Embed Size (px)

Citation preview

The information contained herein is based on sources which Phillip Securities (Thailand) believes reliable. We do not guarantee its accuracy or completeness. Opinions and estimates expressed herein are subject to change without notice. This report is for information only and should not be construed as an offer or solicitation for the purchase or sale of any securities referred to herein. We accept no liability for any loss, direct or indirect, from the use of this document. The directors and/or employees of Phillip Securities and or its associates may have an interest in the securities mentioned in the securities mentioned herein. 1

MONTHLY SET STRATEGY: Thai Stock Market Outlook & Stock Picks for May 2017

Strategy TeamMay 2, 2017

Sideways – sideways down

2

Thai stock market outlook for May 2017

Summary Several external factors still need to be closely monitored: External uncertainties may put a lid on the market’s

upside potential and bring a sporadic bout of volatility to the market. Key external factors to watch in the month of May include France’s presidential election, US-North Korea tensions in the Korean peninsula, US Federal Reserve’s tightening cycle and OPEC and non-OPEC output cut extension.

BOT seen staying pat on rates in May: Despite an imminent upward interest rate cycle, we feel the Bank of Thailand’s Monetary Policy Committee will likely leave its benchmark interest rate on hold at 1.5% at its May 24 policy meeting as it may need to take time to assess the impact of changes in economic policies of major global economies on the global economic recovery and the impact of the government’s mega-investment projects on the domestic economy.

Foreign fund outflows still a concern: Foreign fund outflows from Thai equities have continued unabated due partly to the strength of the US dollar driven by the Federal Reserve’s guidance of at least three rate hikes in 2017, US President Donald Trump’s tax reform plan which would lure more funds back to the US and the absence of fresh triggers after the delay in some of the government’s mega-investment projects.

Thai stock market outlook for May: Historical statistics show May is normally a bearish month for Thai stocks like the proverbial saying ‘Sell on May and Go Away.’ Statistics aside, we believe ongoing external uncertainties and a persistent lack of strong positive domestic triggers to take the market higher should leave Thai stocks locked in a sideways/sideways down range this month. Supports are seen at 1530 and 1500 points and resistance at 1580 points.

Interesting theme to play and stock picks in the month of May: With earnings season underway, earnings plays will provide lots of action this month. Here are three good candidates for earnings plays: IRPC, PSTC and WICE.

3

Key external factors to watch

French presidential runoff Geopolitical tensions on Korean peninsula

US rate hike cycle

Far-right leader Marine Le Pen

48 years old

Centrist Emmanuel Macron

39 years old

Source: BloombergPotential OPEC cut extension

It is widely expected that OPEC, which will meet in Vienna on May 25 will extend a global deal to cut oil supplies for another six months until the end of this year. However, the move may provide only a limited boost to oil prices against the backdrop of rising US shale oil production after a steady decline in breakeven cost per barrel to a mere US$40-US$45/barrel in 4QFY16 from US$60-US$65/barrel in 2HFY14. (Source: US Bureau of Labor Statistics, SG Cross Asset Research)

The latest opinion polls showed centrist Emmanuel Macron would still comfortably beat far-right candidate Marine Le Pen by 60% to 40% in the presidential runoff vote on May 7, allaying fears of a possible French exit from the euro zone, the so-called ‘Frexit’ ahead of the election outcome. However, if election polls miss their mark with Le Pen’s victory, it could deal a heavy blow to risk sentiment and trigger another rout in global financial markets on Frexit jitters.

Geopolitical tensions in the Korean peninsula will be one of the key risk factors that need to be closely monitored this month. The back-and-forth rhetoric between US and North Korea has ratcheted up geopolitical tensions in the Korean peninsula especially after the US decision to divert its navy strike group to Korean waters in response to North Korea’s nuclear threat while Pyongyang continues with its ballistic missile tests in a show of power and threatens to sink a US aircraft carrier.

87%

30% 27%15% 14% 11%13%

61% 58%

44% 43%36%

0%9% 14%

34% 35%37%

0%

20%

40%

60%

80%

100%

May-17 Jun-17 Jul-17 Sep-17 Nov-17 Dec-17

0.75%-1% 1%-1.25% 1.25%-1.5%

4

BOT seen leaving rates steady at 1.5%

Source: Bloomberg

Thailand’s inflation is likely to pick up pace to 1.2% in FY17 from 0.2% in FY16 as soaring global oil prices and ERC’s decision to raise the fuel tariff (Ft) by 12.52 satang per KWh for May to Aug 2017 because of rising natural gas and oil prices would drive up inflation in FY17.

Thai policy rates remain moderate compared to other Asian countries.

Uncertainty over changes in economic policies of major global economies which could have a broad implication on the global economy and delays in some of the government’s mega-investment projects may give the BOT an excuse to leave its policy rate on hold at 1.5% at its May 24 policy meeting.

5

Foreign fund outflows still a concern

Foreign fund outflows from Thai equities have continued unabated due partly to the strength of the US dollar driven by the Federal Reserve’s guidance of at least three rate hikes in 2017, US President Donald Trump’s tax reform plan which would lure more funds back to the US and the absence of fresh triggers after the delay in some of the government’s mega-investment projects.

Source: Bloomberg

6

PSR 3-6 months portfolio

7

Current portfolio position

Stocks to be added to portfolio in May 2017 FY17 FV (Bt)

WICE 4.80

IRPC 6.00

PSTC 1.23

BCH8%

CK7%

TACC8%

KTC6%

BANPU8%

BEAUTY8%

MTLS7%

RJH8%

AAV8%

MALEE8%

WICE8%

IRPC8%

PSTC8%

Portfolio Position

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecPSR Port -0.1% -1.9% -1.7% -3.0%SET 2.2% 1.1% 2.1% 1.5%

-5.0%-4.0%-3.0%-2.0%-1.0%0.0%1.0%2.0%3.0%

% R

ET

UR

N (Y

TD

)

Cumulative Return

8

Rebalancing of portfolio holdings for May 2017: Additions

Add

ition

sAdditions Inclusion Date % Weight FV’17 (Bt) P/E (x) P/BV (x) Dividend Yield

IRPC 28 Apr 2017 8.00% 4.80 19.10 2.60 3.66%

PSTC 28 Apr 2017 8.00% 6.00 12.54 1.30 1.96%

WICE 28 Apr 2017 8.00% 1.23 8.89 2.02 4.50%

9

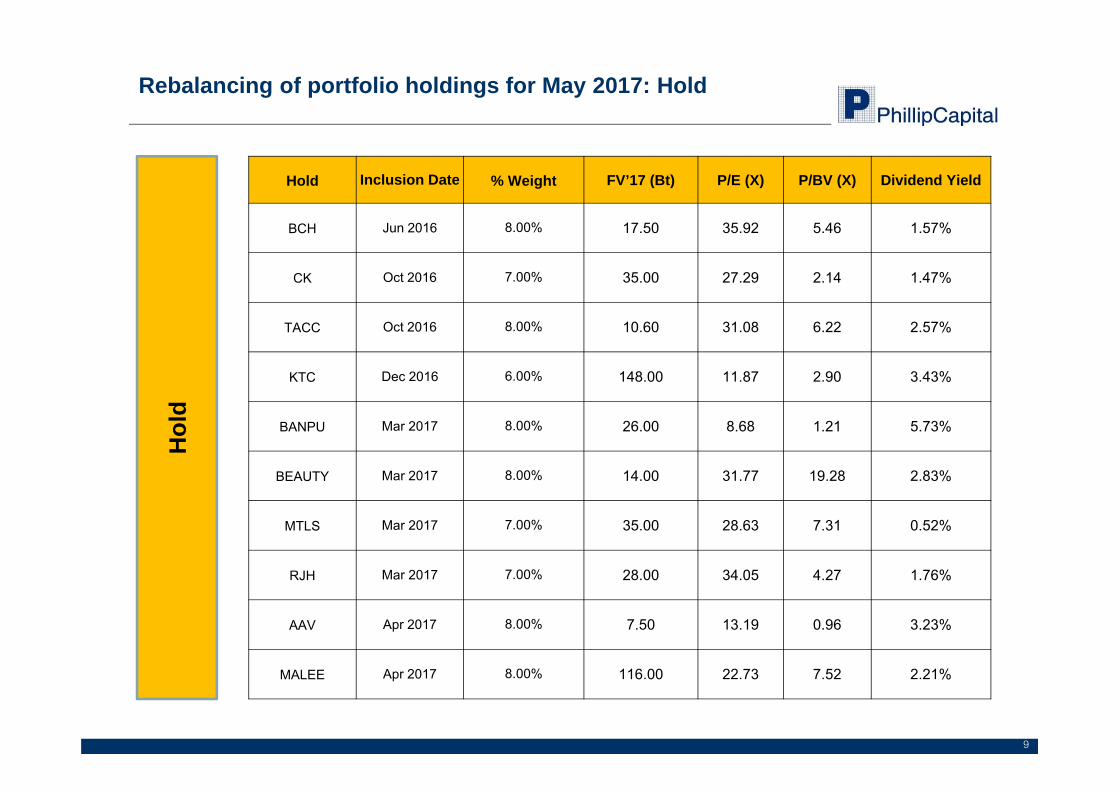

Rebalancing of portfolio holdings for May 2017: Hold

Hol

dHold Inclusion Date % Weight FV’17 (Bt) P/E (X) P/BV (X) Dividend Yield

BCH Jun 2016 8.00% 17.50 35.92 5.46 1.57%

CK Oct 2016 7.00% 35.00 27.29 2.14 1.47%

TACC Oct 2016 8.00% 10.60 31.08 6.22 2.57%

KTC Dec 2016 6.00% 148.00 11.87 2.90 3.43%

BANPU Mar 2017 8.00% 26.00 8.68 1.21 5.73%

BEAUTY Mar 2017 8.00% 14.00 31.77 19.28 2.83%

MTLS Mar 2017 7.00% 35.00 28.63 7.31 0.52%

RJH Mar 2017 7.00% 28.00 34.05 4.27 1.76%

AAV Apr 2017 8.00% 7.50 13.19 0.96 3.23%

MALEE Apr 2017 8.00% 116.00 22.73 7.52 2.21%

10

Rebalancing of portfolio holdings for May 2017: Deletions

Del

etio

ns

Deletions Return(gain/loss) FV’17 (Bt) P/E (X) P/BV (X) Dividend Yield

ROBINS -3.90% 74.00 22.89 3.91 2.11%

IVL +4.99% 41.00 19.60 1.87 2.04%

MAKRO +1.47% 37.75 28.40 9.49 2.64%

11

Investment theme and stock picks for May 2017

12

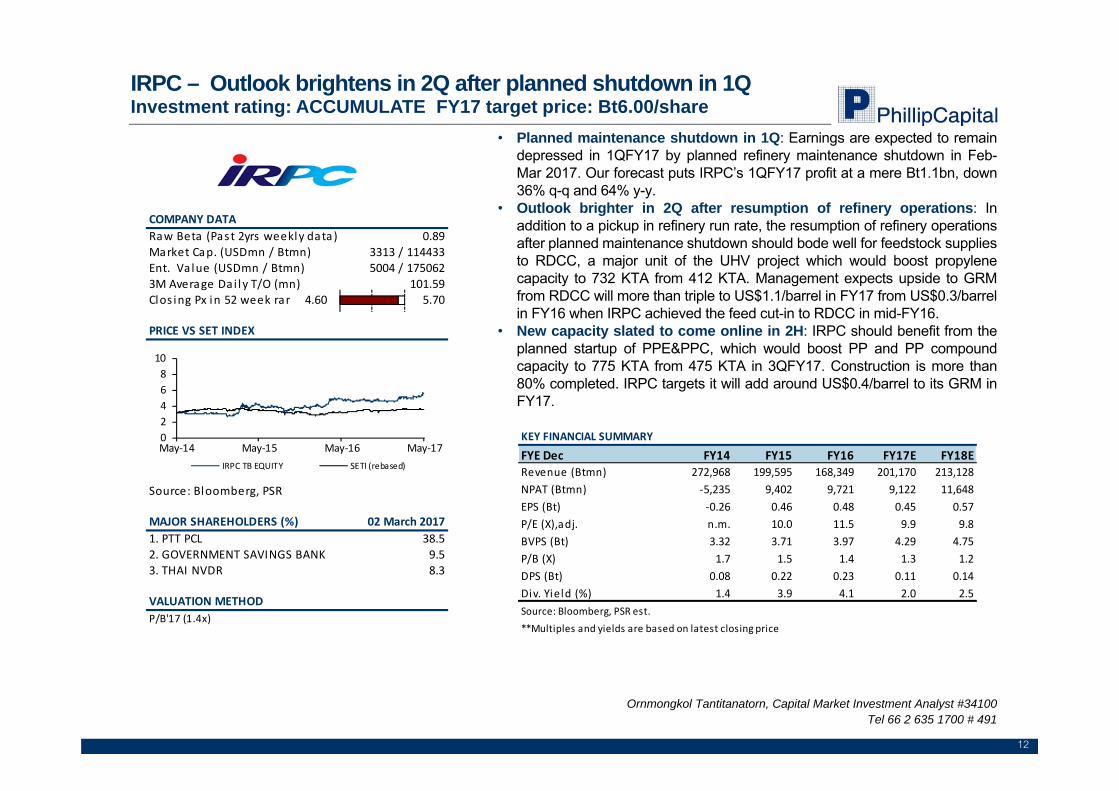

IRPC – Outlook brightens in 2Q after planned shutdown in 1QInvestment rating: ACCUMULATE FY17 target price: Bt6.00/share

• Planned maintenance shutdown in 1Q: Earnings are expected to remain depressed in 1QFY17 by planned refinery maintenance shutdown in Feb-Mar 2017. Our forecast puts IRPC’s 1QFY17 profit at a mere Bt1.1bn, down 36% q-q and 64% y-y.

• Outlook brighter in 2Q after resumption of refinery operations: In addition to a pickup in refinery run rate, the resumption of refinery operations after planned maintenance shutdown should bode well for feedstock supplies to RDCC, a major unit of the UHV project which would boost propylene capacity to 732 KTA from 412 KTA. Management expects upside to GRM from RDCC will more than triple to US$1.1/barrel in FY17 from US$0.3/barrel in FY16 when IRPC achieved the feed cut-in to RDCC in mid-FY16.

• New capacity slated to come online in 2H: IRPC should benefit from the planned startup of PPE&PPC, which would boost PP and PP compound capacity to 775 KTA from 475 KTA in 3QFY17. Construction is more than 80% completed. IRPC targets it will add around US$0.4/barrel to its GRM in FY17.

Ornmongkol Tantitanatorn, Capital Market Investment Analyst #34100 Tel 66 2 635 1700 # 491

KEY FINANCIAL SUMMARY

FYE Dec FY14 FY15 FY16 FY17E FY18ERevenue (Btmn) 272,968 199,595 168,349 201,170 213,128NPAT (Btmn) ‐5,235 9,402 9,721 9,122 11,648EPS (Bt) ‐0.26 0.46 0.48 0.45 0.57P/E (X),adj. n.m. 10.0 11.5 9.9 9.8BVPS (Bt) 3.32 3.71 3.97 4.29 4.75P/B (X) 1.7 1.5 1.4 1.3 1.2DPS (Bt) 0.08 0.22 0.23 0.11 0.14Div. Yield (%) 1.4 3.9 4.1 2.0 2.5Source: Bloomberg, PSR est.**Multiples and yields are based on latest closing price

COMPANY DATARaw Beta (Past 2yrs weekly data) 0.89Market Cap. (USDmn / Btmn) 3313 / 114433Ent. Value (USDmn / Btmn) 5004 / 1750623M Average Dai ly T/O (mn) 101.59Clos ing Px in 52 week ran 4.60 5.70

PRICE VS SET INDEX

Source: Bloomberg, PSR

MAJOR SHAREHOLDERS (%)1. PTT PCL 38.52. GOVERNMENT SAVINGS BANK 9.53. THAI NVDR 8.3

VALUATION METHODP/B'17 (1.4x)

02 March 2017

0246810

May‐14 May‐15 May‐16 May‐17IRPC TB EQUITY SETI (rebased)

13

PSTC – Q-Q profit turnaround expected in 1QFY17 Investment rating: BUY FY17 target price: Bt1.23/share

• Q-Q profit turnaround expected in 1QFY17: We expect PSTC will swing back to a net profit of Bt45mn in 1QFY17 from a net loss in 4QFY16 after some of its power plants which had been shut for maintenance in 2HFY16 were back in operation in 1QFY17 and exceptional expenses related to machinery upgrade would drop sharply.

• Profit poised for record in FY17: Our forecast shows PSTC’s net profit will hit a fresh record of Bt391mn in FY17, underpinned by full-year revenue contribution from solar, biomass and biogas power plants with a combined total capacity of 29.7 MW and new capacity additions of another 12.6 MW slated to come online in FY17.

• Potential upside from pipeline of projects under ERC plan in FY17: In our view, there remains an upside risk to the outlook from potential new capacity additions to its current portfolio of 46.3 MW as PSTC plans to take part in other new renewable energy projects under ERC’s plan to buy more than 1,000 MW of renewable power in FY17. The 2nd phase of the Agro-Solar Project with 219 MW up for grabs through a lucky draw process in May-Jun is one of the potential projects for the meantime.

Thanatphat Suksrichavalit, Securities Investment Analyst #84741Tel 66 2 635 1700 # 532

COMPANY DATARaw Beta (Past 2yrs weekly data) 1.37Market Cap. (USDmn / Btmn) 100 / 3457Ent. Value (USDmn / Btmn) 138 / 48293M Average Dai ly T/O (mn) 32.30Clos ing Px in 52 week ran 0.41 0.89

PRICE VS MAI INDEX

Source: Bloomberg, PSR

MAJOR SHAREHOLDERS (%)1.Mr.Soammaphat Tra isorat 12.02.Mrs .Wal lapa Tra isorat 11.53.Mr.Pharana i Gengvanrat 9.2

VALUATION METHODSOTP

04 April 2017

0

1

2

3

May‐14 May‐15 May‐16 May‐17PSTC TB EQUITY MAII (rebased)

KEY FINANCIAL SUMMARY

FYE Dec FY14 FY15 FY16 FY17E FY18ERevenue (Btmn) 424 480 599 1,818 2,757NPAT (Btmn) 39 15 ‐39 391 557EPS (Bt) 0.017 0.007 ‐0.009 0.088 0.126P/E (X),adj. 45.5 119.0 n.m. 8.9 6.2BVPS (Bt) 0.23 0.24 0.31 0.39 0.47P/B (X) 3.4 3.2 2.5 2.0 1.6DPS (Bt) 0.0074 0.0018 0.0000 0.0351 0.0504Div. Yield (%) 0.9 0.2 0.0 4.5 6.5Source: Bloomberg, PSR est.**Multiples and yields are based on latest closing price

14

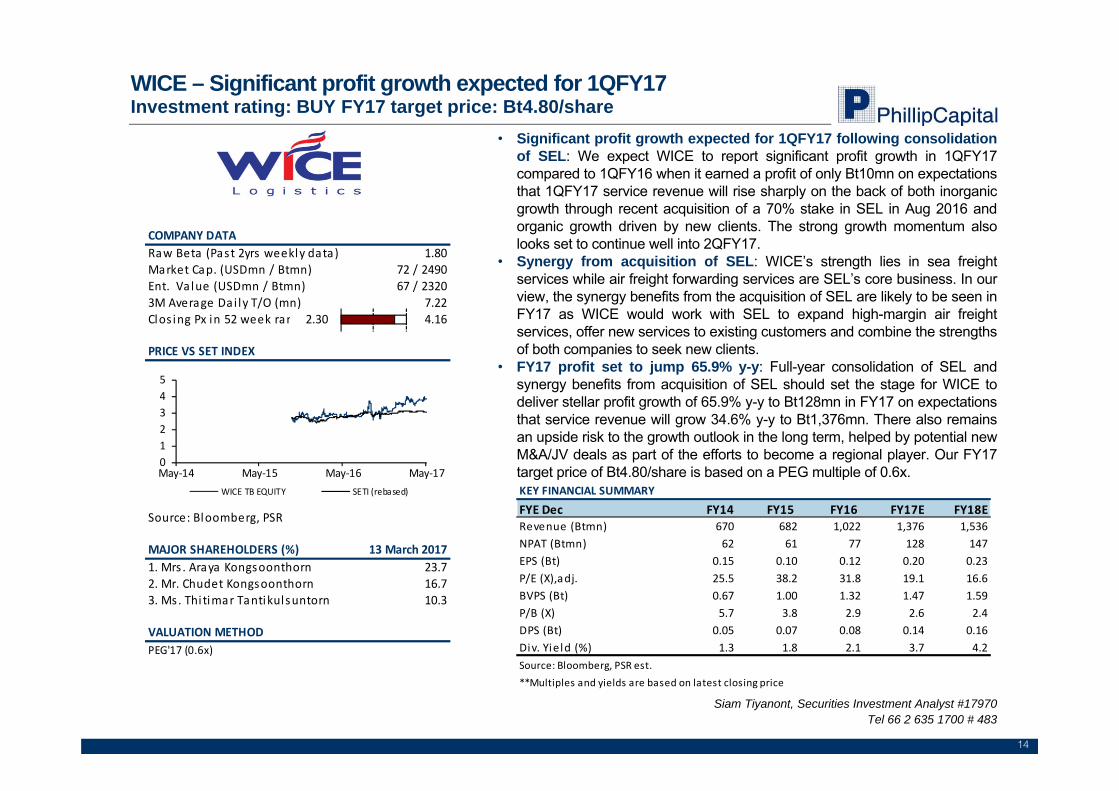

WICE – Significant profit growth expected for 1QFY17 Investment rating: BUY FY17 target price: Bt4.80/share

• Significant profit growth expected for 1QFY17 following consolidation of SEL: We expect WICE to report significant profit growth in 1QFY17 compared to 1QFY16 when it earned a profit of only Bt10mn on expectations that 1QFY17 service revenue will rise sharply on the back of both inorganic growth through recent acquisition of a 70% stake in SEL in Aug 2016 and organic growth driven by new clients. The strong growth momentum also looks set to continue well into 2QFY17.

• Synergy from acquisition of SEL: WICE’s strength lies in sea freight services while air freight forwarding services are SEL’s core business. In our view, the synergy benefits from the acquisition of SEL are likely to be seen in FY17 as WICE would work with SEL to expand high-margin air freight services, offer new services to existing customers and combine the strengths of both companies to seek new clients.

• FY17 profit set to jump 65.9% y-y: Full-year consolidation of SEL and synergy benefits from acquisition of SEL should set the stage for WICE to deliver stellar profit growth of 65.9% y-y to Bt128mn in FY17 on expectations that service revenue will grow 34.6% y-y to Bt1,376mn. There also remains an upside risk to the growth outlook in the long term, helped by potential new M&A/JV deals as part of the efforts to become a regional player. Our FY17 target price of Bt4.80/share is based on a PEG multiple of 0.6x.

Siam Tiyanont, Securities Investment Analyst #17970Tel 66 2 635 1700 # 483

KEY FINANCIAL SUMMARY

FYE Dec FY14 FY15 FY16 FY17E FY18ERevenue (Btmn) 670 682 1,022 1,376 1,536NPAT (Btmn) 62 61 77 128 147EPS (Bt) 0.15 0.10 0.12 0.20 0.23P/E (X),adj. 25.5 38.2 31.8 19.1 16.6BVPS (Bt) 0.67 1.00 1.32 1.47 1.59P/B (X) 5.7 3.8 2.9 2.6 2.4DPS (Bt) 0.05 0.07 0.08 0.14 0.16Div. Yield (%) 1.3 1.8 2.1 3.7 4.2Source: Bloomberg, PSR est.**Multiples and yields are based on latest closing price

COMPANY DATARaw Beta (Past 2yrs weekly data) 1.80Market Cap. (USDmn / Btmn) 72 / 2490Ent. Value (USDmn / Btmn) 67 / 23203M Average Dai ly T/O (mn) 7.22Clos ing Px in 52 week ran 2.30 4.16

PRICE VS SET INDEX

Source: Bloomberg, PSR

MAJOR SHAREHOLDERS (%)1. Mrs . Araya Kongsoonthorn 23.72. Mr. Chudet Kongsoonthorn 16.73. Ms. Thi timar Tantikulsuntorn 10.3

VALUATION METHODPEG'17 (0.6x)

13 March 2017

012345

May‐14 May‐15 May‐16 May‐17WICE TB EQUITY SETI (rebased)

15

Sector update

16

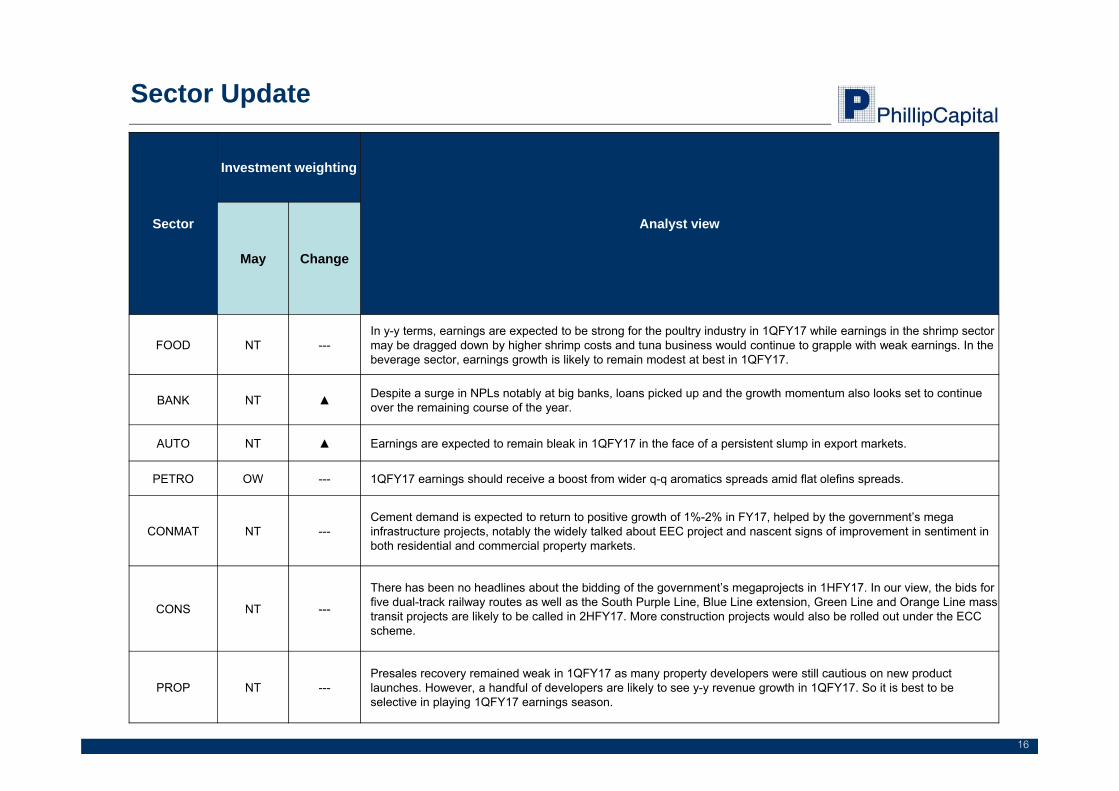

Sector Update

Sector

Investment weighting

Analyst view

May Change

FOOD NT ---In y-y terms, earnings are expected to be strong for the poultry industry in 1QFY17 while earnings in the shrimp sector may be dragged down by higher shrimp costs and tuna business would continue to grapple with weak earnings. In the beverage sector, earnings growth is likely to remain modest at best in 1QFY17.

BANK NT ▲ Despite a surge in NPLs notably at big banks, loans picked up and the growth momentum also looks set to continue over the remaining course of the year.

AUTO NT ▲ Earnings are expected to remain bleak in 1QFY17 in the face of a persistent slump in export markets.

PETRO OW --- 1QFY17 earnings should receive a boost from wider q-q aromatics spreads amid flat olefins spreads.

CONMAT NT ---Cement demand is expected to return to positive growth of 1%-2% in FY17, helped by the government’s mega infrastructure projects, notably the widely talked about EEC project and nascent signs of improvement in sentiment in both residential and commercial property markets.

CONS NT ---

There has been no headlines about the bidding of the government’s megaprojects in 1HFY17. In our view, the bids for five dual-track railway routes as well as the South Purple Line, Blue Line extension, Green Line and Orange Line mass transit projects are likely to be called in 2HFY17. More construction projects would also be rolled out under the ECC scheme.

PROP NT ---Presales recovery remained weak in 1QFY17 as many property developers were still cautious on new product launches. However, a handful of developers are likely to see y-y revenue growth in 1QFY17. So it is best to be selective in playing 1QFY17 earnings season.

17

Sector Update

Sector

Investment weighting

Analyst viewMay Change

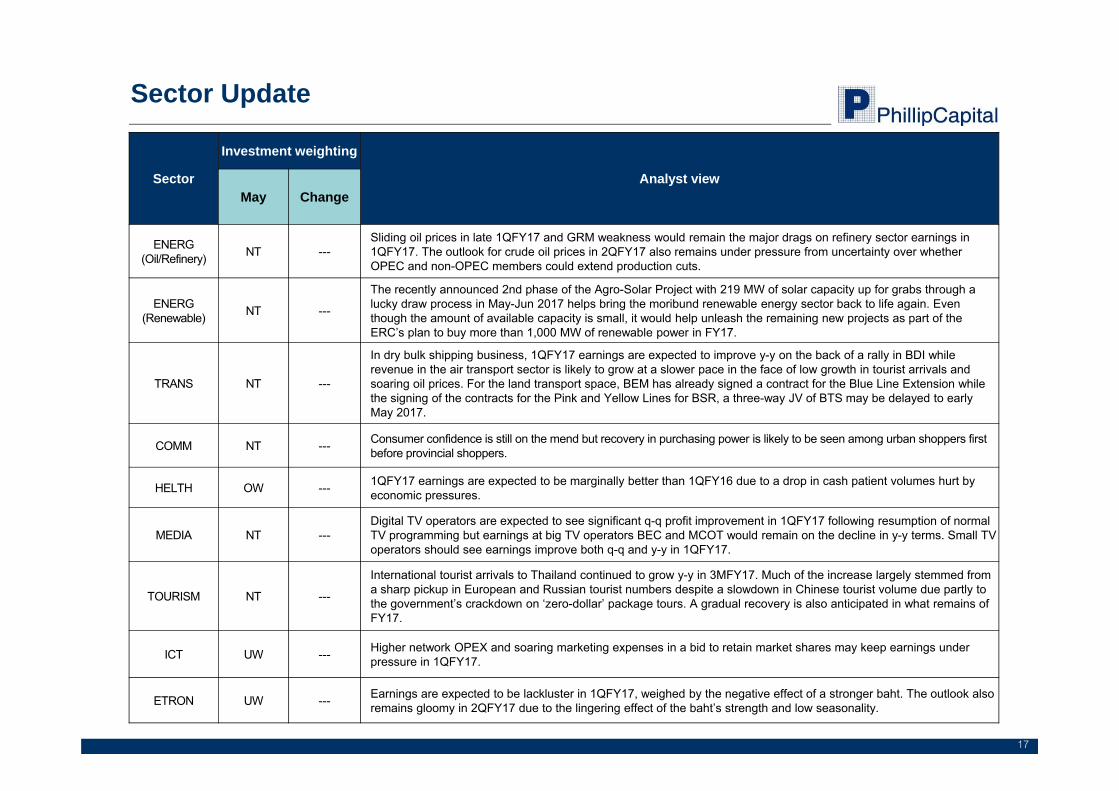

ENERG(Oil/Refinery) NT ---

Sliding oil prices in late 1QFY17 and GRM weakness would remain the major drags on refinery sector earnings in 1QFY17. The outlook for crude oil prices in 2QFY17 also remains under pressure from uncertainty over whether OPEC and non-OPEC members could extend production cuts.

ENERG(Renewable) NT ---

The recently announced 2nd phase of the Agro-Solar Project with 219 MW of solar capacity up for grabs through a lucky draw process in May-Jun 2017 helps bring the moribund renewable energy sector back to life again. Even though the amount of available capacity is small, it would help unleash the remaining new projects as part of the ERC’s plan to buy more than 1,000 MW of renewable power in FY17.

TRANS NT ---

In dry bulk shipping business, 1QFY17 earnings are expected to improve y-y on the back of a rally in BDI while revenue in the air transport sector is likely to grow at a slower pace in the face of low growth in tourist arrivals and soaring oil prices. For the land transport space, BEM has already signed a contract for the Blue Line Extension while the signing of the contracts for the Pink and Yellow Lines for BSR, a three-way JV of BTS may be delayed to early May 2017.

COMM NT --- Consumer confidence is still on the mend but recovery in purchasing power is likely to be seen among urban shoppers first before provincial shoppers.

HELTH OW --- 1QFY17 earnings are expected to be marginally better than 1QFY16 due to a drop in cash patient volumes hurt by economic pressures.

MEDIA NT ---Digital TV operators are expected to see significant q-q profit improvement in 1QFY17 following resumption of normal TV programming but earnings at big TV operators BEC and MCOT would remain on the decline in y-y terms. Small TV operators should see earnings improve both q-q and y-y in 1QFY17.

TOURISM NT ---

International tourist arrivals to Thailand continued to grow y-y in 3MFY17. Much of the increase largely stemmed from a sharp pickup in European and Russian tourist numbers despite a slowdown in Chinese tourist volume due partly to the government’s crackdown on ‘zero-dollar’ package tours. A gradual recovery is also anticipated in what remains of FY17.

ICT UW --- Higher network OPEX and soaring marketing expenses in a bid to retain market shares may keep earnings under pressure in 1QFY17.

ETRON UW --- Earnings are expected to be lackluster in 1QFY17, weighed by the negative effect of a stronger baht. The outlook also remains gloomy in 2QFY17 due to the lingering effect of the baht’s strength and low seasonality.

18

Key factors to watch in the month of May 2017

19

Economic calendar for May 2017

Source: Bloomberg

May 1 May 2 May 3 May 4 May 5 May 6 May 7US: Markit

Manufacturing PMI, ISM Manufacturing

EU: Markitmanufacturing PMI, unemployment

TH: CPI

US: ADP employment, Markit PMI, Markit servicesPMI, ISM non-manufacturing

EU: GDP

US: FOMCEU: Markit PMI,

Markit services PMI

US: Nonfarm payrolls, unemployment

May 8 May 9 May 10 May 11 May 12 May 13 May 8 CN: Exports,

imports

CN: PPI, CPI US: PPI, core PPI

US: CPIEU: Industrial

production

May 15 May 16 May 17 May 18 May 19 May 20 May 21CN: Retail salesTH: GDP

TH: MSCI May semi-annual index review announcement

EU: CPI

20

Economic calendar for May 2017

Source: Bloomberg

May 22 May 23 May 24 May 25 May 26 May 27 May 28

US: Existing homes sales

TH: MPC rate decision

May 29 May 30 May 31

TH: Exports, imports

TH: Implementation date for MSCI May semi-annual index review

Contact Information of Hong Kong Representatives

Research

Benny WANG

Dealing Director

(852) 2277 6720

ZHANG Jing

Research Analyst

Transportation and Automobiles

(86) 21 51699400-103

John WONG

Research Analyst

HK & Mainland Properties, Hotels &

Entertainment

(852) 2277 6527

Sales

Aric AU

Manager, Corporate & Institutional Sales

(852) 2277 6783

FAN Guohe

Research Analyst

Pharmaceutical, Health & Personal Care, TMT

(86) 21 51699400-110

WANG Yannan

Research Analyst

New Energy

(86) 21 51699400-107

Matthew WONG

Manager, International Sales

(852) 2277 6678

Tim WONG

Research Analyst

Utilities

(852) 2277 6516

Ocean PAN

Research Analyst

Industrial Goods, Textiles &

Clothing, Basic Materials

(852) 2277 6515

Yoshikazu SHIKITA

Manager, International Sales

(Japan Team)

(852) 2277 6624

PHILLIP RESEARCH STOCK SELECTION SYSTEMS

Total Return Recommendation Rating Remarks

> +20% Buy 1 >20% upside from the current price

+5% to +20% Accumulate 2 +5% to +20% upside from the current price

-5% to +5% Neutral 3 Trade within +/- 5% from the current price

-5% to -20% Reduce 4 -5% to -20% downside from the current price

< -20% Sell 5 -20% downside from the current price

We do not base our recommendations entirely on the above quantitative return bands. We consider qualitative factors like (but not limited to) a stock’s risk reward

profile, market sentiment, recent rate of share price appreciation, presence or absence of stock price catalysts, and speculative undertones surrounding the stock,

before making our final recommendation

GENERAL DISCLAIMER

This publication is distributed in Hong Kong by Phillip Securities (Hong Kong) Limited (“PSHK”), which is licensed in Hong Kong by the Securities and

Futures Commission for regulated activities, including Type 4 regulated activity (advising on securities). This publication was originally prepared by analysts

from our overseas affiliates. The information contained herein is based on sources that PSHK and its affiliates believe to be accurate and any analysis, forecasts,

projections, expectations and opinions contained in this publication are based on such information and are expressions of belief only. This material is prepared for

general circulation to clients and is not intended to provide tailored investment advice and does not take into account the individual financial situation and

objectives of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness of any investments or securities

discussed or recommended in this report. This report is not (and should not be construed as) a solicitation to act as securities broker or dealer in any jurisdiction by

any person or company that is not legally permitted to carry on such business in that jurisdiction. This research report may not be redistributed, retransmitted or

disclosed, in whole or in part or and any form or manner, without the express written consent of PSHK. Please direct any enquiries to

Investment involves risks. For details of product risks, please view the Risk Disclosures Statement on http://www.phiIlip.com.hk.

PhillipCapital's Global Presence

SINGAPORE JAPAN

Phillip Securities Pte Ltd PhillipCapital Japan K.K.

HONG KONG CHINA

Phillip Securities (HK) Ltd Phillip Financial Advisory (Shanghai) Co. Ltd

INDONESIA FRANCE

PT Phillip Securities Indonesia King & Shaxson Capital Ltd

THAILAND UNITED STATES

Phillip Securities (Thailand) Public Company Limited Phillip Futures Inc.

~

UNITED KINGDOM

King & Shaxson Capital Ltd

AUSTRALIA

Phillip Capital Australia

MALAYSIA

Phillip Capital Management Sdn Bhd