Embed Size (px)

Citation preview

Morris GelbChief Operating Officer

Morgan StanleyFebruary 13, 2002

Statements in this presentation relating to matters that are not historical facts are forward-looking statements. These forward-looking statements are just predictions or expectations and are subject to risks and uncertainties. Actual results could differ materially, based on factors including but not limited to future global economic conditions, availability of capital markets, industry production capacity and operating rates, technological developments, the supply demand balance for the products produced by the Company and its joint ventures, competitive products and pricing pressures, increases in raw material and/or energy costs, changes in governmental regulations and other risk factors. For more detailed information about the factors that could cause our actual results to differ materially, please refer to Lyondell Chemical Company's Annual Report on Form 10-K for the year ended December 31, 2000, Lyondell’s Quarterly Report on Form 10-Q for the quarter ended September 30, 2001, as well as Lyondell’s Annual Report on Form 10-K for the year ended December 31, 2001 and Lyondell’s 2002 proxy statement, which will be filed with the SEC. Page 2

Safe Harbor Language

Page 3

Lyondell Chemical Company - Intermediate Chemicals and

Derivatives

– World’s leading producer of PO and derivatives

– 100% Ownership

Equistar - Petrochemicals and Polymers

– A leading North American producer of ethylene, propylene and

polyethylene

– Low cost position based on feedstock flexibility and scale

– 41% Ownership

LCR - Refining

– Unique capability to refine heavy crude oils

– Contractually stable business; strong cash flow generator

– 58.75% Ownership

Lyondell Operates in 3 Major Businesses

Page 4

Roadmap to Success

Executing our Strategic Plan

Prudently Managing Quality Assets

Delivering Results in Difficult Environment

Positioned for Significant Returns in Up-Turn

Page 5

Our Beliefs in the Drivers of Success Remain Constant

Sustainable Competitive Advantages Technology Market Position

Low Cost Production Scale Breadth and Depth of Product Offering Global Reach Capital Market Liquidity

Page 6

Strategy for Value Creation

Page 7

Leading Positions in All Key Products

* Source: CMAI, LYO capacities as of 1/1/01

Product Annual Capacity* Capacity Position

1st in North America

1st in the world

1st in North America

3rd in the world

1st in North America

1st in the world

2nd in North America

3rd in the world

2nd in North America

6th in the world

3rd in North America

3rd in the world

Ethylene (lbs) 11.6 billion

Propylene Oxide (lbs)

Styrene Monomer (lbs)

MTBE (bbl/day)

3.9 billion

3.7 billion

58,500

Propylene (lbs) 5.0 billion

Polyethylene (lbs) 5.7 billion

Eq

uis

tar

IC&

D

Page 8

Products Serve Key Durable & Non-Durable Markets

EthylenePropylene

Antifreeze / deicers

Food Packaging

ToysAutomotive Components

Consumer Products

Home Construction

Pharmaceuticals

Apparel

Automotive Seating

Home Furnishings

Grocery Sacks

Page 9

Sustainable Advantages in Key Businesses

Petrochemicals – Low Cost Advantage Feedstock flexibility historically provides 4 cpp

variable cost advantage

Refining – Strong Cash Generation Heavy Crude Processing Capability Unique “Deemed Margin” Contract Improved Operational Reliability

IC&D – PO Cost and Technology Leadership Proprietary Process Technology Leader Global Production Base Important Derivative Positions

Page 10

Large Asset Base Provides Opportunities to Optimize the Portfolio

Polymers• Shut-Down Port Arthur• Expanded Matagorda & Victoria

IC&D• Exited ADI• Sold Polyols

Petrochemicals• Idled Lake Charles

Page 11

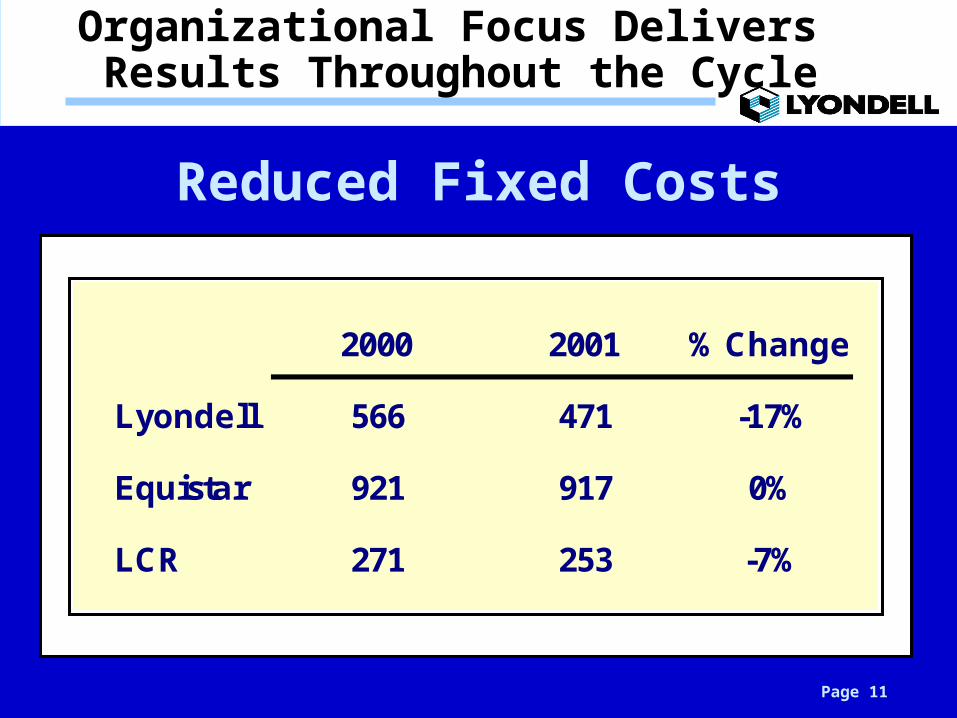

Organizational Focus Delivers Results Throughout the Cycle

2000 2001 % Change

Lyondell 566 471 -17%

Equistar 921 917 0%

LCR 271 253 -7%

Reduced Fixed Costs

Page 12

Day

s o

f W

ork

i ng

Cap

i tal

Reduced Working Capital

2001 Cash fromWorking Capital: LYO $128MM Equistar $282MM*

0102030405060708090

1998 1999 2000 2001

Lyondell Equistar

* Includes elimination $130 million AR securitization

Page 13

Prudently Managing Assets($

,MM

)

0

50

100

150

200

1999 2000 2001 2002 LE

Equistar Lyondell

($M

M)

Disciplined Capital Expenditures

PO11 Spending

Page 14

Minimal Near Term Debt Maturities

0

500

1,000

1,500

2,000

2002 2003 2004 2005 2006 2007 2008 2009

$MM

Lyondell Equistar

Debt Maturity Schedule

1 – LYO Revolver Expires

1

Page 15

Significant Liquidity

Lyondell Equistar

Cash Balance 12/31/01 $146MM $202MM

Revolver 12/31/01 $500MM $500MM

Total Liquidity $646MM $702MM

1 2

1 – excludes approximately $4.5 million committed against letters of credit2 – excludes approximately $0.7 million committed against letters of credit

Page 16

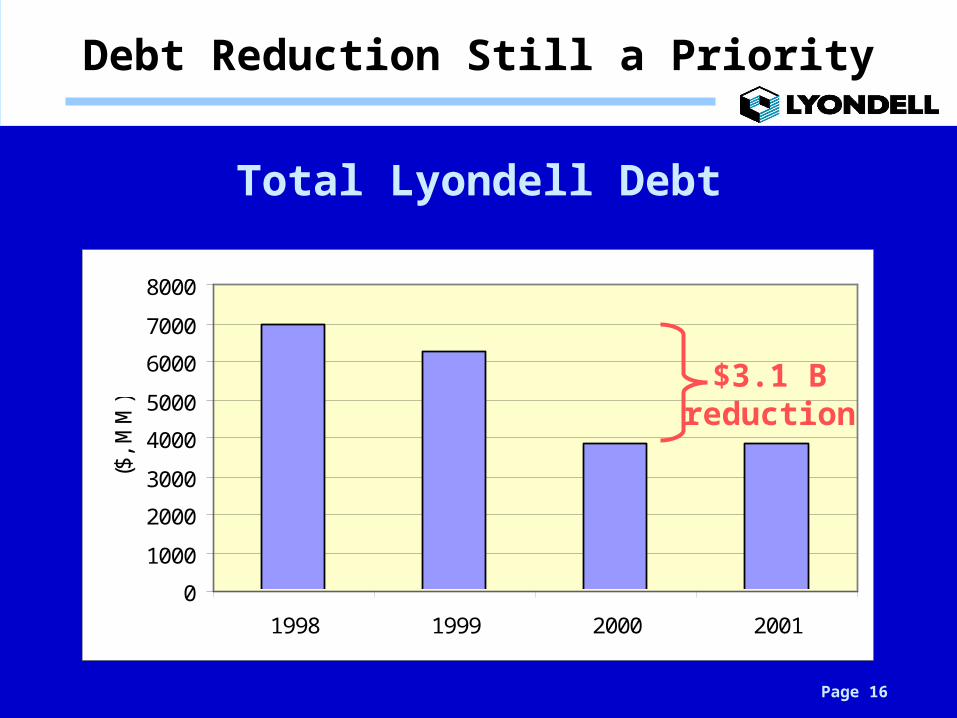

Debt Reduction Still a Priority

Total Lyondell Debt

0

1000

2000

3000

4000

5000

6000

7000

8000

1998 1999 2000 2001

($,

MM

)

$3.1 B reduction

Page 17

Equistar Transactions

Lyondell Sells Package of Securities Lyondell Sells Package of Securities

to Occidentalto Occidental– 30 – 34 million shares of Series B stock30 – 34 million shares of Series B stock

– 5 million, 5 year $25 warrants5 million, 5 year $25 warrants

– Payments equivalent to 7.38% of ’02 & ’03 Payments equivalent to 7.38% of ’02 & ’03

Equistar distributions up to $35 millionEquistar distributions up to $35 million

Lyondell buys Occidental’s 29.5% Lyondell buys Occidental’s 29.5%

share of Equistarshare of Equistar

Page 18

Normalized Equistar EBITDA1 = $1.0 billion

Increase in proportional Equistar EBITDA $300 millionImpact of $300 million of Lyondell debt reduction $0.12/share

Impact of Occidental Transaction on Cash Generation and Earnings Potential

Impact of $0.01/lb margin increase on EPS

Before AfterEthylene 0.24 0.32Polymers 0.14 0.19

Impact of accelerated debt reduction . . .

1 - Pro forma assuming 1993 (trough) and 1995 (cyclical upturn) CMAI cash margins, Equistar product capacities as of 2000 and up to $280 million of cost savings resulting from Equistar formation.

Page 19

Ethylene Demand 1970-2002United States

5000

15000

25000

35000

45000

55000

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

Mn

Lb

s

-5%

0%

5%

10%

15%

20%

25%

30%

% C

hg

GD

P

GDP %AGR Ethylene consumption

?

Past Demand Contractions Were Followed by Periods of Strong Growth

Source: DRI & ChemData

Page 20

Executing our strategy

Accumulated leading positions in all key

products

Established low cost producer positions

Delivering results in difficult environment

Preserving our liquidity

Committed to debt reduction and our dividend

Investment Highlights

Morgan Stanley

February 13, 2002