Embed Size (px)

Citation preview

Monetary Policy and Inflation TargetingModule 4

Contemporary Themes in India’s

Economic Development and the Economic Survey.

Arvind Subramanian

Chief Economic Adviser

Government of India

MINISTRY OF FINANCE

GOVERNMENT OF INDIA

1

Overview

• Objective of Monetary Policy

• Monetary Policy Transmission

• Monetary Policy Framework

• Rationale

• How it works

2

Part I

Objective of Monetary Policy

3

Objective of Monetary Policy

• Keep inflation and inflation

expectations low and stable

• Help stabilize economy, including

avoiding and responding to

financial crisis

4

Objective of Monetary Policy

why are price and economic stability important?

• High inflation creates uncertainty, reduces investment

and reduces economy’s supply potential

• Inflation adversely affects income distribution

• Inflation is a tax on poor

• Iron Law of Indian political-economy – Inflation more

than 5% counterproductive

5

Objective of Monetary Policy

6

1

3

5

7

9

11

13

1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

pe

r ce

nt

Indian CPI inflation

Economy

overheating

Economy below

potential

Potential

Economy

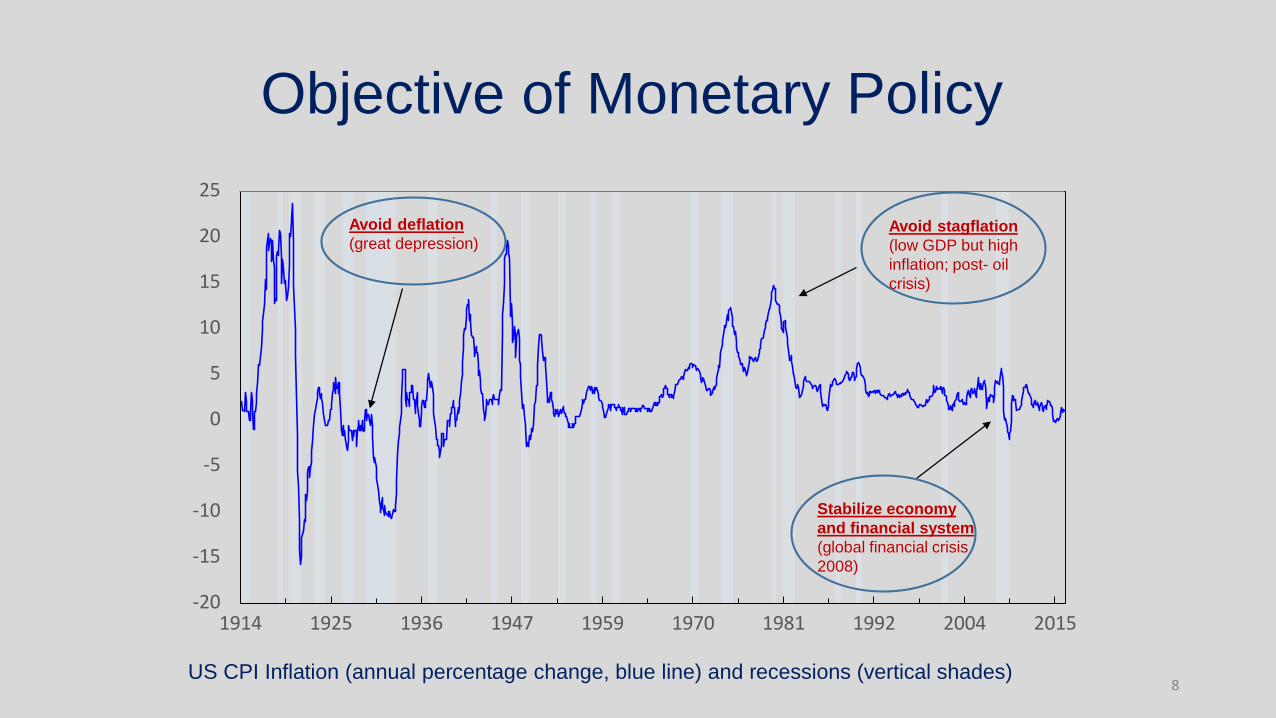

Objective of Monetary Policy

7

25

20

15

10

5

0

-5

-10

-15

-201914 1925 1936 1947 1959 1970 1981 1992 2004 2015

US CPI Inflation (annual percentage change, blue line) and recessions (vertical shades)

Avoid stagflation

(low GDP but high

inflation; post- oil

crisis)

Avoid deflation

(great depression)

Stabilize economy

and financial system

(global financial crisis

2008)

Objective of Monetary Policy

8

Part II

Transmission of Monetary Policy

9

Monetary Policy Transmission 1: Interest Rate and Borrowing Channel

6

6.5

7

7.5

8

8.5

9

9.5

10

10.5

Apr.

21,

201

7

Ma

r. 3

, 2

01

7

Ja

n.

13

, 20

17

Nov. 2

5, 2

016

Oct. 7

, 2

016

Aug

. 19

, 2

016

Ju

l. 1

, 20

16

Ma

y 1

3,

20

16

Ma

r. 2

5,

20

16

Ja

n.

22

, 20

16

Dec. 4

, 20

15

Oct. 1

6,

201

5

Aug

. 28

, 2

015

Ju

l. 1

0, 2

015

Ma

y 2

2,

20

15

Ma

r. 2

7,

20

15

Fe

b.

6, 2

01

5

Dec. 1

9, 2

014

Oct. 3

1,

201

4

Sep

. 12

, 2

014

Ju

l. 2

5, 2

014

Ju

n.

6,

201

4

Apr.

18,

201

4

Fe

b.

28,

20

14

Ja

n.

10

, 20

14

Nov. 2

2, 2

013

Oct. 4

, 2

013

Aug

. 16

, 2

013

Ju

n.

21

, 20

13

Ma

y 3

, 2

01

3

Ma

r. 1

5,

20

13

Ja

n.

25

, 20

13

Dec. 7

, 20

12

Oct. 1

9,

201

2

Aug

. 31

, 2

012

Ju

l. 6

, 20

12

Ma

y 1

8,

20

12

Ma

r. 3

0,

20

12

Fe

b.

10,

20

12

Dec. 2

3, 2

011

Policy Repo Rate

Base Rate Mean

Term Deposit Rate Mean

Policy rate lending rate borrowing 10

Monetary Policy Transmission 1A: Interest Rate and Borrowing Channel, Transmission of Recent Rate Cuts

Impeded by Rising NPAs

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

Apr.

21,

201

7M

ar.

10

, 20

17

Ja

n.

27

, 20

17

De

c. 1

6, 2

016

Nov. 4

, 20

16

Sep

. 23

, 2

016

Aug

. 12

, 2

016

Ju

l. 1

, 20

16

Ma

y 2

0,

20

16

Apr.

8, 2

016

Fe

b.

19,

20

16

Ja

n.

1,

201

6N

ov. 2

0, 2

015

Oct. 9

, 2

015

Aug

. 28

, 2

015

Ju

l. 1

7, 2

015

Ju

n.

5,

201

5A

pr.

24,

201

5M

ar.

6,

201

5Ja

n.

23

, 20

15

De

c. 1

2, 2

014

Oct. 3

1,

201

4S

ep

. 19

, 2

014

Aug

. 8,

20

14

Ju

n.

27

, 20

14

Ma

y 1

6,

20

14

Apr.

4, 2

014

Fe

b.

21,

20

14

Ja

n.

10

, 20

14

No

v. 2

9, 2

013

Oct. 1

8,

201

3S

ep

. 6,

20

13

Ju

l. 2

6, 2

013

Ju

n.

7,

201

3A

pr.

26,

201

3M

ar.

15

, 20

13

Fe

b.

1, 2

01

3D

ec. 2

1, 2

012

Nov. 9

, 20

12

Sep

. 28

, 2

012

Aug

. 17

, 2

012

Ju

n.

29

, 20

12

Ma

y 1

8,

20

12

Apr.

6, 2

012

Fe

b.

24,

20

12

Ja

n.

13

, 20

12

Dec. 2

, 20

11

Policy Repo Rate

Base Rate Mean

Term Deposit Rate Mean

11

Monetary Policy Transmission 2: Exchange Rate Channel

6.0

6.5

7.0

7.5

8.0

8.5

9.0

0.014

0.015

0.016

0.017

0.018

0.019

0.02

0.021

No

v. 11, 2011

Jan

. 13, 2012

Mar

. 16, 2012

May

18, 2012

Jul.

27, 2012

Sep

. 28, 2012

No

v. 30, 2012

Feb

. 1, 2013

Ap

r. 5

, 2013

Jun

. 7, 2013

Aug.

16, 2013

Oct

. 18, 2013

Dec

. 20, 2013

Feb

. 21, 2014

Ap

r. 2

5, 2014

Jun

. 27, 2014

Aug.

29, 2014

Oct

. 31, 2014

Jan

. 2, 2015

Mar

. 6, 2015

May

15, 2015

Jul.

17, 2015

Sep

. 18, 2015

No

v. 20, 2015

Jan

. 22, 2016

Ap

r. 8

, 2016

Jun

. 10, 2016

Aug.

12, 2016

Oct

. 14, 2016

Dec

. 16, 2016

Feb

. 17, 2017

Ap

r. 2

1, 2017

$/Rs Repo(RHS)

Policy rate capital inflow weaker local currency (depreciation) 12

Monetary Policy Transmission 3:

Financial Savings Channel

0

2

4

6

8

10

12

14

-2

-1

0

1

2

3

4

5

6

7

8

9

Ja

n-1

2

Ma

r-1

2

Ma

y-1

2

Ju

l-1

2

Se

p-1

2

Nov-1

2

Ja

n-1

3

Ma

r-1

3

Ma

y-1

3

Ju

l-1

3

Se

p-1

3

No

v-1

3

Ja

n-1

4

Ma

r-1

4

Ma

y-1

4

Ju

l-1

4

Sep-1

4

No

v-1

4

Ja

n-1

5

Ma

r-1

5

Ma

y-1

5

Ju

l-1

5

Se

p-1

5

No

v-1

5

Ja

n-1

6

Ma

r-1

6

Real interest rate based on

average inflation of CPI and

WPI

Real Deposit growth

(RHS)

Policy Rate in deposits rate Financial Savings

13

Part III

Monetary Policy Framework

14

India’s Monetary Policy Framework

• India has recently shifted to an inflation targeting framework

• Standard framework used by advanced country central banks

• What is inflation targeting (IT) all about?

15

• Money targeting?

• Exchange rate?

money demand too unstable!

increasing capital mobility, speculative attacks

• IT developed pragmatically

• Disinflation: Canada and New Zealand failed with money targeting

in 1980s, Chile with exchange-rate-based stabilization policies

• End of pegs: U.K., Sweden (1993), Czech Rep. (1997), Brazil (1999)

History of Inflation Forecast

Targeting

• Break of Bretton-Woods system in the 1970s world moved from

fixed to floating regimes need for a new nominal anchor

• Unsuccessful alternatives to IT

16

Understanding IT

• Three key elements

• Objective: inflation target

• Supporting framework: institutional arrangements

• Decision rule: central bank reaction function

17

Empirical Evidence on IT

• OECD: No significant effect on inflation average and variability

• EMEs: Lower average inflation and, typically, inflation

variability. Inflation in IT-countries has come down from a

higher level18

Three questions

• Why an inflation target?

• What institutional arrangements?

• What decision rule?

19

Three questions

• Why an inflation target?

• What institutional arrangements?

• What decision rule?

20

Many potential objectives

• Ensure stable prices

• Promote growth

• Maintain exchange rate peg

• Preserve financial stability

• Contain current account deficit

21

First Answer

• Price stability is very important

22

Second Answer

• India’s historical experience

• Question: why an inflation target now, two decades after IT became popular in the rest of the world?

• Answer: until recently, no pressing reason to change the framework. RBI had kept inflation low, close to world norms

• But after the Global Financial Crisis, world inflation collapsed, while Indian inflation soared

23

Historical Inflation: India and Others

-8

-6

-4

-2

0

2

4

6

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Inflation Differential: India and low/middle income (LMI) countries

Inflation in India

higher than LMI

countries

Inflation in India

lower than LMI

countries

24

Five years of double-digit inflation

1

4

7

10

13

16

19

Ja

n-0

7A

pr-

07

Jul-07

Oct-

07

Ja

n-0

8A

pr-

08

Ju

l-0

8O

ct-

08

Ja

n-0

9A

pr-

09

Ju

l-0

9O

ct-

09

Ja

n-1

0A

pr-

10

Ju

l-1

0O

ct-

10

Jan-1

1A

pr-

11

Ju

l-1

1O

ct-

11

Ja

n-1

2A

pr-

12

Ju

l-1

2O

ct-

12

Ja

n-1

3A

pr-

13

Ju

l-1

3O

ct-

13

Ja

n-1

4A

pr-

14

Jul-14

Oct-

14

Ja

n-1

5A

pr-

15

Ju

l-1

5O

ct-

15

Ja

n-1

6A

pr-

16

Ju

l-1

6O

ct-

16

Ja

n-1

7A

pr-

17

Inflation Repo Rate

25

IT is a promise

• IT is a commitment by the government and RBI that they will

never allow this to happen again

• To show their seriousness, they have formalised the

commitment in a law

• But why only a inflation target? What about the other

objectives?

26

Third answer

• Targeting multiple objectives is problematic

• RBI previously followed a “multiple objectives” regime; that’s how inflation

control was lost

• Tinbergen rule: for every objective, you need an instrument

• Central banks only have one main instrument – interest rates!

• Which means they can really aim at only one objective

27

What about other objectives?

• Central banks still care about:

• growth

• exchange rate

• financial stability

• How do central banks deal with these objectives under IT?

28

Growth objectives

• Growth concern: if interest rates are too high, they could “kill”

the economy

• But how can the RBI chase two targets without violating

Tinbergen Rule?

29

A Miracle!

30

Divine coincidence

• Equilibrium equation: aggregate demand (planned expenditure, PE) =

aggregate supply (Y)

• If PE < Y, that means output is likely to slump and inflation will be “too low”

cut rates, cure both!

• If PE > Y, the economy is overheating and inflation will be too high

raise rates, cure both!

• Miracle: aiming for an inflation target means stabilizing economic growth

31

Caution: miracles not guaranteed!

• Assumed supply is fixed

• But what if there is a supply shock?

• Favourable (fall in oil/food price)

• Best of both worlds: inflation falls and growth rises

• Unfavourable (rise in oil/food price, possibly GST)

• Stagflation: inflation rises and growth falls conflict!

32

Dealing with supply shocks

• Priority is given to controlling inflation

• Cannot control the “first round” impact on price level

• Focus on making sure first round increase doesn’t trigger many subsequent rounds (embedded inflation)

33

Exchange rate objectives

• Exchange rate is more problematic

• Maintaining competitiveness is important

• But central banks face trilemma. Cannot have all three:

• Independent monetary policy (inflation target)

• Exchange rate target

• Free flow of capital

34

The Impossible Trilemma

Only two of the three are possible

Perfect capital mobility;

Fixed/managed exchange rate; and

Independent monetary policy (IMP)

35

The Impossible Trilemma

The Impossible Trinity

Independent

Monetary Policy

Perfect Capital Mobility

Fixed

Exchange

RateChina

36

Impossible Trilemma – Case I

Fixed/Managed

ERIMP

Restrictions on

K-mobility

4

5

6

7

8

9

10

Ja

n-0

7

Au

g-0

7

Ma

r-0

8

Oct-

08

Ma

y-0

9

De

c-0

9

Ju

l-1

0

Fe

b-1

1

Se

p-1

1

Ap

r-1

2

No

v-1

2

Ju

n-1

3

Ja

n-1

4

Aug-1

4

Mar-

15

Oct-

15

CNY/USD

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Ja

n-0

7

Se

p-0

7

Ma

y-0

8

Ja

n-0

9

Se

p-0

9

May-1

0

Ja

n-1

1

Se

p-1

1

Ma

y-1

2

Ja

n-1

3

Se

p-1

3

Ma

y-1

4

Ja

n-1

5

Se

p-1

5

Spread b/w China and US interest rate

37

Impossible Trilemma – Case II

Fixed/Managed

ER

Perfect

K-mobility

MP

independence

lost

5

7

9

11

13

15

17

0.0

1.9

3.8

5.7

7.6

9.5Ja

n-0

7

Ap

r-0

7

Ju

l-0

7

Oct-

07

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oct-

08

Ja

n-0

9

Ap

r-0

9

Ju

l-0

9

Oct-

09

Ja

n-1

0

Repo Rate

Fed Rate

Inflation (RHS)

39

41

43

45

47

49

51

Ja

n-0

7

Apr-

07

Ju

l-0

7

Oct-

07

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oct-

08

Ja

n-0

9

Ap

r-0

9

Ju

l-0

9

Oct-

09

Ja

n-1

0

Rs./US$

38

Impossible Trilemma – Case III

IMPPerfect

K-mobilityFlexible ER

12

13

14

15

16

17

18

19

20

21

2.8

3.8

4.8

5.8

6.8

7.8

8.82

00

4-0

8-0

1

200

4-1

0-0

1

200

4-1

2-0

1

200

5-0

2-0

1

200

5-0

4-0

1

200

5-0

6-0

1

200

5-0

8-0

1

200

5-1

0-0

1

200

5-1

2-0

1

200

6-0

2-0

1

200

6-0

4-0

1

200

6-0

6-0

1

200

6-0

8-0

1

200

6-1

0-0

1

200

6-1

2-0

1

CPI SELIC (RHS)

60

65

70

75

80

85

200

4-0

8-0

1

200

4-1

0-0

1

200

4-1

2-0

1

200

5-0

2-0

1

200

5-0

4-0

1

200

5-0

6-0

1

200

5-0

8-0

1

200

5-1

0-0

1

200

5-1

2-0

1

200

6-0

2-0

1

200

6-0

4-0

1

200

6-0

6-0

1

200

6-0

8-0

1

200

6-1

0-0

1

200

6-1

2-0

1

NEER

39

Possible strategies

• Capital controls: allow exchange rate targeting, but tight controls will cut off inflows needed for growth

• FX intervention: can limit exchange rate appreciation, but will inflate money supply; excessive intervention will jeopardise inflation target

• “Divine coincidence”: appreciation reduces inflation, allowing interest rates to be cut; alleviates but rarely solves problem

• No central bank has found a perfect solution. RBI relies on a mix of above.

40

Group Preference ReasonsManufacturers Low interest rates, weak currency Profits increase, even if some inputs are imported, since

market share grows. This applies both to exporters (clothing)

and to firms producing for domestic market but competing

with imports(steel, aluminium)

Domestically oriented firms Low interest rates Profits increase; debt burden declines

Infrastructure companies Strong currency Typically borrow in dollars, earn in rupees. Strong currency

contains debt service burden without affecting revenues.

Care less about domestic interest rates

Households High interest rates Greater return on savings. Household saving far outweighs

household borrowing.

Equity investors -- Domestic Low interest rates Corporate profits increase, and hence returns.

Equity investors -- Foreign Low interest rates, strong

currency

Combination boosts dollar returns. Tension: low rates

typically lead to weaker currency.

Bond investors -- Domestic Falling interest rates Generates capital gains. Banks prefer low rates; other

investors (LIC) prefer high rates.

Bond investors -- Foreign High but falling interest rates,

strong currency

Combination maximizes dollar returns. Tension: falling rates

weaken currency.

Government Low interest rates Low rates reduce debt service. Extra growth or inflation

increases revenues.

Institutional Biases on Interest Rates and Exchange Rates

41

Financial stability objectives

• Financial stability clearly important (see: Global Financial Crisis)

• Most central banks use prudential/regulatory measures to ensure

stability

• Others argue that monetary policy should also be used, to

reinforce prudential measures

• Increase rates if banks are lending excessively

• Reduce rates if banking system is under stress

42

Bottom Line

• IT means central bank has an inflation target

• Does not mean that inflation is the only objective

• Means that inflation is the primary objective

• Others can be pursued, but inflation takes precedence if a conflict arises

43

Operationalising the Target

• Once IT regime is agreed, must decide:

• particular measure of inflation to target

• specific level of inflation target

44

What Inflation Target?

3.0

3.4

3.8

4.2

4.6

5.0

5.4

5.8

6.2

Ja

n-1

5

Fe

b-1

5

Ma

r-1

5

Ap

r-1

5

Ma

y-1

5

Ju

n-1

5

Ju

l-1

5

Au

g-1

5

Se

p-1

5

Oct-

15

No

v-1

5

De

c-1

5

Ja

n-1

6

Fe

b-1

6

Ma

r-1

6

Ap

r-1

6

Ma

y-1

6

Ju

n-1

6

Ju

l-1

6

Au

g-1

6

Se

p-1

6

Oct-

16

No

v-1

6

De

c-1

6

Ja

n-1

7

Fe

b-1

7

Ma

r-1

7

CPI Headline CPI Core

45

Virtues of CPI

• CPI Headline or CPI Core?• CPI Headline includes oil and food prices whose prices cannot be controlled by

the RBI

• CPI Core basket is 47.3% of the overall CPI basket – RBI can only influence CPI core basket prices

• If so, why all central banks target CPI Headline?• CPI headline reflects the prices consumers and savers face

• Easier to communicate

• Inflation expectations are based on headline CPI inflation46

What level advanced countries target?

• Initially, IT central banks took “price stability” objective literally• Targeted inflation no more than 2 percent

• Since Global Financial Crisis, emphasis on symmetry• Tried to keep inflation near 2 percent, stimulate if too low

• Some have argued for higher target of around 4 percent, to allow highly negative real rates in case of severe recessions

47

What level target/emerging markets?• Many EM’s have targetted inflation around 4 percent, India: 2-6

percent

• Reasons

• EM’s have more bottlenecks, difficult to target very low inflation

• target would keep nominal exchange rate stable

• Maths

• Assume EM productivity growth is 2 percentage points higher than AEs,

• Then EM wage/price growth can be 2 percentage point higher without loss

of competitiveness

• So no need for nominal rate to depreciate

48

Three Questions

• Why an inflation target?

• What institutional arrangements?

• What decision rule?

49

Credibility

• Credibility is critical for central banks

• If the public doesn’t believe the central bank is committed to an

inflation target, interest rates will need to be kept high to prove

intent

• To reinforce credibility, IT central banks institutionalize their

commitment to low inflation

50

Monetary Policy Committee

• IT central banks have monetary policy committees (MPC)

• Purpose: to decide on monetary policy

• Reasons: • Better decision-making, as members bring outside views

• Better credibility, when decisions endorsed by experts

• India’s MPC:• 3 from RBI, including Governor

• 3 external members, appointed by government

• Governor has casting vote

51

Accountability

• Government will hold RBI accountable for achieving inflation target

• Any deviation for three consecutive quarters will have to be explained

• In case of a failure, RBI will have to:• Specify the reasons

• Suggest remedial actions

• Estimate the time period within which the target will be achieved

52

Transparency

• To enhance credibility, RBI explains its actions to the

public:

• Press conference

• Interviews

• Inflation report

• Speeches

53

Independence

• Independence is critical

• Government has set the policy• assigned inflation target to RBI

• RBI needs operational independence so it can achieve target

54

Operational Independence

• RBI must be free to choose appropriate interest rate

• Equally important: RBI must seen to be free

• Otherwise, decisions are seen as politically motivated

• Credibility is damaged, undermining entire exercise

55

Three questions

• Why an inflation target?

• What institutional arrangements?

• What decision rule?

56

Quiz!

• Let’s say that the inflation target is a point target of 4 percent

• What should the RBI do if inflation rises to 7 percent?

• What should it do if inflation falls to 2 percent?

57

Wrong!

58

Reason

59

The Importance of Lags

• Monetary policy cannot control aggregate demand instantaneously

• Effects take about 1 to 2 years

• Implication: monetary policy must be forward looking

60

Looking Forward

• Good monetary policy requires sophisticated, model-based

inflation forecast

• To assess likely path of inflation

• Appropriate interest rate path

• To guide expectations, most central banks (including RBI)

publish their inflation forecasts

• Some also publish expected interest rate path61

Judgement

• But economic models aren’t perfect; future difficult to predict

• Setting monetary policy still requires judgement

• Monetary Policy Committee can help

• But expect the unexpected: inflation will deviate from target

62

Correcting Deviations• Example:

• Target: 4 percent

• Actual: 7 percent

• Question: when should inflation return to target

• Problem 1: try to return to target too soon, high interest rates will “kill”

economy

• Problem 2: adopt gradual approach, high inflation will become entrenched,

and require very high interest rates to eradicate

63

Inflation Forecast Targeting

• Central banks cannot and should not attempt to always achieve inflation target

• Instead, they should target their inflation forecast

• Meaning: set policy in way that target is expected to be achieved over 2 year policy horizon

• Better name: inflation forecast targeting (IFT)

64

Possible Evolution in Inflation Targeting

• Nominal GDP Target

• Forward Guidance

• Olivier Blanchard Solution

65

Answers• Why an inflation target?

• Maintaining price stability is the fundamental objective of central bank

• Other objectives can be pursued, as long as they don’t pose a conflict

• What institutional arrangements?

• Monetary Policy Committees

• Accountability

• Transparency

• Operational independence

• What policy strategies?

• Forward looking,

• Policymaking is difficult, requires careful assessment and judgement66

Recommended Readings

• Urjit Patel Committee Report

67

Thank You

68