Embed Size (px)

Citation preview

FOR INVESTMENT PROFESSIONALS ONLY

M&G (Lux) Absolute Return Bond Fund First quarter 2018 Co-fund managers – Jim Leaviss and Wolfgang Bauer

Quarterly Review

Highlights • The first quarter of 2018 saw the return of volatility, which appeared to be driven by rising US interest rate

expectations and fears of a potential US-China trade war.

• The fund delivered a negative return over the quarter, due primarily to credit market weakness, while performance from government bonds was mixed.

• The fund remains cautiously positioned in terms of interest rate risk, while retaining exposure to selected credit opportunities designed to drive performance over the medium term.

Fund performance

Past performance is not a guide to future performance.

Risks associated with this fund: For any past performance shown, please note that past performance is not a guide to future performance.

The value of investments and the income from them will rise and fall. This will cause the fund price, as well as any income paid by the fund, to fall as well as rise. There is no guarantee the fund will achieve its objective, and you may not get back the amount you originally invested.

The fund may use derivatives with the aim of profiting from a rise or a fall in the value of an asset (for example, a company’s bonds). However, if the asset’s value varies in a different manner, the fund may incur a loss.

The fund may use derivatives to gain exposure to investments exceeding the value of the fund (leverage). This may cause greater changes in the fund’s price and increase the risk of loss.

Further risk factors that apply to the fund can be found in the fund’s Key Investor Information Document (KIID).

Things you should know: The fund allows for the extensive use of derivatives. The fund may invest more than 35% in securities issued by any one or more of the governments listed in the fund prospectus. Such exposure may be combined with the use of derivatives in pursuit of the fund objective. It is currently envisaged that the fund’s exposure to such securities may exceed 35% in the governments of Germany, Japan, UK, USA although these may vary subject only to those listed in the prospectus.

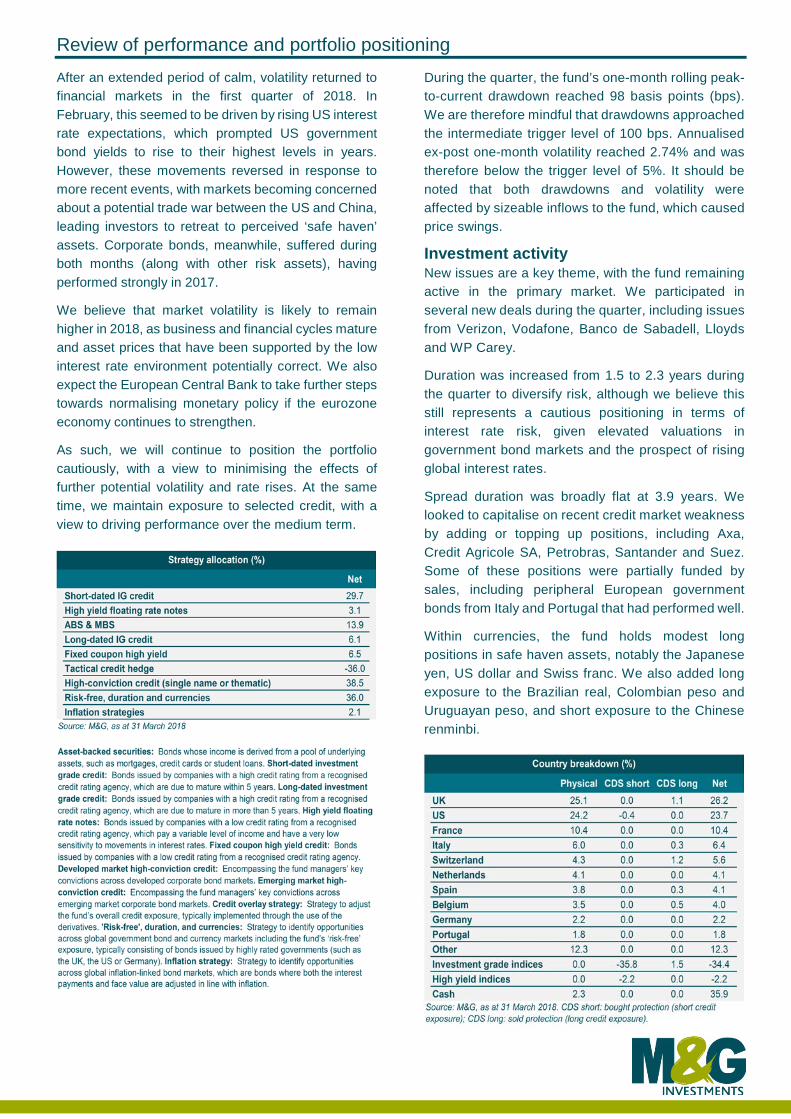

Review of performance and portfolio positioning After an extended period of calm, volatility returned to financial markets in the first quarter of 2018. In February, this seemed to be driven by rising US interest rate expectations, which prompted US government bond yields to rise to their highest levels in years. However, these movements reversed in response to more recent events, with markets becoming concerned about a potential trade war between the US and China, leading investors to retreat to perceived ‘safe haven’ assets. Corporate bonds, meanwhile, suffered during both months (along with other risk assets), having performed strongly in 2017.

We believe that market volatility is likely to remain higher in 2018, as business and financial cycles mature and asset prices that have been supported by the low interest rate environment potentially correct. We also expect the European Central Bank to take further steps towards normalising monetary policy if the eurozone economy continues to strengthen.

As such, we will continue to position the portfolio cautiously, with a view to minimising the effects of further potential volatility and rate rises. At the same time, we maintain exposure to selected credit, with a view to driving performance over the medium term.

During the quarter, the fund’s one-month rolling peak-to-current drawdown reached 98 basis points (bps). We are therefore mindful that drawdowns approached the intermediate trigger level of 100 bps. Annualised ex-post one-month volatility reached 2.74% and was therefore below the trigger level of 5%. It should be noted that both drawdowns and volatility were affected by sizeable inflows to the fund, which caused price swings.

Investment activity New issues are a key theme, with the fund remaining active in the primary market. We participated in several new deals during the quarter, including issues from Verizon, Vodafone, Banco de Sabadell, Lloyds and WP Carey.

Duration was increased from 1.5 to 2.3 years during the quarter to diversify risk, although we believe this still represents a cautious positioning in terms of interest rate risk, given elevated valuations in government bond markets and the prospect of rising global interest rates.

Spread duration was broadly flat at 3.9 years. We looked to capitalise on recent credit market weakness by adding or topping up positions, including Axa, Credit Agricole SA, Petrobras, Santander and Suez. Some of these positions were partially funded by sales, including peripheral European government bonds from Italy and Portugal that had performed well.

Within currencies, the fund holds modest long positions in safe haven assets, notably the Japanese yen, US dollar and Swiss franc. We also added long exposure to the Brazilian real, Colombian peso and Uruguayan peso, and short exposure to the Chinese renminbi.

276307_293609