Embed Size (px)

Citation preview

Monetary Targets and Monetary Policy in Canada: A Critical AssessmentAuthor(s): Pierre FortinSource: The Canadian Journal of Economics / Revue canadienne d'Economique, Vol. 12, No. 4(Nov., 1979), pp. 625-646Published by: Wiley on behalf of the Canadian Economics AssociationStable URL: http://www.jstor.org/stable/134871 .

Accessed: 12/06/2014 18:33

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Wiley and Canadian Economics Association are collaborating with JSTOR to digitize, preserve and extendaccess to The Canadian Journal of Economics / Revue canadienne d'Economique.

http://www.jstor.org

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets and monetary policy / 625

Monetary targets and monetary policy in Canada: a critical assessment

PIERRE FORTIN / Universite Laval

I N T R O D U C T I O N

After more than a decade of forceful pronouncements on the need for a stable Canadian dollar price of the us dollar and on the correlative requirement of money supply flexibility (e.g. Canada, 1971), the Bank of Canada announced in September 1975 that from then on it would be committed to effect a gradual reduction in the mean and the variance of the growth rate of the money supply (Ml) and to maintain it thereafter at a low and stable level to establish a low and steady rate of inflation in the long run.

This move was prepared by a long sequence of historical events and theoretical developments in the 1970s. Foremost among these were, first, the air of international respectability given to the control of monetary aggregates by the us Federal Reserve Board and the us Congress from 1970 on by the adoption of a similar money-stock approach in Germany and Switzerland in 1975; secondly, the generalization of floating exchange rates after February 1973, which relieved central bankers from the monetary discipline imposed by the previous commitments to fixed exchange rates and at the same time started a search for a new code of good monetary behaviour; thirdly, the mediocre record of inflation control since the mid- 1960s, culminating on the Canadian scene in the wage explosion of 1974-5 and the fall 1975 offensive against inflation; and, fourthly, the demonstration by Poole (1970) that under some conditions nominal income fluctuations could be made smaller if at least some attention were paid by central banks to the behaviour of monetary aggregates beyond the traditional focus on interest rates.

The particular strategy of monetary control the Bank of Canada announced it would follow after September 1975 has been described in the recent Annual Reports of the governor to the minister of finance and aptly summarized by Courchene (1977). In a nutshell, the Bank said it would attempt to keep the growth rate of the seasonally adjusted MI aggregate within a band of ?2 percentage points around steadily diminishing rates of increases of about 12 per cent a year from 5M75 to 3M76, 10 per cent from 3M76 to 6M77, 9 per cent from 6M77 to 6M78, and 8 per cent after 6M78.1

The Bank has sought to achieve its monetary goal through changes in

For their helpful comments or advice I am grateful to Bernard Decaluwe, Claude Felteau, Bernard Fortin, Peter Howitt, Robert Lafrance, John Sargent, David Slater, Gordon Sparks, and Bill White, although there is no suggestion that the end-product reflects their views on Canadian monetary policy.

1 The symbols 1M75, 1Q75, 1S75, etc. refer to the first month, quarter, and half of 1975, and so on.

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

626 / Pierre Fortin

interest rates to induce the public to demand the right amount of Ml, and not through changes in the reserve base, which would have influenced the money supply. The reasons for this choice are explained in the companion articles by White and Sparks. First, under current institutional arrangements, this month's reserves are held by chartered banks against last month's deposits, and reserve borrowing at the central bank is discouraged, so that the achieve- ment of rigid unborrowed reserve targets could produce extreme interest rate instability and very loose control on monetary aggregates. Secondly, even if the lag in the reserve settlement system were abandoned and borrowing at the central bank made easier, it is not likely that control of the money supply would be much improved if realized through the reserve base, in view of the short-run instability of the money supply multiplier.2

This 'new view' of monetary policy in Canada raises a number of very important questions, around which this paper is organized. First, has the Bank of Canada actually succeeded in reducing the growth rate of MI gradu- ally and in 'placing considerably more weight on stability in monetary expan- sion than was formerly the case,' as promised in 1975? Has actual behaviour followed policy statements? Secondly, what practical difference does the new view make for the conduct of monetary policy in Canada, compared to the 'old view' that prevailed before 1975? Is all this mere window-dressing? Thirdly, how does the new monetary rule fare in the light of recent developments in the theory of monetary policy, and how do the Bank's arguments in favour of a constant-growth-rate (CGR) rule square with this theory? Is the CGR rule the best theoretical approach to policy? And fourthly, even if not an optimal strategy is the CGR rule an improvement over the previous discretionary approach to policy, or do there exist more satisfactory and practical rules of behaviour for the central bank? Is the CGR rule the best practical approach to policy?

The next four sections address each of these issues in turn.

HAS ACTUAL BEHAVIOUR FOLLOWED POLICY

S T A T E M E N T S ?

Table 1 indicates that between the second quarter of 1975 and May 1979 the Bank of Canada was successful in reducing the average growth rate of M1 in each of the four three-to-five-quarter averaging periods. This has been im- plemented by decreasing the mean target growth rate of M 1 from one period to the next, by always selecting the starting point for the new lower target in the lower half of the previous band, and by keeping M I in that lower half or below the band itself two months out of three.3

2 us evidence indicates that a pure interest rate strategy dominates a pure reserve base strategy by some margin (Federal Reserve Bank of New York, 1974; Friedman, 1977). In this paper I shall continue to assume that the reserve base does not dominate short-run interest rates as an instrument of money supply control.

3 A quick count reveals that in the period of forty-four months extending from October 1975 to May 1979, M l was above the target band on five occasions, in the upper half of the band on

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets and monetary policy / 627

TABLE 1

Announced and realized percentage increases (at annual rates) of the seasonally-adjusted Ml, Canada 1975-9

Date of Target Base Actual announcement band period growth ratea

November 1975 10-14a 2Q75 I , b

August 1976 8-12 2M-3M-4M76 10.2 October 1977 7-11 6M77 9. lb

September 1978 6-10 6M78 8.2C Average 7.7-11.7c,d 2Q75 8.9c

a The upper bound was rather imprecisely stated by the Bank of Canada. b From given base period to next c From given base period to 5M79 d Averages of the lower and upper limits of the four target bands SOURCE: Statistics Canada (CANSIM series B 1609)

TABLE 2

Mean and standard error of the percentage increase (at annual rates) of the seasonally-adjusted semi-annual averages of Ml, Canada 1970-5 and 1975-9

Number of Standard Series Period observations Mean error-

UA 1970-1975 10 11.9 4.4 UA 1975-1979 7 8.8 3.8

APS74 1970-1975 10 11.9 3.9 APS75 1975-1979 7 8.8 1.9

NOTE: The basic unadjusted series is constructed as 2 (m8-m8-1)1ms l, where m, is the simple average of Ml over the six-month period s. UA

is the basic unadjusted series; APS74 and APS75 are adjusted for the significant postal strikes of 2Q74 and 4Q75. In these two quarters the averages of Ml were replaced by simple interpolations of the averages for 1Q74 and 3Q74 and for 3Q75 and 1Q76 respectively. The averages for the relevant half-years were then modified accordingly. For 1970-5 the first half-year (s = 1) included the last two quarters of 1970 and last half-year included the first two quarters of 1975. For 1975-9 the first half-year included the last quarter of 1975 and the first quarter of 1976, and the last half-year included the last quarter of 1978 and the first quarter of 1979. SOURCE: Statistics Canada (CANSIM series B 1609)

As opposed to the average growth rate of M1, the stability of monetary expansion is more difficult to gauge, although here also the record seems to indicate that the Bank has kept its promise of lesser volatility (Bank of Canada, 1976, 12). Table 2 compares the mean and standard error of monetary growth in the recent 'monetarist' period (1975-9) with those in the im-

eleven occasions, in the lower half of the band on eighteen occasions, and below the band on ten occasions. The criterion of the band is applied to the entire period even if the concept was introduced only in 1977.

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

628 / Pierre Fortin

mediately preceding flexible exchange rate period (1970-5). For the reason- able half-year horizon, the mean growth rate of MI has decreased 3.1 percent- age points from the first to the second period, while the standard error around mean has declined only slightly from 4.4 to 3.8 percentage points. However, if one is ready to smooth the time series for M1 in the two most important episodes of mail service interruption (2Q74 in the first period and 4Q75 in the second period), one can readily see from the table that the standard error of the growth rate of MI has been exactly halved from 1970-5 to 1975-9.

The money stock did remain within the specified target bands two-thirds of the time between October 1975 and May 1979. It erred on the high side in 4Q75 and 4Q78 under the influence of postal strikes and of a financial shock in the Canada Savings Bonds market. It fell below the band in the period from fall 1976 to summer 1977 partly because nominal growth was unexpectedly weak and partly because of the suspicion that the demand for Ml had shifted downwards.

The over-all picture that emerges is that in accordance with its pronounce- ments the Bank of Canada has so far actually delivered the goods: a gradually declining and more stable average growth rate for Ml. It has applied a close approximation of the monetarist CGR rule. This is perhaps in contrast with the situation in the United States, where strong evidence has been adduced to show that the Federal Reserve Board has not shifted its policies in a manner consistent with controlling the monetary aggregates, despite official state- ments to the contrary (Pierce, 1978).

IS ALL THIS MERE WINDOW-DRESSING?

If the Bank sticks to its CGR rule of converging to the desired mean and minimal variance of monetary growth - and it could not abandon it without losing much of it credibility - the behaviour of the money supply and its meaning for stabilization policy will differ substantially from that before 1975 in the more activist era. To be sure, it is certainly conceivable that the recent gradual offensive against inflation, with the same degree of attention paid to the danger of excessive unemployment, could have been waged without any direct concern over the time path of the money stock, and that the simple application of the 'old medicine' could have yielded approximately the same results for money-stock statistics.

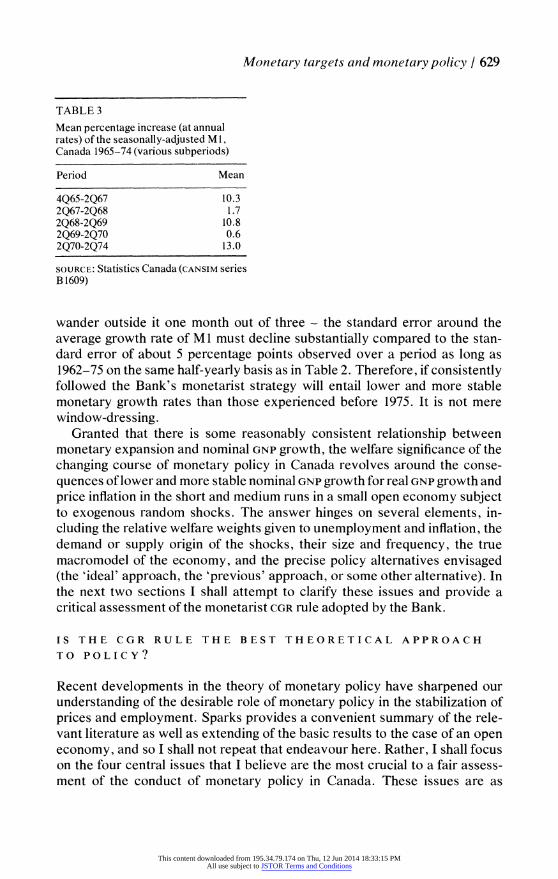

However, in the medium to long run the Bank is now severely constrained by its new approach. With a band of 6 to 10 per cent a year for 1978-9, decreasing eventually to perhaps 4 to 8 per cent a year, the rate of increase of MI cannot exceed 10 per cent or fall short of 2 per cent a year for any significant period in the future. In other words, the new strategy by definition excludes the stop-go pattern of monetary expansion characteristic of the years 1966 to 1974 (Table 3). Under any reasonable rule of thumb for the flexibility of limits imposed by the growth corridor - such as allowing MI to

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets and monetary policy / 629

TABLE 3

Mean percentage increase (at annual rates) of the seasonally-adjusted M 1, Canada 1965-74 (various subperiods)

Period Mean

4Q65-2Q67 10.3 2Q67-2Q68 1.7 2Q68-2Q69 10.8 2Q69-2Q70 0.6 2Q70-2Q74 13.0

SOURCE: Statistics Canada (CANsIM series B 1609)

wander outside it one month out of three - the standard error around the average growth rate of MI must decline substantially compared to the stan- dard error of about 5 percentage points observed over a period as long as 1962-75 on the same half-yearly basis as in Table 2. Therefore, if consistently followed the Bank's monetarist strategy will entail lower and more stable monetary growth rates than those experienced before 1975. It is not mere window-dressing.

Granted that there is some reasonably consistent relationship between monetary expansion and nominal GNP growth, the welfare significance of the changing course of monetary policy in Canada revolves around the conse- quences of lower and more stable nominal GNP growth for real GNP growth and price inflation in the short and medium runs in a small open economy subject to exogenous random shocks. The answer hinges on several elements, in- cluding the relative welfare weights given to unemployment and inflation, the demand or supply origin of the shocks, their size and frequency, the true macromodel of the economy, and the precise policy alternatives envisaged (the 'ideal' approach, the 'previous' approach, or some other alternative). In the next two sections I shall attempt to clarify these issues and provide a critical assessment of the monetarist CGR rule adopted by the Bank.

IS THE CGR RULE THE BEST THEORETICAL APPROACH

TO POLICY?

Recent developments in the theory of monetary policy have sharpened our understanding of the desirable role of monetary policy in the stabilization of prices and employment. Sparks provides a convenient summary of the rele- vant literature as well as extending of the basic results to the case of an open economy, and so I shall not repeat that endeavour here. Rather, I shall focus on the four central issues that I believe are the most crucial to a fair assess- ment of the conduct of monetary policy in Canada. These issues are as

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

630 / Pierre Fortin

follows: (1) Is the use of a CGR rule as an operational guide to monetary policy consistent with the optimal policy framework developed by Poole (1970) and B. Friedman (1975; 1977) and summarized by Sparks? (2) To what extent do uncertain forecasts, uncertain structural parameters (including long and un- certain lags), and the behaviour of private expectations frustrate the efficiency of the optimal policy approach and make the CGR rule near-optimal in real- world policy-making? (3) Is the intermediate-target procedure, which consists in minimizing the mean square error of the money stock around its desired path in the short run as a surrogate for minimizing the mean square error of nominal income around its desired path, an efficient procedure in the conduct of monetary policy? (4) What kind of role should exchange rate control play in the present system of floating exchange rates?

To the first question the answer is that a CGR rule is clearly inconsistent with the theory of monetary policy in a Poole-Friedman context. Optimal be- haviour on the part of the central bank requires that it follow a reaction function based on some linear or non-linear combination of the reserve base, the interest rate, and the exchange rate,4 with the money supply remaining in the background as a variable not directly relevant (in the Tinbergen sense) to the choice of the policy instrument(s).5 The resulting reduced form path for the money supply is obviously a function of the parameters of the welfare function, of the target path of real income and prices, of the time path of the vector of all relevant exogenous variables, and of the structural parameters. Only under an extremely rare set of circumstances would such a path follow a CGR trend. A positive rate of time preference, frequent and sizable demand and supply shocks, and a strongly autoregressive process for aggregate price formation, combined with a pronounced non-linearity in the Phillips curve, are simply inconsistent with a +2 per cent constant-growth-rate band actually containing the optimal money supply path. In other words - and this often goes unnoticed - Poole's framework implies that, to the extent that it is desirable, the control of monetary aggregates should be exercised in the context of discretionary countercyclical monetary policy, not in that of a CGR

rule. This is indeed the way it has been understood so far in the United States, where monetary policy has remained predominantly discretionary since 1970 despite the greater official emphasis on the stabilization of monetary expan- sion.

On the second question proponents of the CGR rule often criticize the

4 In that sense one can speak of a reserve base strategy, an interest rate strategy, an exchange rate strategy, or a combined policy. As I mentioned in the introduction the Bank of Canada stresses that its preferred approach is the rough stabilization of money supply growth around its desired path with the help of interest rates as the control instrument. This is called an interest rate strategy in the present paper, but the reader should keep in mind that money supply growth remains the intermediate target of the Bank's strategy.

5 Friedman (1975). Poole and Friedman developed their approach in the context of a unique policy target (nominal income), but it can be extended to the two-target case (inflation and unemployment) (see Decaluwe, 1972).

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets and monetary policy / 631

optimal policy approach to monetary (and fiscal) policy for relying on the extremely fragile assumptions that forecasts and 'backcasts' are certain, that there is a consensus among professionals on the values of the structural parameters of the macromodel, and that the formation of private expectations can be confidently predicted. For example, the Bank of Canada argued that activism was tried and found often to have a destabilizing influence on the cyclical pattern of nominal expenditure growth in the economy for reasons that included the difficulty of making reliable short-term economic forecasts, the long and variable time lags involved in monetary policy, and the difficulty of making judgments about appropriate interest rate levels in periods when future inflation is expected (Bank of Canada, 1976, 12).

The consequences for practical policy-making of uncertainty, lags, and expectations are certainly most relevant and were notably discussed by Milton Friedman as early as 1953 (Friedman, 1953). They no doubt decrease the true distance between the CGR approach and the optimal approach in the real world. However, results obtained on these issues in the last two decades tend to support the view that the CGR rule remains distinctly suboptimal in the presence of uncertainty, lags, and expectations.

Theil (1961) showed that the availability of unbiased forecasts of the current and future path of the policy target variables allows the policy-maker to reach the optimal strategy by acting as though he were certain of the forecast (the certainty-equivalence principle). The expected loss is then higher than if certain forecasts were available, but minimal under the cir- cumstances. McNees (1978) has recently reported comforting results on the ability of three major private us forecasters to make unbiased predictions of the rate of growth of real GNP four quarters ahead in the very short and turbulent sample period 1970-5. No direct evidence is available yet on the biases of Canadian forecasters, but the use of similar techniques in the two countries at least suggests that unbiasedness might be within their reach.

In the presence of uncertainty about structural parameters (including vari- able lag parameters) and consequently about dynamic policy multipliers, Brainard (1967) showed that the policy reaction function should aim at closing only part of the expected income gap, not the entire gap as in the traditional Poole analysis. The appropriate degree of activism is reduced by these con- siderations, and hence a weaker (but not a zero) response is called for.6 More recently, Cooper and Fischer (1973) have demonstrated that a greater length

6 Note, in particular, that this principle of prudence applies to the imprecise knowledge of the natural rate of unemployment, in which case it lowers the probability of undershooting the natural rate under monetary activism. This probability is also made smaller by virtue of the sluggishness of the price adjustment process, which gives the policy-maker time to correct its course when the evidence shows that the current natural rate target induces accelerating or decelerating inflation. It is superfluous to emphasize here that basic research on the most probable range for the natural rate of unemployment should receive high priority, given the importance of the recent structural shifts in demography, unemployment insurance and minimum wage regulations, public sector wage policy, etc.

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

632 / Pierre Fortin

of the average lags of the dynamic policy multipliers was a reason for more vigorous, rather than less vigorous, use of active stabilization policy. All these results have clearly weakened the classical case for the non-interventionist plank based on the existence of long and uncertain policy lags.

Since the future is involved in economic behaviour, expectations play a crucial role in private decision-making and thus in any macromodel of the economy that pretends to be useful to policy-makers. There is no question that the processes of private expectations formation are very difficult to model and that expectations cannot always be confidently predicted. However, just as in the case of other types of additive or multiplicative uncertainties, optimality can be maintained if discretionary policy relies on unbiased fore- casts of the target variables (Theil's principle) and proceeds cautiously (Brainard's principle). It is an exaggeration to argue that the unobservability of expected price inflation makes it too difficult to have a sufficiently precise idea of its value to evaluate the stance of monetary policy at any moment in terms of the rough value of the real interest rate. In addition, the very sluggishness of the inflationary process ensures that, in the short run, changes in nominal interest rates induce changes in real interest of the same order of magnitude.

Potentially more destructive to the usefulness of active discretionary pol- icy is the argument that private expectations are influenced by systematic policy behaviour, as they must be to have some element of rationality (Lucas, 1976). If it is assumed that economic agents use efficiently whatever informa- tion is available and form their expectations as if they knew how the economic system works, up to an additive disturbance, then it is a fundamental theorem (Sargent and Wallace, 1975) that under any systematic policy rule and in the short run unemployment and inflation can differ from the natural rate of unemployment and the anticipated rate of monetary growth (less real GNP

growth) respectively only by some white noise.7 In these circumstances anticipated changes in monetary growth will immediately provoke one-for- one changes in expected and actual rates of inflation and no changes in the unemployment rate. Optimal policy under such rational expectations would exclude any non-systematic, activist behaviour on the part of the authorities, since it would only serve to increase uncertainty about monetary growth and the variance of the white noise around unemployment and inflation. Systema- tic policy feedback rules would do neither good nor harm as long as they were well known, but the simplicity and understandability of the CGR rule would presumably make it a preferred candidate.

Of course the full rational expectations hypothesis and its stark implica- tions for the conduct of macroeconomic policy are highly questionable and have recently been faced with three lines of criticism. First, the hypothesis

7 Plus a lag term in the past difference between the actual and the natural rates of unemploy- ment, as when the delays in the flow of information and the cost of getting information are taken into account, or when trade balance adjustments are slow in an open economy.

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets and monetary policy / 633

has been attacked for its inconsistency with the perceived stickiness of wages and prices, which adjust to monetary and other influences only over a number of years. This should be true for closed economies (Gordon, 1976; Fischer, 1977) as well as for open economies, where substantial and persistent devia- tions from purchasing power parity have been observed (Officer, 1976; Kravis and Lipsey, 1978). Building on these rigidities, Baily (1978) and Hall (1978) have constructed models in which rational expectations increase, rather than offset, the effectiveness of activist, non-CGR policies.

The second line of attack has been directed against the implausible amount of knowledge that economic agents are required to possess under the full rational expectations hypothesis (Friedman, 1979; Rymes, 1979). By assum- ing that they attempt to learn the values of the structural parameters of the true model of the economy instead of supposing that they know it up to an additive disturbance (but still granting they know the correct model specification). Friedman has shown that private expectations can plausibly be approximated by the familiar adaptive mechanism 'a la Cagan, which is the most widely used expectations-generating formula in optimal-policy models.

It is now hard to avoid being impressed by the recent theoretical arguments and empirical evidence against the usefulness of the application of the full rational expectations hypothesis to macroeconomic analysis and policy and supporting the relevance of the optimal policy approach. So far, the Bank of Canada has not invoked the full rational expectations hypothesis in support of its new monetary strategy. However, central banking circles in Canada and elsewhere usually argue for a milder form of the hypothesis, which is that the simplicity and understandability of the CGR rule, together with the 'well- understood' long-run association between monetary growth and inflation, are bound to have some beneficial influence on inflationary expectations and decrease the cumulative amount of unemployment needed to suppress inflation. There is a grain of truth in this argument, but the question is: how much influence? and compared with what alternative policy behaviour? If the long-run association between prices and money is obscured by significant and persistent noise in the short and medium runs, the best forecasting strategy on the part of economic agents may still be adaptive expectations under most circumstances: they believe that inflation will delecerate only when they have evidence that it has begun to decelerate. If this is true, inflationary expecta- tions would be lower on average under a CGR rule only to the extent that this type of monetary policy would maintain unemployment higher and inflation lower on average than under the envisaged competing alternative policy rules. The adoption of a CGR rule would thus move the economy along the Phillips curve, but not shift the curve in a favourable direction. Hence, the subopti- mality of the CGR rule would hardly be corrected by the argument about its direct impact on inflationary expectations.

On the third question it must be acknowledged that, despite the 'irrele- vance' of the money supply in the choice of the policy instrument(s), there is

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

634 / Pierre Fortin

indeed some sense in which the observed difference between the current value of the money stock and its desired or expected value contains informa- tion about unknown current and future values of the numerous exogenous shocks to which the economy is subject. The point here is that we do not live in a static world in which data on parameter values and levels of income and of all exogenous variables are known contemporaneously and with certainty and in which structural lags are absent. When data and structural lags exist and knowledge of the money supply is more contemporaneous and certain than many other variables, it is natural to adopt the intermediate-target procedure of attempting to minimize E(M - M*)2 instead of E(Y - y*)2. Operationally, this may be translated into keeping the money supply M within a small band around the target path M*, as the Bank of Canada says it is doing.

Friedman (1977) has formally shown that the intermediate-target proce- dure amounts to a very special way of using observations on the money supply to infer information about the (real or financial) sources and sizes of the exogenous shocks and then adjusting policy on the basis of that information. More precisely, the procedure is inefficient for the minimization of E( -

y-)2

in that it does not make an appropriate use of money-stock observations (except in the very restrictive case where the demand for money is totally insensitive to the interest rate and the LM curve is perfectly stable, if the interest rate is the control instrument) and makes no use at all of any other financial or non-financial information.

However, this is only a logical conclusion on the blind application of the intermediate-target procedure as defined, and not an inference that central bankers do not in fact use a better control procedure. As pointed out earlier, the us evidence seems to indicate that the Open Market Committee of the Federal Reserve Board does not adhere to any rigid, mechanical inter- mediate-target procedure but instead 'looks at everything.' In Canada there is ample evidence that the central bank uses much more than pure monetary information to distinguish between real shocks (induced by shifts in the IS curve) and financial shocks (induced by shifts in the LM curve) giving rise to monetary surprises. The Bank's new approach to short-run monetary control is essentially a derivative stabilization rule for interest rates (and more recently the exchange rate) in the face of undesired nominal income shocks, as they are reflected by those changes in the money supply which can be attributed to shifts in the nominal IS curve on the basis of other financial as well as non-financial information. There has not been a knee-jerk reaction to short-term deviation of the money stock from target. On the contrary, be- tween October 1975 and May 1979 the Bank has gone so far as letting M I leave the target band one month out of three. An examination of the fifteen monthly occasions (out of forty-four) on which the M 1 figures were above or below the band reveals that these were instances of important financial shocks (LM shifts due to postal strikes, the CSB market, or an apprehended permanent increase in MI velocity), or were due to lags in the reaction of nominal growth

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets anld monetary policy / 635

to the application of the interest-rate feedback rule (4Q76-2Q77). In 1978 the Bank ran the risk of letting M l fall below the band by maintaining high interest rates in order to stabilize the value of the Canadian dollar, but it was 'saved' by the simultaneously rising trend of nominal GNP growth.

The fourth question refers to one obvious extension of the basic Poole- Friedman approach to the monetary policy problem, namely, the inclusion of the exchange rate together with the interest rate and the reserve base in the list of controllable instruments available to the central bank (Sparks). If the reserve base is eliminated from consideration for institutional reasons, this addition to the list gives rise to the following proposition:

PROPOSITION: The more open the economy the more likely it is that a pure exchange rate strategy will dominate a pure interest-rate strategy. In usual circumstanices, however, the optimal central bank reaction function will be an 'impure' combination of the two. Most itnportant, a pure interest rate strategy would be optimal only if the exchange rate did not influence nominal income and the balance-of-payments equation were perfectly stable.

The proof of this proposition is straightforward and relegated to a technical appendix. It asserts that, from the point of view of exchange market interven- tion, a managed float is optimal.8 It gives theoretical support to the recent preoccupation of the Bank of Canada with 'excessive' exchange rate depre- ciation and to its switch from a pure interest rate strategy to a combined interest-rate-cum-exchange-rate strategy (Bank of Canada, 1979, 6-10). It should also be emphasized that the preoccupation with exchange rate stabili- zation must normally receive some weight in the social preference function of the central bank for two additional reasons. First, 'excessive' exchange rate variations can have huge redistributional consequences within a small open country in the short and medium runs. Second, unanticipated exchange rate changes, whose importance is shown by the bad record of forward exchange rates as predictors of future spot exchange rates, add to the microeconomic risks of doing business between countries. And the more open the economy the more significant these two reasons become.

To summarize the argument of this section, against the standard of the recent developments in the theory of monetary policy just reviewed, the Bank of Canada's stated objective of gradual achievement of a low and stable growth rate of M1 would clearly appear suboptimal. First, the optimal ap- proach stipulates that the mean annual growth rate of M1 should not remain rigidly geared to the non-inflationary growth rate of nominal inicome but should on the contrary fluctuate to offset actively the effects of changing exogenous influences on income, even when forecasts are uncertain, when dynamic policy multipliers are uncertain and operate with long lags, and when private expectations are difficult to predict. Secondly, it has also been estab-

8 Boyer (1978) arrives at a similar result in a somewhat more limited context.

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

636 / Pierre Fortin

lished that the minimization of the variance of MI around some historical mean could not be envisaged as the chance outcome, and even less as a serious objective, of stabilization policy, and that the short-run inter- mediate-target procedure for MI variance minimization could claim to efficiency only in the unlikely case of a perfectly stable and interest-inelastic demand for money. Thirdly, the optimal stabilization procedure in an open economy was shown to involve some kind of managed float in the context of a mixed interest-rate-cum-exchange-rate strategy.

In practice, however, it would be unjust to fault the Bank of Canada too much on the second and third points. I have argued above that the Bank's readiness on occasion to let M I leave the ?2 per cent corridor around its mean target path reveals that it uses much more than pure monetary information to distinguish between the real and the financial shocks giving rise to monetary surprises. Therefore, its approach to monetary policy is by no means com- pletely rigid. Moreover, the 1977-8 weakness of the Canadian dollar has shown the existence of some critical point beyond which the Bank will not permit short-run exogenous shocks to exert excessive pressure on prices and nominal income via the exchange rate.

In the final analysis it is the Bank's pledge to come gradually to set the growth rate of Ml on an annual basis with a view towards achieving a non-inflationary growth rate of nominal income whatever the nature, strength, and frequency of the exogenous shocks affecting the economy which conflicts most clearly with the optimal approach to stabilization policy. This optimal approach calls for cautiously active monetary and fiscal policy - rough tuning as opposed to fine tuning - and not for the monetarist CGR rule that the Bank of Canada now adheres to.

IS THE CGR RULE THE BEST PRACTICAL APPROACH?

I suspect that, if pushed hard enough against the theoretical arguments, most proponents of a CGR rule, and most central bankers actually putting the rule into action, would agree that the monetarist approach is not optimal. But they would go along with it in practice for two reasons. First, they believe that the CGR rule is an improvement over the previous discretionary approach to monetary policy, which historically was applied in less than ideal fashion. And secondly, they criticize the opponents to the CGR rule for failing to provide alternative feedback rules demonstrably superior to the CGR rule and able to be implemented practically.

A fair assessment of the respective merits of the new as against the old approach to monetary policy should be based on a comparison of the respec- tive contributions of the two strategies to a social welfare indicator of the joint unemployment-inflation malaise, everything else being held constant. This is a difficult task, however, because we do not know what weights to assign to inflation and unemployment and how to hold everything else constant, and

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets and monetary policy / 637

because the CGR rule has not been enforced long enough. But what can be done is to listen to the arguments of those who believe that a monetarist rule is a practical improvement over the previous conduct of monetary policy and examine them at face value.

Besides emphasizing the technical difficulties (uncertainty, lags, and ex- pectations) of implementing an activist monetary policy, the Bank of Canada has developed three main arguments in favour of the adoption of a CGR rule and rejecting the unconstrained approach (Bank of Canada, 1976, 11-12):

1 The CGR rule ensures the long-run stabilization both of real GNP growth at potential and of inflation at a small rate.

2 The CGR rule acts as an efficient short-run automatic couritercyclical stabilizer of nominal aggregate spending growth.

3 The temporary increases in the rate of monetary growth, which would be attractive in the short run under an activist policy, tend to fuel persis- tent increases in inflationary expectations and behaviour and are therefore difficult to reverse later (as they must if the longer-run trend of inflation is not to accelerate over time) without adverse short-term effects on econ- omic activity.

Argument 1 is commonly agreed upon by (almost) all macroeconomists, whether monetarist or non-monetarist. It simply asserts that, given enough time, the economy will adjust to any exogenous shock by returning to a steady-state position made of the natural rate of unemployment and of a rate of inflation just equal to the (constant) rate of growth of the money supply, minus the product of the trend growth rate of potential real GNP times the income-elasticity of the demand for real balances. At first glance this argu- ment may not seem relevant to the monetarist-activist controversy, since any activist policy (or non-CGR rule) resulting in some historical average monetary growth will generate the same long-run solution for unemployment and inflation as a CGR policy that would fix monetary growth at that average year after year. The point of the argument, however, is that, contrary to the discipline imposed by a self-enforced or constitutional CGR rule, discretiornary policy does not by itself ensure that low average monetary growth will be achieved, as witnessed, say, by the record of accelerating monetary growth of 1955-75. Hence the real question turns out to be whether the kind of discretionary policy followed before 1975 was in fact responsible for acceler- ating monetary growth and inflation in that period. Argument 3 makes clear that the Bank's answer to this question is affirmative, and I shall comment upon it later.

Argument 2 leaves the long run and offers an idealized picture of the working of CGR rule as a short-run automatic stabilizer. Here we are told that in the face of excessive aggregate spending, stability in the rate of monetary growth will induce an automatic tightening of credit conditions that will eventually check the rate of spending by raising unemployment and lowering

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

638 / Pierre Fortin

inflation. The opposite sequence of events will occur if the level of spending slackens but the quantity of money keeps growing on trend (Bank of Canada, 1976, 1 1). It is clear from the context that the Bank's over-all evaluation of the short-run automaticity and efficiency properties of this derivative interest rate stabilization rule compared with the previous discretionary approach is favourable to the rule.

The claim of automaticity is well-taken, but a proper examination of its real significance is naturally postponed until the discussion of Argument 3. How- ever, an automatic rule is not necessarily a good rule, and the claim of relative efficiency for the CGR rule seems highly questionable. I would argue on the contrary that, compared to the unconstrained approach practiced before 1975, the CGR rule may be distinctly inferior. It is not only theoretically bad; it may be practically worse.

It is hard to understand the rationale for stabilizing nominal income growth in the short run, if prices and quantities constitute separate policy variables. To be sure, the stabilization of nominal spending can make some contribution to social welfare in the aftermath of aggregate demand shocks that produce excessive real growth, decrease unemployment below its natural rate, and accelerate inflation, because then the rise of nominal GNP growth gives an unambiguous signal of the need for monetary restraint. However, there are two basic problems with this approach. First, the feedback rule entailed by the CGR strategy gives rise to a very slow adjustment process which may be acceptable only for small demand shocks. And secondly, in the case of aggregate supply shocks the rule is inefficiently biased towards unemploy- ment creation.

On the first point the Bank has never produced the slightest evidence that a CGR rule can prove to be an effective short-run stabilization device, bringing the economy back to equilibrium quickly after an exogenous shock. It is simply not true that, left to its own stabilizing forces, the economy will correct the effect of any significant shock within one or two years, as the several episodes of high and persisting unemployment and/or inflation since the Depression amply demonstrate. Ironically, one of the most important pieces of evidence of the sluggish adjustment process of the economy to shocks is the Bank's own structural model of the Canadian economy, RDX2, which reveals the prevalence of long distributed lags everywhere in the demand and supply blocks of equations and a slow response of wage and prince inflation to excess demand and, even more, to excess supply pressure (de Bever and Maxwell, 1979). This evidence strongly suggests that a CGR rule is a very ineffective short-run stabilization device and that there is a significant welfare gain to be reaped from cautious monetary activism or from a non-CGR policy feedback rule aiming at rough tuning when the economy is very clearly far from equilibrium. This theory of the 'shot in the arm' to quicken the pace of the adjustment process is precisely what the practice of discretionary policy was all about before 1975.

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets and monetary policy / 639

On the second point it should be noted that under the CGR rule an inflation- ary aggregate supply shock will give rise to a higher level of nominal income growth, to higher interest rates, and to higher uinemployment. The induced recession will be protracted and its depth very pronounced compared to the kind of partially accommodating monetary policy followed, say, in the after- math of the oil price shock of 1974. There are two reasons for this unemployment-generating bias. First, the Phillips curve is non-linear, so that the cumulative excess unemployment and the time required for the return to equilibrium increase more than proportionally with the size of the shock. Secondly, as long as the rate of inflation is above its long-run level we are in a period not only of a high but also of a rising rate of unemployment, since real GNP growth is maintained below potential. Hence, a period of below- equilibrium inflation is needed for real GNP growth to rise above its potential and for unemployment to decrease to its natural rate (e.g. Modigliani, 1977). The absence of monetary accommodation in the face of significant aggregate supply shocks can therefore be very serious in its practical welfare implica- tions. And there is no reason why these kinds of supply shocks in agricultural and basic commodity markets and in exchange rate markets, which have been quite substantial in the 1970s, will not be as prevalent in the 1980s in the world and domestic economies. If this is so, that +2 per cent around the mean target growth rate of M 1 will not provide enough leeway for quick and smooth returns to equilibrium after the shocks.

Argument 3 asserts that discretionary monetary policy is fraught with an inherent inflationary bias, in the sense that monetary accelerations initially intended to be temporary display a natural tendency to become permanent because of the political difficulty of raising interest rates and reversing the monetary growth trend downwards later. This observation calls for some rule (not necessarily the CGR rule) that will check the inflationary 'ratchet' and the stop-go character of monetary expansion described succinctly by Table 3. This is done mainly by ensuring that interest rates will increase automatically by 'the right amount at the right time,' in spite of adverse political pressure. The important question here is whether the positive temporal association between discretionary monetary policy and rising inflation, most notably in 1965-9 and in 1971-4, reflects a causal relationship from the former to the latter, or whether the correlation is spurious.

From 1961 to early 1965 the growth rate of MI was relatively stable at 5 per cent a year but accelerated thereafter to 10 per cent a year in mid-1967, partly to adjust to the once-for-all move out of chequable savings deposits, but essentially to accommodate the rising inflationary trend largely imported from the United States at the going fixed price of the Canadian dollar. In turn, as is well known, the acceleration of inflation in the United States arose from the decision to finance the Vietnam war by printing money instead of raising taxes or interest rates, despite widespread professional warning of excess demand pressure. It was not a technical failure of the monetary activists, but a result of

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

640 / Pierre Fortin

political objections to the medicine (especially after the 'credit crunch' blun- der of 1966), which is precisely the point of Argument 3. This is certainly a valid criticism of monetary activism to some extent, but it is weakened by at least two considerations.

First, in that historical instance the politicians and the public adopted a daring attitude towards the danger of accelerating inflation because they had no fresh experience to warn them of the hard reality of the Phillips curve and the evils of inflation. It is doubtful that such a mistake could be repeated in the 1980s in the light of the macroeconomic events of the last fifteen years, especially in Canada, where the private costs of unemployment have been considerably reduced by the unemployment insurance reform of 1971 and where an anti-inflationary bias of social preferences and of economic policy has consequently developed, rightly or wrongly.9

Secondly, if there was indeed an inflationary bias in favour of low interest rates in the decision-making process at the political level, as many authors have argued (Nordhaus, 1975; Gordon, 1975), monetary activism would be a consequence, not a cause, of this bias, and a strict CGR rule would have had no chance of being accepted by the policy-makers because of the wider swings in interest rates they knew it required. Hence, the very fact that Canada has opted for a CGR rule suggests that the strength of the political bias against high interest rates for anti-inflationary purposes is not as high as might have been thought. '0

The most traumatic experience, though, was the great acceleration of inflation from 1.5 per cent in 1971 to 12.5 per cent in 1974 and the high (and stable) four-quarter growth of M1 which averaged 14 per cent a year between 2Q71 and 2Q74. The stance of Canadian monetary policy in that period is again explained by the objective of exchange rate stabilization, which re- quired accommodation of nominal GNP growth at the requisite levels of interest rates. In a genuine sense, therefore, the cause of monetary accelera- tion, just as in 1965-7, was not monetary activism in Canada but the Canadian monetary rule of fixing the value of the Canadian dollar at about parity with the us dollar, combined with monetary activism in the United States and elsewhere. Was international monetary activism responsible for the accelera- tion of world inflation from 5 per cent in 1971 to 12.5 per cent in 1974? As Table 4 shows, with an average potential growth rate higher than 4 per cent a year for real GNP in the large industrial countries the 10 to 11 per cent average rates of monetary expansion of 1971-3 were consistent with rates of cPi inflation of at most 7 per cent in the long run, so that only about half of the 1974 peak inflation rate of 12.5 per cent can be explained by the delayed impact of previous

9 This is evidenced by the greater amount of excess unemployment which has come to be accepted in Canada in the 1970s both absolutely and relative to the natural rate.

10 This is not intended to contradict the proposition that casting the debate in terms ofthe money supply does make it even easier to gain public acceptance for significant increases in interest rates from time to time.

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets and monetary policy / 641

TABLE 4

Annual rate of growth of the money stock (M 1) and of the consumer price index in fourteen large industrial countries 197 1-6 (percentages)

1971 1972 1973 1974 1975 1976

Money supply 11.3 11.4 10.0 6.6 8.0 8.7 Consumer price index 5.1 4.6 7.5 12.5 10.8 7.7

SOURCE: IMF, Intel national Financial Statistics

monetary growth. What made expansion in Canada particularly strong in 1973-4 was not the excessive monetary growth compared to other countries but the extremely favourable terms-of-trade effect generated by the agricul- tural, raw materials, and oil price explosion, which in turn generated higher wage and price inflation than abroad. Of course the other half of the story is that monetary expansion did in fact accelerate excessively in North America in 1971-3, partly because of the us presidential election of 1972.

Over-all, I take the evidence of the comparative efficiency of the CGR rule and the discretionary policy as practised before 1975 to favour the latter. On the other hand, one can make a mild but convincing case that some non-CGR rules of behaviour may prove to be superior to unconstrained monetary policy, although this case is mildest in countries like Canada where the social preferences against inflation have been perhaps most clearly expressed through the very adoption of a CGR rule.

The search for practical and better alternative (non-CGR) rules should therefore receive high priority in monetary policy research. The claim that the CGR rule is suboptimal, however founded, will not convince central bankers until other feasible, demonstrably superior rules are put forward and tested, since they believe (wrongly in my opinion) that the CGR rule is itself better than the former way of doing things.

The first step towards a systematic policy framework in Canada should be a clear declaration of objectives by the federal government and the federal- provincial conference of premiers. I would support the following list of four objectives:

Steer the economy towards the natural rate of unemployment. This re- quires that a relative consensus among professional economists emerge on the most probable range containing the natural rate. Such a task is not easy, but it seems within reach in view of recent research progress in that area. My own estimate for 1979 is 6.5 per cent.

Reduce the natural rate of unemployment. There are at least three likely reasons why the natural rate has increased by perhaps two percentage points in Canada since 1955: the significant demographic flow of young persons and adult women into the labour force, the distributional anomalies and adverse incentives created by the 1971 unemployment insurance reform, and the jump

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

642 / Pierre Fortin

in some provincial minimum wages in the 1970s. Although little can be done about the demographic tide, a better design of the unemployment insurance regulations and care on relative minimum wage increases would be welcome. Beyond that, policies to counter the seasonal instability of employment and to fight discrimination, protection, and exclusion practices in the labour market are clearly in order.

Keep domestic sources of cost inflation in check. This can be done with the help of agricultural price support policies, minimum wage policies, public sector wage policies, tax policies, energy policies, exchange rate policy, and market power policies. Greater cost stability of course means the cumulative savings of percentage points of excessive unemployment.

Stabilize the exchange rate. The very high costs of transition to a very low domestic rate of inflation in disregard of the rate of inflation achieved in the United States suggest that the relative inflation target adopted by the Eco- nomic Council of Canada in 1973 is sound. In the long run a necessary condition for the fulfilment of this goal is a stable exchange rate. In addition, as emphasized earlier, exchange rate stability enhances price stability directly, reduces the risks of doing business internationally, and avoids potentially huge and arbitrary redistributional shocks, all of which are more important the more open the economy is. Substantial variations of the exchange rate should be kept for the exceptional circumstances in which excessive inflation (as in 1970) or unacceptable unemployment (as in 1977-8) is the only alternative to restoring balance-of-payments equilibrium. Otherwise, I would favour keep- ing the exchange rate of the us dollar in Canadian currency within the relatively narrow band of ?2.5 per cent observed by the Bank of Canada in 1970-3.

The second step would consist in adjusting means to ends. I believe it is necessary to recognize the fundamental principle of the comparative advan- tage of monetary policy for exchange rate and price stabilization and that of fiscal policy for employment stabilization in an open economy (Mundell, 197 1; Dornbusch and Krugman, 1976). If some natural-rate-of-unemployment budget surplus criterion is adopted for fiscal policy, the application of this principle yields precise, albeit flexible, rules as to the required over-all orien- tation of credit conditions and of public sector budgets. These rules would be simple and understandable; they could weaken public resistance to high interest rates when needed; they could speed up the adjustment of the economy to significant exogenous shocks; they could accommodate supply shocks partially; and they would contain some elements of a safeguard against the apprehended inflationary bias of discretionary policy.

The foregoing proposals have been only briefly sketched and clearly need refinement and debate. However, they serve to indicate that alternative stabilization rules can be designed and compared with the rather inefficient monetarist CGR rule.

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets and monetary policy /643

CONCLU SION

My assessment of the adoption of a constant-growth-rate rule for monetary expansion by the Bank of Canada since 1975 has not been very enthusiastic. The Bank has succeeded in reducing the mean and variance of the growth rate of M 1 and is more seriously constrained by its new approach to monetary policy than it was by its previous approach in the 1960s and early 1970s. I have argued that the CGR rule is distinctly inferior to the traditional optimal policy approach even when it is amended to take account of uncertainty, lags, and private expectations. I have expressed doubts about the efficiency claimed for the rule compared with the previous more activist strategy as implemented and about the need to protect the Canadian economy against the alleged inflationary bias of discretionary policy. Finally, I have sketched a practical alternative policy framework in which clearly stipulated objectives about inflation and unemployment could be achieved with the help of a more flexible rule based on Mundell's principle of comparative advantage.

APPENDIX: PROOF OF THE PROPOSITION

Assume one wishes to minimize the loss function

E(y - y*)2 (Ey - y*)2 + vary,

where y * is the fixed target value of y, subject to the system

y -a1r + a2e + az +- u, (la)

e = -fir +f2y +fz + u2, (2a)

by the appropriate choice of either a pure interest rate strategy or a pure exchange rate strategy. Here, y is nominal income, r is the interest rate, e is the exchange rate, z is a vector of exogenous variables, a 1, a 2, f i, and f2 are positive constants, a and f are vectors of coefficients, and u1 and u2 are zero-mean random disturbances. Equations (la) and (2a) are formally identi- cal to equations (8) and (7) in Sparks. Then under the pure interest rate strategy E(y - y*)2 iS minimized for Fy = y * or r is set at the value

r*= (a1 + a2f1) ' ((a + a2f)z - (1 - a2J2)y*) a2f2 < 1

in which case

y - y* = (1 - a2f2)-' (U1 + a2U2)

and

E(y y*)2- vary (1- a2f2)2(o-I + a 2o2 + 2a2pa10-2), (3a)

a, and 0-2 being the standard deviations of the zero-mean disturbances u 1 and

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

644 / Pierre Fortin

u2 respectively and p their correlation coefficient. Under the pure exchange rate strategy E(y -y *)2 is again minimized for Ey = y * or e is set at the value

e* = (a2+ h)-l ((1 + hf2)y* (a - hb)z), h = a1f,

in which case

y - y (1 + hf2)-l (ul - hU2)

and

E(y - y*)2 = vary = (1 + hf2)-2 (o- + h2o22 - 2hp-102). (4a)

Now, let

P = ((1 - a2f2)I(1 ? hf2))2 (0-2 + h2 - 2pho-)I(oT2 + a2 ? 2pa2O), (Sa)

where oa = O1/f2, be the ratio of var y under the e-strategy to var y under the r-strategy, i.e. the ratio of (4a) to (3a). Then one must select the e-strategy if t < 1 and the r-strategy if P > 1.

In order to give the proposition a precise content in terms of the values of the parameters a2, f2, h, and a-, which influence the value of P, one has to indicate how these parameters change when an economy becomes more open. We take 'greater' openness to mean the following:

- a2 increases, because depreciation of the domestic currency (a rise in e) raises both real aggregate demand and prices to a larger extent (recall that y is nominal income);

- h decreases, becausef 1 increases as international capital flows become more elastic;

- f2 increases, to the extent that, as an-indicator of the demand for imports of foreign goods and financial claims, y becomes a more important determin- ant of the exchange rate;

- o- decreases, as foreign exchange market surprises become more significant and frequent relative to aggregate demand and supply shocks (O72

rises relative to oh).

The squared expression on the right-hand side of (5a) is smaller than 1, and the more so the largerf2 is. Hence, a sufficient - but by no means necessary - condition for T < 1 to hold is that

var (ul - hu2) - var (uI + a2u2),

which is fulfilled for a2 - h - 2po-. As a2 increases, as h decreases, and as C- tends to zero, this last inequality is more likely to be satisfied (for arbitrary values of p), as claimed by the proposition.

The best combined strategy consists of selecting values g1 and g2 in the equation

e = g1 + g2r,

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

Monetary targets and monetary policy / 645

so that E(y - y*)2 iS minimized, again subject to (la) and (2a). The optimal value of g2 is readily found to be

9 2 - (a, -f1f2o-2 - (f1 - a1f2)po-)I(a2 +f202 + (1 + a2f2)Po).

Clearly, a pure r-strategy is optimal only forg2 = oo, that is, for a2 = O and o- = 0 (for arbitrary values of p), as claimed by the proposition.

REFERENCES

Baily, Martin N. (1978) 'Stabilization policy and private economic behavior.' Brook- ings Papers on Economic Activity 1, 11-50

Bank of Canada (1976) Annual Report 1975 (Ottawa: Bank of Canada) Bank of Canada (1979) Annual Report 1978 (Ottawa: Bank of Canada) Boyer, Russell S. (1978) 'Optimal foreign exchange market intervention.' Journal of

Political Economy 86, 1045-55 Brainard, William (1967) 'Uncertainty and the effectiveness of policy.' American

Economic Review 57, 411-25 Canada (1971) 283, 1970-71. The Senate of Canada. Proceedings of the Standing

Senate Committee on National Finance. No 21. Thursday June 17, 1971. Eighteenth Proceedings on the Question ofGrowth, Employment andPrice Stabil- ity (Ottawa: Queen's Printer)

Cooper, J. Phillip and Stanley Fischer (1973) 'Stabilization policy and lags.' Journal of Political Economy 81, 847-77

Courchene, Thomas J. (1977) The Strategy of Gradualism: An Analysis of Bank of Canada Policy from Mid-1975 to Mid-1977 (Montreal: C.D. Howe Research Insti- tute)

de Bever, Leo and Thomas Maxwell (1979) 'An analysis of some of the dynamic properties of RDX2.' This JOURNAL 12, 162-81

Decaluwe, Bernard (1972) Variables instrumentales optimales dans un modele stochastique: une ge'ne'ralisation (Working Paper 7208, Institut des Sciences Economiques, Louvain)

Dornbusch, Rudiger and Paul Krugman (1976) 'Flexible exchange rates in the short run.' Brookings Papers on Economic Activity 3, 537-75

Federal Reserve Bank of New York (1974) Monetary Aggregates andMonetary Policy (New York: Federal Reserve Bank of New York)

Fischer, Stanley (1977) 'Long-term contracts, rational expectations, and the optimal money supply rule.' Journal of Political Economy 85, 191-206

Friedman, Benjamin M. (1975) 'Targets, instruments, and indicators of monetary policy.' Journal of Monetary Economics 1, 443-73

Friedman, Benjamin M. (1977) 'The inefficiency of short-run monetary targets for monetary policy.' Brookings Papers on Economic Activity 2, 293-335

Friedman, Benjamin M. (1979) 'Optimal expectations and the extreme information assumptions of "rational expectations" macromodels.' Journal of Monetary Eco- nomics 5, 23-41

Friedman, Milton (1953) 'The effects of a full-employment policy on economic stabil- ity: A formal analysis.' In Essays in Positive Economics (Chicago: lJniversity of Chicago Press)

Gordon, Robert J. (1975) 'The demand for and supply of inflation.' Journal ofLaw and Economics 18, 807-36

Gordon, Robert J. (1976) 'Recent developments in the theory of inflation and unem- ployment.' Journal of Monetary Economics 2, 186-219

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions

646 / Pierre Fortin

Hall, Robert E. (1978) 'The macroeconomic impact of changes in income taxes in the short and medium runs.' Journal of Political Economy 86, S71-S85

Kravis, Irving and Robert E. Lipsey (1978) 'Price behavior in the light of balance of payments theory.' Journal of International Economics 8, 193-246

Lucas, Robert E. Jr (1976) 'Econometric policy evaluation: a critique.' In Brunner, Karl and Allan H. Meltzer, eds The Phillips Curve and the Labor Market, Carnegie-Rochester Conference Series on Public Policy. Vol. 1 (Amsterdam: North-Holland) 19-46

McNees, Stephen K. (1978) 'The rationality of economic forecasts.' American Eco- nomic Review 68, 301-5

Modigliani, Franco (1977) 'The monetarist controversy or, should we forsake stabili- zation policies?' American Economic Review 67, 1-19

Mundell, Robert A. (1971) The Dollar and the Policy Mix 1971. Essays in International Finance 85 (Princeton University, International Finance Section)

Nordhaus, William D. (1975) 'The political business cycle.' Review of Economic Studies 42, 169-90

Officer, Lawrence 0. (1976) 'Purchasing power parity theory of exchange rates: a review article.' International Monetaly Fund Staff Papers 23, 1-60

Pierce, James L. (1978) 'The myth of Congressional supervision of monetary policy.' Journal of Monetary Economics 4, 363-70

Poole, William (1970) 'Optimal choice of monetary policy instrument in a simple stochastic macro model.' Quarterly Journal of Economics 84, 197-216

Rymes, Thomas K. (1979) 'Money, efficiency and knowledge.' This issue of the JOURNAL

Sargent, Thomas J. and Neil Wallace (1975) "'Rational" expectations, the optimal monetary instrument, and the optimal money supply rule.' Journal of Political Economy 83, 241-57

Theil, Henri (1961) Economic Forecasts and Policy 2nd edition (Amsterdam: North- Holland)

This content downloaded from 195.34.79.174 on Thu, 12 Jun 2014 18:33:15 PMAll use subject to JSTOR Terms and Conditions