Embed Size (px)

Citation preview

Retail Payments Global Consulting Group L.L.C.

Mobile PaymentsA Strategic Overview of

Mobile Payments in the USAMerchant Advisory Group 2013 Annual Conference

New Orleans, LAOctober 7th, 2013

Mobile Payments Agenda

PaymentsFramework

ConsumerAttitudes

ConsumerMobile Apps

MobileTechnologies

Mobile at the Point of Sale

Conclusions and Q & A

Payment Is An Exchange of Value

Value

Financial

In Financial Institutions

Deposits Credit Lines

Outside Financial

Institutions

Credit Lines Cash Other

Non Financial

Reward Miles & Points

Mobile Minutes

For most people value is money and money is normally kept in bank accounts

The Value Layer

Financial Institutions hold the biggest portion of value in most economies

Most payments are funded by credit lines and deposits being held at financial institutions

Value Layer

Credit Lines Deposit Accounts Cash Other

The Instrument Layer Financial Institutions

provide customers with payment instruments so they can access their value

These instruments are the credentials that are exchanged to initiate a payment

Value Layer

Credit Lines Deposit Accounts Cash Other

Instrument Layer

Credit Cards Debit Cards RTN/Acct Numbers Checks

The Network Layer

In a multi‐bank environment payment instrument credentials travel across networksand clearing systemsto accomplish the transfer of value

Networks can bephysical or electronic

This framework has been the traditional approach to payments for over 50 years

Value Layer

Credit Lines Deposit Accounts Cash Other

Instrument Layer

Credit Cards Debit Cards RTN/Acct Numbers Checks

Network Layer

VI/MC/AX, etc. EFT Networks ACH Networks Check Clearing Houses

Additional Layers In The Framework

Emergence of a New Delivery Layercontaining Wallets,Aggregators, Gateways, etc.

These players “wrap” themselvesaround traditionalpaymentinstruments

Value Layer

Credit Lines Deposit Accounts Cash Other

Instrument Layer

Credit Cards Debit Cards RTN/Acct Numbers Checks

Network Layer

VI/MC/AX, etc. EFT Networks ACH Networks Check Clearing Houses

Delivery Layer

E-Wallets M-Wallets Aggregators Other

Additional Boxes in The Framework Emergence of new

ways to access value at purchasetime (e.g. OBePs)

Emergence of newinstruments to initiate payment (e.g. phone number) and networks to carry these transactions

New sources of value accessible to consumers

Value Layer

Credit Lines Deposit Accounts Cash Other Stored

ValueTelco Credit

Lines

Instrument LayerCredit Cards Debit Cards RTN/Acct

Numbers Checks User Id and Password

Telephone Number

Network LayerVI/MC/AX,

etc.EFT

NetworksACH

NetworksCheck

Clearing Houses

Pre-paid Vendors

Telco Carriers

Delivery Layer

E-Wallets M-Wallets Aggregators Other Online Banking Screen Scraper

Mobile Technology Evolution 1G in 1980’s

– Primarily voice

– Analog radio signals

– Launched in Japan

– Ameritech first US network

– 1G speeds vary between speeds of 2.9Kbs/s to 5.6Kb/s.

4G in 2009– Mobile ultra‐broadband

access to USB modems, tablets, smartphones, etc

– Two systems WiMax (Korea) and LTE (Scandinavia)

– 4G offer rates up to 1 Gbit/s fixed speeds and 100 – 128 Mb/s to mobile users

Countries with commercial LTE serviceCountries with commercial LTE network deployment on-going or plannedCountries with LTE trial systems (pre-commitment)

Mobile Phone Penetration

By end of 2013 there will be 6.8 Billion mobile subscriptions globally*– Global 96% penetration– Developed world reached saturation point– Developing world accounts for 76% of global subscriptions

2.7 Billion people (almost 40% of theworld population) are online

* International Telecommunications Union/ICT Indicators Database estimate

Mobile Broadband High Growth

More than 2 Billion subscriptions worldwide*

* International Telecommunications Union/ICT Indicators Database estimate

US Smart Phone Penetration

Growth of US smartphones continues…

…even across “challenged” demographic segments– Cost conscious largefamilies and low incomegroups

– Network subsidy helpingadoption

Smart Phones and Tablets Creating Convergence

Nearly half of digital time spent on retail properties now occurs via smartphones and tablets

Tablet ownership growingat an un‐precedent pace

Tablets overtaking smartphonesin m‐commerce 55% to 45%*

Retail Category Time Spent by Platform:Desktop, Smartphone and Tablet Source: comScore Media Metrix Multi-Platform, U.S., March 2013

Desktop, 52%

Smart phone, 34%

Tablet, 14%

Source: ComScore 2013 Mobile Future in Focus* Internet Retailer

The Major OSs

Android iOS Windows Phone 8 Blackberry Other Players

– Symbian/Nokia– Meego/Tizen– Bada/Samsung

Android Developed by Google Open source – meaning it’s able to be modified Apps for Android are written in Java programming language Any hardware manufacturer may utilize the FREE operating system

– Google has activated more than 500 million devices (over 1 million/day) Google’s mobile initiative

– Acquired Motorola Mobility in August 2010– Introduced Nexus 7, a tablet to compete with iPads

Current version – 4.1 Jelly Bean– Announced in June 2012, and released on July 9, 2012.– Previous Versions

• 4.0 ‐ Ice Cream Sandwich• 3.0 ‐ Honeycomb• 2.3 ‐ Gingerbread• 2.2 ‐ Froyo

– What does Froyo stand for? Announced latest release 4.4, KitKat

Google Play ‐ The Android App Store

Over 1 Million applications as of Sept 2013 and over 50 Billion downloads since Android began*

Had a reputation as a “free for all” site hosting many rogue apps ‐‐ including copycat games, spam, and malware

Google enforcingrules has significantlyreduced thenumber of rogue apps

* Source: Google, October 2012

Apple’s iOS

Developed by Apple, Inc. NOT Open source Limited to one hardware manufacturer – Apple Apps for iOS are written in Objective C programming language

Current version – 7.0– Version of iOS does not equate to version of iPhone– Current version of iPhone – 5S

The Apple App Store

One Million applications and over 50 Billion downloads*

Tight control over what applications are loaded onto the store. Many apps are rejected– Limited audience– Repetitive apps– Unrefined/poorly created– Improper use of APIs– Poaching keywords– Little usefulness

* Source: Apple, May 2013

Developed by Microsoft, Inc. NOT Open source Support multiple phone manufacturers although Microsoft

bought Nokia devices and services businesses in Sept 2013 (€3.79 Billion)

Version of Windows 8 OS tailored to fit smaller screens Windows Phone 8 will support native code —

– Apps programmed for Windows 8 will work on Windows Phone 8. Native code support also means it’ll be easier to port complex iOS and Android apps to Windows Phones

Windows Phone 8 under the “One Microsoft” strategy Windows Phone 8.1 Release expected in early 2014

Windows Phone

Windows Phone Store

Over 100k Windows Phone 8 apps available in Windows Store driving more than 200 Million monthly downloads (both Windows Phone and Windows 8)

MS exercising same controls as Apple for apps introduced to Windows Store

Developers can write apps in languages such as JavaScript, C#, Visual Basic, or C++,

Microsoft offers developers up to 80 percent rev share when reaching $25K in revenue

Blackberry OS Developed by Research in Motion, Inc. (RIM) Company name changed to BlackBerry Limited to one hardware manufacturer – RIM Blackberry Handset Generally, apps are written in Java language

– Over 60K apps available, over 2 Billion downloads Current version – 10

– Launched in January, 2013– Supports Multi‐tasking and a message hub to

integrate e‐mail, Twitter, Linkedin, and Facebook messages Introduced two new devices supporting OS

– Z10 a touch screen handset– Q10 with a QWERTY keyboard– Shipped over more than 1MM units thus far

Company in $4.7B deal with Fairfax Financial

Other Mobile OS HP’s webOS

– Linux kernel based OD initially developed by Palm and later acquired by HP– Launched in January 2009. Various versions of webOS have been featured on several

devices, including Pre, Pixi, and Veer phones and the HP TouchPad tablet. MeeGo

– Linux‐based fee mobile OS project hosted by the Linux Foundation– OS aimed at netbooks, tables, smart phones, SmartTV, ConnectedTV, IPTV‐boxes and other

embedded systems Symbian

– Closed source C++ embedded OS developed initially by Nokia and currently maintained by Accenture

– Nokia announced its intention to migrate to Windows Phone OS Bada

– Meaning "ocean" or "sea" in Korean is a mobile OS for devices such as smartphones and tablets. It is developed by Samsung Electronics

– Samsung uses its own Bada OS, in parallel with Android OS and Windows Phone. All Bada‐powered devices are branded under the Wave name; whereas Android‐powered devices are branded under the name Galaxy

App Users Are Active Users App downloaders with Apple iOS and Android OS smartphones have more

applications on their mobile phones than those with other kinds of smartphones, with an average of 48 apps on iPhones and 35 apps on Android phones. (By comparison, app downloaders with BlackBerry smartphones only had an average of 15 apps on their phones.)

They also use their apps more often: 68% of app downloaders with iPhones and 60% of those with Android phones reported using their mobile apps multiple times a day compared to 45 % of those with BlackBerry phones.

According to a new research report from the analyst firm Berg Insight, the number of mobile application downloads worldwide doubled during 2012 and reached 60.1 billion, up from 29.5 billion in 2011. The growth will continue and annual downloads will reach 108 billion by 2017.

Functional Architecture

It is not your father’s phone anymore!

Important Payment Technology Bits

SMS / Premium SMS Mobile Browsers HTML 5 Communications

– WiFi– Bluetooth and Bluetooth Low Energy (BLE)– Bar codes and RFID– Attached card readers– NFC– Other

• Modulated Audio • Biometrics

SMS/Premium SMS Short Message Service (SMS) is a text communication service using

standardized communications protocols that allow the exchange of short text messages between mobile phone devices.

The key idea for SMS was to use a telephony‐optimized system, and to transport messages on the signaling paths needed to control the telephony traffic during time periods when no signaling traffic existed. In this way, unused resources in the system could be used to transport messages at minimal cost. However, it was necessary to limit the length of the messages to 128 bytes (later improved to 140 bytes, or 160 seven‐bit characters) so that the messages could fit into the existing signaling formats.

SMS text messaging is the most widely used data application in the world, with 3.6 billion active users, or 78% of all mobile phone subscribers

Premium SMS

Premium‐rated short messages provide premium rate services to subscribers of a telephone network

Deliver digital content such as news alerts, financial information, logos and ring tones

Used to make smaller payments online, for example for file sharing services or in mobile application stores

Outside the online world, one can make a donation, buy a bus ticket, beverages from ATM, pay parking ticket, order a store catalog or some goods (e.g. discount movie DVDs) and many more.

Text Messaging is Relevant

American subscribers averaged 664 messages per month during the second quarter 2012, more than consumers in any other global market

The total number of SMS sent globally tripled between 2007 and 2010, from an estimated 1.8 trillion to a staggering 6.1 trillion. In other words, close to 200,000 text messages are sent every second.

The Philippines and the United States combined accounted for 35% of all SMS sent in 2009.

Mobile Browsers

Web browser designed for use on mobile device– Micro browser or wireless internet browser (WIB)– Access web through cellular network or through wireless LAN (e.g. WiFi)– Web sites designed for WIB access called wireless portals

Sample browsers and manufacturers– Android browser/Google– BlackBerry browser/RIM– Firefox for mobile/Mozilla– IE Mobile/Microsoft– Kindle Fire Silk browser/Amazon– PlayStation Portable web browser/Sony– Series 60 web browser/Nokia– Safari/Apple

HTML 5 HTML is a markup language for structuring and presenting Web content HTML 5 is the fifth revision since HTML was introduced in 1990 A World Wide Web Consortium (W3C) Candidate Recommendation Not software but a version of the language used to build web sites Adds <video>, <audio>, <canvas> elements and other features

intended to include multimedia and graphical content without need of plug‐ins (e.g. Flash)

Additional features for mobile phones such as Geolocation API, offline web application, WebStorage, Metro Style apps (WP8)

Native apps (i.e. built to utilize the native OS of the handset) may offer more robust functionality, but at a longer and more expensive development process

Currently in development– W3C targets 2014 for HTML5 Specification Recommendation– Mozilla’s HTML5‐based Firefox OS released in July 2013

Wi‐Fi

Technology to exchange data using radio waves (wirelessly) over a computer network

Based on IEEE 802.11 standard Positive Aspects

– Support high speed internet connections– Well understood and commonly used– Low cost

Drawbacks– Requires login sequence– Security concerns

Bluetooth Proprietary open wireless technology standard for fixed and mobile devices to

exchange data over short distances (using short‐wavelength radio transmissions in the 2400–2480 MHz band)

Standardized under IEEE 802.15 Created by Ericsson in 1994. It can connect several devices, overcoming problems of

synchronization. Intended as a replacement for RS‐232 cables Positive Aspects

– Well understood and installed in many phones– Low cost– Some BT card readers are now available (e.g. Mpowa)

Drawbacks– Requires pairing/bonding sequence– Much longer range than needed (150 feet)– Security concerns

Bluetooth Low Energy (BLE)– Compatible only with Bluetooth 4.0 dual mode– To be marketed as Bluetooth Smart

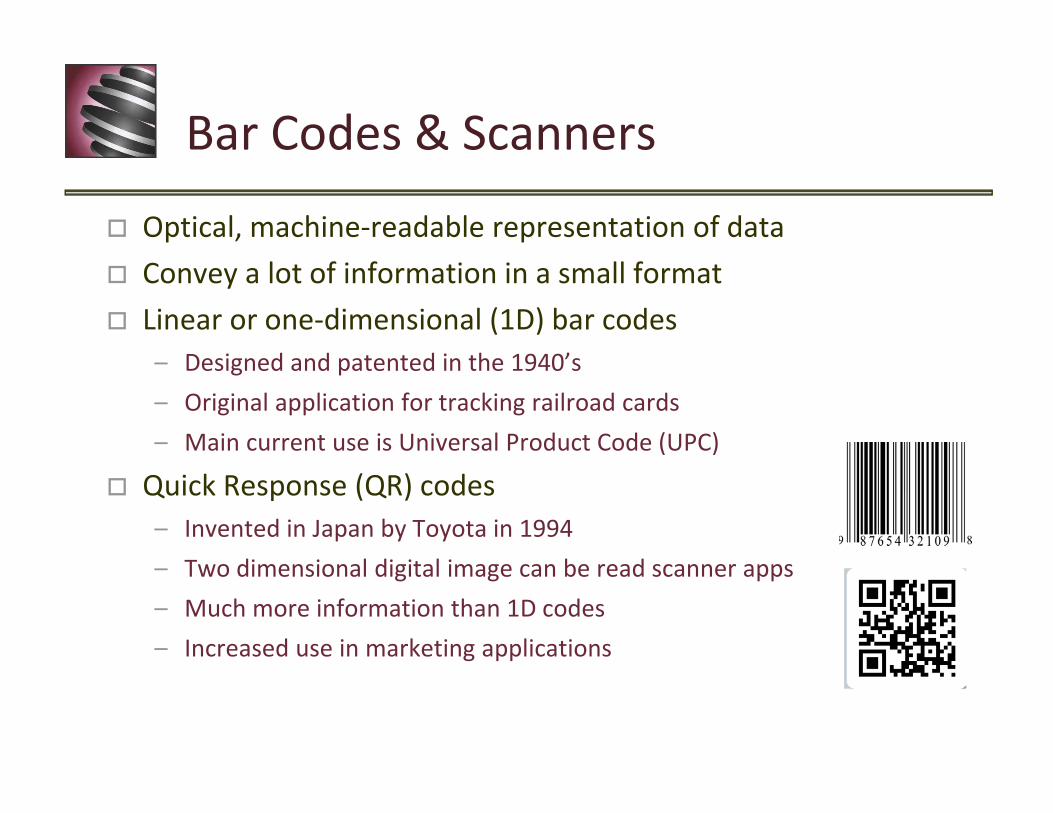

Bar Codes & Scanners

Optical, machine‐readable representation of data Convey a lot of information in a small format Linear or one‐dimensional (1D) bar codes

– Designed and patented in the 1940’s– Original application for tracking railroad cards– Main current use is Universal Product Code (UPC)

Quick Response (QR) codes– Invented in Japan by Toyota in 1994– Two dimensional digital image can be read scanner apps– Much more information than 1D codes– Increased use in marketing applications

Radio Frequency Identification (RFID)

Technology that uses communication via radio waves to exchange data between a reader and an electronic tag attached to an object, for the purpose of identification and tracking.

Information is in a self‐contained chip (or tags) Tags can be powered or activated by the reader’s

electromagnetic field Tag does not need to be within line of sight of

reader Use to track things (i.e. automobiles

during production line, pharmaceutical products in warehouses, implanted in livestock, tolls on highways and bridges, etc.)

Attached Card Readers

Device attached to a smartphone or tablet turning them into a card accepting terminal

Readers must encrypt data and be PCI compliant Industry “launched” by Square Intuit, PayPal, iZettle, Pay Anywhere, Sum up, and few more, many offering readers from Roam.

Readers evolving in Europe to support chip and PIN as well as to use remote connectivity (BT with mPowa)

Near Field Communications (NFC)

NFC is a set of standards for smart phones and similar devices to establish radio communication with each over very short ranges

NFC is a “flavor” of RFID using the 13.56MHz band at rates of 106 k/bits to 424 k/bits per second.

NFC can be used to communicate between two powered devices (peer‐to‐peer) and one powered device and an unpowered “tag”

NFC is slower than Bluetooth but consumes much less power and does not require pairing

NFC in Payments

NFC has existed in the payments space for several years– White label payment systems (e.g. Vivotech)– Closed loop transit systems (e.g. UK’s Oyster)– Tag‐based payments (e.g. Bling Nation)– MasterCard’s paypass– Visa’s payWave

NFC began to make inroads onmobile phones in 2007‐2008– Attach a tag to a phone– Acquire and insert a SIM on mobile– Phones with built‐in NFC chip

NFC in Mobile Payments

Secure Element– Stores information in a secure manner– It is controlled by the telephone carrier!

Different implementations– Embedded in mobile phone– SIM based– Removable SE (SD Card)

Visa/MC approach– Store the card number in the SecureElement portion of the NFC Chip

Many standard setting bodies– ISO/IEC (18092), ECMA (340), NFC Forum, GSMA, EMVCO

Payment Credentials in NFC Phone

IssuerAcquirer

5 5 8 8 3 2 0 1 2 3 4 5 6 7 8 95 5 8 8 3 2 0 1 2 3 4 5 6 7 8 9

NFC leverages the existinginfrastructure but does notcreate anything more thana new way to enter traditional payment instrument data into the networks

Payment Credentials in NFC Phone

Pros– Leverages existing infrastructure– Consistent with other card based payment– Secure element protects card number

Cons– Required investment to obtain NFC readers– Another “silo” – Requires smart phones with NFC chips– Limited to “enabled” funding sources– Expensive – issuer must pay a

“rent” fee ($3‐$5) to carrier percard number stored

NFC is the approach preferred by established players

Payment Credentials In The Cloud

Merchants’Banks

Consumers’Banks

Communications

Exchange

MerchantServer

Consumer PaymentServer

Card Schemes

Clearing House

MerchantPayment Information

ConsumerPayment Information

IndependentSchemes

A F 8 8 C M 0 1 9 H W G 7 3 A G 8 9

Payment Credentials In The Cloud Pros

– Some implementations can be done with feature phones and other non—smart phone devices

– May not need expensive investment at POS to support payments– Can be used outside the POS (e.g. QR codes in a poster)– Can be done as “push” or “pull” payments– Can access more than one funding source– Is not exclusive of NFC

Cons– Still requires POS investment– Schemes must provide equal

or better security than NFC– Change in consumer behavior– Banks must be active participants

Many new creative ideas and players outside of NFC

Mobile Payments Agenda

PaymentsFramework

ConsumerAttitudes

ConsumerMobile Apps

MobileTechnologies

Mobile at the Point of Sale

Conclusions and Q & A

Mobile Payment Projections E‐Marketer (July 2013)

– US Mobile payments to top $1B in 2013; estimates to grow to $58Billion in 2017 Javelin (April 2013)

– Mobile adoption and industry push for mobile payments will cause the amount of mobile payments at the point of sale will increase from $398 million last year to $5.4 billion in 2018.

Forrester (January 2013)– Forrester forecasts that US mobile payments will reach $90B in 2017, a 48% compound annual growth

rate (CAGR) from the $12.8B spent in 2012. Gartner (May 2012)

– m‐payments will total US $171.5 billion in 2012 (up 61.9 percent from $105.9 billion in 2011).– In 2016 there will be 448 million m‐payment users, in a market worth $617 billion. – Asia/Pacific will have the most m‐payment users, but Africa will account for the highest revenues.

Yankee Group (June 2011)– Global mobile transactions predicted to be US$241 billion in 2011 growing to >$1 Trillion by 2015– EMEA is the mobile money hot spot accounting for 41% of mobile transactions value in 2011, compared

to 35% in North America, 22% in Asia‐Pacific and just 1% in Latin America. Juniper Research (July 2011)

– Total value of mobile payments for digital and physical goods, money transfers and NFC transactions will reach $670bn by 2015, up from $240bn this year..

– 1.8 billion consumers globally will buy digital goods via their mobile in 2011, this will rise to 2.5 billion in 2015 account for nearly 40% of the market

US Consumers Attitudes

Are US consumers demanding mobile payments?

51% of consumers were aware of mobile payments, 23% said they were interested in the technology, but only 1% said they were using it 1

17%

16%

42%

31%

0% 20% 40% 60% 80%100%

Liklely to use a mobile phone tobuy online

Likely to use a mobile phone tobuy in‐store

Likely to use a mobile phone tocheck store location

Would receive promotionalmessages on mobile

US Consumer AttitudesGartner Survey

1 Source: Mercator Advisory Group (February 2012)

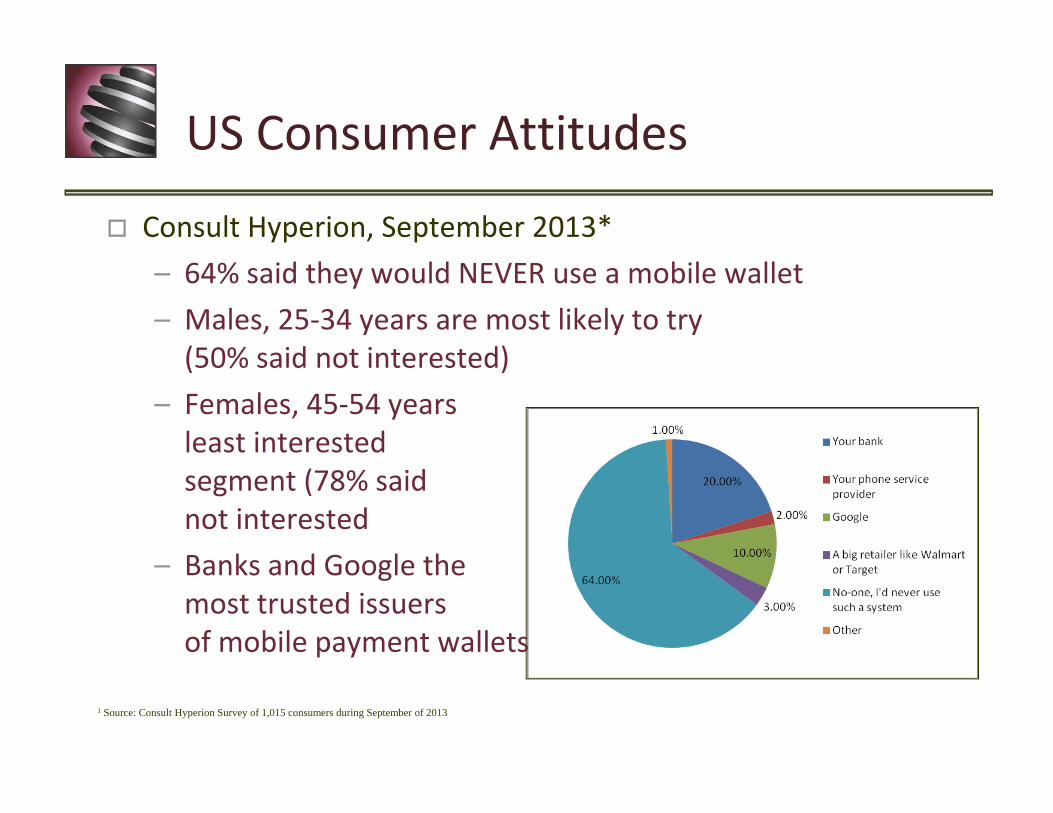

US Consumer Attitudes

Consult Hyperion, September 2013*– 64% said they would NEVER use a mobile wallet– Males, 25‐34 years are most likely to try(50% said not interested)

– Females, 45‐54 years least interestedsegment (78% said not interested

– Banks and Google themost trusted issuers of mobile payment wallets

1 Source: Consult Hyperion Survey of 1,015 consumers during September of 2013

Computer remains payment king– Across all commerce segments phone or tablets account for less

than 10% of total volume Consumers need incentives to use mobile payments*

– 41% highly aware of mobiles as payment instrument, yet only 16% use them this way

– 37% find cash more convenient– Half of non‐users worry about security and one third worry about privacy– 60% of mobile payments users

would probably do so more often if they received instant coupons

– Additionally, over half would pay by phone more frequently if they could use their phones to track receipts, manage their personal finances and show proof of a driver’s license or valid insurance.

M‐Commerce Has A Way To Go

* Source: Accenture Survey of 4,000 smartphone users in US and Canada, 2013

Source: Adyen

But Then…,There Is Starbucks

A Customer Hit?– First mobile app in September 2009– Over 10 Million “active” users – 4.5 Million mobile payments/week– Account for over 10% of US “tender” at Starbucks

It is not all about payments– Loyalty point tracker– Store locations and hours of operation– Product and nutritional information– Drink builder– Gift cards marketplace – “Value added” iTunes songs & apps

Puzzle Components

Merchant Acceptance– Use mobile phones as a POS– Leverage mobile and tablet technologies to revolutionize Point of Sale experience

– Use mobile to gather consumer data

Consumer Wallets– NFC or cloud based– Generic or merchant specific– Single or multiple purpose – Added‐value features

Mobile devices need to “talk” to other devices to initiate transaction– A POS terminal– Another mobile device

Multiple technologies– NFC– Bluetooth LE– Bar codes and QR Codes– Wi‐Fi– Bump– RFID– Infrared– Sound– Biometric

POS environment will undergo massive changes– From specialized to commodity devices– From specialized functions to all‐in‐one

Impact On Payments Acceptance

Square Founded by Jack Dorsey of Twitter Fame with notable investor roster

– Visa, Kleiner Perkins Caufield and Byers, Sir Richard Branson (Virgin), Starbucks

Fee structure– 2.75% per swipe, $0 per month– $275 per month, 0% per swipe

Primary focus on very small merchants– Recent partnership with Intuit

– Supporting online (CNP) purchases through“market embedding”

Growth by pursuing larger merchants – Introduction of Square Stand and “Business in a Box”

• $299 (iPad not included)

• Works with iPad 2 and 3

• Connects to cash drawer and receipt printer

• Sold at Apple stores

PayPal Here Extending online presence to physical space

– Leveraging existing relationship with thousands of merchants Fee structure

– 2.70% + 30¢ per swipe, $0 per month– Waving fees for selected merchants until end of 2013

Evolving its presence across many channels– Partnership with Discover– Partnership with Mercury Payments, Gravity Payments, others– Partnership with Alliance Data and Moneygram– Recently announced acquisition of Braintree

Expanding functionality beyondpayments– Partnerships with Leaf, Leapset,

NCR Silver, ShopKeep POS and Vend

– Partnership with Shopventory– Offering Small Business Loans

(small, by invitation, programs)

Intuit GoPayment

Launched in 2009 and currently supports– iPhones, iPad, Android devicers– Visa, MasterCard, American Express, Discover cards– One of several payment acceptance channels

• Mobile, Online, Web Store, QuickBooks

Pricing– 2.75% + 0¢ swiped fee, $0/Month– 1.75% + 0¢ swiped fee, $12.95/month– Free card reader and app

Developments– Integration with Quickbooks POS– Allowing card scanning using tablets– Attempt to deploy internationally– Recent re‐organization– Partnership with Square

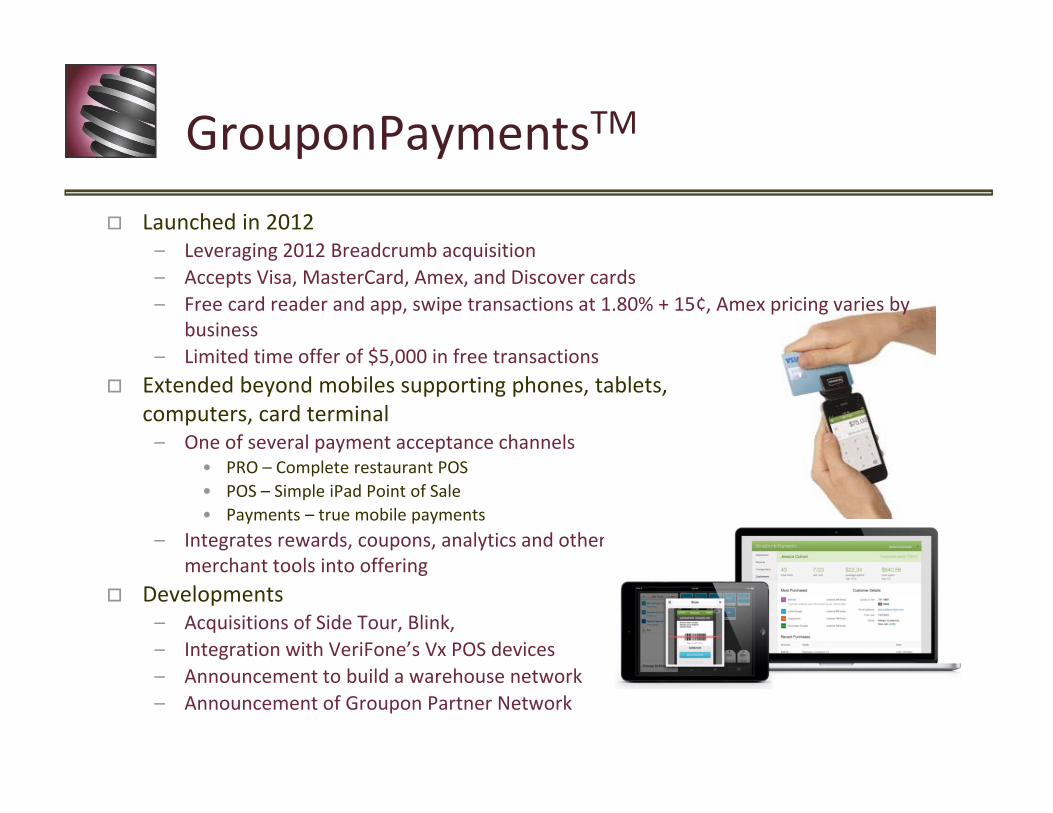

GrouponPaymentsTM

Launched in 2012– Leveraging 2012 Breadcrumb acquisition– Accepts Visa, MasterCard, Amex, and Discover cards– Free card reader and app, swipe transactions at 1.80% + 15¢, Amex pricing varies by

business– Limited time offer of $5,000 in free transactions

Extended beyond mobiles supporting phones, tablets, computers, card terminal – One of several payment acceptance channels

• PRO – Complete restaurant POS• POS – Simple iPad Point of Sale• Payments – true mobile payments

– Integrates rewards, coupons, analytics and other merchant tools into offering

Developments– Acquisitions of Side Tour, Blink,– Integration with VeriFone’s Vx POS devices– Announcement to build a warehouse network– Announcement of Groupon Partner Network

Other Entrants LevelUp

– Combines marketing campaigns with payment processing– Both a wallet and a POS solution accepting Visa, MasterCard, Amex, and Discover

cards– Merchant fee for payment processing is 2% flat fee or 0% but get 25% of value of

every campaign redeemed (hardware is additional cost)– White label offering

Leaf NCR Silver VeriFone Sail Large Acquirers

– BofA, – Chase, – First Data

Non US Based Entrants iZettle

– Swedish based company positioned as “Europe’s rival to Square”– Present in SE, NO, DK, FI,UK, DE, ES, MX, BR– Accepts Visa, MasterCard, Maestro, Vpay,

Visa Electron, Amex, & JCB– Supports iOS and Android with Chip and signature and

Chip and PIN readers– Pricing changes by country, UK oricing ranges from 2.75% to 1.50% (no flat fees) depending

on sales volume (automatically adjusted)• Chip and signature reader is €25 in EU • Chip and PIN is £82 in UK €99 in EU

– Relationship with Banco Santander helping in Spain and Latin America SumUp

– Uk based company present in AT,BE,DE,ES,FR, EI, IT, NL, PT, UK– Supporting iOS and Android devices with Chip and PIN reader– Just reduced fee to 1.95% per transaction ‐ card reader is offered free– AmEx and Groupon invest in SumUp– Recent partnership with BBVA in preparation for entry in Latin America– Partnership with Revel Systems, a maker of iPad POS software,

More Non‐US Based Entrants Mpowa

– UK based company, claiming presence in over 40 countries in Europe and LatAmand just opened an office in US

– Accept Visa, MasterCard, V Pay, and Maestro– Support iOS, Android, BlackBerry, Windows Phone– Fee is 2.95% per transaction or allows merchants to continue using own merchant account

at 0.25% ‐ Bluetooth Chip and PIN readers is £49.99– Allowing consumers to purchase by just pointing mobile camera to desired item– Whitelabel deal with Telecom Purtugal

Payleven– UK based company present in UK, BR, BE. DE, IT, NL, AT, PL– Accept Visa, MasterCard, V Pay, and Maestro– Support iOS and Android devices and offers product catalog, sales analytics, etc.– Fee is 2.75% per transaction ‐ Chip and PIN reader is £89 in UK and €49 in EU– Partnert with MICROS for Chip & PIN‐Supported hospitality POS System– Just announced deal with Italy’s Posta Italiana and Banco Posta

Jusp– Italian based company just closing a $6Million financing round– Support iOS and Android connecting to device’s audio jack– Fee is 2.50% per transaction – Chip and PIN reader is €39

More Intelligence at POS

Introduction of tablets at POS have given merchants more computing power to do much more than just accept payments

With tablets integrated at POS, merchants can– Better track inventory– Enhance their merchandising– Accept coupons & vouchers

But it also has introduced challenges– Acceptance of multiple tenders in a single integrated checkout experience

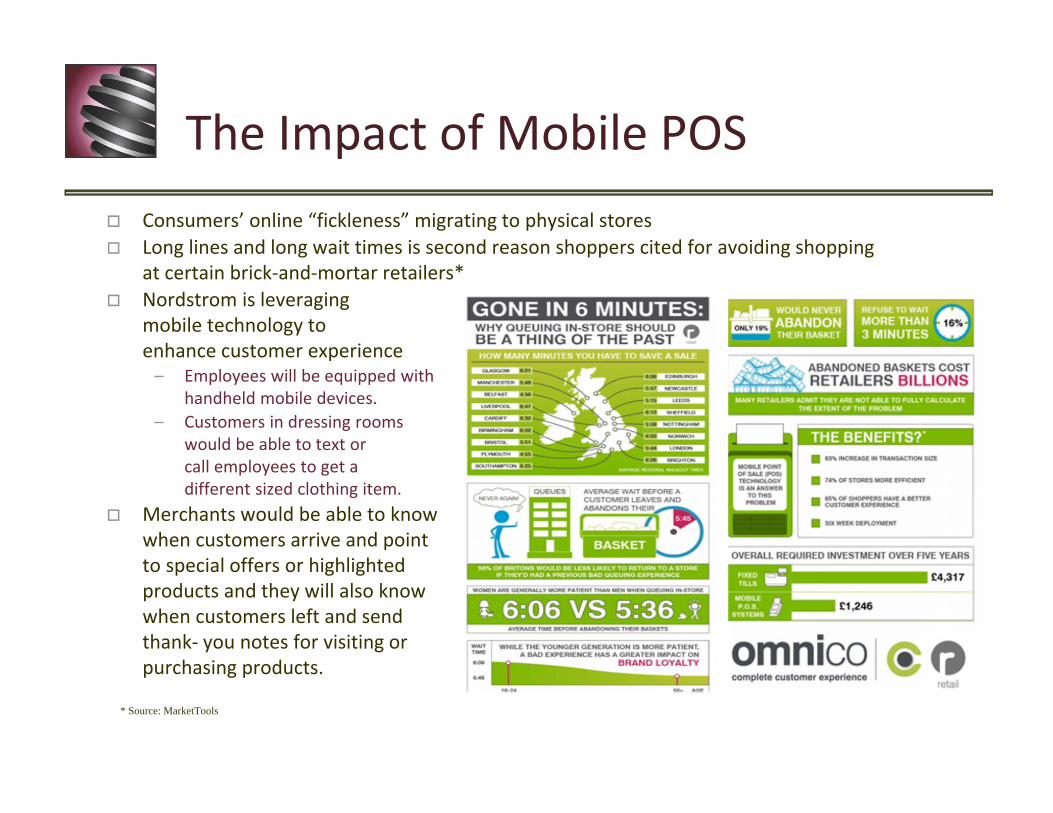

The Impact of Mobile POS Consumers’ online “fickleness” migrating to physical stores Long lines and long wait times is second reason shoppers cited for avoiding shopping

at certain brick‐and‐mortar retailers* Nordstrom is leveraging

mobile technology to enhance customer experience– Employees will be equipped with

handheld mobile devices. – Customers in dressing rooms

would be able to text or call employees to get a different sized clothing item.

Merchants would be able to know when customers arrive and point to special offers or highlighted products and they will also know when customers left and send thank‐ you notes for visiting or purchasing products.

* Source: MarketTools

Checkout Will Evolve Dramatically

Tesco/Homeplus “Shopping Wall” in South Korea

Mobile Payments Agenda

PaymentsFramework

ConsumerAttitudes

ConsumerMobile Apps

MobileTechnologies

Mobile at the Point of Sale

Conclusions and Q & A

Mobile Payments? There are NO MOBILE PAYMENTS, just MOBILE WALLETS

– Most mobile solutions wrap themselves around a traditional payment instruments (e.g. bank cards)

– Exceptions are direct carrier billing solutions or solutions where the value is exchanged directly by the phone (e.g. mobile minutes)

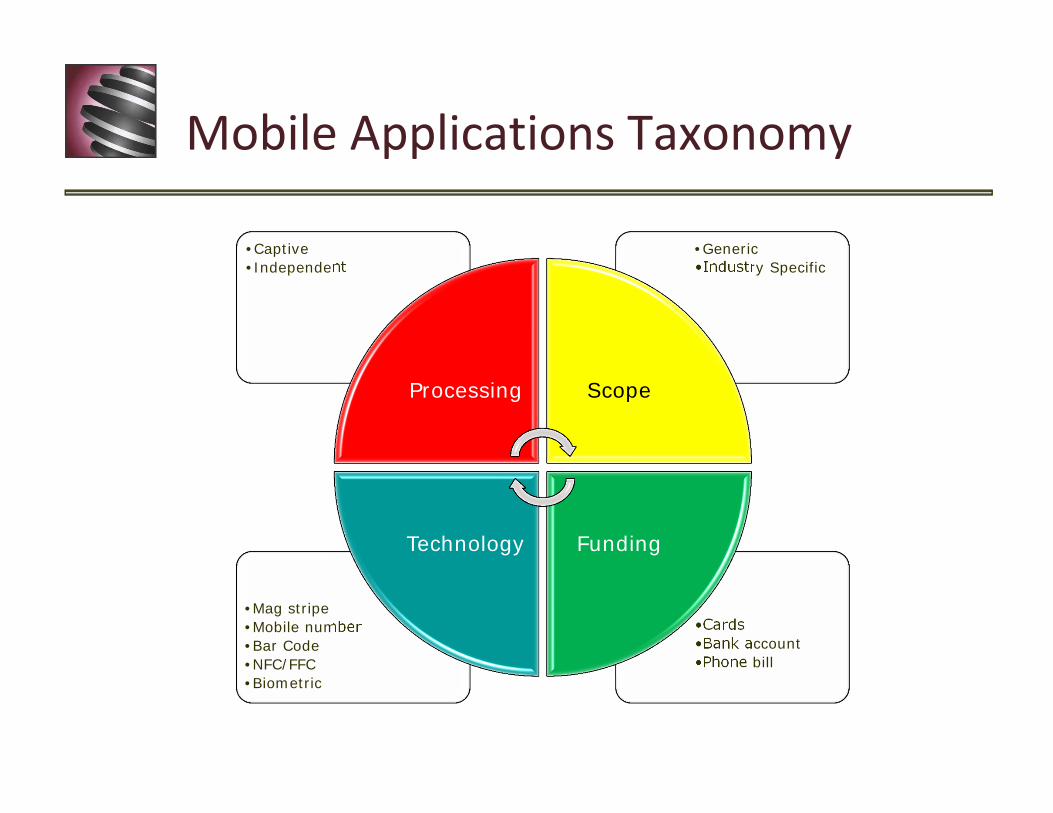

Taxonomy of mobile payments solutions is based on– Scope (e.g. open vs. closed loop; generic

vs. industry‐specific)– Technological implementation

(e.g. NFC vs. non‐NFC)– Funding sources

(e.g. cards, carrier billing, anything else)– Processing (e.g. own acquirer, through

mobile app provider)

Mobile Applications Taxonomy

•Cards•Bank account•Phone bill

•Mag stripe•Mobile number•Bar Code•NFC/FFC•Biometric

•Generic•Industry Specific

•Captive•Independent

Processing Scope

FundingTechnology

Google Wallet 1.0 Background

– Released in late 2011– Required many things to line up

• A Citibank issued MasterCard credit card • A specific phone model (Nexus S 4G) connected to the Sprint Network• A merchant equipped with NFC terminal

How it works– Card number stored in Secure Element in phone– Consumers shop at any MasterCard accepting merchant equipped with a NFC

capable POS terminal where they tap the phone– Transaction travels through regular credit card networks and it is authorized

in an identical manner to credit cards – Merchants gets paid by its regular acquirer along with other MasterCard

transactions (no special interchange for these transactions has been identified) Results

– Could not get other banks to load their cards to Wallet– Limited consumer acceptance– Some security flaws identified

• Cards• Bank account• Phone bill

• Mag stripe• Mobile

number• Bar Code• NFC/FFC• Biometric

• Generic• Industry

Specific

• Captive• Independent

Processing Scope

FundingTechnology

Google Wallet 2.0 Background

– Released in Summer 2012 to address weaknesses of 1.0– Allows consumers to load any credit card they wish as funding source– Remain dependent on Sprint (only Virgin Mobile added) but more phones supported– “Pre‐loaded” with a pre‐paid MasterCard from The Bancorp Bank as the tender mechanism– Incorporates Google Offers

How it works– Consumer’s card numbers stored in the Cloud but pre‐paid card stored in Secure Element– Consumers shop at any MasterCard accepting merchant equipped with a NFC

capable POS terminal where they tap the phone– Transaction using pre‐paid card travels through regular credit card networks, eventually

requesting an authorization from Google– Google retrieves the consumers’ funding instrument and initiates an

authorization of that credit card – Upon approval, it authorizes the purchase at merchant– Merchants gets paid by its regular acquirer along with other MasterCard

transactions (no special interchange for these transactions has been identified)

• Cards• Bank account• Phone bill

• Mag stripe• Mobile

number• Bar Code• NFC/FFC• Biometric

• Generic• Industry

Specific

• Captive• Independent

Processing Scope

FundingTechnology

Google Wallet 2.5? Recent Developments

– Major reorganization, May 2013– Google Checkout shutting down and functions to be assumed by Google Wallet– Google Wallet definition expanded to computer, not just mobile

Announcements– Store payment credentials in Chrome and

automatically fill in all necessary fields at checkout– Google Wallet API for mobile checkout independent

of browser or m‐OS– Instant Buy Android API (2‐click checkout)– Google Wallet on e‐mail allowing P2P payments

Recent Developments – Released NFC‐free version for most Android and iPhones– Focus on P2P payments– Closers integration with merchants’ coupons and offers

• Cards• Bank account• Phone bill

• Mag stripe• Mobile

number• Bar Code• NFC/FFC• Biometric

• Generic• Industry

Specific

• Captive• Independent

Processing Scope

FundingTechnology

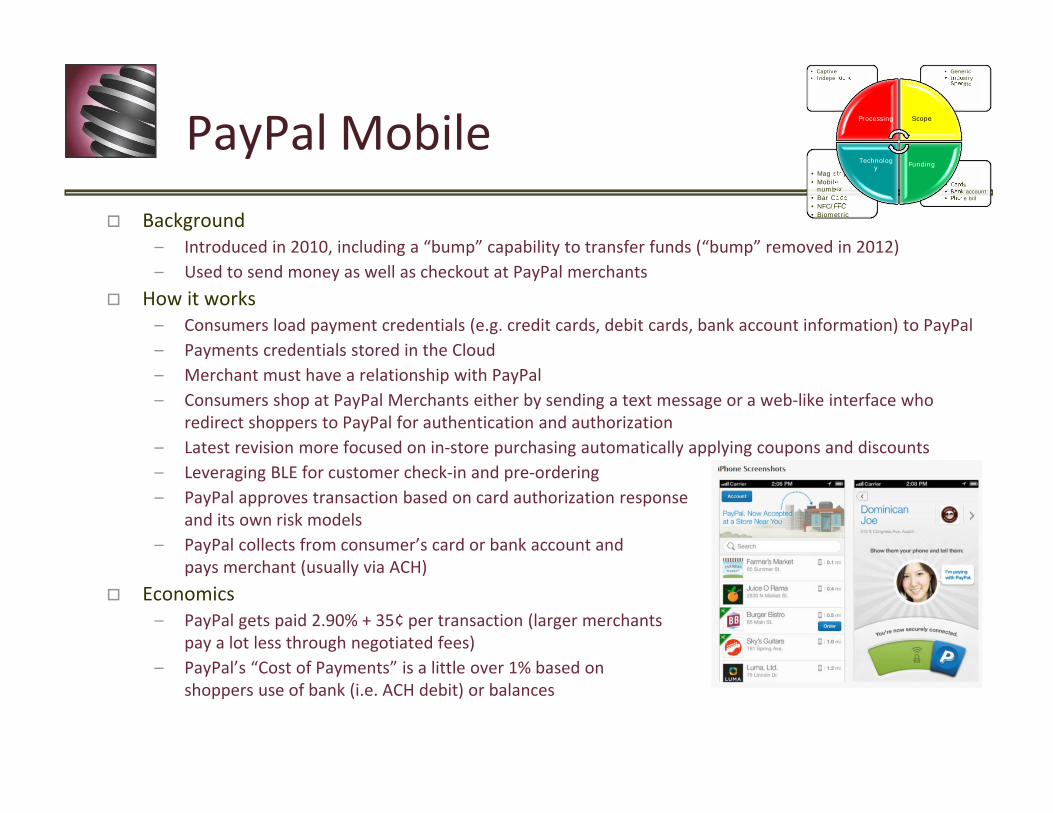

PayPal Mobile Background

– Introduced in 2010, including a “bump” capability to transfer funds (“bump” removed in 2012)– Used to send money as well as checkout at PayPal merchants

How it works– Consumers load payment credentials (e.g. credit cards, debit cards, bank account information) to PayPal– Payments credentials stored in the Cloud– Merchant must have a relationship with PayPal– Consumers shop at PayPal Merchants either by sending a text message or a web‐like interface who

redirect shoppers to PayPal for authentication and authorization– Latest revision more focused on in‐store purchasing automatically applying coupons and discounts– Leveraging BLE for customer check‐in and pre‐ordering– PayPal approves transaction based on card authorization response

and its own risk models– PayPal collects from consumer’s card or bank account and

pays merchant (usually via ACH) Economics

– PayPal gets paid 2.90% + 35¢ per transaction (larger merchants pay a lot less through negotiated fees)

– PayPal’s “Cost of Payments” is a little over 1% based on shoppers use of bank (i.e. ACH debit) or balances

• Cards• Bank account• Phone bill

• Mag stripe• Mobile

number• Bar Code• NFC/FFC• Biometric

• Generic• Industry

Specific

• Captive• Independent

Processing Scope

FundingTechnology

PayPal In Stores Consumers register PayPal account to pay at stores

– Consumers select a PIN for their mobile phones– Consumers select their funding methods and their priority– Consumers get a card in the mail (a Discover card)

Consumer shop at stores– Merchants must have a relationship with PayPal– Enters mobile phone number on POS device

(or swipe card through a Discover issued card)– Enters PIN– Transaction is approved by PayPal based on

funding instrument and PayPal’s risk models Economics

– Because of its lower funding costs it is possible for PayPal to offer lower payment processing costs than credit cards

– Merchants also have the potential for gettingmore marketing data

– PayPal Offers Merchants Free Processing to Push Mobile Point of Sale

76

• Cards• Bank account• Phone bill

• Mag stripe• Mobile

number• Bar Code• NFC/FFC• Biometric

• Generic• Industry

Specific

• Captive• Independent

Processing Scope

FundingTechnology

Background– Isis is a joint venture of AT&T Mobility, T‐Mobile USA, and Verizon Wireless– Allows consumers to pay for goods and services using one’s mobile phone and NFC

How It Works– Consumers load payment credentials to Isis

• Support American Express, Capital One, Barclays, and JP Morgan Chase Bank CREDIT cards only• HTC, LG, Motorola Mobility, RIM, Samsung Mobile and Sony Ericsson to introduce NFC‐enabled mobile devices

implementing Isis’ NFC standards– Payment credentials stored in the phone’s SE– Merchant must have a relationship with Isis but also has a relationship with its acquirer– Wallet supports offers, deals , loyalty cards and promotions– Consumers shop by tapping phone at any Isis enabled accepting merchant equipped with a NFC POS– Merchants gets paid by its regular acquirer along with other Visa and MasterCard transactions (no

special interchange for these transactions has been identified) Business Model

– Isis gets paid an undisclosed share of the interchange income by issuer

Recent Developments– Pilots in Austin, TX and Salt Lake City, UT concluded and

planning for a national rollout– Capital One and Barclays bail out– Developing an iPhone version

Isis – A Mobile Carrier JV• Cards• Bank account• Phone bill

• Mag stripe• Mobile

number• Bar Code• NFC/FFC• Biometric

• Generic• Industry

Specific

• Captive• Independent

Processing Scope

FundingTechnology

Apple – Passbook Background

– Industry pundits projecting Apple’s entry into payments space (it hasn’t so far)– Many were betting that iPhone 5 would have a NFC chip (it didn’t)– Some claim that Passbook is the first step towards the entry into payments (it may or not)

Analysis– Apple is primarily a hardware company and likes high margin products whereas payments is a

service business with very thin margins.– Apple is a pretty focused company, doing a few things well. – Apple needs more than millions of consumers that have payment instruments with iTunes.

They need merchants and building this base is expensive and time consuming – Building a payment service requires know‐how– Apple iTunes stores only bank cards (not ACH) placing them at a disadvantage against PayPal

who has lower funding costs What are they doing?

– Licensing their checkout software to other merchants– Positioning iPads as the POS device of choice– Positioning passbook as a wallet but with no money

movement capabilities

Square Wallet Background

– Renamed Card Case app to “Pay with Square” to “Square Wallet” How It Works

– Consumers download the Square Wallet app and load payment credentials (e.g. credit cards or debit cards) and a photo – works with IOS and Android phones and most networks

– Payments credentials are stored in the Cloud– Consumer select the Square enabled merchant they want to shop at , and “start a tab”– At checkout, consumers give their name to the Square merchant, effectively using their

name and photo as the payment credentials– Square approves transaction based on card authorization response– Square collects from consumer’s card and pays merchant (via ACH)

Economics– Merchants pay 2.75% per swipe, no additional fees, next day deposit– Unknown COP but expected CNP average of 2.10% ± a few bps

Recent Developments– Visa makes undisclosed investment in Square (2011)– Starbucks invested $25 Million in, and switched its payments

processing to Square (2012)– US Bank encouraging customers to link their US Bank cards to Square

• Cards• Bank account• Phone bill

• Mag stripe• Mobile

number• Bar Code• NFC/FFC• Biometric

• Generic• Industry

Specific

• Captive• Independent

Processing Scope

FundingTechnology

Tabbedout – Mobile Tabs Background

– Company founded in 2009 as a payments solution for bars and restaurants How it works

– Consumers download the Tabbedout app and load payment credentials (e.g. credit cards or debit cards) – works with IOS and Android phones

– Payments credentials are stored in the phone (but not using NFC / SE); only last 4 digits are displayed, consumer use passwords to access app

– Merchant must be a Tabbedout merchant (bar or restaurant)– When consumer “starts a tab” s/he receives a five digit code which must

be presented to server – Consumer name and payment card information is sent to merchant’s POS

(not using NFC) – Consumers can pay the tab by selecting payments card, calculating and

adding tip and pressing “pay tab” Economics

– Merchant processes the transaction via its own card processor– Merchant pays a licensing fee to Tabbedout– Tabbedout offering SDK for merchants and third party providers

(e.g. T.G.I. Friday’s)– Google Wallet available on Tabbedout

• Cards• Bank account• Phone bill

• Mag stripe• Mobile

number• Bar Code• NFC/FFC• Biometric

• Generic• Industry

Specific

• Captive• Independent

Processing Scope

FundingTechnology

Boku – Pay Through Carrier Background

– Founded in 2009 to use mobile phone number as a safe payment method– Acquired Paymo and Mobilcash also in 2009– Currently serving 66 countries, 240 carriers globally

How it works– There is no registration process; payment credential is the mobile phone number– Merchant must be a Boku merchant– Consumers enters phone number when checking out– Consumers receive a prompt through SMS asking to confirm purchase with a “Y”– Purchase is charged to phone bill (either pre‐ or post‐paid)– Carrier pays Boku and Boku pays merchant

Economics– Merchant fee can be >10% limiting

acceptance to digital goods only– Recent deals with PlayJam and Sony

PlayStation

• Cards• Bank account• Phone bill

• Mag stripe• Mobile

number• Bar Code• NFC/FFC• Biometric

• Generic• Industry

Specific

• Captive• Independent

Processing Scope

FundingTechnology

Starbucks – “Gold Standard”?

Background– Launched first mobile app in September 2009

How it works– Consumers download the Starbucks app and load payment credentials (e.g.

credit cards or debit cards) – works with iOS and Android phones – Payment credentials in in the Cloud– Merchants are only Starbucks stores (closed loop)– Consumer must preload funds into their Starbuck wallet (normally $20 or $25)– Consumer presents bar code representing Starbucks Stored Value card number

to scanner– Value is automatically debited from stored value

Economics ‐ A Financial Success– Over $1B loaded to card balances in Q1 2013

• (mobile is 25% of card volume)– Average load/purchase $25/$5– Card fee savings per load $1– Card program contribution of $170MM/Qtr.

• Cards• Bank account• Phone bill

• Mag stripe• Mobile

number• Bar Code• NFC/FFC• Biometric

• Generic• Industry

Specific

• Captive• Independent

Processing Scope

FundingTechnology

Other Retailer Wallets

The “Layering” of Mobile Payments

App1Function1

Function2

Function3

Payments

App2Function1

Function2

Function3

Payments

App 3Function1

Function2

Function3

Payments

App1Function1

Function2

Function3

Payments

App2Function1

Function2

Function3

Payments

App 3Function1

Function2

Function3

PaymentsPayments

Other Wallets Worth Mentioning Wallets offered by Card Schemes

– V.me by Visa, MasterCard’s PayPass Wallet Services are primarily online wallets accepting only cards (a.k.a. PayPal minus the ACH). Mobile services “coming soon”

– Amex’s Serve is a pre‐paid card where mobile can be used to send or receive money but not to conduct any purchases

Traditional Online Wallets– Amazon’s Flexible Payments, ClickandBuy, Skrill Moneybookers all are

traditional online wallets with possibility of entering mobile payments

Industry Specific Wallets– Parking and Tolls (ParkNow!, ParkMobile, PayByPhone)

– Vending (Apriva)

– Food / QSR (OLO/GoMobo, GrubHub, Menuism, GoPago, Jamba Juice)

– Closed Loop (Chipotle, Burger King, T.G.I. Friday’s)

– Gift cards and promotions (Mocapay, Modo)

Other carrier billing wallets– PayByPhone, Zong, BilltoMobile

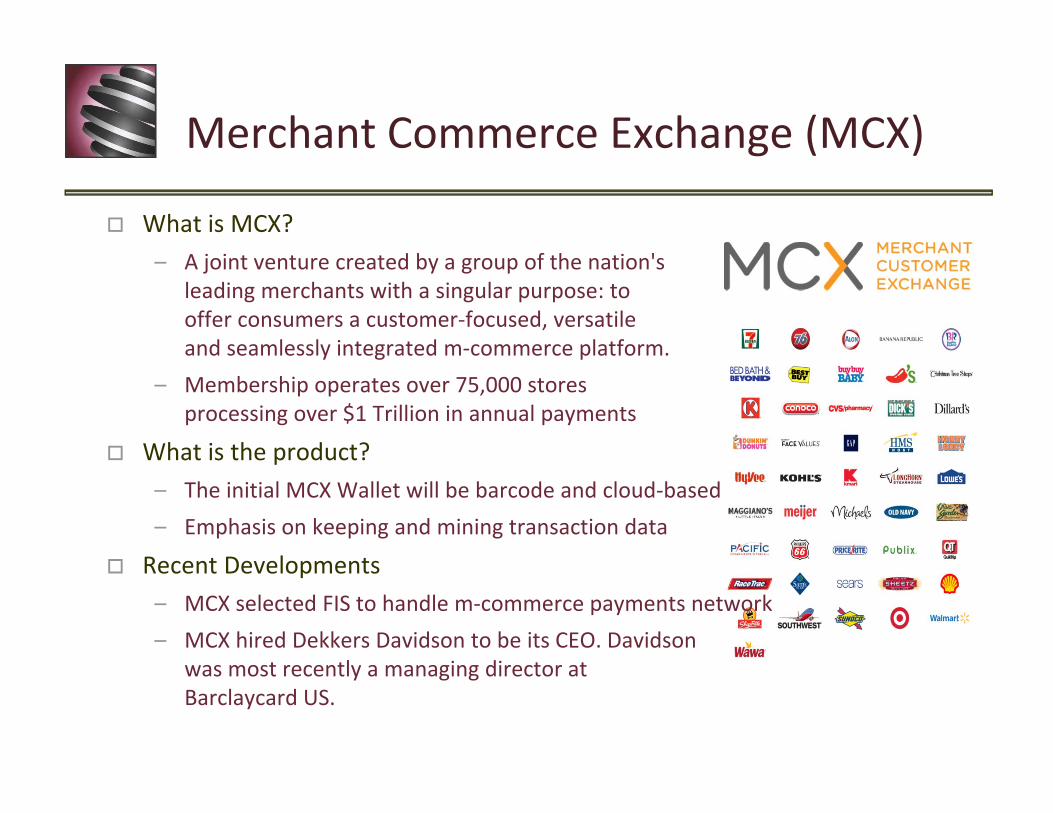

Merchant Commerce Exchange (MCX)

What is MCX?– A joint venture created by a group of the nation's

leading merchants with a singular purpose: to offer consumers a customer‐focused, versatile and seamlessly integrated m‐commerce platform.

– Membership operates over 75,000 stores processing over $1 Trillion in annual payments

What is the product?– The initial MCX Wallet will be barcode and cloud‐based– Emphasis on keeping and mining transaction data

Recent Developments – MCX selected FIS to handle m‐commerce payments network– MCX hired Dekkers Davidson to be its CEO. Davidson

was most recently a managing director at Barclaycard US.

At the End of the Day…

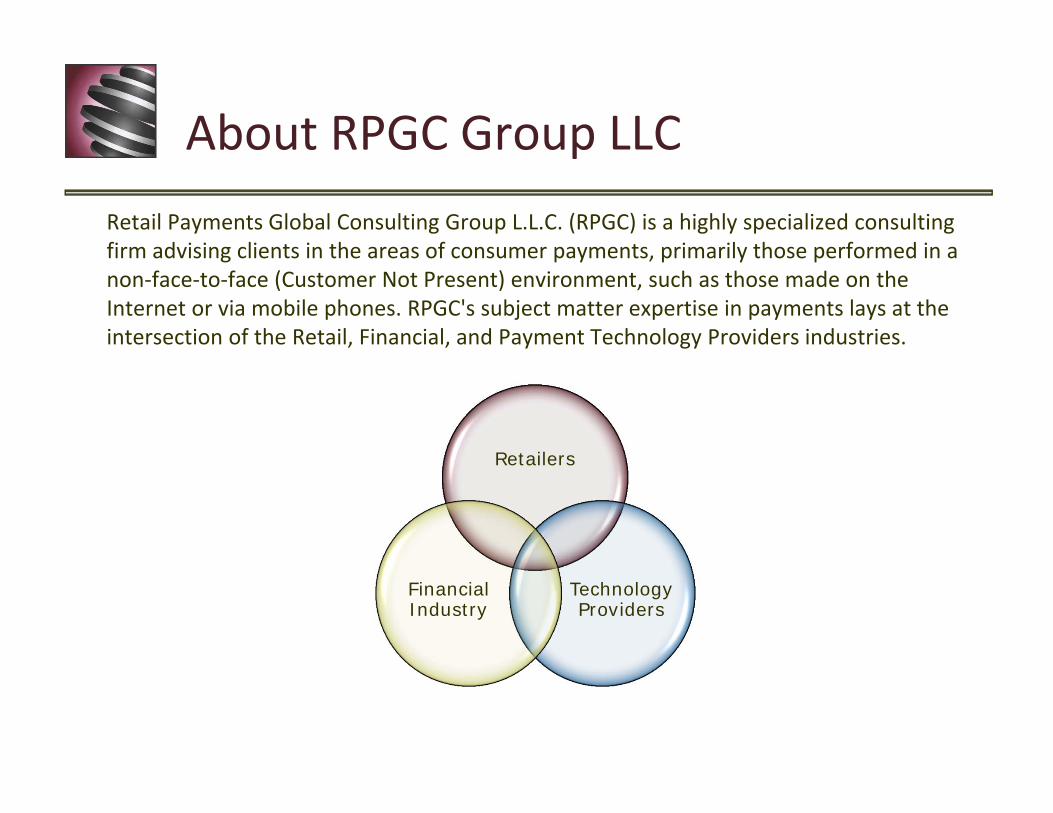

About RPGC Group LLCRetail Payments Global Consulting Group L.L.C. (RPGC) is a highly specialized consulting firm advising clients in the areas of consumer payments, primarily those performed in a non‐face‐to‐face (Customer Not Present) environment, such as those made on the Internet or via mobile phones. RPGC's subject matter expertise in payments lays at the intersection of the Retail, Financial, and Payment Technology Providers industries.

Retailers

Technology Providers

Financial Industry

RPGC Group Areas of Expertise Payments Strategic Thinking

– Situation Assessment Workshops– Strategic Planning Facilitation

Payment Processing Optimization– Financial Optimization– Best Practices Audit– RFP/RFI Management

Product Management & Marketing– Product “Tune Up”– Product Management & Marketing

Global Payments Education– Payments 101 – Payment Basics– Payments 201 – Payment Economics– Payments 301 – Global Payments– Customized classes

Payments Strategic Thinking

Payment Processing Optimization

Payment Product Management &

Marketing

Global Payments Education

RPGC

Contact Information

15805 212th Ave NEWoodinville, WA 98077, U.S.A.

Phone: +1‐425‐788‐0500Web: www.rpgc.com