Embed Size (px)

Citation preview

MoneyCounts: A Financial Literacy Series

Budgeting Fundamentals

Dr. Daad RizkMoneyCounts: A Financial Literacy Series240D Outreach BuildingUniversity Park PA [email protected] 814-863-0214

MoneyCounts: A Financial Literacy Series

Learning Objectives

• 5 steps to budgeting– Set up SMART goals– Collect financial information – Track money coming in – Track money going out– Review cash flow and set up a budget

MoneyCounts: A Financial Literacy Series

On Budgeting

• Theo's Budget [YouTube]

MoneyCounts: A Financial Literacy Series

What is Budgeting?Budgeting is the process of creating a plan to spend your money. It is spending less than earning as you plan for your financial goals

How do I allocate my income to pay my expenses?

Where did my money go?

Why am I always broke?

A financial tool to help manage cash flow!

Budgeting is never “ONLY” about money!

What is Budgeting?

MoneyCounts: A Financial Literacy Series

Budgeting is simply balancing your expenses with your income.If they don't balance and you spend more than you make, you will have a problem

Many people don't realize that they spend more than they earn and slowly sink deeper into debt

Why is it important?

MoneyCounts: A Financial Literacy Series

To meet your financial goals

To achieve financial security

To prevent financial crisis

To get out of financial crisis

Goal is to maintain financial stability in good times and financial sustainability in hard times

An important component of financial success

Adopt a budget prior to financial crisis

When Should you budget?

MoneyCounts: A Financial Literacy Series

Step 1 – Start by setting smart goals

Short term & long term goals/personal, educational, social, financial and recreational

– What are my values, my needs, what is my life situation?

– What are my goals, what do I hope to accomplish?

– Before you plan, picture the destination

The Budgeting Process – Step 1

MoneyCounts: A Financial Literacy Series

SMART – GOALS

Prioritize goals using the SMART Model

= Specific

= Measurable

= Attainable

= Realistic

= Timely

Goals should be crystal clear in their definition

SMART

MoneyCounts: A Financial Literacy Series

Step 2 – Get Organized

Collect Financial Information Pay Stub

Bank Records

Financial Aid Awards Insurance

Tuition and Fees Bills Groceries Receipts

Bookstore Bills Eating Out Receipts

Credit Card Bills Personal

Utility Bills Pets

Electronics Miscellaneous

The Budgeting Process – Step 2

MoneyCounts: A Financial Literacy Series

Step 3 – Money coming in/ Income & Borrowing• Wages, Salaries

• Family Help

• Interest Income

• Other Income

• Grants and Scholarships– Loans

– Perkins

– Subsidized

– Unsubsidized

– Other Loans

The Budgeting Process – Step 3

MoneyCounts: A Financial Literacy Series

Step 4 – Money going out/Saving & Spending

Saving

– At least 10% of net income

– Pay yourself first

– Establish/ keep an emergency fund

– Invest and plan for retirement

The Budgeting Process – Step 4

MoneyCounts: A Financial Literacy Series

Step 4 – Money going out / Saving & Spending

Spending

– Know needs from wants, what are my spending habits? How do I make spending decisions?

– List all spending – Tracking process

Fixed & Variable

» Tuition, Fees, Books

» Housing and Groceries

» Car expenses, Electronics, Insurance,

Eating out, Personal, Pets, etc.

» Periodic expenses, gifts, entertainment,

Charity, etc.

The Budgeting Process – Step 4

MoneyCounts: A Financial Literacy Series

The Budgeting Process – Step 4

MoneyCounts: A Financial Literacy Series

Step 4 – Money going out / Saving & Spending

• Saving is 10% of income – pay yourself first

• Spending• Housing should not exceed 30% of your net income

• Meals and eating out should not exceed 20% of your

net income

• Utilities should not exceed 5% of your net income

• Car expense should not exceed 10% of your net income

• Electronics, phone, Internet should not exceed

5% of your income

• All other expense is 20% of your net income

The Budgeting Process – Step 4

MoneyCounts: A Financial Literacy Series

Balancing Act

– Use Loans only to pay for tuition, fees, & books

– Use income to pay for housing, food, electronics, entertainment, insurance, credit cards, car expense, gas, personal, pets & miscellaneous• Do a monthly budget, use accurate figures/amounts

• Avoid “PILS” Penalties, Interest, Late fees & Surcharges

• Keep a saving account

• Shop based on Needs not Wants

• Pay Credit Card in full each month

• Allow for some fun items, but stick to your budget

The Budgeting Process – Step 5

MoneyCounts: A Financial Literacy Series

The Budgeting Process – Step 5

Earning and Borrowing• Net income• Family support• Grants and Scholarships• Loans

– Perkins– Subsidized– Unsubsidized

Saving and Spending• Saving, emergency fund• Tuition, fees and books• Housing and utilities• Car expense• Phone, Internet,

electronics, videos• Loan origination fees• Insurance, medical,

entertainment

MoneyCounts: A Financial Literacy Series

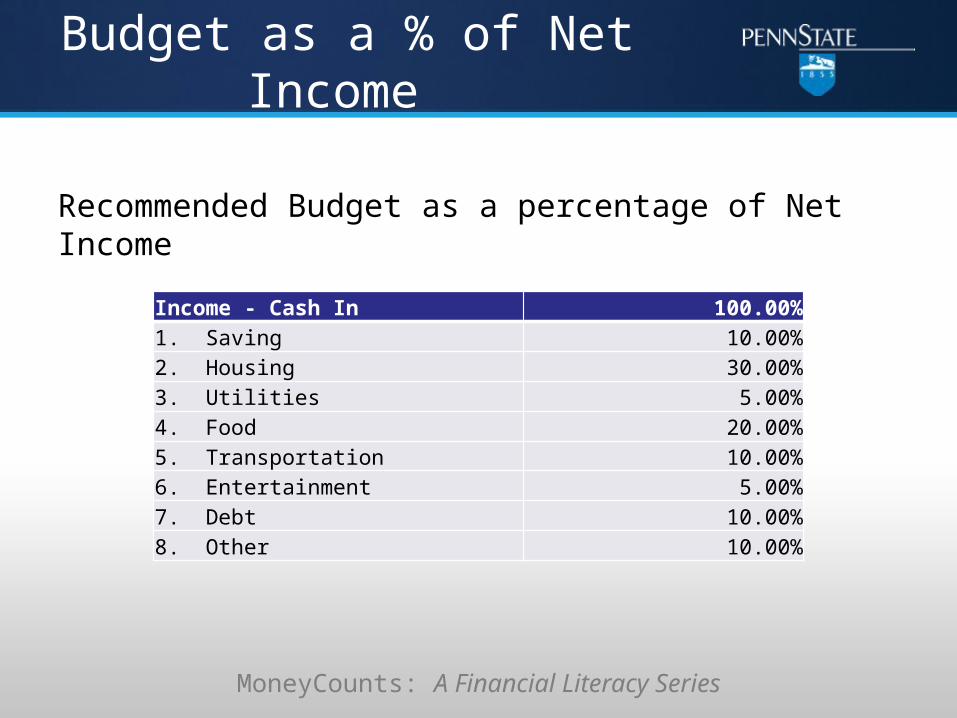

Recommended Budget as a percentage of Net Income

Income - Cash In 100.00%1. Saving 10.00%2. Housing 30.00%3. Utilities 5.00%4. Food 20.00%5. Transportation 10.00%6. Entertainment 5.00%7. Debt 10.00%8. Other 10.00%

Budget as a % of Net Income

MoneyCounts: A Financial Literacy Series

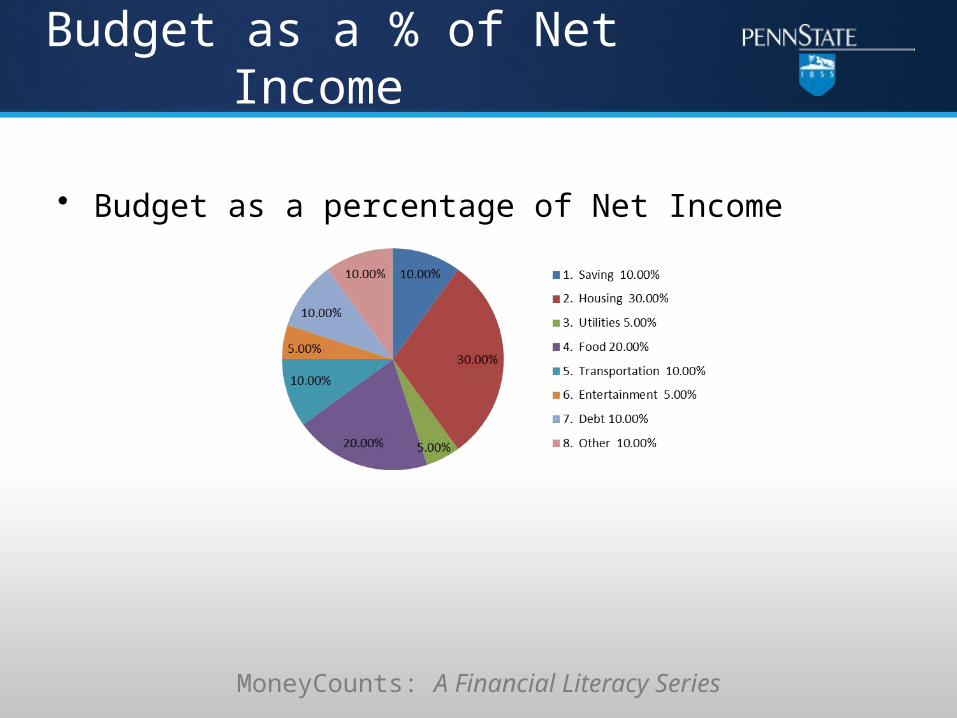

• Budget as a percentage of Net Income

Budget as a % of Net Income

MoneyCounts: A Financial Literacy Series

Use a Monthly Calendar

• Use Black color for income • Use Red color for expenses• Helps you visualize the entire month• Helps you evaluate timing of payments• Helps you improve your budget strategies

MoneyCounts: A Financial Literacy Series

Tracking Expenses

MoneyCounts: A Financial Literacy Series

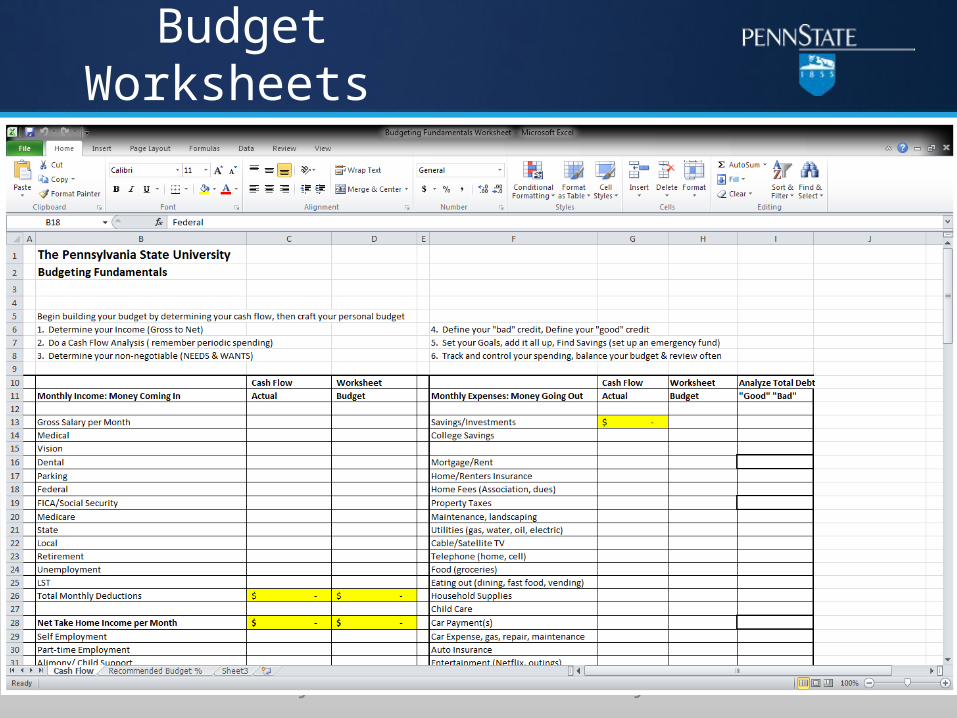

Budget Worksheets

MoneyCounts: A Financial Literacy Series

• financialliteracy.psu.edu/

• Email: [email protected]

Financial Literacy Website!

MoneyCounts: A Financial Literacy Series

Thank You!

Comments and Questions

Dr. Daad RizkMoneyCounts: A Financial Literacy Series240D Outreach BuildingUniversity Park PA [email protected] 814-863-0214