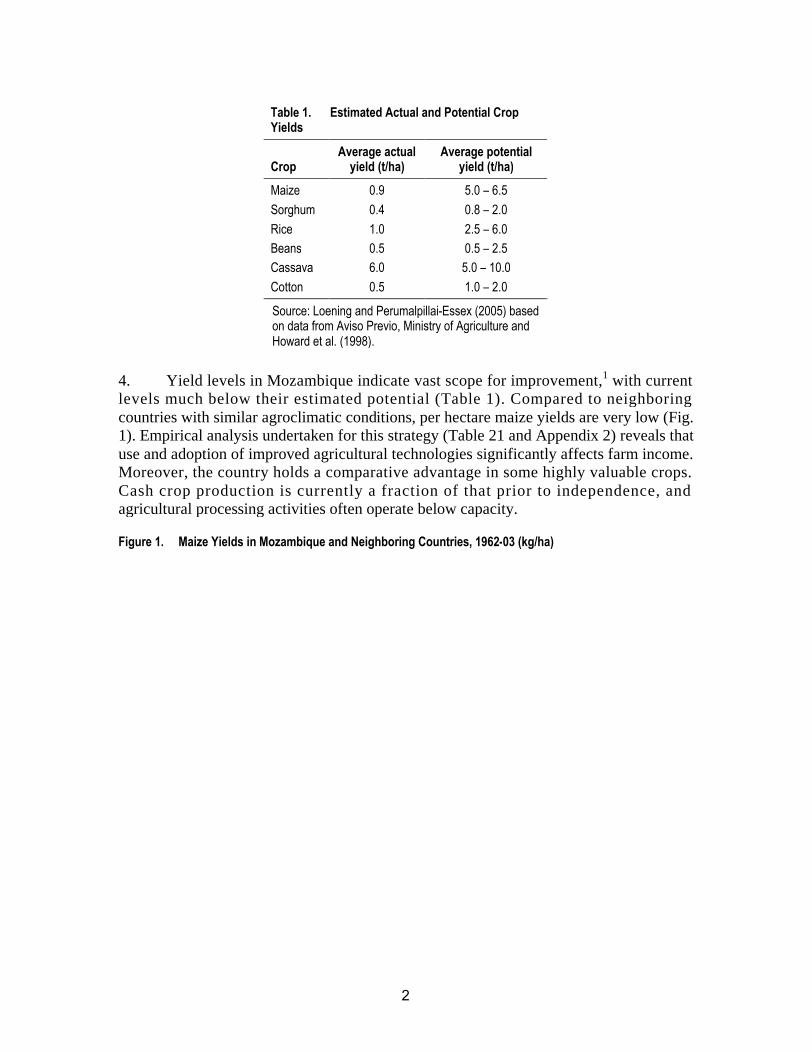

Table 1. Estimated Actual and Potential Crop Yields

CropAverage actual

yield (t/ha)Average potential

yield (t/ha)Maize 0.9 5.0 – 6.5Sorghum 0.4 0.8 – 2.0Rice 1.0 2.5 – 6.0Beans 0.5 0.5 – 2.5Cassava 6.0 5.0 – 10.0Cotton 0.5 1.0 – 2.0

Source: Loening and Perumalpillai-Essex (2005) based on data from Aviso Previo, Ministry of Agriculture and Howard et al. (1998).

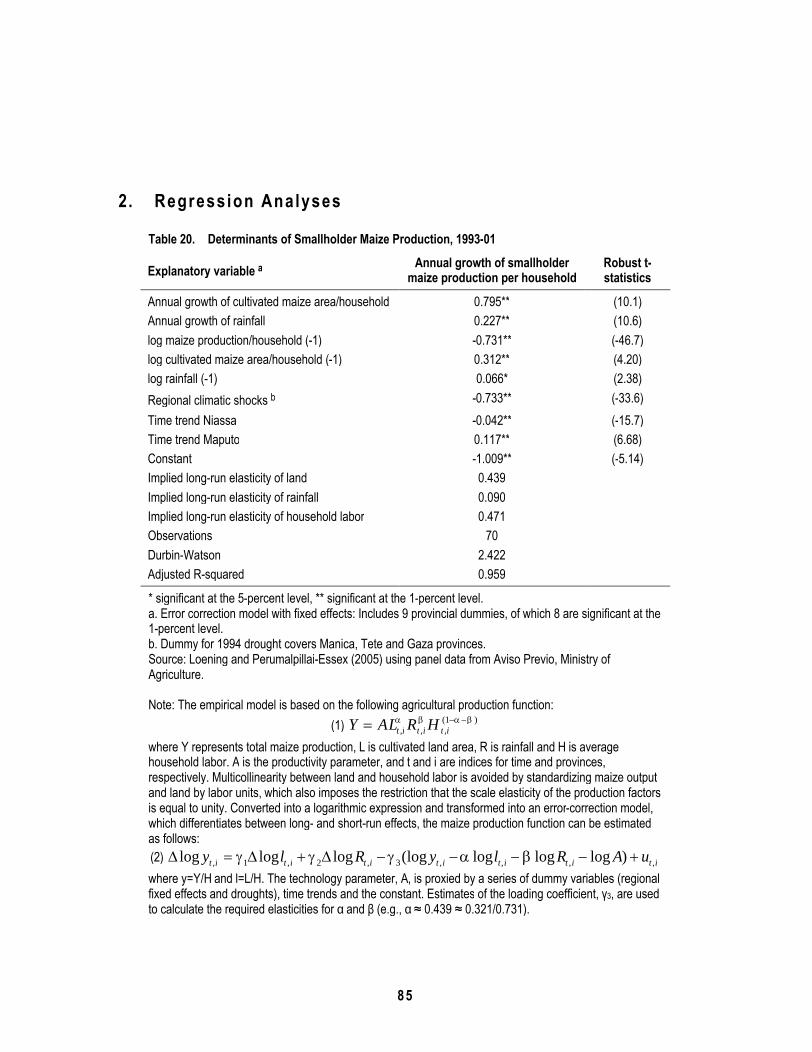

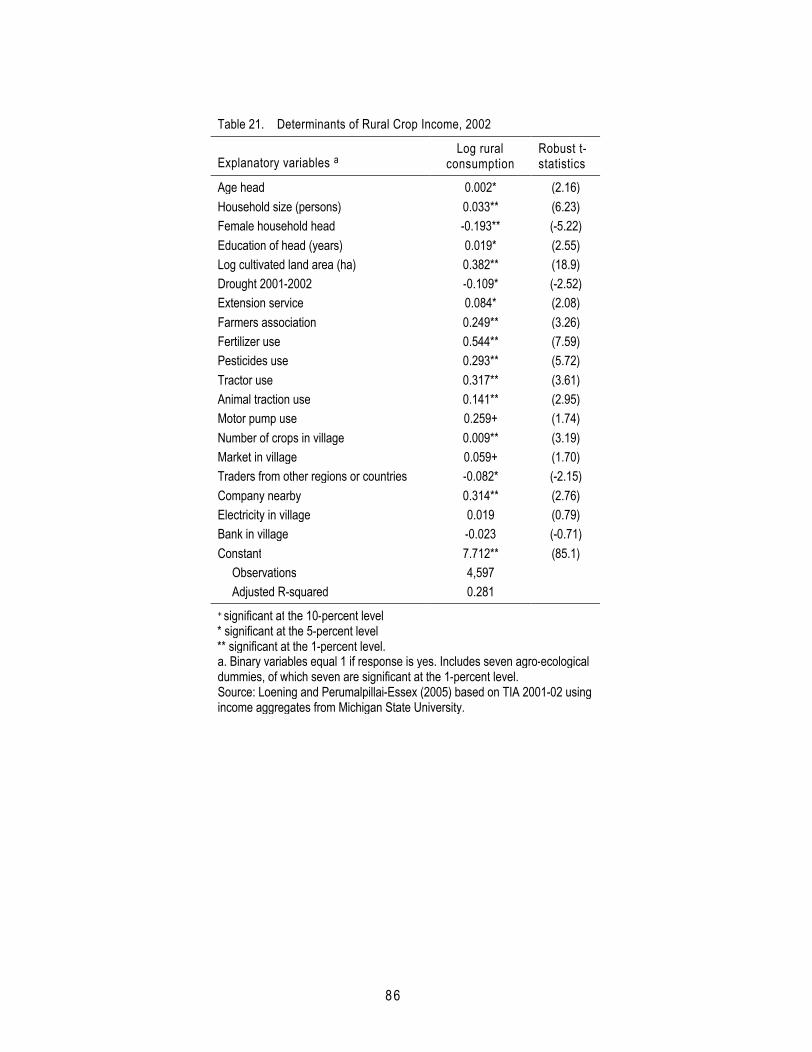

4. Yield levels in Mozambique indicate vast scope for improvement,1 with current levels much below their estimated potential (Table 1). Compared to neighboring countries with similar agroclimatic conditions, per hectare maize yields are very low (Fig. 1). Empirical analysis undertaken for this strategy (Table 21 and Appendix 2) reveals that use and adoption of improved agricultural technologies significantly affects farm income. Moreover, the country holds a comparative advantage in some highly valuable crops. Cash crop production is currently a fraction of that prior to independence, and agricultural processing activities often operate below capacity.

Figure 1. Maize Yields in Mozambique and Neighboring Countries, 1962-03 (kg/ha)

0

500

1000

1500

2000

2500

62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 '00 '02

Mozambique Zambia Malawi Tanzania Zimbabwe

Source: Loening and Perumalpillai-Essex (2005) based on FAOSTAT, three-year moving averages

3

5. Only about 4.5 million of 36 million hectares of potentially arable land are cultivated. The country has considerable untapped opportunities for irrigation, with only 14 percent of a potential 3.3 million hectares irrigated. In addition, major river systems remain largely unexploited (for example, the Zambézi, Save, and Limpono systems).

6. Mozambique benefits from its location and neighbors. With a long coastline and three major ports, the country provides shipping services to the land-locked countries of Malawi, Zambia, and Zimbabwe. Informal cross-border trade between Mozambique and its neighbors enables farmers to take advantage of input and output markets in other countries, and mobility across borders is already important. For example, labor currently migrates from Malawi to Mozambique to help sustain growth in the tobacco sector. Likewise, due to the political situation in their country, a number of Zimbabwe farmers cultivate tobacco and other high-value crops in Mozambique.

7. This chapter describes the factors behind agricultural growth and the decline of rural poverty over the past decade. In addition, it analyzes the constraints facing smallholder agriculture and rural non-farm employment, provides a snapshot of the agricultural sector, analyzes the determinants of agricultural growth, discusses the determinants of the decline in rural poverty, and briefly examines the non-farm sector and labor markets in rural Mozambique.

Mozambique’s Agr icul tural Sector8. Agriculture in Mozambique is dominated by smallholders who farm in a risky environment that is vulnerable to droughts and floods, with 15 over the last 25 years. Crop production varies by region, with large differences in rainfall, temperature, soil types, and market access. Farming in Mozambique was dramatically affected by three decades of war.

Dominance of Smallholder Agriculture

9. Agriculture in Mozambique is almost entirely dominated by smallholders. The agricultural economy is a major source of livelihood, and food represents about two-thirds of total consumption, especially among the rural poor. An estimated 68 percent or about 12.5 million people live in rural areas. Rural households are predominantly smallholders who provide about 95 percent of agricultural GDP with the balance from a small number of medium and large commercial farms.2 Average cultivated area per household is only about 1.4 hectares. In 2003, there were an estimated 3.2 million farm families cultivating some 4.5 million hectares (Table 2). Medium- and large-scale farmers are almost insignificant in terms of land area and numbers of farms.3 Two-thirds of agricultural production is for home consumption and only 5 percent is generated by large-scale agriculture. Most of the agricultural land area for small (less than 10 hectares) and medium farms (10-50 hectares) is cultivated for basic food crops. By contrast, large farm enterprises (more than 50 hectares) produce mostly cash-crops.

10. Landless wage earners are often women and are among the poorest. Seasonal and casual farm laborers are also often women and from some of the poorest rural households. As in much of Sub-Saharan Africa, these female-headed households tend to

4

be more disadvantaged than the average rural household in terms of access to productive assets and education. Anecdotal evidence suggests that many must rely entirely on their meager wage income because they do not receive remittances from male members of the household. Because of the protracted wars, women were 53 percent of the population in 1997, the year of the latest population census, compared to 51 percent in 1981. Also, in rural areas women tend to work predominantly in the agriculture sector and are about two-thirds of the total agricultural labor force.4 Although in 2003 about 23 percent of rural households were headed by females, it should be noted that landless labor in Mozambique is somewhat rare. It is the combination of a lack of productive factors and human capital that makes land-constrained rural households among the poorest.

11. Migration has been an important feature of rural life. Migration in rural Mozambique has different patterns: rural-rural, rural-urban, and from Mozambique to its neighbors (in particular, the male out-migration to South Africa). In its tumultuous past during the protracted wars of independence (until 1975) and the subsequent civil war (until 1992), the rural population migrated significantly. The exact magnitude of rural migration flows are poorly documented. During the civil war, an estimated 1.5 million people left Mozambique, while some 4 million moved internally. Migrants typically moved to more secure rural areas and to urban or peri-urban areas. To this point more than 1 million refugees have returned,5 which has enormous implications for agricultural land use. Also, the promotion of communal production has affected population settlements and agricultural land use.

Livelihood in a Risky Environment

12. Mozambique is highly vulnerable to droughts and floods, with a total of 15 over the last 25 years. These events greatly affected the rural sector and the country’s overall economy. For example, the major floods of 2000 led to an abrupt fall of agricultural GDP and affected some 2 million people. Similarly, the regional droughts of 1994 and 1996 slowed total agricultural GDP growth and affected some 1.5 million people in the southern and central parts of the country, and were then followed by a cholera epidemic.6

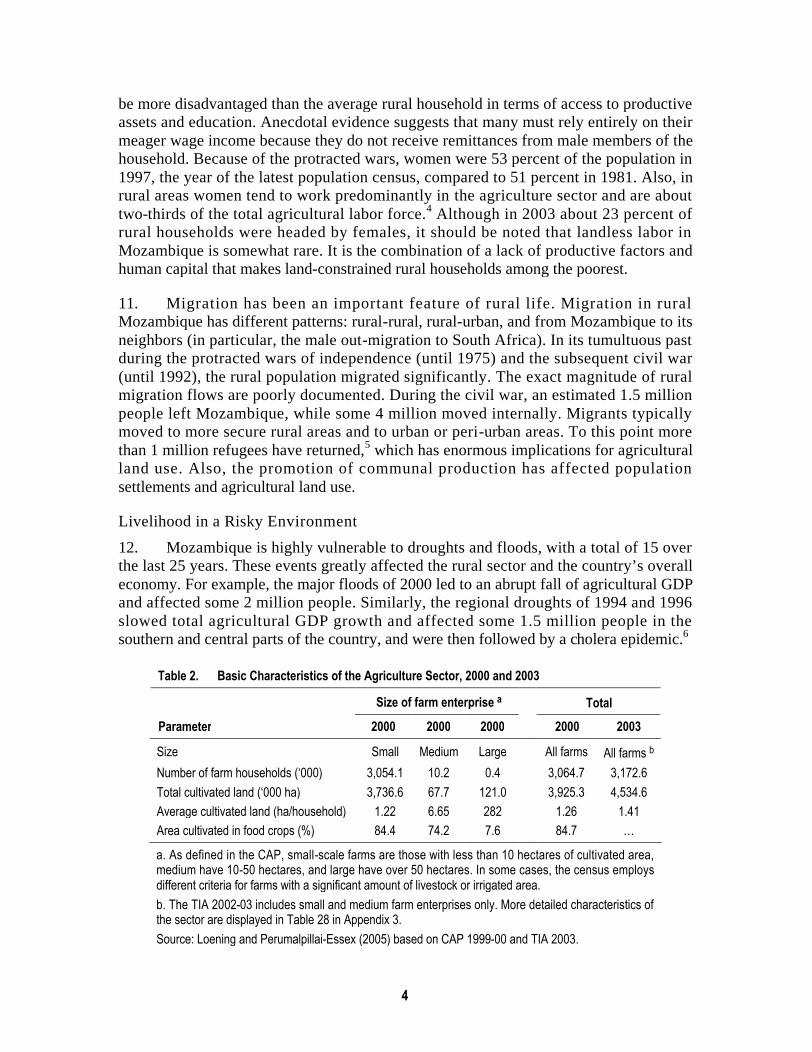

Table 2. Basic Characteristics of the Agriculture Sector, 2000 and 2003

Size of farm enterprise a TotalParameter 2000 2000 2000 2000 2003

Size Small Medium Large All farms All farms b

Number of farm households (‘000) 3,054.1 10.2 0.4 3,064.7 3,172.6Total cultivated land (‘000 ha) 3,736.6 67.7 121.0 3,925.3 4,534.6Average cultivated land (ha/household) 1.22 6.65 282 1.26 1.41Area cultivated in food crops (%) 84.4 74.2 7.6 84.7 …

a. As defined in the CAP, small-scale farms are those with less than 10 hectares of cultivated area, medium have 10-50 hectares, and large have over 50 hectares. In some cases, the census employs different criteria for farms with a significant amount of livestock or irrigated area. b. The TIA 2002-03 includes small and medium farm enterprises only. More detailed characteristics of the sector are displayed in Table 28 in Appendix 3.Source: Loening and Perumalpillai-Essex (2005) based on CAP 1999-00 and TIA 2003.

5

13. Low productivity agriculture provides a precarious livelihood. The smallholder sector in Mozambique is characterized by holdings of multiple small plots, multiple crops, low input use, and low productivity. Average crop yields (Table 1)are about one-half of the regional average.7 Smallholders have limited access to capital, little schooling, are at the mercy of highly variable rainfall, and suffer seasonal price risks. Farms typically use manual cultivation techniques and little or no purchased inputs. In 2003, only about 4 percent of farmers used chemical fertilizers and only about 5 percent used pesticides. The use of chemical inputs is generally concentrated among cash crop growers. Only about 11 percent of households use some form of irrigation.8

14. Food crop production is Mozambique’s most important agriculture sub-sector. Most rural households diversify to cope with low productivity and income, and smallholders are poorly integrated with markets. The majority practice extensive shifting cultivation, only about one-third sell any crop output, and almost two-thirds live in households that lack food security. The most important food crops are cassava and maize, followed by sorghum and rice. Cassava is an important component of the smallholder’s risk reduction strategy in the context of Mozambique’s variable climate because it is drought tolerant and resistant to disease.9 For the most part, food crop producers use seeds reserved from the previous year’s crop. About 82 percent of rural households identify seed supply as their predominant agricultural problem.10

15. Smallholders do, however, contribute to the production of export crops, particularly cashew, cotton, and tobacco. An estimated 16 percent of rural households engage in cash crop production. These smallholders are contracted by larger firms under out-grower schemes. Contracting arrangements are one way to overcome the failure of input and credit markets. These arrangements allow farmers to access extension advice, inputs, and credit, but oblige them to sell their output to the input provider . As a consequence, the number of farmers growing tobacco and cotton has risen significantly from 1995-96 to 2002-03.11

Regional Variation of Crop Production

16. Mozambique is a vast country with a wide variety of regional cropping patterns. Large regional differences include rainfall, temperature, soil types, and market access. Although the country is grouped into 10 agroecological zones, it can be broadly divided into three geographical regions: North (Niassa, Cabo Delgado, and Nampula), Center (Zambézia, Tete, Manica, and Sofala) and South (Inhambane, Gaza, and Maputo province) (Table 3). Appendix 4 displays the main features of Mozambique’s agroecological regions and its farming systems. Mozambique’s agroclimatic zones range from arid and semi-arid (mostly in the south and southwest) to the sub-humid zones (mostly in the center and the north) to the humid highlands (mostly the central provinces). The arid regions of the south and southwestern part of Gaza province are suitable only for livestock. The principal regional variation of cropping practices is based on soil conditions and rainfall with changes in quantity and predictability from north to south.

6

Table 3. Agroecological Conditions and Regional Crop Production Patterns

Category North Center South

Annual rainfall (mm) 1,000 – 1,800 1,000 – 1,200 400 – 1,000

Main food crops Cassava, maize, rice, sorghum, sweet potatoes, beans

Cassava, sweet potatoes, maize, rice, beans, sorghum, millet

Cassava, maize

Main cash crops Tobacco, cotton, cashew, groundnuts

Tobacco, cotton, groundnuts, horticulture

Only limited agricultural production

Livestock Large pasture areas in Tete province

Pasture areas in Sofala Pasture areas with rural population raising cattle and goats

Source: Compiled from Appendices 3 and 4.

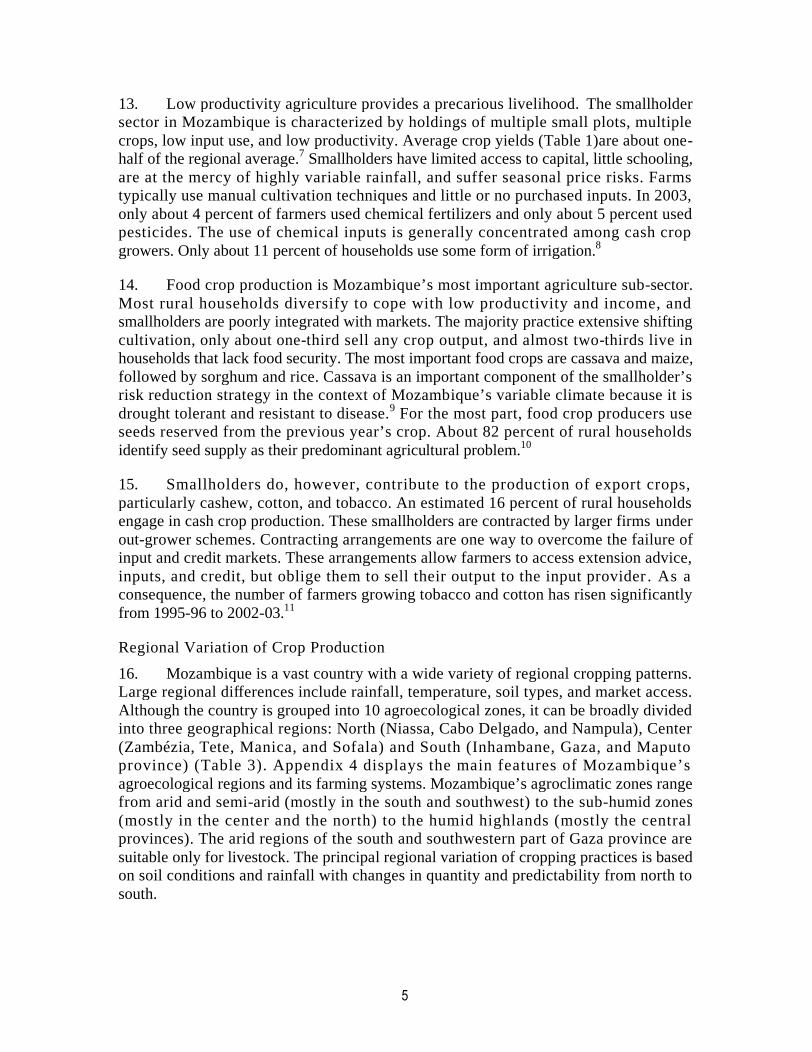

17. The most fertile areas are in the northern and central provinces. Annual rainfall in the north ranges from 1,000 to 1,800 mm (Table 3). The overwhelming part of agricultural production takes place in the north. Farmers in this region use a combination of food and cash crops — cassava and maize are the most important food crops, followed by rice, sorghum, beans, and sweet potatoes. Important cash crops are cotton, cashew, and groundnuts (Map 2). In addition, Tete and Niassa provinces are Mozambique’s mostimportant tobacco areas. The central region also has good potential for agriculture with good soils and annual rainfall ranging between 1,000 and 1,200 mm. In central Mozambique, cassava, maize, and sweet potatoes are the most important food crops, followed by beans, sorghum, millet, and rice. The central region is also an important producer of several horticultural products, as well as coconuts, principally in the coastal areas. Important cash crops in central Mozambique, although produced in much lesser quantities than in the north, include cotton, groundnuts, and some cashew.

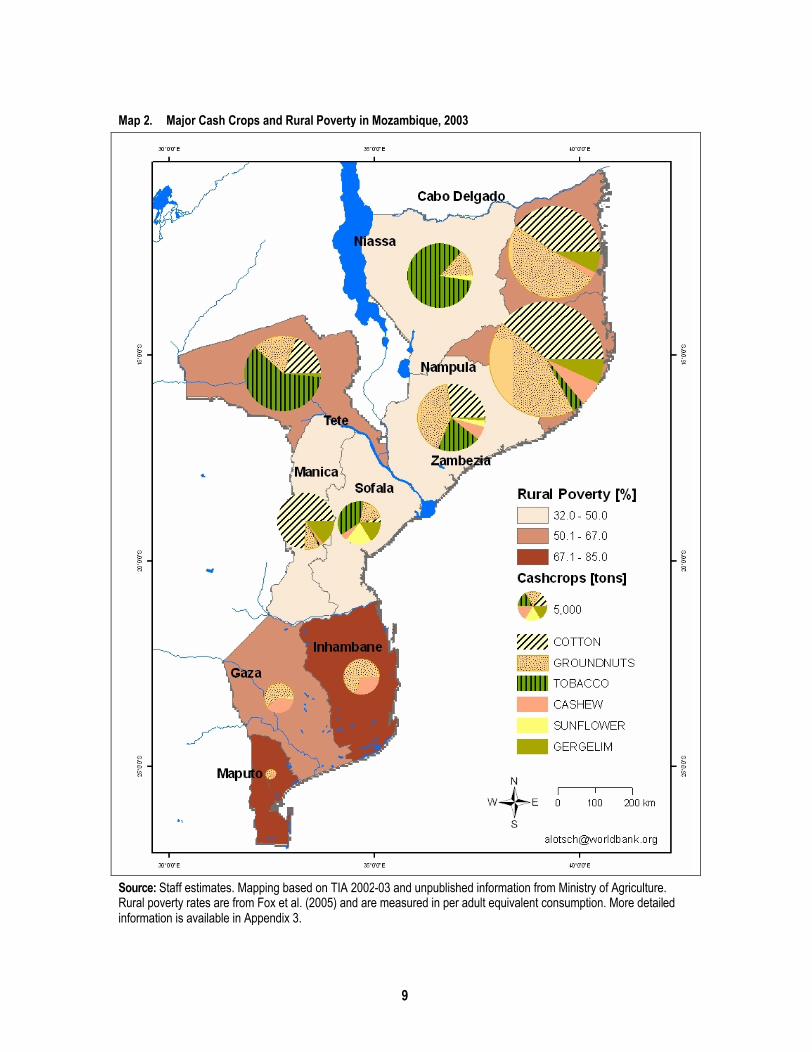

18. The southern region is drier with sandy, infertile soils, and a higher risk of drought losses. Total agricultural output from the southern region, compared to the central and northern regions, is relatively low. The main crop is cassava, followed in very low quantities by maize, rice, groundnuts, sweet potatoes, and cashew. In the southern provinces, cassava and maize are still the most important crops in terms of land area, even though maize yields are lower and the agroecological conditions are not conducive to grow maize. The southern region is also the heart of Mozambique’s livestock activities (Map 3) because animals there are less prone to diseases.

Food Crops, Cash Crops, and Livestock

19. For this analysis, the agriculture sector is divided into three broad sub-sectors —food crops, cash crops, and livestock.

7

Map 1. Major Food Crops and Rural Poverty in Mozambique, 2003

Source: Staff estimates. Mapping based on TIA 2002-03 and unpublished information from Ministry of Agriculture. Rural poverty rates are from Fox et al. (2005) and are measured in per adult equivalent consumption. More detailed information is available in Appendix 3.

8

FOOD CROPS

20. Subsistence agriculture has significant growth potential in Mozambique. To ensure household food security, most cultivated land is used to grow low-value maize and cassava (more than 50 percent of the total).12 With the remaining area, smallholders diversify with a wide variety of other food crops, and further diversify risk by planting in both low lying and higher elevation areas. Yields are low and show stagnant patterns, moreover, yields are estimated at only a small fraction of their potential (Table 1).

CASH CROPS

21. The cash crop sector has the potential for substantial yield increases. Today cash crops occupy roughly 5 percent of cultivated land and contribute to some 5 percent of agriculture GDP, which in turn is about 6 percent of the country’s exports. The traditional cash crop sector includes cotton, tobacco, cashew, sugar, and tea. Cotton and tobacco are grown under contract, cashew is a smallholder crop, and sugar and tea are plantation crops. As in the food crop sector, there is a major gap between potential and actual yields. Seed cotton is one example. Yields in Mozambique are significantly constrained by a lack of high-yielding, pest-resistant varieties adapted to local agroclimatic conditions. Yields average 0.6 tons per hectare compared to 0.9 in Zimbabwe and over 1.0 in francophone West Africa.13 Yields also vary within Mozambique — a high-input block may yield 1.4 tons per hectare while a low-input block may produce only 0.5-0.7.14

22. Another important example is cashew, which is of great importance to smallholders. Cashew trees are often old and diseased. The most recent plantings date from the 1950s and 1960s, and average yields are only 1.5-3.0 kilograms per tree, whereas the potential can be as high as 10-15. One-quarter of the national stock of about 25-26 million old trees is attacked by powdery mildew (Oidium) and other diseases, which reduces yields by as much as 70 percent.15 During the dry season trees are damaged by fire.16 These problems not only affect yield, but also reduce quality

23. With a potential irrigated area of about 3 million hectares, irrigation of more land will increase the yield and quality of cash crops. Mozambique’s irrigated areas lie mainly in the central and northern provinces, with the Zambézi basin accounting for nearly 60 percent of the total. There is less irrigated land in the south, about 300,000 hectares. Out of the 3 million hectares that are estimated to be irrigable, about 97,000 are equipped for irrigation but only 37,000 (or 40 percent) actually are irrigated.17 Of the three types of irrigation — large-scale public, donor-funded small-scale, and farmer-run micro irrigation — smallholdings are most likely to be expanded where the second and third types or irrigation are available. The first type is mainly used by large commercial farmers. For example, about 36,000 hectares are currently cultivated for sugar.18 Other than rice and sugar, a variety of high-value horticultural crops can be grown on irrigated areas.

9

Map 2. Major Cash Crops and Rural Poverty in Mozambique, 2003

Source: Staff estimates. Mapping based on TIA 2002-03 and unpublished information from Ministry of Agriculture. Rural poverty rates are from Fox et al. (2005) and are measured in per adult equivalent consumption. More detailed information is available in Appendix 3.

10

Table 4. Livestock in Mozambique, 1994-2003 (‘000)

Livestock 1994 1996 2000 2002 2003

Cattle 470 573 722 791 969Goats 1,655 3,101 5,047 4,938 4,748Sheep 129 211 174 196 136Pigs 1,694 1,382 2,347 1,601 1,354Chickens 10,844 17,459 23,587 22,616 17,647Ducks 1,858 2,838 4,132 2,126 1,537Source: Ministry of Agriculture.

24. Irrigated agriculture for smallholders has high growth potential. Developing smallholder irrigation would cost an estimated US$600-800 per hectare compared to US$3,000 per hectare for large farms. Most smallholder irrigation is now used for double cropping food crops — intercropping with vegetables and at times cash crops. Under existing cropping patterns, the average value-added is estimated at US$500-600 on the smallest farms and US$800-1,000 for farms of between 5 and 10 hectares. If a total of US$20 million were invested per year, that investment could generate about US$250 million of value added in agriculture (even assuming no major shifts in cropping patterns).19

LIVESTOCK

25. Livestock make significant contributions to the livelihood of smallholders and the rural poor. The number of livestock has grown significantly over the past decade (Table 4). They are owned by the rural poor to increase and diversify income, and to reduce risk. The very poor can afford only some chickens and pigs, while those at the next level can add goats and a few cattle, and the better off among the poor can afford larger numbers of chickens, pigs, and cattle.20 Cattle are used mainly for animal traction, as a status symbol, and are rarely sold. Nationwide, only 4 percent of the population possesses cattle.21

Livestock holdings include other animals such as rabbits, ducks, and guinea pigs. As with other agricultural activities, the roles of men and women differ. Women often raise chicken and pigs while men raise goats and cattle.

26. The contribution of livestock to family income varies by area but is generally significant. In Muchamba, Tete for example, livestock provided 45 percent of family income for the poorest to nearly 60 percent for the less poor. In Massalane, Inhambane, the range was 21 percent to 65 percent.22 Using stylized household income models in the four sets of provinces, northern, central western, central eastern, and southern, the estimated potential contributions of livestock to family income were 12 percent, 34 percent, 16 percent, and 27 percent, respectively.23 The contribution of livestock is more significant in the arid zones of Tete, Manica, Gaza, and Maputo. Currently, more than two-thirds of Mozambique’s cattle herd is located in Tete, Gaza, and Manica provinces.24

About two-thirds of total livestock production is in northern provinces and the central eastern provinces. Of the total production in these provinces, some 55 percent is pork and 40 percent goats and poultry. For the provinces supplying Maputo, pork was also

11

important at 25-30 percent, goats and poultry at 45 percent, with beef providing the remaining 25-30 percent.25

27. Several constraints undermine an increase in livestock numbers, but chief among them is a high prevalence of disease. For example, Newcastle disease is a major problem for poultry, in the northern provinces tsetse flies affect cattle, and African swine fever affects pigs. In addition, the inadequacy of animal husbandry services is a common problem because extension services do not cover all districts. The ability of communities to expand grazing for cattle is also determined by the availability and variability in pasture quality, and access to water and veterinary services. There are some conflicts between crop agriculture and livestock, especially under drought conditions and when the animals are large. Where there are crops nearby, animals need to be tethered to reduce the possibility of conflict. The lack of access to credit is problem in crop agriculture and also undermines the livestock sector. Poor families cannot raise credit to purchase animals, and women have difficulty accumulating livestock. If widowed, they are stripped of all family assets upon the death of their husbands, including family animals.

28. The commercial sector serves primarily a quality-conscious but price insensitive urban market of restaurants and hotels. The family sector serves domestic demand forcheap meat cuts. The commercial sector has better access to surplus grain and crop by-products than the family sector, which sells through a well-established network of local traders, butchers, and other farmers, and typically has no problem selling its products.

29. Family livestock shows substantial potential for growth. Financial analyses for households rearing chickens and pigs using stylized household enterprise models suggest that the contribution of these to household income can be substantial. For example, the contribution of chickens to household income can be 7 percent in the northern provinces, 15 percent in the central northern provinces, 8 percent in the central southern provinces, and up to 13 percent in southern provinces. For pigs, the contribution is much higher at 29, 38, 23, and 38 percent, respectively). The contribution of cattle in non-tsetse areas is even more important, ranging from around 40 percent in the northern and southern provinces, to 52 percent in the central western, to 32 percent in the central eastern provinces (Map 3).26

Effects of Three Decades of War on Commercial Farming

30. Despite considerable reconstruction efforts after three decades of war, much of the physical infrastructure remains deficient.27 There was massive destruction of housing, communications networks, and education and public health facilities. Livestock herds were decimated and fields were abandoned. The population of 19 million was severely affected, with more than 1 million dead, 1.5 million refugees, and 3.2 million people internally displaced. After the General Peace Agreement in 1992 and democratic elections in 1994, the agriculture sector moved away from centrally planned state intervention in agricultural management, pricing, and marketing toward market allocation of agricultural resources, liberalized pricing policies, and privatization of state assets. Economic reform, initial rehabilitation of rural infrastructure, and the rapid post-conflict expansion in production have also stimulated a small agribusiness sector.

12

Map 3. Cattle Population and Rural Poverty in Mozambique, 2003

Source: Staff estimates. Mapping based on TIA 2002-03 and unpublished information from Ministry of Agriculture. Rural poverty rates are from Fox et al. (2005) and are measured in per adult equivalent consumption. More detailed information is available in Appendix 3.

13

31. Large-scale commercial farming, however, has declined in importance since the 1970s. Until independence in 1975, cash crops (such as cashew, sisal, and cotton) were almost two-thirds of total exports. The decline started with the exodus of the Portuguese and other settlers after independence, which was a major loss of managerial and technical staff. It was hastened by nationalization, poor management, inappropriate investments in plants and machinery, overvalued exchange rates, low fixed prices, marketing controls, declining international prices, and sabotage during the civil war.

32. Today, most of the companies have been privatized but struggle with obsolete machinery, weak markets, and low competitiveness. As part of its strategy for agricultural development, the Government has attempted to revive both cash crop production and agroprocessing with some recent success (e.g., tobacco and horticulture). Some of the policy instruments, however, have proved politically contentious and created uncertainty in the relevant industries. Larger farms in Mozambique tend to be in the zones where animal or mechanical traction is possible and where market access is adequate. Cash crops are mainly grown for export and account for about one-third of total exports, but occupy only up to 5 percent of the total planted area.

Determinants of Agricultural Growth33. The rapid growth of Mozambican agriculture is primarily a result of increased area and household labor. Crop diversification has significantly increased, but adoption and use of technologies has seen only modest advances. Extension coverage is limited, but where available, significantly affects rural crop production, but smallholder yields are low.

Rapid Growth in Agriculture

34. Starting from a low base of per capita income, agricultural growth was high during the mid-1990s, in fact, Mozambique has one of the highest growth rates in the region. Since the Peace Accords the agriculture sector has grown rapidly because farmers were able to return to their land and markets opened up. Average annual GDP growth for the agriculture, livestock, and forestry sectors was 6.2 percent between 1992 and 2003.28

In favorable years growth has peaked at about 10 percent annual growth. Over the past decade the rural economy has suffered heavily from climatic shocks (droughts in 1994 and 1996, and floods in 2000) (Fig. 2). These events were, however, followed by an immediate recovery of the economy.

35. Mozambique’s high agricultural growth rates are consistent with household-level evidence.29 Considering rural population growth of about 1.9 percent annually, estimates from a background study of the 2005 Country Economic Memorandum reveal that total rural consumption grew annually at about 6 percent between 1996 and 2003.30 This compares favorably with the average annual growth rate of 6.6 percent for the agriculture, livestock, and forestry sectors over the same period. Part of the difference may be attributed to real income growth of the non-farm economy, as shown in the following sections. Growth of maize production, Mozambique’s predominant food crop as a proxy indicator, equally confirms the basic production trends (Fig. 3). Maize is

14

cultivated by about 79 percent of rural households and occupies about 35 percent of total planted area.31

Figure 2. Growth of Agricultural GDP, 1992-03 (percent)

-30%

-20%

-10%

0%

10%

20%

30%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Source: Loening and Perumalpillai-Essex (2005) based on National Accounts data, Instituto Nacional de Estatística (INE). Agriculture includes the livestock and fishery sectors.

Figure 3. Maize Production, 1993-03 (‘000 tons)

0

200

400

600

800

1,000

1,200

1,400

93-94 94-95 95-96 96-97 97-98 98-99 99-00 00-01 01-02 02-03

Maize AP Maize TIA

Source: Loening and Perumalpillai-Essex (2005) based on Aviso Previo (AP) and Trabalho de Inquérito Agrícola ao Sector Familiar (TIA), Ministry of Agriculture.

15

36. Over the past decade, sectoral shifts have been moderate, but the agriculture sector remains important. In 2003, agriculture was the largest sector and contributed 25percent of total GDP compared to 24 percent in 1992 and 31 percent in 1996.32 In context, however, agriculture makes a relatively modest contribution to total GDP considering that farmers are about 90 percent of the rural workforce and about 68 percent of Mozambique’s population of 19 million lives in rural areas.

37. Production of basic food crops is the key driver for increased agricultural production. Basic food crop production grew at an average rate of about 3-4 percent annually. Maize and millet production showed the highest increases, followed by sorghum, beans, rice, and cassava. Groundnut production may have declined by about 1 percent. Regionally, production increases were highest in the central regions, particularly in Tete province (Table 26).33