Embed Size (px)

Citation preview

More than Words: Markets’ Expectations andECB’s talking about future∗

Maddalena Galardo† Cinzia Guerrieri‡

Preliminary and incomplete, please do not quote without authors permissionThis version: May 2016

Abstract

After the Global Financial Crisis, policy interest rates have beenreduced towards the effective lower bound across many advancedcountries. The impairments to the standard transmission mechanismshave enhanced the importance of communication and forward guidanceto signal longer-lasting accommodative stance. This paper investigatesthe signaling channel for the European Central Bank communicationstrategy from a semantic perspective. We construct an indicatorof future-sentiment by applying the wordscore methodology to theIntroductory statement of the press conference. Then, we exploit thisindicator to extract a measure of communication shock. By running anevent-study regression, we analyze the main determinants of changesin money markets’ rates occurred around the monetary policy decisionday. Our results suggest that communication shocks affect market’sexpectations. The robustness analysis confirms this thesis.

JEL classification: E43, E44, E52, E58, E61, G14Keywords: ECB communication, semantic analysis, signaling channel, forward guidance,unconventional monetary policy

∗The paper benefited from extensive discussions with Pierpaolo Benigno and GiuseppeFerrero. We also gratefully acknowledge suggestions from Nicola Borri, Martina Cecioni,Paolo Emilio Mistrulli, Carlo Rosa and Pierre Siklos. We also thank participants atthe conference Money, Banking and Finance (Rome, Italy), and at seminar at LUISSUniversity of Rome for useful comments. The opinions expressed are those of the authorsand do not reflect views of their respective institutions. Any remaining errors are the soleresponsibility of the authors.†Department of Economics and Finance, LUISS University of Rome. E-mail:

[email protected]‡Department of Economics and Finance, LUISS University of Rome. E-mail:

1

Non-technical Summary

As a consequence to the Global Financial Crisis, policy interest rates have been reducedtowards the effective lower bound across many advanced countries. This has underminedthe possibility of using the standard monetary policy instrument to define the currentmonetary policy and to signal possible future moves. Therefore, communication andforward guidance have become a crucial monetary policy instrument to convince firmly thefinancial markets operators that future monetary policy stance will remain accommodative.This paper explores the extent to which the European monetary authority has been ableto shape financial markets expectations of future short-term interest rates by using aparticular language to communicate its future monetary policy stance, i.e. the signalingchannel.In particular, we look at the evolution of the verbal tenses employed during the pressconference which follows the monetary policy meeting, from January 2002 to the end of2014, with focus on the section of the Introductory statement dedicated to the explanationof the policy decision (namely the policy summary). In other terms, we study if andhow the structure of forward-looking statements has changed over time in response tothe increasing need of managing expectations. We observe that the language used tocommunicate future developments has evolved from softer future tenses, used to statesomething likely to happen in the future, to stronger future tenses, used to convincefirmly financial markets operators of longer-lasting accommodative stance. We interpretthis evidence as an important effort to signal that monetary policy stance will remainaccommodative in the future, by underscoring both the commitment to its mandate andalso its firm reaction to any further worsening of economic conditions by ensuring futurelow interest rates and assets purchases.To uncover the extent to which different kinds of communication about future affectexpectations, we restrict the analysis to the policy summary and construct an objectiveindicator, which is named the future-sentiment index, as a weighted sum of differentcategories of future verbal tenses. Then, we identify the unexpected component in thecommunication about future by defining the process followed by the future-sentimentindex. We explore if and how the surprise in communication about future, identifiedas described above, affects the signaling channel. By running an event-study regression,we investigate the main determinants of interest rates movements occurred around themonetary policy decision day. As we focus on the signaling channel, we look at the Euriborrates at different maturities which reflect the financial markets’ expectations. Our resultsshow that the long end of the Euribor term structure reacts more than the short end,suggesting that the stronger is the surprise in speaking about future the higher is theeffect of ECB’s communication on interest rates, especially on maturities between six andtwelve months.

2

1 Introduction

Over the last decade, transparency has been widely recognized as the new paradigmof central bank governance. In fact, world’s major central banks have enhanced theircommunication to become more transparent, especially about the objective and themonetary policy strategy.1 The prevailing orientation, among both academics and centralbankers, is that during normal times transparency is sufficient to allow markets’ operatorsto infer the central bank reaction function.2 However, after the onset of the GlobalFinancial Crisis, the role of central bank communication has evolved remarkably.In reaction to the financial turmoil and the following severe economic recession, policyinterest rates have been reduced towards the effective lower bound across many advancedcountries. This has undermined the possibility of using the standard monetary policyinstrument to define the current monetary policy and to signal possible future moves. Theclose proximity of the policy rate to the effective lower bound, the impairments to themonetary policy transmission mechanism, and the persistence of the Great Recession haverisen the need of (i) enhancing further the communication strategy and introducing (orreinforcing in same cases) the forward guidance; (ii) changing the size and composition ofthe central bank balance sheet.3 The former should work through the signaling channel(i.e. by managing expectations), while the latter should activate the portfolio balancechannel (i.e. by influencing specific financial market prices).This paper investigates the signaling channel for the European Central Bank (ECB)communication strategy, i.e. it explores the extent to which the European monetaryauthority is able to shape financial markets expectations of future short-term interestrates by using a particular language to communicate its future monetary policy stance.Although there is a large literature on this issue, our paper adds several novelties.First, we contribute to the literature on the semantic content of the ECB communicationby showing that the language used to communicate future developments has evolvedfrom softer future tenses, used to state something likely to happen in the future,to stronger future tenses, used to convince firmly financial markets operators oflonger-lasting accommodative stance. Exploiting this evidence, we construct an indicatorof communication as a weighted sum of different categories of future verbal tenses: strongfuture and weak future. We apply automatically the wordscore methodology to selectthe future tenses4 employed during the press conference which follows the monetarypolicy meeting, with focus on the section of the Introductory statement dedicated tothe explanation of the policy decision (namely the policy summary). Our indicator ofcommunication differs from previous ones because we do not consider words but only

1See Siklos (2011), Dincer and Eichengreen (2014) for a recent analysis of central banktransparency.

2More predictable future policy decisions turns into better expectations about futurepolicy rates, which influence the current long-term interest rates. In few words, centralbank transparency should improve the monetary policy effectiveness. For a comprehensiveanalysis please see Woodford (2003). On the importance of communication for monetarypolicy, see Woodford (2005), Issing (2005), and Praet (2014)

3Refer to Bernanke and Reinhart (2004) and Blinder (2010) for a discussion of theunconventional monetary policies at the zero lower bound.

4Wordscores extract information using word frequencies, this methodology wasintroduced by Laver et al. (2003).

3

verbal tenses. We exploit the fact that the use of verbal tenses belongs to a preciseand stable system of rules (the grammars) which are not dynamic entities as words are.5Moreover, the grammars are not subjective rules and therefore no authors’ interpretationis needed to identify if the future verbal tense used is a strong future or a weak future.From a methodological point of view, our indicator of communication, which is named thefuture-sentiment index, is quite appealing since it is easy to construct, replicable, does notdepend on time-varying glossary, and it is not undermined by possible declassification dueto personal judgments. We then explore the process underling the future-sentiment indexand use it to extract the surprise in ECB’s communication about future.A key contribution of our paper is to determine how the surprise in communication aboutfuture affects the signaling channel. We run an event-study regression, to identify the maindeterminants of interest rates movements occurred around the monetary policy decisionday. As we focus on the signaling channel, we look at the Euribor rates at differentmaturities which reflect the financial markets’ expectations on future short-term interestrates. Our results show that the long end of the Euribor term structure reacts more thanthe short end, suggesting that the stronger is the surprise in speaking about future thehigher is the effect of ECB’s communication on interest rates, especially on maturitiesbetween six and twelve months. In other terms, speaking about future emerged as a usefulpolicy tool to ease further monetary policy.Moreover, this article contributes to the recent literature on the effects of theannouncements of unconventional monetary policies: including dummy variables thataccount for the announcement of unconventional monetary policy, we are able todisentangle the movements in markets’ expectations due to language from those due tothe announcement per se.The results from robustness analysis confirm the importance of either signaling futurepolicy intentions for shaping expectations and having a measure of talking about futurein the empirical model to capture the effect of the announcement of forward guidance.The remainder of the paper is organized as follows. Section 2 discusses the main referenceson central bank communication and highlights our contribution to the literature. Section3 illustrates some evidence on the evolution of the ECB press conference and Section 4introduces our future-sentiment index. Section 5 presents the empirical strategy and theresults; this section includes also some robustness analysis. Finally, Section 6 concludes.The Appendix provides details on the data used in this paper.

2 Literature Review

This paper is related to and contributes to three strands of a well-developed literature.While we focus only on the literature which investigates the effects of central bankcommunication on asset prices movements around monetary policy decisions, we classifythe main references according to three ways communication has been identified.6First, many papers apply the factor analysis approach to extrapolate the communicationshock related to future policy inclination.7 As an example of application to the ECB, see

5Language is a dynamic entity and words can change meaning according tocircumstances. In addition, new words can be introduced.

6For the sake of brevity, we report the main applications to the European Central Bank.7See the pioneer work by Gurkaynak et al. (2005)

4

Brand et al. (2010) which determines the principal components from a matrix containingthe changes in forward rates with several maturities. Nevertheless, the factor analysisapproach can only investigate the extent to which the communication on policy inclinationis relevant for the expectations of market participants. By their nature, it cannot revealanything about why market participants forecast a different forward path for interest ratesafter the statement release, or which aspect of the statement constitutes the news thatchanges their beliefs.8 We improve this strand of literature identifying the aspect of thestatements which influences financial markets’ expectations.Second, our paper contributes to the literature on the semantic content of the centralbank communication. Here we can distinguish between two main streams according to themethodologies used to extract words or sentences, i.e. automated versus manual approach.In turn, both approaches can be used to construct subjective or objective indicators.An automated approach, based on a mechanical manner using a set of search words,is applied e.g. by both Ehrmann and Fratzscher (2007) and Ehrmann and Fratzscher(2009). However, they differ in relation to the indicator constructed: while the formerpropose two subjective indicators of monetary policy inclination and economy outlook, thelatter relies on dummy variables corresponding to several types of information.9 Rosa andVerga (2007) provides an example of manual approach, based on the analysis of the policysummary. By looking at the forward-looking statements, they propose a classificationbased on their interpretation of hawkish and dovish tone. Ferrero and Secchi (2009)propose instead an analysis of different levels of information related to future policyinclination, by constructing several dummy variables for both quantitative and qualitativeannouncements.10 To our knowledge, none of the indicators used in the literature aboutcentral banks communication, as well as those constructed by the cited works, are able tocapture the surprise in communication abstaining from subjective indicators or to measurethe intensity of future tenses.Finally and most importantly, our paper contributes to the recent literature on the effectsof announcements of unconventional monetary policies (henceforth, UMP). While thereare many studies applied to the US and UK economies, there is scarce evidence for theEuro Area.11 As our index reflects also the future verbal tenses used to announce centralbank balance sheet policies, we follow the standard approach and include the correspondingdummy variables in the extended analysis in order to identify the contribution of each typeof UMP to the signaling channel. However, relying on dummy variables, though widelyused, limits the validity of this empirical strategy, because it assumes that the entireannouncement was a complete surprise. As pointed out by Christensen and Rudebusch(2012), this is likely to underestimate the interest rate response as, especially for the laterannouncements, market participants may have anticipated some action. This drawbackputs a premium on the need to have a measure of communication shock, as we show here.

8The limits of this kind of analysis are amply discussed in Woodford (2012).9They differ also in relation to the source of information: while Ehrmann and Fratzscher

(2007) classifies the extracted sentences from inter-meeting speeches held by centralbankers, Ehrmann and Fratzscher (2007) uses Reuters snaps of the ECB press conferenceconcerning the economic outlook, inflation, money growth, and interest rates.

10Namely, numerical interest rate path (quantitative announcement), verbal hints onthe future evolution of policy rates (qualitative announcement) with clear timing (clearqualitative announcement) or ambiguous timing (opaque qualitative announcement), andno announcement.

11For a literature review please see Falagiarda and Reitz (2015)

5

3 Evidence on the ECB press conference

In this section we illustrate some evidence concerning the ECB press conference whichfollows the monetary policy decision. In particular, we focus on the time spanning fromJanuary 2002 to December 2014 with monthly frequency.12The timing of the communication strategy is the following: the press release reporting thedecision on the key interest rates is issued at 1:45 p.m. CET/CEST; it is followed shortlyby the press conference starting at 2:30 p.m., which is divided in two main sessions, i.e.the Introductory statement and the Question and Answer Session.13 The former reportsall the necessary information concerning the ECB monetary policy stance in a simple andsystematic way, while the latter is often used to clarify ECB’s messages.The structure of the Introductory statements has remained quite the same since the verybeginning: (i) the first part reports a summary of the ECB’s monetary policy decisionand balance of risks to price stability, and since July 2013 it includes also an open-endedforward guidance; (ii) the second part discusses both real and monetary developments inthe Euro area (first and second pillar) and from May 2003 it is followed by a “sum-up andcross-check” paragraph which repeats the initial synthetic assessment; (iii) finally, the ECBPresident concludes with some considerations on fiscal policy and structural reforms.Although the structure of the press conference has not changed over time, its lengthhas increased (Figure 1). In particular, we notice that the first section of Introductorystatement - the policy summary from now onwards - has more than doubled between 2008and 2014 (dashed line in Figure 2). Most of this increase has occurred between 2008and 2012, a period characterized by increasing uncertainty and the use of unconventionalmeasures with a wider range of possible monetary policy responses to a given shock. Thishas called for a greater effort in communication by the monetary authority: as stated bythe ECB President Mario Draghi, “Our response was to place more emphasis on enhancedcommunication - both regarding our commitment to our price stability objective, andregarding our assessment of and response to the rapidly changing economic and financialsituation”, Draghi (2014).Furthermore, the policy summary has evolved from a content perspective too. Figure 3provides a visual overview of the most frequent words used for three main sub-periods.Interestingly, we observe that the frequency of talking about future using the tenseconstructed with the “will” has increased over time reaching its maximum in 2014 (Figure4). It is worth noticing that this “strong” future verbal tense is used to communicatesome different but complementary aspects of the monetary policy stance: from pricestability objective to future policy interest rates path, to the monitoring of risks, to theannouncements of central bank balance sheet policies. As an example, let’s consider thefollowing policy summary in the Introductory statement of June 2014: «. . . the measureswill contribute to a return of inflation rates to levels closer to 2% [. . . ] Looking ahead, theGoverning Council is strongly determined to safeguard this anchoring. Concerning ourforward guidance, the key ECB interest rates will remain at present levels for an extendedperiod of time in view of the current outlook for inflation [. . . ]Moreover, if required, wewill act swiftly with further monetary policy easing.» It is evident that the “strong” future

12From January 2015, the frequency of the monetary policy meetings has been reducedfrom monthly to every six weeks.

13The Introductory statement read by the Governor is simultaneously published onlineat http://www.ecb.europa.eu/press/html/index.en.html.

6

verbal tense based on the use of “will” is related to ensure that (i) the objective of pricestability will be reached according to the measures taken; (ii) the policy interest rates willcontinue to be low, (iii) the ECB is ready to react by easing further the monetary policystance.We interpret this evolution of language towards a stronger future verbal tense as animportant communication effort to signal and convince financial markets that monetarypolicy stance will remain accommodative in the future. To sum up, the ECB “talkingabout future” has changed both quantitatively (ECB President speaks more, Figures 1and 2) and qualitatively (the future verbal tense used has evolved towards a strongermeaning, Figures 3 and 4).Next section describes how we measure these changes, in order to construct a validindicator able to capture the evolution of the language.

4 The Future-Sentiment Index

This paper enriches the literature on the semantic content of the ECB communication byaccounting explicitly for the future tenses used during the monthly press conference whichfollows the monetary policy meeting.Our approach consists of two steps. First, by restricting the analysis to the policysummary, we apply automatically the wordscore methodology using search words related tothe two future tenses categories, namely “weak” and “strong”. As human spoken languagescan be described as a system of symbols and rules (the grammars) by which the symbolsare manipulated, the identification of the future tense is straightforward: every completesentence is built around a verb that indicates the time when action occurs (present, pastand future). By properly differentiating between different future forms, the verb tense canalso communicate accordingly promises, intentions, or facts likely to happen in the future.Thus, different is the form of the aforementioned future used, different is the messagetransmitted and received by the public.As mentioned, we distinguish the future forms between: (i) action stated as likely orpossible to happen in the future, but which aren’t completely certain or refer to conditionalsituation (weak future tense); and (ii) decision stated as promises, threats or commitments(strong future tense).14 To make this distinction clear we provide some examples usingtexts extracted from press conferences: (i) on May 2010 the ECB’s President said «Overall,we expect price stability to be maintained over the medium term [. . . ] Monetary policywill do all that is necessary to maintain price stability in the euro area over the mediumterm.»; (ii) on November 2014 «Our accommodative monetary policy stance will underpinthe firm anchoring of medium to long-term inflation expectations [. . . ], our monetarypolicy measures will together contribute to a return of inflation rates to levels closer to ouraim.». On May the President expects that all the necessary monetary policy measures tocontribute to price stability over the medium term. On November the President reinforcesits message, by ensuring that price stability objective will be reached.The aim of the measure discussed here is to capture this difference: we categorize theexpect-based future tense as weak future and the will-based ones as strong future.

14The distinction is clearly reported in the Oxford Dictionaries at http://www.oxforddictionaries.com/words/verb-tenses .

7

The second step of our approach consists of using the word counts to construct an objectiveindicator, named the future-sentiment index, which is obtained as follows

FSt =

∑ji=1 wiFutureTensei,t

Nt(1)

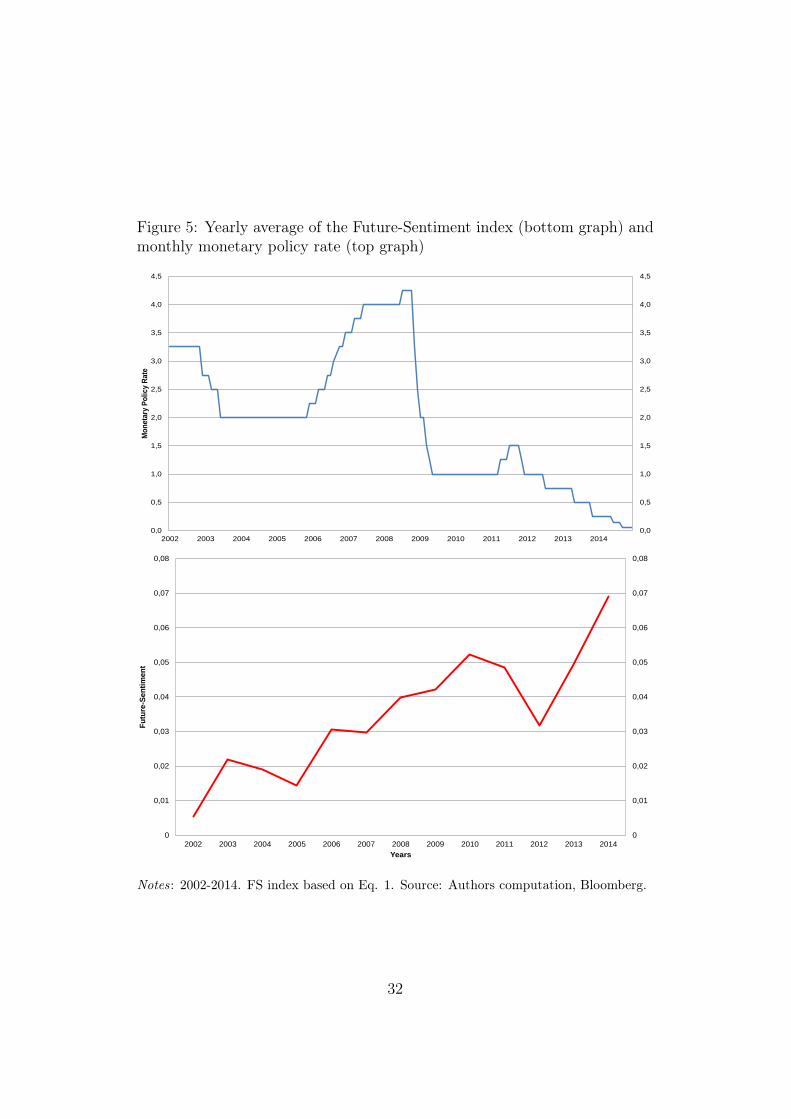

where j is the number of future tenses contained in the policy summary of time t, wi isthe weight associated to the future tense i and Nt is the total number of words, exceptnumbers and stop words, composing the policy summary of time t which have a sparsitylower than 80 per cent.15The denominator reports the total number of words of the summary, Nt, to avoid thepossibility that the phenomenon captured by the index is just the increase in speakingby the central bank (see Section 3). The numerator is a weighted sum of the futureforms, where the weights are defined as follows: zero if the tense is not a future, 0.5 if itis a weak future and 1 for a strong future. This weighting scheme reflects the degree of“aggressiveness” in talking about the future. In other terms a higher value of the indexreflects a more aggressive approach of the ECB in speaking about the future monetarypolicy stance.We have computed the future-sentiment index from January 2002 to December 2014.16Figure 5 reports the yearly average of the index. It measures an increasing path forthe future-sentiment in ECB’s announcements with higher values occurring after thebeginning of the financial turmoil, consistently with the need of a more aggressivecommunication about future to menage expectations during periods of increasinguncertainty. In 2013 and 2014 the index explodes: phenomenon consistent with theintroduction of an explicit forward-guidance in the ECB’s communication strategysince July 2013. The future sentiment index, in fact, is constructed to capture theaggressiveness in communication about future, therefore it is able to measure forwardguidance as well.

4.1 The Surprise component in Future-Sentiment

As emphasized by Kuttner (2001), in a forward-looking environment financial marketsshould react only to the surprise element of monetary policy actions. Therefore, inassessing the market response to monetary authority’s communication about future, it’simportant to focus on the surprise component of the future-sentiment. In order to identifythis component, we explore the process underlying the future-sentiment index verifyingthe following equation

FSt+1 =

n∑i=1

φiFSt+1−i +

m∑j=1

βjXjt + ξt+1

15We consider as stop words articles, prepositions, conjunctions and so on (please seethe Table A.1 in the Appendix). Words which have a sparsity lower than 80 per centappear once in at least 30 policy summaries.

16The complete data set is available from the authors upon request. Please see theAppendix A where we provide some examples.

8

where n and m identify, respectively, lagged values of the Future-Sentiment indexand different macro-variables, precisely Xt = {ut, πt, πet , yt, ZEWt}. Using a general tospecific approach, we gradually eliminate lags of the future-sentiment index and regressorsgenerally considered relevant for monetary policy actions, such as the GDP growth rate,yt, the changes in unemployment rate, ut, and current inflation, πt, that turn out to benot statistically significant. We also control for expected inflation,17 πet , and a measureof expectation about the economic activity, namely the ZEW Financial Market Surveyindex, ZEWt,18 in order to capture all the information which hits financial markets inthe timespan occurring between the last press conference and the next one (capturedrespectively by FSt and FSt+1). The econometric method used is ordinary least squareswith Newey-West correction for the standard errors. Regression results are reported inTable 1. Although statistically significant the effect of ZEWt is almost null and notrelevant to identify the process of the future-sentiment index.We find that the process which better describes our future-sentiment measure is anaugmented AR(2), namely:

FSt+1 = φ1FSt + φ2FSt−1 + φ3πet + ξt+1, (2)

where FS is the future-sentiment measured as described in chapter 4, πet reflects expectedinflation and ξt+1 is the error term.In other terms, how much the ECB talks today about future depends on the past twomonths communication, consistently with the persistence of the economic environment.Not surprisingly, it is also affected by the expected inflation, given that the ECB aims atmanaging inflation expectations in the pursuit of price stability.19Given the information set preceding the next press conference, the markets’ prediction ofECB talking about future can be represented by

F̂St+1 = φ̂1FSt + φ̂2FSt−1 + φ̂3πet (3)

where φ̂1, φ̂2, φ̂3 are the coefficients estimated using process 2. Assuming that agentsidentify this process and use the ECB’s past declaration about future in formingexpectations about what will be declared, the surprise can be approximated by theestimated innovations, that is

ξ̂t+1 = FSt+1 − F̂St+1. (4)

17We use as proxy of the inflation expectation the forecast for CPI inflation fixed horizonconstructed using Consensus Economics CPI inflation forecast for current year and nextyear. Consensus Economics forecasts are released at the end of each month, about tendays before the ECB’s monthly press conference.

18The ZEW Financial Market Survey is carried out on a monthly basis, it is updatedat the end of each month around a week before the press conference. About 350 financialanalysts from banks, insurance companies and large industrial enterprises participatein this survey. The indicator reflects the difference between the share of analysts thatare optimistic and the share of analysts that are pessimistic for the expected economicdevelopment in the Eurozone in six months.

19Price stability is defined as a year-on-year increase in the Harmonised Index ofConsumer Prices (HICP) for the euro area of below 2%. On the Press Release “TheECB’s monetary policy strategy” (May 2003) « [. . . ] the Governing Council confirmedthis definition (which it announced in 1998). At the same time, the Governing Councilagreed that in the pursuit of price stability it will aim to maintain inflation rates close to2% over the medium term. [. . . ]».

9

Using an increasing window which includes the information set preceding each pressconference, we estimate the communication shock for each Governing Council monetarypolicy meeting starting as of September 2004, to have at least 30 observations for the firstestimation. The series of innovations obtained is reported in Figure 6.It is evident that in last years ECB has increased deeply its effort to communicate whatit will do in the future but it is not clear if it is effective in moving financial markets’expectations. Next chapter empirically analyses this issue.

5 Empirical Analysis

5.1 Data and Methodology

As our aim is to investigate the signaling channel of the ECB communication strategy,we focus on the Euribor rate which incorporates the financial markets’ expectations onfuture short-term interest rates.20 For our analysis, we use daily data of the one-month(1M), the three-month (3M), six-month (6M), nine-month (9M) and twelve-month (12M)maturities of the Euribor rate that were obtained from Bloomberg (Figure 7).Our thesis is that talking about the future could play an important role in affectingthe Euribor term structure, especially at longer horizon. We proceed as follows. Weapply a standard event-study regression approach, restricting our empirical analysis to thedays of the ECB Governing Council monetary policy meetings spanning from September2004 to December 2014. Conditionally on the assumption that financial markets areinformationally efficient and respond only to news that could affect their belief aboutthe future, we focus on the daily changes of the Euribor rate as a measure of changesin expectations that might be related to the information released on the ECB meetingday. Our empirical strategy is based on three main assumptions: i. on meeting daysthe relevant news for financial markets concerns the policy rates (the main refinancingrate and the lending facilities rates) and the ECB press conference; ii. the expectationhypothesis holds; iii. and the term premium is constant during a one-day window.21The first assumption implies that, to study the effectiveness of the communication strategyproxied by the shock in the future-sentiment index, we control for the news relatedto the monetary policy decision. In addition, given that the ECB starts to announceunconventional monetary policies during the press conference as of August 2007, wealso include several dummy variables which take value 1 when a non-standard measureis announced. Following Falagiarda and Reitz (2015), we update and extend theirclassification up to ten categories i. liquidity provisions in foreign currencies through

20The Euribor (Euro Interbank Offered Rate) is a daily reference rate, based on theinterest rates at which banks offer to lend unsecured funds to other banks in the eurowholesale. Euribor is determined (fixed) at about 11:00 CET/CEST each working day,as a filtered average of the inter-bank deposit rates offered by a large panel of designedcontributor banks for maturities ranged from one week to one year.

21Nonetheless, we acknowledge that someone could question the validity of thisassumption after the onset of the crisis. It is a testable hypothesis and we leave theanswer to it to future research.

10

swap lines with major central banks (FOR); ii. unlimited provisions of liquidity throughfixed rate tenders with full allotment for the main refinancing operations (FRTFA); iii.extensions of the list of collateral assets (COLL); iv. operations concerning long-termrefinancing operations (LTRO); v. outright purchases of covered bonds (CBPP); vi.purchases of government bonds carried out under the Securities Market Programme(SMP); vii. purchases of government bonds carried out under the Outright MonetaryTransactions (OMT); viii. asset-backed securities purchase programme (ABSPP); ix.targeted longer-term refinancing operations (TLTRO); and x. forward guidance (FG).22As our index measures also the future verbal tenses used to announce UMP, by controllingfor them, we are able to disentangle the effects due to language from those due to theannouncement per se. We expect a negative sign on the coefficients of the UMP, especiallyon the forward guidance, given that they mean generally to accommodate the monetarypolicy stance and in particular to alleviate liquidity conditions on specific financial markets.We construct also a dummy taking value 1 if Mario Draghi is the ECB’s President in charge.Finally, we include a set of control variables which could affect the dynamics of the Euriborrate other than the ECB news: i. the surprise of U.S. initial jobless claims, defined asthe difference between the actual release and market expectations measured through themean response of a Bloomberg survey among market participants23; ii. changes in the EuroStoxx volatility as a measure of financial turmoil;24 iii. three dummies corresponding tothree main phases of the crisis that started in August 2007, namely the financial turmoilfrom 9 August 2007 to the collapse of Lehman Brothers, the Great Recession phase from15 September 2008 until 7 May 2010, and the Eurozone sovereign debt crisis from May2010 until November 2012.25Specifically, we estimate the following equation using ordinary least squares with robustcorrection of standard errors:

∆rk,t+1 = α+ βMPSMPSt+1 + βξ ξ̂t +

10∑i

βi,uUMPi,t + δPrest + βusUSt + βv∆V IXt+

+ δRect + δFinCrisist + δSovCrisist + εt+1 (5)

where the time index t refers to the press conference day, while t + 1 to the dayafter. The dependent variable, ∆rk,t+1 = rk,t+1 − rk,t, represents the first differenceof the daily Euribor rate with a maturity of three, six, nine and twelve months (k ∈3M, 6M, 9M, 12M). The main regressors MPSt+1 and ξ̂t stand for the monetary policyshock and the innovation in future-sentiment, respectively. The unexpected component ofthe monetary policy decision is measured by the first difference of the one-month Euribor

22The means by which an unconventional policy decision is communicated to financialmarkets can include press releases, press conferences, speeches and interviews. For thepurpose of our analysis, we consider only the unconventional monetary policies announcedduring the press conference.

23The release is issued every Thursday at 2:30 pm CET/CEST.24As in Arghyrou and Kontonikas (2012), Glick and Leduc (2012) and Falagiarda and

Reitz (2015). As robustness check, we control also for changes in market volatility the daybefore the press conference.

25A similar identification of the crisis periods has been suggested by Drudi et al. (2012).

11

rate around the press conference, that is MPSt+1 = r1M,t+1 − r1M,t.26 The innovation infuture-sentiment ξ̂t is estimated as described in section 4. The other variables representthe announcement of the unconventional monetary policies UMPi with i ∈ [1, 10] , thedummy for the ECB’s President in charge δPres, the surprise of US initial jobless claimsUSt, the changes in the Euro Stoxx volatility ∆V IXt, and the crisis periods dummiesδFinCrisis, δRec and δSovCrisis.

5.2 Main results

The estimation results for Equation (5) are reported in Table 2. The main drivers ofmarkets’ expectations are the unexpected change in the policy rate and the news aboutfuture intentions. In fact, the former is statistically different from zero at the 99% levelfor all the maturities analyzed and the effect on money markets’ expectations is positiveand decreasing along maturities. The coefficients for the innovation in future-sentimentare all significantly different from zero too. The communication shock has a negativeimpact which is higher for longer maturities. Therefore, our findings suggest that theECB communication about future influences the money market interest rates. This effectis negative, meaning that a positive surprise about future-sentiment induces a reduction inthe expected money markets rates. As an illustrative example, when the ECB’s Presidentstates:

"Looking ahead, our monetary policy stance will remain accommodative for as long asnecessary. The Governing Council expects the key ECB interest rates to remain atpresent or lower levels for an extended period of time. In the period ahead, we will

monitor all incoming information" (FS=0.05)

while the public predicts a future sentiment index of 0.02, the one year Euribor rate onaverage (and ceteris paribus) falls down more than half basis point. Instead, if marketsexpect a stronger talking about future (FS=0.08), then the one year Euribor rate jumpsup more than half basis point. A surprise of 0.03 in the future sentiment index causes avariation of half basis point in the one year Euribor rate.Findings for the UMP announcements are consistent with other researches aboutunconventional monetary policies.27 The money markets react relatively little tounconventional monetary policy. The announcements of sovereign bond purchases (SMPand OMT) seems to have very poor effects on interest rates, consistently with their aimto mitigate the conditions on sovereign markets through the portfolio balance channel.We obtain similar results for COLL, LTROs and TLTROs, which result to not diminishthe Euribor rates. This can be due to several reasons. Brunetti et al. (2011), in fact,show that during crisis long term refinancing operations are not effective in reducing

26Regression results are robust using directly changes in the policy rate. We usevariations in one month Euribor after the press conference to account for markets’anticipations of changes in the policy rate.

27See Cecioni et al. (2011), for a review of the effects of unconventional monetary policiesin the US and euro area interbank market until mid-2011.

12

prices and interbank market uncertainty due to the crowding-out effect that dominatesthe intervention news effect. On the contrary, liquidity provisions in foreign currenciesthrough swap lines with other central banks (FOR) and forwards guidance (FG) resultto be effective. In fact, following the announcement of bilateral central bank swaplines (FOR), Euribor rates diminished. Even if the main goal of the swap line is toprovide foreign currency liquidity to domestic banks, this instrument has been effective inmitigating negative spillovers effects, by protecting the euro area interbank market fromexternal tensions.28 As expected, the announcement of forward guidance had a relievingimpact on money market rates.

5.3 Robustness checks

So far we have considered changes in the Euribor rates at different maturities to determineif and how the surprise in communication about future affects the signaling channel. TheEuribor rates reflect all the expectations on short-term interest rates up to a specifichorizon: for higher maturity, such as 12 months, the spot rate incorporates all the effectsthat the communication shock has on shorter maturities. This could cause the increasingeffect along maturity that we find for the coefficient of the innovation in future sentiment.To asses this issue, we estimate Equation (5) using the Euribor Implied Forward Ratesas alternative dependent variable. Implied forward rates measure the financial markets’expectation on the very-short term interest rate several months ahead. Table 3 reports theresults for the three months implied forward rate three, six and nine months ahead. Thecoefficients on the surprise in future-sentiment are, as in previous estimates, all negative,increasing in absolute value with maturities. Actually the coefficients are larger in absolutevalue than previous estimates reported in Table 2 and all significant at least at the 95 percent level.To further assess the robustness of our results, we estimate Equation (5) using alternativemeasures of communication: i. the Future-Sentiment Index; ii. the surprise in strongfuture; iii. and a variable accounting for the direction of the policy summary (hawkish,dovish or neutral).Table 4 reports the results when we estimate the model using directly the Future-SentimentIndex constructed as described in section 4. The coefficients of the Future-Sentiment Indexfor maturities between 6 and 12 months are all negative, similarly as in Table 2, but smallerin absolute value and significant at the 95 per cent level.Second, Table 5 reports the results for the estimation with the surprise in strong future.To identify the surprise in strong future we proceed in two steps, as for the surprise in theFuture-Sentiment Index. First, we construct an indicator of communication as the ratiobetween the strong future tenses (will-based future tenses) and the number of words ofthe policy summary.29 Then we identify the surprise as the estimated innovation of theprocess underlying the strong future indicator. The coefficients of the surprise in strongfuture are again all negative, increasing in absolute value with maturities and significant

28For more details on the effectiveness of the swap lines, see the article "Experience withforeign currency liquidity-providing central bank swaps", Monthly Bulletin, August 2014.

29As before, words having a sparsity lower than 80 per cent except numbers and stopwords.

13

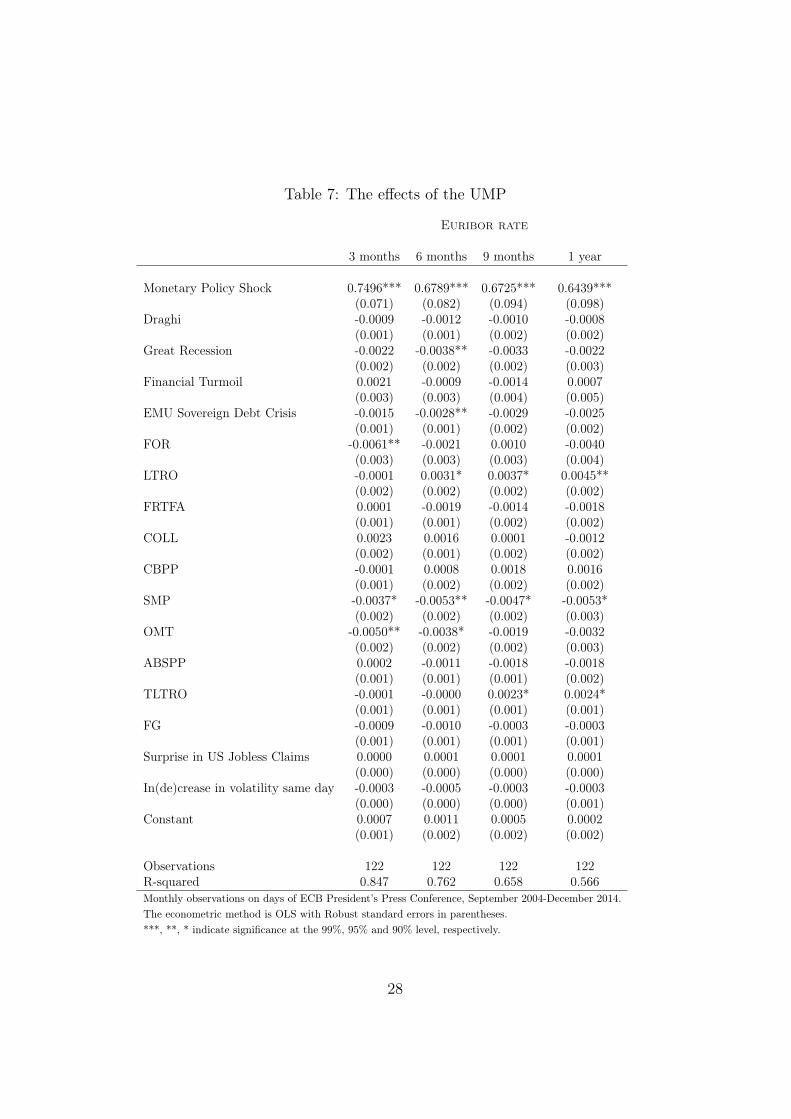

at the 99 per cent level for maturities between 6 and 12 months.Finally, since the future sentiment index is just a synthetic assessment of the verbal tensesused in the policy summary, and thus it does not account for the easing or tightening tone,we introduce in our empirical model a measure of the tone used. We use an indicator wecall direction, that is a variable on a three-value scale from -1 to +1, constructed followingRosa and Verga (2008). The value zero suggests that the current level of the policy rate isappropriate to maintain price stability over the medium term; the value -1 characterize aneasing tone while 1 a tighter monetary stance. Estimation results for the extended modelare reported in Table 6. The econometric results for the coefficients of the surprise infuture sentiment are qualitatively the same obtained in previous results and remain highlystatistically significant even if we control for an indicator of the ECB monetary policystance.As last exercise, we estimate Equation (5) without our measure of surprise incommunication about future. Results are reported in Table 7. The estimation resultswe get are mostly the same obtained in Table 2, except for the announcement of forwardguidance (FG) which is now not statistically significant. The announcement of FG andour measure of surprise in communication about future are correlated, meaning that,leaving ξ̂ away, the coefficients for FG are biased. Including the measure of surprise incommunication about future results relevant to capture the effect of the announcement ofFG on market’s expectations.

6 Conclusion

By controlling directly the very short-term interest rate, the central banks aim atinfluencing the long-term interest rates, which are crucial for the transmission of themonetary policy to the real economy. In fact, according to the term structure theory, thelong-term interest rate is an average of current and expected future short term interest ratesplus a term premium. While during normal times policy rates decisions can signal futurepolicy intensions and then affect the expectations of short-term interest rates, in the newenvironment characterized by policy rates close to the ZLB, the standard monetary policyinstrument has become severely inefficient. As a consequence, central banks have increasedtheir efforts to effectively communicate their strategy, and in particular to convince firmlyfinancial markets about a longer-lasting accommodative monetary policy stance.This paper has focused on the signalling channel of the European Central Bankcommunication strategy. As discussed in the descriptive analysis, the ECB has emphasisedwhat it will do in the future in order to steer expectations. Our results have showedthat using a future tense that is perceived by the public as a commitment in pursuing aparticular monetary policy stance is indeed more effective on affecting future short-termexpectations. In particular, the stronger is the surprise in speaking about future, thestronger is the effect on interest rates, especially for longer maturities.It is worth highlighting that our measure of surprise covers news on several butcomplementary aspects that signal the future monetary policy stance, namely forwardguidance, announcements of asset purchases and monetary policy objective. While itis clear the role of forward guidance, it is less evident why the last two factors shouldhave an impact on financial market expectations of short-term interest rates. In fact,communication on the price stability target is generally oriented to anchor the inflation

14

expectations (and thereof to influence more effectively the real long-term interest rates),and asset purchases programs should have a direct impact on the term premium. We arguethat a particular language used to communicate asset purchases and inflation objective, inaddition to forward guidance, may contribute to signal the will of the European CentralBank to do whatever it takes to ease further the monetary stance and to halt the declinein economic activity.To conclude, we have performed our analysis during a period characterized mostly by adovish attitude, and thereof the results are valid in a context of accommodative monetarypolicy stance. Although it is not possible to state if these implications apply also in ahawkish context, it remains essential to carefully choose the verbal tenses to signal theexit strategy.

15

A Appendix

List of the macroeconomic series

1. Future Sentiment Index, Authors computation

2. Euribor rate, Bloomberg

3. Euro Stoxx Volatility Index, Thomson Reuters-Datastream

4. ZEW Index, Bloomberg

5. CPI Inflation Expectations Current and Next Year, Consensus Economics

6. Dummy Liquidity in foreign currencies (FOR), Authors computation

7. Dummy Long Term Refinancing Operations (LTRO), Authors computation

8. Dummy Fixed-rate full-allotment (FRTFA), Authors computation

9. Dummy Extensions of the list of collaterals (COLLl), Authors computation

10. Dummy Covered bond purchasing programme (CBPP), Authors computation

11. Dummy Security Market Programme (SMP), Authors computation

12. Dummy Outright Monetary Transactions (OMT), Authors computation

13. Dummy Asset-Backed Securities Purchasing Programme (ASBPP), Authorscomputation

14. Dummy Targeted longer-term refinancing operations (TLTRO), Authorscomputation

15. Dummy Forward Guidance (FG), Authors computation

16. Dummy Draghi, Authors computation

16

Examples of ECB policy summary

Below we provide some examples of the ECB policy summary along with the correspondingFuture-Sentiment index (FS) and the direction of the tone. The FS index is computedaccording to Eq. 1. The tone is identified based on Rosa and Verga (2008) approach(1=hawkish, 0=neutral, -1=dovish).

i. January 2002: « [. . . ] The Governing Council concluded that recent developmentsare in line with the interest rate decisions taken in the course of last year. Wehave therefore decided to keep the key ECB interest rates unchanged. We alsoconfirmed that the current level of key ECB interest rates remains appropriate forthe maintenance of price stability over the medium term.»FS: 0 Tone: 0

ii. June 2004: « [. . . ] Nevertheless, we are still of the view that the medium-term outlookremains in line with price stability. Accordingly, we left the key ECB interest ratesunchanged. The low level of interest rates continues to support the economic recovery.We will remain vigilant with regard to all developments which could affect the risksto price stability over the medium term.»FS: 0.023256 Tone: 0

iii. October 2006: «[. . . ] Today’s decision will contribute to ensuring that medium tolonger-term inflation expectations in the euro area remain solidly anchored at levelsconsistent with price stability. Such anchoring is a prerequisite for monetary policy tomake an ongoing contribution towards supporting sustainable economic growth andjob creation in the euro area. [. . . ] Our monetary policy therefore continues to beaccommodative. If our assumptions and baseline scenario are confirmed, it will remainwarranted to further withdraw monetary accommodation. The Governing Councilwill therefore continue to monitor very closely all developments so as to ensure pricestability over the medium and longer term.»FS: 0.046512 Tone: 1

iv. January 2008: « [. . . ] The Governing Council remains prepared to act pre-emptivelyso that second-round effects and upside risks to price stability over the medium termdo not materialise and, consequently, medium and long-term inflation expectationsremain firmly anchored in line with price stability. Reflecting its mandate, suchanchoring is of the highest priority to the Governing Council. The economicfundamentals of the euro area are sound. [. . . ] We will continue to monitor veryclosely all developments over the coming weeks.»FS: 0.041096 Tone: 0

v. July 2010: «[. . . ] Based on its regular economic and monetary analyses, the GoverningCouncil views the current key ECB interest rates as appropriate. [. . . ] Our monetaryanalysis confirms that inflationary pressures over the medium term remain contained,as suggested by weak money and credit growth. Overall, we expect price stability to bemaintained over the medium term, thereby supporting the purchasing power of euroarea households. [. . . ] Monetary policy will do all that is needed to maintain pricestability in the euro area over the medium term. [. . . ] We remain firmly committedto price stability over the medium to longer term. The monetary policy stance and

17

the overall provision of liquidity will be adjusted as appropriate. Accordingly, theGoverning Council will continue to monitor all developments over the period aheadvery closely.»FS: 0.062069 Tone: 0

vi. April 2012: « [. . . ] Inflation rates are likely to stay above 2% in 2012, with upsiderisks prevailing. Over the policy-relevant horizon, we expect price developments toremain in line with price stability. Consistent with this picture, the underlying paceof monetary expansion remains subdued. [. . . ] Medium-term inflation expectationsfor the euro area economy must continue to be firmly anchored in line with our aim ofmaintaining inflation rates below, but close to, 2% over the medium term. [. . . ] Thiscombination of measures has contributed to a stabilisation in the financial environmentand an improvement in the transmission of our monetary policy. We need to carefullymonitor further developments. [. . . ]»FS: 0.019802 Tone: -1

vii. July 2014: « Based on our regular economic and monetary analyses, we decided tokeep the key ECB interest rates unchanged.[. . . ] The monetary operations to takeplace over the coming months will add to this accommodation and will support banklending. As our measures work their way through to the economy, they will contributeto a return of inflation rates to levels closer to 2%. Concerning our forward guidance,the key ECB interest rates will remain at present levels for an extended period of timein view of the current outlook for inflation. [. . . ]»FS: 0.045872 Tone: -1

18

Table A.1: Stop words

i them by then thanme their for once toomy theirs with here verymyself themselves about there ecbwe what against when governmentour which between where governingours who into why councilourselves whom through how todayyou this during all yearyour that before anyyours these after bothyourself those above eachyourselves a below fewhe an to morehim the from mosthis and up otherhimself but down someshe if in suchher or out nohers because on norherself as off notit until over onlyits while under ownitself of again samethey at further so

Notes: This table lists the stop words used for the text analysis. The latter are words whichare filtered out when computing the numerator for the Future sentiment index. In semanticcontent analysis stop words usually refer to the most common words in a language, herewe add to the commonly used list words such as ECB and governing council.

19

ReferencesArghyrou, Michael G. and Alexandros Kontonikas, “The EMU sovereign-debt

crisis: Fundamentals, expectations and contagion,” Journal of International FinancialMarkets, Institutions and Money, 2012, 22.

Bernanke, Ben S and Vincent R Reinhart, “Conducting monetary policy at very lowshort-term interest rates,” American Economic Review, 2004, pp. 85–90.

Blinder, Alan S, “Quantitative Easing: Entrance and Exit Strategies (DigestSummary),” Federal Reserve Bank of St. Louis Review, 2010, 92 (6), 465–479.

Brand, Claus, Daniel Buncic, and Jarkko Turunen, “The Impact of ECB MonetaryPolicy Decisions and Communication on the Yield Curve,” Journal of the EuropeanEconomic Association, 2010, 8.

Brunetti, Celso, Mario di Filippo, and Jeffrey H. Harries, “Effects of Centralbank Intervention on the Interbank Market during the Subprime Crisis,” The Reviewof Financial Studies, 2011, 24.

Cecioni, Martina, Giuseppe Ferrero, and Alessandro Secchi, “Unconventionalmonetary policy in theory and in practice,” Bank of Italy Occasional Paper, 2011,(102).

Christensen, Jens HE and Glenn D Rudebusch, “The Response of Interest Rates toUS and UK Quantitative Easing*,” The Economic Journal, 2012, 122 (564), F385–F414.

Dincer, Nergiz and Barry Eichengreen, “Central bank transparency andindependence: updates and new measures,” International Journal of Central Banking,2014.

Draghi, Mario, “Monetary policy communication in turbulent times,” Speech at theConference De Nederlandsche Bank 200 years: Central banking in the next two decades,April, European Central Bank 2014.

Drudi, Francesco, Alain Durré, and Francesco Paolo Mongelli, “The interplay ofeconomic reforms and monetary policy : the case of the eurozone,” Journal of CommonMarket Studies, 2012.

Ehrmann, Michael and Marcel Fratzscher, “Communication and Decision-Makingby Central Bank Committees: Different Strategies, Same Effectiveness?,” Journal ofMoney,Credit and Banking, 2007, 39.

and , “Explaining Monetary Policy in Press Conferences,” International Journal ofCentral Banking, 2009, 5.

Falagiarda, Matteo and Stefan Reitz, “Announcements of ECB unconventionalprograms: Implications for the sovereign spreads of stressed euro area countries,”Journal of International Money and Finance, 2015, 53.

Ferrero, Giuseppe and Alessandro Secchi, “The announcement of monetary policyintentions,” Bank of Italy Temi di Discussione (Working Paper) No, 2009, 720.

20

Glick, Reuven and Sylvain Leduc, “Central bank announcements of asset purchasesand the impact on global financial and commodity markets,” Journal of InternationalMoney and Finance, 2012, 31.

Gurkaynak, Refet S., Brian Sack, and Eric T. Swanson, “Do Actions SpeakLouder Than Words? The Response of Asset Prices to Monetary Policy Actions andStatements,” International Journal of Central Banking, 2005, 1.

Issing, Otmar, “Communication, transparency, accountability: monetary policy in thetwenty-first century,” Federal Reserve Bank of St. Louis Review, 2005, 87 (March/April2005).

Kuttner, Kenneth N., “Monetary policy surprises and interest rates: Evidence fromthe Fed funds futures market,” Journal of Monetary Economics, 2001, 47.

Laver, M., M. Benoit, and J. Garry, “Extracting policy positions from political textsusing words as data,” American Political Science Review, 2003, 2.

Praet, Peter, “Current issues and challenges for central bank communication,” Speech atthe Conference The ECB and its Watchers XV, March, European Central Bank 2014.

Rosa, Carlo and Giovanni Verga, “On the consistency and effectiveness of centralbank communication: Evidence from the ECB,” European Journal of Political Economy,2007, 23.

and , “The impact of central bank announcements on asset prices in real time,”International Journal of Central Banking, 2008.

Siklos, Pierre L, “Central bank transparency: another look,” Applied Economics Letters,2011, 18 (10), 929–933.

Woodford, Michael, Interest and prices: Foundations of a theory of monetary policy,Princeton University Press, 2003.

, “Central bank communication and policy effectiveness,” National Bureau of EconomicResearch, 2005.

, “Methods of Policy Accomodation at the Interest-Rate Lower Bound,” in “Proceedings- Economic Policy Symposium - Jackson Hole” 2012.

21

Table 1: The Future-Sentiment Index Process

I II III IV

FSt 0.2601** 0.2541** 0.2597** 0.2599**(0.114) (0.116) (0.117) (0.116)

FSt−1 0.4810*** 0.4900*** 0.4830*** 0.4813***(0.094) (0.095) (0.098) (0.097)

πet 0.0033*** 0.0032*** 0.0031** 0.0033***

(0.001) (0.001) (0.001) (0.001)ut 0.0010 -0.0013

(0.039) (0.039)yt 0.0003

(0.001)πt -0.0004

(0.001)ZEWt -0.0002*

(0.000)

Observations 149 149 149 149R-squared 0.699 0.705 0.699 0.699The econometric method is OLS with Newey-West heteroscedasticity andautocorrelation robust standard errors in parentheses.***, **, * indicate significance at the 99%, 95% and 90% level, respectively.

22

Table 2: Empirical Model

Euribor rate

3 months 6 months 9 months 1 year

Monetary Policy Shock 0.7481*** 0.6759*** 0.6690*** 0.6400***(0.067) (0.074) (0.084) (0.086)

Surprise in Future Sentiment -0.0763* -0.1527*** -0.1802*** -0.2080***(0.043) (0.048) (0.065) (0.073)

Draghi -0.0013 -0.0020 -0.0020 -0.0019(0.001) (0.001) (0.002) (0.002)

Great Recession -0.0030 -0.0055*** -0.0053** -0.0045(0.002) (0.002) (0.002) (0.003)

Financial Turmoil 0.0020 -0.0012 -0.0018 0.0002(0.003) (0.003) (0.004) (0.004)

EMU Sovereign Debt Crisis -0.0018 -0.0033** -0.0034* -0.0032(0.001) (0.001) (0.002) (0.002)

FOR -0.0078*** -0.0054** -0.0030 -0.0086**(0.003) (0.003) (0.003) (0.004)

LTRO 0.0005 0.0044** 0.0052** 0.0062***(0.002) (0.002) (0.002) (0.002)

FRTFA 0.0013 0.0004 0.0013 0.0014(0.001) (0.002) (0.002) (0.002)

COLL 0.0022 0.0014 -0.0002 -0.0014(0.003) (0.003) (0.003) (0.003)

CBPP 0.0008 0.0025 0.0038 0.0039(0.002) (0.002) (0.003) (0.003)

SMP 0.0013 0.0047 0.0071 0.0083(0.004) (0.004) (0.005) (0.006)

OMT -0.0035 -0.0008 0.0017 0.0009(0.003) (0.003) (0.003) (0.003)

ABSPP 0.0009 0.0004 -0.0000 0.0002(0.002) (0.003) (0.003) (0.004)

TLTRO -0.0013 -0.0025 -0.0006 -0.0010(0.002) (0.003) (0.003) (0.004)

FG -0.0021** -0.0034*** -0.0031** -0.0035**(0.001) (0.001) (0.001) (0.002)

Surprise in US Jobless Claims 0.0000 0.0001* 0.0001 0.0001(0.000) (0.000) (0.000) (0.000)

In(de)crease in volatility same day -0.0003 -0.0005 -0.0003 -0.0003(0.000) (0.000) (0.000) (0.000)

Constant 0.0008 0.0014 0.0009 0.0006(0.001) (0.001) (0.002) (0.002)

Observations 122 122 122 122R-squared 0.851 0.782 0.684 0.598Monthly observations on days of ECB President’s Press Conference, Sepember 2004-December 2014.The econometric method is OLS with Robust standard errors in parentheses.***, **, * indicate significance at the 99%, 95% and 90% level, respectively.

23

Table 3: The effects of ECB talking about future on the Euribor ImpliedForward rates

Implied Forward rate

3 months in 3 months 3 months in 6 months 3 months in 9 months

Monetary Policy Shock 0.5984*** 0.6518*** 0.5489***(0.120) (0.117) (0.125)

Surprise in Future Sentiment -0.2338*** -0.2409** -0.2958**(0.072) (0.114) (0.125)

Draghi -0.0027 -0.0023 -0.0013(0.002) (0.003) (0.004)

Great Recession -0.0077** -0.0050 -0.0019(0.004) (0.004) (0.005)

Financial Turmoil -0.0043 -0.0030 0.0065(0.005) (0.006) (0.008)

EMU Sovereign Debt Crisis -0.0049** -0.0040 -0.0023(0.002) (0.003) (0.004)

FOR -0.0034 0.0019 -0.0257***(0.004) (0.006) (0.007)

LTRO 0.0083*** 0.0069** 0.0091**(0.003) (0.003) (0.004)

FRTFA -0.0004 0.0035 0.0019(0.002) (0.003) (0.003)

COLL 0.0009 -0.0036 -0.0056(0.003) (0.003) (0.003)

CBPP 0.0042 0.0069 0.0043(0.003) (0.004) (0.004)

SMP 0.0082 0.0123 0.0119(0.006) (0.008) (0.009)

OMT 0.0018 0.0070* -0.0031(0.004) (0.004) (0.005)

ABSPP -0.0001 -0.0009 0.0005(0.004) (0.005) (0.006)

TLTRO -0.0039 0.0038 -0.0020(0.004) (0.005) (0.006)

FG -0.0048*** -0.0025 -0.0049(0.002) (0.003) (0.003)

Surprise in US Jobless Claims 0.0001* 0.0001 0.0002(0.000) (0.000) (0.000)

In(de)crease in volatility same day -0.0006 0.0001 -0.0005(0.001) (0.001) (0.001)

Constant 0.0019 -0.0002 -0.0003(0.002) (0.003) (0.004)

Observations 122 122 122R-squared 0.565 0.422 0.285Monthly observations on days of ECB President’s Press Conference, September 2004-December 2014.The econometric method is OLS with Robust standard errors in parentheses.***, **, * indicate significance at the 99%, 95% and 90% level, respectively.

24

Table 4: The effects of the Future-Sentiment Index

Euribor rate

3 months 6 months 9 months 1 year

Monetary Policy Shock 0.7536*** 0.6877*** 0.6827*** 0.6551***(0.069) (0.075) (0.086) (0.090)

Future Sentiment Index -0.0582* -0.1271*** -0.1477** -0.1606**(0.035) (0.048) (0.065) (0.078)

Draghi -0.0006 -0.0005 -0.0003 0.0001(0.001) (0.001) (0.002) (0.002)

Great Recession -0.0023 -0.0040** -0.0036* -0.0025(0.002) (0.002) (0.002) (0.002)

Financial Turmoil 0.0026 0.0001 -0.0003 0.0019(0.003) (0.003) (0.004) (0.004)

EMU Sovereign Debt Crisis -0.0015 -0.0027* -0.0027 -0.0024(0.001) (0.001) (0.002) (0.002)

FOR -0.0067*** -0.0034 -0.0006 -0.0057(0.003) (0.003) (0.003) (0.004)

LTRO 0.0006 0.0046** 0.0054** 0.0063***(0.002) (0.002) (0.002) (0.002)

FRTFA 0.0008 -0.0004 0.0003 0.0001(0.001) (0.001) (0.002) (0.002)

COLL 0.0033 0.0038 0.0027 0.0017(0.002) (0.003) (0.003) (0.003)

CBPP 0.0012 0.0035 0.0051* 0.0051(0.002) (0.002) (0.003) (0.003)

SMP -0.0018 -0.0013 -0.0001 -0.0003(0.003) (0.003) (0.003) (0.004)

OMT -0.0063** -0.0065* -0.0050 -0.0066*(0.003) (0.003) (0.003) (0.004)

ABSPP 0.0019 0.0026 0.0025 0.0027(0.001) (0.002) (0.002) (0.003)

TLTRO -0.0008 -0.0017 0.0004 0.0003(0.001) (0.002) (0.002) (0.002)

FG -0.0008 -0.0008 -0.0000 0.0000(0.001) (0.001) (0.001) (0.001)

Surprise in US Jobless Claims 0.0000 0.0001* 0.0001 0.0001*(0.000) (0.000) (0.000) (0.000)

In(de)crease in volatility same day -0.0003 -0.0004 -0.0002 -0.0002(0.000) (0.000) (0.000) (0.001)

Constant 0.0016 0.0032* 0.0029 0.0028(0.001) (0.002) (0.002) (0.003)

Observations 122 122 122 122R-squared 0.850 0.777 0.677 0.586Monthly observations on days of ECB President’s Press Conference, September 2004-December 2014.The econometric method is OLS with Robust standard errors in parentheses.***, **, * indicate significance at the 99%, 95% and 90% level, respectively.

25

Table 5: The effects of the Surprise in Strong Future

Euribor rate

3 months 6 months 9 months 1 year

Monetary Policy Shock 0.7488*** 0.6773*** 0.6707*** 0.6418***(0.067) (0.073) (0.083) (0.085)

Surprise in Strong Future -0.0761* -0.1484*** -0.1722** -0.2016***(0.044) (0.050) (0.066) (0.074)

Draghi -0.0013 -0.0019 -0.0019 -0.0018(0.001) (0.001) (0.002) (0.002)

Great Recession -0.0030 -0.0055*** -0.0052** -0.0044(0.002) (0.002) (0.002) (0.003)

Financial Turmoil 0.0021 -0.0011 -0.0016 0.0004(0.003) (0.003) (0.004) (0.004)

EMU Sovereign Debt Crisis -0.0018 -0.0033** -0.0035** -0.0033(0.001) (0.001) (0.002) (0.002)

FOR -0.0078*** -0.0054** -0.0028 -0.0085**(0.003) (0.003) (0.003) (0.004)

LTRO 0.0006 0.0045** 0.0053** 0.0063***(0.002) (0.002) (0.002) (0.002)

FRTFA 0.0014 0.0004 0.0013 0.0014(0.001) (0.002) (0.002) (0.002)

COLL 0.0021 0.0013 -0.0003 -0.0016(0.003) (0.003) (0.002) (0.002)

CBPP 0.0009 0.0026 0.0039 0.0040(0.002) (0.002) (0.003) (0.003)

SMP 0.0014 0.0046 0.0068 0.0081(0.004) (0.004) (0.005) (0.006)

OMT -0.0034 -0.0007 0.0017 0.0010(0.003) (0.003) (0.003) (0.003)

ABSPP 0.0010 0.0004 -0.0000 0.0002(0.002) (0.002) (0.003) (0.003)

TLTRO -0.0010 -0.0019 0.0001 -0.0002(0.002) (0.002) (0.003) (0.003)

FG -0.0024** -0.0039*** -0.0037** -0.0043**(0.001) (0.001) (0.002) (0.002)

Surprise in US Jobless Claims 0.0000 0.0001* 0.0001 0.0001(0.000) (0.000) (0.000) (0.000)

In(de)crease in volatility same day -0.0003 -0.0005 -0.0003 -0.0004(0.000) (0.000) (0.000) (0.000)

Constant 0.0008 0.0013 0.0008 0.0005(0.001) (0.001) (0.002) (0.002)

Observations 122 122 122 122R-squared 0.851 0.780 0.680 0.594Monthly observations on days of ECB President’s Press Conference, September 2004-December 2014.The econometric method is OLS with Robust standard errors in parentheses.***, **, * indicate significance at the 99%, 95% and 90% level, respectively.

26

Table 6: The effects of the Direction variable (-1 if dovish, 0 if neutral, 1 ifhawkish)

Euribor rate

3 months 6 months 9 months 1 year

Monetary Policy Shock 0.7364*** 0.6679*** 0.6607*** 0.6369***(0.069) (0.075) (0.085) (0.087)

Surprise in Future Sentiment -0.0799* -0.1551*** -0.1827*** -0.2089***(0.043) (0.049) (0.065) (0.072)

Direction 0.0013 0.0009 0.0009 0.0003(0.001) (0.001) (0.002) (0.002)

Draghi -0.0001 -0.0011 -0.0011 -0.0016(0.001) (0.002) (0.003) (0.003)

Great Recession -0.0024 -0.0051*** -0.0049** -0.0044(0.002) (0.002) (0.002) (0.003)

Financial Turmoil 0.0016 -0.0015 -0.0021 0.0001(0.003) (0.003) (0.004) (0.005)

EMU Sovereign Debt Crisis -0.0016 -0.0031** -0.0033* -0.0031(0.001) (0.001) (0.002) (0.002)

FOR -0.0071** -0.0050 -0.0025 -0.0084*(0.003) (0.003) (0.004) (0.005)

LTRO 0.0009 0.0046** 0.0054** 0.0063***(0.002) (0.002) (0.002) (0.002)

FRTFA 0.0016 0.0006 0.0015 0.0015(0.001) (0.002) (0.002) (0.002)

COLL 0.0015 0.0010 -0.0006 -0.0016(0.003) (0.003) (0.003) (0.003)

CBPP 0.0010 0.0026 0.0040 0.0040(0.002) (0.002) (0.003) (0.003)

SMP 0.0015 0.0049 0.0073 0.0084(0.004) (0.005) (0.005) (0.006)

OMT -0.0025 -0.0001 0.0024 0.0012(0.003) (0.004) (0.004) (0.004)

ABSPP 0.0012 0.0006 0.0002 0.0003(0.002) (0.003) (0.003) (0.003)

TLTRO -0.0011 -0.0024 -0.0005 -0.0010(0.002) (0.003) (0.003) (0.004)

FG -0.0017* -0.0031*** -0.0028* -0.0034*(0.001) (0.001) (0.002) (0.002)

Surprise in US Jobless Claims 0.0000 0.0001* 0.0001 0.0001(0.000) (0.000) (0.000) (0.000)

In(de)crease in volatility same day -0.0003 -0.0004 -0.0003 -0.0003(0.000) (0.000) (0.000) (0.000)

Constant 0.0004 0.0011 0.0005 0.0005(0.001) (0.001) (0.002) (0.002)

Observations 122 122 122 122R-squared 0.853 0.783 0.685 0.598Monthly observations on days of ECB President’s Press Conference, September 2004-December 2014.The econometric method is OLS with Robust standard errors in parentheses.***, **, * indicate significance at the 99%, 95% and 90% level, respectively.27

Table 7: The effects of the UMP

Euribor rate

3 months 6 months 9 months 1 year

Monetary Policy Shock 0.7496*** 0.6789*** 0.6725*** 0.6439***(0.071) (0.082) (0.094) (0.098)

Draghi -0.0009 -0.0012 -0.0010 -0.0008(0.001) (0.001) (0.002) (0.002)

Great Recession -0.0022 -0.0038** -0.0033 -0.0022(0.002) (0.002) (0.002) (0.003)

Financial Turmoil 0.0021 -0.0009 -0.0014 0.0007(0.003) (0.003) (0.004) (0.005)

EMU Sovereign Debt Crisis -0.0015 -0.0028** -0.0029 -0.0025(0.001) (0.001) (0.002) (0.002)

FOR -0.0061** -0.0021 0.0010 -0.0040(0.003) (0.003) (0.003) (0.004)

LTRO -0.0001 0.0031* 0.0037* 0.0045**(0.002) (0.002) (0.002) (0.002)

FRTFA 0.0001 -0.0019 -0.0014 -0.0018(0.001) (0.001) (0.002) (0.002)

COLL 0.0023 0.0016 0.0001 -0.0012(0.002) (0.001) (0.002) (0.002)

CBPP -0.0001 0.0008 0.0018 0.0016(0.001) (0.002) (0.002) (0.002)

SMP -0.0037* -0.0053** -0.0047* -0.0053*(0.002) (0.002) (0.002) (0.003)

OMT -0.0050** -0.0038* -0.0019 -0.0032(0.002) (0.002) (0.002) (0.003)

ABSPP 0.0002 -0.0011 -0.0018 -0.0018(0.001) (0.001) (0.001) (0.002)

TLTRO -0.0001 -0.0000 0.0023* 0.0024*(0.001) (0.001) (0.001) (0.001)

FG -0.0009 -0.0010 -0.0003 -0.0003(0.001) (0.001) (0.001) (0.001)

Surprise in US Jobless Claims 0.0000 0.0001 0.0001 0.0001(0.000) (0.000) (0.000) (0.000)

In(de)crease in volatility same day -0.0003 -0.0005 -0.0003 -0.0003(0.000) (0.000) (0.000) (0.001)

Constant 0.0007 0.0011 0.0005 0.0002(0.001) (0.002) (0.002) (0.002)

Observations 122 122 122 122R-squared 0.847 0.762 0.658 0.566Monthly observations on days of ECB President’s Press Conference, September 2004-December 2014.The econometric method is OLS with Robust standard errors in parentheses.***, **, * indicate significance at the 99%, 95% and 90% level, respectively.

28

Figure 1: Evolution of the ECB press conference’s lenght (in words)

0

1000

2000

3000

4000

5000

6000

0

1000

2000

3000

4000

5000

6000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Len

gth

in w

ord

s

Years

Press Conference

Figure 2: Share of the press conference dedicated to the each session

0

10

20

30

40

50

60

70

80

90

100

0

10

20

30

40

50

60

70

80

90

100

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Pe

rce

nta

ge

Years

Q&A Introductionary Statement without Policy Summary Policy Summary Portion of the policy summary in the introdutory statement

Trichet Duisenberg Draghi

Notes: 2002-2014. Figure 1: Press conference (blue bars) and linear trend (gray dashedline). Figure 2: Introductory statements without the policy summary (green bars), thepolicy summary (red bars), Questions and Answers sessions (blue bars), and the share ofthe Introductory statement dedicated to the policy summary (gray dashed line). Source:Authors computation.

29

Figure 3: The Word Clouds: an overview of the policy summary

expectationsreal

continue

are

financialgrowth

analyses

remains

key

leav

e

upside

stance

assessment

have

monitor

price

riskssupport

policywarranted

appropriate

area

rate

s

inflationlevels

regular

monetary

term

also

basis

remain

interest

accordingly

developmentseconomic

currentdecidedeuro

inflationary

ongoing

strong

stability

outlook

meeting

willlow

accommodative

medium

has

unchanged

2002-2006

linerate

regularrisks

aheadexpectations

leaveinformation

inflation asse

ssm

ent

firmly

creditperiod

willanchored

price

growth

operations

interest

uncertainty

money

euro

term

basis

continue

since

medium

remain

unchanged

policy

meeting

monetary

expect

developments

stability

available

has

areacurrent

have

monitor

rates

financial

remains

analyses

decidedclosely

economic

key

are

2007-2010

aimunchanged

stability

timerisks

continue

underlying

ratepolicy

outlo

ok

regular

close stance

price financial

willdecided

activity

operations

has

firmly

are

infla

tion

measures

refinancing

developments

monetarymedium

remains

havesubdued

economic

expectations

term

rates

maintaining

key

remain

growth

market

necessary

euro

economy

analyses

interest

line

low

areabased

period

2011-2014

Notes: The 50 most frequent words. The size of each word maps the frequency and thecolor the frequency range. Source: Authors computation.

30

Figure 4: Expect VS. Will

0

2

4

6

8

10

12

14

16

18

20

01-0

20

7-0

20

1-0

30

7-0

30

1-0

40

7-0

40

1-0

50

7-0

5

01-0

6

07-0

6

01-0

7

07-0

7

01-0

8

07-0

8

01-0

9

07-0

9

01-1

0

07-1

0

01-1

1

07-1

1

01-1

2

07-1

2

01-1

3

07-1

3

01-1

4

07-1

4weak future strong future

Notes: 2002M1-2014M12. Future forms used in the policy summary. Weak futureindicates decisions likely or possible to happen in the future based on "expect" futureverb tense; Strong future indicates stating decisions based on "will" future verb tense.Source: Authors computation.

31

Figure 5: Yearly average of the Future-Sentiment index (bottom graph) andmonthly monetary policy rate (top graph)

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mo

neta

ry P

olic

y R

ate

0

0,01

0,02

0,03

0,04

0,05

0,06

0,07

0,08

0

0,01

0,02

0,03

0,04

0,05

0,06

0,07

0,08

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Fu

ture

-Sen

tim

en

t

Years

Notes: 2002-2014. FS index based on Eq. 1. Source: Authors computation, Bloomberg.

32

Figure 6: Monthly estimated innovation in Future-Sentiment index

-0,08

-0,06

-0,04

-0,02

0

0,02

0,04

0,06

0,08

0,1

0,12

-0,08

-0,06

-0,04

-0,02

0

0,02

0,04

0,06

0,08

0,1

0,12

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Es

tim

ate

d In

no

va

tio

n i

n F

utu

re S

en

tim

en

t

Notes: 2004M09-2014M12. Monthly estimated innovation in FS index. Source: Authorscomputation.

33

Figure 7: Evolution of the Euribor rate

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

5,5

6,0

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

5,5

6,0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

3 months

6 months

9 months

12 months

1 month

Notes: 2002M12-2014M12. Source: Bloomberg.

34