Embed Size (px)

Citation preview

MID Webinar Business Models

November 11, 2008

Moderated by Jim McGregor Principal Analyst and Research DirectorIn-Stat

Introduction• Welcome to the Mobile Internet Device (MID) webinar

series featuring:– MID Market Overview – 6/26/08– MID Hardware Architectures – 8/7/08– MID Software Architectures – 9/24/08– MID Business Models – 11/12/08

• Today’s host:– Jim McGregor, Principal Analyst & Research Director, In-Stat

• Agenda– 5-minute overview – 30-minute discussion by panelists – 45-minute live Q&A

• Archive of webinar available at:– www.ti.com– www.instat.com

Panelists• Seshu Madhavapeddy

– General Manager, Mobile Internet Device Business Unit, Texas Instruments– Joined TI in 2008– Former president, CEO and founder of various technology start-up companies– Guides TI’s MID business strategy, software and hardware platforms, strategic

partnerships and customer relationships

• Mike Woodward– Vice President, Smart Devices, AT&T– Joined AT&T in 2001– Leads AT&T’s wireless data device strategy for business and consumer segments

including both stocked and non-stocked

• Bob Sullivan– President and CEO of Sullivan and Associates Consulting – 28 Years – Senior Broadcast Management Positions Including:

• Vice President, Gannett Television (CBS Division) Oversaw five, Gannett CBS TV Station• President and General Manager, WUSA-TV, the Gannett owned, flagship, CBS affiliate in

Washington, D.C.

Successful MIDs offer solutions

Smartphone WLAN/3G/ WiMAX/LTE…

Content & applications

Internet

Web 2.0

MusicVideo

Social networking

Ringtones

Internet

NavigationNews & information

Devices Services

Software

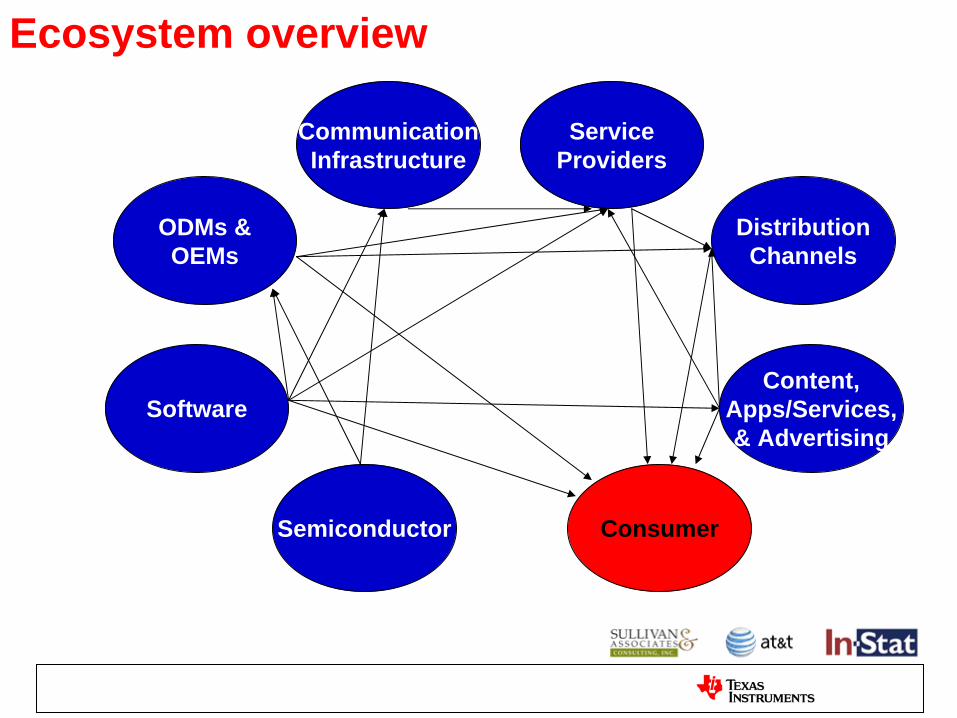

Ecosystem overview

Semiconductor

ODMs &OEMs

Software

ServiceProviders

DistributionChannels

Content,Apps/Services,& Advertising

Consumer

CommunicationInfrastructure

Ecosystem overview

Semiconductor

ODMs &OEMs

Software

ServiceProviders

DistributionChannels

Content,Apps/Services,& Advertising

Consumer

CommunicationInfrastructure

Mix of business models

Existing• Subsidized devices• Minute-by-minute/bit-by-bit• Service tied to device• Multiple services• Closed platforms/one point

of contact

Emerging• Subsidized services• All you can get• Service tied to customer• Multiple devices• Open platforms/multiple

points of contact• Single log-on• Ad revenue sharing• Content revenue sharing• Service/application

revenue sharing

Business model requirements

• Support technology innovation• Support growth for the entire ecosystem• Support investment in new communications

infrastructure• Support enhanced services, content, and

applications for consumers• Must meet consumers’ growing and varying

expectations• Must reduce strain on discretionary income to

support continued growth

Technology Provider PerspectiveSeshu Madhavapeddy General Manager, Mobile Internet Device Business UnitTexas Instruments

Consumer expectations for MID performance

Base Line Requirements:• Full web browsing• High resolution display• Wireless broadband• All day power• True portability• Intuitive UI

TI Delivers:• Complete hardware and software

reference platform for MIDs• OMAP™ 3 processor provides laptop-like

performance at low power

Opportunities• Build ongoing relationship with

customers• Create new revenue streams for

applications and services

• No-compromise internet browsing• HD video & music player• Ultimate TV & radio experience• Games, e-mail, photo viewer, widgets• Media Club – movie purchase

• 4.8” WVGA• Touch• WLAN• HSDPA• 60 GB Hard Drive• 13 mm thickness

ARCHOS 5

It’s about delivering content and services

Content & services delivery platform

Music

Video

Social networking

Gaming

Movies

MapsNews & information

Widgets

Content & Services Client

User Interface

Applications

Middleware

Kernel

Internet

OMAP™ 3MID H/W Platform

OMAP™ 3MID H/W Platform

Engaging with ARCHOS Media Club

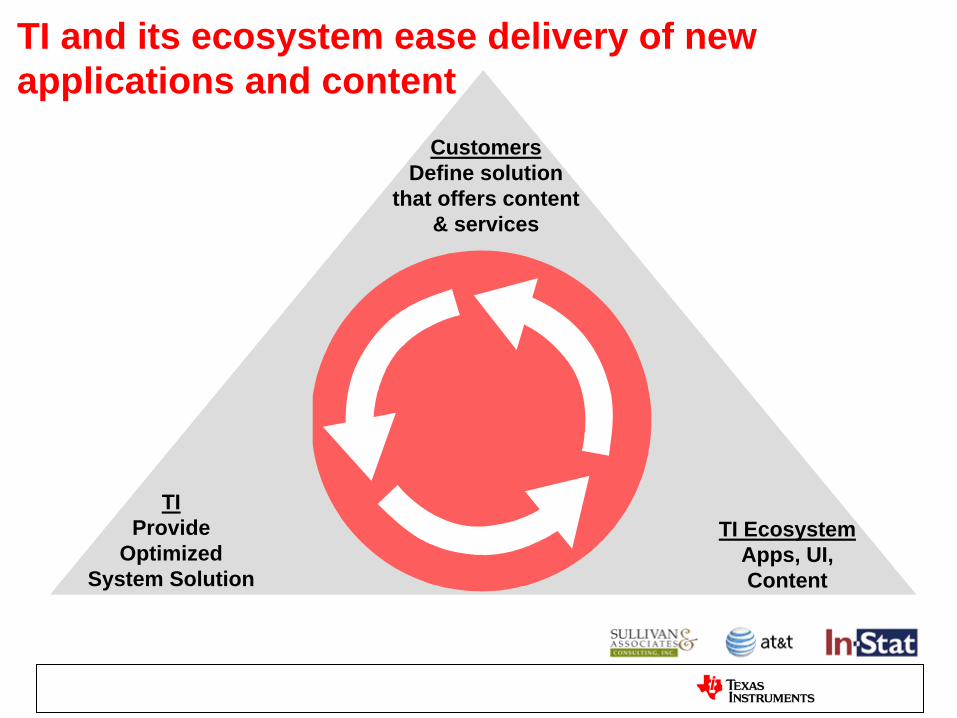

TI and its ecosystem ease delivery of new applications and content

TIProvide

Optimized System Solution

TI Ecosystem Apps, UI, Content

CustomersDefine solution

that offers content & services

Service Provider Perspective

Mike WoodwardVice President of Smart DevicesAT&T

Overview

• Existing smartphone model is thriving• Mobile broadband is becoming ubiquitous• MIDs offer a compelling opportunity• Ecosystem value chain / revenue sources• MID business model considerations

Existing smartphone model is thriving

• Business email drove early smartphone adoption

• Processing power, battery life, screen size, keyboard usability have converged for great devices

• Now 3G handsets combine with rich browsers and apps to deliver compelling handheld experience

• Business model: – Incoming: data plan revenue– Outgoing: device subsidy to customers

SUBSIDIZED

Device Evolution

Mobile Broadband is becoming ubiquitous

• Network and device speed and performance have reached critical mass to grow the market

• 3G is a household name

• “Built-in” mobile broadband laptops has been a slow starter but is gaining momentum

• Business model: – Incoming: data plan revenue– Outgoing: either commission to PC-

OEMs (embedded) or Subsidy (cards)

Worldwide WWAN by device

0

5

10

15

20

25

30

2006 2007 2008 2009 2010 2011

Ship

men

ts (M

illio

ns)

External Cards

Internal Modems

USB Modems

Future Roadmap

10 Mbps

1 Mbps

100 Mbps

2006

3.6

07-08

7.2

08-09

14.4

2009+

80

>2010

200

2005

1.8

HSDPA HSUPA HSPA+ LTE

COMMISSIONED

Source: IDC

MIDs offer a compelling opportunity• Rich browsing, open access and new embedded form factors

are combining to create the new MID category

Feature Phone

Smartphone

MID

Netbook

Premium Notebook

Porta

bilit

y

Functionality

COMMISSIONED

SUBSIDIZED

Ecosystem value chain / revenue sources

Chipset / OS Devices CarrierDistribution

Customers

Hardware sales and OS licenses

Hardware sales Service fees, activation bounties,

equipment margin

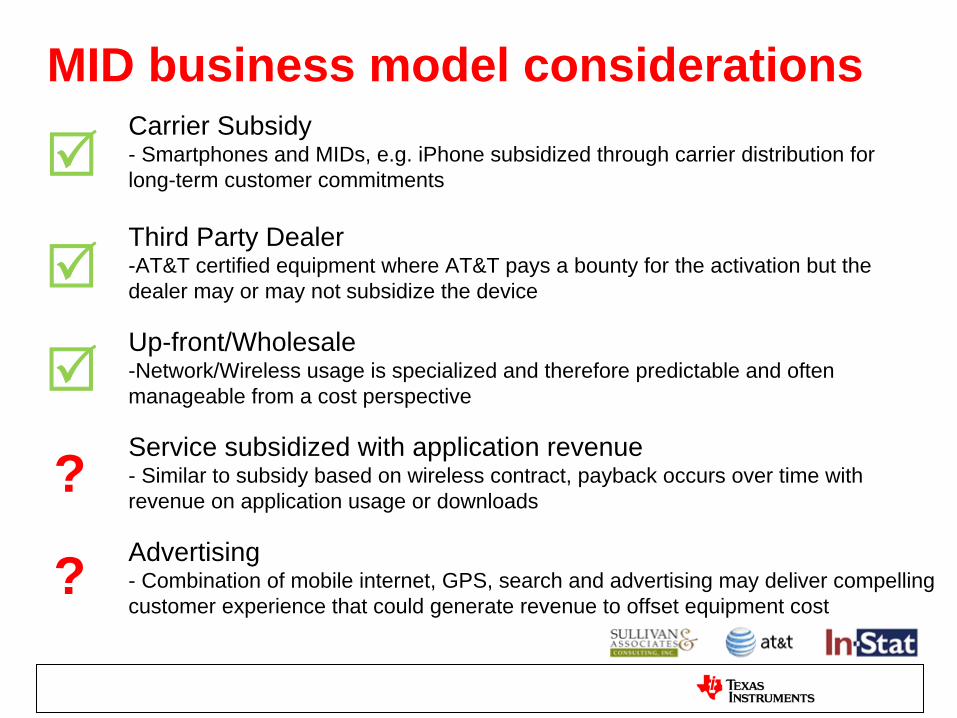

MID business model considerations

Up-front/Wholesale-Network/Wireless usage is specialized and therefore predictable and often manageable from a cost perspective

Service subsidized with application revenue- Similar to subsidy based on wireless contract, payback occurs over time with revenue on application usage or downloads

Advertising- Combination of mobile internet, GPS, search and advertising may deliver compelling customer experience that could generate revenue to offset equipment cost

Carrier Subsidy- Smartphones and MIDs, e.g. iPhone subsidized through carrier distribution for long-term customer commitments

Third Party Dealer -AT&T certified equipment where AT&T pays a bounty for the activation but the dealer may or may not subsidize the device

?

?

Moving and Selling Content

Bob SullivanPresident & CEOSullivan & Associates

“Pulse Check”• TV-still dominant: 2008*

-TV viewing: 389 billion viewing hours -Online viewing: 800 million viewing hours

• 1/3 of all household Internet activity happens while also watching TV+– Growing paradox: rising TV viewership and growing

popularity of new media

• TV viewership: 127 hours per month• Internet usage: 26 hours per month

*Black Arrow (10-08’)+Nielsen (10-08’)

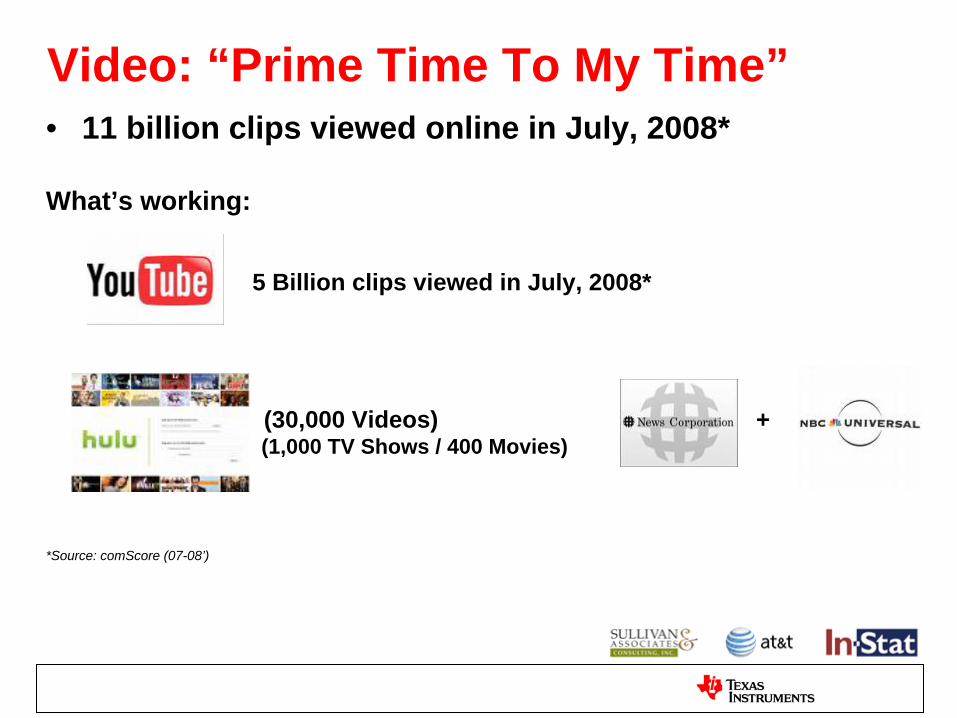

Video: “Prime Time To My Time”• 11 billion clips viewed online in July, 2008*

What’s working:

5 Billion clips viewed in July, 2008*

(30,000 Videos) +(1,000 TV Shows / 400 Movies)

*Source: comScore (07-08’)

New applications

• New: Just Announced

MTVMusic.com(22,000 Music Videos)

30 million profilesadding video / programs

New applications• NFL on cell phones: (last Thursday)

(Broncos vs. Browns)

• Feature movies:

• Videos: +

(Most frequently cited movie information web source ages 15-24*)

*Source: Nielsen

Video Internet TV

• New crop of special purpose devices:

+ 12,000 movies / shows on demand(Streamed by Netflix on Internet)

Trends• “Cable Cutters”

Video: “Prime Time To My Time”

Misses:• Titan media: closed summer 08’

• Break media / ManiaTV / Veoh: October layoffs

• Yahoo: 1,400 jobs cut: 2009

Local news• “Backpack journalists”• Multi-tasking staff:

-Reporters who shoot video-Photographers who report-Producers who edit-Assignment editors who write

• Newsrooms of the future• “Information centers”• Internet editorial staff hiring• Stand alone site development: HS football

Online advertising: Print - TV• Old model:

– Selling Internet as “value add”– Banner display ads

• New model: (not about transactions-about interactions)

– Stand alone web sales– Search / usage / behavioral targeting– Precision advertising – paying for results

(Decreasing sales employee bonuses for print only sales from 95% to 70% in 2009)

Online advertising: Print - TV• Total local advertising on the web 2008:

$12.9 billion (5 x more than 2004)

• Total revenue local newspaper sites-2008:$3.7 billion* (6.5 % of gross revenues (2011 estimate: 10% of gross revenues)

But:

44% of local Internet revenue in 200427% of local Internet revenue in 2008

• Total revenue local television sites-2008:$1.2 billion* (3 % of gross revenues)(2011 estimate: 6% of gross revenues)

*Source: Borrell Associates

Online advertising2009:

• “Like skeet shooting in the wind”*– Got the velocity and trajectory down pat– Gusts caused by credit crisis-hard to pinpoint the

target

Offline media: Down 1.4%Online media: Up 7.2% ($13.9b)

*Source: Borrell Associates

0

2

4

6

8

10

12

14

2007 2008 2009

Billions

Online advertising

Automotive:The 300 pound gorilla is losing weight

• September / October 08: sales down 30%• By year end: 700+ dealership closures• 2008 sales platforms

# 1: Television (# 1 in 2007)# 2: Internet (# 3 in 2007)# 3: Newspaper (# 2 in 2007)

Newspapers: Last call?• Current: Still most profitable media web sites

but…..Challenges up / revenues down

• Future: Will be surpassed by TV*• Since 2002:

-Overall web advertising: 40.5% compound annual growth rate-(Newspapers: same period: 33%)-(TV: same period: 67%)

• Layoffs / shrinkage

*Source: Borrell Associates

Online advertising

Keys to survive:• Skate to where the puck will be –Wayne Gretsky

• Go where your customers are going• Use their technologies to engage• Explore unique / creative “touch points”• Create new sales designs to stay connected• Monitor brand reputation constantly• Constantly scan on your competition

Summary

• The MID market– Has elements of existing markets– Is dynamic and changing rapidly

• The business model– No single business model– Likely to influence traditional markets and applications– Requires closer partnerships throughout the value

chain

Q & A

• To participate, click on the Ask a Question link on the left side of the interface; enter your question in the box on the screen; hit “Submit.” We’ll answer them during the Q&A session or after the webcast.

www.ti.com/midcommunity.ti.com/blogs/mobilemomentum

Contact information

Jim McGregorPrincipal Analyst & Research [email protected]

Seshu Madhavapeddy General ManagerMobile Internet Device Business UnitTexas [email protected]

Bob SullivanPresident & CEO Sullivan & [email protected]

Mike WoodwardVice President of Smart DevicesAT&[email protected]

SWPT033

![[Archived] Managing and Sharing 3D Models for Construction ...Webinar 1: Overview of 3D Models for Construction Webinar 2: Creating 3D Engineered Models Webinar 3: Applications of](https://img.dokumen.tips/doc/110x75/600cf621a56e8668ed30b854/archived-managing-and-sharing-3d-models-for-construction-webinar-1-overview.jpg)