Embed Size (px)

Citation preview

NASDAQ OMX

MIFID II – STATUS: ÄR BOLAGEN REDO? VAD SAKNAS

OCH VAD ÄR DOM STÖRSTA UTMANINGARNA?

Jimmy Kvarnström

Vice President, Head of Nordic/Baltic Legal

NASDAQ OMX

Nasdaq Commodities Product offering

2or US participants2

EXISTING PRODUCTSEXISTING PRODUCTS

POWER• Nordic • German• UK• Dutch• El‐Cert

POWER• Nordic • German• UK• Dutch• El‐Cert

EMISSIONS• EUA • EUAA• CER

EMISSIONS• EUA • EUAA• CER

GAS• UK Gas• Spark spreads

GAS• UK Gas• Spark spreads

FUTURE DEVELOPMENTSFUTURE DEVELOPMENTS

• Coal• Continental energy markets• Renewables• Steel• Oil‐ NFX

• Coal• Continental energy markets• Renewables• Steel• Oil‐ NFX

FREIGHT• Dry• Tankers • Fuel Oil• LPG• Iron ore

FREIGHT• Dry• Tankers • Fuel Oil• LPG• Iron ore

SEAFOOD• SalmonSEAFOOD

• Salmon

NASDAQ OMX

STRATEGY AND GROWTH APPROACH

GTMS Strategy ‐ 2015 3

Nasdaq Commodities’ strategy is to expand into a global unit

Be a leading Global Commodity exchange and clearing house

Our geographical extension include NFX (Nasdaq Futures, Inc.) in the US, Asian Strategy for Freight and Steel, the German Power initiative and soon other European Power markets

Continue to build a global product portfolio

Advantage of Nasdaq’s global brand

Increase distribution through GCMs / FCMs

MIFID II – IMPACT ON COMMODITIES

A REVOLUTION FOR COMMODITIES TRADING?

• Many energy and commodity trading business will be brought intothe mainstream of financial regulation

• Or several curtail their market activities• Including possibly market activities• Significant liquidity impact, especially in energy

• Consequential extension of other regiemes, especially EMIR

• New position controls on them and existing regulated firms

• New Transparancy requirements

MIFID II FOCUS AREAS FOR COMMODITIES

DEFINITION OF FINANCIAL INSTRUMENT

EXEMPTIONS ANCILLARY SERVICES

POSITION LIMITS / POSITION REPORTING

OPEN ACCESS

DETAILS STILL BEING DISCUSSED!!

77© Oliver Wyman

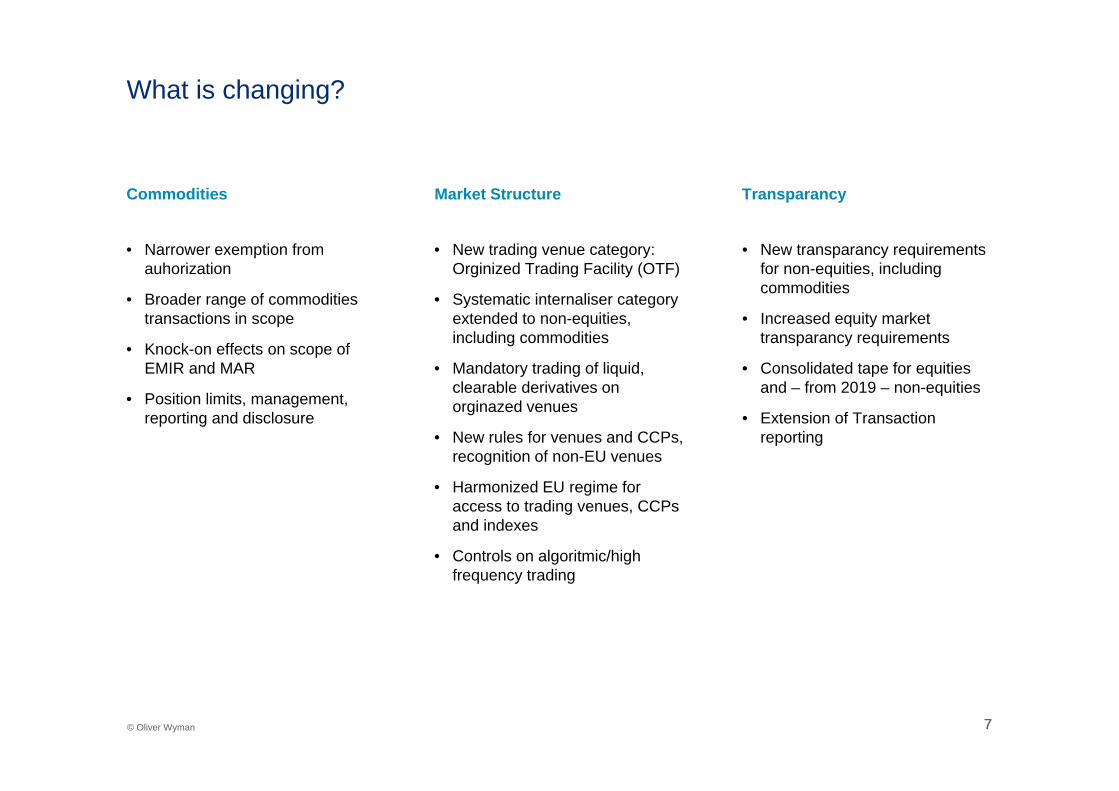

What is changing?

• Narrower exemption from auhorization

• Broader range of commoditiestransactions in scope

• Knock-on effects on scope of EMIR and MAR

• Position limits, management, reporting and disclosure

• New trading venue category: Orginized Trading Facility (OTF)

• Systematic internaliser categoryextended to non-equities, including commodities

• Mandatory trading of liquid, clearable derivatives on orginazed venues

• New rules for venues and CCPs, recognition of non-EU venues

• Harmonized EU regime for access to trading venues, CCPsand indexes

• Controls on algoritmic/highfrequency trading

• New transparancy requirementsfor non-equities, includingcommodities

• Increased equity market transparancy requirements

• Consolidated tape for equitiesand – from 2019 – non-equities

• Extension of Transaction reporting

Commodities TransparancyMarket Structure

88© Oliver Wyman

…and what else?

• Some big changes, many small changes

• Conflicts of interest, includinginducements and remuneration

• Best execution

• Safe guarding client assets

• Product governance: manufacture and distribution

• Information for and reporting toclients

• Suitability, appropriateness and independent advice

• New trading venue category: Orginized Trading Facility (OTF)

• Systematic internaliser categoryextended to non-equities, including commodities

• Mandatory trading of liquid, clearable derivatives on orginazed venues

• New rules for venues and CCPs, recognition of non-EU venues

• Harmonized EU regime for access to trading venues, CCPsand indexes

• Controls on algoritmic/highfrequency trading

• Some harmonization of MemberState access requirements

• Retail and profesional clients: MS may require branch or applyexisting national rules

• Per se profesional clients and ECPs: harmonized third country equivalence regime for cross border services

• Register + TC equivalence + TC reciprocity + TC MoU

Conduct Third country firms’ accessSupervision and Enforcement

Swedish Energy Days

IMPLEMENTATION PROJECT

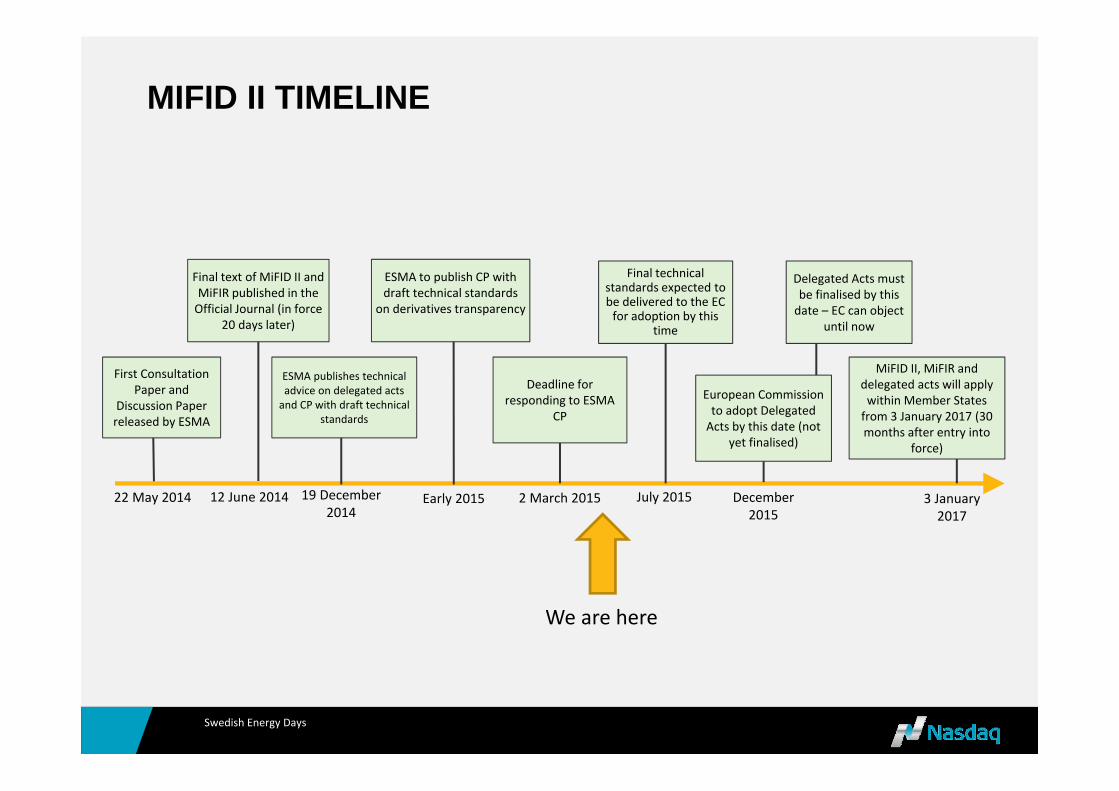

MIFID II TIMELINE

First Consultation Paper and

Discussion Paper released by ESMA

22 May 2014

Final text of MiFID II and MiFIR published in the Official Journal (in force

20 days later)

ESMA publishes technical advice on delegated acts and CP with draft technical

standards

ESMA to publish CP with draft technical standards

on derivatives transparency

Deadline for responding to ESMA

CP

European Commission to adopt Delegated Acts by this date (not

yet finalised)

MiFID II, MiFIR and delegated acts will apply within Member States from 3 January 2017 (30 months after entry into

force)

12 June 2014 19 December 2014

Early 2015 2 March 2015 December 2015

3 January 2017

Delegated Acts must be finalised by this date – EC can object

until now

Final technical standards expected to be delivered to the EC for adoption by this

time

July 2015

We are here

Swedish Energy Days

1111© Oliver Wyman

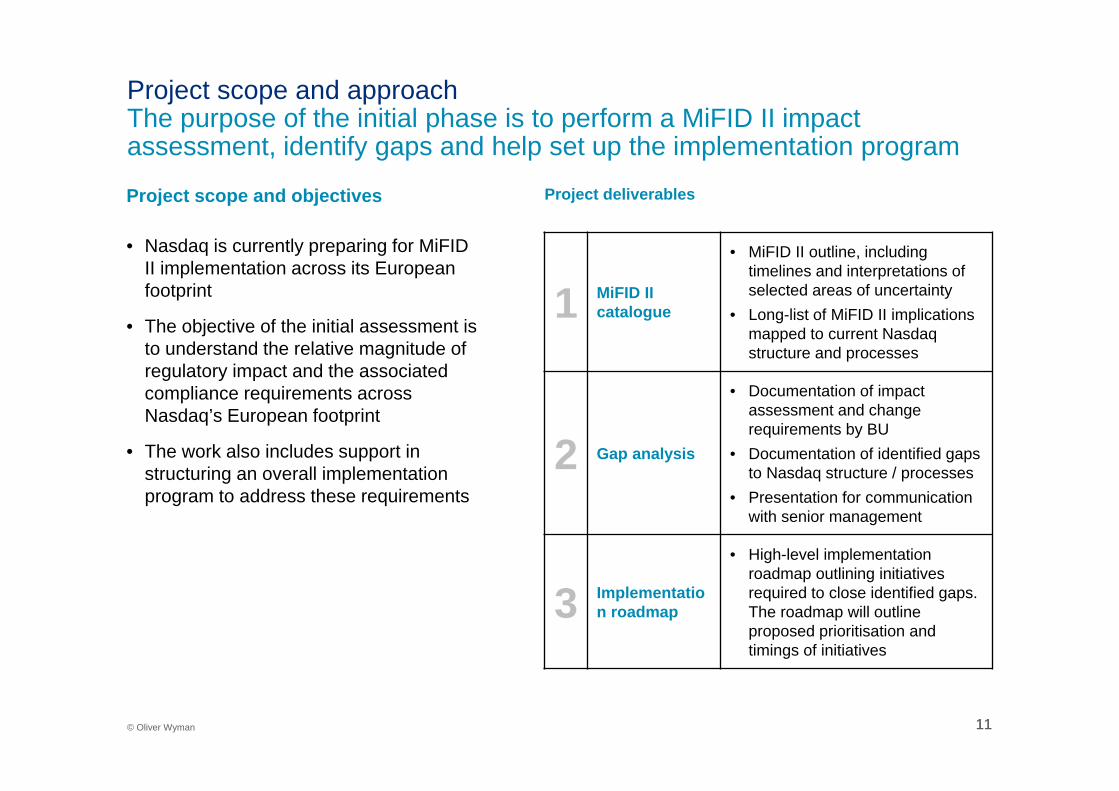

Project scope and approachThe purpose of the initial phase is to perform a MiFID II impact assessment, identify gaps and help set up the implementation program

1 MiFID II catalogue

• MiFID II outline, including timelines and interpretations of selected areas of uncertainty

• Long-list of MiFID II implications mapped to current Nasdaq structure and processes

2 Gap analysis

• Documentation of impact assessment and change requirements by BU

• Documentation of identified gaps to Nasdaq structure / processes

• Presentation for communication with senior management

3 Implementation roadmap

• High-level implementation roadmap outlining initiatives required to close identified gaps. The roadmap will outline proposed prioritisation and timings of initiatives

Project deliverablesProject scope and objectives

• Nasdaq is currently preparing for MiFID II implementation across its European footprint

• The objective of the initial assessment is to understand the relative magnitude of regulatory impact and the associated compliance requirements across Nasdaq’s European footprint

• The work also includes support in structuring an overall implementation program to address these requirements

Swedish Energy Days

MIFID II – IMPACT OVERVIEW

13© Oliver Wyman 13

Most gaps identified have simultaneous business, operations and control function implications hence stretching across the value chain (1/2)

MiFID II / MiFIR themes: Impact assessment

A. Fixed Income

B. Equity Derivatives

C. Commodities

D. Cash equities

E. Global Data Products / Index

F. Surveillance

G. Broker Services

H. Clearing

I. CCG Listing services

J. Regulatory compliance

K. Market Operations

L. Governance

Legend (impacted business units)

High impact; urgent action required

Medium impact; some action required

Minimal impact; no direct action required

Indirect impact; Stakeholder in process

High involvement in discussion required (natural owner) To be included in discussion for information

# Themes A B C D E F G H I J K L

1 Dark pool volume limits

2 Pre-trade and post trade transparency requirements for trading venues for equity instruments

3 Pre-trade and post-trade transparency requirements for non-equities

4 Obligation to make pre-trade and post-trade data available separately

5 Uphold market integrity and maintain records

6 Obligation to supply financial instrument reference data

7 Derivative trading obligation

8 Clearing Obligation for derivatives on regulated markets

9 Non-discriminatory access to a CCP

10 Non-discriminatory access to a trading venue

11 Non-discriminatory access to and obligation to licence benchmarks

12 Portfolio compression

13 Synchronisation of business clocks

14 Application for data service authorisation

15 Data reporting services organisational requirements (APA & CTP)

16 Data reporting services organisational requirements (ARM)

1414© Oliver Wyman

MiFID II / MiFIR themes: Impact assessment Legend (impacted business units)

High impact; urgent action required

Medium impact; some action required

Minimal impact; no direct action required

Indirect impact; Stakeholder in process

High involvement in discussion required (natural owner) To be included in discussion for information

# Themes A B C D E F G H I J K L

17 MTF and OTF operating requirements1

18 Possible introduction of an organised trading facility (OTF)

19 Admission and suspension rules for financial instruments on a regulated market

20 Admission of access to regulated markets

21 Investment firms, algorithmic trading

22 SME Growth market

23 Systems resilience , market maker agreements, circuit breakers, etc.

24 Tick sizes

25 Commodity derivative positions

26 Data requirements on TVs resulting from Best Execution

27 Authorisation of regulated market

28 Organisation of regulated markets

29 Reporting of infringements

30 Increased requirements for investment firms (implications on Broker Services)

A. Fixed Income

B. Equity Derivatives

C. Commodities

D. Cash equities

E. Global Data Products / Index

F. Surveillance

G. Broker Services

H. Clearing

I. CCG Listing services

J. Regulatory compliance

K. Market Operations

L. Governance

Most gaps identified have simultaneous business, operations and control function implications hence stretching across the value chain (2/2)

1 No additional requirements as part of this theme – impact is covered as part of other themes that apply to RMs

1515© Oliver Wyman 0

Low work load(Existing resources to devote part of their time)

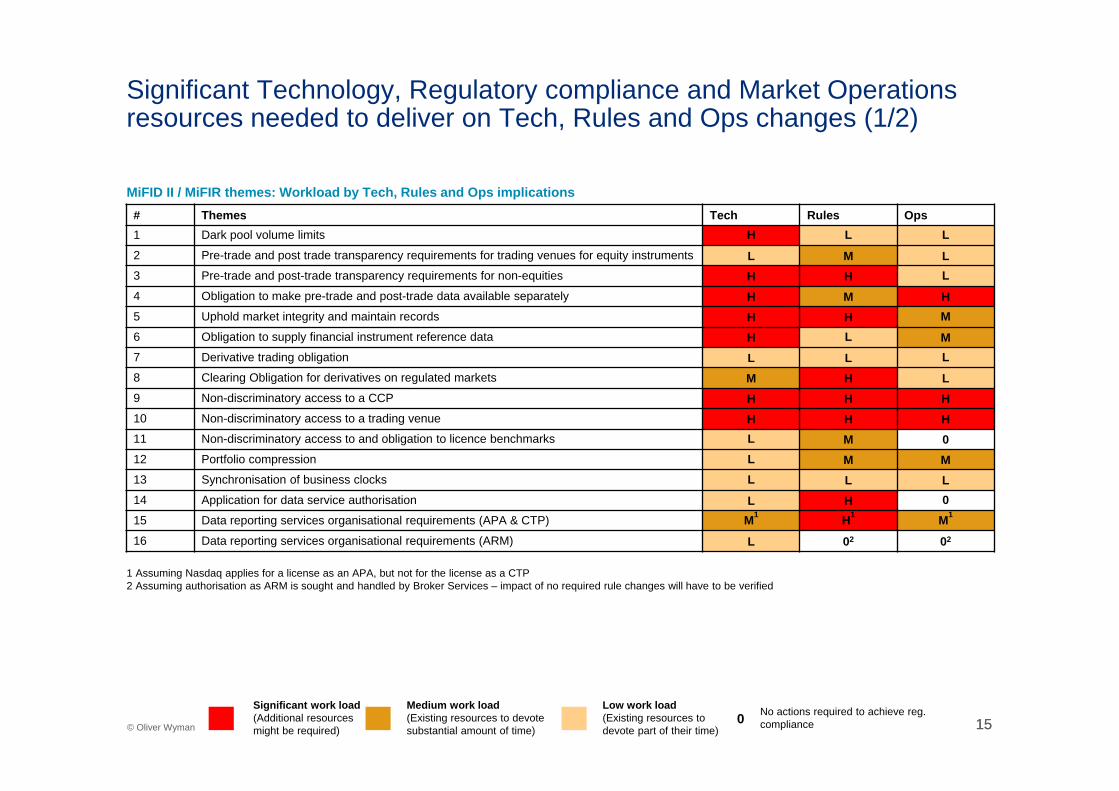

Significant Technology, Regulatory compliance and Market Operations resources needed to deliver on Tech, Rules and Ops changes (1/2)

Significant work load(Additional resourcesmight be required)

Medium work load(Existing resources to devotesubstantial amount of time)

MiFID II / MiFIR themes: Workload by Tech, Rules and Ops implications# Themes Tech Rules Ops1 Dark pool volume limits H L L2 Pre-trade and post trade transparency requirements for trading venues for equity instruments L M L3 Pre-trade and post-trade transparency requirements for non-equities H H L4 Obligation to make pre-trade and post-trade data available separately H M H5 Uphold market integrity and maintain records H H M6 Obligation to supply financial instrument reference data H L M7 Derivative trading obligation L L L8 Clearing Obligation for derivatives on regulated markets M H L9 Non-discriminatory access to a CCP H H H10 Non-discriminatory access to a trading venue H H H11 Non-discriminatory access to and obligation to licence benchmarks L M 012 Portfolio compression L M M13 Synchronisation of business clocks L L L14 Application for data service authorisation L H 015 Data reporting services organisational requirements (APA & CTP) M1 H1 M1

16 Data reporting services organisational requirements (ARM) L 02 02

No actions required to achieve reg.compliance

1 Assuming Nasdaq applies for a license as an APA, but not for the license as a CTP2 Assuming authorisation as ARM is sought and handled by Broker Services – impact of no required rule changes will have to be verified

1616© Oliver Wyman 0

Low work load(Existing resources to devote part of their time)

Significant Technology, Regulatory compliance and Market Operations resources needed to deliver on Tech, Rules and Ops changes (2/2)

Significant work load(Additional resourcesmight be required)

Medium work load(Existing resources to devotesubstantial amount of time)

MiFID II / MiFIR themes: Workload by Tech, Rules and Ops implications

No actions required to achieve reg.compliance

# Themes Tech Rules Ops17 MTF and OTF operating requirements 01 01 01

18 Possible introduction of an organised trading facility (OTF) M2 H2 H2

19 Admission and suspension rules for financial instruments on a regulated market L M L20 Admission of access to regulated markets M M M21 Investment firms, algorithmic trading H M H22 SME Growth market 03 03 03

23 Systems resilience , market maker agreements, circuit breakers, etc. H H M24 Tick sizes L L L25 Commodity derivative positions H M H26 Data requirements on TVs resulting from Best Execution H 0 L27 Authorisation of regulated market L L 028 Organisation of regulated markets L M L29 Reporting of infringements L L 030 Increased requirements for investment firms (implications on Broker Services) H M 0

1 No additional requirements as part of this theme – impact is covered as part of other themes that apply to RMs2 Assuming Nasdaq introduces an OTF3 No changes required to Tech, Rules, Ops when Nasdaq decides to introduce a SME Growth market segment – impact of no required rule changes will have to be verified

MIFID II CATALOUGE AND GAP ANALYSIS

18© Oliver Wyman 18

Business requirements

Tasks Owner Tech: BAOrequired

Rules / Agreements

Ops: Policies / Process

Current compliance / Next steps

Impact on Members

Trading venues are obliged or have right to:1. Monitor

interest positions

2. Access information regarding size and purpose of position, beneficial etc.

3. Require persons to terminate/reduce positions, put liquidity into market etc.

4. Publish aggregate positions on a weekly basis

5. Provide regulator at least daily with complete positions held by all persons

Evaluate business opportunity to develop a technical solution for reporting of commodity positions

MarketTech

• No • No • No Next steps:• Market Technology to

assess whether this seen as a strategic opportunity

• High• Negative

impact for members due to extensivereporting requirements both to TV and CA

• Members will need to report positions to Alien Competent Authorities

Set up procedures in order to produce and make public weekly reports on aggregate positions held (ITS 31)

• Yes • Yes• Update

General terms for Commodities 10/11

• Yes. • Processes

that secure reporting is made duly

Next steps:• Evaluate whether to build

or buy solution for this. Baseline is to build as this should be relatively straightforward.

Set up procedures in order to produce and communicate to the FSAs and ESMA complete daily breakdown of the positions held by all members and participants (incl. their clients) (ITS 31)

• Yes • Yes• Update

General terms for Commodities 10/11

• Yes. • Processes

that secure reporting is made duly.

Next steps:• Evaluate whether to build

or buy solution for this. • Challenge in reporting

requested (time horizon spot month vs. future) not in line with Product structure

Set up a system to receive reports (incl. additionally required data) from participants or members

• Yes • Yes• Obliged to

ensure that CA required information is forwarded

• Yes• Processes

that secure reporting is made duly.

Next steps:• Evaluate whether to build

or buy solution for this. • Key challenge is that

Clearing does not have information on beneficiaryfor trades – need to be requested from members

Implementation complexity

3 monthsLow (<1 month) High (>6 months)

Input from business areas Business Support Control

Example: Commodity derivative positions (MiFID II – 57, 58, 69)25

Commodities

19© Oliver Wyman 19

Business requirements

Tasks Owner Tech: BAO required Rules / Agreements Ops: Policies / Process

Current compliance / Next steps

See previous page Implement classification system of persons holding positions

• Yes• Changes to

Genium INET: CDB/CL

• Yes• Requirements on

members to maintain and share information on beneficiaries with TV and regulator (General terms 10/11)

Next Steps• BAO in process,

dependency on RTS/ESMA guidance on Beneficial Onwer

• Assess which functionalities from US system solutions could be leveraged

Position management controls to be applied in connection to applicable position limits that are introduced, in line with RTS 29 (e.g. access information about size and purpose of a position, or reduce or liquidate positions)

• Yes• Changes to

Genium INET: CDB, CL

• Yes• Monitoring rules,

powers etc. have to be established

Comments:• Meeting held with

NO FSA 07/May/15

• Concern about definition of deliverable supply, challenge for cash settled contracts

Next steps• Further action

requires guidancefrom NOFSA/ESMA

Commodity derivative positions (MiFID II – 57, 58, 69)25

Swedish Energy Days

IMPLEMENTATION ROADMAP

2121© Oliver Wyman

Initiative overviewPosition limits and reporting & Credit limits

6C

Business unit impact heatmap Tech Rules

Trading venues

- Cash equities INet NMR

- Equity derivatives

- Fixed income

- Commodities

- NLX

- Iceland

- Baltics

Clearing

CCG – Listing Services

Broker services Wizer

Global Data Products GCF

Index

Support impact heatmap

Global Access Serv Mgmt

Market Operations

Governance

Control impact heatmap

Regulatory compliance

Surveillance Smarts

H High impact; urgent action required M Medium impact;

some action required L Minimal impact; no direct action required I Indirect impact;

Cooperation required

Description

• The operational side of position reporting and limits is very unclear, because it covers also the OTC market

Position limits:• Position management controls to be applied by market operators in connection to

applicable position limits that are introduced, in line with RTS 29 (e.g. access information about size and purpose of a position, or reduce or liquidate positions)

Position Reporting: • Trading venues need to make public weekly reports and report daily to the FSAs, which

poses larger reporting requirements on the venue and on its members

Process requirements to be clarified

• Definition of financial instruments to be included• What type of products to be considered as part of regulation • Need to clarify regulatory requirements of how implementation of position limits is

envisaged in practice• Unclear how Nasdaq can ensure confidentiality in the reporting chain. Verify whether

Nasdaq has to develop products and services related to position reporting• Some definitions from the Level 1 text still need to be clarified, such as economically

equivalent and deliverable supply

Key challenges

• Ensure alignment and common approach to topic between BUs for changes to systems, rules and processes

• Overall there is large uncertainties around how the requirements should be implemented

• If reporting is required on very small markets with few players, these markets may entirely disappear

• Position limit reporting will be a large operational burden

Work-steam details

• Lead: Stefan Wilhelms• Team: Patrik Westerberg + local general counsel in DK, NO, SWE, FIN• Status: Initial assessment done in connection to Nasdaq reply to the ESMA

Consultations• External dependencies: -

GeniumInet

Deriv. exch.rules/

COM rules

2222© Oliver Wyman

2015 2016 2017

Implement changes to Genium Inet (CDB, CL etc.), SMARTS and PRM

Change Genium INET, CDB & CLImplement classification system of persons holding positions

Member readiness activitiesCross-BU alignment

NTMS MT decisionStrategic decisionBAO v2.0 completed

Position management controls to be applied in connection to applicable position limits that are Introduced (in line with RTS 29)

Market Technology to assess whether this seen as a strategic opportunity

Build or buy reporting solution

Task

Implement rule changesRequire members to maintain and

share information on beneficiaries with TV and regulator

Evaluate business opportunity to develop a technical solution for reporting of commodity positions

1. Update market model for COM2. Add new section in General terms 3. Establish monitoring rules

Evaluation of changes necessary Ops changes Rules changesTech changes Communication

to members Go Live Market Operations: milestones

Implementation roadmapPosition & Credit & Reporting Limits

3FPotentially running out-of-time in case position management controls can only be started once

classification of members has been fully implemented

Preliminary hypothesis

APPENDIXES

DEFINITION OF FINANCIAL INSTRUMENTS – REMIT CARVE OUTAnnex I Section C (6) defines commodity derivatives as “Options, futures, swaps, and any other derivative contract relating to commodities that can be physically settled provided that they are traded on a regulated market, a MTF, or an OTF, except for wholesale energy products traded on an OTF that must be physically settled;”

Recital 10 of requires that the limitation of scope should be ‘limited to avoid a loophole which may lead to regulatory arbitrage’

To secure a uniform interpretation across the Union: Requirement to have proportionate arrangements to make or take the delivery of

gas or power, (point 1. i ESMA’s Technical Advice, p 406.) quantitative measurement of the participants’ physical arrangement commodity‐by‐commodity basis accounts with TSOs and possibly also notification to the TSOs Clarify delivery capacity in each area as requirement

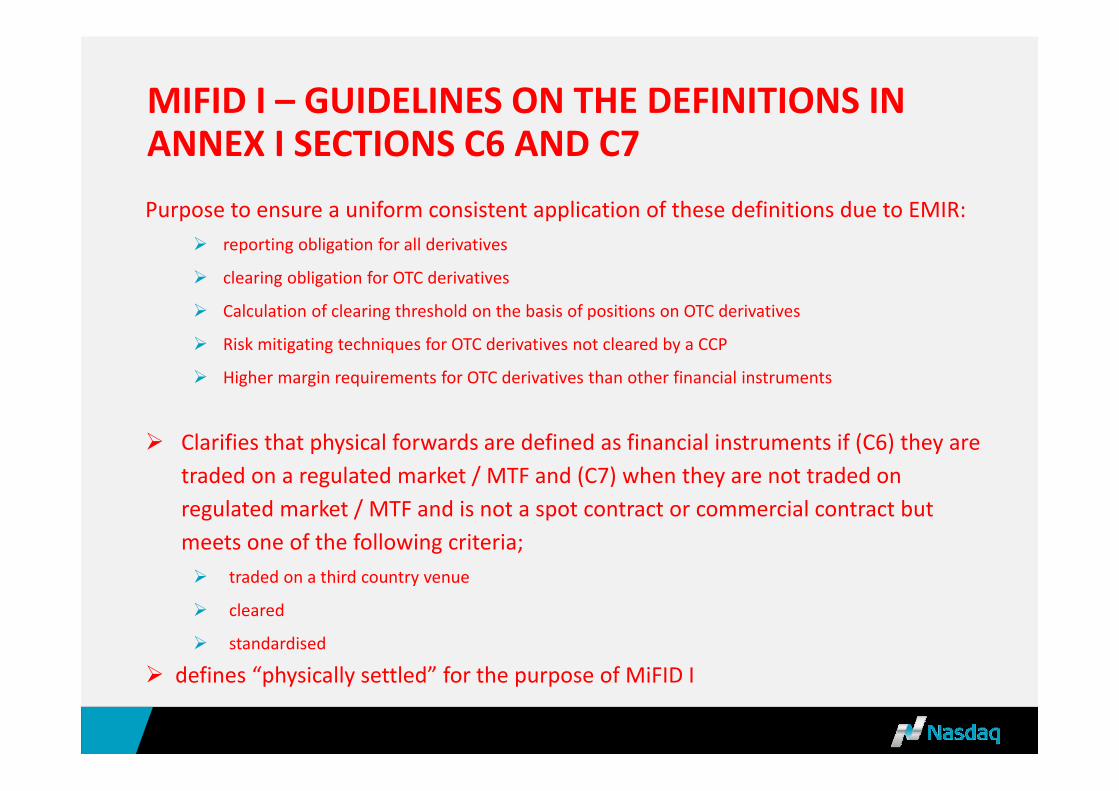

MIFID I – GUIDELINES ON THE DEFINITIONS IN ANNEX I SECTIONS C6 AND C7Purpose to ensure a uniform consistent application of these definitions due to EMIR:

reporting obligation for all derivatives

clearing obligation for OTC derivatives

Calculation of clearing threshold on the basis of positions on OTC derivatives

Risk mitigating techniques for OTC derivatives not cleared by a CCP

Higher margin requirements for OTC derivatives than other financial instruments

Clarifies that physical forwards are defined as financial instruments if (C6) they are traded on a regulated market / MTF and (C7) when they are not traded on regulated market / MTF and is not a spot contract or commercial contract but meets one of the following criteria; traded on a third country venue

cleared

standardised

defines “physically settled” for the purpose of MiFID I

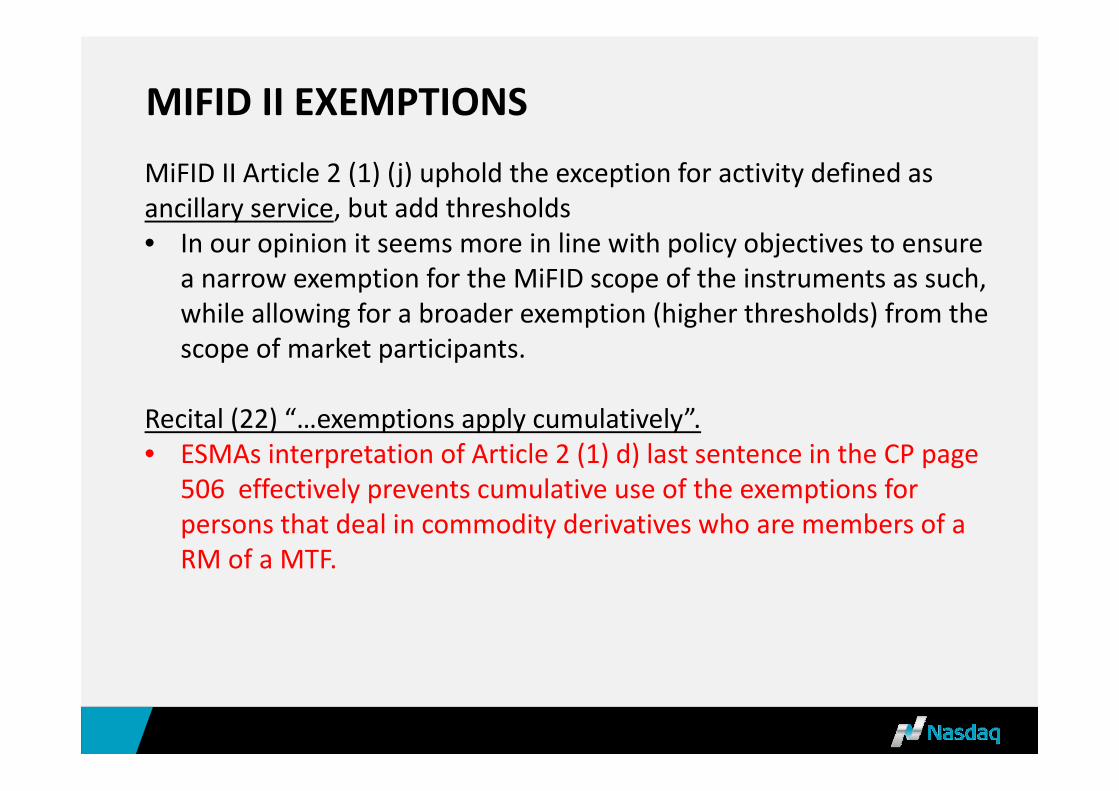

MIFID II EXEMPTIONS

MiFID II Article 2 (1) (j) uphold the exception for activity defined as ancillary service, but add thresholds• In our opinion it seems more in line with policy objectives to ensure

a narrow exemption for the MiFID scope of the instruments as such, while allowing for a broader exemption (higher thresholds) from the scope of market participants.

Recital (22) “…exemptions apply cumulatively”. • ESMAs interpretation of Article 2 (1) d) last sentence in the CP page

506 effectively prevents cumulative use of the exemptions for persons that deal in commodity derivatives who are members of a RM of a MTF.

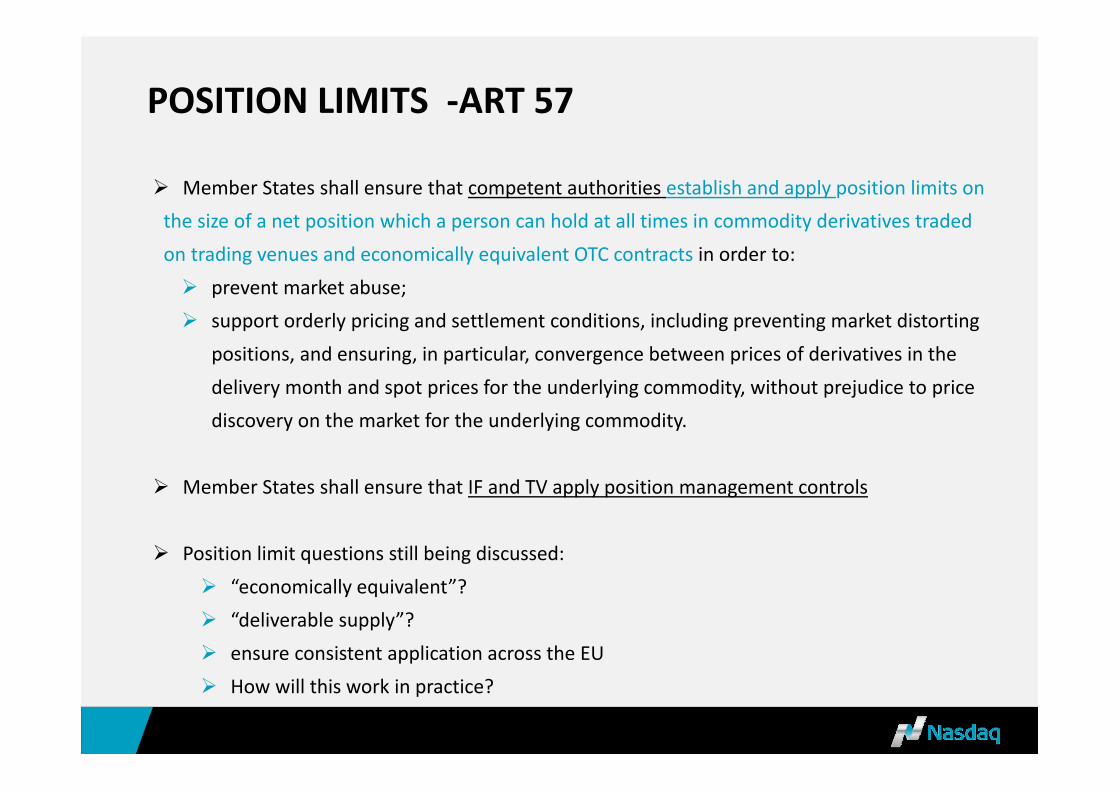

POSITION LIMITS ‐ART 57

Member States shall ensure that competent authorities establish and apply position limits on the size of a net position which a person can hold at all times in commodity derivatives traded on trading venues and economically equivalent OTC contracts in order to: prevent market abuse; support orderly pricing and settlement conditions, including preventing market distorting

positions, and ensuring, in particular, convergence between prices of derivatives in the delivery month and spot prices for the underlying commodity, without prejudice to price discovery on the market for the underlying commodity.

Member States shall ensure that IF and TV apply position management controls

Position limit questions still being discussed: “economically equivalent”? “deliverable supply”? ensure consistent application across the EU How will this work in practice?

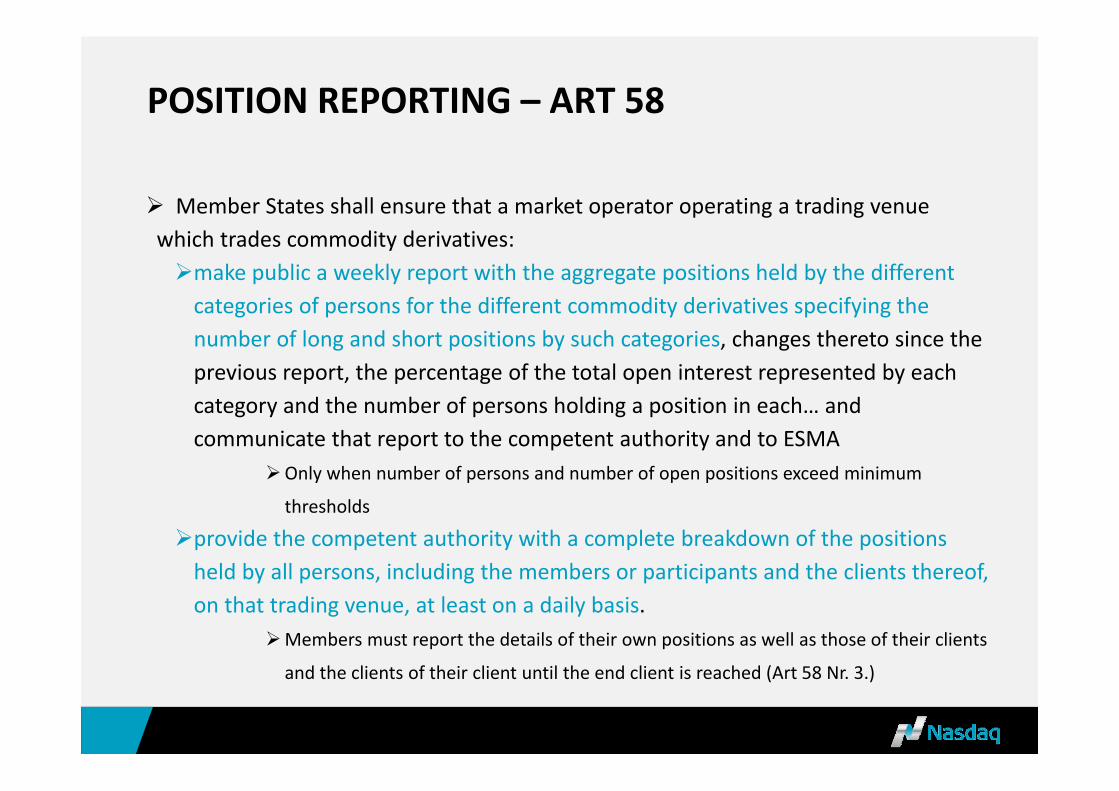

POSITION REPORTING – ART 58

Member States shall ensure that a market operator operating a trading venue which trades commodity derivatives:make public a weekly report with the aggregate positions held by the different categories of persons for the different commodity derivatives specifying the number of long and short positions by such categories, changes thereto since the previous report, the percentage of the total open interest represented by each category and the number of persons holding a position in each… and communicate that report to the competent authority and to ESMA

Only when number of persons and number of open positions exceed minimum

thresholds

provide the competent authority with a complete breakdown of the positions held by all persons, including the members or participants and the clients thereof, on that trading venue, at least on a daily basis.

Members must report the details of their own positions as well as those of their clients

and the clients of their client until the end client is reached (Art 58 Nr. 3.)

MIFID IIPOST‐TRADE ISSUES

TOPICS DIRECTLY RELATING TO CLEARING

Post‐trade/STP Indirect Clearing Open Access

POST‐TRADE/STP Certainty of clearing

• Pre‐trade checks: Member should provide client limits to trading venue, which should perform pre‐trade checks, within 60 seconds of receiving order (ETD), or 10 minutes (other).

– Possible changes in final regulation. Industry has proposed removal for ETD.

Timeframe for submission to the CCP• Trade should be submitted to CCP within 10 seconds of execution (ETD), within 10 minutes (non‐

electronic TV, within 30 minutes (bilateral). – Support different timeframes for different types of transactions.

Timeframe for clearing member acceptance• Member’s RM to review transaction before clearing. CCP should provide member with info on

bilateral transactions, within 60 seconds from CCP receiving info. – OK, already provide info.

Timeframe for CCP acceptance• CCP should accept/reject trades within 10 seconds from submission or from receipt of clearing

member acceptance.– OK for ETD– For OTC, we propose that pre‐novation/”pending” state is allowed– We are preparing for removal of ”pending” state

INDIRECT CLEARING

CCP requirements• Must be able to hold separate accounts for client’s house business vs omnibus accounts for indirect

clients – OK

• If the indirect client selects a gross omnibus account, the CCP must be able to calculate margin requirements separately for each indirect client

– OK• CCP must also be able to hold collateral values for each indirect client

– We are preparing to make changes to provide this

Potential market impact• Indirect clearing is frequent in ETD market, but without MiFIR rules/protection• Will impose a lot of change to current practice• In ETD, there are long chains of indirect clearing, MiFIR in practice only allows 4 levels. Will result in

indirect clients being forced out of current structures.• Unclear how MiFIR would prevail over national insolvency law and assets would not be held up, but

this is primarily of concern for the clearing members• Questions around third country provisions

Position of Nasdaq Clearing• Nasdaq Clearing relatively well positioned to handle indirect clearing• Concern that gross omnibus model will be expensive to implement but is unlikely to be used

Member Indirect clientClientCCP

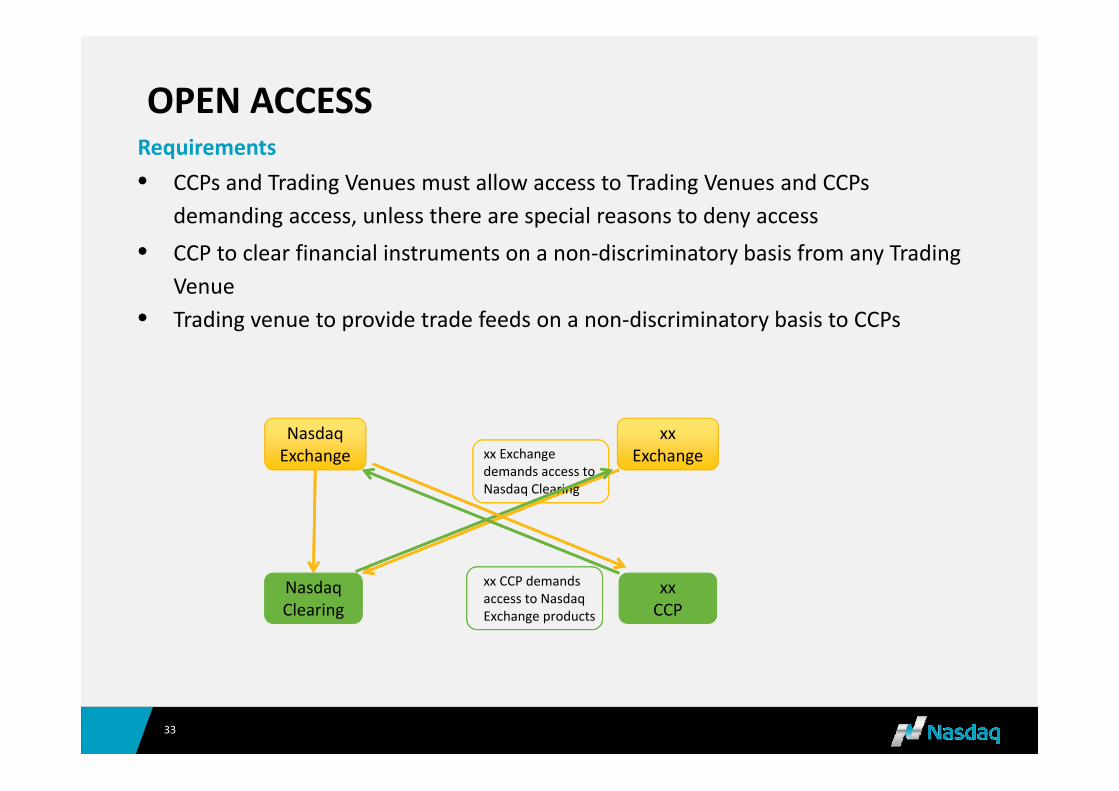

OPEN ACCESS

33

• CCPs and Trading Venues must allow access to Trading Venues and CCPs demanding access, unless there are special reasons to deny access

Requirements

Nasdaq Exchange

Nasdaq Clearing

xxExchange

xx CCP

xx Exchange demands access toNasdaq Clearing

xx CCP demandsaccess to Nasdaq Exchange products

• CCP to clear financial instruments on a non‐discriminatory basis from any Trading Venue

• Trading venue to provide trade feeds on a non‐discriminatory basis to CCPs

OPEN ACCESS Contents of proposal

• Reasons for CCP to deny access• Reasons for TV to deny access• Competent authority can deny access, in certain cases• Fees charged by TVs and CCPs• Non‐discriminatory treatment of contracts• Transitional provisions

Nasdaq Clearing’s position on Open Access• Nasdaq Group is pro Access• Increased competition will lead to customer value through:

– Technical innovation– Lower costs– Greater choices

• Proposal has some room for denying access