Embed Size (px)

Citation preview

Classification: Confidential (C-3)

Monthly Economic Insight

Prepared by TMB Analytics

Date: 13 July 2017

Executive Summary

Better-than-expected Eurozone economy remained a solid driver for global economic outlook

which reflected by resilient manufacturing and services industry activities (higher PMI

figures). Additionally, the US manufacturing sector also showed sign of stronger expansion.

Nevertheless, there were persisting downside risks such as Brexit talk, “early” Italian election

and uncertainty of Trumponomics which could disrupt worldwide economic activities and

recovering global trades.

In May, the Thai economy continued to expand well as the ongoing recovery in external

demand and the growing tourism sector while the private investment remained fragile.

Private consumption continued to expand, supported by improvement in farm income, while

private investment remained contracted albeit improvement in business sentiment.

May exports surged by 13.2% mainly due to global economic recovery, while the effect of oil

price was starting to dissipate. Most of export products registered positive growth, indicating

product diversification and upward trends of global exports. Imports of raw material and

capital goods continued to grow at the high level of 18.2%, responding to a continuing

economic and export expansion.

-2-

Executive Summary

Manufacturing production increased +1.4%yoy in May, thanks to higher outputs of food,

electronic, vehicle and part supported by export market recovery. However, beverages in

alcohol product dropped due to gov’t will charging more excise tax, as well as construction

material declined from low demand in real estate sector.

Tourist attracted 2.59 million international visitors in May (+5%yoy) and monthly receipts

were 125 billion Baht (+6.9%yoy), these attributed from Chinese rebound to “Growth” zone

faster than forecast. During first five months, inbound tourists were recorded by 14.6 million

arrivals (+3.2%yoy) and the accumulation of oversea revenue generated 747 billion

(+5.1%yoy), showing that sector be able to grow right on target.

Inflation rate in June slowed down further to -0.05% due to high base effect from last year

drought. In 2017, 1.50% Policy rate is expected due to weak private investment and fragile

export recovery.

In the past month, Thai baht appreciated against the USD by 0.27% due to unclear path of

Trumponomics and future Fed’s rate hike. Fed and other central banks’ actions to start

reducing easing monetary policy later this year, could boost fund outflows from Thailand . In

near term, the dollar is expected to trade near 34.30 THB/USD in the 3rd Quarter of 2017.-3-

Classification: Confidential (C-3)

Economic Updates

Updates on Global Economy

Updates on Thai Economy

Classification: Confidential (C-3)Classification: Confidential (C-3)

Global Economy

1H2017 2H2017

EM risk-off

High corporate debt

Fed funds rate hike

UK trigger Article

50

Fed fund rate hike

Return of private investment

German

Election

0.75 to 1.00

French

Election

-6-

Debt Ceiling is back

Fed fund rate hike

1.00 to 1.251.25 to 1.50

UK

Election

Italy

Election

1Q2018

Era of Rising Interest Rate and Series of Elections

1H2017 2H2017

UK trigger Article

50 German

Election

French

Election

-7-

Theresa May

failed to win

majority in

parliament (317/650 seats)

UK

ElectionItaly

Election

1Q2018

“Bye Bye EUSee you (Softer)Hard Brexit”

“En Marche!” (Forward!)

“Progressive Movement”

Emmanuel Macron beat Marine Le Pen in presidential election

and won 350/577 seats in parliament

Angela Merkel’s

CDU/CSU* party is

expected to win

40% of votes

according to opinion polls

5 stars movement

party is losing popularity

Dutch

Election

Mark Rutte beat

Geert Wilders,

destroyed hope for Nethexit

*CDU = Christian Democratic Union of Germany

*CSU = Christian Social Union in Bavaria

Political Risk Subsided as Eurosceptic Lost in Elections

Classification: Confidential (C-3) -8-Source: Bloomberg, CEIC, and TMB Analytics

5

10

15

20

25

30EURUSD Volatility

GBPUSD Volatility

%

Fear of

Brexit

Brexit

Vote

Article50

Triggered

French

Election

UK Snap

election

EU FX Volatility Varied by Series of Political Risks

Source: ING and TMB Analytics -9-

Possible “Softer” Hard Brexit Talk

“Bye Bye EUSee you (Softer)Hard Brexit”

March 2017

March 2019

UK leaves EU

EU finalizes “divorce”

term with UK

1-3 Months

6-8 Months

10-11 Months

4-5 Months

Preparation

time

Future deals between

UK and EU negotiation

27 individual EU members

will ratify the deal

It will still take about 2 years to formally divorce EU as the talk could be less intense.

UK General Election June 8th 2017

-10-

Funding

Source: Bloomberg, ING, GovTrack, RealClearPolitics, FlatIcon, CBO, Wikipedia, and TMB Analytics

“39% of R-Congress are very Conservative … They will oppose my great plans !!!”

Trumpcare

Delayed!!

Tax Reform Infrastructure

Will also be Delayed!!

+0.3 Trillion USD over 10 years

Border

Adjustment Tax

-1 Trillion USD over 10 years

-1.2 Trillion USD over 10 years

+1.0 Trillion USD over 10 years

Trumponomics Likely Brings Disappointment This Year

Trump’s great stimulus plan timelines will be extended longer than market’s expectations as Healthcare reforms was delayed indefinitely.

Classification: Confidential (C-3) -11-Source: Fed, ECB, BOJ, Bloomberg, CEIC, and TMB Analytics

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

Fed B/S

ECB B/S

BOJ B/S

Trillion USD

Fed QE

Fed Tightening & Balance sheet reduction

BOJ QE

ECB QE

Dec-17

4.37

Trillion USD

4.40

Trillion USD

4.5

Trillion USD

Global B/S have been Swollen by Quantitative Easing

-12-Source: Fed, BoJ, ECB, Bloomberg and TMB Analytics

Short-term rate: Fed Fund

Dovish Hawkish

Short-term rate: Refin RateDovish Hawkish

Short-term rate: PR-BalancesDovish Hawkish

2H/2017 1H/2018 2H/2018

FED

BOJ

ECB

1 Rate Hike 1 Rate Hike 1 Rate Hike

Start B/S run-off

$ -10 bn $ -20 bn $ -30 bn $ -40 bn $ -50 bn

0 Rate Hike 0 Rate Hike 1 Rate Hike

Start QE Tapering

EUR 60 bn EUR 40 bn

0 Rate Hike 0 Rate Hike 0 Rate Hike

Start QE Tapering

JPY 80 Trillion / year

EUR 20 bn

JPY 60 Trillion / year JPY 40 Trillion / year

Major Central Banks could be More Hawkish Next Year

70

101

178

6.4

6.8

7.2

7.6

0

50

100

150

200

2017 2018 2019

Average 5YCorporatebond yield

-13-Source: Bloomberg, PBOC, TradingEconomics and TMB Analytics; as of June 17

China Corporate Debt: Ticking Time-Bomb

Rollover Risk Looms As Cost of Funds RiseCorporate debt is absurdly high (156% of GDP)

%to GDP

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17

Shadow loans MoMBank loans MoM

PBOC’s loans tightening spur shadow loans

Billion Yuan

3

24

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014 2015 2016

Trillion Yuan

Shadow banking loans keep swelling up

Billion Yuan

Yearly amount due

on Corporate Bond

rated AA- or lower

Shadow loans = 13% of total debt

%

100156

73 85

160

257

0

100

200

300

400

500

600

2008 2016 2016 2016

Corporate Debt Household Debt

Bank Debt Government Debt

95

100

105

110

115

120

125

130

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17

SET

S&P500

-100

-50

0

50

100

150

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17

ST Bonds (TTM < 1y) LT Bonds Net Equity Foreign Flows

-14-Source: CEIC and TMB Analytics

Risk of Fund Flow Reversal ?

bn.THB

Allocations move from

DM to EM; debt to

equity as Brexit and Fed hike delay

Foreign fund continuously flows into Thailand as US election reflected higher risk appetite

EM outflows

from fear of

trade protectionism

Inflows to EM

from unclear Trumponomics

Fear of Trump’s victory

Reflationary

Theme boost “Risk-Appetite”

YTD Net Inflows = 135 bn. THB

-15-Source: CEIC and TMB Analytics

The Market Vs. The Fed: Who Will be Right?

The Fed remain faithful that economic growth and inflation will be picked up but the market seem to

disagree with the Fed. Delayed Trumponomics decimated “Reflation traders”.

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

'98 '01 '04 '07 '10 '13 '16

UST10Y-UST2Y

200D-Moving Average

50D-Moving Average

90% of Dead Cross

signal followed by a deep dive in yields spread

Inverted Yields Curve is a

good predictor of economic slowdown

%Dead Cross signal

Inverted

yields curve

Trump presidency

ignited “A New Hope on Reflation”

Weak economic data and

concerns over pro-growth agenda led to bond inflows

45.0

50.0

55.0

60.0

Jun-14 Jun-15 Jun-16 Jun-17

EU_Service_PMI

EU_Mfg_PMI

-16-

New US government

policies create more

volatility to economic

projections

Subdued inflation could be

persist until consumer

spending grows stronger

Economy is projected to

expand 2.0% in 2017 from

1.6% in 2016

United States Eurozone

Activity

1.2%QoQ SAAR Real

GDP 1Q17

Price

1.9%YoY SA CPI

May 17

Labor Mkt

4.4%Unemployment

Rate June 17

UK economy expands more

than expected, eases fears of

economic ramifications from

Brexit

Stronger expansion among

manufacturing and service

sectors sustain EU’s growth

Growth in 2017 is expected

to be around +1.8% better

than +1.6% in 2016

EU Activity

1.7%YoY SWDA GDP 1Q17

UK Activity

Industry

Latest Releases Latest Releases

Source: Bloomberg, and TMB Analytics’ projection

2.0%YoY SWDA GDP 1Q17

57.4EU Mfg PMI

June 17

Flattening yields curve could hint market top Steady Recovery in EU Manufacturing & Services

Solid Growth Momentum Among Developed Economies

(bps)

↑ Expansion

↓ Contraction

-100

-50

0

50

100

150

200

250

300

200.0

700.0

1,200.0

1,700.0

2,200.0

Mar-90 Mar-96 Mar-02 Mar-08 Mar-14

S&P500 (LHS)

UST10Y-UST2Y (RHS)

-17-Source: Bloomberg, and TMB Analytics’ projection

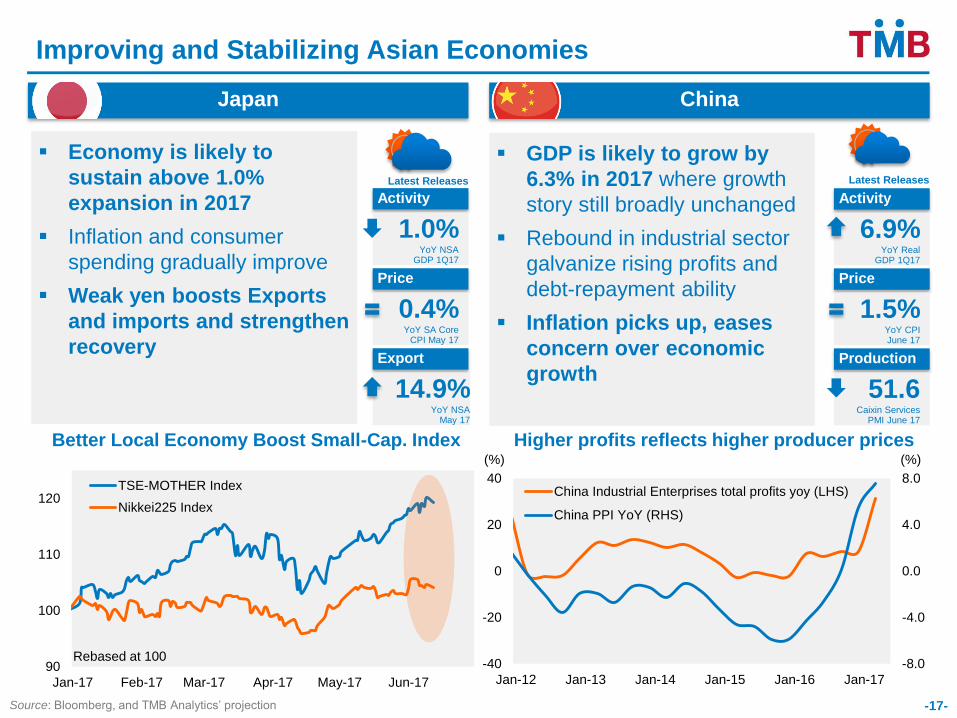

Economy is likely to

sustain above 1.0%

expansion in 2017

Inflation and consumer

spending gradually improve

Weak yen boosts Exports

and imports and strengthen

recovery

Japan China

Activity

1.0%YoY NSA

GDP 1Q17

Price

0.4%YoY SA Core

CPI May 17

Export

14.9%YoY NSA

May 17

GDP is likely to grow by

6.3% in 2017 where growth

story still broadly unchanged

Rebound in industrial sector

galvanize rising profits and

debt-repayment ability

Inflation picks up, eases

concern over economic

growth

Activity

6.9%YoY Real

GDP 1Q17

Price

1.5%YoY CPI June 17

Production

51.6Caixin Services

PMI June 17

Higher profits reflects higher producer prices

Latest Releases Latest Releases

Better Local Economy Boost Small-Cap. Index

Improving and Stabilizing Asian Economies

(%)(%)

-8.0

-4.0

0.0

4.0

8.0

-40

-20

0

20

40

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

China Industrial Enterprises total profits yoy (LHS)

China PPI YoY (RHS)

90

100

110

120

Jan-17 Feb-17 Mar-17 Apr-17 May-17 Jun-17

TSE-MOTHER Index

Nikkei225 Index

Rebased at 100

45

50

55

60

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

Japan Services

China Services

45

50

55

60

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

US Services

EU Services

45

50

55

60

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

China Manufacturing

Japan Manufacturing

45

50

55

60

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

US Manufacturing

EU Manufacturing

-18-Source: Bloomberg, PBOC, TradingEconomics and TMB Analytics; as of June 17

Steady Rise in EU Industry Activities while US loses Momentum

Industry activities in Japan start to rise steadilyEU Manufacturing sector continues to expand

No problem in Big Economies’ services sectors Japan Services finally escape from contraction

↑ Expansion

↓ Contraction

↑ Expansion

↓ Contraction

-100

-50

0

50

100

150

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17

ST Bonds (TTM < 1y) LT Bonds Net Equity Foreign Flows

-19-Source: Bloomberg, CEIC and TMB Analytics

bn.THB

Allocations move from

DM to EM; debt to

equity as Brexit and Fed hike delay

EM outflows

from fear of

trade protectionism

Inflows to EM

from unclear Trumponomics

YTD Net Inflows = 166 bn. THB

Equity = 13 bn. THBBond = 153 bn. THB

-5

5

15

25

35

South Korea China Indonesia Thailand Phillippines Malaysia

Equity Bond

bn.USD

Thailand

Risk of Fund Flow Reversal ?

Foreign fund continuously flows into Thailand as US election reflected higher risk appetite

Year to date foreign fund flows into Asian mainly go into bond markets

Source: CEIC and TMB Analytics; as of June 2017 -20-

33.0

34.0

35.0

36.0

37.0

Oct-

16

De

c-1

6

Feb

-17

Ap

r-1

7

Ju

n-1

7

Aug-1

7

Oct-

17

De

c-1

7

Trump presidency leads to EM sell-off

1 Hikes & Trump Disappointed

34.30

Fed hiked policy rate by

25bps and planned to raise the rate 75bps in 2017

CBs’ Aggressive & Trumponomics

Strong

Thai Baht

Weak

Thai Baht

Other Central Banks Reduce QE, Rate hike

Pro-growth Trumponomics

Fed’s Tightening Cycle with B/S reduction

Trump “Too Strong Dollar”

Robust Thai economy and high C/A surplus

Geopolitical Risks

EM Risk-Off

THB

Risk Factors

2 Fed Hikes and B/S reduction in September

+ Pro-growth agendas pass congress

+ ECB communicate QE tapering

35.00

1 Fed Hikes and B/S reduction in December 2017Trump budgets less than what he proposes

33.90period-end

Improving Domestic Fundamentals Lessen Baht’s Depreciation

-21-

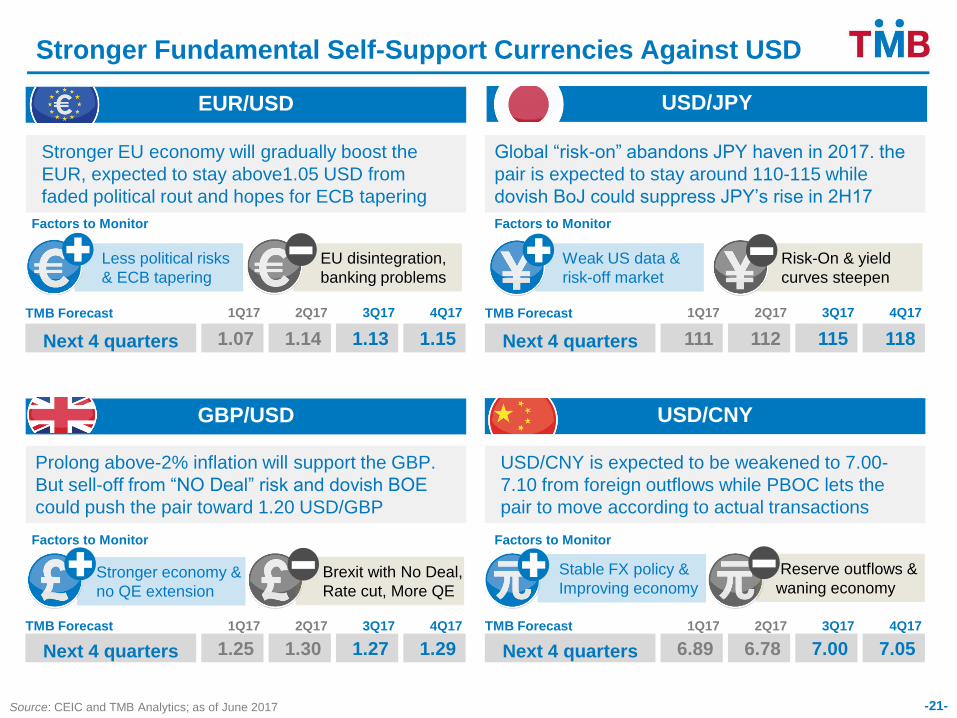

Stronger Fundamental Self-Support Currencies Against USD

Prolong above-2% inflation will support the GBP.

But sell-off from “NO Deal” risk and dovish BOE

could push the pair toward 1.20 USD/GBP

GBP/USD

1.291.271.301.25Next 4 quarters

4Q173Q172Q171Q17TMB Forecast

USD/CNY is expected to be weakened to 7.00-

7.10 from foreign outflows while PBOC lets the

pair to move according to actual transactions

USD/CNY

7.057.006.786.89Next 4 quarters

4Q173Q172Q171Q17TMB Forecast

Stronger EU economy will gradually boost the

EUR, expected to stay above1.05 USD from

faded political rout and hopes for ECB tapering

EU disintegration,

banking problems

Less political risks

& ECB tapering

EUR/USD

1.151.131.141.07Next 4 quarters

4Q173Q172Q171Q17TMB Forecast

Global “risk-on” abandons JPY haven in 2017. the

pair is expected to stay around 110-115 while

dovish BoJ could suppress JPY’s rise in 2H17

Risk-On & yield

curves steepen

Weak US data &

risk-off market

118115112111Next 4 quarters

4Q173Q172Q171Q17TMB Forecast

USD/JPY

Brexit with No Deal,

Rate cut, More QE

Stronger economy &

no QE extension

Reserve outflows &

waning economy

Stable FX policy &

Improving economy

Source: CEIC and TMB Analytics; as of June 2017

Factors to Monitor Factors to Monitor

Factors to Monitor Factors to Monitor

1.64

2.67

1.0

1.5

2.0

2.5

3.0

15Q1 15Q3 16Q1 16Q3 17Q1 17Q3

TGB2YTGB10Y

Source: MOC, CEIC and TMB Analytics -22-

% TMB’s Projection

0

1

2

3

4

5

15Q1 15Q3 16Q1 16Q3 17Q1 17Q3 18Q1 18Q3

2017 Policy Rate: 1.5%

%

2018 Policy Rate: 2.0%

2017 TGB 2Y: 1.64%

2017 TGB 10Y: 2.67%

Policy Rate will Reach 2.0% in 2018 amid Global Tightening Cycle

TGB yields will gradually rise as BoT hike rate

Thai Economy

65

70

75

80

85

-30

-20

-10

0

10

20

May-14 Nov-14 May-15 Nov-15 May-16 Nov-16 May-17

Services Durable Cons Confidence (RHS)

%yoy Index

Private Consumption Gained Traction

Source: BOT, OAE and TMB Analytics

Overall private consumption expanded well

especially in services from continual improvement

in farm income. Durable consumption persistently

expanded, while non-durable consumption slightly

contracted from the same period last year.

Farm income continuously grew, though at slower

rate due to lower price compared to last year as

there was high base effect from last year’s drought.

Quantity rise was mainly from rice production.

Private investment remained contracted even with

improving business sentiment.

Continual Expansion in Private Consumption Private Investment Remained Contracted

Farm Income Continuously Grew

44

47

50

53

-4

-1

2

5

May-14 Nov-14 May-15 Nov-15 May-16 Nov-16 May-17

Private Investment Biz Sentiment (RHS)

%yoy Index

-45

-30

-15

0

15

30

45

Apr-14 Oct-14 Apr-15 Oct-15 Apr-16 Oct-16 Apr-17

Price Quantity Farm Income

%yoy

-24-

-25-Source: Ministry of Finance and TMB Analytics

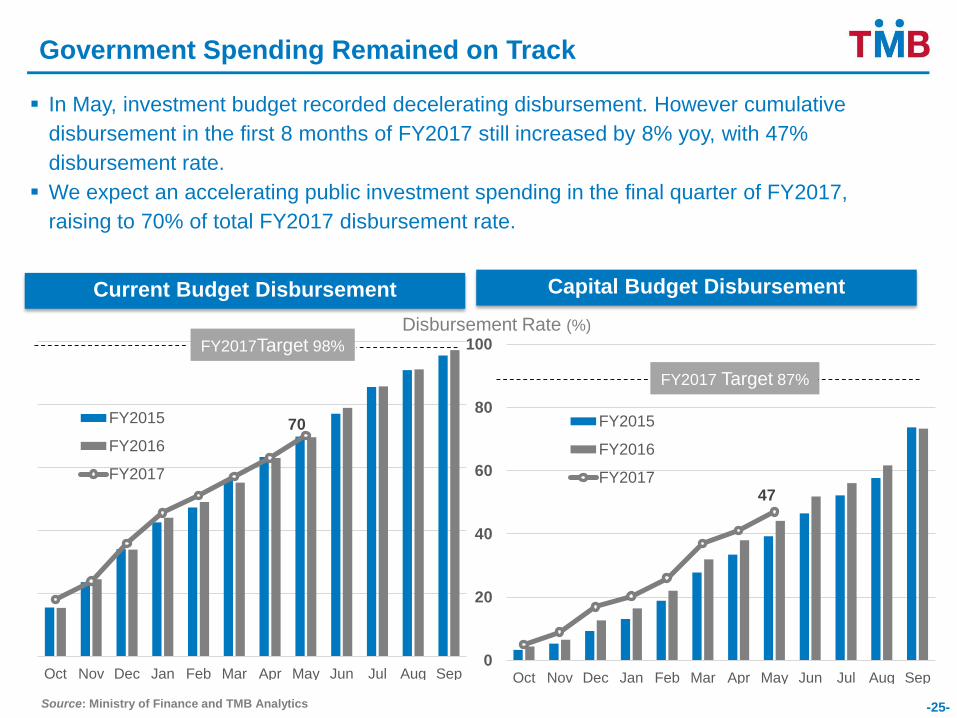

Government Spending Remained on Track

47

0

20

40

60

80

100

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

FY2015

FY2016

FY2017

Capital Budget Disbursement

Disbursement Rate (%)

FY2017 Target 87%

70

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

FY2015

FY2016

FY2017

Current Budget Disbursement

FY2017Target 98%

In May, investment budget recorded decelerating disbursement. However cumulative

disbursement in the first 8 months of FY2017 still increased by 8% yoy, with 47%

disbursement rate.

We expect an accelerating public investment spending in the final quarter of FY2017,

raising to 70% of total FY2017 disbursement rate.

7.6 4.6

57.866.3

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Dec-1

4

Ma

r-1

5

Jun

-15

Se

p-1

5

Dec-1

5

Ma

r-1

6

Jun

-16

Se

p-1

6

Dec-1

6

Ma

r-1

7

Growth of No. of Tourists (%yoy)

May'17May'16

+114k

Occupancy Rate (%) +8.5%

2.48

2.5924k

38k

46k 7k10k

1k 4k-6k-9k

+3%

+13%

+6%

-2% +7% +6% -19% +5% +6%

Ma

y'1

6

Ch

ina

(29%

)

Ea

stA

sia

(Excl.C

hin

a)

(13%

)

AS

EA

N (

30%

)

Eu

rop

e (

12

%)

Am

eri

ca

s (

4%

)

So

uth

Asia

(6%

)

Mid

dle

East

(2%

)

Afr

ica (

1%

)

Oc

ea

nia

(3

%)

Ma

y'1

7May'16

Million

Million

May'17

Ch

ina

(2

9%

)

Source: Department of Tourism, BOT, and TMB Analytics

Good Momentum And Right On Target Chinese Returned To Growth Zone After Crackdown

May 2017, number of tourists were 2.59 million, raised up almost 5%yoy and inbound tourism revenue generated

125 billion, increased 6.9%yoy. These attributed mainly from the resumption of Chinese and coincided with

growing in East Asia and ASEAN arrivals.

During first five month, tourist arrivals were recorded at 14.6 million, grew by 3.2% and the accumulation of

receipts at 747 billion baht also indicated strong growth by 5.1% compared to the same period last year.

Occupancy rate higher than May’16 by 8.5%, emphasized the improvement of recovery sign in tourism sector.

*Note:± x % represents the growth of tourist arrival (yoy)( %) represents the share of tourist arrivals

Chinese rebounded … Bringing smile back to Thailand

+5%

-26-

Number of Tourists (Mill people)

2.482.59

27

0.5 0.8

-0.3

7.2

3.83.4

13.2

10.5

2.7

Value Volume Price

2016 YTD May-17

Trade Balance

+944 mn USD

Export Import

-3.7

-1.1-2.6

15.2

5.46.9

18.2

13.8

4.4

Value Volume Price

2016 YTD May-17

May Export 2017

May export was 19.94 bn USD, expanding by 13.2% from the same period last year and the highest in 52 months. Therefore, the first five months grew by 7.2%.

The strong growth mainly came from an increase in volume, while price effect was starting to dissipate.

May Import 2017

May import value was 19.0 bn USD grew by 18.2% from the same period last year.

Products with highest import growth

Electronic/Computer & Parts (+16.1%)

Chemical (+27.3%)

Energy Product (+18.9%)

Steel & Metal Producer (+16.9%)

Machinery Trader (+16.8%)

Vehicle (+12.9%)

A Surge in Export and Continuing Rise in Import Growth Driven by Strong Global

Demand

Source: MOC, and TMB Analytics-27-

28

Export Growth was More Diversified Both at Products and Markets Level

Key productsOutlook Major exporting market

Industrial

Consumption & Agriculture

%YTD Share

Vehicle 17.6

Electronic Home 7.2

Food 5.8

Agro 4.1

YTD Apr May

13.2 19.2

1.2 24.6

1.17.3

7.5 27.8

Electronic Com 17.4

Machinery Trader 6.2

2.818.5

0.212.2

• Auto Parts( 9.7%),Commercial

vehicles( 24.9%), Passenger car (0.4%)

• Consumer Electronics(20.5%)

• Seafood(6.2%),Chicken (20.7%)

• Vegetable & Fruits(45%), Sugar(45%)

• Electronics Parts (26.3%), Consumer Electronics (45.3%), HDD (20.6%)

• Industrial Machinery(13.4%)

• Australia (21%), EU25 (8%), Middle East (7%)

• USA (35%), Japan (17%), EU25 (9%)

• Japan (34%), EU25(17%), USA (14%)

• CLMV (25%), ASEAN5(21%), CHINA (12%)

• USA (18%), EU25 (15%), China (15%)

• EU25 (18%), USA (17%), JAPAN (15%)

May Growth (%) % YTD Share

8.3%

16.3%

7.3%

20.3%

3.2% 3.4%

-1.6%

-7.0%

12.8% 13.0% 14.3%

26.8% 25.2%

8.8%12.8% 11.7%

-15%

-5%

5%

15%

25%

35%

WORLD ASEAN5 CLMV CHINA JAPAN USA EU25 MIDDLE EAST

YTD April May

Thai Export to Major Markets

Source: MOC, and TMB Analytics -28-

CLMV

(2016 -0.2)

+6.5

Rubber

+38.5(2016 -3.8)

-29-Source: MOC CEIC and TMB Analytics

What is 2017 outlook for Thai Export?

Total

(2016 +0.5)

+3.7

ASEAN5

(2016 -1.4)

+2.2

Japan

(2016 +2.4)

+2.8

China

(2016 -0.8)

+9.3

USA

(2016 +1.7)

+3.5

EU

(2016 +0.5)

+2.4

Able to grow from

global demand

recovery despite higher

uncertainty from

political and geopolitical risk

Strong

consumption demand

Oil price

recovery helps

raw mat and commodities

Recovered

investment in Asia

help supply chain with Japan

Continual

economic recovery

Protectionism

unlikely to take

full effect this year

Thai Export: Recovery … Not A Significant Boost

Computer&Parts

+6.3(2016 -2.0)

Beverages

+0.5(2016 +5.8)

Electrical appliances

+5.4(2016 -1.3)

Rising demand

for tire mfg from

China and price increase

Drop comes

mainly from

middle east market

Global economic recovery and increase in

oil price which is expected to be 57 dollar per barrel at the end of 2017

Energy drink

market growth

contributes to overall growth

Market

Product

High

economic growth

Vehicles

-0.9(2016 +4.6)

Chemical

+8.3(2016 -7.5)

-30-

MPI increased +1.4%yoy, Because of Export Market Recovery

85.5

80

85

90

95

100

105

Jan-14 Jan-15 Jan-16 Jan-17

Diffu

sio

n In

de

x

BA

DG

OO

D

May 2017, MPI unexpectedly rose +1.4%yoy, thanks to higher

production of food, electronic, vehicle and part as export market

recovery.

Positive Growth: food, electronic part, vehicle & part, petroleum

Negative Growth: beverages, construction material, fashion

product

Manufacturing Product Index (MPI)

Negative gr.( MPI < 0%)

Low gr.( 0%<MPI < 3%)

Moderate gr.(3% <MPI<5%)

High gr.(MPI > 5%)

Source: OIE, BOT, FTI, classified industry group and calculated by TMB Analytics

-60

-40

-20

0

20

40

60

80

Jan-14 Jan-15 Jan-16 Jan-17

%Y

oY

Fuel Industry

Industry Indicator

II.Industrial Confidence

I.Raw Materials Import2016 May-17

Q4 Q1 Apr May (%MoM,sa)

Capacity Utilization Rate (%) 100.0 60.0 59.5 62.6 53.7 62.1 0.6

Manufacturing Product Index (MPI) (%YoY) 100.0 1.6 0.3 -1.5 -1.8 1.4 2.3

Food 15.3 2.7 2.8 5.1 1.5 8.2 0.1

Vehicle 11.8 2.2 -4.8 -7.3 -10.7 3.3 12.9

Electronic/Computer & Parts 11.2 2.7 13.9 7.0 8.2 9.1 -0.2

Autopart 9.8 -1.0 -3.2 0.2 0.5 3.4 3.3

Fashion Products 9.8 -2.8 -5.4 -10.3 -7.0 -4.0 3.5

Steel Products 5.9 5.3 8.8 -11.0 -5.4 -14.1 -13.1

Rubber Products 5.8 -0.7 -2.6 7.8 2.3 8.1 2.0

Construction Material 5.6 -0.9 -1.2 -5.0 -0.2 -6.1 -6.0

Electronic/Electric Home Appliance 4.3 15.1 -2.6 -2.5 0.5 -1.4 6.8

Beverage 4.0 -0.2 -1.7 -3.6 -5.5 -11.7 -2.7

Petroleum 3.3 2.4 -0.2 7.1 2.7 7.1 2.7

Plastics Products 3.1 4.2 -2.6 -3.8 -4.8 3.2 4.7

Papers & Printing 2.7 5.2 -1.2 0.1 0.8 -0.4 -2.5

Furniture and Household Products 1.8 -17.3 -2.0 -5.3 -15.9 4.2 8.5

Chemical 1.6 0.5 -1.5 1.5 -4.5 6.3 6.2

Healthcare 1.3 -1.2 13.4 1.9 2.4 4.0 0.7

Consumer Goods 1.3 1.1 -5.0 -10.1 -7.7 -6.8 4.7

Tabacco 1.1 -9.2 -5.0 -10.5 -15.0 -0.3 10.7

Agri.Machinery 0.1 5.8 -14.9 -0.6 -26.9 12.8 40.6

(%)

Weight2016

2017

-31-

90

100

110

120

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

MP

I (B

AS

E =

20

11

, S

A)

Export market (export > 60%)

Both market (30% < export < 60%)

Domestic market (export < 30%)

Growth +8.2%

100

103

105

108

110

113

Jan

-16

Jul-

16

Jan

-17

MP

I (B

ase

= 2

01

1, S

A)

Highlight of Manufacturing Production Index (May 2017)

MPI by Export Share

FoodSeafood, Sugar, Cooking oil,

flour products

High Growth High Decline

Source: OIE, BOT, FTI and TMB Analytics Note: Growth as of May-17

Growth+9.1%

Electronic HDD, Monolithic IC, Transistors

90

95

100

105

110

115

120

Jan

-16

Jul-

16

Jan

-17

MP

I (B

ase

= 2

01

1, S

A)

Growth-11.7%

BeverageLiquor, Soda, Water

110

115

120

125

130

135

140

Jan

-16

Jul-

16

Jan

-17

MP

I (B

ase

= 2

01

1, S

A)

Growth-6.1%

Con. Mat.Cement, Concrete, Ceramic

88

91

93

96

98

101

103

Jan

-16

Jul-

16

Jan

-17

MP

I (B

ase

= 2

01

1, S

A)

+Export growth

Expect Rate Normalization in 2018 and 1.50% Policy Rate in 2017

Source: MOC, CEIC and TMB Analytics

Headline Inflation Stands above Zero for 2 Consecutive Months

Policy Rate is Expected to be Held at 1.50% as Inflation Remains Low

2 Consecutive Months of Negative Inflation from Last Year’s High Base

May inflation rate turned negative at

-0.05% due to high base effect from last

year drought, while energy price continued

to increase as global energy price rose.

We expect inflation rate to turn positive

again in latter half of the year and

averaged at 1% in 2017 from increase in

energy price.

-32-

-2

-1

0

1

2

3

14Q1 14Q3 15Q1 15Q3 16Q1 16Q3 17Q1

%yoy

June 2017 = -0.04%

Avg 2016 = 0.2%

Policy rate is expected to be maintained at 1.50%

throughout 2017 to accommodate economic

recovery especially private investment. Moreover,

inflationary pressure remained low.

We expect the rate normalization to begin in 2018

as global interest rate is on an upward trend

following 3 expected fed rate hikes in 2017.

However, there is still concern over recovery of

private investment, which can delay Thai rate

normalization.0

1

2

3

4

5

15Q1 15Q3 16Q1 16Q3 17Q1 17Q3 18Q1 18Q3

%

THANK YOU

Disclaimer

This document is issued by TMB Analytics, a division of TMB Bank PCL. All analyses are based on information available to

the public. Although the information contained herein is believed to be gathered from reliable sources, TMB makes no

guarantee to its accuracy and completeness. TMB may have issued, and may in the future issue, other reports that are

inconsistent with, and reach different conclusions from, the information presented in this report. Opinions or predictions

expressed herein reflect the authors’ views, not that of TMB, as of date of the analysis and are subject to change without

notice. TMB shall not be responsible for the use of contents and its implication.

![Monthly Economic Reviewbsl.gov.sl/MER October 2019- Finalised Version.pdf · Monthly Economic Review October 2019 Publisher: The Monthly Economic Review [MER] is published by the](https://img.dokumen.tips/doc/110x75/5eddde83ad6a402d66691757/monthly-economic-october-2019-finalised-versionpdf-monthly-economic-review-october.jpg)

![Monthly Economic Reviewbsl.gov.sl/MER February 2020- Final.pdf · Monthly Economic Review February 2020 Publisher: The Monthly Economic Review [MER] is published by the Research Department,](https://img.dokumen.tips/doc/110x75/5fba3d20bddd3601b021cd66/monthly-economic-february-2020-finalpdf-monthly-economic-review-february-2020.jpg)