Embed Size (px)

Citation preview

Melbourne Sydney Brisbane Wellington Johannesburg Cape Town Windhoek

Asset Management Frameworks with regard to Future Financial Planning –What a Municipal Officer Should Know

SAHA Information SessionIMFO 6 October 2009

1

INTRODUCTION

• Asset Management prescriptions for municipalities has increased rapidly since 1996.

• The guidelines are numerous and sometimes confusing as to their interaction.

• The purpose today is to provide - EVERY OFFICIAL’S GUIDE TO MUNICIPAL ASSET PLANNING.

• Not necessary give a technical discussion on the details of the latest asset management frameworks – but to provide you with a presentation to hand to all municipal officials that has interaction with municipal assets to explain their role in asset management planning for the financial cycle.

WHY THE EMPHASES ON ASSETS• Since 1996, municipalities’ service delivery

requirements increased drastically.• Municipalities are custodians of hundreds of billions of

Rand in public assets – these officials mostly non financial functionary officials.

• Challenge to address infrastructure backlogs, the expansion of capital works - also maintain or renew existing assets.

• Maintenance is critical as it will always cost more to replace an asset – asset management includes:– maintaining, renewing existing assets as well as providing access

to new assets and services in sustainable and affordable manner.

LEGISLATIVE & GUIDELINE FRAMEWORKNT issued a frightening array of documents:–Asset Management Framework–Local Government Capital Asset Management Guideline–The DPLG “Guidelines for Infrastructure Asset

Management in Local Government”–Sector specific guidelines on asset management in

certain sectoral assets:Verification and Valuation of Major Water Infrastructure Assets –Department of Water and Forestry Affairs (DWAF);International Infrastructure Management Manual co-authored by Institute of Municipal Engineering of Southern Africa IMESA; andNational Infrastructure Maintenance Strategy (NIMS) managed by Department of Public Works (DPW).

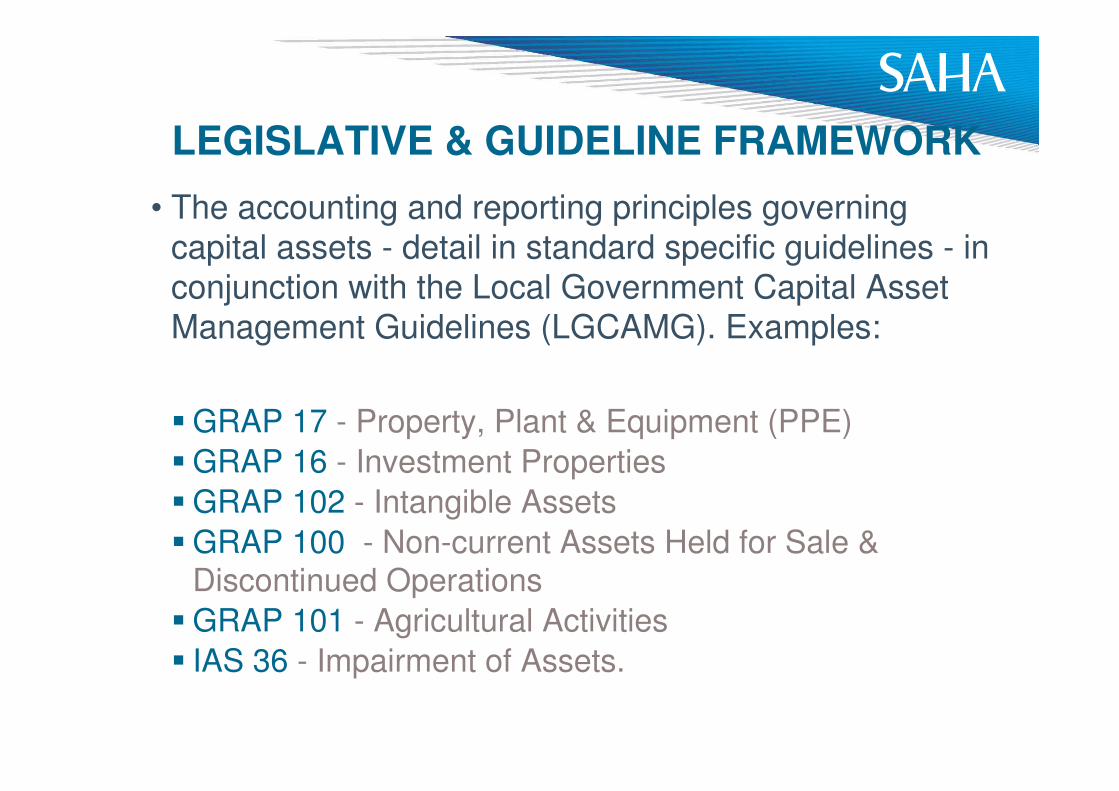

LEGISLATIVE & GUIDELINE FRAMEWORK

• The accounting and reporting principles governing capital assets - detail in standard specific guidelines - in conjunction with the Local Government Capital Asset Management Guidelines (LGCAMG). Examples:

� GRAP 17 - Property, Plant & Equipment (PPE)� GRAP 16 - Investment Properties� GRAP 102 - Intangible Assets� GRAP 100 - Non-current Assets Held for Sale &

Discontinued Operations� GRAP 101 - Agricultural Activities� IAS 36 - Impairment of Assets.

Asset Management – Legislative Framework

• The safeguarding, utilisation and disposal of assets are regulated by legislation (being direct or legislation that has an indirect impact).

• Some of the examples are-– Municipal Finance Management Act, 2003 (Act 56 of 2003), (sec

14, 90, 96 (responsibility directly linked to accounting officer);– Bylaws (sport facilities, libraries, heritage sites, markets, parks

etc – which deals with the management of immovable assets);– SCM for as far as that regulates the acquisition/leasing in or

out/disposal of assets both fixed and movable;– Sec 60 of the Municipal Systems Act, 2000 (Act 32 of 2000);– Municipal Asset Transfer Regulations.

BRINGING ASSET PLANNING HOME• Challenge is therefore to in crisp steps explain what

information, steps and or planning is necessary to:

–Know what assets a municipality have;–Know what the status of the assets are (value, kind,

what maintenance are required, future acquisitions necessary, assets that can be sold);

–Why this info is necessary for statutory budget requirements;

–How the info must be captured in the statutory framework;

–How planning are effected by the info.

ROLE PLAYERS - ASSET MANAGEMENT CHALLANGES

�Various role players in a municipality that deals on a daily basis with assets.

�The diversity of people / functionaries is a challenge in itself.

ASSET MANAGEMENT CHALLENGES- DIVERSE ROLE PLAYERS

• Non Management officials such as maintenance crew

ASSET MANAGEMENT CHALLENGES- DIVERSE ROLE PLAYERS

�The Line function manager directly responsible for the delivery of services by utilising the asset.

�The utilisation must be on par with the long term vision of the executive and the everyday realistic asset requirements from the base level maintenance official

ASSET MANAGEMENT CHALLENGES- DIVERSE ROLE PLAYERS

� The Accountants / CFO that is directly responsible for the correct financial recording of information associated with assets / technical recording of financial data

� This data must guide the line managers, executive to strategic financial planning regarding assets and provide for financial planning for the street level requirements of asset maintenance.

ASSET MANAGEMENT CHALLENGES- DIVERSE ROLE PLAYERS

�The Council that is responsible for executing the long term vision/policy of government regarding assets / final asset guardians

�Guided by the financial data, the line function requirements and what is the actual street level status of the various assets.

ASSET MANAGEMENT CHALLENGES- DIVERSE ROLE PLAYERS

ASSET MANAGEMENTHOLISTIC APPROACH

NECESSARY

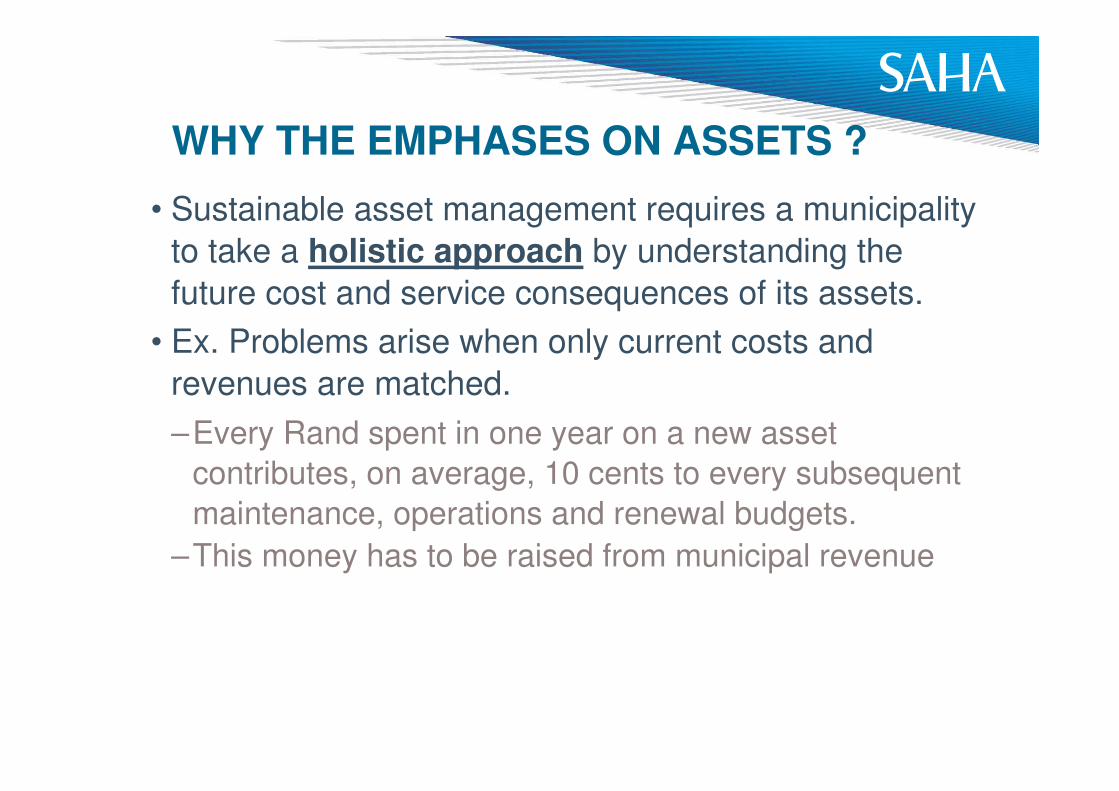

WHY THE EMPHASES ON ASSETS ?

• Sustainable asset management requires a municipality to take a holistic approach by understanding the future cost and service consequences of its assets.

• Ex. Problems arise when only current costs and revenues are matched. –Every Rand spent in one year on a new asset

contributes, on average, 10 cents to every subsequent maintenance, operations and renewal budgets.

–This money has to be raised from municipal revenue

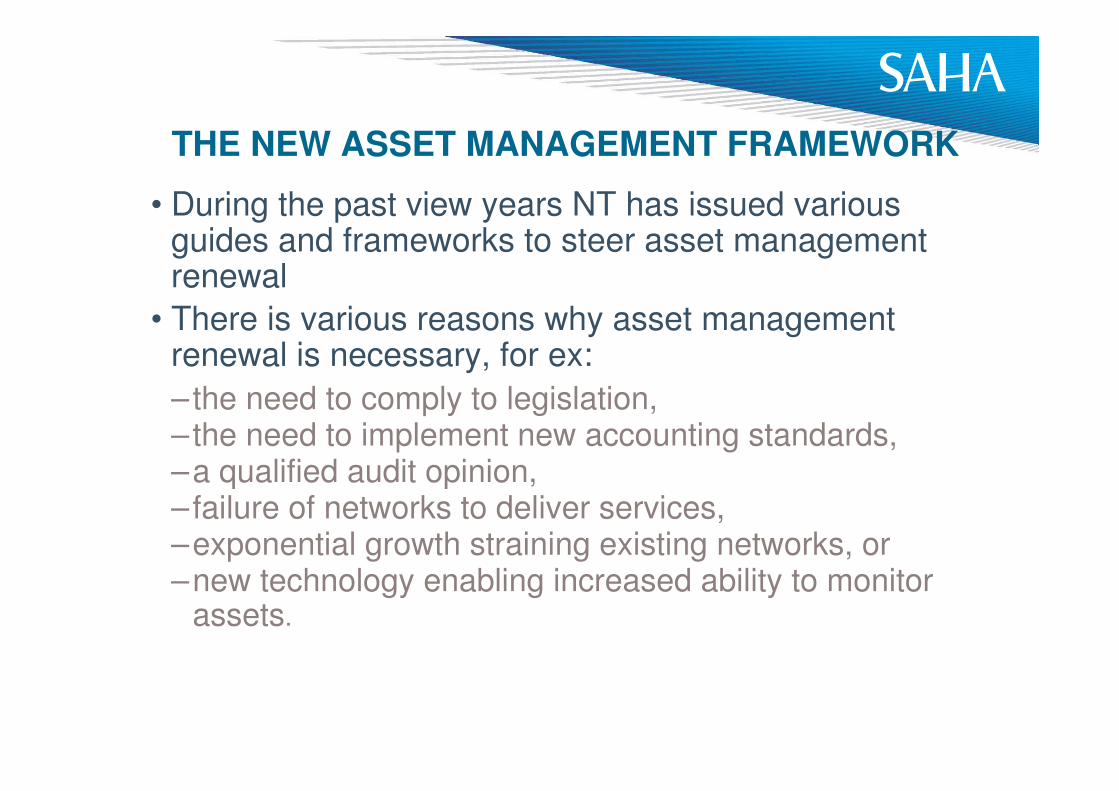

THE NEW ASSET MANAGEMENT FRAMEWORK

• During the past view years NT has issued various guides and frameworks to steer asset management renewal

• There is various reasons why asset management renewal is necessary, for ex:–the need to comply to legislation,–the need to implement new accounting standards,–a qualified audit opinion,–failure of networks to deliver services,–exponential growth straining existing networks, or–new technology enabling increased ability to monitor

assets.

THE NEW ASSET MANAGEMENT FRAMEWORK

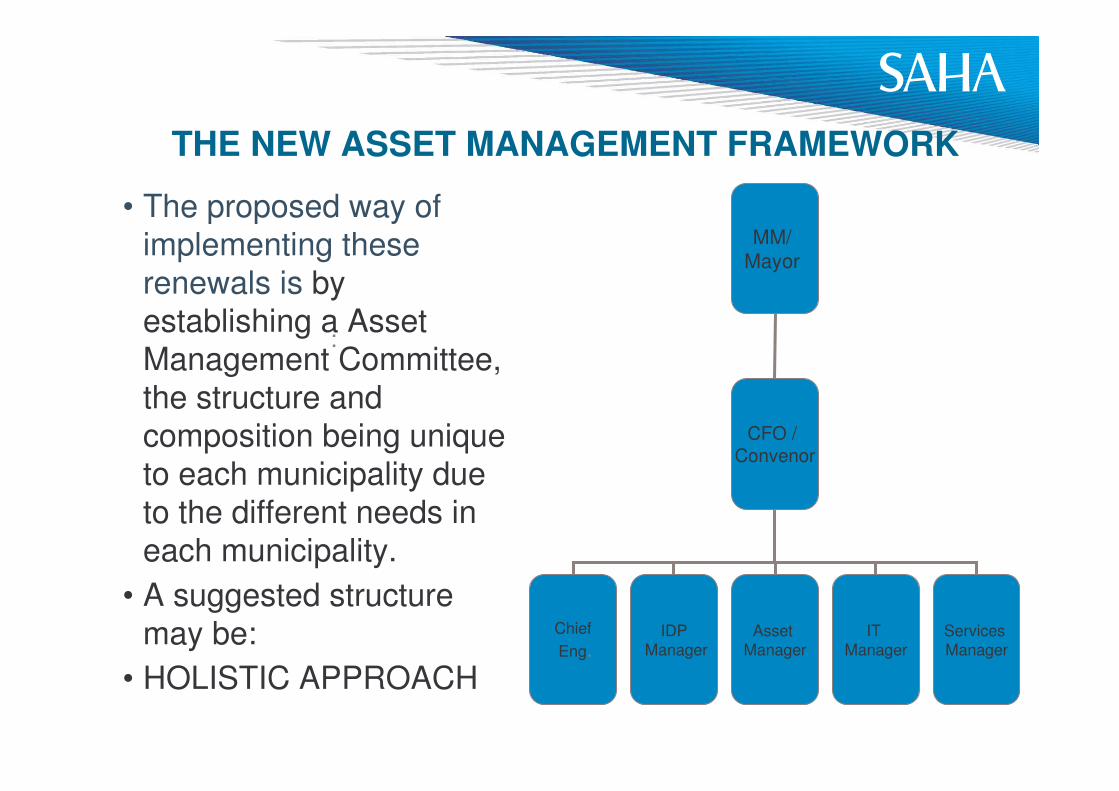

• The proposed way of implementing these renewals is by establishing a Asset Management Committee, the structure and composition being unique to each municipality due to the different needs in each municipality.

• A suggested structure may be:

• HOLISTIC APPROACH

:

MM/ Mayor

CFO / Convenor

ChiefEng.

IDPManager

Asset Manager

IT Manager

Services Manager

THE NEW ASSET MANAGEMENT FRAMEWORK

• Typically the following structure (with related functions) will support the Asset Management Steering Committee

:

Asset Management SteeringCommittee

Asset Management Project Team

Asset Management Task Teams

BASIC STEPS TO PRUDENT ASSET MANAGEMENT

Update Asset Registerand verify

IDP interaction

Develop a Financial Planfor Assets – incorporate in budget

Develop an Asset Management Policy / Strategy

Establish Required Levels ofService and Municipal Strategy

Identify existing Assets

ASSET MANAGEMENT CHALLENGES- REALISE AND POSITIVELY IDENTIFY ASSETS

• Before any budgetary planning can be effected regards assets, the assets must first be identified in order to know what must be managed.

• “Assets” are resources controlled by an entity as the result of past events and from which future economic benefits or potential service provision are expected to flow to the entity.

• Legally two kinds of assets:– Movable– Immovable / Fixed

ASSET MANAGEMENT CHALLENGES- REALISE AND POSITIVELY IDENTIFY ASSETS

• For financial asset management purposes and accounting standard purposes GAMAP 17 and GRAP 17 there are 5 main categories:

• Infrastructure assets – any asset that is part of a network of similar assets. It is specialized in nature, do not have an alternative use. It is immovable and may be subject to constraints on disposal.

– Examples are roads, water reticulation schemes, sewerage purification and trunk main, transport terminals and car parks.

ASSET MANAGEMENT CHALLENGES- REALISE AND POSITIVELY IDENTIFY ASSETS

• Community assets –are defined as any asset that contributes to the community’s wellbeing.

–Examples are parks, libraries and fire stations.

ASSET MANAGEMENT CHALLENGES- REALISE AND POSITIVELY IDENTIFY ASSETS

• Heritage assets –are defined as culturally significant resources.

–Examples are works of art, historical buildings and statues.

ASSET MANAGEMENT CHALLENGES- REALISE AND POSITIVELY IDENTIFY ASSETS

• Land and buildings – are defined as owner-occupied property held by the owner, or by the lessee under a finance lease, for use in the production or supply of goods and services or for administration purposes.

ASSET MANAGEMENT CHALLENGES- REALISE AND POSITIVELY IDENTIFY ASSETS

• Other assets – are defined as asset utilized in normal operations.

–Examples are plant and equipment, motor vehicles and furniture and fittings.

ASSET MANAGEMENT CHALLENGES- THE ASSET REGISTER

• Once we have identified the assets the assets must be recorded in an asset register.

• This is part of the control and safeguarding of assets.

• The MFMA (section 63) states specific duties in respect of asset management, i.e. the safeguarding and maintenance of assets, valuation in accordance with GRAP, maintaining a system of internal control over assets and keeping an asset register.

ASSET MANAGEMENT CHALLENGES- THE ASSET REGISTER

• Overall Responsibility of Municipal Manager• Must identify Asset Managers which maintain the

registers to help them with the actual management of their assets, line function managers actually responsible for the asset.

• The asset manager will require financial information to complete the asset register, some information may not initially be available

ASSET MANAGEMENT CHALLENGES- THE ASSET REGISTER

The Asset Register will include the information to assets such as:–The depreciation methods

used–The useful life–Depreciation charges

(current year)–The carrying amount–The accumulated

depreciation–Date of acquisition–Date and price of disposal

(if relevant)

– Increase / decrease resulting from re-valuations (if relevant)

–Physical location–The responsible Asset

user–Cost Centre of user –Brief but meaningful

description–Identification number

where applicable–Valuation–Source of finance

ASSET MANAGEMENT CHALLENGES- THE ASSET POLICY

• The Municipal Asset Management Policy provides an overarching guideline to a municipality on how the municipality will IN PRINCIPAL manage their assets.

• The asset management policy deals with the municipal rules required to ensure the enforcement of appropriate stewardship of assets being:– Financial administration by the Chief Financial Officer; and– Physical administration by the individual asset managers.

• Statutory provisions are being implemented to protect public property against arbitrary and inappropriate management or disposal by a local government.

ASSET MANAGEMENT CHALLENGES- THE ASSET PLAN

• The development of asset management plans is interactive process, starts with the ID of service delivery needs and ends with an approved “multiyear” budget

• Seeks most cost-effective method of delivering that service. The asset manager should:–consider the service-level requirements ID in IDP

process;– review the current levels of service provided;–conduct a “gap analysis” of required vs. current service;– identify a range of options to resolve gap;–conduct a preliminary feasibility assessment of options;

ASSET MANAGEMENT CHALLENGES- THE ASSET PLAN

• develop a business case for the most feasible option or options. This business case should include:

the proposed service delivery option,identified benefits and identified needs,a full life-cycle-costs forecast,credible revenue forecasts including other funding sources;a risk assessment across the whole life cycle of each option, andperformance measures that can be used to assess the success of the options and implementation progress.

Key Principles of Asset Plan• Immovable asset management requires an integrated

approach

Key Aspects of asset plan - Asset Lifecycle

DisposalPlanning Acquisition In-usemanagement

Assetoperation

Maintenance/refurbishments

Managing/monitoring asset performance

Managingrisk

• Asset management is a systematic, structured process covering the whole life of an asset. The underlying assumption is that assets exist to support programme delivery. The asset management process should therefore at all times be focused on the optimal support for service delivery objectives.

Asset Management Plans in Context

33

ASSET MANAGEMENT CHALLENGES- PLANNING interaction

• The ASSET planning phase determines the future direction of the municipality.

• Councillors and the community have big impact on the activities of the municipality in terms of delivering services.

• The IDP is adopted by Council through an extensive community consultation process

• The development of asset management plans and performance agreements are all linked to and driven by the IDP process and documented.

ASSET MANAGEMENT CHALLENGES- PLANNING interaction

MSA, section 25, defines the IDP as “a single, inclusive and strategic plan for the development of the municipality which ––(a) links, integrates and co-ordinates plans;–(b) aligns the resources and capacity of the municipality

with implementation of–the plan;–(c) forms the policy framework and general basis on

which budgets must be based; …”

ASSET MANAGEMENT CHALLENGES- PLANNING interaction

The development of the IDP requires clear answers to the following questions:–What existing assets do you have and where are they?

(Asset Registers)–What are the existing assets worth? (Valuation)–What are their condition and their expected remaining

useful life? (Condition Assessments)–What is the expected or required level of service? (IDP

development)–How can that level of service be achieved? (Asset

Management and Operational Plans)

ASSET MANAGEMENT CHALLENGES- PLANNING interaction

–What additional assets do you require? (GAP analysis)–How much will that level of service cost and when or

how can we fund it? (Multi-year Capital and Operating Budgets)

–How can we ensure that level of service is “financially sustainable” (Fiscal Policy, Short to Long-Term Financial Plans)

–How will we manage and monitor the delivery of that level of service? (SDBIP, Performance Management System and Performance Agreements)

ACCOUNTABILITY CYCLE = FINANCIALPLANNING CYCLE

IDP

Budget

SDBIP

In-year Reporting

Annual Financial

Statements

Annual Report

5 year Strategy

Three year Budget

Annual Plan to Implement

Standard Chart of Accounts (SCOA)

Monitoring

Oversight Reports

Focus of MBRR

Focus of MBRR������

����

������

����

������

����

������

����

IDP

Budget

SDBIP

In-year Reporting

Annual Financial

Statements

Annual Report

5 year Strategy

Three year Budget

Annual Plan to Implement

Standard Chart of Accounts (SCOA)

Monitoring

Oversight Reports

Focus of MBRR

Focus of MBRR������

����

������

����

������

����

������

����

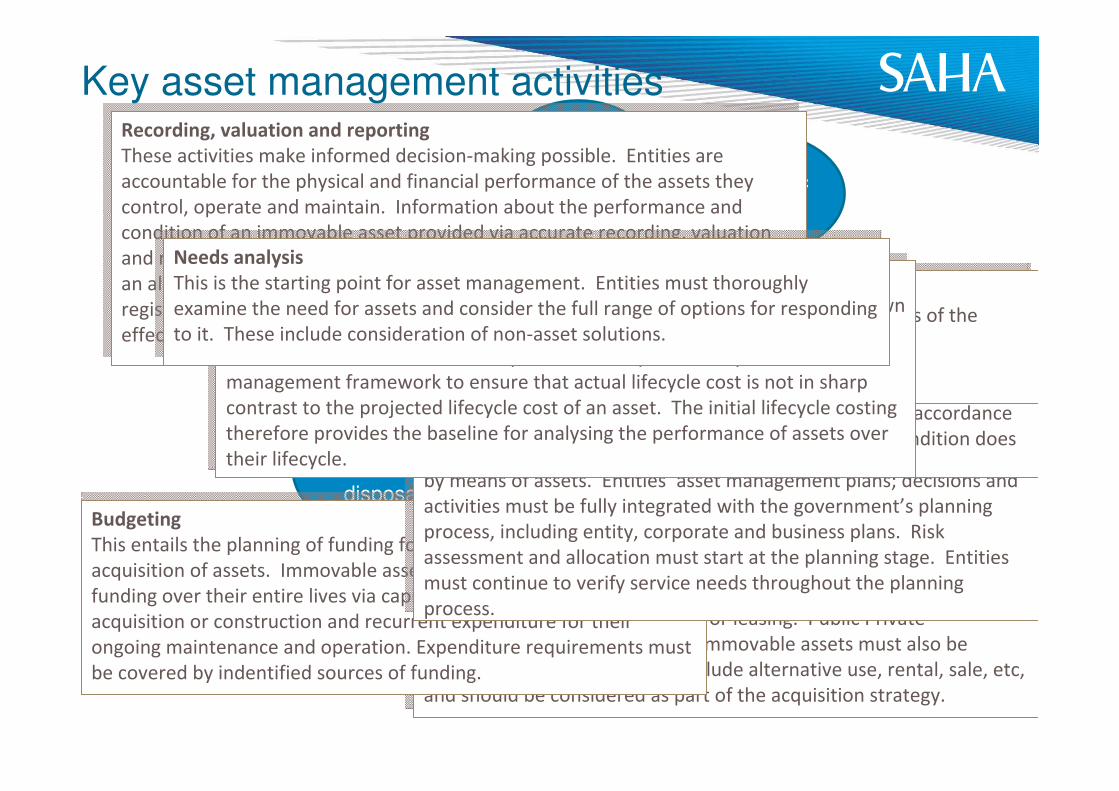

Key asset management activitiesNeeds

Analysis Economic appraisal

Planning

BudgetingLifecycle costing

Acquisition and

disposal

Recording, valuation

and reporting

Maintenance and

management

Asset management

���������� �� ����� �����������

������������������ ������������ ���� ������������� ���������

����� ����������������������� ��� � ������������ ����������������������

�� ��������������� ���� �� ���� ������� ������������������� ���� ��

�� ��� ����� ��������������������������������������� �������� �

� �������� ������������������������������� ��������� ������������������ ��

� ������ ��������������������������� ��������������� �� � �� ���� �������

��������������������� ������������������ �������� ������������ �����������

������������� ���� ��������������������� �

���������� �� ����� �����������

������������������ ������������ ���� ������������� ���������

����� ����������������������� ��� � ������������ ����������������������

�� ��������������� ���� �� ���� ������� ������������������� ���� ��

�� ��� ����� ��������������������������������������� �������� �

� �������� ������������������������������� ��������� ������������������ ��

� ������ ��������������������������� ��������������� �� � �� ���� �������

��������������������� ������������������ �������� ������������ �����������

������������� ���� ��������������������� �

������������ ��������� �

������� �� ��������������� ������������������� �� ��� �� ��

��� ����������������������� ����������� �����������������

�������� ������� ��������� ��������� ����!�����!�����

!��� ������� ���������� ��������������������������������

�� ���������" ����������� �� ����������� ����������� ����������������

� �������������� ����������������������������� ����������

������������ ��������� �

������� �� ��������������� ������������������� �� ��� �� ��

��� ����������������������� ����������� �����������������

�������� ������� ��������� ��������� ����!�����!�����

!��� ������� ���������� ��������������������������������

�� ���������" ����������� �� ����������� ����������� ����������������

� �������������� ����������������������������� ����������

�������

����� ������������ ������� � ������������ ����� ��� ��

������� ����������������������������������������������� �����

�� � ������������ ������������������ �� ���������������

������� ������ ������� �� ��������� ��� �� ���������������

� �� ���� �� � ���� ��������� ��� �� �������������� �������

������������� �� ���� ������������� � ��

�������

����� ������������ ������� � ������������ ����� ��� ��

������� ����������������������������������������������� �����

�� � ������������ ������������������ �� ���������������

������� ������ ������� �� ��������� ��� �� ���������������

� �� ���� �� � ���� ��������� ��� �� �������������� �������

������������� �� ���� ������������� � ��

�� ����

!�� ������������ ����������������� �����������������#������

������ ��������������� ����$ �������� ����� ����� �%������ ��� ��

��������������������� ���������� ����������� �� �$����� ��

��������� ���� ��� ���������������� ����� ������� ����&���

�������� ��� ���������� ���������������������� ����������� �����

������� � ����������������� ����������������������� ��

����������

�� ����

!�� ������������ ����������������� �����������������#������

������ ��������������� ����$ �������� ����� ����� �%������ ��� ��

��������������������� ���������� ����������� �� �$����� ��

��������� ���� ��� ���������������� ����� ������� ����&���

�������� ��� ���������� ���������������������� ����������� �����

������� � ����������������� ����������������������� ��

����������

� ����� ���� ���� � �� ���

!������ ������������������� ���������������� �� ���� ��

����� ������������������� ���� �� � �����'�� ��� ��� ��������

����������� ���� ���� ����������������� �� ���� ������������������

������������!�� ����� �� � ��������������� ������� �������� ���

� ��������������� ������ �������������������������� ��� �����

������������� ������ ������� �����

� ����� ���� ���� � �� ���

!������ ������������������� ���������������� �� ���� ��

����� ������������������� ���� �� � �����'�� ��� ��� ��������

����������� ���� ���� ����������������� �� ���� ������������������

������������!�� ����� �� � ��������������� ������� �������� ���

� ��������������� ������ �������������������������� ��� �����

������������� ������ ������� �����

������ ��� ��� �� �

������������������� ��� ������������������� ���� ������������

�������������� �� � ������������������� ���� �������

������ ��� ��� �� �

������������������� ��� ������������������� ���� ������������

�������������� �� � ������������������� ���� �������

����������������

����������������� ���� ����������������� ��� �������������� ����������� �� �

����������� ������$������ ����������� ���� ���������������������������������

������������������������� � �������������������������������������� ���

�� ����� �������� �������� ��������������������������������� �� �������

�� ����������������#������������������������ ������������� ����������������� ��

�������������������������� ������� ���� �������������� ����� �����������

��������������

����������������

����������������� ���� ����������������� ��� �������������� ����������� �� �

����������� ������$������ ����������� ���� ���������������������������������

������������������������� � �������������������������������������� ���

�� ����� �������� �������� ��������������������������������� �� �������

�� ����������������#������������������������ ������������� ����������������� ��

�������������������������� ������� ���� �������������� ����� �����������

��������������

������ � �����

��������������� ���� �������������� ����� ����� ���������������������

� �� ������ ���������������� ���� ���������������� ���������� ����������� � ��

������������� �������� ������� ���� � ������������� ��

������ � �����

��������������� ���� �������������� ����� ����� ���������������������

� �� ������ ���������������� ���� ���������������� ���������� ����������� � ��

������������� �������� ������� ���� � ������������� ��

![11042 Microsoft PowerPoint - Non Performing Asset [Compatibility Mode]](https://img.dokumen.tips/doc/110x75/577cc1011a28aba71191ebac/11042-microsoft-powerpoint-non-performing-asset-compatibility-mode.jpg)