Embed Size (px)

Citation preview

© 2012 Deloitte LLP Private and confidential

Mobile taxation in Africa and the Kenyan case study

February 2012Davide Strusani, Deloitte LLP

© 2012 Deloitte LLP Private and confidential

Mobile telephony is often subject to discriminatory taxation in developing countries compared to other services

• The GSMA has recently commissioned Deloitte to undertake a global study on consumer taxation on mobile services in 111 countries worldwide

• We present and discuss here the results of the study in relation to Africa

• We also discuss the findings of a study that measures the relationship between mobile telephony and economic growth

• Finally, we show the positive impact of reductions in mobile telephony taxation in Kenya

2

© 2012 Deloitte LLP Private and confidential

In our study, tax is measured as a proportion of mo bile service costs

• Mobile service costs are expressed as Total Cost of Mobile Ownership (TCMO) and the Total Cost of Mobile Usage (TCMU)

3

TCMO

Handset Connection Rental Calls SMS

Handset Cost Tax Connection Cost

Tax Rental Cost Tax Call Usage Price

Tax SMS Usage Price

Tax

VAT( $)

Customs Duty

VAT( $) VAT( $) VAT( $)

Telecoms Specific Tax

Telecoms Specific Tax

Telecoms Specific Tax

Telecoms Specific Tax

Telecoms Specific Tax

VAT( $)

Total TaxesVAT ($), Customs Duty, Telecoms Specific Tax

Total Taxes as a proportion of service costs

Service cost without tax

© 2012 Deloitte LLP Private and confidential

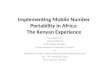

Gabon, DRC and Madagascar have the highest tax as p roportion of TCMO in Africa

4

37.20%

29.14%

28.33%

28.17%

27.80%

26.23%

24.47%

23.82%

23.29%

22.01%

21.21%

20.53%

20.37%

20.18%

18.90%

18.74%

18.59%

18.41%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Gabon

Dem Rep. Congo

Madagascar

Uganda

Tanzania

Zambia

Rwanda

Sierra Leone

Niger

Ghana

Senegal

Kenya

Cameroon

Congo B

Cote d'Ivoire

Guinea

Chad

Global Average

Source: Deloitte/GSMA, Global Mobile Tax Review

Tax as a proportion of TCMO

© 2012 Deloitte LLP Private and confidential

Taxes on mobile usage, or ‘airtime taxes’, have als o increased significantly in the last four years in Africa

5

18%

12%

10%

10%

10%

10%

10%

7%

6%

5%

5%

3%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Gabon

Uganda

Dem Rep. Congo

Kenya

Sierra Leone

Tanzania

Zambia

Madagascar

Ghana

Rwanda

Senegal

Niger

18%

12%

10%

10%

10%

10%

10%

7%

6%

5%

5%

3%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Gabon

Uganda

Dem Rep. Congo

Kenya

Sierra Leone

Tanzania

Zambia

Madagascar

Ghana

Rwanda

Senegal

Niger

Source: Deloitte/GSMA, Global Mobile Tax Review

© 2012 Deloitte LLP Private and confidential

Tax as a share of handset costs represents over two thirds of the costs of a handset in Gabon and Niger

6

80%66%

49%49%

48%48%

46%45%

39%38%

35%31%

30%29%

28%27%27%

25%23%

0% 10% 20% 30% 40% 50% 60% 70% 80%

GabonNiger

CameroonCongo BRwandaGuinea

MadagascarDem Rep. Congo

Cote d'IvoireChad

GhanaZambia

Gambia TheRegional Average

TanzaniaEthiopiaMalawi

MozambiqueGlobal Average

Source: Deloitte/GSMA, Global Mobile Tax Review

Tax as a proportion of handset costs

© 2012 Deloitte LLP Private and confidential

20 African countries still impose custom duties on handsets

7

47%30%30%30%30%30%

27%25%

21%20%20%

12%10%10%10%10%

9%8%

5%2%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

NigerCameroon

Congo BGabonGuinea

RwandaDem Rep. Congo

MadagascarCote d'IvoireGambia The

GhanaEthiopia

ChadMalawi

TanzaniaZambiaLesotho

MozambiqueNigeriaKenya

Source: Deloitte/GSMA, Global Mobile Tax Review

Custom duties

© 2012 Deloitte LLP Private and confidential

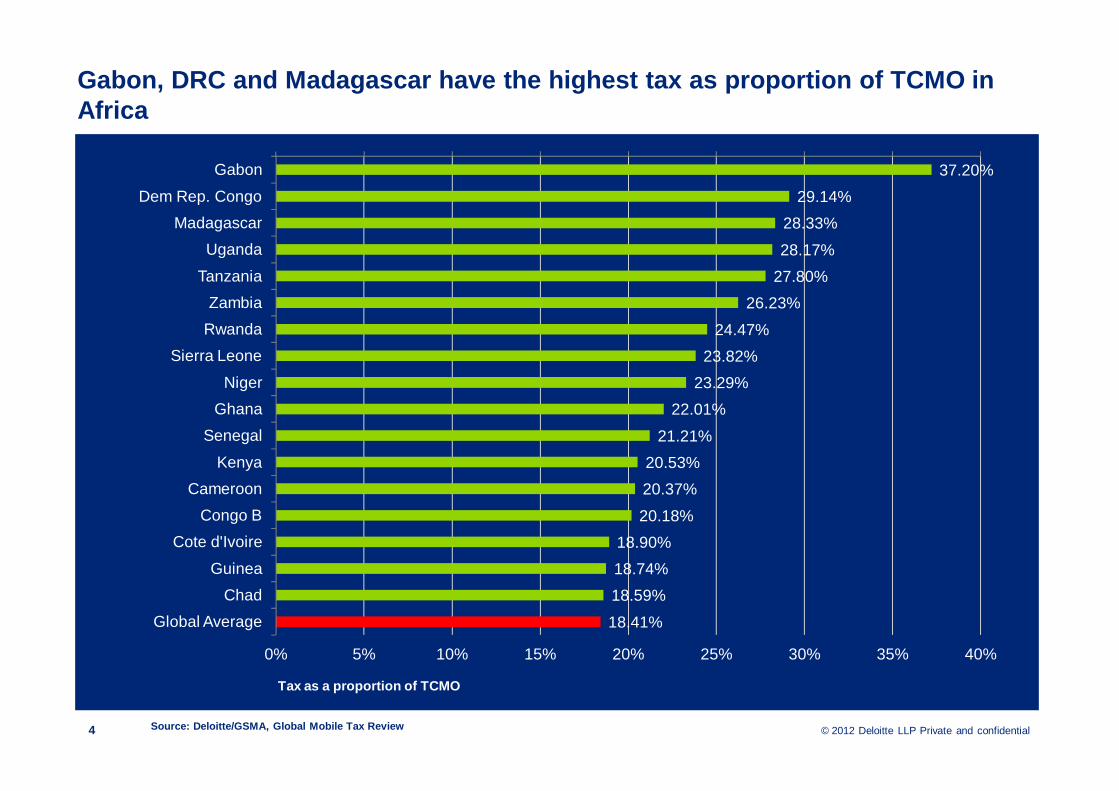

18%17%

31%

19% 19%

29%

0%

5%

10%

15%

20%

25%

30%

Tax/TCMO Tax/TCMU Tax/Handsets

2007

2011

As a result, taxation as a proportion of mobile cos ts has increased in the last four years in Africa...

8

18%17%

31%

19% 19%

29%

0%

5%

10%

15%

20%

25%

30%

Tax/TCMO Tax/TCMU Tax/Handsets

2007

2011

18%17%

31%

19% 19%

29%

0%

5%

10%

15%

20%

25%

30%

Tax/TCMO Tax/TCMU Tax/Handsets

2007

2011

Source: Deloitte/GSMA, Global Mobile Tax Review

© 2012 Deloitte LLP Private and confidential

19.32%

17.17%

14.65%

12.78%

19.06%

16.91%

13.94%

12.77%

29%

27%

21%

17%

0% 5% 10% 15% 20% 25% 30%

Africa

Latin America

ME & Maghreb

Asia Pacific

Tax as a proportion of TCMOTax as a proportion of TCMUTax as a proportion of handset price

19.32%

17.17%

14.65%

12.78%

19.06%

16.91%

13.94%

12.77%

29%

27%

21%

17%

0% 5% 10% 15% 20% 25% 30%

Africa

Latin America

ME & Maghreb

Asia Pacific

Tax as a proportion of TCMOTax as a proportion of TCMUTax as a proportion of handset price

19.32%

17.17%

14.65%

12.78%

19.06%

16.91%

13.94%

12.77%

29%

27%

21%

17%

0% 5% 10% 15% 20% 25% 30%

Africa

Latin America

ME & Maghreb

Asia Pacific

Tax as a proportion of TCMOTax as a proportion of TCMUTax as a proportion of handset price

9

60%

100%

95%

75%

Pen.

... and mobile taxation as a proportion of mobile c osts in Africa is higher than in other developing regions

Source: Deloitte/GSMA, Global Mobile Tax Review

© 2012 Deloitte LLP Private and confidential

Mobile taxes and unbalanced taxes on handsets const rain mobile penetration and economic activity

10 Source: Deloitte/GSMA, Global Mobile Tax Review

Reducing the imbalance on handset taxation

Increase in handset circulation and mobile penetration

Positive effect on GDP growth

Positive effect on government taxation receipts

© 2012 Deloitte LLP Private and confidential

A 10% increase in mobile penetration leads to signi ficant increases in growth of GDP per capita

11

3.88

3.81

3.70

3.51

3.29

3.16

2.66

2.49

2.43

2.08

1.92

1.76

1.75

1.66

1.44

1.34

1.25

1.24

1.22

0 0.5 1 1.5 2 2.5 3 3.5 4

Sierra Leone

Zimbabwe

Liberia

Madagascar

Mozambique

Mali

Sudan

Guinea-Bissau

Zambia

Lesotho

Cameroon

Nigeria

Benin

Kenya

Ghana

Swaziland

Congo, Rep.

Cote d'Ivoire

Namibia

Source: Deloitte analysis, forthcoming

%

© 2012 Deloitte LLP Private and confidential

Kenya has successfully reduced mobile specific taxa tion

12

• The Kenyan government recognised that handset price represented a barrier to the development of the sector

• In August 2009, the 16% VAT on mobile phone handsets was removed

2011

Source: Deloitte/GSMA, Global Mobile Tax Review

© 2012 Deloitte LLP Private and confidential

Lowering taxation has significantly increased hands et circulation...

13

0

50,000

100,000

150,000

200,000

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Source: Deloitte/GSMA, Mobile telephony and taxatio n in Kenya

© 2012 Deloitte LLP Private and confidential

... and has contributed to increased mobile penetra tion above African average

14

40%

45%

50%

55%

60%

65%

70%

Q1 2009Q2 2009Q3 2009Q4 2009Q1 2010Q2 2010Q3 2010Q4 2010Q1 2011Q2 2011

Source: Deloitte/GSMA, Mobile telephony and taxatio n in Kenya

© 2012 Deloitte LLP Private and confidential

0.003

0.013

0.023

0.033

0.043

0.053

0.063

0.073

0.083

0.093

0.103

0

1

2

3

4

5

6

7

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011

Min

s,

bn

Tax reductions and healthy competition have also lo wered mobile prices and increased usage

15 Source: Deloitte/GSMA, Mobile telephony and taxatio n in Kenya

© 2012 Deloitte LLP Private and confidential

In Kenya, consumers, businesses and government have benefitted from developments in the mobile sector

16 Source: Deloitte/GSMA, Mobile telephony and taxatio n in Kenya

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2008 2009 2010 2011

KH

S, m

Intangible benefits

Productivity increases

Supply side

© 2012 Deloitte LLP Private and confidential

Reducing taxation contributes to increase service p enetration and benefits economic activity

• In Africa, the contribution of mobile communications is particularly important to countries’ economic and social development, especially as a result of the limited fixed telecommunications infrastructure

• The Kenyan government has recognised the importance of removing taxes on access to mobile services

• The reduction in handset costs has led to substantial increases in handset circulation and mobile penetration

• This has resulted in notable benefits to consumers and to the economy

• Other African countries could consider the benefits that removing handset tax has provided for Kenya, and the positive benefits that increases in mobile penetration have on GDP growth rates

17

© 2012 Deloitte LLP Private and confidential

• http://www.gsma.com/tax-research-and-resources/

18

Any questions?

Davide StrusaniAssistant Director, TMT Economic [email protected]

© 2012 Deloitte LLP Private and confidential

Member of

Deloitte Touche Tohmatsu

19

This document is confidential and prepared solely for your information. Therefore you should not, without our prior written consent, refer to or use our name or this document for any other purpose, disclose them or refer to them in any prospectus or other document, or make them available or communicate them to any other party. No other party is entitled to rely on our document for any purpose whatsoever and thus we accept no liability to any other party who is shown or gains access to this document.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom.

Deloitte LLP is the United Kingdom member firm of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, whose member firms are legally separate and independent entities. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Member of Deloitte Touche Tohmatsu Limited