Embed Size (px)

DESCRIPTION

of MichiganManagedBy • Safeguarding Your Records • BHPH: What’s in Store for 2012 • Compliance Overdrive Visit Us Online At www.miada.org PAID Winter 2012 PRSRT Standard U.S. Postage DALLAS, TEXAS Permit No. 2079

Citation preview

In This Issue

of MichiganManaged ByWinter 2012

Visit Us Online At www.miada.org

Are You Keeping Your Records

Safe?

PRSRT StandardU.S. Postage

PAIDDALLAS, TEXASPermit No. 2079

• Safeguarding Your Records• BHPH: What’s in Store for 2012• Compliance Overdrive

MI_0112.indd 1 12/20/11 10:57 AM

MI_0112.indd 2 12/20/11 10:57 AM

WINTER 2012 D R I V E L I N E

3

w w w . m i a d a . o r g

INSIDE

MIADAEVENTS

MAGAZINECONTENTS

ADVERTISERSINDEX

NATIONAL INDEPENDENT AUTOMOBILE DEALERS ASSOCIATIONWWW.NIADA.COM • WWW.NIADA.TVNIADA HEADQUARTERS: 2521 BROWN BLVD. • ARLINGTON, TX 76006-5203 PHONE (817) 640-3838FOR ADVERTISING INFORMATION CONTACT: TROY GRAFF (800) 682-3837 OR [email protected] DRIVELINE IS A PUBLICATION OF THE MICHIGAN INDEPENDENT AUTOMOBILE DEALERS ASSOCIATION INC., BUT IS ALSO MAILED TO NON-MEMBER DEALERS IN MICHIGAN IN AN EFFORT TO ENCOURAGE THEM TO JOIN AND SUPPORT OUR EFFORTS TO IMPROVE THE PROFIT POTENTIAL FOR THE INDUSTRY. THE DRIVELINE IS PUBLISHED QUARTERLY BY AUTOMOTIVE DEALERS RESOURCE OF MICHIGAN, 55 E LONG LAKE RD. PMB 233, TROY, MI AND THE NATIONAL INDEPENDENT AUTOMOBILE DEALERS ASSOCIATION SERVICES CORPORATION, 2521 BROWN BLVD., ARLINGTON, TX 76006. PERIODICAL POSTAGE IS PAID AT ARLINGTON TX, AND AT ADDITIONAL OFFICES. THE STATEMENTS AND OPINIONS EXPRESSED HEREIN ARE THOSE OF THE INDIVIDUAL AUTHORS AND DO NOT NECESSARILY REPRESENT THE VIEWS OF THE MICHIGAN INDEPENDENT AUTOMOBILE DEALERS ASSOCIATION INC., AUTOMOTIVE DEALERS RESOURCE OF MICHIGAN, OR THE NATIONAL INDEPENDENT AUTOMOBILE DEALERS ASSOCIATION. LIKEWISE, THE APPEARANCE OF ADVERTISERS, OR THEIR IDENTIFICATION AS MEMBERS OF THE MICHIGAN OR NATIONAL ASSOCIATIONS DOES NOT CONSTITUTE AN ENDORSEMENT OF THE PRODUCTS OR SERVICES FEATURED. FOR 31 YEARS, WE HAVE WORKED TO REPRESENT THE INDEPENDENT AUTOMOBILE DEALERS IN MICHIGAN. WE NEED YOUR SUPPORT. PUBLISHER/EDITOR AT LARGE: Nancy R. ChapmanFRONT COVER BY Mike MorganSTATE MAGAZINE MGR./SALES Troy Graff • [email protected] Andy Friedlander • [email protected]/PRODUCTION MGR. Christy Haynes • [email protected] Nieman Printing

R�EASTERN CHAPTER MEETING: Tuesday, Jan. 10, 7 p.m., American Polish Cultural Center, 2975 E. Maple Rd., Troy

RMIADA BOARD OF DIRECTORS MEETING: Wednesday, Feb. 29, 6 p.m., Lexington Lansing Hotel, Lansing

RMID MICHIGAN CHAPTER MEETING: Contact Leon Fransisco at 517-272-5000

RNORTHERN MICHIGAN CHAPTER MEETING: Contact Dennis Craig at 231-938-2627

R WEST MICHIGAN CHAPTER MEETING: Monday, Feb. 20, 6:30 p.m., Brann’s Steakhouse, Grand Rapids

All events are listed online at: www.miada.org

• Quick Turnaround Service within Michigan • Easy One Page Application • No Financial Statements Required in Most Cases • Checks and Credit Cards Accepted • Lost Title Bond Service • High Risk Bonding Sources Available

FOR INFORMATION ON THESE AND OTHER BONDS: Apply over the phone at: 888-855-0100 * fax: 888-855-7111 or email: [email protected]

CHECK With Bond Source Insurance Agency For Your Bonds

Dealer Bond RatesMI MVD $10,000 Bond:MIADA Member: $100/1 yr; $250/3 yr (for qualifying dealers)R

CHAIRMAN OFTHE BOARD Ed OphoffOphoff Motor Sales2921 S. DivisionWyoming, MI [email protected]

PRESIDENTJerry DrouillardAutohaus4411 DelemereRoyal Oak, MI [email protected]

VICE PRESIDENTRay CampiseCertified Motors23509 Little MackSt. Clair Shores, MI 48080586-775-7000sales@[email protected]

TREASURERArt DouglasJim Douglas Auto Sales1153 BaldwinPontiac, MI [email protected]

Board of Directors

04 Safeguarding Your Records08 IRS Form 8300 14 Welcome New/Renewing Members15 Records Retention Guidelines 17 MIADA Membership Application

ADESA ...................................... Inside Front CoverAutoTrader.com....................................Back CoverBlue Cross Blue Shield ...................................... 14Greater Kalamazoo Auto Auction .......................9Indiana Auto Auction ........................................10Insurance Auto Auctions ......................................7Lakeside Insurance Agency ...............................11Protective ................................. Inside Back CoverSmartAuction ......................................................5United Acceptance ...........................................13

The Purpose for Which MIADA was OrganizedREPR INTED FROM THE M IADA ART ICLES OF INCORPOR AT ION, JUNE 22, 1981

To unite in common organization those engaged in the automobile business and others interested in said business and in the welfare of our State;

To protect and promote the mutual interest of its Members;To formulate and maintain ethical standards for the guidance of its members in their relations

with each other and with the public;To advocate necessary public improvements and oppose unnecessary or wasteful expenditure

of public funds;To promote and encourage the enactment of just and reasonable laws and ordinances affecting

the licensing, regulating and conducting of the automobile business, and to oppose the enactment of those that would be unjust and unreasonable;

To correlate the activities of the National Independent Automobile Dealers Association with the Michigan Independent Dealers Association and local dealer Associations in this State.

SECRETARYTed CooperGenesys Systems360 E. MapleTroy, MI [email protected]

DIRECTORSDebbie RichardsEllis Richards Motors24900 GratiotEastpointe, MI [email protected]

Dennis CraigInstant Car CreditP.O. Box 146Acme, MI [email protected]

Jeffrey BraatzParadise Motors8212 W. Saginaw Hwy.Lansing, MI [email protected]

Jetre OrmsbeeOrmsbee Implement241 M-68 Hwy. EastAfton, MI 49705231-238-9928

Jim VerWysSuperior Automotive1100 S. WashingtonHolland, MI 49423616-396-7600

Joe KuhtaGWC8865 ReeseClarkston, MI [email protected]

Leon FransiscoFransisco Automotive Enterprises1835 E. JollyLansing, MI [email protected]

Mike TokieJack’s Auto ServiceP.O. Box 52Grawn, MI [email protected]

Nigel FoxSovereign Auto Purchasing730 N. MainFlushing, MI [email protected]

INSIDE

Rick RynbergRynberg’s Car Company3880 Holton Rd.Muskegon, MI [email protected]

Robert VanCoillieVan’s Motor Sales Inc.1507 Garfield Rd.Traverse City, MI [email protected]

Tony LoBrettoAlamo Valley Auto Sales6100 West “D” Ave.Kalamazoo, MI [email protected]

MI_0112.indd 3 12/20/11 10:57 AM

D R I V E L I N E WINTER 2012

4

w w w . m i a d a . o r g

THE SAFEGUARDS RULE is one of several federal regulations concerned with the protection and safekeeping of consumers’ private personal information. Like the Privacy Rule, the Safeguards Rule derives from the Gramm-Leach-Bliley Act, often referred to as the Privacy Act.

As implemented by the Federal Trade Commission (FTC), the Safeguards Rule requires financial institutions to develop, implement, and maintain a comprehensive information security program. The program must be in written format and must contain administrative, technical, and physical safeguards appropriate to your business. For purposes of the GLB, a “financial institution” includes businesses – such as car dealers – involved in the extension of credit or in activities related to the extension of credit.

The end of year is an excellent time to review and update existing Safeguards Plans, or to develop one if necessary. The objective of your Safeguards Plan is to define and document your dealership’s procedures for safeguarding, or physically securing and protecting, consumers’ personal private information.

At a minimum, your Safeguards Plan will document:

• The personal identifying information you collect.

• How it is collected.• Where it is stored and how it is

safeguarded while it is “active” – while the sale is in process.

• Where it is stored and how it is safeguarded on a permanent basis.

• How long the data is retained.• How the data is handled for disposal.• Employee security training and

certifications.• Security threat and incident response

plan.

Step 1: Get OrganizedEffective data security starts with

assessing what information you have and identifying who has access to it. Understanding how personal information moves into, through and out of your business,

and who has – or could have – access to it is essential to assessing security vulnerabilities. You can determine the best ways to secure the information only after you have identified it and traced how it flows through your business.

Determine what personal information you have in your files and on your computers.

Inventory hard copy records, such as:• File cabinets• File drawers• Archived storage• Off-site storageInventory digital records, including:• Desktop computers• Laptop computers• Tablets (iPads, etc.)• Cellphones• External drives• Flash drives• DVDs/CDs• Online data storage• Offsite/archived digital records• Employee-owned computers and

equipmentDetermine who has access to each of the

various data repositories.Track the flow of data through the business.

Only by understanding the flow of data can you identify points where the information is vulnerable. Take note of:

• Who gives personal information to your business

• How the information is received• What kind of information is collected at

each point• Where you keep the information as it

moves through the business• Who has access to the information as it

moves through the business

Step 2: MinimizeAfter you inventory what information you

already have and where and how it is stored, determine what part of it is necessary for your business, considering both your business needs as well as state and federal regulatory requirements. Then, plan to collect only what you need, and plan to keep it only as long as you must. Information can include:

Customer identification: Dealers are required by federal law to identify their customers prior to completing a sale. Therefore, you are obliged to collect and retain some amount of personal identifying information, such as name, residential address and date of birth. You may collect the individual’s social security number, but it is not required at this time.

• Copy of government-issued photo ID, such as driver’s license, passport, etc.

• Documentation of steps taken to confirm customer identity

• Specially Designated Nationals (SDN) List printout. The Office of Foreign Assets Control maintains a list of persons, typically terrorists and narcotics smugglers, whose assets are blocked. U.S. persons are generally prohibited from transacting business with them. For each sale, you should search the alphabetical list for your customer’s name and print the appropriate page, thereby documenting the absence of your customer’s name. The list is accessible through the MIADA website at www.miada.org.

It will also include completed forms for the vehicle sold, including:

• FTC Buyer’s Guide• Retail Purchase Agreement/Bill of

Sale, which includes Buyer’s Order, Dealer Warranty Statement, Trade-In Record and, optionally, Odometer Disclosure

• We owe/delivery confirmation• Privacy Notice• Retail Installment Sales Contract (if

financed)• RD-208 Title Registration formConsumer credit reports: You may

have a legitimate business need to obtain consumer credit reports from consumer reporting agencies, either for your employees or for your customers. Credit reports obviously contain highly personal information about the subject individuals. If you obtain credit reports, it is imperative that you adequately safeguard them. Restrict access to the reports, retain them no longer than necessary, then dispose of them appropriately, such as by shredding.

ProtectionNews

Developing Your Safeguards Plan

BY A

DR S

TAFF

YOUR SAFEGUARDS PLAN WILL INCLUDE PROCEDURES FOR PROPER DISPOSAL OF RECORDS YOU NO LONGER NEED. KEEP IN MIND THAT CONSUMER CREDIT REPORTS AND OTHER PERSONAL INFORMATION MAY BE SUBJECT TO THE DISPOSAL RULE.

CONTINUED ON PAGE 6

In This Issue

of MichiganManaged ByWinter 2012

Visit Us Online At www.miada.org

Are You Keeping Your Records

Safe?

MI_0112.indd 4 12/20/11 10:58 AM

MI_0112.indd 5 12/20/11 10:58 AM

D R I V E L I N E WINTER 2012

6

w w w . m i a d a . o r g

Credit and debit cards: The FTC recommends businesses not retain the account number and expiration date of consumer credit and debit cards unless absolutely necessary.

Financial account information: You will have occasion to collect financial account information, such as checking account numbers, when you receive payment from your customers. Retain this information only if you have an ongoing business need for it.

Step 3: DisposeYour Safeguards Plan will include

procedures for proper disposal of records you no longer need. Keep in mind that consumer credit reports and other personal information may be subject to the Disposal Rule (derived from the Fair and Accurate Credit Transactions Act of 2003), which means you cannot simply throw the information in the dumpster.

For all information collected, determine a retention period and document it in your Safeguards Plan. Keep in mind the minimum retention periods prescribed by various governing agencies and rules. Proof of compliance with Truth In Lending Act disclosures, such as on installment sales contracts, must be held two years from date of disclosure. Check with your accountant or tax attorney for guidelines regarding data retention for taxation purposes.

For that same information, document an appropriate disposal plan.

The Disposal Rule dictates disposal of paper records containing personal information by shredding, burning or pulverizing.

Digital records should be erased or the media physically destroyed. Be aware that deleting a computer file is not the same as erasing it. Deleting the file is not adequate destruction.

Step 4: ProtectIn your written plan, document

your procedures for safeguarding the information you do keep. Consider the following guidance provided by the FTC:

• Store paper documents and files as well as CDs, external computer hard drives, flash drives and other backups containing personally identifiable information in locked rooms or locked file cabinets. Limit and control who has keys and the number of keys.

• Remind employees not to leave sensitive papers out on their desks when they are away from their workstations.

• Require employees to put files away, log off their computers and lock their file cabinets and office doors at the end of the day.

• Implement a building security plan. At a minimum, ensure doors and windows are locked at the end of the day. Ensure emergency responders have appropriate contact numbers. Consider installing a security alarm system.

• Assess the vulnerability of your office network. Depending on your circumstances, it may be appropriate for you to engage an independent professional to conduct a full-scale security audit.

• At a minimum, don’t store sensitive consumer data on any computer with an Internet connection unless it’s essential for conducting your business.

• At a minimum, regularly run up-to-date antivirus and anti-spyware programs on individual computers and on servers on your network.

• At a minimum, use firewalls to protect your network and computers.

• Control access to sensitive information by

requiring employees to use passwords. The passwords should be “strong,” including a mix of letters, numbers and special characters. Do not allow simple passwords that can be easily guessed. In addition, the passwords should be changed regularly.

• Forbid transmission of personally identifying data through unencrypted email.

• Restrict use of laptops for storing sensitive information. If laptops are used, consider implementing a policy of using cords and locks to secure laptops to employees’ desks.

• Limit wireless and remote access to your network.

Step 5: TrainIn your Safeguards Plan, define the steps

you will take to engage your office staff in the security effort.

Check references or do background checks before hiring employees who will have access to sensitive data.

Consider asking new employees to sign an agreement to follow your company’s confidentiality and security standards.

Remind employees of your company’s policy and any legal requirements to keep customer information secure and confidential.

Know which employees have access to consumers’ sensitive personal information. Limit that access to employees with a “need to know.”

Implement a regular schedule of employee security training.

Require employees to notify you immediately if there is a potential security breach, such as loss of a laptop.

Consider implementing disciplinary measures for security policy violations.

Step 6: RespondFinally, decide how you will respond in

the event of a security incident or threat and document appropriate procedures in your written plan.

Designate a senior employee to coordinate and implement the response plan.

If a computer is compromised, disconnect it immediately from the network and the Internet.

Investigate security incidents immediately and take steps to close off existing vulnerabilities or threats to personal information.

Consider who to notify in the event of an incident. You may need to notify consumers, law enforcement, customers, credit bureaus and other businesses.

Don’t overlook the security threat associated with natural disasters. Any event that disrupts your normal business environment can result in a compromise of data in your possession. Consider how you would protect the data in the event of a fire, flood or tornado, any of which could leave your normally secure office vulnerable.

The stated objective of the Safeguards Rule is to protect consumers’ private information. You may find, however, as you develop your plan, that the procedures you put in place could easily extend to other segments of your records. With a minimal amount of extra effort, the result could be a viable working plan that will help protect all of your business records.

NOTE: WE ARE NOT ATTORNEYS. THIS ARTICLE WAS PREPARED

FOR INFORMATIONAL PURPOSES ONLY. IT HAS BEEN MADE

AVAILABLE WITH THE UNDERSTANDING THAT NEITHER ADR

OF MICHIGAN NOR MIADA IS ENGAGED IN RENDERING LEGAL

ADVICE. YOU ARE URGED TO CONTACT LEGAL COUNSEL FOR ITS

APPLICATION TO YOUR OPERATION.

BY ADR STAFF

CONTINUED FROM PAGE 4

WORL

D AUTOMOBILE

CHAMPIONSHIP

IN NOVEMBER, THE NATIONAL HIGHWAY TRAFFIC SAFETY ADMINISTRATION (NHTSA) and the Environmental Protection Agency (EPA) issued a joint proposal regarding new fuel economy and greenhouse gas emission standards for passenger cars and light trucks for model years 2017 through 2025. The proposed Corporate Average Fuel Economy (CAFE) standards range from 40.1 mpg in model year 2021 to 49.6 mph in model year 2025.

Detailing the costs and benefits of the program, the proposal states, “The agencies estimate that fuel savings will far outweigh higher vehicle costs.” The report estimates the technologies required to achieve the fuel economy standards will add, on average, $2,000 to the cost of MY 2025 vehicles, while fuel savings are forecast to range from $5,200 to $6,600 over the life of the vehicles.

Based on those costs and savings, the proposal calculates it will take four years for a consumer purchasing a MY 2025 vehicle with cash to realize savings. Consumers financing a MY 2025 vehicle on a five-year loan are projected to realize a cash flow savings of about $12 per month during the loan period.

The proposed standards for MY 2017-2025 include new options for manufacturers to achieve compliance. Beginning with MY 2017, manufacturers will be able to generate fuel consumption improvement values for improvements in air conditioning system efficiency to comply with the CAFE standards. They will also be able to apply savings from “off-cycle” technologies such as solar panels on hybrids, adaptive cruise control or active aerodynamics. In addition, the proposal includes manufacturer incentives encouraging hybridization of full-size pickup trucks.

The agencies’ joint proposal was published in mid-November, and public comments will be accepted through mid-January. For more information, the rule and related documents can be accessed on the NHTSA’s CAFE website at www.nhtsa.gov/fuel-economy.

BY ADR STAFF

CAFE Standards Update

THIS YEAR’S WORLD AUTOMOBILE AUCTIONEERS Championship will be webcast live for the very first time, courtesy of NIADA.TV. The live webcast of the 2012 WAAC can be viewed in its entirety on the home pages of www.niada.tv, www.niada.com and www.waacnet.net . The live online coverage of the event begins at 11 am ET on Friday, March 3O, 2012 and is free for all online viewers. Cheer on your hometown favorite Auctioneers and Ringmen, and catch all of the fun and excitement of the 2012 World Automobile Auctioneers Championship at your leisure, exclusively on all three websites. For more detailed information please visit www.niada.com and click on the “EVENTS” tab or call (303) 807-1108.

World Automobile Auctioneers Championship

MI_0112.indd 6 12/20/11 10:58 AM

WINTER 2012 D R I V E L I N E

7

w w w . m i a d a . o r g

THE LATEST EQUIFAX NATIONAL CREDIT Trends Report declared auto finance companies have significantly increased lending. In fact, the growth is more than 47 percent during the past two years.

Analysts discovered auto finance lenders outpaced bank and credit union lending to subprime borrowers during the past two years, as well. Equifax defines subprime borrowers as consumers with credit scores less than 640.

According to the most recent monthly report, there were 854,800 auto finance company-originated loans in July, compared to 581,300 for July 2009. Equifax tabulated that vehicle loans to subprime borrowers now account for 38.5 percent of all auto loan originations for auto finance companies and 17.6 percent for banks and credit unions — numbers that are quickly approaching pre-recession levels.

By contrast, analysts pointed out 820,200 loans were originated by banks and credit unions for the same period in July, versus 832,000 for July 2009. That’s a decrease of less than 2 percent.

Equifax mentioned delinquency rates continue to improve for outstanding vehicle loans currently 60 or more days past due.

Michael Koukounas, senior vice president of special client services for Equifax, indicated the rate is now down to 1.63 percent of loans, compared to a peak that was near 3 percent. Koukounas believes the decline reflects a continuation of sustained credit retraction that the auto lending industry is experiencing earlier than other loan types.

“With unemployment rates remaining elevated for a prolonged period, auto lenders have proactively adopted more comprehensive data and verification tools for greater loan-level transparency in evaluating a wider band of consumers, which has helped enable the auto lending industry to recover more quickly than others,” Koukounas explained.

To support his theory, Koukounas pointed out that in July, 1.7 million auto loans were originated, worth $32 billion collectively. From January through July, he said, 11.3 million new auto loans were originated — a 13.2 percent increase over the same span last year.

The collective amount of these loans is 14.8 percent greater than in 2010, climbing to $213.9 billion.

Equifax’s report also revealed the average monthly payment has remained relatively unchanged during the past year. For auto finance company-originated loans, the payment ticked up to $407 in July from $404 in the same month last year. For bank and credit union-originated loans, the payment slid down to $364 in July from $377 in July of last year.

Equifax insisted the changes clearly show that the growth the industry is experiencing is tied to increases in number of loans rather than an increase in average loan amount.

SUBPRIME AUTO FINANCENEWS

Subprime Auto Loans are on the Rise

IndustryNews

(from left) Harold Murdock Flint Auto Auction, Art Douglas MIADA Treasurer, Jerry Drouillard MIADA President, Dan Johnson (raffle winner), Nigel Fox MIADA Director, and Jim Latimer (raffle winner).

2011 $10,000 Raffle Winners

MI_0112.indd 7 12/20/11 10:58 AM

D R I V E L I N E WINTER 2012

8

w w w . m i a d a . o r g

Reminder: Companies must furnish a written notice to any individual named on a Form 8300 by January 31.

Trades and businesses that receive more than $10,000 cash for a business transaction must report these payments to the Internal Revenue Service within 15 days of the transaction using Form 8300, Report of Cash Payments Over $10,000 Received in a Trade or Business. The reporting requirement may be the result of a single transaction or the result of two or more related transactions.

In addition to filing Form 8300 with the IRS, companies must also furnish to each person whose name is required to be included in the Form 8300 a written statement by January 31 of the year following the transaction. This statement must include:• the name, address, contact person, and

telephone number of the business filing Form 8300,

• the aggregate amount of cash the business reported to the IRS, and

• a statement that the business provided this information to the IRS.

Cash reporting is a requirement of both the Internal Revenue Code and the Bank Secrecy Act. It is important that businesses comply with these laws to assist the IRS and the Financial Crimes Enforcement Network in their efforts to combat money laundering and to avoid potential civil and criminal penalties. Penalties for violation of the Form 8300 filing and furnishing requirements have been increased by the Small Business Jobs and Credit Act of 2010. Increased penalties apply with respect to Forms 8300 required to be filed and related notices required to be furnished on or after Jan 1, 2011.Penalty for failure to file a timely and correct Form 8300 has been raised from $50 to $100. However, an intentional disregard for failure to file a timely and correct Form 8300 can result in a penalty of greater of $25,000 or the amount of cash received in such transaction not to exceed $100,000. The failure to furnish a statement to the persons whose names were required to be included in the Form 8300 has been raised from $50 to $100 per violation. A copy of Form 8300 can be found in this publication. The PDF-fillable version of the form is available at www.irs.gov, along with complete instructions.

IRS Form 8300 Motor Vehicle Dealership Q & A

The Motor Vehicle Technical Advisor Program, in conjunction with IRS specialists on money laundering, has compiled a list of motor vehicle

dealership-specific questions and answers relative to Form 8300. Some of the questions are the basics and some are dealership-specific.

The BasicsWhat does “cash” mean for the purposes of

Form 8300?• Cash is money: currency and coins of the

United States and any other country. • Cash is also certain monetary instruments –

a cashier’s check, bank draft, traveler’s check or money order – if it has a face amount of $10,000 or less and the business receives it in:

• A designated reporting transaction (generally, a retail sale of a consumer durable, a collectable, or a travel or entertainment activity) or

• Any transaction in which the recipient knows the payer is trying to avoid the reporting of the transaction on Form 8300.

What is a related transaction?• Transactions between a buyer and a seller

that occur within a 24-hour period are related transactions.

• Transactions more than 24 hours apart are related if the recipient of the cash knows, or has reason to know, that each transaction is one of a series of connected transactions.

Does the 24-hour period mean one day such as all day Tuesday or does it mean literally 24 hours such as from 11 a.m. on Tuesday to 11 a.m. on Wednesday?

• A 24-hour period is 24 hours, not necessarily a calendar day or banking day.

When is the Form 8300 due?• Form 8300 is due within 15 days after the

date the cash was received. • If there are subsequent payments that are

made with respect to a single transaction (or two or more related transactions), the Form 8300 is due when the total exceeds $10,000.

• Each time the payments aggregate in excess of $10,000 the business must file another Form 8300 within 15 days of the payment that causes the additional, previously unreportable payments to total more than $10,000.

Must a business notify its customer that it has filed a Form 8300 regarding the cash transaction with the customer?

• Yes, a business must notify its customer, in writing, by January 31 of the subsequent calendar year.

If a business filed a Form 8300 on an individual and checked the suspicious transaction box, and a Form 8300 was not otherwise required, does the business have to inform the individual that a Form 8300 was filed?

• Reporting of the suspicious transaction in this instance is voluntary. A business is only required to provide a statement to individuals if the filing of the Form 8300 is required. A business is prohibited from informing the buyer that the suspicious transaction box was checked.

Instead of sending the customer a separate notification letter, can the dealership use the sales invoice as the notification requirement, if the sales invoice has language printed on it that the IRS will be furnished with information for cash sales over $10,000?

• There is nothing in the Code or regulations mandating a specific format for the customer statement. The regulations, however, establish certain minimum requirements. As long as these minimum requirements are met, there would be no problem if the seller chose to print the required language on an invoice.

• The statement must contain the following information:

• The name and address of the person completing Form 8300;

• The aggregate amount of reportable cash in all related cash transactions;

• A legend stating that the information contained in the statement is being reported to the Internal Revenue Service.

• If during the calendar year, the dealer has more than one transaction with the customer, furnishing multiple copies of the sales invoice would not meet the notice requirements because it is not a “single” statement. In this situation, the dealer should provide a single written notice for all of the transactions.

Is a personal check considered cash for reporting on Form 8300?

• No, personal checks are not considered cash. If the business is unable to obtain the

Taxpayer Identification Number of a customer making a cash payment of over $10,000, should the business file Form 8300 anyway?

• Yes, the business should file Form 8300 with a statement explaining why the Taxpayer Identification Number is not included.

Does a wholesaler (no retail) report transactions paid in US (or foreign) coins and currency only?

• Yes, if the wholesaler receives payment in the form of coins or currency. A wholesaler, however, need not report transactions paid with cashier’s checks, bank drafts, traveler’s checks or money orders unless the recipient knows, or has reason to know, the payer is trying to avoid the reporting of the transaction on Form 8300.

IRSNewsews

BY A

DR S

TAFF

REPORT OF CASH PAYMENTS OVER $10,000 RECEIVED IN A TRADE OR BUSINESS

IRS Form 8300 Reminder

To download Form 8300, go to www.irs.gov/pub/irs-pdf/f8300.pdf.

CONTINUED ON PAGE 10

MI_0112.indd 8 12/20/11 10:58 AM

WINTER 2012 D R I V E L I N E

9

w w w . m i a d a . o r g

Auto Makers Now Import JobsFOR YEARS, THE DETROIT Three have moved production out of their U.S. plants to avoid the high cost of union labor. Ford Motor Co. recently signed a tentative labor contract with the United Auto Workers union that partly reverses that trend.

With union labor costs edging toward its lowest-cost competitors, Ford is moving to bring work back into U.S. plants. An underutilized factory in Flat Rock, Mich., will help build the next generation Fusion mid-sized car that to date has been produced only in Mexico. Another Ford plant in Kentucky will assemble commercial vans the company now builds in Turkey.

EXCERPTED FROM THE WALL STREET JOURNAL

AutoNews

The National Auto Auction Association (NAAA) recently issued notice to its members to be on the alert for digital odometer tampering. The NAAA has received reports of digital odometer tampering through the use of odometer mileage programming devices. Since odometers do occasionally malfunction, manufacturers provide legitimate repair facilities security codes to use with authorized odometer mileage programming devices. The NAAA indicates the codes may have been compromised, allowing non-authorized devices to be manufactured and sold online.

The NAAA further reports that the National Highway Traffic Safety Administration (NHTSA) is familiar with the practice and has been in contact with auto manufacturers about the issue.

The NAAA recommends its member auctions be on alert for potential mileage discrepancies that crop up between time of check-in and sale and between time of assignment and delivery to the auction, as this could be an indication that the vehicle was tampered with to decrease its value and provide a fraudulent benefit to the ultimate buyer of the vehicle.

Individuals with information concerning odometer fraud schemes are encouraged to contact the NHTSA’s Office of Odometer Fraud at 202-366-5953. Complaints concerning a single vehicle should be reported at the state level.

Digital Odometer Tampering

MI_0112.indd 9 12/20/11 10:58 AM

D R I V E L I N E WINTER 2012

10

w w w . m i a d a . o r g

What if a retailer also does some wholesale transactions, must the business report all transactions, or just the retail ones?

• If the trade or business of the seller principally consists of sales to ultimate consumers, then all sales, including wholesale transactions, are considered “retail sales” and are subject to the Form 8300 reporting requirements.

Does a dealer need to accumulate individual sales to a customer, or sales to a wholesaler, throughout a 12-month period and report whenever they exceed a cumulative $10,000?

• Each transaction stands on its own. But if the dealership knows that any of the individual purchases are related, a Form 8300 should be filed.

If a customer purchased an item, then eight weeks later the same customer purchased a different item, are these amounts aggregated and reported on the Form 8300?

• No, if the two payments are for separate unrelated transactions.

Dealership-Specific QuestionsA customer purchased a vehicle for $9,000

cash. Within the next 12 months, the customer paid the dealership additional cash of $1,500 for a repair to the vehicle’s transmission, accessories and a customized paint job, etc. Should a Form 8300 be filed?

• No, unless the dealer knew or had reason to know the sale of the vehicle and the subsequent transactions were a series of connected transactions (for example, if the dealer and the customer agreed, as a condition of the sale of the vehicle, that the customer would be obligated to buy an additional $1,500 of goods or services).

• Transactions are related if they occur within a 24-hour period. Transactions are related even if they are more than 24 hours apart if you know, or have reason to know, that each is one of a series of connected transactions. For example, items or services negotiated during the original

purchase are related to the original purchase. A customer wired $7,000 from his bank

account to the dealership’s bank account and also presented a $4,000 cashier’s check. Does the dealership complete Form 8300?

• A wire transfer does not constitute cash for Form 8300 reporting. Since the remaining cash remitted was less than $10,000, the dealer has no 8300 filing requirement.

A customer makes weekly payments in cash to a dealership as a lease payment or loan payment on a vehicle. During a 12-month period, these payments total more than $10,000. Are these payments considered related transactions and is the dealership required to file a Form 8300?

• Yes, the weekly lease or loan payments constitute payments on the same transaction (the leasing or purchase of the vehicle).

• Accordingly, the dealership is required to file Form 8300 when the total amount exceeds $10,000.

• Each time the payments aggregate in excess of $10,000 the dealership must file another Form 8300 within 15 days of the payment that causes the previously unreportable payments to total more than $10,000

A husband and wife purchase two cars at one time from the same dealer and the total cash received is $10,200. How many Form 8300s should the car dealer file?

• The transaction(s) can be viewed as either a single transaction or two related transactions. Either way, it warrants only one Form 8300.

If a customer purchased a cashier’s check at the bank for over $10,000, would the bank report the transaction? Does the seller of a vehicle need to report the transaction if the same cashier’s check is subsequently used to purchase a vehicle?

• If the cashier’s check was purchased with cash exceeding $10,000, the bank would file a Currency Transaction Report (not a Form 8300).

• The purchase of a vehicle with a cashier’s check, bank draft, traveler’s check or money

order with a face amount of more than $10,000 is not treated as cash and a business does not have to file Form 8300 when it receives them.

How should a dealership handle a nonresident alien with no SSN?

• Use the IRS Individual Taxpayer Identification Number (ITIN) if the nonresident has one. If there is no ITIN enter (NONE) on Item 6 of Form 8300. Pub 1544 provides a list of exceptions in which a filer is not required to provide a Taxpayer Identification Number of a person who is a nonresident alien individual or a foreign organization.

• You must verify the individual’s name and address and insert this information on Item 14 of Form 8300. For nonresident aliens, acceptable documentation would include a passport, alien registration card or other official document.

Do payments in excess of $10,000 in cash paid to a body shop need to be reported? Do the 8300 filing requirements apply to services as well as goods?

• Yes. Cash, in the form of currency, received in excess of $10,000 must be reported. However, a service is not a consumer durable so the expanded definition of cash does not apply to payments for services. The body shop would file an 8300.

A dealership sold cars on Jan. 31 and Feb. 6 to one customer and received $20,000 cash in two payments of $10,000 each on the same date for the two cars. Is a Form 8300 required?

• Yes. The dealership received over $10,000 in cash within 24 hours.

Customer purchased five cars, each separately, through the year totaling $15,000 and none of which individually exceeded $10,000. Is Form 8300 required?

• If the dealer knows, or has reason to know, that each transaction is one of a series of connected transactions a Form 8300 would be required. If there is no reason to believe that they are connected, the five transactions would be viewed as separate transactions none of which exceed $10,000 in cash and a Form 8300 would not be required.

Are wire transfers considered cash?• Wire transfers are not considered to be cash and

no Form 8300 is required to be filed. • The money services business (MSB) or bank that

handles the wire transfer must document these types of transactions by filing a CTR on amounts over $10,000.

A dealership receives greater than $10,000 in cash on day one for the sale of a vehicle. On day three, the deal is canceled due to an inability to finance the deal. The dealership returns the cash. Is a Form 8300 required?

• Yes. Once the dealership receives cash exceeding $10,000, a Form 8300 must be filed.

• The deal not going through may in fact be an attempt to launder illegal funds.

• If $10,000 or less was received by the dealer and the deal was canceled, the dealer may voluntarily file a Form 8300 if the transaction appears suspicious.

If a dealership receives a bank check drawn on the funds of the bank (not a personal checking account check or a check drawn on a personal account of the customer) with the customer’s personal account number and customer name on it, is this considered cash or a cash equivalent?

• Bank checks (drawn on the bank’s account, not the account of the customer) of $10,000 or less are cash under the expanded definition of cash, unless they are loan proceeds.

• The fact that there are notations on the check or even that the check is made payable to the dealership does not negate this.

A customer purchases a vehicle for $15,000 and pays for it with $9,000 in cash and puts the remaining $6,000 on a personal credit card. Should a Form 8300 be filed? Instead of a personal credit card, the customer pays the remaining $6,000 with his ATM card. Is the ATM amount considered cash or a cash equivalent that makes the total amount received over $10,000 and thus reportable on Form 8300?

CONTINUED FROM PAGE 8

MI_0112.indd 10 12/20/11 10:58 AM

WINTER 2012 D R I V E L I N E

11

w w w . m i a d a . o r g

• No Form 8300 is required. • Less than $10,000 in cash was received. A credit

card is not cash. • The ATM card works the same as a credit card

in this instance. The only difference is that the account will be charged with a debit against existing funds instead of charged for a debit to nonexisting funds, but a promise to repay later.

• An ATM transaction is not given the consideration of cash; therefore, since the amount received in cash or cash equivalents is less than $10,000, the transaction is not reportable.

For wholesalers, where a purchasing retailer buys more than one vehicle in a single day, is that one transaction, a series of related transactions or a series of unrelated transactions given that there are multiple vehicles? What happens on separate purchases over the course of a week? What about a month?

• Two or more transactions within a 24-hour period are related transactions. A trade or business that receives more than $10,000 in related transactions must file Form 8300.

• If purchases are more than 24 hours apart and not connected in any way that the seller knows, or has reason to know, then the purchases are not related and a Form 8300 is not required.

For sales to individual retail customers, payment of cash for one car at multiple time periods is a series of related transactions. However, what about when the same purchaser buys a second car one week later and provides enough cash to trigger the reporting requirement? Since they are two separate vehicles, are those related transactions? What is the time period break for considering them unrelated transactions?

• The car purchases are separate transactions unless the purchase of the second car was negotiated at the same time of the first car or the seller otherwise knows or has reason to know that the transactions are connected.

• When an installment arrangement is established on a single transaction, the dealer must file a Form 8300 when cash payments received exceed $10,000 within a 12-month period. After filing the 8300, a new count of cash payments from the buyer would begin.

• The time period break for considering transactions unrelated is 24 hours.

What exactly can be said to a customer who inquires about IRS Form 8300 reporting? Some dealers are advised not to refer to IRS Form 8300 reporting in the presence of the customer. In particular, dealers are concerned that advising customers that they need information for an IRS 8300 report could degenerate into a structuring conversation. What if the customer asks what the information is for? Can the dealer volunteer that it is for IRS Form 8300 reporting?

• A customer can be, but is not required to be, told at the time of the transaction about the law requiring the reporting of cash payments over $10,000 to the IRS and FinCEN.

• What a dealer cannot do is aid a customer in structuring a transaction to prevent a Form 8300 from being filed.

• A dealer who is filing Form 8300 voluntarily because of suspicious activity cannot inform the customer of the filing.

What are the penalties if a dealership does not file a Form 8300?

• There are civil penalties for failure to file a correct Form 8300 by its due date and for failure to provide a statement as required.

• Additional penalties apply for intentional disregard of the filing requirements.

• Criminal penalties may apply in the case of willful filing of false or fraudulent Forms 8300.

A dealership receives monthly ACH payments [automatic payments from a customer bank account]. If the payments total in excess of $10,000, should the payments be treated as cash?

• ACH payments are not considered cash for the purpose of reporting on Form 8300.

A related finance company provides financing to customers of multiple related used vehicle dealerships. The finance company purchases

contracts from the used car lot and a bank check is issued to the car lot for the amount of the car deal. Would the definition of cash to include cashier’s checks and money orders apply to the finance company?

• As to the sale to the customer, the dealership’s sale of the vehicle constitutes a retail sale of a consumer durable requiring reporting of certain monetary instruments if the face amount was $10,000 or less and the total transaction exceeds $10,000.

• When the finance company purchases the “finance contract,” they do not have a designated reporting transaction. The finance contract is not a consumer durable, collectible, or travel or entertainment activity. Thus monetary instruments with a face amount of $10,000 or less received from the finance company to pay off the finance contract would under normal situations not be reportable.

What type of records might an examiner request during an 8300 examination?

• Records requested may vary by examiner but typically the following records are requested:

• Checking, savings, and/or other financial account statements and deposit slips.

• An electronic bank deposit reconciliation in Excel format extracted from the dealer’s Dealers Management System (DMS). The report generally requires all receipts of the business from any source including:

• the amount, date received, method of payment (cash, check, credit card number, etc.),

• payer name, and • receipt number. • Receipt sources should include new and used

vehicle sales, leases, service, parts, body shops and any non-customer receipts.

• Deal jackets for leases and sales during the examination period.

• Sales journals, cash receipts journals, accounts/notes receivable, sales invoices.

MI_0112.indd 11 12/20/11 10:58 AM

D R I V E L I N E WINTER 2012

12

w w w . m i a d a . o r g

BHPHNews

What’s in Store for 2012

WHAT’S IN STORE FOR YOUR STORE IN 2012? If it’s anything like 2011, it should be another good year to be in the Buy Here-Pay Here industry. The coming year will not be without its challenges, though. In fact, there are certain areas of the industry that could be more challenging than ever.

To get an idea of what to look forward to in 2012, we first need to review how 2011 treated the BHPH world. It was probably the weirdest year I can remember in the 15-plus years I’ve been in the business. Tax season was sporadic at best, which pretty much set the tone for all facets of the business for the rest of the year.

From a profitability standpoint, the dealers I have the distinct privilege of working with enjoyed an 11 percent overall increase in 2011 versus 2010. This increase was due mostly to the rightsizing of operations. Dealers focused on their entire operations, from top to bottom, on cutting the fat and running their operations based on the cash they were generating instead of relying on lines of credit.

I expect this focus to continue in 2012. Though funding sources have become more readily available, most dealers will be focusing again on generating the capital necessary to run their businesses from their businesses. As always, there will be dealers looking to grow aggressively through borrowing, and rates will continue to make this a very viable option. I don’t see rates rising drastically in the coming year, so it will still be a good time to borrow.

Having said that, I still see it being more difficult to secure new lines of credit in 2012. It’s going to take some patience and the willingness to educate some institutions about our industry.

Our dealer clients saw sales volume increase by almost 6 percent in 2011 despite

a sporadic tax season. Not a record-setting year by any means, but this was driven more by cash management. Dealers seemed to want to sell what their cash flow dictated rather than sell as much as possible. We all know we can sell as many vehicles as we want or have the financial resources to in this industry. There doesn’t seem to be a lack of customers needing or wanting what we have to offer.

The same will hold true for 2012. We should have the customers in the market to sell as much as we want. The biggest question will be inventory availability. Now, I’m normally a glass-half-full kind of guy, but when it comes to this, I think the glass may be half empty. Even though the prices somewhat leveled off the last half of last year, the numbers seem to be dwindling even more than usual.

Portfolio performance in 2011 included some stabilization from a dollar-loss standpoint, but from a number-loss standpoint, there was a slight increase or worsening in 2010. This was driven by a couple of factors, beginning with the need for inventory. Some dealers accelerated their repo times when a desirable unit was involved. This also helped stabilize the dollar losses, as vehicles were repossessed earlier and in better condition and thus earned higher recovery amounts.

The other factor was a renewed focus on underwriting and the overall collection process. Dealers remained more disciplined in both areas, seeking quality over quantity.

There will be more of the same this year. Dealers have seen the error of their past ways and are enjoying the spoils of their more disciplined labor. I expect the average charge-off to remain essentially the same and the number as a percent of sold to remain higher than in past years,

and collections dollars to improve as well as overall collection effectiveness.

The biggest thing to affect our industry in 2012 will come from the compliance front. The Consumer Finance Protection Act was signed in July 2010, establishing the Consumer Finance Protection Bureau. The rules of the Act were to have been drafted by August 2011, so we were hoping to know what kind of field we will be playing on. But, as with most things in our government, the rules are behind schedule. In the interim, I have already heard from a few dealers who have received a letter from the FTC – the Bureau’s governing body – informing them of pending audits.

That has dealers debating whether to remain in the industry, and is causing some who are looking at getting into the industry to delay their entry until the rules are set. This act and bureau are going to separate the men from the boys, so to speak. The dealers who are trying to the best of their ability to do the right things will survive, while those who operate in the gray areas will fall by the wayside. And the waysiders are going to cause the cost of doing business to increase for everyone else.

So here is the best advice I can give to dealers, as well as those wanting to get into the business in the coming year: Don’t wait. Don’t wait to get compliant. Don’t wait to spend a little money to do so. Don’t wait to review all processes and procedures. Don’t wait to review all expenses. Don’t wait to review all of your employees. Don’t wait to train. And definitely don’t wait to sell cars, collect money, and make money.

THE DEALERS WHO ARE TRYING TO THE BEST OF THEIR ABILITY TO DO THE RIGHT THINGS WILL SURVIVE, WHILE THOSE WHO OPERATE IN THE GRAY AREAS WILL FALL BY THE WAYSIDE.

BY BRENT CARMICHAELEXECUTIVE CONFERENCE MODERATOR

NCM ASSOCIATES INC.

MI_0112.indd 12 12/20/11 10:58 AM

WINTER 2012 D R I V E L I N E

13

w w w . m i a d a . o r g

Thank YouEastern Chapter Open HouseSponsorsAlly BankAutoZoneFlint Auto AuctionGenesys SystemsGWC WarrantyLakeside AgencyLoftus & Associates Inc.McLeod Koski AgencyNationwide Acceptance CorporationRoute One

Highlights From the Eastern Chapter

Open House

LocalNews

MI_0112.indd 13 12/20/11 10:58 AM

D R I V E L I N E WINTER 2012

14

w w w . m i a d a . o r g

Plans to cover groups and individuals.

A promise to cover everyone.

We have a broad range of group plan options, including PPO,

Flexible Blue (HSA), HMO, Dental and Vision. We also offer

affordable individual health care for you and your family, at any

stage of your life.

Blues group and individual members have unparalleled statewide

and nationwide access to the doctors and hospitals they need.

We accept everyone, regardless of medical condition and will never

drop your employees for health reasons. Our nonprofit mission

means you can trust us to put your needs first instead of paying

dividends to stockholders. We reinvest in health care for Michigan.

Because Michigan is our home.

For more information, contact:

bcbsm.com MiBCN.com

BCBSM-Half-GroupIHISndColor.indd 1 1/10/08 9:52:30 AM

Michigan Independent Automobile Dealers Association

248-828-7010

SAFEPAK CORPORATION, MAKER OF ELECTRONICALLY monitored deposit stations and ATM security products for banks, is entering the car business with a new line of electronic key control products aimed at dealerships.

SafePak’s Electronic Key Control Systems, priced from $1,995 up, can handle from five to 500 keys. The KeyStations range from from simple wall-mount and countertop varieties to vault-like free-standing kiosks for maximum key security.

SafePak featured its systems at the the recent International Autobody Congress and Exposition and the SEMA show, and the response led the company to add more key control products, SafePak president Buzz Siler said.

“We looked at all the competition’s products in this key management field and saw a huge gap,” he said. “We decided that, with the right investment in the latest technology, we could offer every feature that they did, but at much lower prices.”

Siler previously created the first remote access key dispenser for Cendant/Avis/Budget, a rental kiosk and lock dispenser for the self-storage industry and specialized key dispensers for the aviation and hotel industry.

For more information, visit http://safepakcorp.com/key-control.

Security Is Key as SafePak Adds New Product for Dealers

NewNews

WIN

TER 2

012 D

RIV

ELIN

E

NewADESA Great LakesDCT Marketing & ConsultingDodson GroupDyer Auto BodyEastpointe Car & Gold ExchangeJSJ 7 LLCLakeview Auto LLCMichigan Schools & Government Credit UnionMike Wawee & Sons Auto SalesMonoco Motors LTDQuality Wholesale Cars Inc.Ultimate Used Car Store Inc.Union City Auto SalesUsed Cars.com By Dealix

RenewA & B AutomotiveA.R. GroupAgeless AutosAIS Equipment Co.Andrews AutomotiveAuto CityAuto Group Leasing LLCAuto Salvage AuctionsAutobahn SalesAutohaus Royal OakAutoSave/Charter WarrantyAutosmart AmericaB & B Car Co., Inc.B & B Used CarsBest Deals Auto SalesBig Three Auto Sales Inc.Birmingham Motors LTDBMW MotorsBowen-Fischer Motors Inc.C B R Auto SalesCar Financial Services Inc.Cars.ComCertified MotorsCheboygan Auto Brokers Inc.City of CarsCorepointe Insurance Co.Crandall Auto SalesDick Sova Auto Sales Inc.Don’s Adopt-A-CarDrivers Choice Auto & Truck LLCFlint Auto AutionFS Acceptance LLC

Genesys Systems Inc.Good Motor Company LLCGreat Deal Auto SalesGWC WarrantyHandy Car CleanI-75 AutoInter-City Auto Sales Inc.Joe Ross Used Cars Inc.John Sommerville MotorsKadrich Used CarsKals Auto SalesKals Auto Sales IIKeweenaw Automotive Inc.Koppinger Motors Inc.Lakeland Car Co. LLCLarry’s Used CarsLaw Auto Sales Inc.Low Cost Auto SalesLucky Auto Sales Inc.Majestic Car CompanyMark’s Autos LLCMarty Hart’s Auto SalesMarv’s Car Lot Inc.MD Auto Sales LLCMike’s Car ConnectionMoore VehiclesMt. Morris Auto Sales Inc.Pete’s Auto SalesPrestige Imports West MichiganQuality MotorsR & R Vehicle SalesRandy Merren Auto Sales Inc.Red Cedar Auto SalesRental’s Inc.Richards Motor Sales LTDRick’s Motor Car Co.Rite On Inc.RPM Auto SalesRyan’s Wheels & DealsScotty’s Fine Cars, Inc.Select Motor Cars LLCSelect MotorsSouthfield Quality Cars, Inc.Superior MotorsTom Baker Automotive LLCUnity Motors LLCVan’s Motor Sales Inc.Walt Sicard Car CompanyWilliams Automotive Inc.Wolverine Auto Brokers

WEL

CO

ME

NEW

/REN

EW M

EMBE

RS

MI_0112.indd 14 12/20/11 10:58 AM

WINTER 2012 D R I V E L I N E

15

w w w . m i a d a . o r g

INDEPENDENT DEALERSHIPS NATIONWIDE contribute every day to their communities but often go unrecognized for their community support. While many participate through special projects, others provide sponsorships and financial contributions, or lead innovative community improvement activities.

The NIADA/ Manheim National Community Service Award was created to honor those independent dealerships. Nominees must be members in good standing of the National Independent Automobile Dealers Association and nominations may be made by the dealership, a community business or organization, the state independent automobile dealers association, a community member or even a loyal customer.

Five finalists will be selected, and the winning dealership will be named June 13 at the Leadership Awards Banquet during the Annual NIADA Convention & Expo in Las Vegas. Manheim representatives will present the award, along with a $5,000 check made payable to the dealership’s chosen charity (which must be classified as a charitable organization under section 501(c)(3) of the Internal Revenue Code).

The nomination form can be found by clicking on “Manheim Dealer’s Edge” under the “Services” tab on NIADA.com. Please submit the form, along with the required nomination packet contents, by April 1 to the Community Service Award Selection Committee, NIADA, 2521 Brown Blvd., Arlington, TX, 76006. For additional details please contact Georgia Brown at (800) 756-4232.

NIADA/ Manheim National Community Service Award 2012

Records Retention GuidelinesTHE BEGINNING OF THE TAX YEAR usually triggers a mad scramble to locate all of the necessary documents to prepare tax returns.

If you retain absolutely all of your records, you might be faced with the monumental task of sorting through the mountains of paper to locate the documents you actually need. One occasionally needs to clear away unused items, but tossing the wrong paper or deleting a necessary data file can have dire consequences, especially for a business.

When disposing of documents, you may want to consider shredding.When you establish a records retention policy, some things to consider are:

• Is there a legal requirement for keeping the document?• Could the item serve any other purpose after it is used for its intended

purpose? Would the documents be needed to support or oppose a position in an investigation or litigation? Could the document support a tax deduction?

• What is the consequence of not being able to locate the document?• Can the item be reliably reproduced if needed?• How long should documents be retained?• Keep any document related to pending or threatened litigation until the

matter is settled and all appeals are exhausted.

Here are some general rules for how long to keep other records:One year: Duplicate deposit slips, I-9s (after termination), receiving sheets.Twenty-five months: Customers’ credit applications that were denied.Three years: General correspondence, employment applications, expired

insurance policies, petty cash vouchers.Four years: Freight bills; inventory lists; invoices; bank deposit slips,

reconciliations, statements, canceled checks; contracts – purchase and sales; depreciation records (retention begins after expiration); employee expense reports.

Five years: OSHA logs; photostat, carbon or other facsimile copies of each odometer mileage statement issued or received. Auction companies are required to keep records of the “most recent owner,” presumably the seller, as well as the name of the buyer, the vehicle identification number and the odometer reading on the date the auction company took possession of the motor vehicle.

Six years: Employee payroll records (W-2, W-4, annual earnings records – retention begins after termination).

Seven years: Accident reports; general ledger; accounts payable and receivable ledgers; bank statements; checks (most); contracts and leases (expired); electronic funds transfer documents; employee personnel records (after termination); expense analyses; product, materials and supplies inventories; notes receivable ledgers; purchase orders and time books and cards.

Eleven years: Worker’s compensation documents.Twenty years: Real estate records.Indefinitely: Accountants’ audit reports; cash books; account charts;

construction documents; important correspondence; deeds, mortgages, bills of sale and titles; depreciation schedules; financial statements; general ledgers; journals; licenses; loan documents; minute books of directors and stockholders, including by-laws and charter; property appraisals; articles of incorporation; by-laws; tax returns and worksheets and trademark registrations.

Employee records should be retained for the length of the employee’s tenure with the company, plus at least the statute of limitations period. Employment records may contain sensitive information and should be stored in a secure area. Immigration and Naturalization Services’ I-9 forms should be kept separate from active employee files to avoid discrimination claims.

A copy of each version of employment and training manuals should be kept with the dates that version was in use.

A D D I T I O N A L I N F O R M A T I O N R E G A R D I N G B U S I N E S S R E C O R D S R E T E N T I O N C A N

B E F O U N D A T W W W. I R S . G O V/ P U B / I R S - P D F/ P 5 8 3 . P D F . P E R S O N A L R E C O R D S

R E T E N T I O N I N F O R M A T I O N C A N B E L O C A T E D A T W W W. I R S . G O V/ P U B / I R S - P D F/

P 5 5 2 . P D F .

IndustryUpdate

Learn More

IndustryNews

MI_0112.indd 15 12/20/11 10:58 AM

D R I V E L I N E WINTER 2012

16

w w w . m i a d a . o r g

Member BenefitsMember BenefitsMember BenefitsMember Benefits

Auction Discounts • VIP Auction Discount Cards at auctions throughout

Michigan, Ohio & Wisconsin

Business Savings • FedEx Office • HP business product discounts • OfficeMax product discounts • Biz Filings discounts

Business Utilities Savings • Affiliated Power Purchasers Int’l

Credit Card • NIADA Visa Platinum Credit Card Program

Car Rental Discounts • Hertz • Thrifty

Credit Report Savings • ProCredit Express

Dealership Accounting Tools • NIADA Accounting Manuals

Education & Comradery • Local chapters provide town-hall style meetings,

showcase guest speakers, presentations and compli-mentary meals while networking with member deal-ers and vendors

• Certified Master Dealer Program • NIADA.tv • NIADA’s Annual Conventions, Education and Expo-

sition

Financing Solutions • Auto Portfolio Services, LLC • RouteOne • Smallbiz America • Vehicle Acceptance Corporation • Wolters Kluwer Financial Services

Forms Savings • Mandatory Forms discount program

Hotel Savings • Choice Hotels International

Insurance Products/Savings • Blue Cross Blue Shield of Michigan • Lot Liability & Garagekeepers Insurance program • Dealer bond discounts for qualified members • Berkshire Risk Services • Long Term Care Financial Partners

Internet Search Engine Application • Auto Search Technologies, Inc.

Internet Marketing Solution • Liquid Motors Inc.

Reach the MIADA 24 hours a day, seven days a week at

www.miada.org

Telephone Assistance to members at (248) 828-7010

*Benefits subject to change without notice

Legislative Information • Legislative Representation in Lansing by Public Af-

fairs Associates • Updates on laws and regulations

Parts and Service Discounts • AutoZone

Payment Processing Discounts • Paymaxx Pro • FirstData • Solveras

Prescription Drug Savings • Enhanced Benefits Card

Publications • The Driveline - the official publication of the MIADA • Used Car Dealer Magazine

Retirement Program • NIADA’s Retirement Program administered by NA-

DART

Scholarship Opportunities • Annual Scholarships awarded to eligible family

members on a regional and state-wide basis • NIADA Scholarship Programs

Shipping Services Savings • FedEx • Yellow & Roadway

Skip Tracing • Skip-Tracing & Repossession Assistance on a nation

-wide basis

Software Solutions • Dealer Management System discount program through Genesys Systems Inc.

Telecommunications Discounts • TelSpan Worldwide Conferencing Services • InterCall Audio/Web conferencing discounts

Title/Salvage Verification • CheckThatVIN

Vehicle History Reporting • CARFAX special pricing options

Vehicle Pricing Guide Discounts • Black Book • NADA

Vehicle Sales Leads Service • Dealix Usedcars.com

Vehicle Service Contract Products • Portfolio

Vehicle Transport Service Savings • ShipCarsNow • uShip

Camaraderie

MI_0112.indd 16 12/20/11 10:58 AM

WINTER 2012 D R I V E L I N E

17

w w w . m i a d a . o r g

MI_0112.indd 17 12/20/11 10:58 AM

D R I V E L I N E WINTER 2012

18

w w w . m i a d a . o r g

FORMS AMOUNTS UNIT PRICE QUANTITY TOTAL

RD-108, 4-Part NCR 50 250 500

12.75 60.00 115.00

Imprinted RD-108, black ink 250 500

145.00 205.00

Privacy Forms (Complete FTC Worksheet online at: www.buyadr.com)

100 500

30.00 50.00

FTC Buyers Guide, 2-Part NCR, with adhesive

100 500

15.50 72.50

FTC Spanish Buyers Guide, 2-Pt NCR, with adhesive

100 500

14.00 65.00

Deal Jacket Envelopes 9” x 12”

100 500

22.25 101.25

Odometer Forms 3-Part NCR

100 500

11.75 53.75

“Police” Record Book per book 28.50

MI Retail Purchase Agreements 3-Part NCR

100 500

23.00 100.00

Imprinted MI Retail Purchase Agreement, 3-Part NCR, black ink

500 1000

241.75 341.75

HARDWARE AMOUNTS UNIT PRICE QUANTITY TOTAL

Thumb Screws 50 12.50

Pan Head Screws 100 8.00

Hex Head Screws 100 9.00

Metric Screws 100 8.00

License Plate Magnet, Vinyl Coated each 8.75

BOOKS AMOUNTS UNIT PRICE QUANTITY TOTAL

NADA Used Car Guide 1 book 8.00

NADA Older Car Guide 1 book 30.00

NADA Recreation Vehicle Guide 1 book 45.00

NADA Marine Appraisal Guide (7-100’) 1 book 45.00

NADA Motorcycle-Snowmobile Guide 1 book 30.00

NADA Classic Car Guide Book 1 book 30.00

ADVERTISING SUPPLIES AMOUNTS UNIT PRICE QUANTITY TOTAL

Grease Pencils - Yellow or White each 1.00

“Jumbo Line” Waterbase Markers Fluorescent Colors - Red, White, Pink, Yellow or Blue

each 9.00

“Broad Line” Waterbase Markers Fluorescent Colors - Pink, Green, Yellow or Orange

each 5.00

“Medium Line” Waterbase Markers Fluorescent Colors - White, Red, Yellow, Black or Blue

each 4.00

ADVERTISING SUPPLIES AMOUNTS UNIT PRICE QUANTITY TOTAL

Windshield Numbers Peel & Stick 7-1/2” - Neon Green or Pink: “$”, “0” thru ”9”

per dozen 3.25

Slogan Signs: 15” Neon Green: 0 Down, 4-Cylinder, 4x4, 6-Cylinder, Air Conditioning, All Wheel Drive, Automatic, Certified, Diesel, Down, Extra Clean, Financing Available, Gas Saver, Great Gas Mileage, Lease, Leather, Like New, Loaded, Low Mileage, One Owner, Per Month, Reduced, Sharp, Special, V-8, War-ranty

per dozen 3.50

Year Model Slogan Oval

“2003” Red/Yellow or Green/Black per dozen 7.50

“2004” Red/Yellow or Green/Black per dozen 7.50

“2005” Red/Yellow or Green/Black per dozen 7.50

“2006” Red/Yellow or Green/Black per dozen 7.50

“2007” Red/Yellow or Green/Black per dozen 7.50

“2008” Red/Yellow or Green/Black per dozen 7.50

“2009” Red/Yellow or Green/Black per dozen 7.50

“2010” Red/Yellow or Green/Black per dozen 7.50

“2011” Red/Yellow or Green/Black per dozen 7.50

“2012” Red/Yellow or Green/Black per dozen 7.50

Mirror Tags: Fluorescent Colors: As Advertised, Lease - Pink or Yellow Blank - Green, Red, Pink, Yellow Red Tag Special, Was/Now - Red Sale - Green, Red, Pink, Yellow Special - Green, Red, Pink, Yellow

pack of 50 18.50

Antenna Flags: Fluorescent Colors Yellow, Multi, Red-White-Blue or Red

per dozen 21.00

Antenna Flags: Black & White Checkered per dozen 21.00

American Clip on Flags per dozen 21.00

Pennants: 120 ft. String Multi-Color each 21.00

SUPPLIES AMOUNTS UNIT PRICE QUANTITY TOTAL

Key Tags - Blue Cardboard Yellow Hard Plastic “Versatags” - Red, White, Blue, Green or Yellow

500 250 250

35.00 21.00 27.00

Red/Blue Stock Stickers 100 8.00

Single Edged Razor Blades box of 100 8.00

Metal Scraper each 2.50

Rubber Plate Holders each 12.00

Snow Rakes each 17.00

REV. 11/20/2011 PAGE 1 SUBTOTAL

PAGE 1

□ MasterCard □ VISA □ Discover □ American Express

ADDRESS

Date of Order ADR of Michigan 55 E. Long Lake Rd., PMB 233, Troy, MI 48085

www.buyadr.com 888-855-0100 · Fax: 888-855-7111

NOTE: Payment must accompany your order. MI sales tax will be added to all orders. Prices are subject to change without notice. Please allow 2-3 weeks for customized orders. Make check payable to: ADR of Michigan

SHIP TO NAME

CITY, STATE, ZIP CODE

(AREA CODE) PHONE (AREA CODE) FAX

Credit Card Charge to:

Credit Card Account Number:

Signature (required for credit cards only)

ORDER ONLINE, BY PHONE, FAX, OR MAIL

IS THIS A RESIDENTIAL ADDRESS? YES___ NO___

Available Online at: www.buyadr.com

Billing Address:____________________________________________________________

Name on Card:_____________________________________________________________

Exp. Date:_________________________ Customer Security Code (CSC):_____________

MI_0112.indd 18 12/20/11 10:58 AM

WINTER 2012 D R I V E L I N E

19

w w w . m i a d a . o r g

PAGE 2

ADDITIONAL FORMS AMOUNTS UNIT PRICE QUANTITY TOTAL Customer Proposal - 2 Part: Provides info the dealer-ship needs to complete a transaction.

100 $23.00

Trade-In Vehicle Appraisal - 2 Part: Ensures informa-tion is available to represent vehicle for sale.

100 $23.00

Test Drive Agreement - 2 Part: Obtains important cus-tomer information, including insurance coverage.

100 $23.00

Good Will Repair Acknowledgement - 2 Part: Protects the dealer’s ability with regard to implied warranties.

100 $23.00

Wholesales Purchase Agreement - 2 Part 100 $23.00 Acknowledgement of AS-IS Sale - 2 Part: Verifies that the consumer is satisfied with vehicle & understands the transaction.

100 $23.00

Delivery Confirmation - 2 Part: Verifies that the con-sumer is satisfied with the vehicle and understands the transaction.

100 $23.00

Delivery Confirmation-S: Spanish version of the above form.

100 $23.00

Delivery Confirmation-F: Other foreign language ver-sions of the Delivery Confirmation.

100 $23.00

Interpreter’s Acknowledgement - 2 Part: For use when sale is conducted in language other than English

100 $23.00

Customer Delivery Checklist - 2 Part: Records existing rights and/or responsibilities of the parties.

100 $23.00

Notice to Co-Signer - 2 Part: Discloses the obligations they are undertaking by agreeing to act as a co-signer.

100 $23.00

Insurance Coverage Acknowledgement - 2 Part: Con-firms customer’s obligation to maintain insurance cov-erage.

100 $23.00

F & I Product Confirmation - 2 Part: Confirms which products the consumer purchased.

100 $23.00

Authorization to Release Payoff Info - 2 Part: Dealer-ship can get protected information concerning a lien release.

100 $23.00

Used Vehicle Limited Warranty - 2 Part: Enables the dealership to sell a vehicle with a “Limited” warranty.

100 $23.00

Deposit Receipt - Documents transaction information required to comply with UDAP statutes

200 $21.00

Arbitration Agreement 100 $23.00

Service Loaner Agreement 100 $23.00

Acknowledgement of Voluntary Resign 100 $23.00

SUBTOTAL: PAGE 2

SUBTOTAL: PAGE 1

TOTAL

*FREIGHT

**GRAND TOTAL

MIADA MEMBER DISCOUNT (10%)

* UPS Freight Charge will be added onto order. (for a freight quote, please call)

**Complete Payment Information on the Top of Page 1

Now View Products & Place Orders Online! Visit Us at: www.buyadr.com

www.buyadr.com www.buyadr.com

MI_0112.indd 19 12/20/11 10:58 AM

D R I V E L I N E WINTER 2012

20

w w w . m i a d a . o r g

MI_0112.indd 20 12/20/11 10:58 AM

WINTER 2012 D R I V E L I N E

21

w w w . m i a d a . o r g

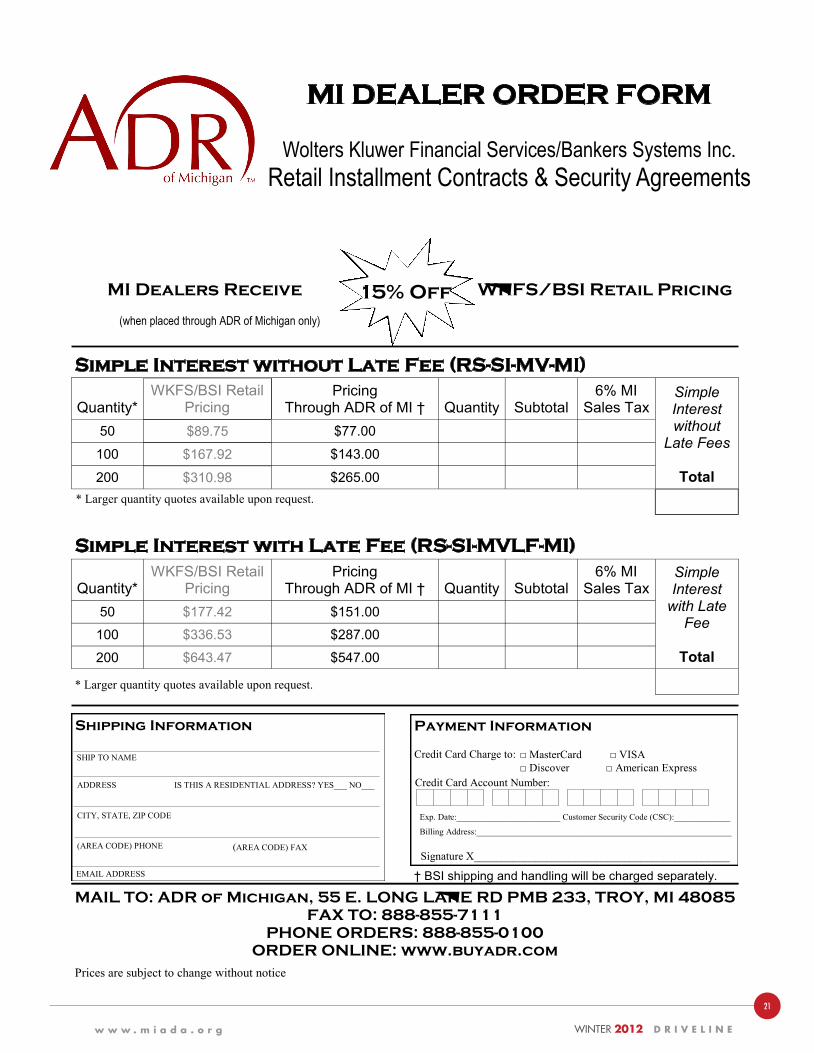

MI DEALER ORDER FORM

Wolters Kluwer Financial Services/Bankers Systems Inc. Retail Installment Contracts & Security Agreements

MI Dealers Receive WKFS/BSI Retail Pricing

(when placed through ADR of Michigan only)

15% Off

Simple Interest without Late Fee (RS-SI-MV-MI)

Quantity* WKFS/BSI Retail

Pricing Pricing

Through ADR of MI † Quantity 6% MI

Sales Tax Simple Interest without

Late Fees

Total

Subtotal 50 $89.75 $77.00

100 $167.92 $143.00

200 $310.98 $265.00

Simple Interest with Late Fee (RS-SI-MVLF-MI)

Quantity* WKFS/BSI Retail

Pricing Pricing

Through ADR of MI † Quantity 6% MI

Sales Tax Simple Interest

with Late Fee

Total

Subtotal 50 $177.42 $151.00

100 $336.53 $287.00

200 $643.47 $547.00

* Larger quantity quotes available upon request.

* Larger quantity quotes available upon request.

Shipping Information

ADDRESS

SHIP TO NAME

CITY, STATE, ZIP CODE

(AREA CODE) PHONE (AREA CODE) FAX

IS THIS A RESIDENTIAL ADDRESS? YES___ NO___

MAIL TO: ADR of Michigan, 55 E. LONG LAKE RD PMB 233, TROY, MI 48085 FAX TO: 888-855-7111

PHONE ORDERS: 888-855-0100 ORDER ONLINE: www.buyadr.com

† BSI shipping and handling will be charged separately.

Prices are subject to change without notice

EMAIL ADDRESS

Payment Information

□ MasterCard □ VISA □ Discover □ American Express

Credit Card Charge to:

Credit Card Account Number:

Signature X______________________________________________

Billing Address:___________________________________________________________

Exp. Date:________________________ Customer Security Code (CSC):_____________

MI DEALER ORDER FORM

Wolters Kluwer Financial Services/Bankers Systems Inc. Retail Installment Contracts & Security Agreements

MI Dealers Receive WKFS/BSI Retail Pricing

(when placed through ADR of Michigan only)

15% Off

Simple Interest without Late Fee (RS-SI-MV-MI)

Quantity* WKFS/BSI Retail

Pricing Pricing

Through ADR of MI † Quantity 6% MI

Sales Tax Simple Interest without

Late Fees

Total

Subtotal 50 $89.75 $77.00

100 $167.92 $143.00

200 $310.98 $265.00

Simple Interest with Late Fee (RS-SI-MVLF-MI)

Quantity* WKFS/BSI Retail

Pricing Pricing

Through ADR of MI † Quantity 6% MI

Sales Tax Simple Interest

with Late Fee

Total

Subtotal 50 $177.42 $151.00

100 $336.53 $287.00

200 $643.47 $547.00

* Larger quantity quotes available upon request.

* Larger quantity quotes available upon request.

Shipping Information

ADDRESS

SHIP TO NAME

CITY, STATE, ZIP CODE

(AREA CODE) PHONE (AREA CODE) FAX

IS THIS A RESIDENTIAL ADDRESS? YES___ NO___

MAIL TO: ADR of Michigan, 55 E. LONG LAKE RD PMB 233, TROY, MI 48085 FAX TO: 888-855-7111

PHONE ORDERS: 888-855-0100 ORDER ONLINE: www.buyadr.com

† BSI shipping and handling will be charged separately.

Prices are subject to change without notice

EMAIL ADDRESS

Payment Information

□ MasterCard □ VISA □ Discover □ American Express

Credit Card Charge to:

Credit Card Account Number:

Signature X______________________________________________

Billing Address:___________________________________________________________

Exp. Date:________________________ Customer Security Code (CSC):_____________

MI_0112.indd 21 12/20/11 10:58 AM

D R I V E L I N E WINTER 2012

22

w w w . m i a d a . o r g

What is Your Agreement?

WHEN IT COMES TO THE AGREED-ON SALES finance terms between a dealer and a buyer, a lot of questions need to be addressed to avoid misunderstandings and, consequently, compliance and legal troubles for a dealership.