Embed Size (px)

Citation preview

Mississippi Association of Self-Insurers

Mississippi Insurance DepartmentFebruary 25, 2014

Kaiser Family Foundation Presents:“The YouToons Get Ready for Obamacare”

2

Federally-Facilitated Marketplace

• The ACA requires that every State will have an operational Health Insurance Marketplace, either established by the state or federal government by January 1, 2014.

• The Mississippi Health Insurance Marketplace will be operated entirely by the federal government.

• The Federal Department of Health and Human Services assumes full responsibility for the establishment and operation of the Federally-Facilitated Marketplace (FFM) in Mississippi.

3

Federal Government Role in the Mississippi FFM

• Controls the criteria for plan certification and participation and also has regulatory authority over plans offered in the Mississippi FFM.

• Determines who will serve as navigators, agents, brokers, and assisters in Mississippi and oversees the standards and financing of these roles.

• Administers the application process and operates customer service for the Mississippi FFM.

• Determines advanced premium tax credits and eligibility.

4

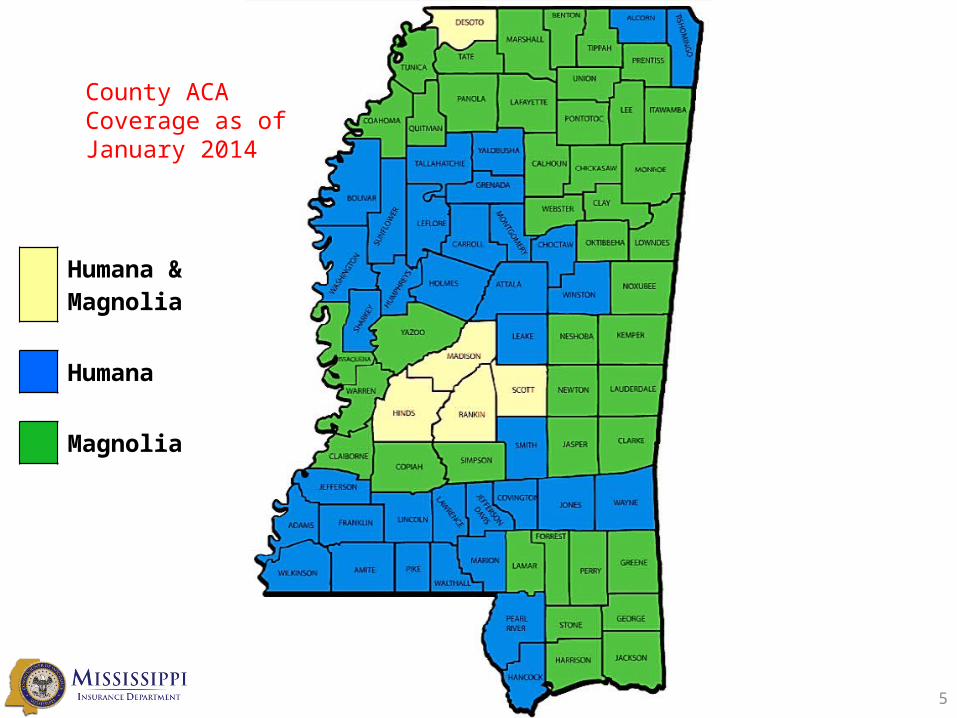

5

Humana & Magnolia

Humana

Magnolia

County ACA Coverage as of January 2014

6

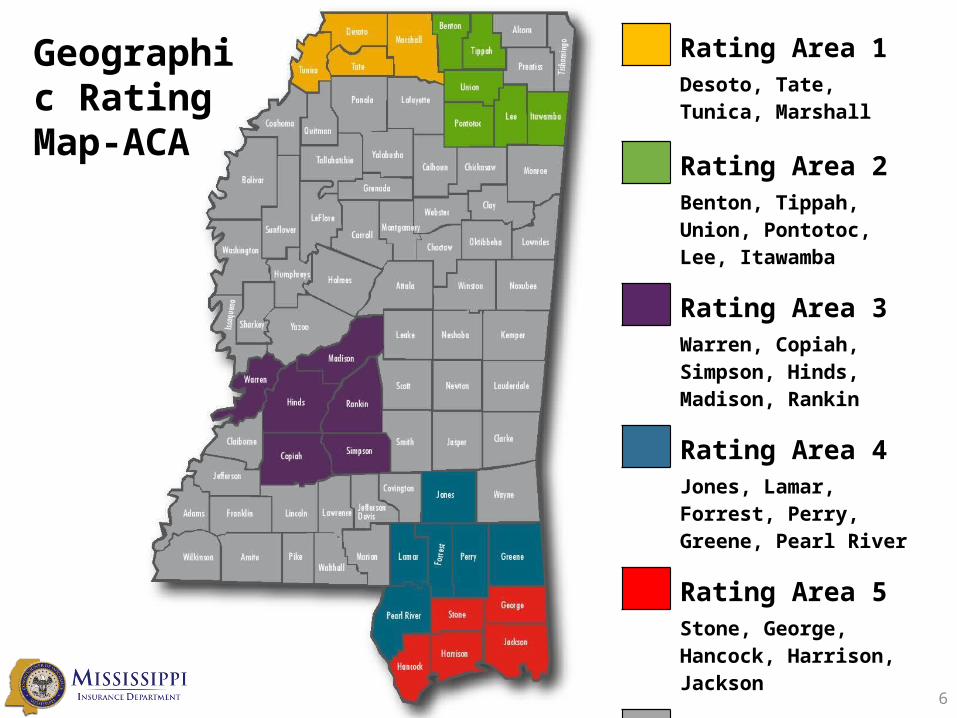

Geographic RatingMap-ACA

Rating Area 1Desoto, Tate, Tunica, Marshall

Rating Area 2Benton, Tippah, Union, Pontotoc, Lee, Itawamba

Rating Area 3Warren, Copiah, Simpson, Hinds, Madison, Rankin

Rating Area 4Jones, Lamar, Forrest, Perry, Greene, Pearl River

Rating Area 5Stone, George, Hancock, Harrison, Jackson

Rating Area 6All Remaining Counties

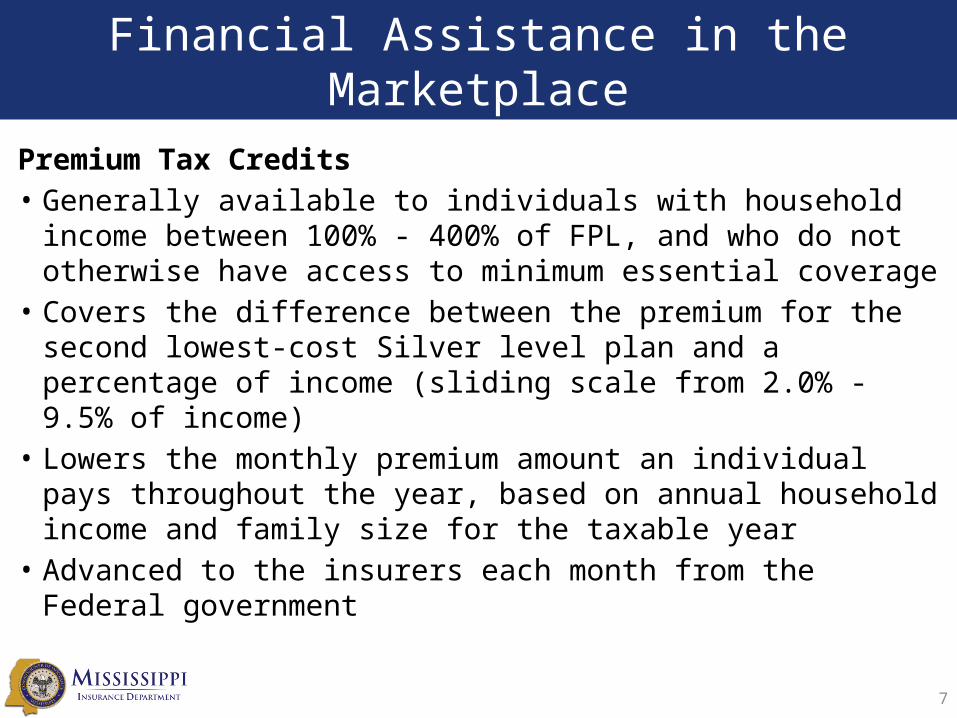

Financial Assistance in the Marketplace

Premium Tax Credits• Generally available to individuals with household income

between 100% - 400% of FPL, and who do not otherwise have access to minimum essential coverage

• Covers the difference between the premium for the second lowest-cost Silver level plan and a percentage of income (sliding scale from 2.0% - 9.5% of income)

• Lowers the monthly premium amount an individual pays throughout the year, based on annual household income and family size for the taxable year

• Advanced to the insurers each month from the Federal government

7

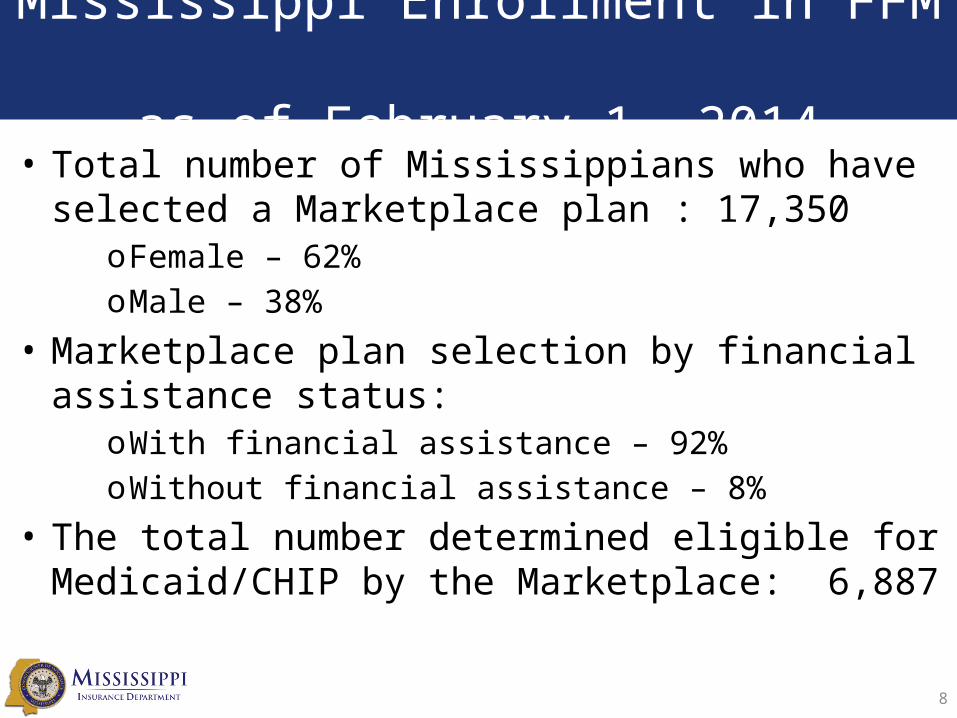

Mississippi Enrollment in FFM as of February 1, 2014

• Total number of Mississippians who have selected a Marketplace plan : 17,350

oFemale – 62%oMale – 38%

• Marketplace plan selection by financial assistance status:

oWith financial assistance – 92%oWithout financial assistance – 8%

• The total number determined eligible for Medicaid/CHIP by the Marketplace: 6,887

8

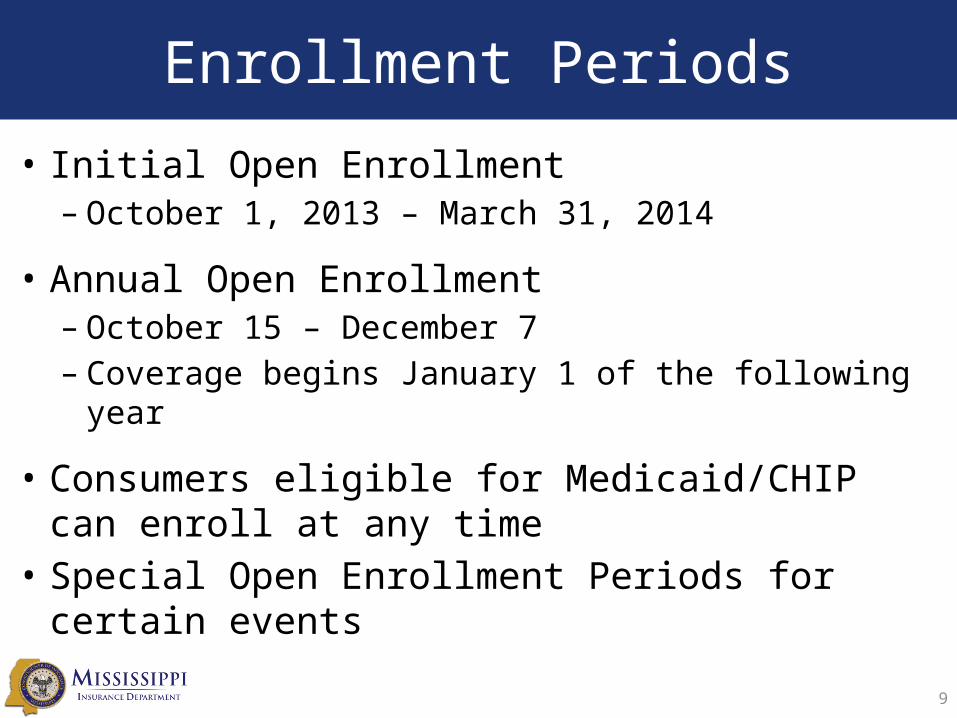

Enrollment Periods

9

• Initial Open Enrollment– October 1, 2013 – March 31, 2014

• Annual Open Enrollment– October 15 – December 7– Coverage begins January 1 of the following year

• Consumers eligible for Medicaid/CHIP can enroll at any time

• Special Open Enrollment Periods for certain events

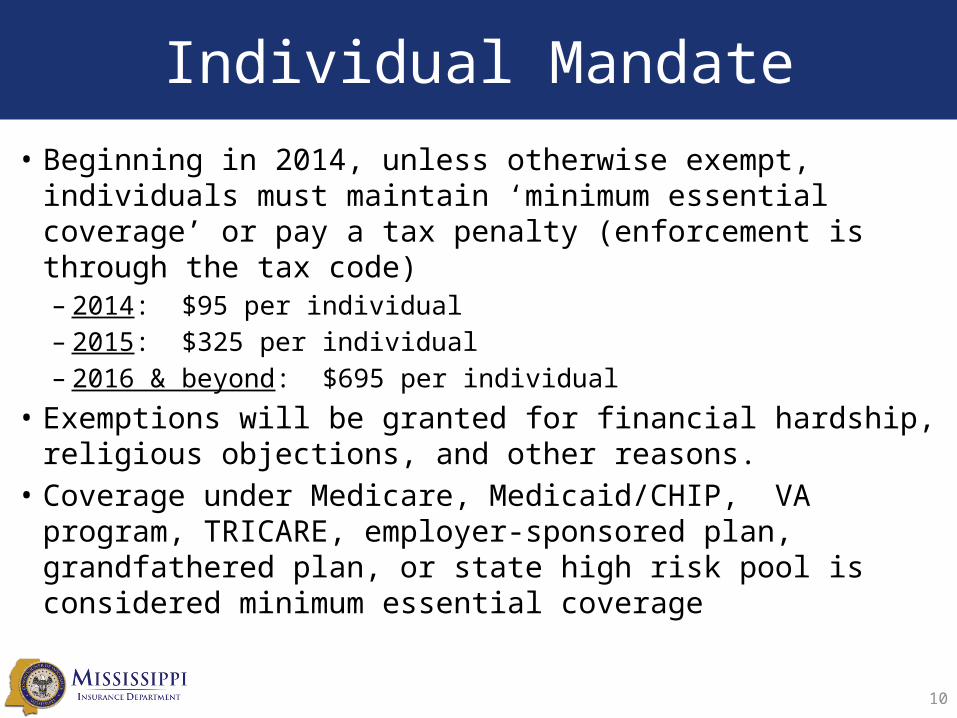

Individual Mandate

10

• Beginning in 2014, unless otherwise exempt, individuals must maintain ‘minimum essential coverage’ or pay a tax penalty (enforcement is through the tax code)– 2014: $95 per individual– 2015: $325 per individual– 2016 & beyond: $695 per individual

• Exemptions will be granted for financial hardship, religious objections, and other reasons.

• Coverage under Medicare, Medicaid/CHIP, VA program, TRICARE, employer-sponsored plan, grandfathered plan, or state high risk pool is considered minimum essential coverage

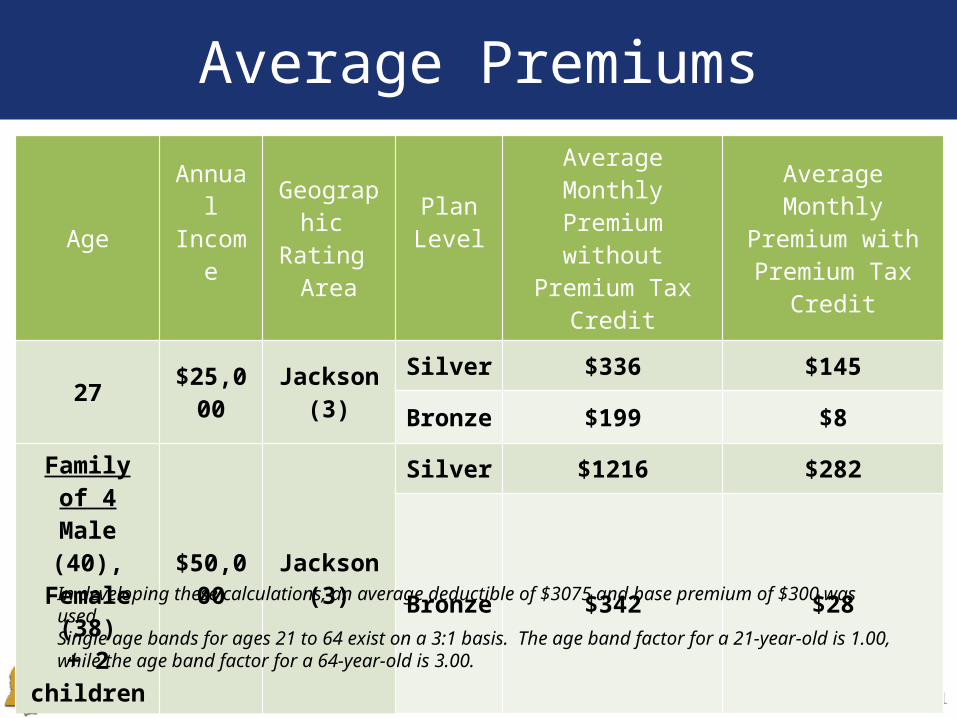

Average Premiums

11

AgeAnnual Income

Geographic Rating Area

Plan Level

Average Monthly Premium

without Premium Tax Credit

Average Monthly Premium with

Premium Tax Credit

27 $25,000 Jackson (3)Silver $336 $145

Bronze $199 $8

Family of 4Male (40),

Female (38)+ 2 children

$50,000 Jackson (3)

Silver $1216 $282

Bronze $342 $28

In developing these calculations, an average deductible of $3075 and base premium of $300 was used.Single age bands for ages 21 to 64 exist on a 3:1 basis. The age band factor for a 21-year-old is 1.00, while the age band factor for a 64-year-old is 3.00.

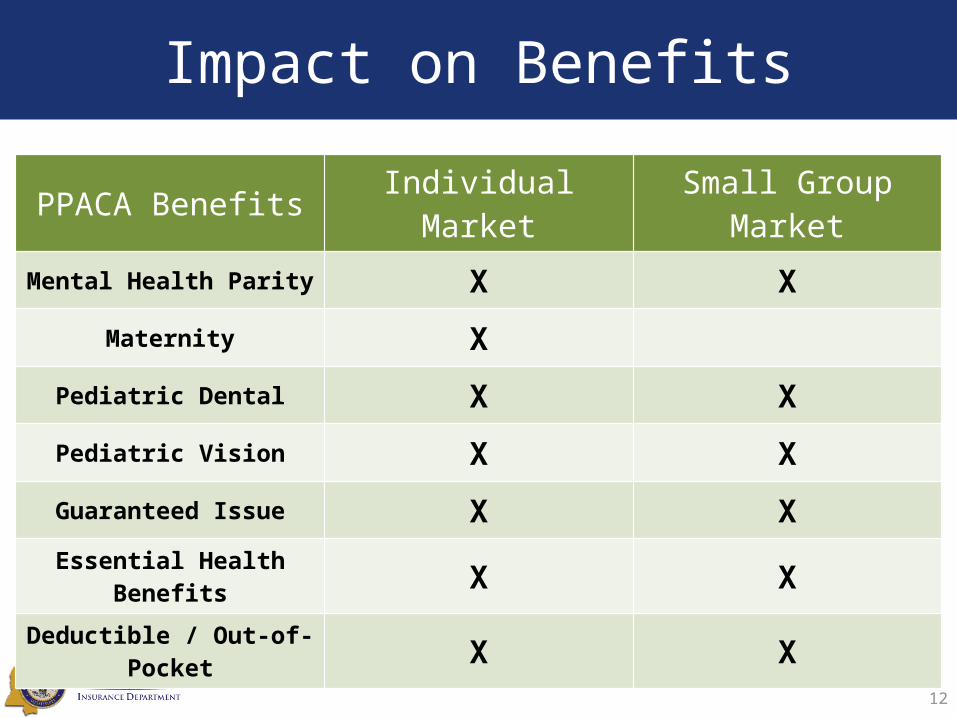

Impact on Benefits

12

PPACA Benefits Individual Market Small Group Market

Mental Health Parity X X

Maternity X

Pediatric Dental X X

Pediatric Vision X X

Guaranteed Issue X X

Essential Health Benefits X X

Deductible / Out-of-Pocket X X

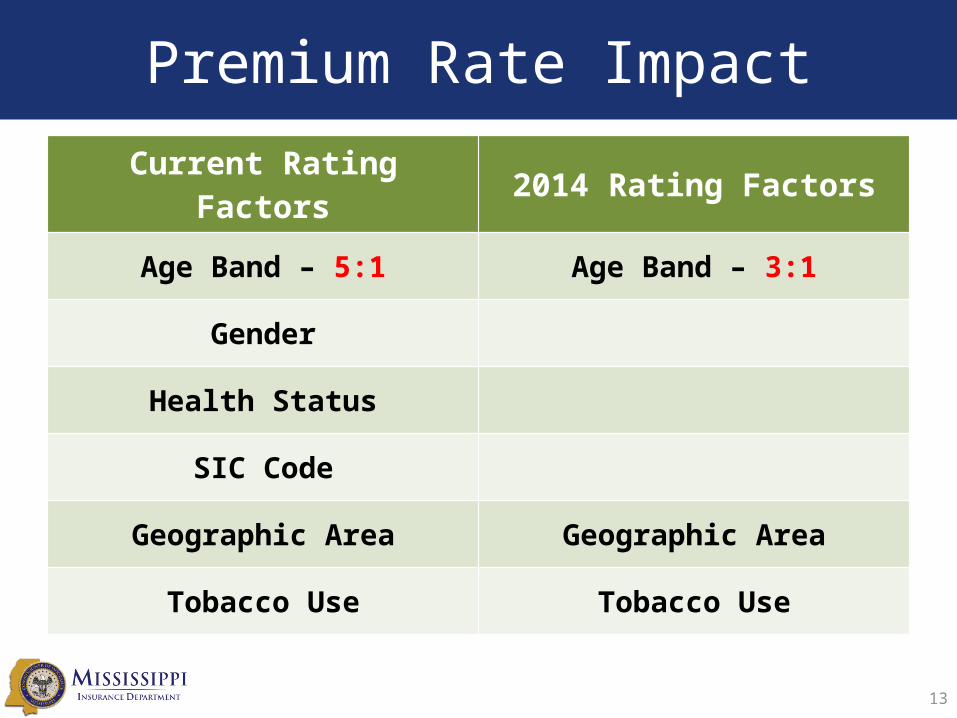

Premium Rate Impact

13

Current Rating Factors 2014 Rating Factors

Age Band – 5:1 Age Band – 3:1

Gender

Health Status

SIC Code

Geographic Area Geographic Area

Tobacco Use Tobacco Use

14

lim𝑛→∞ (1+ 1𝑛 )

𝑛

“The ACA unknown effect on Health Care and Insurance cost”

15

Series10

20

40

60

80

100

120

140

160

180

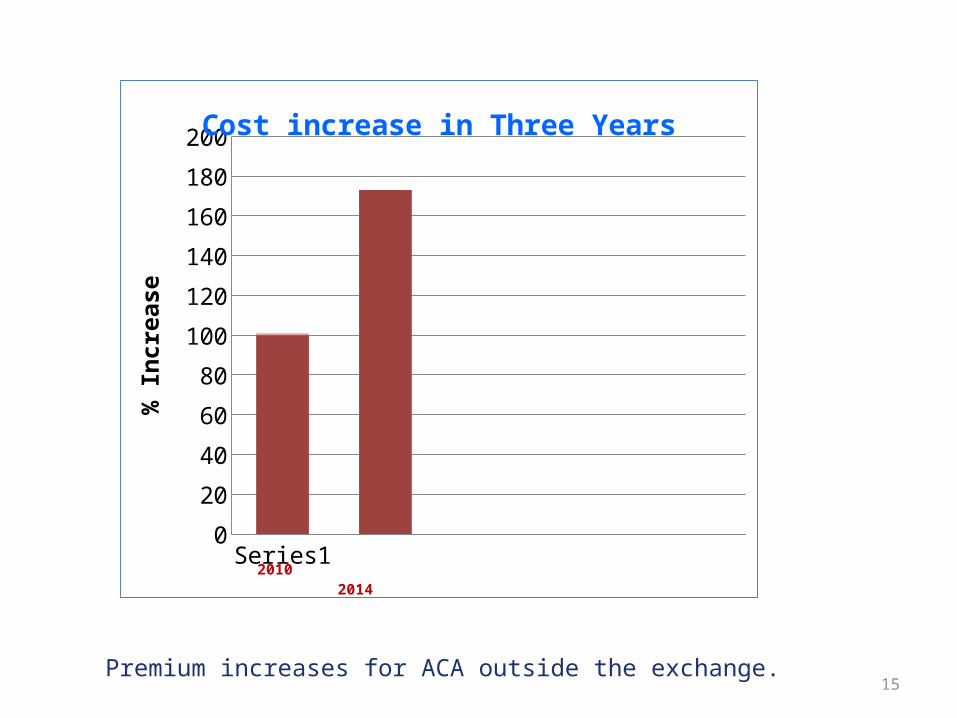

200Cost increase in Three Years

% In

crea

se

2010 2014

Premium increases for ACA outside the exchange.

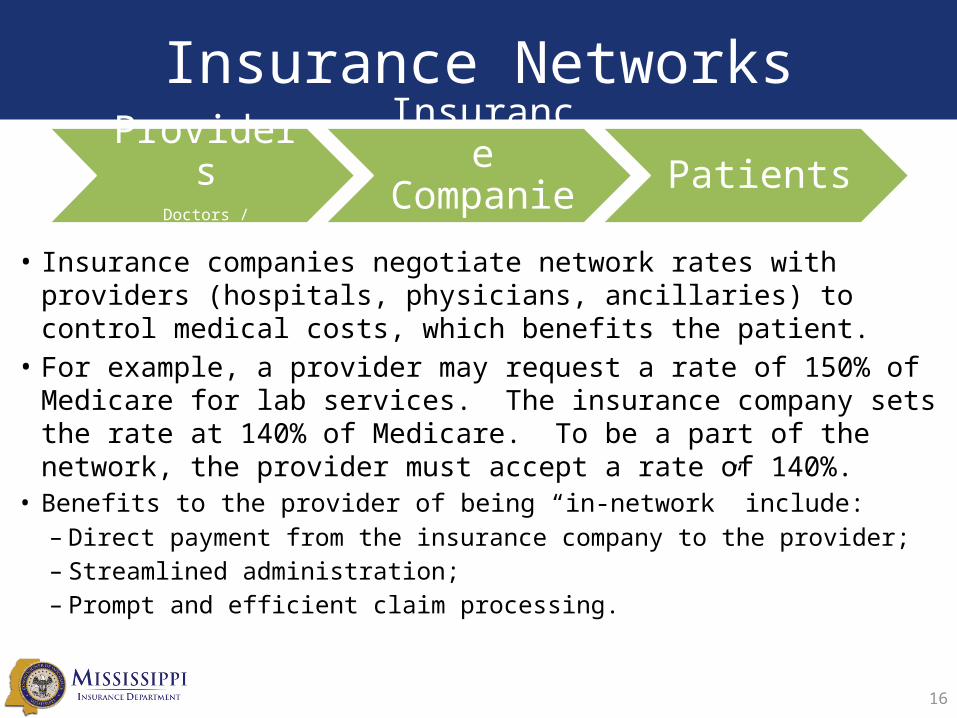

Insurance Networks

ProvidersDoctors / Hospitals / Clinics

Insurance Companies Patients

16

• Insurance companies negotiate network rates with providers (hospitals, physicians, ancillaries) to control medical costs, which benefits the patient.

• For example, a provider may request a rate of 150% of Medicare for lab services. The insurance company sets the rate at 140% of Medicare. To be a part of the network, the provider must accept a rate of 140%.

• Benefits to the provider of being “in-network” include:– Direct payment from the insurance company to the provider;– Streamlined administration;– Prompt and efficient claim processing.

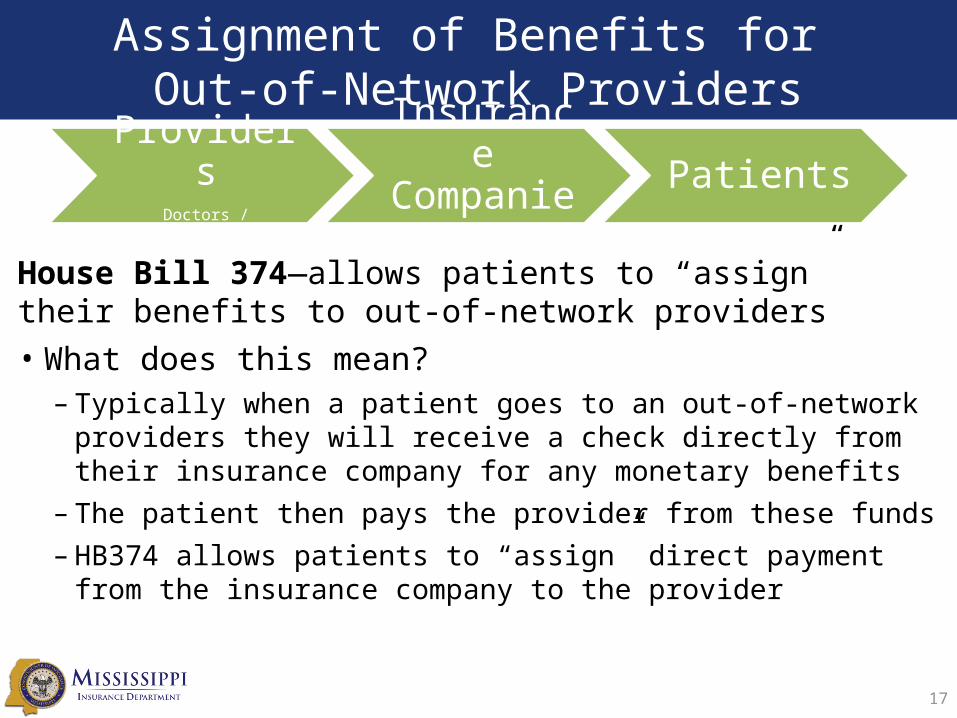

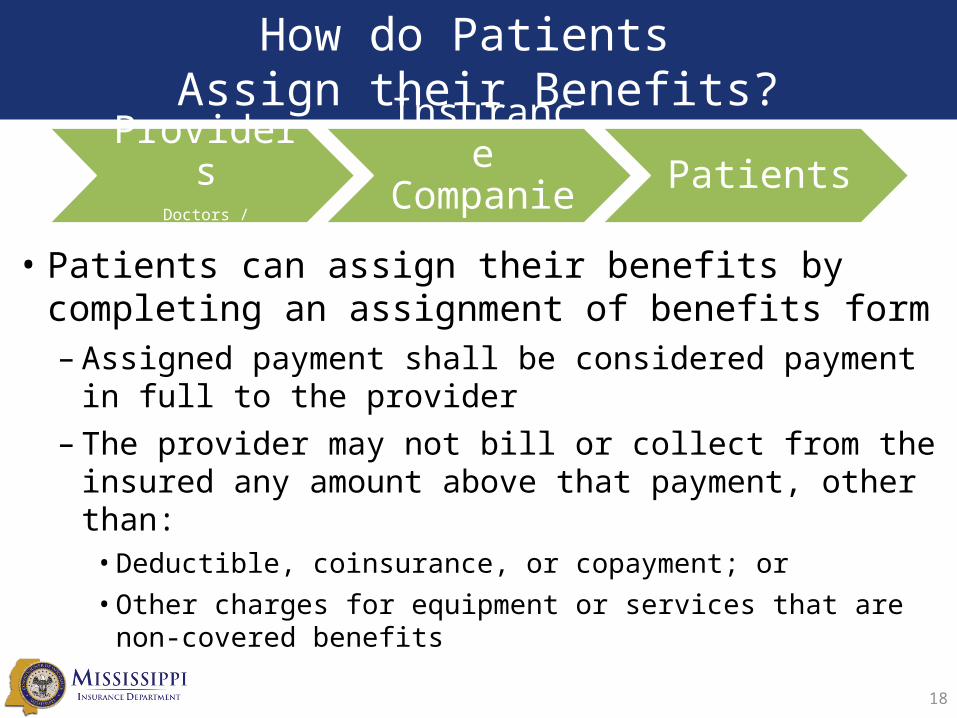

Assignment of Benefits for Out-of-Network Providers

House Bill 374—allows patients to “assign” their benefits to out-of-network providers• What does this mean?– Typically when a patient goes to an out-of-network

providers they will receive a check directly from their insurance company for any monetary benefits

– The patient then pays the provider from these funds

– HB374 allows patients to “assign” direct payment from the insurance company to the provider

17

ProvidersDoctors / Hospitals / Clinics

Insurance Companies Patients

How do Patients Assign their Benefits?

• Patients can assign their benefits by completing an assignment of benefits form– Assigned payment shall be considered payment in full to

the provider

– The provider may not bill or collect from the insured any amount above that payment, other than:• Deductible, coinsurance, or copayment; or

• Other charges for equipment or services that are non-covered benefits

18

ProvidersDoctors / Hospitals / Clinics

Insurance Companies Patients

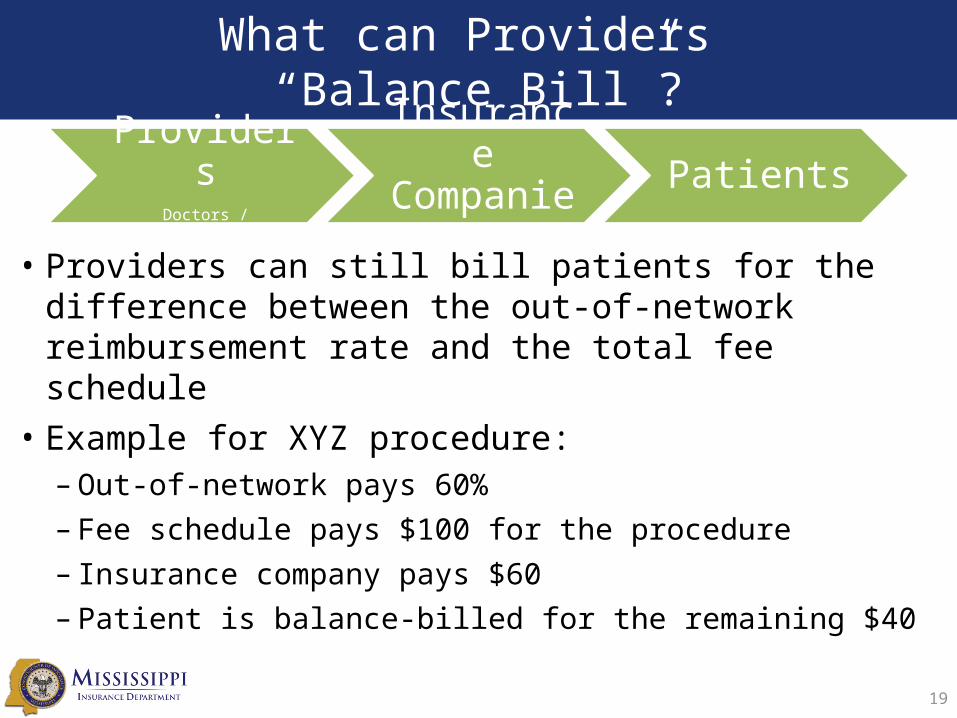

What can Providers “Balance Bill”?

• Providers can still bill patients for the difference between the out-of-network reimbursement rate and the total fee schedule

• Example for XYZ procedure:– Out-of-network pays 60%

– Fee schedule pays $100 for the procedure

– Insurance company pays $60

– Patient is balance-billed for the remaining $4019

ProvidersDoctors / Hospitals / Clinics

Insurance Companies Patients

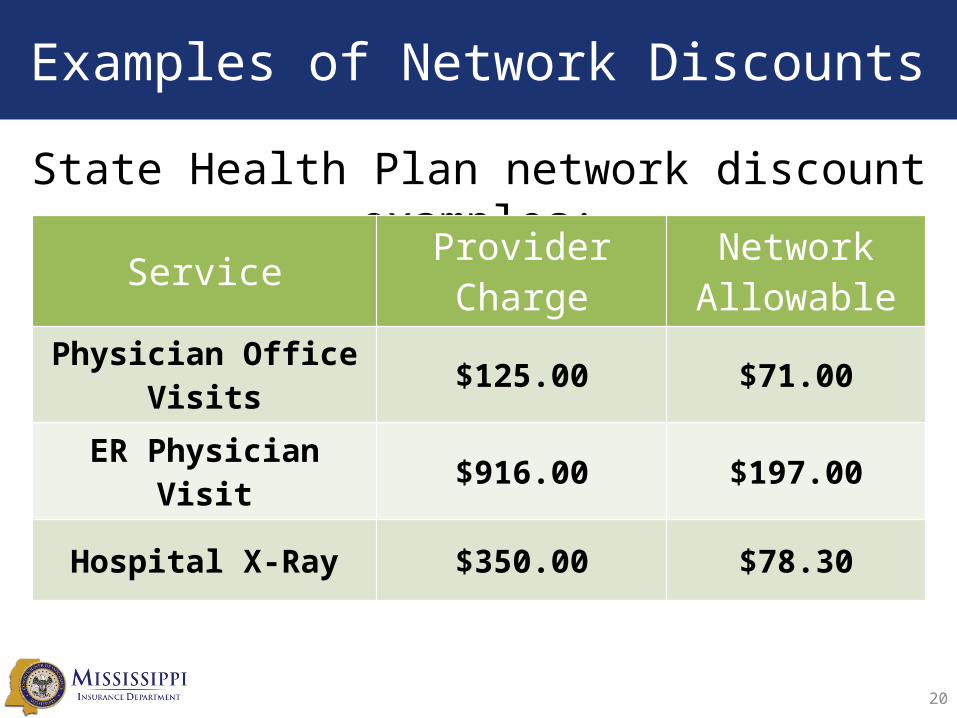

Examples of Network Discounts

State Health Plan network discount examples:

20

Service Provider Charge Network Allowable

Physician Office Visits $125.00 $71.00

ER Physician Visit $916.00 $197.00

Hospital X-Ray $350.00 $78.30

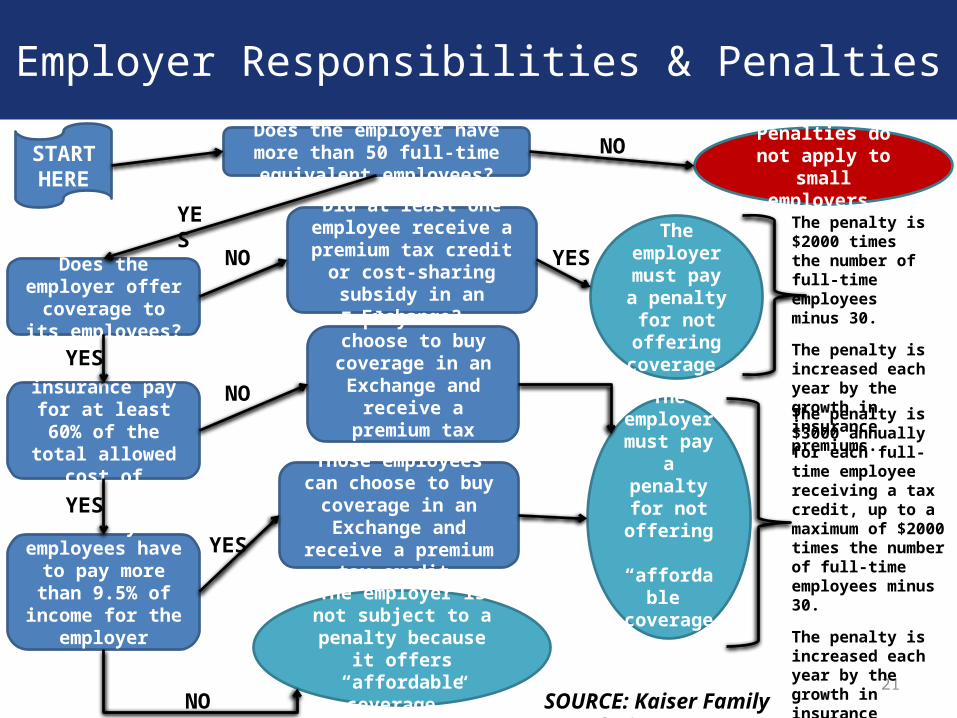

Employer Responsibilities & Penalties

21

Does the employer have more than 50 full-time equivalent employees?

Does the employer offer coverage to its

employees?

Did at least one employee receive a premium tax credit or cost-sharing

subsidy in an Exchange?

Penalties do not apply to small

employers.

The employer

must pay a penalty for not offering

coverage.

Does the insurance pay for at least 60% of the total allowed

cost of benefits?

Employees can choose to buy coverage in an

Exchange and receive a premium tax credit.

Do any employees have to pay more

than 9.5% of income for the employer

coverage?

Those employees can choose to buy coverage in an Exchange and receive a

premium tax credit.

The employer

must pay a penalty for

not offering “affordable”

coverage.

START HERE

NO

YES

NO YES

YES

YES

NO

YES

The employer is not subject to a penalty

because it offers “affordable coverage.”

NO

The penalty is $2000 times the number of full-time employees minus 30.

The penalty is increased each year by the growth in insurance premiums.

The penalty is $3000 annually for each full-time employee receiving a tax credit, up to a maximum of $2000 times the number of full-time employees minus 30.

The penalty is increased each year by the growth in insurance premiums.

SOURCE: Kaiser Family Foundation

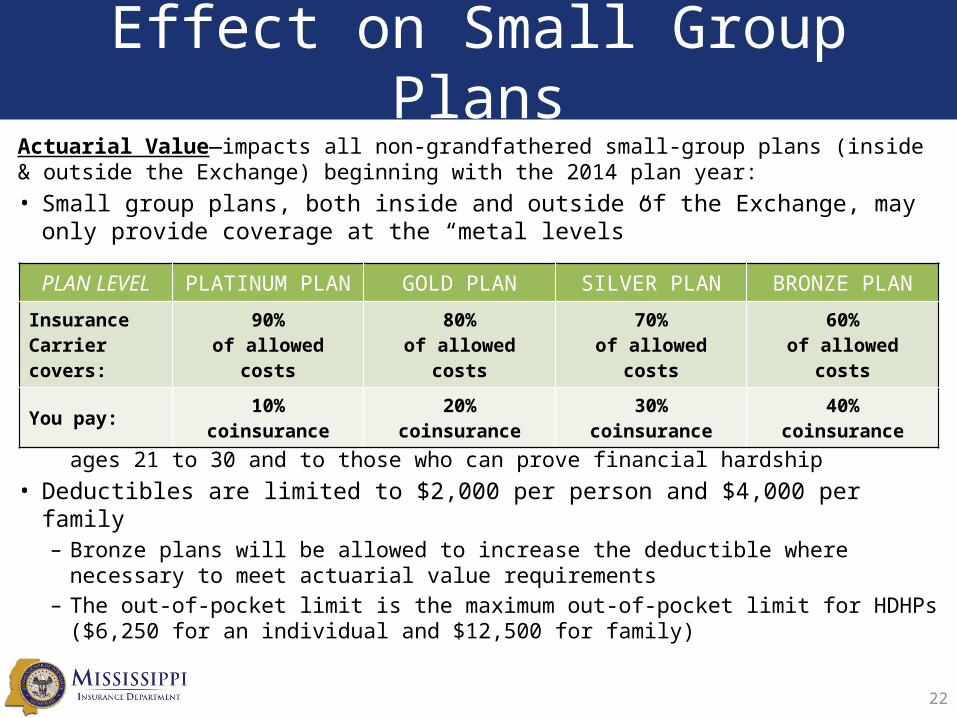

Effect on Small Group Plans

22

Actuarial Value—impacts all non-grandfathered small-group plans (inside & outside the Exchange) beginning with the 2014 plan year:• Small group plans, both inside and outside of the Exchange, may only provide

coverage at the “metal levels”

– Catastrophic Plan—offered both in & out of Exchanges to individuals ages 21 to 30 and to those who can prove financial hardship

• Deductibles are limited to $2,000 per person and $4,000 per family– Bronze plans will be allowed to increase the deductible where necessary to meet

actuarial value requirements– The out-of-pocket limit is the maximum out-of-pocket limit for HDHPs ($6,250 for

an individual and $12,500 for family)

PLAN LEVEL PLATINUM PLAN GOLD PLAN SILVER PLAN BRONZE PLAN

Insurance Carrier covers:

90%of allowed costs

80%of allowed costs

70%of allowed costs

60%of allowed costs

You pay:10%

coinsurance20%

coinsurance30%

coinsurance40%

coinsurance

Employer Responsibilities

23

• Large employers (generally those with over 50 full-time employees) are subject to the Employer Shared Responsibility Provisions

• Under these provisions, if an employer does not offer affordable health coverage that provides a minimum level of benefits to their full-time employees, the employer may be assessed a payment if at least one of their full-time employees receives a premium tax credit through the Exchange– Affordable: Employee’s share of the premium costs less than

9.5% of the employee’s W-2 wages– Minimum value: the plan offered must cover at least 60% of

the total allowed cost of benefits

• Small employers are not subject to these provisions

The Employer Shared Responsibility Provisions arenot effective until January 1, 2015.

Benefits of Employee Choice

• Benefits of an employee choice model include:– More predictable costs for the employer, since they

can choose the amount each year to contribute– Reduced administrative burden for employers,

since they do not have to choose a plan for all employees or manage the employees’ plan

– Employees would be able to select a plan that is best for them and their families

24

25

Conditional Approval Process

• September 18, 2013:– Mississippi representatives participated in the

required Exchange Grant Design Review with Centers for Medicare & Medicaid Services (CMS) staff for approval to move forward

• October 1, 2013:– MID received letter from Kathleen Sebelius,

Secretary of Health and Human Services, granting MID conditional approval to operate a SHOP Marketplace

26

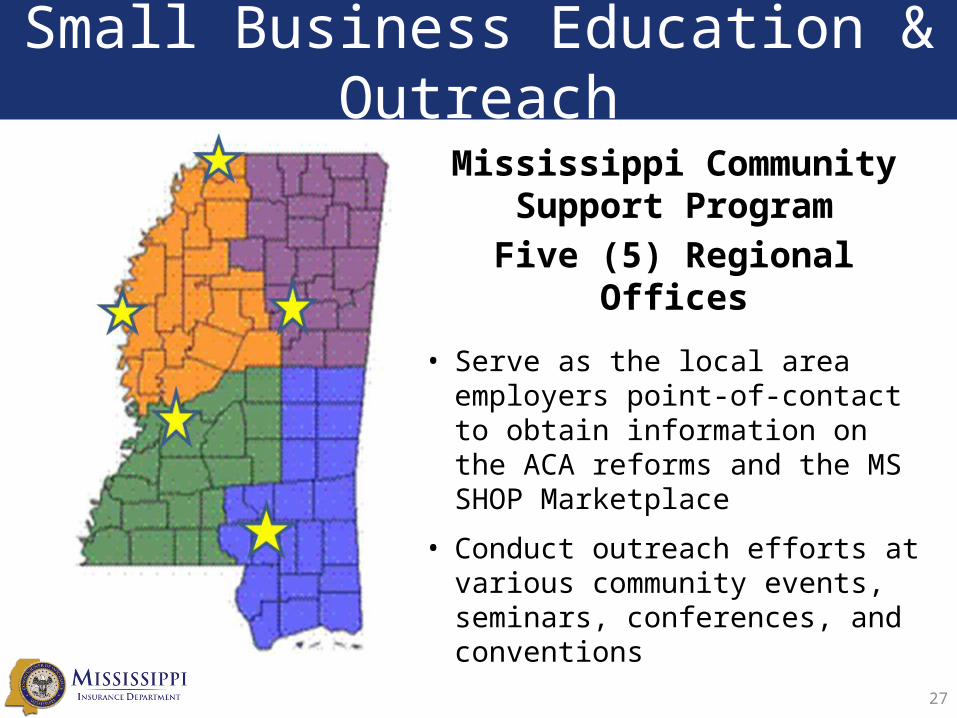

Small Business Education & Outreach

Mississippi Community Support Program

Five (5) Regional Offices

• Serve as the local area employers point-of-contact to obtain information on the ACA reforms and the MS SHOP Marketplace

• Conduct outreach efforts at various community events, seminars, conferences, and conventions

27

Small Business Tax Credit

28

• Employers that meet the following qualifications could be eligible for a Small Business Tax Credit of up to 35% (25% for nonprofits):– Employ 25 or fewer full-time equivalent employees;– Pay average annual wages below $50,000; and– Cover at least 50% of the cost of individual health insurance for

each employee.

• Beginning in 2014, the Small Business Tax Credit increases to 50% (35% for non-profits) for qualifying businesses

• www.irs.gov/uac/Small-Business-Health-Care-Tax-Credit-for-Small-Employers

Mississippi SHOP Marketplace

• SHOP—Small Business Health Options Program• Recent Federal regulations allow states to apply to operate a

state-based SHOP marketplace, which Mississippi has moved forward with pursuing.

• A SHOP Marketplace is designed to assist small employers and facilitate online enrollment of employees into a variety of health plans, as well as:– Offer a flexible and easy-to-understand plan selection process, and– Include services for premium billing and payment processing for

employers.

• MID has received conditional approval from CMS to develop a SHOP Marketplace to be operational in early 2014.

29

What Are Hospitals Facing?Requirements for 501(c)(3) Hospitals Under the ACA:

Any 501(c)(3) hospital organization that operates one or more hospital facilities will be required to meet four general requirements on a facility-by-facility basis:– Establish written financial assistance and emergency medical care

policies;– Limit amounts charged for emergency or other medically necessary care

to individuals eligible for assistance under the hospital’s financial assistance policy;

– Make reasonable efforts to determine whether and individual is eligible for assistance under the hospital’s financial assistance policy before engaging in extraordinary collection actions against the individual; and

– Conduct a community health needs assessment (CHNA) and adopt an implementation strategy at least once every three years (These CHNA requirements are effective for tax years beginning after March 23, 2012).

30

What Are Hospitals Facing?

Physician-Owned Hospitals Restrictions– Prohibits existing physician-owned hospitals from

adding beds or operating rooms in order to qualify for Medicare payments

– Blocks new physician-owned hospitals from being opened

31

What Are Hospitals Facing?

Hospital Readmissions Reduction Program– Hospitals who readmit “excessive” numbers of Medicare patients

within 30 days of discharge now face significant penalties. The maximum penalty is 1% of hospitals Medicare reimbursement, but will increase to 3% in 2015.

Will the ACA Reduce Hospital Pricing Variations?– Recently CMS released data on rates charged by more than 3,000

hospitals who receive payments for Medicare inpatient services, which showed a very wide variation between hospitals rates for the same procedures.

– It is believed that the ACA will largely eliminate these price variations, by increasing the proportion of Americans with health insurance, thereby leading insurance providers to negotiate more reasonable prices from hospitals.

32

Resources

33

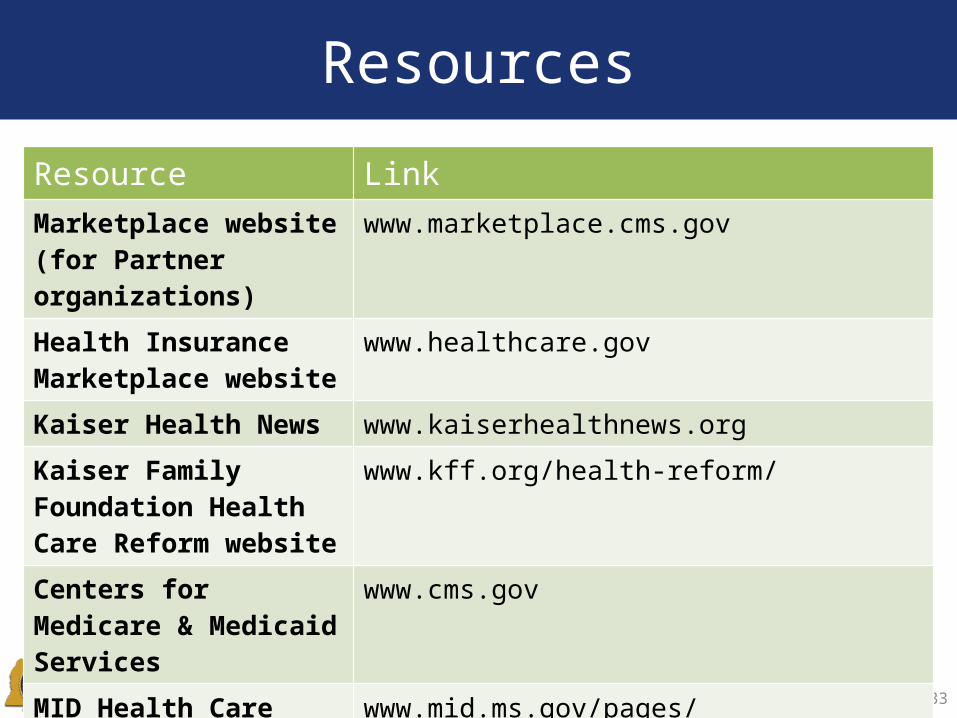

Resource LinkMarketplace website(for Partner organizations)

www.marketplace.cms.gov

Health Insurance Marketplace website

www.healthcare.gov

Kaiser Health News www.kaiserhealthnews.orgKaiser Family Foundation Health Care Reform website

www.kff.org/health-reform/

Centers for Medicare & Medicaid Services

www.cms.gov

MID Health Care Reform website

www.mid.ms.gov/pages/health_care_reform.aspx

Mississippi Insurance DepartmentCommissioner Mike Chaney

www.mid.ms.gov(601) 359-3569 • (800) 562-2957