Embed Size (px)

Citation preview

Paper submitted to International Journal of Computer Integrated Manufacturing

Tooling Cost Estimation driven by Part, Mould and Method design

and its application for Design to Cost of Cast Products

Durgesh Joshi

Reader, Dept. of Industrial and Production Engineering,

SGS Institute of Technology and Science Indore

Dr. B Ravi

Professor, Dept. of Mechanical Engineering,

Indian Institute of Technology Bombay

ABSTRACT

In the present change driven environment, cost is determined by the competition. Hence, it

has become necessary to determine cost of new product early during the design stage. Tooling

cost is the major component of the fixed cost for new product development and is often

determined based on past experience. In this work the tooling cost is estimated by performing

regression analysis on 150 tooling pertaining to 50 cast parts of varying size and complexity.

Parameters considered for cost estimation are volume ratio, thickness ratio, flat surface ratio,

curved surface ratio, control dimensions, accuracy and surface finish. An integrated

framework for Design to Cost is proposed in this paper. In this framework solid model of cast

part is taken as input along with metal and process data. Automated parting surface selection,

along with simulation of feeding and gating system is performed to ensure optimal mould,

and method design. Part and mould design generate the basic form of the tooling. Additional

features are added on this basic form by method design to complete the tool design.

Parameters required for tooling cost estimation are computed from the solid model of the tool

design and cost of tooling is determined in advance at the design stage.

1. INTRODUCTION

Early cost estimation employing design to cost techniques translates into larger profits

because the cost reduction advantage starts from the first unit. It also enables companies to

deploy R&D resources for more innovative ideas, instead of modifying existing designs to

reduce costs (Davila and Wouters 2004). Also managing the cost during development stage –

while the design is still fluid – is usually easier and cheaper than after the product is

introduced. Target costing is the most popular Design to Cost technique. The target costing

process begins by establishing a selling price, based on market research, for the new product.

From this target selling price, the desired (target) profit is subtracted to determine the target

cost. In all likelihood, this target is below the company‟s current manufacturing cost. Teams

from many departments then perform functional cost analysis in an attempt to meet the target

cost. If the current cost estimate is at the target, or above the target, functional cost analysis is

used to make changes and prepare another cost estimate (Gagne and Discenza 1995).

Functional cost analysis requires a framework that relates the cost drivers and cost modifiers

to the geometry, quality and process parameters. This work focuses on development of such

framework for new products made by sand casting process. The total cost of a sand cast

product comprises of tooling cost, cost of metal, cost of indirect material, cost of processing,

cost of melting and cost of machining. The cost of tooling (patterns and core boxes) is

amortized over the number of castings produced, and can be a significant proportion of the

casting cost, especially when the order quantity is low. Research in casting cost estimation is

primarily focused on process and material selection to facilitate quotations. Traditionally in

industry especially small and medium enterprises (SMEs), tooling cost estimation is done

primarily by weight calculation. Some efforts have been made by researchers for estimating

the tooling cost on the basis of product complexity. We present a new approach to estimate

the tooling cost based on geometry parameters and quality parameters of existing tooling. The

geometric parameters considered are volume ratio, thickness ratio, flat surface ratio, and

curved surface ratio. The quality parameters considered are control dimensions and accuracy.

Tooling cost can be obtained for new product under development. Other costs are added to

tooling cost to facilitate functional cost analysis

2. LITERATURE REVIEW

A significant portion of profit that the product generates over its life is determined before the

product reaches to the market (Davila and Wouters 2004). During the product development

stage, the organization designs the features that (1) give the product an edge over competition

and (2) affect the cost that will shape the profit margins. Product design significantly affects

the revenue side - technological performance, customer appeal and timely market introduction

- before the first unit is sold. The cost side follows a similar pattern as a rule of thumb 80% of

the costs are engineered in, during the product development. Thus managing cost at the

product development stage emerges as important process to increase the profitability of future

products. Target costing is the most popular Design to Cost technique.

2.1 Design to Cost

Target costing was invented by Toyota in 1965 (Gagne and Discenza 1995). The target

costing process begins by establishing a selling price, based on market research, for the new

product. From this target selling price, the desired (target) profit is subtracted to determine the

target cost. In all likelihood, this target is below the company‟s current manufacturing cost.

Teams from many departments then perform functional cost analysis in an attempt to reach

the target cost. If the current cost estimate is at the target, the firm must decide whether or not

to introduce the new product. If the current cost estimate is above the target, functional cost

analysis is used to make changes and prepare another cost estimate. Bayou and Reinstein

(1998) presented three routes of target costing these are (1) Value Engineering: VE refers to

cost improvements through basic functional changes in product development stage VE is

conducted before mass production of model begins. (2) Cost Improvement: Cost improvement

refers to cost development by employing a structure that connects costing, pricing, market

share, normal profit margin and long term investment into a unified whole. This structure is

called Total cost management (TCM). The basic structure of cost development includes the

strategies for comprehensiveness, integration, flexibility, dynamic and long term continuity.

(3) Cost Cutting and Cost Shifting: Cost cutting entails slashing cost without going through

TCM. Thus the decision to reduce the last years cost by 20% is a cost cutting judgment. Cost

cutting refers to, decreasing the avoidable inefficiencies. To reduce unavoidable inefficiencies

redesigning or restructuring the production may be necessary. Cost shifting differs from cost

cutting in that it aims at reducing the cost even by decreasing the unavoidable inefficiencies.

Some ways of decreasing unavoidable inefficiencies can be: the manufacturer replaces the

current supervisor, leased or owned equipment and facilities, insurance policies or insures

with ones requiring less fixed expenditures. Variable cost items are decreased in quality also,

for example, by switching to cheaper raw material, less skilled hourly labor and less

expensive maintenance and repair supplies. For the cost iterations with above approaches it is

required to develop functional cost analysis models. These cost models must be complete and

must relate the cost drivers and cost modifiers with parameters related to geometry, process,

and quality. The existing models of cost estimation of cast products are presented as under

2.2 Casting cost estimation

The major cost elements of a casting cost such as material, labor, energy, tooling and

overheads have been identified by early researchers (Chronister, 1975; Jain, 1987; Kulkarni,

1988). The material cost includes metal cost (actual cost of metal and alloys), and indirect

material cost (dispensable mold material, fluxes, sleeves, filters, chills, etc.). Metal casting is

an energy intensive process requiring large amount of energy for different activities,

dominated by melting. The tooling cost covers the cost of pattern/die and core boxes. The

overheads include expenses for equipment usages, supervisory staff, inspection staff and

administrative staff. The other costs include transportation, taxes, and premium (such as for

special inspection and just in time delivery). The other elements that have a significant

impact on the casting cost are productivity, yield and defects. The productivity varies

depending on the equipment used. The yield of a foundry is defined as the percentage output

of castings per kg of input to the melting unit. On the other hand, casting yield gives an

indication of additional metal (for gating and feeding system) melted and poured for getting a

casting. The defect level in foundries may range from 2 to 20 percentage during regular

production.

Cost models have been proposed by identifying and calculating the detailed cost elements.

Ajmel developed a computer aided process planning and cost estimating system (Ajmel and

Dale, 1990). It has an interactive data base system in which data was fed by the user. The

system had different modules to estimate volume and weight, density and cost per unit

weight, labor time, labor and material cost. Similar cost model are also reported by Creese et

al., 1992; Creese and Rao, 1995. These systems are meant for cost estimation at the

manufacturing stage and it did not have any facility to perform „what if‟ analysis to study the

effect of change in design on cost. The DFMA (Design for Manufacture and Assembly)

software has a detailed casting cost estimation module aimed at product designers (Boothroyd

and Dewhurst Inc., 2003). It however, requires a considerable amount of interactive input

about the process, such as the time required for each activity and the corresponding labor rate.

It does not consider the effect of two key parameters that significantly affect casting cost:

internal quality requirement (which depends on the end application) and yield (which varies

with casting geometry, metal and process).

2.3 Tooling cost estimation

The cost of tooling (pattern, core box, mold, etc.) is amortized over the number of castings

produced, and can be a significant proportion of the casting cost, especially when the order

quantity is low. Considerable efforts have been made in tooling cost estimation for injection

moulding and pressure die casting (Lowe, et al. 1985; Chin, et al. 1996; Sundaram, et al.

1999; Smith, 1999; Duverlie, et al. 1999; Naganumiah and Ravi, 2005). Even though, sand

casting process produces 90% of total casting by weight as per 41st Census of casting

production (MCS, 2005), less work has been reported for tooling cost estimation for sand

casting process. A parametric equation for tooling cost, driven by volume, shape complexity

of part and accuracy alone has been developed employing regression analysis for sand cast

parts (Chougule and Ravi, 2006). Shape complexity has been considered in their equation

based on part geometry alone. In practice, tooling geometry is determined by combination of

part design, mould design and method design.

There appears need for developing a cost model that can evaluate tooling cost while

performing iterations with mould design, gating design and feeding design. Such a cost model

in conjunction with standard cost element can be utilized for early cost estimation of sand cast

products. In practice, many foundries and their customers still estimate cost based on

component weight, corrected for the expected level of production difficulties, scrap and yield.

The weight based method involves accounting all expenses (material, energy, labor, etc.) and

total weight of saleable castings produced, during a predetermined period. Based on this data,

the average rate of castings per kg is calculated, and is used for calculating the cost of new

castings based on their weight. The method works well in mass production foundries making

castings of similar characteristics, but is not suitable for job shop or batch type foundries that

have a wide range of products. Each foundry usually specializes in a particular process (such

as green sand casting, investment casting or gravity die casting), focusing on a narrow range

of metals (either ferrous or non-ferrous) and applications (in terms of size/weight and

geometric complexity). It may have a unique combination of equipment, automation level,

worker skill and past experience. The tooling (patterns, core boxes, molds) and methoding or

rigging (feeding and gating systems), which greatly affect casting quality and yield, are

designed in different ways based on knowledge gained from previous projects. These factors

lead to significant variations in manufacturing cost among different foundries. Ironically,

most foundries do not maintain detailed cost data, making it difficult to establish the

profitability of specific casting projects. This is becoming critical in the light of increasing

pressure from original equipment manufacturers to reduce casting prices on a continuous

basis.

3. TOOLING COST ESTIMATION

Mould design establishes the parting surface that in turn determines the mould segments.

Optimal mould design implies minimum mould division with minimum complexity and

maximum conformance resulting in greater economy due to reduced tooling cost and higher

yield. The mould segments can be one of the following types (1) Mould segments that

represent the external shape of the cast product (2) Mould segments that represent the internal

cavities or hollow portions or undercut features of cast product (cored features) (3) Mould

segments added due to methoding.

{Add figure for tooling design and explain the same}

Mould division determines the number of mould segments and their complexity. More

number of mould segments are not desirable as each mould segment require separate tooling

and with increasing number of mould segments, mould assembly requires more time also

possibilities of flash and mould segments‟ mismatch increases. The cavity generated by the

assemblage of these mould segments is the cast part. A more complex mould segment

requires more steps in producing the tooling as well as costly machining operations of surface

(freeform) machining of convex or concave pockets. A mould segment whose tooling requires

only plane surface machining and cylindrical surface machining results in better economy.

Thus more the complexity of mould segments higher will be tooling cost.

3.1 Tooling Element Cost

Each of the mould segments requires a corresponding tooling element. Total tooling cost is

the summation of individual tooling elements cost. Tooling element cost has two components,

material cost and manufacturing cost (machining cost). Material cost is dependent on order

quantity and accuracy. Total tooling manufacturing cost depends on number of tooling

elements and their volume as well as complexity and accuracy of individual tooling element

3.2 Estimation of manufacturing cost for a tooling element

Cost of a tooling element depends on volume, complexity, accuracy and material.

Tooling element manufacturing cost = f (volume, complexity, material) (1)

Complexity of a tooling element is evaluated by comparing its machining cost with respect to

simple shapes as cubes or spheres. Geometry that has higher variation in section thickness,

larger surface area, less volume as compared to the volume of bounding box, smaller

orthogonal surface area, larger free form surface area, results in higher machining cost. Also

tooling with convex shape will be more costly as compared to concave shape. Thus, cost of a

tooling element depends on volume, complexity, accuracy and material.

Complexity = f (Vr, tr,, Acurved, Aortho, Ncd , Ql) (2)

Vr Volume ratio = volume of bounding box / volume of part contained by the tooling

Tr Thickness ratio = Max. thickness / min. thickness

Acurved Curved SA ratio = total SA / Curved SA

Aortho Orthogonal SA ratio = total SA / Orthogonal SA

Ncd No of controlled dimensions and surfaces

Ql Accuracy required

Tooling element manufacturing cost

TEcost= W1 + W2Vr+W3tr+ W4Vcurved+ W5Aortho + W6Ncd + W7Ql (3)

The above eight interdependent parameters can be obtained from a CAD model of the tooling

element. The weights for the above can be determined by regression analysis.

Ctooling = 1/N. ( n

i miiTEi

n

iCV ..TE

costi ) (4)

Ctooling Cost of tooling

N Order Quantity

n Number of tooling elements

costiTE Tooling element cost

VTEi Volume of tooling element

i Density of tooling material

Cmi Cost of tooling material

3.3 Regression analysis for tooling cost estimation

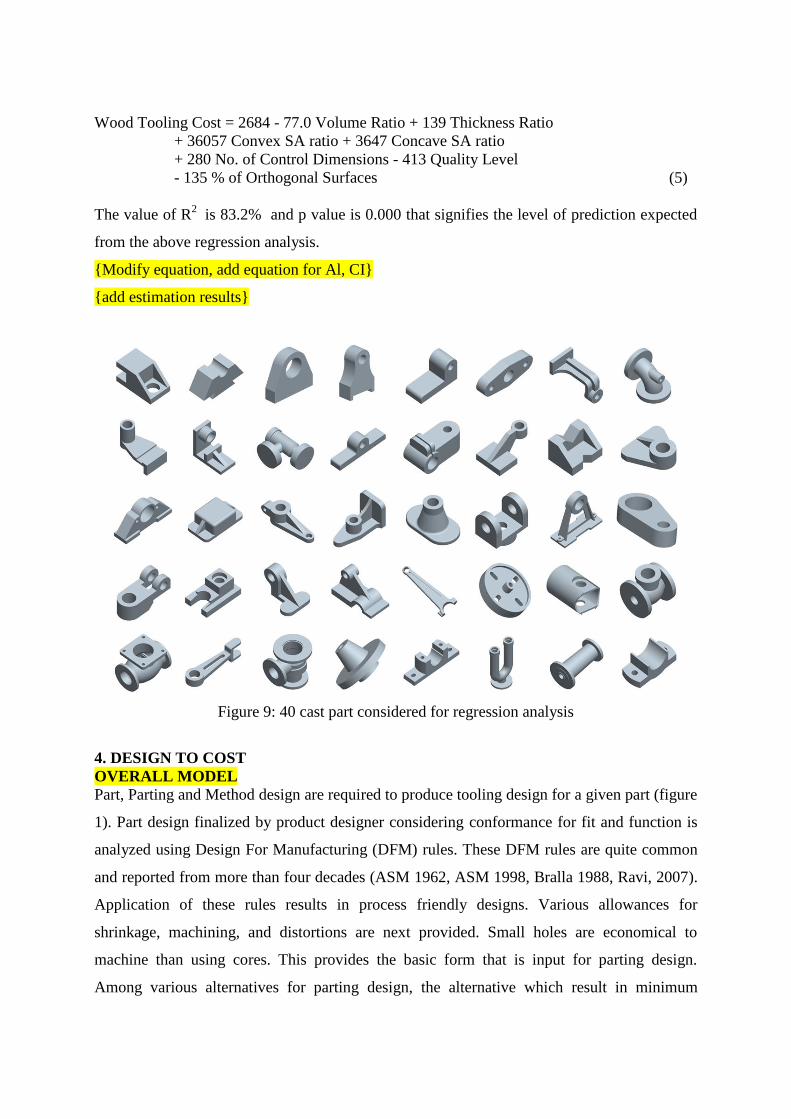

The above parameters are computed for 40 parts (figure 1) resulting in 102 tooling elements.

Seven parameters, Volume ratio, Thickness ratio, Curved SA ratio, Orthogonal SA, No of

control dimensions, and Quality level are compiled for these 102 tooling (Appendix I). Cost

data for manufacturing of wooden tooling is obtained by tooling experts. Regression is

performed using Mintab statistical analysis software. The regression equation obtained is as

follows.

Wood Tooling Cost = 2684 - 77.0 Volume Ratio + 139 Thickness Ratio

+ 36057 Convex SA ratio + 3647 Concave SA ratio

+ 280 No. of Control Dimensions - 413 Quality Level

- 135 % of Orthogonal Surfaces (5)

The value of R2

is 83.2% and p value is 0.000 that signifies the level of prediction expected

from the above regression analysis.

{Modify equation, add equation for Al, CI}

{add estimation results}

Figure 9: 40 cast part considered for regression analysis

4. DESIGN TO COST

OVERALL MODEL

Part, Parting and Method design are required to produce tooling design for a given part (figure

1). Part design finalized by product designer considering conformance for fit and function is

analyzed using Design For Manufacturing (DFM) rules. These DFM rules are quite common

and reported from more than four decades (ASM 1962, ASM 1998, Bralla 1988, Ravi, 2007).

Application of these rules results in process friendly designs. Various allowances for

shrinkage, machining, and distortions are next provided. Small holes are economical to

machine than using cores. This provides the basic form that is input for parting design.

Among various alternatives for parting design, the alternative which result in minimum

number and complexity of tooling elements as well as minimum draw distance is the optimal

one. Optimal feeding design ensures casting free from hot posts during solidification with

maximum feeder yield. Similarly optimal gating design ensures smooth, uniform and

complete filling while maximizing gating yield. Criteria for optimal part design, parting

design, feeding design and gating design have been reported by Ravi and Srinivasan (1995)

and Ravi et al (2007). Here we present in brief about mould design, feeding design and gating

design.

{Add new framework, discuss}

Figure 1: Methodology for tool design

3.1 Mould design

Optimal mould design implies the minimum number and complexity of mould elements to

create the casting cavity closest to the desired geometry.

Non planer parting surface, complex mould elements more number and volume of cored and

undercut features result in more costly tooling hence mouldability is directly associated with

tooling cost. A parting surface which results in more draw distance decreases the casting yield

(figure 2). Higher mouldability is necessary for better economy of cast product. Figure depicts

the various options of parting plane for a given cast geometry. Option „A‟ results in more

number of undercut / core features while option „C‟ results in less undercut volume with non

planer parting plane and increased draw distance. Option „B‟ can be considered best as it

results in flat parting plane, minimum undercuts, with minimum draw distance.

Figure 2: Part orientation effect on mould design

3.2 Gating design

Optimal gating design implies smooth, uniform and complete filling of mould cavity with

molten metal.

The flow of molten metal after being poured is a transient phenomenon accompanied by

turbulence, splashing, separation of streams near change of sections, branching off and

rejoining of streams, and the onset of solidification. Two major characteristics of flow in

casting is fluidity and turbulence. Lack of fluidity results in defects like misrun and cold shut

while higher turbulence results in gas and air entrapment as well as can cause slag and sand

inclusions.

3.3 Feeding design

Optimal feeding design implies every location inside a casting receives feed metal (from a

neighbouring location) to compensate for solidification shrinkage.

The temperature history of a location inside the casting with respect to the neighbouring

locations governs the formation of hot spots in casting. A hot spot in a casting will solidify

last and will eventually result in shrinkage cavity. This can be avoided by attaching a feeder

designed to solidify later than the hot spot. A modest 4% volumetric shrinkage in a Short

freezing range alloy can cause a cavity of size d/3 in a cube of size d in case of no feeders. It

is not only important to have feeders of necessary volume, it is equally important to locate

them so that they keep supplying liquid metal to last solidifying regions.

4. AUTOMATED PARTING AND METHOD DESIGN

CASE STUDY FOR PARTS FOR SIMULATION AND APPLYING TARGET

COSTING

BRACKET CASTING

PORWAL PART

The method design and casting simulation is carried out using AutoCAST (r) software

program (Ravi and Srinivasan, 1999). The main inputs include: part model, casting alloy, and

process. Method design involves three major tasks: (i) parting, mould and core design, (ii)

feeder and feedaid design, and (iii) gating system design. Process simulation includes mould

filling and casting solidification.

The parting line is generated to minimise undercuts and draw distance (Ravi and Srinivasan,

1990). The mould size is selected to provide sufficient gap around the casting cavity. Holes

are automatically recognised, and the corresponding cores (along with support) are designed

to minimise failure by distortion and other modes. Figure 3 shows a casting (valve body) and

its STL representation. The STL file is input to the AutoCAST software. The parting design

and core design are shown in figure 4.

Figure 3: Model of valve body and its STL representation

Figure 4: Parting design and core design

Feeder design mainly involves decisions regarding the number, location, shape and

dimensions of feeders and feed-aids. Automated feeder design uses geometric reasoning to

suggest the best location of feeder (closest to the hot spot, on a flat surface at the top or side,

preferably a thick section to facilitate fettling). Its dimensions are calculated based on

geometric modulus of the region surrounding the hot spot. Based on the dimensions, the

feeder model is created and attached to the casting through an appropriately sized neck. The

user may modify the dimensions of the feeder and model it again, and add more feeders, if

necessary. Feed-aids such as insulating and exothermic sleeves and covers, and chills are also

semi-automatically designed and modelled in a similar manner (figure 5).

Figure 5: Feeder design and cooling map

Casting solidification is simulated using the Vector Element Method, which traces the feed

metal paths in reverse to pinpoint the location of hot spots (Ravi, and Srinivasan, 1996) It is

based on the principle that the direction of the highest temperature gradient (feed metal path)

at any point inside the casting is given by the vector sum of individual thermal flux vectors in

all directions around the point. Multiple hot spots, if present, are detected by starting from

several directions. Ideal feeding implies that the feed paths connect and converge inside a

feeder.

Gating system design includes deciding the number and location of gates, and designing the

choke so that the mould fills in a predetermined range of time (Ravi, 1997). The gate

locations are suggested at thick sections along the parting line that have low free fall height

and fewer obstructions (such as cores blocking the path of metal emerging from an ingate).

The program determines ideal filling time (function of casting weight, section thickness and

fluidity), followed by choke velocity (based on metallostatic head), and choke area (using the

gating ratio). Other process parameters are determined by comparing with similar previous

projects (Chougule et al 2004).

The mould filling is simulated to determine the actual fill time and velocity of metal at

different locations (figure 3.6). It uses a layer-by-layer filling algorithm that considers the

instantaneous velocity of metal through the gates (which depends on the head), and the area of

casting cross-section being filled up. Part property, parting and core design, feeding design,

gating design, and pouring data are presented in table 1, table 2, table 3, table 4, and table 5

respectively.

Figure 6: Gating design and mould filling simulation

Table 1: Part Properties

Cast Metal Surface Area

(mm2)

Volume (mm3)

[Bounding box size] Weight (Kg)

Cast Iron 784639 1802656

[375*290*270] 12.7

Table 2: Parting and core design

No. of Cores Under Cut

Volume (mm3)

Mould Box Size Match Plate Size

1 8932799 600*450*400 800*600

Table 3: Feeding design No. of

Feeders

Feeder Size

L/D

Feeder Weight

(Kg)

Hot Spot in

Feeder

Feeder Yield

(%)

4 90/60 4 Yes 74.8

Table 4: Gating design

No. of

In-gates

Gating

Weight

(Kg)

Gating

Yield (%) Gating Ratio

Choke

Area

(mm2)

In-gate

Cross

Section

Runner

Cross

Section

Fill

time

(secs)

Max.

Velocity

(m/s)

1 1.8 87.8 1.00:1.42:1.29 85 20*13 15*19 21.3 21.3

Table 5: Pouring data

5. TOOLING DESIGN

Application of parting design and method design results in tooling design. For the valve body

part under consideration the tooling required would be (1) pattern for cope (2) pattern for

drag, and (3) core box for the hollow cavity. These are shown in figure 7 and 8.

Figure 7: Pattern for cope and drag for valve body

Figure 8: Lower core box for valve body.

Pouring Time

(sec.)

Pouring Rate

(Kg/sec.)

Pouring Temp.

(Cel.)

5.8 2.2 1324

7.0 CONCLUSION

Parting design and method design along with part design determine the tooling design. Parting

design determines the number of tooling elements and complexity of individual tooling.

Feeding design determines the feeder layout that adds to volume and complexity of the

tooling. Similarly gating design also contributes to the tool design. In this work optimal

tooling design methodology was discussed with an example. Seven parameters, volume ratio,

thickness ratio, convex SA ratio, concave SA ratio, orthogonal SA, no of control dimensions,

and quality level were complied for 102 tooling elements belonging to 40 cast parts. The

regression equation thus obtained can be used for estimation of tooling cost.

REFERENCES

ASM 1962, Casting Design Handbook, American Society of Metals

AutoCAST user guide, Advanced Reasoning Technologies, 2007

Bidanda B, Kadidal M, Billo R, “Development of an Intelligent Castability and Cost Estimation

System,” International Journal of Production Research, Vol. 36, No. 2, pp. 547–568, (1998).

Boothroyd and Dewhurst Inc., “Design for Manufacture Concurrent Costing Software – User

Manual, Boothroyd and Dewhurst Inc: RI, (2003).

Bralla J, “Handbook of Product Design for Manufacturing.” McGraw-Hill Book Company, New

York, (1988).

Chen Yuh-Min, and Liu Jang-Jong, “Cost effective design for injection molding,” Robotics and

Computer Integrated Manufacturing, Vol. 15, pp. 1-21, 1999.

Chin, K.S. and Wong, T.N., “Developing a knowledge based injection mold cost estimation

system by decision tables,” International Journal of Advanced Manufacturing Technology,

Vol. 11, No. 5, pp. 353-365, 1996.

Chougule, R.G. and Ravi, B., “Casting cost estimation in an integrated product and

process design environment”, International Journal of Computer Integrated

Manufacturing, Vol. 19, No. 7, pp.676-688, 2006.

Chougule R G, Jalan M K and Ravi B, Casting Knowledge Management for Concurrent Casting

Product Process Design, Transactions of the AFS, 112, 2004, pp 105-114.

Creese R, Rao A, “Scrap vs. Profitability,” Modern Casting, August 1995, pp. 38-41, (1995).

Creese R, Adithan M, Pabla B, “Estimating and Costing for the Metal Manufacturing Industry,”

Cost Engineering Series, Volume 18, Marcel Dekker Inc., pp. 1-5, (1992).

Duverlie, P.J. and Castelain, M., “Cost estimation during design step: parametric method versus

case based reasoning method,” International Journal of Advanced Manufacturing

Technology, Vol. 15, pp. 895-906, 1999.

Lowe, P.H. and Walshe, K.B.A., “Computer aided tool cost estimating: an evaluation of the

labor content of injection molds,” International Journal of Production Research, Vol. 23, No.

2, pp. 371-380, 1985.

Nagahanumaiah, Ravi, B., and Mukherjee, N.P., “Rapid tooling manufacturability evaluation

using Fuzzy-AHP methodology,” International Journal of Production Research, submitted in

May 2005

Sundaram, M. and Masleka,r D. “A regression model for mold cost estimation,” Proceedings of

8th Industrial Engineering Research Conference, Phoenix, Arizona, 1999

Ravi B, Intelligent Design of Gating Channels for Casting, Materials Science and

Technology, 13, No. 9, 1997, pp 785-790.

Ravi, B., 2007, Metal Casting-computer aided design and analysis, Prentice Hall India

Smith, C.S. “The Manufacturing Advisory Service: Web based process and material selection,”

Ph.D. Thesis, University of California, Berkeley, Spring 1999.

Ravi B, Creese, R C, and Ramesh, D, “Design for Casting - A New Paradigm for Preventing

Potential Problems”, AFS Transactions, vol. 107, p197-202, (1999)

Ravi, B, Srinivasan M. N., "Casting solidification analysis by modulus vector method", Int. J.

Cast Metals Res., vol. 9, p1-7 (1996)

Ravi, B, Srinivasan M. N., "Feature based Castability Evaluation", Int. J. Prodn. Res., vol. 22,

p3367-3380 (1995)

Ravi, B., Srinivasan, M. N., "Decision criteria for computer-aided parting surface design",

Computer Aided Design, vol. 22 No jan/feb, 1990, p11-1

ASM Metal Handbook Volume 15 Casting, American Society of Metals (1998)

B Ravi, Durgesh Joshi, Rahul Chougule, 2005, Survey of Computer Applications in Indian

Foundry Industry: Benefits and Concerns, proceedings of 53rd

Indian Foundry Congress,

Kolkata, January 2005

APPENDIX

Regression data

S.

No.

Volume

Ratio

Thickness

Ratio

Convex

SA

ratio

Concave

SA ratio

% of

Orthogonal

Surfaces

No. of

Control

Dimensions

Quality

Level

Wood

Tooling

Cost

(Rs)

1 6.266 4.000 0.075 0.000 37.13 7 2 747.16

2 6.277 4.000 0.074 0.000 37.44 6 2 747.16

3 1.186 6.000 0.000 0.110 21.36 3 2 347.95

4 1.213 5.000 0.000 0.119 21.29 2 1 140.28

5 10.004 1.000 0.099 0.000 43.33 12 3 2929.16

6 10.038 1.000 0.100 0.000 43.48 11 3 2929.16

7 1.763 6.000 0.000 0.194 19.20 2 3 313.97

8 1.122 2.750 0.000 0.116 20.95 2 3 330.97

9 6.646 1.000 0.075 0.000 38.20 8 3 1965.60

10 1.472 3.500 0.000 0.226 25.12 2 3 276.86

11 6.343 2.000 0.081 0.000 44.02 16 3 903.90

12 6.394 2.000 0.085 0.000 44.51 14 3 903.90

13 1.288 3.000 0.000 0.202 24.16 2 3 92.03

14 1.297 2.500 0.000 0.163 24.90 2 3 108.82

15 3.659 1.000 0.065 0.000 41.41 11 2 615.62

16 3.672 1.000 0.061 0.000 41.74 10 2 615.62

17 1.595 2.760 0.000 0.250 24.71 2 2 100.15

18 3.798 1.000 0.089 0.000 37.41 9 3 562.95

19 3.803 1.000 0.084 0.000 37.53 8 3 562.95

20 1.410 2.456 0.000 0.219 25.05 2 3 92.24

21 4.174 4.750 0.072 0.000 38.10 8 1 604.82

22 1.355 2.456 0.000 0.183 23.27 2 1 78.83

23 3.467 2.000 0.055 0.000 38.57 9 1 853.42

24 1.408 3.000 0.000 0.222 28.14 2 1 2469.19

25 6.863 3.000 0.152 0.000 32.69 10 1 4416.26

26 6.949 3.000 0.133 0.000 32.93 9 1 4416.26

27 5.025 3.800 0.060 0.007 40.19 7 1 2785.07

28 5.678 3.800 0.076 0.006 36.84 6 1 2812.60

29 1.301 2.600 0.000 0.187 24.85 2 1 78.70

30 5.341 1.000 0.090 0.000 40.88 4 1 809.53

31 1.563 4.933 0.000 0.224 19.18 3 2 397.95

32 9.041 1.000 0.078 0.000 33.70 12 2 1355.85

33 10.595 1.000 0.086 0.000 33.84 11 2 1355.85

34 1.214 2.750 0.000 0.145 23.62 5 2 1575.42

35 1.253 1.000 0.000 0.155 23.01 2 3 78.72

36 1.361 1.000 0.000 0.200 22.63 2 3 120.67

37 1.221 1.000 0.000 0.172 28.49 2 3 78.57

38 12.685 7.000 0.131 0.000 38.02 10 3 1333.48

39 9.266 1.500 0.070 0.002 40.68 11 2 2761.61

40 9.369 1.500 0.062 0.002 41.01 10 2 2761.61

41 7.598 2.500 0.068 0.002 41.71 19 1 2987.72

42 7.671 2.500 0.070 0.002 42.48 18 1 2987.72

43 1.413 2.600 0.000 0.177 21.63 2 1 138.32

44 1.453 2.700 0.000 0.223 24.51 2 1 92.80

45 8.295 12.000 0.083 0.001 38.68 19 2 6182.96

46 8.558 12.000 0.062 0.001 39.73 17 2 6182.96

45 1.639 2.980 0.000 0.185 20.89 2 2 275.60

48 7.476 2.000 0.057 0.000 41.90 9 2 1216.46

49 6.169 2.000 0.120 0.000 42.58 9 2 1216.46

50 8.267 2.610 0.000 0.208 23.42 2 2 85.53

51 5.797 4.000 0.055 0.000 38.99 9 2 2104.88

Regression data (continued)

S.

No.

Volume

Ratio

Thickness

Ratio

Convex

SA

ratio

Concave

SA

ratio

% of

Orthogonal

Surfaces

No. of

Control

Dimensions

Quality

Level

Wood

Tooling

Cost

(Rs)

52 6.488 4.000 0.051 0.000 42.05 8 2 2104.88

53 1.406 2.530 0.000 0.196 23.36 2 2 79.06

54 9.166 13.000 0.149 0.000 39.05 15 3 6584.76

55 9.513 13.000 0.150 0.000 39.72 14 3 6584.76

56 5.611 3.000 0.081 0.000 37.52 15 2 1755.03

57 1.298 7.200 0.000 0.135 19.91 3 2 139.55

58 1.520 2.970 0.000 0.185 20.59 2 2 92.62

59 11.387 5.000 0.056 0.000 42.67 10 2 470.31

60 8.477 5.000 0.090 0.000 37.49 10 2 1282.43

61 1.609 2.840 0.000 0.241 23.86 2 2 119.57

62 1.609 2.840 0.000 0.241 23.86 2 2 119.57

63 1.332 2.454 0.000 0.169 22.58 2 2 78.72

64 5.595 1.000 0.106 0.000 40.34 5 2 1709.18

65 1.726 5.042 0.000 0.239 24.33 2 2 275.42

66 5.470 3.000 0.058 0.000 41.61 9 2 1694.23

67 5.478 3.000 0.060 0.000 41.79 7 2 1694.23

68 1.472 2.646 0.000 0.208 23.20 2 2 105.41

69 6.242 7.200 0.070 0.000 39.20 10 2 2458.56

70 6.264 7.200 0.066 0.000 39.58 9 2 2133.56

71 1.364 2.380 0.000 0.209 25.23 2 2 79.01

72 1.453 3.500 0.000 0.198 22.69 2 2 205.12

73 6.306 2.000 0.042 0.000 43.05 18 1 2817.83

74 6.306 2.000 0.036 0.000 43.04 16 1 2817.83

75 1.802 2.800 0.000 0.224 27.05 2 1 112.06

76 1.374 2.800 0.000 0.170 28.24 2 1 66.51

77 1.374 2.800 0.000 0.170 28.24 2 1 66.51

78 6.995 8.000 0.140 0.000 29.70 11 1 6882.72

79 7.167 8.000 0.143 0.000 30.20 6 1 6882.72

80 6.590 2.063 0.068 0.000 38.24 16 2 1794.96

81 6.624 2.063 0.068 0.000 38.60 14 2 1794.96

82 1.505 3.400 0.000 0.236 24.87 2 2 92.86

83 1.505 3.400 0.000 0.236 24.87 2 2 92.86

84 6.207 1.814 0.120 0.000 31.15 16 2 6345.61

85 6.946 1.814 0.128 0.000 31.37 14 2 5565.61

86 6.785 4.286 0.154 0.000 27.17 17 1 10278.06

87 6.783 4.286 0.155 0.000 27.21 16 1 10278.06

88 6.982 4.600 0.152 0.000 28.42 19 2 11654.50

89 7.573 3.864 0.020 0.000 41.62 11 1 2753.01

90 6.036 3.864 0.110 0.000 41.30 8 1 3143.01

91 1.237 2.500 0.000 0.192 26.88 5 1 268.43

92 5.530 1.432 0.057 0.000 39.39 18 2 3854.18

93 5.545 1.432 0.056 0.000 39.57 17 2 3854.18

94 1.124 1.700 0.000 0.090 27.25 2 2 164.60

95 1.154 1.800 0.000 0.256 27.03 2 2 106.15

96 11.195 5.250 0.062 0.000 39.54 13 2 955.53

97 11.443 5.250 0.049 0.000 40.32 12 2 955.53

98 1.312 2.600 0.000 0.195 25.28 2 2 78.78

99 7.550 2.143 0.150 0.000 30.06 15 3 7869.16

100 7.615 2.143 0.149 0.000 30.31 14 3 7869.16

101 1.334 2.500 0.000 0.227 27.21 2 2 166.04

102 1.193 2.500 0.000 0.148 27.50 2 2 166.04

ALTERNATE REGRESSION ANALYSIS

S.

No.

Volume

Ratio

Thickness

Ratio

Conve

x SA

ratio

Concave

SA ratio

% of

Orthogona

l Surfaces

No. of

Control

Dims

Quality

Level

Wood

Pattern

Cost

(Rs)

1 6.266 4.000 0.075 0.000 37.130 7 2 747.156

2 6.277 4.000 0.074 0.000 37.440 6 2 747.156

3 1.186 6.000 0.000 0.110 21.360 3 2 347.945

4 1.213 5.000 0.000 0.119 21.290 2 1 140.279

5 10.004 1.000 0.099 0.000 43.330 12 3 2929.160

6 10.038 1.000 0.100 0.000 43.480 11 3 2929.160

7 1.763 6.000 0.000 0.194 19.200 2 3 313.967

8 1.122 2.750 0.000 0.116 20.950 2 3 330.972

9 6.646 1.000 0.075 0.000 38.200 8 3 1965.600

10 1.472 3.500 0.000 0.226 25.120 2 3 276.865

11 1.288 3.000 0.000 0.202 24.160 2 3 92.033

12 1.297 2.500 0.000 0.163 24.900 2 3 108.818

13 3.672 1.000 0.061 0.000 41.740 10 2 615.615

14 1.595 2.760 0.000 0.250 24.710 2 2 100.151

15 1.410 2.456 0.000 0.219 25.050 2 3 92.239

16 1.355 2.456 0.000 0.183 23.270 2 1 78.826

17 3.467 2.000 0.055 0.000 38.570 9 1 853.424

18 6.863 3.000 0.152 0.000 32.690 10 1 4416.263

19 6.949 3.000 0.133 0.000 32.930 9 1 4416.263

20 1.301 2.600 0.000 0.187 24.850 2 1 78.698

21 5.341 1.000 0.090 0.000 40.880 4 1 809.530

22 1.563 4.933 0.000 0.224 19.180 3 2 397.946

23 10.595 1.000 0.086 0.000 33.840 11 2 1355.855

24 1.214 2.750 0.000 0.145 23.620 5 2 1575.419

25 1.253 1.000 0.000 0.155 23.010 2 3 78.723

26 1.361 1.000 0.000 0.200 22.630 2 3 120.671

27 1.221 1.000 0.000 0.172 28.490 2 3 78.574

28 9.266 1.500 0.070 0.002 40.680 11 2 2761.614

29 7.598 2.500 0.068 0.002 41.710 19 1 2987.718

30 7.671 2.500 0.070 0.002 42.480 18 1 2987.718

31 1.413 2.600 0.000 0.177 21.630 2 1 138.320

32 1.453 2.700 0.000 0.223 24.510 2 1 92.799

33 1.639 2.980 0.000 0.185 20.890 2 2 275.603

34 7.476 2.000 0.057 0.000 41.900 9 2 1216.464

35 8.267 2.610 0.000 0.208 23.420 2 2 85.532

36 5.797 4.000 0.055 0.000 38.990 9 2 2104.879

37 1.406 2.530 0.000 0.196 23.360 2 2 79.057

38 1.298 7.200 0.000 0.135 19.910 3 2 139.545

39 1.520 2.970 0.000 0.185 20.590 2 2 92.619

40 11.387 5.000 0.056 0.000 42.670 10 2 470.308

41 1.609 2.840 0.000 0.241 23.860 2 2 119.570

42 1.609 2.840 0.000 0.241 23.860 2 2 119.570

43 1.332 2.454 0.000 0.169 22.580 2 2 78.723

44 5.595 1.000 0.106 0.000 40.340 5 2 1709.175

45 1.726 5.042 0.000 0.239 24.330 2 2 275.419

46 5.470 3.000 0.058 0.000 41.610 9 2 1694.228

47 5.478 3.000 0.060 0.000 41.790 7 2 1694.228

48 1.472 2.646 0.000 0.208 23.200 2 2 105.405

49 6.242 7.200 0.070 0.000 39.200 10 2 2458.560

50 6.264 7.200 0.066 0.000 39.580 9 2 2133.560

51 1.364 2.380 0.000 0.209 25.230 2 2 79.007

52 1.453 3.500 0.000 0.198 22.690 2 2 205.119

53 6.306 2.000 0.042 0.000 43.050 18 1 2817.830

54 1.802 2.800 0.000 0.224 27.050 2 1 112.059

55 1.374 2.800 0.000 0.170 28.240 2 1 66.510

56 1.374 2.800 0.000 0.170 28.240 2 1 66.510

57 6.995 8.000 0.140 0.000 29.700 11 1 6882.720

58 6.624 2.063 0.068 0.000 38.600 14 2 1794.957

59 1.505 3.400 0.000 0.236 24.870 2 2 92.857

60 1.505 3.400 0.000 0.236 24.870 2 2 92.857

61 6.207 1.814 0.120 0.000 31.150 16 2 6345.612

62 6.946 1.814 0.128 0.000 31.370 14 2 5565.612

63 6.036 3.864 0.110 0.000 41.300 8 1 3143.010

64 1.237 2.500 0.000 0.192 26.880 5 1 268.432

65 5.530 1.432 0.057 0.000 39.390 18 2 3854.175

66 5.545 1.432 0.056 0.000 39.570 17 2 3854.175

67 1.124 1.700 0.000 0.090 27.250 2 2 164.604

68 1.154 1.800 0.000 0.256 27.030 2 2 106.151

69 11.195 5.250 0.062 0.000 39.540 13 2 955.529

70 11.443 5.250 0.049 0.000 40.320 12 2 955.529

71 1.312 2.600 0.000 0.195 25.280 2 2 78.776

72 7.550 2.143 0.150 0.000 30.060 15 3 7869.160

73 1.334 2.500 0.000 0.227 27.210 2 2 166.038

74 1.193 2.500 0.000 0.148 27.500 2 2 166.038

Wood Cost = 463 - 155 Volume Ratio + 53.6 Thickness Ratio + 37484 convex ratio

+ 3920 concave ratio + 246 No. of Control Dimensions

- 76.6 % of Orthogonal Surfaces + 163 Quality Level

Rsq= 91.7 p=0.000

Part attributes as thickness ratio, area ratio, and volume ratio influence the shape complexity.

Mould design determines the number of tooling elements and their complexity, volume of

tooling elements, volume of undercut and cored features. Method design consists of gating

design and feeding design. Gating design should ensure complete, uniform, and smooth filling

of mould cavity. Feeding design should ensure absence of isolated hot spots in casting during

solidification and uniform cooling. Gating layout, channel shape and size, and other elements

of gating system influence the tooling cost. Similarly feeder layout, feeder size and shape,

provision of feed aids increase the tooling volume and its complexity.

Thus managing cost at the product development stage emerges as important process to

increase the profitability of future products.

Table 6: Parameters for tooling cost estimation for valve body part.

Tooling Ele. V Vb Tmax Tmin SA Aconvex Aconcave Aortho Ncd QL

Cope 8606152.2 54000000 120 28 1043024.7 153218 0 27.17 17 1

Drag 7955386 54000000 120 28 992354.53 153606 0 27.21 16 1

Core Up. 25135995 30000000 150 37.5 771374.15 0 119331 25.92 9 1

Core Lo. 25135995 30000000 150 37.5 771374.15 0 119331 25.92 9 1

(V: Volume, Vb: Volume of bounding box, Tmax: Maximum thickness; Tmin: Minimum

thickness, SA: Surface Area)

Cost Drivers / Cost modifiers

Part Design

Volume, Vpart Material cost, rmetal Surface area, SA Number of control dimension, Ncd Quality level, Ql Order quantity, n

Material Selection

Density, Specific heat, Cp Thermal conductivity, K Melting temp (range), Tm Latent heat, L

Process Design

Furnace efficiency, fefficiency Factor for metal loss, fmetal_loss Factor for mold material loss in process, fmold_mat_loss Factor for sand recycling, frecycle Factor for mould rejection, fmold_rej Factor for casting rejection, fcast_rej

Mould Design

Draft Volume, Vdraftvol Volume to be machined (Machining allowance), Vmachining Volume of small holes (require drilling), Vmach_holes Volume of moulding sand, Vmould_sand Volume of core sand, Vcore_sand Amount of mould additives (binders), B% Mould making cost, Mrate

Feeder Design Feeder Yield, Fyield Amount of feed aids, Nchills, Nex_sleeves, Nex_cover, Nins_sleeves, Nins_cover Feeder fettling cost, Ffettling

Gating Design Gating Yield, Gyield Gate fettling cost, Gfettling

Mould design, Feeder design and Gating design

Number of tooling, Nt Complexity of tooling elements (Vr, tr,, Acurved, Aortho, Ncd , Ql) Tooling material cost, rtool_metal

Total cost equation

The total cost of a cast product comprises of tooling cost per part, cost of metal, cost of

indirect material, cost of processing, cost of melting and cost of machining.

Ccasting = Ctooling +Cmetal + Cind_mat + Cprocess + Cmelting + Cmachining. (6.1)

Ctooling tooling cost per part

Cmetal metal cost per part

Cind_mat indirect material cost per part

Cprocess process cost per part

Cmelting secondary process cost per part

Cmachining machining cost per part

Cost of Metal

Cmetal = rmetal × ρmetal × Vcasting × fmetal_loss (6.5)

Vcasting = (Vpart + Vmachining + Vdraftvol) / Casting Yield (6.6)

Vmachining = Vmach_surface + Vmach_holes (6.7)

Vmach_surface = pmach_surface × Apart × amach (6.8)

rmetal cost rate of metal

ρmetal density of metal

Vcasting volume of as-cast part (without feeder, gating)

fmetal_loss factor for metal loss in casting process

Vpart volume of the machined part

Vmachining volume to be machined

Vdraftvol volume of drafts

Vmach_surface volume of surface machining (excluding holes)

Vmach_holes total volume of (uncored) holes to be machined

pmach_surface percentage of part surface to be machined (decimal)

Apart surface area of part

amach machining allowance

Cost of Indirect Metal

Cind_mat = Cmold_sand + Cmisc_mat (6.9)

Cmold_sand = rmold_sand × Wmold_sand × frecycle × fcast_rej × fmold_rej (6.10)

Wmold_sand = Vmold_sand ×ρmold × fmold_mat_loss (6.11)

Vmold_sand = Apart × wmold (6.12)

Cmisc_mat = Cmold_sand × fmisc_mat (6.13)

Cmold_sand cost of mold sand mix

Cmisc cost of miscellaneous items (cores, wax, filters, etc.)

rmold_sand cost rate of moulding sand mix

Wmold_sand weight of mold sand mix required per casting

frecycle factor for sand recycling

fcast_rej factor for casting rejection

fmold_rej factor for mold rejection

Vmold_sand volume of mold material

ρmold_sand density of mold material

fmold_mat_loss factor for mold material loss in process

Apart Surface area of part

wmold Average thickness of mold wall

Cmold_sand cost of mold sand mix

fmisc_mat factor for miscellaneous materials

Cost of Process

Cprocess = Cmolding +Cmelt_pour + Cfettling + Cother + Cenergy (6.14)

Cmolding = ( Vmold_sand / Rmolding ) × rlabor_mold × fcast_rej × fmold_rej × fshape (6.15)

Cmelt_pour = (( Vcasting ×ρmetal )/( Rmelt_pour ×Y )) × rlabor × fcast_rej (6.16)

Cfettling = ( Vcasting ×ρmetal ) / ( Rfettling ×Y )× rlabor ×fshape (6.17)

Cother = (Cmolding + Cmelt_pour + Cfettling) × fother_labor (6.18)

Cenergy = Cmelting + Cother_energy (6.19)

Cmelting = lossmetalrejcastefficiencyenergy fffEr __ (6.20)

E = ρmetal × (Vcasting / Y) × (L + (ssp ×Ttap)) (6.21)

Cother_energy = Cenergy × fother_energy (6.22)

Csec_process = Cheat_treat + Cinspection (6.23)

Cheat_treat = Vcasting × ρmetal ×rheat_treat (6.24)

Cinspection = Vcasting ×rinspection × fshape× fclass (6.25)

Cmolding processing cost to create mold (ready to pour)

Cmelt_pour processing cost for melting and pouring

Cfettling processing cost for cleaning and fettling

Cother processing cost for other tasks in casting

Cenergy energy cost in casting process

Vmold_sand volume of mold

Rmolding production rate of molding - casting volume basis

rlabor cost rate of labour

fcast_rej factor for casting rejection

fmold_rej factor for mold rejection

fshape part shape complexity

Vcasting volume of as-cast part (without feeder, gating)

ρmetal density of metal

Rmelt_pour production rate of melting and pouring

Y yield of casting (as-cast weight / poured weight)

rlabor cost rate of labour

fcast_rej factor for casting rejection

Vcasting volume of as-cast part (without feeder, gating)

ρmetal density of metal

Rfettling production rate of fettling

Y yield of casting (as-cast weight/ poured weight)

rlabor cost rate of labor

fshape part shape complexity

Cmolding processing cost to create mold (ready to pour)

Cmelt_pour processing cost for melting and pouring

Cfettling processing cost for fettling

fother_labor factor for labor required for other tasks in casting

Cmelting cost of melting the metal to tapping temperature

Cother_energy total cost of energy other than melting

renergy cost rate of energy

E energy required for melting

fefficiency factor for furnace efficiency

fcast_rej factor for casting rejection

fmetal_loss factor for metal loss in casting process

ρmetal density of metal

Vcasting volume of as-cast part (without feeder, gating)

Y yield of casting (as-cast weight/ poured weight)

L latent heat of fusion of metal

ssp specific heat of metal

Ttap tapping temperature of metal

Cenergy energy cost

fother_energy factor for energy other than melting

Cheat_treat cost of heat treating the casting

Cinspection cost of inspecting the casting

Vcasting volume of as-cast part

ρmetal density of metal

rheat_treat average cost of heat treating per unit volume

Vcasting volume of as-cast part

rinspection average cost of fettling per unit volume

fshape part shape factor

fclass casting class factor

Cost of machining processes

Cmachining = Cmach_surface + Cdraft_surface + Cmach_holes (6.26)

Cmach_surface =(Vmach_surface + Vdraft_surface) ×rmachining × fshape× faccuracy (6.27)

Cmach_holes = Vmach_holes ×rdrilling × fpart_shape× faccuracy (6.28)

Cmach_surface cost of machining surfaces (excluding holes)

Cmach_holes cost of drilling holes

Vmach_surface volume of surface machining including drafts (excluding holes)

Vdraft_surface volume of draft surface machining including drafts

rmachining average cost of machining per unit volume

fshape part shape factor

faccuracy accuracy factor: standard = 1.0, high = 1.5, very high = 2.0

Vmach_holes volume of holes to be drilled

rdrilling average cost of drilling per unit volume

fpart_shape part shape factor

faccuracy accuracy factor: standard = 1.0, high = 1.5, very high = 2.0