Embed Size (px)

Citation preview

©2014 Kansas City Southern

Mexico: Business Climate Update

and Port Expansion Review

Pat Ottensmeyer, EVP & CMO

©2014 Kansas City Southern 2

KCS Rail Network

©2014 Kansas City Southern

Founded in 1887, KCS is a 127

year old growth story

More than 6,400 track miles

Seamless network in and out of

Mexico

Service to 12 Gulf ports and 1

Pacific Ocean port

Service to more than 140 transload

centers and 11 intermodal ramps

©2014 Kansas City Southern

The New York Times

3

How Mexico Got Back in the

Game

Mexico: The New China

“That’s because the TJ template

isn’t so much about outsourcing

as it is quicksourcing. And that’s

also the way to create

thousands of good jobs in the

United States.

As any entrepreneur can tell

you, the shorter and more

nimble a supply chain is, the

better.”

By Chris Anderson

By Thomas L Friedman

“That’s because the TJ template

isn’t so much about outsourcing

as it is quicksourcing. And that’s

also the way to create

thousands of good jobs in the

United States.

As any entrepreneur can tell

you, the shorter and more

nimble a supply chain is, the

better.”

“Chrysler, for example, is using

Mexico as a base to supply some of

its Fiat 500s to the Chinese market.”

What struck me most here in

Monterrey, though, is the number of

tech start-ups that are emerging from

Mexico’s young population — 50

percent of the country is under 29 —

thanks to cheap, open source

innovation tools and cloud

computing.”

http://www.nytimes.com/2013/02/24/opinion/sunday/friedman-

how-mexico-got-back-in-the-game.html

http://www.nytimes.com/2013/01/27/opinion/sunday/the-tijuana-

connection-a-template-for-growth.html?hp&_r=0

©2014 Kansas City Southern

Foreign Direct Investment (FDI) in Mexico

4

• 2013 Foreign Direct

Investment (FDI) reached

$39.2 Billion (120%

increase vs 2012)

• Manufacturing sector

was key in 2013 with

72.3% investments

• 85% of FDI was registered

on states where KCS has

access

• 2014 FDI trough June

reached $9.7 Billion.

– 71.8% manufacturing .

• From 2000 to 2014 FDI

accounts $354.3 BillionElaboration by KCS Market Research based on Secretaría de Economía de México.

Data includes all economic sectors. (2013 & 2014 FDI)

©2014 Kansas City Southern

Why are decision makers

looking at Mexico?

5

©2014 Kansas City Southern 6

Economic Growth

SOURCE: DOC, Bloomberg Businessweek, World Bank, Mexico Today, J.P. Morgan, U.S. Bureau of

Labor Statistics, SICE, Goldman Sachs, Boston Consulting Group, Reuters., IMF

-6%

-4%

-2%

0%

2%

4%

6%

2006 2007 2008 2009 2010 2011 2012 2013 2014e 2015e

Annual GDP Growth Rate

US Mexico

Mexico has a projected growth

rate of 4% for 2013–2019,

According to the U.S.

Department of State’s Bureau of

Economic and Business Affairs

©2014 Kansas City Southern

GuatemalaEl SalvadorHondurasNicaraguaCosta RicaColombiaBoliviaChileUruguayPeruVenezuela

Japan

European UnionIcelandLiechtensteinNorwaySwitzerlandIsrael

Canada

United States

Trade Growth

The U.S. is Mexico’s largest trading partner

U.S. imports from Mexico have risen 23.5% since 2010

SOURCE: DOC, Bloomberg Businessweek, World Bank, Mexico Today, J.P. Morgan, U.S. Bureau of

Labor Statistics, SICE, Goldman Sachs, Boston Consulting Group, Reuters

©2014 Kansas City Southern

80

85

90

95

100

105

110

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

Se

pte

mb

er

2004

Novem

ber

2004

Jan

uary

2005

Ma

rch 2

005

Ma

y 2

005

July

2005

Se

pte

mb

er

2005

Novem

ber

2005

Jan

uary

2006

Ma

rch 2

006

Ma

y 2

006

July

2006

Se

pte

mb

er

2006

Novem

ber

2006

Jan

uary

2007

Ma

rch 2

007

Ma

y 2

007

July

2007

Se

pte

mb

er

2007

Novem

ber

2007

Jan

uary

2008

Ma

rch 2

008

Ma

y 2

008

July

2008

Se

pte

mb

er

2008

Novem

ber

2008

Jan

uary

2009

Ma

rch 2

009

Ma

y 2

009

July

2009

Se

pte

mb

er

2009

Novem

ber

2009

Jan

uary

2010

Ma

rch 2

010

Ma

y 2

010

July

2010

Se

pte

mb

er

2010

Novem

ber

2010

Jan

uary

2011

Ma

rch 2

011

Ma

y 2

011

July

2011

Se

pte

mb

er

2011

Novem

ber

2011

Jan

uary

2012

Ma

rch 2

012

Ma

y 2

012

July

2012

Se

pte

mb

er

2012

Novem

ber

2012

Jan

uary

2013

Ma

rch 2

013

Ma

y 2

013

July

2013

Se

pte

mb

er

2013

Novem

ber

2013

Jan

uary

2014

Ma

rch 2

014

Ma

y 2

014

July

2014

US

In

du

str

ial P

rod

uc

tio

n In

de

x (

ad

jus

ted

)

To

tal T

rad

e w

ith

Me

xic

o (

$ b

illi

on

)

Total Trade with Mexico ($ billions) US Industrial Production Index (adjusted)

U.S. – Mexico Trade Growth

8

Source: Board of Governors of the Federal Reserve System and US Census Bureau

©2014 Kansas City Southern

Labor Force

9

Mexico has a labor force advantage over China

– By 2015, wages in Mexico are forecasted to be 30% lower than in China

– Mexican labor is highly skilled; Mexico manufacturing is moving from low-skill, high volume

products to high-skill, sophisticated products

©2014 Kansas City Southern

0

2

4

6

8

10

12

14

16

18

Dec-0

0

Ap

r-01

Au

g-0

1

Dec-0

1

Ap

r-02

Au

g-0

2

Dec-0

2

Ap

r-03

Au

g-0

3

Dec-0

3

Ap

r-04

Au

g-0

4

Dec-0

4

Ap

r-05

Au

g-0

5

Dec-0

5

Ap

r-06

Au

g-0

6

Dec-0

6

Ap

r-07

Au

g-0

7

Dec-0

7

Ap

r-08

Au

g-0

8

Dec-0

8

Ap

r-09

Au

g-0

9

Dec-0

9

Ap

r-10

Au

g-1

0

Dec-1

0

Ap

r-11

Au

g-1

1

Dec-1

1

Ap

r-12

Au

g-1

2

Dec-1

2

Ap

r-13

Au

g-1

3

Dec-1

3

Ap

r-14

Au

g-1

4

Peso & Yuan Exchange Rate

MXN

CNY

10

Currency Advantage

Source: YCharts

In U.S. dollar terms, since 2005 Chinese products have become about 65% more expensive than those sourced in Mexico

©2014 Kansas City Southern 11

Top Industries for Nearshoring Opportunities

Appliances &

Electronics

Construction

Equipment

Automotive

Furniture

Machinery

Aerospace

High Tech Electronics

Rubber & Plastics

Fabricated

Metals

©2014 Kansas City Southern

Global Automotive Production

©2014 Kansas City Southern©2014 Kansas City Southern

PLANT TIJUANAPLANT

HERMOSILLO PLANT

CHIHUAHUA

PLANT MOTORS

RAMOA ARIZPE

PLANT

SALTILLO

PLANT

SALTILLO

PLANT

RAMOS

ARIZPE

PLANT S.L.P PLANT

MORELOS

PLANT

PUEBLA

PLANT CUATITLANPLANT TOLUCAPLANT TOLUCAPLANT MOTORSPLANT SILAOPLANT CELAYA

PLANT SALAMANCA

PLANT EL SALTO

PLANT

AGUASCALIENTES

PLANT

AGUASCALIENTES

PLANT AUDI 2016

KIA

MONTERREY

2016

PLANT 2017

AGUASCALIENTES

PLANT S.L.P

2019

©2014 Kansas City Southern

New Auto Plant Openings

14

Source: (1) Autocast, June 2014 – Audi (Est. 2017 production)

(2) Manufacturer’s Press Releases

AUDISan Jose Chiapa,

Puebla, Mexico

Opens 2nd Quarter 2016 (1)

Est. Prod Capacity: 173K (1)

BMWSan Luis Potosi, Mexico

Opens 2019 (2)

Est. Prod Capacity: 150K (2)

MERCEDES BENZ/INFINITIAguascalientes, Mexico

Opens 2017 (2)

Est. Prod Capacity: 300K (2)

KIAPesqueria (Monterrey), Mexico

Opens Mid 2016 (2)

Est. Prod Capacity: 300K (2)

©2014 Kansas City Southern 15

By 2019, Mexico’s Auto ProductionExpected to Increase by 1 Million Units

Source: Autocast, September 2014

2014

2015

2016

2017

2018

2019 4.4m

4.2m

4.0m

3.7m

3.3m

3.2m

©2014 Kansas City Southern 16

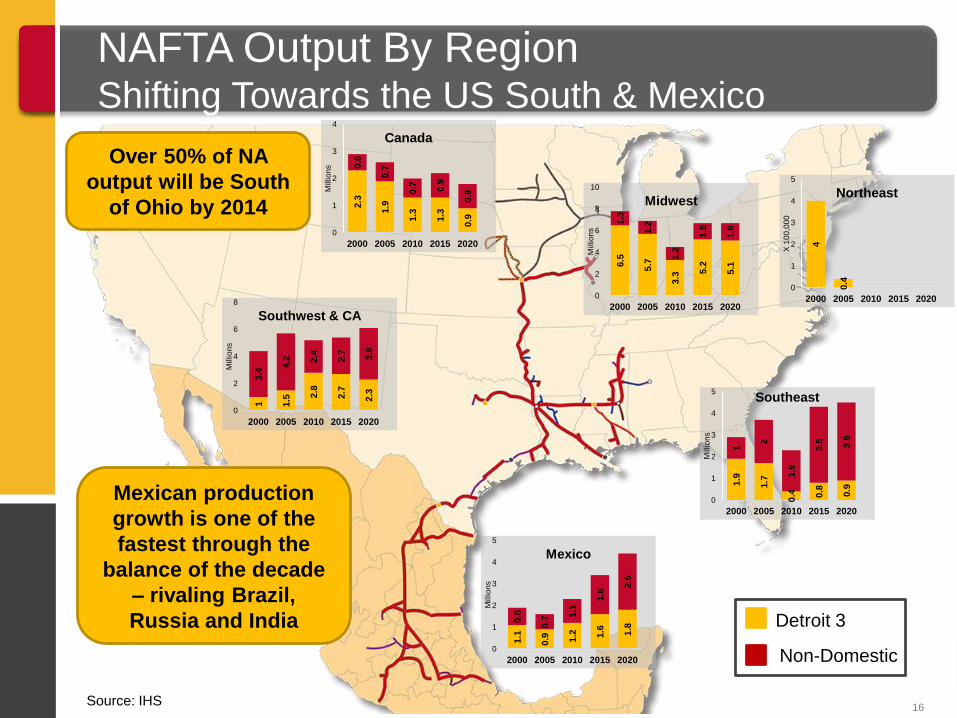

NAFTA Output By RegionShifting Towards the US South & Mexico

Mexican production

growth is one of the

fastest through the

balance of the decade

– rivaling Brazil,

Russia and India

Over 50% of NA

output will be South

of Ohio by 2014

1.1

0.9 1.2 1.6 1.8

0.8

0.7

1.1

1.8

2.6

0

1

2

3

4

5

2000 2005 2010 2015 2020

Millio

ns

Mexico

1.9

1.7

0.4 0.8 0.9

1

2

1.9

3.5 3.6

0

1

2

3

4

5

2000 2005 2010 2015 2020

Millio

ns

Southeast

4

0.4

0

1

2

3

4

5

2000 2005 2010 2015 2020

X 1

00

,00

0

Northeast

2.3

1.9

1.3

1.3

0.9

0.6

0.7

0.7 0.9

0.9

0

1

2

3

4

2000 2005 2010 2015 2020

Millio

ns

Canada

6.5

5.7

3.3

5.2

5.1

1.3

1.2

1.2

1.5

1.6

0

2

4

6

8

10

2000 2005 2010 2015 2020

Millio

ns

Midwest

1 1.5 2

.8

2.7

2.3

3.4

4.2 2

.4

2.7 3.8

0

2

4

6

8

2000 2005 2010 2015 2020

Millio

ns

Southwest & CA

Source: IHS

Detroit 3

Non-Domestic

©2014 Kansas City Southern 17

Automotive Production Has a Large Freight

“Funnel”

©2014 Kansas City Southern

Cross-border truck shipments represent a

significant opportunity for KCS

3.1 million truckloads originate

or terminate in KCS’ Target

Market

50 percent of loads move

to/from locations deep into

Mexico

KCS operates the Laredo rail

bridge on both sides of border

The current KCS intermodal

cross border market share

represents less than 3% of

available market.

18

SOURCE: KCS Market Research derived from BTS Data

©2014 Kansas City Southern

Cross Border Intermodal Coverage

19

Kansas City

Southern covers

60 percent of

Mexico’s

population

and

63 percent of

Mexico’s GDP.

Source: INEGI Censo de Población y Vivienda 2010

©2014 Kansas City Southern

KCS’s Network is the center of the North

American rail system

20

Laredo

Houston

Dallas

Shreveport

East St. Louis

Springfield

Kansas City

Birmingham

Meridian

New Orleans

Jackson

©2014 Kansas City Southern

Mexico Energy Reform is a Reality

21

Reform could drive an increase in

rail shipments in the following ways:

• General economic growth in Mexico

• Increased movement of steel tubing,

frac sand, fuel oil, diesel, gasoline,

LPG and shale oil

• Dec. 2013 – Mexico passed energy

reform legislation in the constitution

• Reform will affect refining, oil & gas

drilling, power generation and new

private-sector driven logistics market

• Laws and regulations associated with

this reform will be decided during

2014

©2014 Kansas City Southern 22

Mexico’s Natural Gas Potential

©2014 Kansas City Southern

1. Importation and intra-Mexico movement of steel pipe for oil fields and natural gas

transmission

New natural gas pipelines are under construction

2. Increased Fuel Oil Moves

KCS current transports fuel from Pemex refineries to export

Energy reform has opened the door to private sector participation in

terminals and more flexible contract guidelines

3. Importation of LPG

Deficit of LPG in Central Mexico

Specialized rail terminal in SLP has been permitted and construction will

begin in 1Q 2015

4. Importation of refined products (gasoline, diesel & biofuels)

Demand is increasing in Mexico

Refining capacity is insufficient

Strategic facilities and partners are being identified

5. Importation of frac sand

6. Shale oil (CBR) shipments from Mexican basins

23

Potential New Business Opportunities Resulting

from Mexican Energy Reform

©2014 Kansas City Southern

Mexico Port Expansions

24

©2014 Kansas City Southern

Pacific

Gulf

Lazaro Cardenas

Manzanillo

Progreso

Veracruz

Altamira

Ensenada

Others

Source: SCT 2013 Data

31%

69%

TEU Distribution per Port 20134,892,881 TEU*

1%

1%

3%

43%

22%

12%

18%

TEU Distribution 20134,892,881 TEU*

Ensenada

Altamira Progreso

Veracruz

Lazaro Cardenas

Manzanillo

Mexico Overview – Container Ports

25

©2014 Kansas City Southern

Expansion of the specialized container terminal &

improvement of technology

26

Port of Manzanillo

Picture: Manzanillo Port Authority, Inc.

Six year

investment of

$200M

Terminal will

increase

capacity to 4

million TEUs.

Source: Mexican PNI (Plan nacional de infraestructura)

©2014 Kansas City Southern

Total Investment - $820M

Will provide better access

via rail and highway

1st port in Latin America

with a deep-water area for

oil rigs & oil platforms

Will also include a station

to compress natural gas

27

Port of Altamira

Source: Mexican PNI (Plan nacional de infraestructura

Photo: Administración Portuaria Integral de Altamira

Expansion started in 2013 and will be completed in 2018

©2014 Kansas City Southern

Total investment - $4.6B

– $1.8B will be invested

between 2013 and

2018.

Will reduce congestion

by tripling capacity

Revival of older areas of

the port which will

integrate it into the

historic part of the city.

28

Port of Veracruz

Photo: International Transport Workers’ Federation

Source: Mexican PNI (Plan nacional de infraestructura)

Expansion started in 2013 and will be completed in 2030.

©2014 Kansas City Southern 29

Port of VeracruzFull Build Out (2030)

Source: SCT

©2014 Kansas City Southern

Lázaro Cárdenas Development Plans

30

• APM Terminals will invest $900m in the project. The new container port will have a

capacity of 1.2 million TEUS when opened and projected volume of +3 million TEUS by

2019. Projected completion is 1st half of 2016.

• In October 2012, SSA Marine won a concession to develop, operate and maintain a

Specialized Auto Terminal capable of handling up to 750,000 autos annually

• Hutchinson Port Holdings installed six new vessel cranes at Lazaro over the past two

years.

Source: APM Terminals Press Release dated October 9, 2014; sct.gob.mx

©2014 Kansas City Southern 31

Lázaro Cárdenas

Growth Plans

Bulk

Facility

New Container

Terminal

New Auto

Terminal

Expanded

Container Terminal

©2014 Kansas City Southern

West Coast Ports… Which

One Looks Different?

32

©2014 Kansas City Southern 33

Prince Rupert

©2014 Kansas City Southern

Vancouver

34

©2014 Kansas City Southern 35

Seattle

©2014 Kansas City Southern 36

Oakland

©2014 Kansas City Southern 37

LA/Long Beach

©2014 Kansas City Southern 38

Manzanillo

©2014 Kansas City Southern

Lázaro Cárdenas

39

©2014 Kansas City Southern 40

Thank you!