Embed Size (px)

Citation preview

Psychological Bulletin1993, Vol. 113, No. 3. 440-450 Copyright 1993 by the American Psychological Association, Inc.

0033-2909/93/S3.00

Motivational Factors in Decision Theories: The Role of Self-Protection

Richard P. Larrick

This article reviews the standard economic and cognitive models of decision making under risk anddescribes the psychological assumptions that underlie these models. It then reviews importantmotivational factors that are typically underemphasized by the standard theories, including themotivation to protect one's self-image from failure and regret. An integrated view of decisionmaking is offered on the basis of a more comprehensive set of psychological assumptions.

Why do people often prefer a bird in the hand to two in thebush? More generally, why do people often choose a certainoutcome to a risky outcome? Answering such questions is cen-tral to understanding how people make the decisions they faceeveryday. Should I continue work on an established line of re-search or branch offinto a new, unproven line that could yield amajor contribution to the field but might also yield nothing atall? Should I invest my year-end bonus in a certificate of deposit(CD) that is guaranteed to pay a return of 8%, or should I investit in a high-risk stock that might pay a much larger return butcould also pay no return at all? Finally, should I have dinnertonight at a restaurant I am always reasonably satisfied with, orshould I have dinner at a restaurant that has occasionally servedan outstanding meal but at other times has served a mediocremeal?

Decision theorists assume that people's preferences for safetyor risk depend on two factors: the value people ascribe to theoutcomes of different courses of action and the probability thateach of the outcomes will occur. This way of characterizing thedecision process focuses on two questions: (a) How do peopleplace a value on the outcomes of their decisions? and (b) Howdo people assess uncertainty and risk? Standard answers tothese questions have appealed to cognitive and psychophysicalfactors underlying decision processes. The three most impor-tant theories of choice in this tradition are cardinal utilitytheory (Bernoulli, 1738/1954), prospect theory (Kahneman &Tversky, 1979), and expected utility theory (von Neumann &Morgenstern, 1944). Although these theories make somewhatdifferent assumptions about the mechanisms that determinethe subjective representations of objective outcomes and proba-

bilities, they all emphasize that decisions are a function of theprobabilities and values of the outcomes of each alternative.

In this article, I argue that the traditional expectancy-valuetheories of choice either have ignored important psychologicalmechanisms that lead to risk preference or have postulated psy-chological mechanisms that incompletely or inadequately de-scribe many actual decisions. Many decisions can be under-stood in terms of a desire to avoid the unpleasant psychologicalconsequences that result from a decision that turns out poorly.Making a choice can be threatening to the self because a pooroutcome can undermine one's sense of competence as a deci-sion maker. This view yields predictions and results differentfrom the traditional expectancy-value models of choice. By ig-noring the eifect that making a choice has on the self-esteem ofthe decision maker, the traditional view has overlooked impor-tant psychological processes underlying choice.

I begin by reviewing the expectancy-value perspective ofchoice as presented in cardinal utility theory, prospect theory,and expected utility theory. I go on to discuss a contrastingperspective that incorporates motivational and affective factorsinto standard expectancy-value choice models. These theoriesinclude such factors as fear of failure and regret. The assump-tion these theories make is that people are concerned with howthe outcome of a decision is going to make them feel about thedecision itself. A comprehensive model of decision making ispresented that describes how people defend themselves againstadverse psychological consequences. Implications for otheraspects of the decision-making process are discussed.

Explanations of Risk Preference

People tend to avoid taking risks. They buy countless variet-ies of insurance to avoid the risk of large but improbable losses.They invest in savings accounts, CDs, and money market fundsin order to avoid the risk of volatile returns from stocks and

This article was written in preparation for the doctoral dissertationat the University of Michigan. I wish to thank Richard E. Nisbett,Claude M. Steele, J. Frank Yates, and three anonymous reviewers for

many stimulating discussions.The research reported in this article was supported by a National

Science Foundation (NSF) graduate fellowship to Richard P. Larrickand in part by NSF Grant No. DBS-9121346 to Richard E. Nisbett.

Correspondence concerning this article should be addressed toRichard P. Larrick, Organization Behavior Department, Kellogg Grad-uate School of Management, Northwestern University, 2001 SheridanRoad, Evanston, Illinois 60208-2011, or beginning fall 1993, Psychol-ogy Department, Rutgers—The State University, New Brunswick, NewJersey 08903.

of action thaT have the same or higher expected value. Thisphenomenon is known in the decision-making literature as riskaversion. It has been demonstrated empirically many times(Mosteller & Nogee, 1951; Schoemaker, 1980). For example,Kahneman and Tversky (1979) asked subjects to choose be-tween (a) winning $3,000 for certain (80%) and (b) winning$4,000 with an 80% probability (20%). Kahneman and Tverskyfound that the majority of the subjects preferred the certaingain to the chance of winning a larger gain. (In the original

440

SELF-PROTECTION IN DECISIONS 441

study, these questions were posed to Israeli subjects and denomi-nated in Israeli pounds. At the time of the study, winning 3,000Israeli pounds was equal to winning a family's monthly in-come.)

Although risk aversion has commonly been assumed to holdfor all decisions (Arrow, 1971), many exceptions have been docu-mented. For example, there is consistent evidence that peopleprefer to take risks when making a choice between a certain lossand a risky loss (Fishburn & Kochenberger, 1979; Hershey &Schoemaker, 1980; Kahneman & Tversky, 1979). For example,Kahneman and Tversky asked subjects to choose between (a)losing $3,000 for certain (8%) and (b) losing $4,000 with an 80%probability (92%). In this case, most people preferred the riskyalternative. The tendency to favor a gamble that has the same orlower expected value than a certain outcome is known in thedecision-making literature as risk seekingness or risk proneness.

I am restricting my examination of risk preference to choicesamong alternatives that yield a single, nonzero outcome withsome probability greater than 0 (up to 1.0) and that otherwiseyield nothing. A risk-averse alternative is defined as a lotterywith a higher probability of success than another alternative ofthe same or higher expected value; a risk-seeking alternative isdefined as a lottery with a lower probability of success. Thisconception of risk is consistent with standard definitions of riskaversion and risk seeking (Keeney & Raiffa, 1976), althoughthere are many other conceptions of risk that would lead todifferent ways of categorizing given alternatives (Yates, 1990;Yates & Stone, 1992). The examination of risk preference is alsorestricted to choices between alternatives for which the likeli-hoods of outcomes are objectively known. Although this as-sumption fails to hold in many actual decision situations, it is astandard starting point for most theories of decision making.

What leads people to be risk seeking or risk averse? The expla-nations offered tend to fall into two categories: universal expla-nations and individual-difference explanations (cf. Lopes,1987). Universal explanations posit that there are basic psycho-logical mechanisms that are true of all people. They also pro-pose that the nature of physical enjoyment and of cognitivejudgment are similar for all people. Two of the most prominentuniversal theories are cardinal utility theory and prospecttheory. Individual-difference explanations, however, offer nogeneral explanations for risk preference. These theories assumethat risk preference is a function of individual differences inattitudes and motivation. The most prominent individual-dif-ference theories are expected utility theory, Atkinson's (1957)theory of achievement motivation, and Lopes's (1987;Schneider & Lopes, 1986) theory of security motivation. In thenext section, I review the universal explanations of risk prefer-ence.

Universal Theories

Cardinal Utility Theory

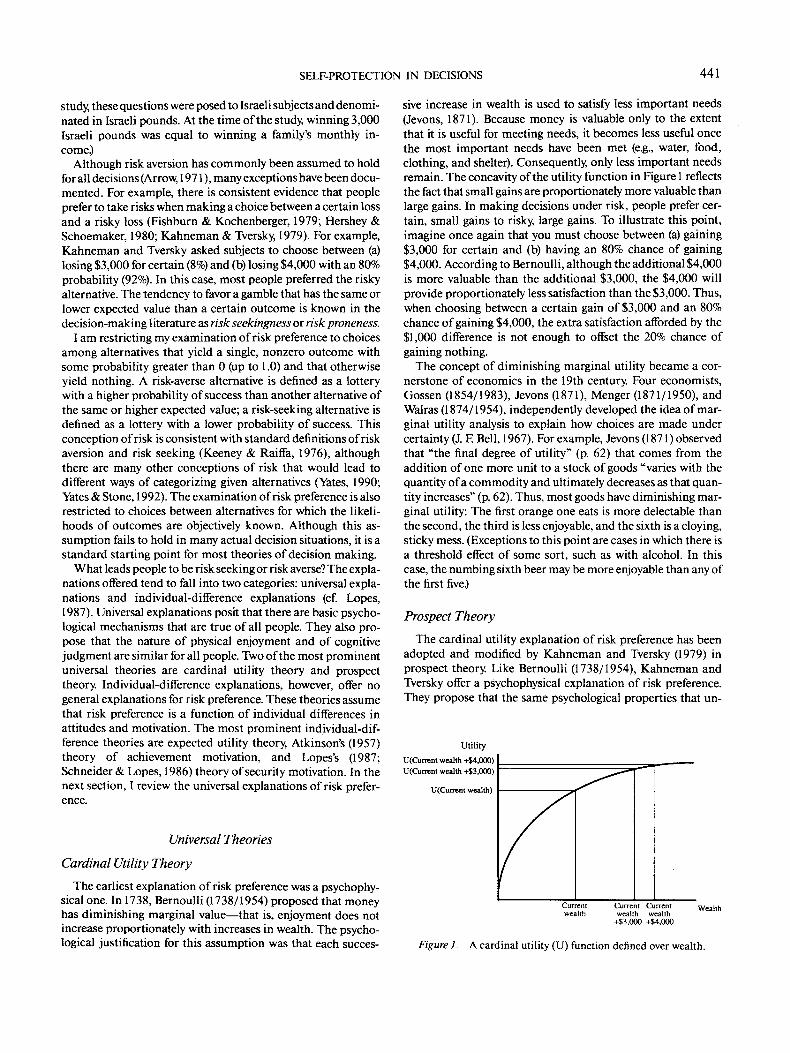

The earliest explanation of risk preference was a psychophy-sical one. In 1738, Bernoulli (1738/1954) proposed that moneyhas diminishing marginal value—that is, enjoyment does notincrease proportionately with increases in wealth. The psycho-logical justification for this assumption was that each succes-

sive increase in wealth is used to satisfy less important needs(Jevons, 1871). Because money is valuable only to the extentthat it is useful for meeting needs, it becomes less useful oncethe most important needs have been met (e.g., water, food,clothing, and shelter). Consequently, only less important needsremain. The concavity of the utility function in Figure 1 reflectsthe fact that small gains are proportionately more valuable thanlarge gains. In making decisions under risk, people prefer cer-tain, small gains to risky, large gains. To illustrate this point,imagine once again that you must choose between (a) gaining$3,000 for certain and (b) having an 80% chance of gaining$4,000. According to Bernoulli, although the additional $4,000is more valuable than the additional $3,000, the $4,000 willprovide proportionately less satisfaction than the $3,000. Thus,when choosing between a certain gain of $3,000 and an 80%chance of gaining $4,000, the extra satisfaction afforded by the$1,000 difference is not enough to offset the 20% chance ofgaining nothing.

The concept of diminishing marginal utility became a cor-nerstone of economics in the 19th century. Four economists,Gossen (1854/1983), Jevons (1871), Menger (1871/1950), andWalras (1874/1954), independently developed the idea of mar-ginal utility analysis to explain how choices are made undercertainty (J. F. Bell, 1967). For example, Jevons (1871) observedthat "the final degree of utility" (p. 62) that comes from theaddition of one more unit to a stock of goods "varies with thequantity of a commodity and ultimately decreases as that quan-tity increases" (p. 62). Thus, most goods have diminishing mar-ginal utility: The first orange one eats is more delectable thanthe second, the third is less enjoyable, and the sixth is a cloying,sticky mess. (Exceptions to this point are cases in which there isa threshold effect of some sort, such as with alcohol. In thiscase, the numbing sixth beer may be more enjoyable than any ofthe first five.)

Prospect Theory

The cardinal utility explanation of risk preference has beenadopted and modified by Kahneman and Tversky (1979) inprospect theory. Like Bernoulli (1738/1954), Kahneman andTversky offer a psychophysical explanation of risk preference.They propose that the same psychological properties that un-

Utility

U(Current wealth +$4,000)

U(Current wealth +$3,000)

U(Current wealth)

Currentwealth

Current Currentwealth wealth+$3,000 +$4,000

Figure 1. A cardinal utility (U) function denned over wealth.

442 RICHARD P. LARRICK

derlie the perception of physical stimuli also underlie the evalu-ation of monetary outcomes. The particular perceptual proper-ties they identify are (a) subjective experience is a concave func-tion of the magnitude of physical change, which is the sameassumption made by cardinal utility theory, and (b) the percep-tual system is sensitive to changes in stimulus level rather thanto absolute magnitudes. The second assumption implies thatdecision outcomes are evaluated in terms of changes from areference point, which is usually a person's current state ofwealth. As a result, diminishing marginal value applies to gainsand to losses rather than to overall wealth. So, just as large gainsdo not add much more to overall enjoyment than do smallgains, large losses do not subtract much more from overall en-joyment than do small losses. The difference in how gains andlosses are valued is captured in prospect theory's S-shapedvalue function depicted in Figure 2. As a result of these differ-ences between gains and losses, prospect theory makes thesame prediction as does cardinal utility theory in choices thatinvolve gains (i.e., people will be risk averse) but predicts thatpeople will be risk seeking in choices that involve losses. Forexample, in the choice between (a) a certain $3,000 loss and (b)an 80% chance of losing $4,000, the value function implies thata $4,000 loss is not much more painful than a $3,000 loss.Therefore, people prefer to take their chances on the $4,000loss rather than settle for a certain $3,000 loss. This change inpreferences from risk aversion in gains to risk seeking in lossesis called the reflection effect (Kahneman & Tversky, 1979).

At the heart of both cardinal utility theory and prospecttheory lies the same psychophysical explanation for risk prefer-ence: The psychological intensity of an outcome diminisheswith its magnitude. The similarity between the two theories isreadily apparent in the functions they propose. The only differ-ence is that prospect theory assumes decisions are based onchanges in wealth rather than on final states of wealth.

Note that the psychophysical explanation for risk preferenceactually has nothing to do with risk. For both the cardinal util-ity function and the prospect theory value function, risk prefer-ence is just a by-product of how people value relative outcomes.However, it seems obvious that people's preferences may de-pend not only on how they value objective outcomes but also onhow they feel about risk. Cardinal utility theory is completelydeficient in this regard. It does not discuss perceptions of orreactions to risk. Prospect theory, on the other hand, does con-sider how people's perceptions of risk affect their choices. Ac-cording to prospect theory, people give disproportionatelygreater weight to certain outcomes than to uncertain outcomes.The explanation for this phenomenon is once again an analogyto perception: There is a category break between certainty andprobabilities that are less than certain. Psychologically, there isa large difference between a probability of 1.00 and a probabil-ity of .99. The result is that the overweighting of certainty rein-forces the risk preferences produced by the value function: Cer-tain gains become even more desirable, and certain losses be-come even more aversive.

The strength of the universal theories is that they are elegant.They propose that a single, hardwired mechanism guides thedecisions of all people. In this respect, however, the approachmay be too general and too basic. The psychophysical approachto decision making fails to capture some of the more human

"Pleasure"

v(+$4,000)v(+$3,000)

-$4,000 -$3,000Losses

Changein Wealth

$3,000+$4,000 Gains

v(-$3,000)v(-$4,000)"Pain"

Figure 2. Prospect theory's value (V) function denned over changesin wealth from a reference point.

aspects of decision making. In fact, it appears to describe thebehavior not just of humans but of nonhumans as well. Forexample, prospect theory has been translated into reinforce-ment theory terms and applied to research on animal learning(Rachlin, 1989; Rachlin, Logue, Gibbon, & Frankel, 1986). Inaddition, empirical tests of prospect theory have yielded mixedsupport for the reflection effect prediction. The results havebeen particularly weak when risk preference for gains andlosses was examined within the same individual (Hershey &Schoemaker, 1980; Schneider & Lopes, 1986). This suggeststhat other factors that affect decisions are not included in theprospect theory account.

Overall, there are two major shortcomings to the psychophy-sical approach to explaining risk preference. First, it does notconsider the possibility that people might have affective re-sponses to risk itself. Second, it assumes that basic psychologi-cal mechanisms governing judgments of risk and value arecommon to all humans. Although Kahneman and Tversky(1982) mention that "individuals differ in their attitudes towardrisk and toward money" (p. 164), the psychophysical theoriesdo not predict any differences between people or describe psy-chological mechanisms that would produce such differences.1

1 An individual-difference interpretation of prospect theory hasbeen suggested and investigated by several researchers (Cohen, Jaffray,& Said, 1985, 1987; Fishburn & Kochenberger, 1979; Schneider &Lopes, 1986). These researchers examined whether a subset of subjectshas a tendency to feel disproportionately more pleasure or pain withlarge changes from their reference. This tendency preserves the twokey features of the psychophysical explanation: (a) people make judg-ments on the basis of reference points and (b) people's response tochanges are consistent, either showing diminishing marginal value, asproposed by prospect theory, or increasing marginal value. If a subsetof subjects showed increasing marginal value, this would be mani-

SELF-PROTECTION IN DECISIONS 443

Individual-Difference Theories

Individual-difference theories of risk preference are funda-mentally different from the universal theories. The individual-difference theories are more comprehensive: They propose thatrisk preference is a function of characteristics of the individual.In a recent review of the individual-difference approach to risktaking, Bromiley and Curley (1992) concluded that, in general,the work on individual differences has been long on uninte-grated descriptions of demographic and personality correlatesof risk taking but short on theoretical explanations. However,in the field of decision making, there are three important the-ories that do provide a framework for understanding individualdifferences in risk preference. Of these, the most prominenttheory is expected utility theory, which explicitly describes pro-cedures for assessing individual differences in feelings aboutrisk. The other two theories, Atkinson's (1957) theory ofachievement motivation and Lopes's (1987; Schneider & Lopes,1986) theory of security motivation, examine how people's mo-tivational needs determine their preferences for risk.

Expected Utility Theory

Expected utility theory does not make any assumptionsabout the psychological origins or experience of utilities.Rather, its goal is purely descriptive. It seeks to summarize indi-viduals' preferences for outcomes, to check for inconsistencies,and to predict future choices. As long as people's choices areconsistent, a utility function can be derived that can captureany type of risk preference: risk averse, risk seeking, risk neu-tral, or any combination of these. For example, to account forthe possibility that a person might buy insurance (a risk-averseact) and play the lottery (a risk-seeking act), Friedman and Sa-vage (1948) demonstrated that a utility function defined overwealth could be constructed that contained both risk-averseand risk-seeking segments. Other modifications of expectedutility theory have abandoned the assumption that utility isdefined over wealth and have incorporated the prospect theoryassumption that utility is defined over changes in wealth.

The psychological factors producing curves of various shapesare not considered explicitly in the theory. However, two factorshave been discussed in the decision literature as producing riskpreference: (a) the value of the outcomes under certainty, whichis identical to the cardinal conception of utility previously dis-cussed, and (b) the attitude the person has about risk. Thus, thereason a person is risk averse is ambiguous. It is not possible totell whether the person actually derives less value from addi-tional units of money, as the 19th-century economists assumed,or whether the person simply dislikes risk. The expected utilityfunction contains both elements (for an overview, see Schoe-maker, 1982).

Tested as risk seeking in gains and risk aversion in losses. Several stud-ies have found that this pattern is extremely rare (Hershey & Schoe-maker, 1980; Schneider & Lopes, 1986), and two studies by Cohen,Jaffray, and Said (1985, 1987) have found that there is no systematicrelationship between preferences in gains and preferences in losses.These results indicate that there is no empirical support for the individ-ual-difference interpretation of the psychophysical approach.

To grapple with this problem, a number of techniques havebeen developed to separate the value of money from feelingsabout risk. These factors can be unconfounded by first having aperson assess the values of outcomes under certainty, whichyields a measure equivalent to a cardinal utility function. Thenthe same person can make a series of choices under uncertainty,which is used to derive an expected utility function. The per-son's risk attitude can be measured by examining the differencebetween the cardinal utility function and the expected utilityfunction, thereby isolating that component of risk preferencethat is due to like or dislike for risk rather than to diminishingmarginal value (Barren, von Winterfeldt, & Fischer, 1984; D. E.Bell & Raiffa, 1988; Dyer & Sarin, 1979, 1982; Keeney &Raiffa, 1976; Pratt, 1964; see Briys, Eeckhoudt, & Louberge,1989, for a discussion of measuring risk preference when risk ispartially under the control of the decision maker). Althoughthere are some theoretical and practical limitations of this ap-proach (Bromiley & Curley, 1992), it is a step toward a morecomprehensive theory.

Expected utility theory has proven problematic as a descrip-tive theory of choice, and many empirical violations have beendocumented (Ellsberg, 1961; Slovic & Lichtenstein, 1968,1983;Tversky & Kahneman, 1986); nonetheless, expected utilitytheory and its modifications offer two improvements over theuniversal theories from a heuristic viewpoint. First, it recog-nizes that people may hold attitudes about risk per se. Second, itrecognizes that there are individual differences in preferencesabout risk. Expected utility theory's weakness, however, is thatit is short on psychological explanations for why people wouldhold specific attitudes about risk or why there would be differ-ences between people. The model treats risk preference as justanother preference: It is a given, and its psychological origin isunquestioned. This is similar to the way risk preference istreated when it is measured as a personality trait, such as sensa-tion seeking (Zuckerman, 1979). Such scales in and of them-selves are simply a description of risk preference rather than anexplanation. Clearly, the intent behind the development ofthese measures is to relate them to explanatory variables. Forexample, Zuckerman, Simons, and Como (1988) have providedresearch showing that there is a biological basis for sensationseeking (cited in Bromiley & Curley, 1992). Additional insightsconcerning the reaction to risk are provided by the motiva-tional theories of Atkinson (1957) and Lopes (1987).

Motivational Theories

Although expected utility theory allows for individual differ-ences in attitudes about risk, it does not describe any sort ofpsychological mechanism that underlies risk attitudes. Severalother individual-difference theories have, however, attemptedto fill in the psychological gaps left by expected utility theory(Atkinson, 1957,1983; Atkinson & Raynor, 1978; Lopes, 1987;Schneider & Lopes, 1986). These theories focus on how motiva-tion influences people's attitudes about risk. They propose thatpeople do not simply respond to the enjoyment that outcomesprovide, as the psychophysical theories suggest, nor do theysimply have a set attitude about risk. Rather, people respond tothe emotional consequences of making a decision that comefrom self-awareness and a sense of agency: feelings of success

444 RICHARD P. LARRICK

and failure, elation and disappointment, efficacy and impo-tence, rejoicing and regret. The motivational theories proposethat the choices people make are often the result of a compro-mise between two competing desires. On the one hand, peoplewant to choose the option that maximizes their outcomes (interms of the value of the outcome); on the other hand, theywant to avoid making poor decisions that may engender feel-ings of failure or disappointment. The tension between thesetwo motives pushes decision makers toward a specific level ofrisk-seeking behavior.

The most prominent of these motivational theories is Atkin-son's (1957,1983; Atkinson & Raynor, 1978) theory of risk tak-ing. Drawing on work from both social psychology (Lewin,Dembo, Festinger, & Sears, 1944) and personality psychology(McClelland, 1951), Atkinson proposed a model of risk takingbased on individual differences in motivation. The social psy-chological component of the model describes what amount ofrisk provides people with the greatest sense of achievement. InAtkinson's model, people are assumed to undertake actionsthat maximize feelings of achievement, which increase with thedifficulty of the task. When the probability of success is high, itprovides very little personal satisfaction when it occurs—it'slike shooting fish in a barrel. When the probability of success islow, people feel a great deal of satisfaction from having the skillto overcome the odds and achieve success. These intuitionssuggest that satisfaction with achieving success is negativelyrelated to the probability of success (1.00 — p). Of course, peopleare not likely to succeed at the very hardest tasks. Therefore, todetermine the level of risk that has the highest expected value,satisfaction must be weighed against the probability of success.The task that provides the optimal level of risk is the one thatmaximizes expected satisfaction, p(l -00 - p), which reaches amaximum value when the probability of success is .50. Themodel predicts that people will prefer to engage in tasks atwhich they expect to succeed half the time.

People differ, however, in the extent to which they are moti-vated to achieve, and some people are actually far more con-cerned with avoiding failure than with achieving success(McClelland, 1951). Atkinson (1957) proposed that peoplewith a high need for achievement will choose a task that is likelyto maximize their sense of achievement, which occurs when theprobability of success is equal to .50. People with a high need toavoid failure will choose a task that is likely to minimize theirsense of failure. The pain of a failure is directly proportional tohow easy a task is: It is not humiliating to shoot for the moonand miss, but it is embarrassing, as the saying goes, to shoot anarrow into the sky and miss. Thus, people who want to avoid asense of failure can do so by choosing tasks at which they arecertain to avoid failure (p = 1.00) or tasks at which the pain offailure is minimal (p = .00).

The strength of Atkinson's (1957,1983; Atkinson & Raynor,1978) theory is that it recognizes that individuals may differ inrisk preference because of psychological mechanisms related tomotivation. It also recognizes that there are emotional conse-quences of making a decision: People enjoy achieving theirgoals and dislike failing to achieve their goals, and they takethese considerations into account when they make a decision.There are serious limitations, however, to using this theory as ageneral theory of risk preference. The main drawback is that

the model is designed to explain decisions about skilled tasksand not about chance events. Although decades of researchhave supported Atkinson's basic model, there is mixed evidenceabout how well it predicts decisions made when outcomes arerandomly determined, such as in gambling experiments (Ko-gan & Wallach, 1964; Littig, 1966). (This raises an interestingquestion: How do people react to risk that arises from variabil-ity in their own performance rather than from variability in theenvironment [Heath & Tversky, 1991 ]? Unfortunately, this topichas not received much attention in most decision-making the-ories.)

A second motivational theory of risky decision making hasbeen proposed by Lopes (1987; Schneider & Lopes, 1986),which also contains a situational component (level of aspira-tion) and a personality component (need for security). The situa-tional factor in Lopes's two-factor theory of risk preference,level of aspiration, is defined as the size of outcome for which aperson is striving. The specific outcome to which a personaspires depends on both internal standards (e.g., a fairly stableestimate of what constitutes a valuable outcome) and the con-text of the choice (e.g., the distribution and size of the outcomesof the other alternative). The personality factor, need for secu-rity, is measured by assessing risk aversion or risk seekingness ina series of choices that pit a safe option against a risky optionwith the same expected value. According to Lopes's model,people who favor the sure thing are motivated to seek security—they are assumed to focus on the worst outcomes that can occurfor each alternative. On the other hand, people who favor therisky outcome are motivated to seek potential—they are as-sumed to focus on the best outcomes that can occur for eachalternative. People's preferences are assumed to be a multiplica-tive function of their need for security and their aspiration level.

Schneider and Lopes (1986) have shown that need for secu-rity is related to preferences over a range of gambles that differin variance and skewness of outcomes. For example, a gamblethat has a distribution of outcomes skewed toward zero but atop payoff of $439 has a low probability of meeting eithergroup's level of aspiration; however, its great potential is entic-ing to risk seekers and its poor security is aversive to riskavoiders. As predicted, this long shot was much more likely tobe favored by risk seekers than by risk avoiders. The specificpreferences of risk seekers and risk avoiders over a range ofgambles is predicted quite accurately by Lopes's (1987;Schneider & Lopes, 1986) two-factor theory.

Despite its descriptive strength, Lopes's (1987; Schneider &Lopes, 1986) theory is not a very comprehensive motivationaltheory of decision making because of its narrow personalitymechanism. In fact, it seems tautological to select people whoare risk averse and risk seeking to predict risk preference. Thetheory avoids tautology, however, because, unlike expected util-ity theory, risk aversion and risk seeking are used as a proxy for amechanism that Lopes claimed actually mediates risk prefer-ence—whether people focus on the best or worst outcomeswhen making a decision. Lopes provided evidence for thisclaim, both indirectly, in the pattern of observed choices, anddirectly, in the protocols people provide when they make deci-sions (although these were not actually subjected to analysis).Although she offers interesting suggestions about the source ofhopes and fears in everyday life, Lopes focused on a rather

SELF-PROTECTION IN DECISIONS 445

narrow individual difference. Atkinson's (1957,1983; Atkinson& Raynor, 1978) model, on the other hand, posits a slightlymore general personality mechanism—need for achievementand avoidance of failure—but it is still fairly specific to the taskof decision making. A question addressed in this article iswhether people's preferences are affected by a more generalneed for self-protection that could motivate behavior in a num-ber of domains.

All told, the motivational approach to decision makingmakes a valuable contribution to ideas about risk taking. Itintroduces both extradecisional factors, such as satisfactionwith success and fear of failure, and individual differences inmotivation, such as need for security and avoidance of failure.The motivational approach assumes that people are not justconcerned with the objective consequences of decisions butalso with the affective consequences of decisions and the moti-vational states that ameliorate or intensify them.

Regret Theory

Avoiding regret in risky decisions. The importance of affectin decision making has been the focus of several theories ofanticipated regret proposed by D. E. Bell (1982,1983), Loomesand Sugden (1982, 1987a), and Josephs, Larrick, Steele, andNisbett (1992). These theories represent a blending of the indi-vidual-difference approaches to decision making: They incor-porate affective and motivational elements into an expectedutility framework. Regret theory proposes that people do notsimply combine probabilities and outcomes to arrive at an over-all value for an alternative, as both cardinal utility theory andprospect theory assume. Instead, once the outcomes of a deci-sion are known, people compare the outcome of the alternativethey chose with the outcome that "might have been" if they hadchosen another alternative. This comparison will lead to eitherfeelings of regret—if the other alternative would have turnedout better—or rejoicing—if the other alternative would haveturned out worse (for a discussion of factors that give rise toregret, see Kahneman & Miller, 1986, and Landman, 1987).Because people know that they experience these feelings follow-ing a decision, they take these feelings into account before theymake a decision and calculate for each alternative how muchregret and rejoicing they are likely to feel once the outcomes areknown. For example, consider the choice between (a) a 100%chance of winning $8 and (b) a 67% chance of winning $12.Imagine that you choose Option B and lose. How much regretwould you feel? On the other hand, how content would you feelif you choose Option B and won? Loomes and Sugden (1982)proposed that the amount of regret people feel depends on howthe outcome they end up with compares to the outcome theywould have had if they had made a different choice.

The key assumption underlying the theory is that larger dif-ferences between outcomes produce disproportionately moreregret than do smaller differences, as shown in Figure 3.2 Apply-ing the regret function to the previous example, the regret pro-duced by choosing Option B and losing (an unfavorable $8 dif-ference) is more than twice the regret produced by choosingOption A and seeing Option B succeed (an unfavorable $4 dif-ference), R(S — 0) > 2R(12 — 8). As a result, regret theory pre-dicts that people will favor Option A over Option B because

Regret

R($8)

R($4)

$4($12 minus $8) ($8 minus $0)

Difference between outcome of foregone option and chosen option

Figure 3. Regret theory's regret (R) function, denned over the differ-ence between the outcome that would have been obtained (given adifferent choice) and the outcome that was obtained.

Option B has a higher expectation of regret, .33/?(8 — 0), thandoes Option A, .67K02 - 8). Loomes and Sugden (1982) pre-dicted that, for most choices involving winning money, peoplewill avoid regret by being risk averse.

Loomes and Sugden (1987b; Loomes, 1988) have tested theirtheory by having subjects make choices such as these for realmoney. The effect of regret is tested by manipulating the waysin which outcomes of different alternatives co-occur and seeingwhether these changes lead to predictable changes in prefer-ence. All told, the empirical evidence collected by Loomes andSugden (1987b; Loomes, 1988) and by others (Battalio, Kagel, &Jiranyakul, 1991; Tversky, Slovic, & Kahneman, 1990) has pro-vided only mixed support for their theory. The main drawbackto their empirical procedure appears to be a pallid manipula-tion. Their experiments depend on subjects noticing how theoutcomes of the alternatives are configured. Although Loomesand Sugden's approach provides an elegant test of their theory,it is not very robust.

A more robust test for the effect of regret is suggested by D. E.Bell's version of regret theory. D. E. Bell (1982,1983,1985) hasproposed that the most important determinant of regret is thepresence or absence of feedback on foregone alternatives. D. E.Bell observed that, as regret is a function of what is learnedabout the outcome of the foregone alternative, it is of muchgreater concern when the foregone alternative will be resolvedthan when it will remain unresolved. Situations vary in howmuch people expect to learn about the outcomes of their deci-sions: Sometimes people expect to learn nothing (e.g., when theconsequences are remote), other times people expect to learnonly about the option they have chosen but nothing about the

2 Although Loomes and Sugden (1982) do not offer a psychologicalexplanation for the shape of the regret function, one possibility is thatits shape is due to the perceptual processes of contrast and assimila-tion. Specifically, outcomes of different alternatives that are close invalue may be assimilated, whereas outcomes of different alternativesthat are discrepant in value may be contrasted.

446 RICHARD P. LARRICK

"road not taken," and other times people expect to learn aboutthe outcome of both the alternative they have chosen and thealternative they have passed up. Thus, expecting vivid, concretefeedback about what definitely would have occurred produces agreater potential for regret than pallid, abstract knowledge ofwhat statistically was likely to occur.

D. E. Bell's (1983) claim received indirect support in a studyby Tindale (1989), which showed that the amount of feedbackpeople expected to receive affected how confident they wereabout their decisions. People who expected no feedback showedthe most confidence in their decision, those who expected feed-back on their chosen alternative showed an intermediateamount of confidence, and those who expected feedback onforegone alternatives showed the least confidence. Presumably,the more feedback people expected to receive, the greater wasthe potential for regret and the lower people's confidence. How-ever, when Kelsey and Schepanski (1991) performed a directtest of the relationship between feedback and risk preference,they found that differences in the expectation of feedback didnot affect the amount of risk that people took. An explanationfor this null result was offered by Josephs et al. (1992) in amodified version of regret theory.

Protecting the self from regret. Josephs et al. (1992) startedwith the assumption that the expectation of feedback createsthe possibility for regret and added a second dimension: peo-ple's vulnerability to feeling regret. They proposed that peoplewant to maintain a good self-image when they make a decision(Baumeister, Tice, & Hutton, 1989; Greenwald, 1980; Steele,1988;Taylor&Brown, 1988;Tesser, 1988)and that regret threat-ens people's self-image because it can lead them to question thewisdom of their original decision (Sugden, 1985). However, peo-ple are differentially susceptible to threats to their self-image,and it is people who are vulnerable to feeling regret who willmake decisions that minimize the possibility of regret. Thespecific variable that Josephs et al. examined was self-esteem.In line with several social psychological theories about the self,Josephs et al. assumed that people with low self-esteem aremore vulnerable to threats to their self-image because they havefewer means of defending against a threat; people with highself-esteem, on the other hand, can have a decision turn outpoorly but draw on various defenses or illusions to maintaintheir positive self-image (Steele, 1988; Taylor & Brown, 1988).For example, subjects with low self-esteem have been shown tobe more upset and more demotivated by failure (Brockner,1979; Brockner, Derr, & Laing, 1987; Sweeney & Wells, 1990)and less able to defend their overall self-image from failure(Kernis, Brockner, & Frankel, 1989) than are subjects with highself-esteem, who are more likely to use self-serving attributionsto preserve their sense of self-worth (Larrick, 1991).

Because subjects with low self-esteem are not as prepared todeal with failure as are subjects with high self-esteem, they mustuse other means to minimize the possibility of failure (see alsoBaumeister et al., 1989; Baumgardner, Kaufman, & Levy,1989). Often these means are preemptive behaviors that includeself-handicapping (Harris & Snyder, 1986; Tice, 1991); failingstrategically to lower expectations (Baumgardner & Brownlee,1987); behaving modestly, especially in public (Baumeister etal., 1989); and avoiding situations that can expose failure(Strube & Roemmle, 1985). Thus, Josephs et al. (1992) proposed

that subjects with low self-esteem should be more motivatedthan subjects with high self-esteem to make decisions that re-duce the possibility of regret.

Several lines of evidence support the claim that people do infact protect their self-image when they make decisions. Oneline of evidence is provided by work on cognitive dissonance(Festinger, 1957, 1964; Wicklund & Brehm, 1976). Cognitivedissonance theory predicts that people will feel discomfortafter making a difficult decision because the desirable aspectsof the foregone alternative and the undesirable aspects of thechosen alternative are discrepant with the choice that was made(Brehm, 1956). In other words, people are bothered by thoseaspects of the decision that could make them regret it. Overtime, however, people rationalize their decision. Steele (1988)has demonstrated that postdecision rationalization can be ex-plained by the motivation to protect one's self-image. Specifi-cally, people who have been protected from regret by beingreminded of something good about themselves show less ratio-nalization than do people who are unprotected from regret(Steele, 1988). Furthermore, people with high self-esteem showless rationalization than do people with low self-esteem (Insko& Gilmore, 1984; Steele, Spencer, & Lynch, in press).

A second line of evidence was provided by Josephs et al.(1992; Larrick, 1991), who extended the self-protection per-spective to decisions under risk. The two factors Josephs et al.examined were (a) the amount of feedback that subjects ex-pected and (b) the subjects' self-esteem. They proposed thatexpecting to learn about the outcomes of foregone alternativescreates the possibility for regret and having low self-esteemmakes people vulnerable to feeling regret. They tested this hy-pothesis in several studies that manipulated how much feed-back people expected to receive about the outcomes of theirdecisions. As predicted, they found that expecting to learnabout the outcomes of foregone alternatives led people with lowself-esteem to make choices that minimized the possibility ofregret. Subjects with low self-esteem were more risk aversewhen they expected feedback on their decisions and were morelikely to shield themselves from learning about the outcomes ofdesirable foregone alternatives. Subjects with high self-esteem,on the other hand, never made regret-minimizing choices.These results indicate that the ability to maintain a good self-image in the face of regret is an important factor in determiningrisk preference.

Several other studies have also examined whether peopleprotect their self-image by avoiding feedback on foregone alter-natives. (Similar behaviors have been studied in the cognitivedissonance literature; see Frey, 1986.) Consistent with this pre-diction, Northcraft and Ashford (1990) found that subjects withlow self-esteem were less likely to seek feedback on their deci-sions than were subjects with high self-esteem. However, otherstudies have found a contrary pattern (Knight & Nadel, 1986;Weiss & Knight, 1980); the actual relationship between self-es-teem and information search may depend on whether the nega-tive information is useful in preventing future failure (Spencer,Josephs, & Steele, 1993).

Research on social comparison theory suggests that theavoidance of feedback on decision outcomes may extend tointerpersonal situations as well. For example, one perspectiveon social comparison theory (Festinger, 1954) contends that

SELF-PROTECTION IN DECISIONS 447

unfavorable social comparisons can damage a person's self-image (Cruder, 1977; Hakmiller, 1966; Tesser, 1988; Wills,1981). Several studies have shown that subjects with low self-es-teem are more adversely affected by unfavorable social compari-sons and more likely to avoid them than are subjects with highself-esteem (Gibbons & Gerrard, 1989; Gibbons & McCoy,1991; Smith & Insko, 1987). Social comparison is important indecision making because people are sensitive to feedback onother people's outcomes (McClintock & McNeel, 1966) and areextremely dissatisfied when they receive an inferior outcome(Loewenstein, Thompson, & Bazerman, 1989). This dissatisfac-tion should be even greater when another person's outcomereflects directly on one's own decision-making ability. For exam-ple, if two people face the same decision but make differentchoices, then learning of the other person's superior outcomecould lead to regret and envy. One strategy for minimizing thisthreat is to avoid feedback on the other person's outcome(Brickman & Bulman, 1977). Another strategy is to choose thesame option as the other person. The latter prevents the possibil-ity of doing worse, and it guarantees that, if the outcome ismisery, there will at least be company. Although these hypothe-ses are untested, social comparison theory represents a promis-ing area for extending the self-protection approach.

Overall, the self-protection approach offers several advan-tages over other theories of decision making. First, the results itpredicts and finds cannot be accounted for by the psychophysi-cal and cognitive theories. Specifically, none of the universaltheories predicts that changing the amount of feedback peopleexpect to receive on the outcomes of their decision would affectsubjects' risk preferences. The expectation of feedback leadspeople with low self-esteem to make defensive choices eventhough the objective description of the alternatives—the proba-bilities and payoffs—remains constant. In addition, prospecttheory and cardinal utility theory, by proposing basic universalmechanisms, cannot account for individual differences in riskpreference.

Second, the self-protection approach focuses on a more gen-eral psychological difference than do the individual-differencetheories of Atkinson (1957, 1983; Atkinson & Raynor, 1978)and Lopes (1987; Schneider & Lopes, 1986). Self-image protec-tion is not as narrow as need for achievement or need for secu-rity. It represents a general set of processes that explains behav-ior across a range of disparate domains. As such, it has thepotential to serve as an important unifying variable in a psycho-logical theory of decision making. The importance of this fac-tor suggests that other aspects of the decision process might befruitfully examined from this perspective. For example, onestrategy for protecting self-image is to make a choice that is easyto justify. Then, even if the decision turns out poorly, it is stillpossible to demonstrate the original merit of the decision bothto yourself (to prevent regret) and to others (to prevent em-barrassment). Simonson (1989) has found that people do in factfavor justifiable alternatives when they must choose betweenalternatives that are difficult to compare. For example, is itbetter to buy a gas guzzler that has a 5-year warranty but onlygets 25 miles to the gallon or a subcompact that has only a2-year warranty but gets 42 miles to the gallon? This decision isdifficult because it is not clear how to make a trade-off betweengas mileage and warranty. In situations such as this, people

increase their preference for a given alternative if a similar,inferior alternative is added to the choice set. For example, if aninferior subcompact is added to the choice set (one that has a1-year warranty and gets 40 miles to the gallon), people shifttheir preference to the original subeompact. Simonson sug-gested that the new, inferior alternative makes the dominantalternative easier to justify. In support of his contention, hefound that this effect was significantly greater when peopleexpected to explain their decision to someone else. Thus, in theface of public scrutiny and potential embarrassment, peopleminimized the threat by favoring the most justifiable alterna-tive. The self-protection view suggests that some people will bemore susceptible to the threat of evaluation and more likely tomake justifiable choices. The tendency to justify choices is oneof many decision phenomena that would be interesting to studyfrom a self-protection perspective.

In sum, these studies support the claim that people antici-pate potential negative consequences of a decision and act inways to defend against them. In particular, people who arevulnerable to threats to their self-image behave in ways thatprotect them from unfavorable information about their deci-sions. However, there are several important drawbacks to theself-protection view of decision making. First, it only describeshow people use decisions to protect their self-image; it does notdescribe how people might use the decision process to enhancetheir self-image. For example, perhaps risk taking can boostself-image. The positive consequences that decision makingmight have for self-image are largely ignored in the currentversion of the theory. This is significant because such factorsmight be particularly important in the behavior of people withhigh self-esteem. A second drawback to the self-protection per-spective is that it does not specify under what conditions indi-viduals with high self-esteem will be concerned with regret.The theory assumes that self-esteem serves as a buffer but notas an insurmountable one. So when the stakes are high enough,everyone will behave defensively. At what point will people withhigh self-esteem become defensive? Finally, another factor toconsider is how people might protect their self-image in waysother than making a defensive choice. For example, perhapspeople reaffirm their competence by reminding themselves ofan important accomplishment that is unrelated to the decisionat hand. Steele (1988) has suggested this possibility, but no onehas examined it directly. Future research on the self shouldprovide greater understanding about self-processes and ad-dress many of these drawbacks.

Integrating Explanations for Risk Preference

Two types of psychological explanation are typically offeredin theories of decision making under risk. One type attributesrisk preference to basic processes common to all people. The-ories that are based on this perspective tend to focus on"colder" psychophysical and cognitive processes. For example,these theories propose that fundamental physiological and per-ceptual mechanisms lead to universal risk preferences. Theother type of explanation attributes risk preference to individ-ual differences. Theories that are based on this perspectivetend to focus on "hotter" affective and motivational processes.For example, these theories propose that situational and person-

448 RICHARD P. LARRICK

ality factors heighten motivational concerns and lead to system-atic differences in risk preference. Taken together, these expla-nations suggest that people focus on two goals when they makedecisions. One goal is to maximize their expected outcomes;the other goal is to maintain a positive self-image. A compre-hensive theory of decision making would reflect both goals.Ideally, such a theory would also include as few parameters aspossible.

How might a comprehensive theory of decision making beconstructed? One approach would be to conduct critical testsof different theories and retain only the most important factors.It is not clear at this point whether such tests would tip thescales in favor of psychophysical or motivational factors. How-ever, constructing such critical tests might be difficult. For ex-ample, a study that had high external validity would probablyinvolve large, real stakes. In this case, both psychophysics andself-relevance would be more pronounced. Thus, these factorsmay be difficult to unconfound in actual studies.

A second and more fruitful approach would be to integratethe two goals within the same theory. Of the extant theories,expected utility theory offers the greatest potential for encom-passing both of these dimensions in a formal framework. D. E.Bell (1983,1985) has demonstrated how a utility function canbe decomposed into measures reflecting cardinal utility, atti-tude about risk, and attitude about regret. However, one draw-back of expected utility theory that has already been discussedis that it is not a psychological theory of decision making and isnot intended to be. It is not interested in explaining why peoplehold a certain attitude about risk or regret; it simply summa-rizes people's preferences.

This article suggests that a psychological theory of decisionmaking should focus on the psychological variables that affectthe processes underlying risk preference: psychophysics andself-protection. This characterization raises two questions: (a)What psychological variables affect each of these processes?and (b) What is the relationship between these processes indetermining risk preference? In response to the first question,psychophysical factors are assumed to be relatively stable anduniversal—perhaps even hardwired. Although there may beindividual differences in the psychophysics of probabilities andoutcomes, such differences have yet to be systematically identi-fied. However, even if differences between individuals exist,the process's hardwired nature should produce relatively stablejudgments for a given individual. On the other hand, the self-protection dimension is more clearly influenced by personalityand situational variables. Specifically, as the threat from a situa-tion increases, or as the person's ability to maintain a sense ofcompetence decreases, motivational factors will lead to moredefensive behavior.

The answer to the second question—What is the relationshipbetween the two processes?—may in fact be related to the issueof stability. If psychophysical processes are indeed stable, theyshould be a factor in all decisions, and they should be the stron-gest determinant of risk preference when motivational factorsare absent. However, as situational and personality factorscreate a greater need for self-protection, people will departmore from the psychophysical pattern in the direction of defen-sive behavior. In sum, I propose that psychophysical processeslie at the core of decision making but are surrounded by a layer

of motivational processes. In the absence of threat, the motiva-tional processes are not significant; but as the potential forthreat is increased, the motivational processes play a larger andlarger role. Although this proposal is necessarily tentative, it isconsistent with the pattern of results obtained by Josephs et al.(1992) on regret. Such an approach should prove useful in un-derstanding the role of other motivational factors.

Conclusion

A review of the psychological assumptions made in decision-making theories suggests that important factors are often ig-nored in cognitive and economic theories. Work by Atkinson(1957,1983; Atkinson & Raynor, 1978); D. E. Bell (1982,1983,1985); Josephs et al. (1992); Loomes and Sugden (1982; 1987a;Sugden, 1985); and Lopes (1987; Schneider & Lopes, 1986) dem-onstrates that a complete theory of decision making must takeinto account the motivational and emotional consequences ofmaking a decision that go beyond the stated probabilities andoutcomes of different alternatives. Such consequences aremany. Some important ones to consider are feelings that arisefrom learning that a decision has turned out poorly, such asfailure, regret, and disappointment (Loomes & Sugden, 1986);feelings that arise from publicly made decisions, such as em-barrassment and pride (Simonson, 1989; Tetlock, 1985); andfeelings that arise from how outcomes are distributed amongpeople, such as envy and gloating (Loewenstein et al., 1989), toname just a few. This is a tentative list, however, and muchremains to be learned about the role of such factors in decisionmaking.

This review proposes that a complete understanding of deci-sion making must take into account both psychophysical andmotivational explanations of behavior. Although a comprehen-sive theory would not be as elegant as any of the existing the-ories of choice, it need not be a disjointed list of effects, either.Instead, the central concepts of psychophysics and self-protec-tion can serve as organizing dimensions in a complete theory ofdecision making.

References

Arrow, J. K. (1971). Essays in the theory of risk-bearing. Chicago: Mark-ham.

Atkinson, J.W (1957). Motivational determinants of risk-taking behav-ior. Psychological Review, 64, 359-372.

Atkinson, J. W (1983). Old and new conceptions of how expected con-sequences influence actions. In N. T. Feather (Ed.), Expectations andactions: Expectancy-value models in psychology (pp. 17-52). Hills-dale, NJ: Erlbaum.

Atkinson, J. W, & Raynor, J. O. (1978). Personality, motivation, andachievement. Washington, DC: Hemisphere.

Barren, F. H., von Winterfeldt, D., & Fischer, G. W (1984). Empiricaland theoretical relationships between value and utility functions.Acta Psychologica, 56, 233-244.

Battalio, R. C, Kagel, J. H., & Jiranyakul, K. (1991). Testing betweenalternative models of choice under uncertainty: Some initial results.Journal of Risk and Uncertainty, 3, 25-50.

Baumeister, R. E, Tice, D. M., & Hutton, D. G. (1989). Self-presenta-tional motivations and personality differences in self-esteem. Jour-nal of Personality, 57, 548-579.

Baumgardner, A. H., & Brownlee, E. A. (1987). Strategic failure in

SELF-PROTECTION IN DECISIONS 449

social interaction: Evidence for expectancy disconfirmation pro-cesses. Journal of Personality and Social Psychology, 52, 525-535.

Baumgardner, A. H., Kaufman, C. M, & Levy, P. E. (1989). Regulatingaffect interpersonally: When low esteem leads to greater enhance-ment. Journal of Personality and Social Psychology, 56, 907-921.

Bell, D. E. (1982). Regret in decision making under uncertainty. Opera-lions Research, 30, 961-981.

Bell, D. E. (1983). Risk premiums for decision regret. ManagementScience, 29,1156-1166.

Bell, D. E. (1985). Putting a premium on regret. Management Science,31,117-120.

Bell, D. E., & Raiffa, H. (1988). Marginal value and intrinsic risk aver-sion. In D. E. Bell, H. Raiffa, & A. Tversky (Eds.), Decision making:Descriptive, normative, and prescriptive interactions (pp. 384-397).Cambridge, England: Cambridge University Press.

Bell, J. F. (1967). A history of economic thought (2nd ed.). New York:Ronald Press.

Bernoulli, D. (1954). Exposition of a new theory on the measurementof risk (L. Sommer, Trans.). Econometrica, 22,23-36. (Original workpublished 1738)

Brehm, J. W (1956). Post-decision changes in desirability of alterna-tives. Journal of Abnormal and Social Psychology, 52, 384-389.

Brickman, P., & Bulman, R. J. (1977). Pleasure and pain in social com-parison. In J. M. Suls & R. L. Miller (Eds.), Social comparison pro-cesses: Theoretical andempiricalperspectives^^. 149-186). Washing-ton, DC: Hemisphere.

Briys, E., Eeckhoudt, L., & Louberge, H. (1989). Endogenous risks andthe risk premium. Theory and Decision, 26, 37-46.

Brockner, J. (1979). The effects of self-esteem, success-failure, andself-consciousness on task performance. Journal of Personality andSocial Psychology, 37, 1732-1741.

Brockner, J., Derr, W R., & Laing, W N. (1987). Self-esteem and reac-tions to negative feedback: Toward greater generalizability. Journalof Research in Personality, 21, 318-333.

Bromiley, P., & Curley, S. P. (1992). Individual differences in risk tak-ing. In J. F. Yates (Ed.), Risk-taking behavior. New York: Wiley.

Cohen, M., Jaffray, J. Y, & Said, T. (1985). Individual behavior underrisk and under uncertainty: An experimental study. Theory and De-cision, 18, 203-228.

Cohen, M., Jaffray, J. Y, & Said, T. (1987). Experimental comparison ofindividual behavior under risk and under uncertainty for gains andfor losses. Organizational Behavior and Human Decision Processes,39, 1-22.

Dyer, J. S., & Sarin, R. K. (1979). Measurable multiattribute valuefunctions. Operations Research, 27, 810-822.

Dyer, J. S., & Sarin, R. K. (1982). Relative risk aversion. ManagementScience, 28, 875-886.

Ellsberg, D. (1961). Risk, ambiguity, and the Savage axioms. QuarterlyJournal of Economics, 75, 643-669.

Festinger, L. (1954). A theory of social comparison processes. HumanRelations, 7, 117-140.

Festinger, L. (1957). A theory of cognitive dissonance. Evanston, IL:Row, Peterson.

Festinger, L. (1964). Conflict, decision, and dissonance. London: Tavis-tock.

Fishburn, P. C., & Kochenberger, G. A. (1979). Two-piece von Neu-mann-Morgenstern utility functions. Decision Sciences, 10, SOS-SIS.

Frey, D. (1986). Recent research on selective exposure to information.Advances in Experimental Social Psychology, 19, 41-80.

Friedman, M., & Savage, L. J. (1948). The utility analysis of choicesinvolving risk. The Journal of Political Economy, 56, 279-304.

Gibbons, F. X., & Gerrard, M. (1989). Effects of upward and down-

ward social comparison on mood states. Journal of Social and Clini-cal Psychology, 8,14-31.

Gibbons, F. X., & McCoy, S. B. (1991). Self-esteem, similarity, andreactions to active versus passive downward comparison. Journal ofPersonality and Social Psychology, 60, 414-424.

Gossen, H. H. (1983). The laws of human relations and the rules ofhuman action derived therefrom (R. C. Blitz, Trans.). Cambridge,MA: MIT Press. (Original work published 1854)

Greenwald, A. G. (1980). The totalitarian ego: Fabrication and revision- of personal history. American Psychologist, 35, 603-618.Gruder, C. L. (1977). Choice of comparison persons in evaluating one-

self. In J. M. Suls & R. L. Miller (Eds.), Social comparison processes:Theoretical and empirical perspectives (pp. 21-41). Washington, DC:Hemisphere.

Hakmiller, K. L. (1966). Threat as a determinant of downward compar-ison. Journal of Experimental Social Psychology, J, 32-39.

Harris, R. N., & Snyder, C. R. (1986). The role of uncertain self-esteemin self-handicapping. Journal of Personality and Social Psychology,51, 451-458.

Heath, C, & Tversky, A. (1991). Preference and belief: Ambiguity andcompetence in choice under uncertainty. Journal of Risk and Uncer-tainty, 4, 5-28.

Hershey, J. C, & Schoemaker, P. J. H. (1980). Prospect theory's reflec-tion hypothesis: A critical examination. Organizational Behaviorand Human Performance, 25, 395-418.

Insko, C. A., & Gilmore, R. F. (1984). Self-esteem and the evaluation ofchosen and unchosen alternatives. Representative Research in SocialPsychology, 14,12-29.

Jevons, W S. (1871). Theory of political economy. London: Macmillan.Josephs, R. A., Larrick, R. P., Steele, C. M., & Nisbett, R. E. (1992).

Protecting the self from the negative consequences of risky deci-sions. Journal of Personality and Social Psychology, 62, 26-37.

Kahneman, D., & Miller, D. T. (1986)! Norm theory: Comparing realityto its alternatives. Psychological Review, 92, 136-153.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis ofdecision under risk. Econometrica, 47, 263-291.

Kahneman, D., & Tversky, A. (1982). The psychology of preferences.Scientific American, 246,160-173.

Keeney, R. L., & Raiffa, H. (1976). Decisions with multiple objectives:Preferences and value tradeoffs. New York: Wiley.

Kelsey, D, & Schepanski, A. (1991). Regret and disappointment intaxpayer reporting decisions: An experimental study. Journal of Be-havioral Decision Making, 4, 33-53.

Kernis, M. H., Brockner, J., & Frankel, B. S. (1989). Self-esteem andreactions to failure: The mediating role of overgeneralization. Jour-nal of Personality and Social Psychology, 57, 707-714.

Knight, P. A., & Nadel, J. I. (1986). Humility revisited: Self-esteem,information search, and policy consistency. Organizational Behaviorand Human Decision Processes, 38,196-206.

Kogan, N, & Wallach, M. A. (1964). Risk taking: A study in cognitionand personality. New York: Holt, Rinehart & Winston.

Landman, J. (1987). Regret: A theoretical and conceptual analysis.Journal for the Theory of Social Behaviour, 17,135-160.

Larrick, R. P. (1991). Protecting the self from regret in decisions underrisk. Unpublished doctoral dissertation, University of Michigan.

Lewin, K., Dembo, T, Festinger, L, & Sears, P. S. (1944). Level ofaspiration. In J. McV Hunt (Ed.), Personality and the behavior dis-orders (pp. 333-378). New York: Ronald Press.

Littig, L. W (1966). Motivational correlates of probability preference.In J. W Atkinson & N. T. Feather (Eds.), A theory of achievementmotivation (pp. 93-102). New York: Wiley.

Loewenstein, G. F, Thompson, L., & Bazerman, M. H. (1989). Socialutility and decision making in interpersonal contexts. Journal ofPersonality and Social Psychology, 57, 426-441.

450 RICHARD P. LARRICK

Loomes, G. (1988). Further evidence of the impact of regret and disap-pointment in choice under uncertainty. Economica, 55, 47-62.

Loomes, G., & Sugden, R. (1982). Regret theory: An alternative theoryof rational choice under uncertainty. Economic Journal, 92, 805-824.

Loonies, G., & Sugden, R. (1986). Disappointment and dynamic con-sistency in choice under uncertainty. Review of Economic Studies,55,271-282.

Loomes, G., & Sugden, R. (1987a). Some implications of a more gen-eral form of regret theory. Journal of Economic Theory, 41, 270-287.

Loomes, G., & Sugden, R. (1987b). Testing for regret and disappoint-ment in choice under uncertainty. Economic Journal, 97, 118-129.

Lopes, L. L. (1987). Between hope and fear: The psychology of risk.Advances in Experimental Social Psychology, 20, 255-295.

McClelland, D. C. (1951). Personality. New York: William Sloane.McClintock, C. G., & McNeel, S. P. (1966). Reward and score feedback

as determinants of cooperative and competitive game behavior.Journal of Personality and Social Psychology, 4, 606-613.

Menger, K. (1950). Principles of economics (J. Dingwall & B. Hoselitz,Trans.). New York: Free Press of Glencoe. (Original work published1871)

Mosteller, F, & Nogee, P. (1951). An experimental measurement ofutility. Journal of Political Economy, 59, 371-404.

Northcraft, G., & Ashford, S. J. (1990). The preservation of self ineveryday life: The effects of performance expectations and feedbackcontext on feedback inquiry. Organizational Behavior and HumanDecision Processes, 47, 42-64.

Pratt, J. W (1964). Risk aversion in the small and in the large. Econo-metrica, 32, 122-126.

Rachlin, H. (1989). Judgment, decision, and choice: A cognitive/beha-vioral synthesis. San Francisco: Freeman.

Rachlin, H., Logue, A. W, Gibbon, J., & Frankel, M. (1986). Cognitionand behavior in studies of choice. Psychological Review, 93, 33-45.

Schneider, S. L., & Lopes, L. L. (1986). Reflections in preferencesunder risk: Who and when may suggest why. Journal of ExperimentalPsychology: Human Perception and Performance, 12, 535-548.

Schoemaker, P. J. H. (1980). Experiments on decisions under risk: Theexpected utility hypothesis. Dordrecht, The Netherlands: MartinusNijhoff.

Schoemaker, P. J. H. (1982). The expected utility model: Its variants,purposes, evidence, and limitations. Journal of Economic Literature,20, 529-563.

Simonson, I. (1989). Choice based on reasons: The case of attractionand compromise effects. Journal of Consumer Research, 16, 158-174.

Slovic, P., & Lichtenstein, S. (1968). The relative importance of proba-bilities and payoffs in risk-taking. Journal of Experimental Psychol-ogy, 75,1-18.

Slovic, P., & Lichtenstein, S. (1983). Preference reversals: A broaderperspective. American Economic Review, 73, 596-605.

Smith, R. H., & Insko, C. A. (1987). Social comparison choice duringability evaluation: The effects of comparison publicity, performancefeedback, and self-esteem. Personality and Social Psychology Bulle-tin, 13, 111-122.

Spencer, S. J., Josephs, R. A., & Steele, C. M. (1993). Low self-esteem:The uphill struggle for self-integrity. In R. Baumeister (Ed.), Self-es-teem and the puzzle of low self-regard. New York: Plenum Press.

Steele, C. M. (1988)." The psychology of self-affirmation: Sustainingthe integrity of the self. Advances in Experimental Social Psychology,21, 261-302.

Steele, C. M., Spencer, S. J., & Lynch, M. (in press). Self-image resil-ience and dissonance: The role of affirmational resources. Journalof Personality and Social Psychology.

Strube, M. J, & Roemmle, L. A. (1985). Self-enhancement, self-assess-ment, and self-evaluative task choice. Journal of Personality and So-cial Psychology, 49, 981-993.

Sugden, R. (1985). Regret, recrimination, and rationality. Theory andDecision, 19, 77-99.

Sweeney, P. D., & Wells, L. E. (1990). Reactions to feedback about per-formance: A test of three competing models. Journal of Applied So-cial Psychology, 20, 818-834.

Taylor, S. E., & Brown, J. D. (1988). Illusion and well-being: Some socialpsychological contributions to a theory of mental health. Psychologi-cal Bulletin, 103. 193-210.

Tesser, A. (1988). Toward a self-evaluation maintenance model of so-cial behavior. Advances in Experimental Social Psychology, 21,181-227.

Tetlock, P. E. (1985). Accountability: The neglected social context ofjudgment and choice. Research in Organizational Behavior, 7, 297-332.

Tice, D. M. (1991). Esteem protection or enhancement? Self-handicap-ping motives differ by trait self-esteem. Journal of Personality andSocial Psychology, 60, 711-725.

Tindale, R. S. (1989). Group vs individual information processing: Theeffects of outcome feedback on decision making. Organizational Be-havior and Human Decision Processes, 44, 454-473.

Tversky, A., & Kahneman, D. (1986). Rational choice and the framingof decisions [Special issue]. Journal of Business, 59, 251-278.

Tversky, A., Slovic, P., & Kahneman, D. (1990). The causes of prefer-ence reversal. American Economic Review, 80, 204-217.

von Neumann, J., & Morgenstern, O. (1944). The theory of games andeconomic behavior. Princeton, NJ: Princeton University Press.

Walras, L. (1954). Elements of pure economics (W. Jaffe, Trans.). Home-wood, IL: Irwin. (Original work published 1874)

Weiss, H. M., & Knight, P. A. (1980). The utility of humility: Self-es-teem, information search, and problem-solving efficiency. Organiza-tional Behavior and Human Performance, 25, 216-223.

Wicklund, R. A., & Brehm, J. W (1976). Perspectives on cognitive disso-nance. Hillsdale, NJ: Erlbaum.

Wills, T. A. (1981). Downward comparison principles in social psychol-ogy. Psychological Bulletin, 90, 245-27'1.

Yates, J. F. (1990). Judgment and decision making. Englewood Cliffs,NJ: Prentice Hall.

Yates, J. F, & Stone, E. R. (1992). The risk construct. In J. F. Yates (Ed.),Risk-taking behavior. New York: Wiley.

Zuckerman, M. (1979). Sensation seeking: Beyond the optimal level ofarousal. Hillsdale, NJ: Erlbaum.

Zuckerman, M., Simons, R. F, & Como, P. G. (1988). Sensation seekingand stimulus intensity as modulators of cortical, cardiovascular, andelectrodermal response: A cross-modality study. Personality and In-dividual Differences, 9, 361-372.

Received October 18,1991Revision received March 2,1992

Accepted April 20,1992 •