Embed Size (px)

DESCRIPTION

Complete survey of Mercedes Benz Sale report

Citation preview

A deliverable sales strategy forMercedes-Benz Claremont

Jaco van Zyl

Mini-research report

presented in partial fulfilment

of the requirements for the degree of

Master of Business Administration

at the University of Stellenbosch

Supervisor: Dr. J. Smith

Degree of confidentiality: A December 2009

ii

Declaration

By submitting this research report, I, Jaco van Zyl, declare that the entirety of the work

contained herein is my own, original work, that I am the owner of the copyright thereof

(unless to the extent explicitly otherwise stated) and that this document has not previously

in its entirety or in part been submitted at any university in order to obtain an academic

qualification.

J. van Zyl 13 March 2009

Copyright © 2009 University of Stellenbosch

All rights reserved

iii

Acknowledgements

I would like to extend my sincerest gratitude to Keith Steele, dealer principle at Mercedes-

Benz Claremont: A true gentleman whose guidance over the last couple of months has

taught me so much about business, philosophy and life. I can never thank you enough.

I would also like to thank my all my friends who always keep reminding me that life is fun

and should be lived flat out.

Finally, I would like to dedicate this work to my mother, who taught me never to give up,

my father for his fatherly mentorship and to my brother for just being a cool guy.

I thank you all for inspiring me to be all that I can be. Your constant motivation and support

kept me going, when at times, the end of this course seemed so far away.

Bless you all!

iv

Abstract

The economic downturn in South Africa since mid 2008 has transformed the motor vehicle

industry into a seriously competitive marketplace. Both large and small dealerships are

finding their volumes and margins under increasing pressure.

Sandown Motor Holdings (Pty) Ltd has a new vision to become the finest motor group in

the world. An openness to ideas and to the external environment in the learning

organisation means that it can excel by exceeding customer expectations’ and

benchmarking against the best in the class (Clarke & Clegg, 2000:5). In this light,

Sandown Motor Holdings needs to adopt certain strategies, policies and practices that

allows for the implementation of new ideas and quick reactions to changes in the external

environment. They need to know what customer expectations are and then exceed them

to enable Sandown Motors to make this vision a reality.

This research report analyses the external and internal environment of Sandown Motor

Holdings (Pty) Ltd in the Western Cape in an attempt to gain insight into the realities facing

the company. The report becomes more focused on Mercedes-Benz Claremont as a

dealership and its pre-owned vehicle sales department as the key department which

serves as an outlet for trade-in pressures, but also as a profit centre which needs to be

developed. Much work is done around market segmentation, product profiling and trading

policies that would positively influence both pre-owned and new vehicle sales.

The pre-owned strategy that emerges also highlights the necessity for an e-commerce

strategy to serve as another platform from which to trade even more pre-owned vehicles.

This strategy specifically aims to establish an online auction system open to traders only.

The report concludes by taking a look at the new vehicle sales department.

The approach taken is customer centric and relies heavily on the customer experience as

a source of competitive advantage over competitors. Processes and performance

indicators are reviewed and an action plan is compiled and put in place. A detailed twelve-

month marketing plan is also developed and is included as an appendix.

The author believes these strategies are crucial for short-term profitability, long-term

survival and the satisfaction of all stakeholders.

v

Opsomming

Die ekonomiese afplatting in Suid-Afrika sedert die middel van 2008 het die motor-

industrie in ‘n streng kompeterende arena omskep. Beide groot en klein handelaars

ondervind toenemende druk op hulle volumes en winsmarges.

Sandown Motor Holdings (Pty) Ltd het ‘n nuwe visie om die beste motorgroep ter wêreld te

word. ‘n Openheid teenoor idees oordie eksterne omgewing in die leergierige organisasie,

beteken dat dit kan presteer deur kliënteverwagtinge te oortref en hulself te kan meet teen

die beste in die klas (Clarke & Clegg, 2000:5). In die lig hiervan moet Sandown Motor

Holdings sekere strategieë, beleidsrigtings en praktyke aanvaar wat die implementering

van nuwe idees en vinnige reaksie op veranderinge in die eksterne omgewing moontlik

maak. Hulle moet weet wat die kliënte se verwagtinge is en dit dan oortref ten einde

Sandown Motors se visie ‘n realiteit te maak.

Hierdie navorsingsverslag analiseer die eksterne en interne omgewing van Sandown

Motor Holdings (Pty) Ltd in die Wes-Kaap in ‘n poging om insig te verkry in die realiteite

wat die maatskappy in die oog staar. Die verslag fokus op Mercedes-Benz Claremont as ‘n

alleenstaande handelaarskap en sy Gebruikte-Voertuie Verkoopsafdeling as die

sleuteldepartement wat dien as ‘n uitlaat vir inruil druk, maar ook as ‘n winssentrum wat

verder ontwikkel moet word. Baie werk is gedoen rondom marksegmentasie,

produkprofiele en handelsbeleid wat positiewe impak op beide nuwe en gebruikte verkope

sal hê.

Die gebruikte-voertuig strategie wat hieruit spruit beklemtoon verder die behoefte aan ‘n

webgebaseerde strategie wat as ‘n verdere afsetpunt kan dien vir nog meer gebruikte-

voertuie verkope. Hierdie strategie is spesifiek gemik op die daarstel van ‘n op-tyd aanlyn

veilingstelsel, uitsluitlik vir die gebruik van motorhandelaars. Die verslag sluit af deur te kyk

na die Nuwe-Voertuig Verkoopsafdeling.

Die benadering wat gevolg word is kliëntgesentreerd en berus op die kliënt se ervaring as

‘n bron van kompeterende voordeel bo die kompetisie. Prosesse en indikators om

prestasie te meet word hersien en die nodige aksieplan word opgestel en toegepas. ‘n

Gedetaileerde twaalf-maande bemarkingsplan is ook ontwikkel en word ingesluit in die

aanhangsels.

vi

Die skrywer glo hierdie strategieë is krities vir korttermyn winsgewendheid, langtermyn

oorlewing en die bevrediging van alle belanghebbendes.

vii

TABLE OF CONTENTS

Page

Declaration ii

Acknowledgements iii

Abstract iv

Opsomming v

List of tables x

List of figures x

List of appendices x

List of acronyms and abbreviations xi

CHAPTER 1: INTRODUCTION 81.1 Brief introduction to the company 8

1.2 Management role of the author in the company 8

1.3 Background setting to the objective of the report 8

1.4 Research design and methodology 8

1.5. Framework for the proposed study 8

1.6 Provisional list of sources 8

CHAPTER 2: DEVELOPING A STRATEGY FOR CLAREMENT PRE-OWNED 82.1 Background on Mercedes-Benz Claremont 8

2.2 Strategy defined 9

2.3 Origin of Claremont’s strategic positioning 11

2.4 Product profile 8

2.4.1 Buying preferences of the target market 8

2.4.2 Competitors 8

2.4.3 Availability of certain vehicle (product) lines 8

2.5 Optimum stock levels 8

2.6 The product mix 8

2.7 Buying policy 8

2.8 Selling (wholesaling) policy 8

2.9 Human capital 8

2.10 Processes 8

viii

CHAPTER 3: DEVELOPING AN E-COMMERCE STRATEGY TO SUPPORT THEMERCEDES PRE-OWNED EFFORT 8

3.1 Introduction 8

3.2 Porter’s approach 8

3.3 Sandown Motor Holdings overall strategy 8

3.4 Industry structure 8

3.5 Competitive positioning 8

3.5.1 SMH strengths 8

3.5.2 SMH weaknesses 8

3.5.3 SMH threats 8

3.6 Achieving sustainable competitive advantage 8

3.7 Strategy formulation 8

3.8 Taking the resource-based view on the situation 8

3.9 The strategy 8

3.10 The value proposition 8

3.11 Stakeholders 8

3.12 Key resources to be mobilised 8

3.13 The customer interface 8

3.14 The 7C’s of the customer interface 8

3.15 Technology and software required 8

3.16 Marketing 8

3.17 Customer screening 8

3.18 The auction process in more detail 8

3.19 Risks and possible pitfalls 8

3.20 Final remarks around e-commerce for SMH 8

CHAPTER 4: CLAREMONT NEW VEHICLE SALES STRATEGY 84.1 Introduction 8

4.2 Passenger car performance overview 8

4.2.1 Interest rate overview against sales performance 8

4.2.2 Other monetary policy and legislative factors to note 8

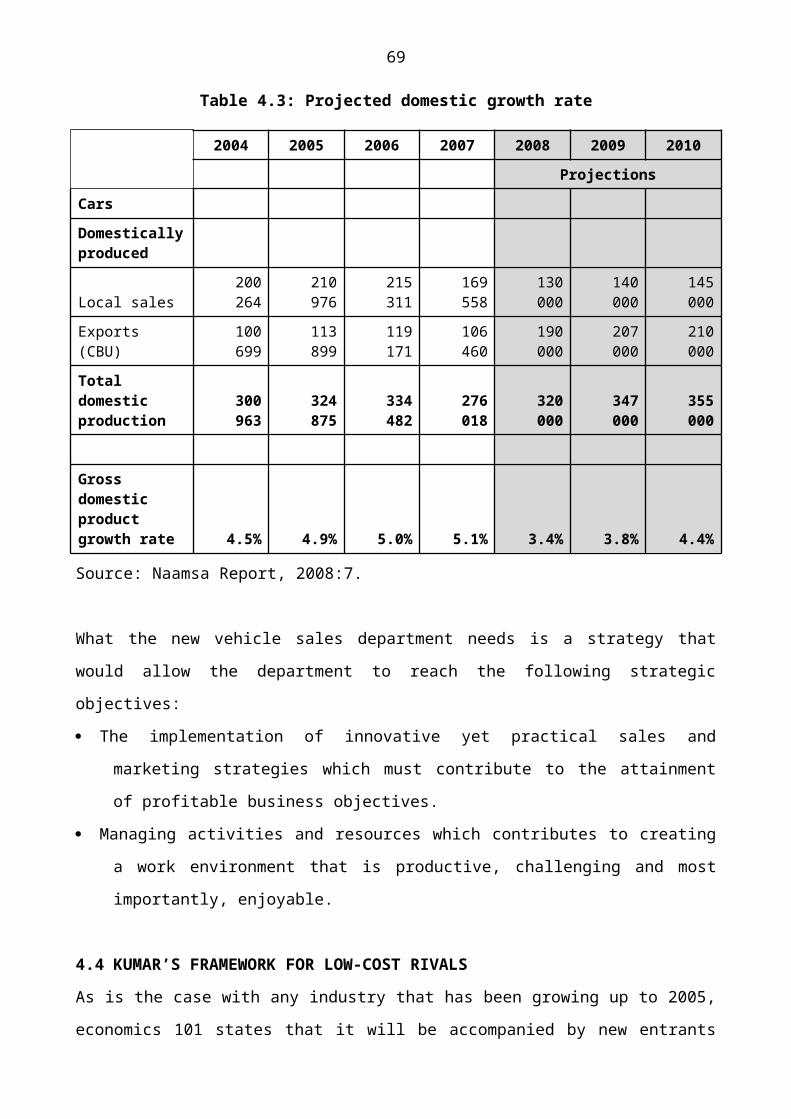

4.3 The next 12 to 24 months 84

4.4 Kumar’s framework for low-cost rivals 86

4.5 Turning Kumar’s strategy into a Claremont reality 89

4.6 Strategy execution 8

ix

4.7 Key objectives and related activities 53

4.7.1 First impressions 54

4.7.2 Daily activities and processes 55

CHAPTER 5: CONCLUSION 8

LIST OF SOURCES 8

x

List of tables

Table 1.1 : Sandown Motor Holdings (Pty) Ltd Shareholding 1

Table 2.1 : Gross profit contributions by department 7

Table 2.2 : Product profile by model and rand value 16

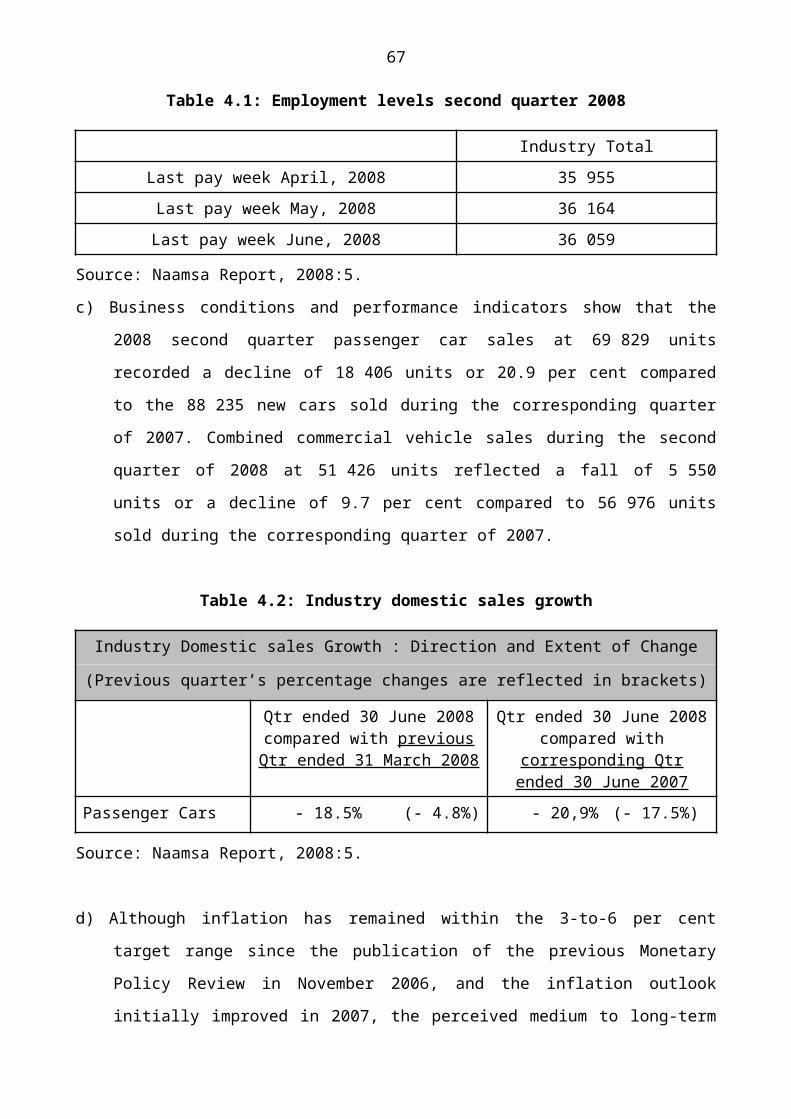

Table 4.1 : Employment levels second quarter 2008 44

Table 4.2 : Industry domestic sales growth 45

Table 4.3 : Projected domestic growth rate 46

Table 4.4 : Goal setting 57

Table 4.5 : Tactics to be employed 58

List of figures

Figure 2.1 : Moving beyond the beachhead: Exotic vehicles 15

Figure 2.2 : Bar Chart: Number of units per model 17

Figure 2.3 : Bar Chart: Stock value by model 17

Figure 2.3 : C@ps Model 23

Figure 4.1 : Vehicle sales over time 43

Figure 4.2 : Kumar’s framework to respond to low-cost rivals 48

List of appendices

Appendix A : Screenshots of e-commerce competitors 64

Appendix B : Projected cash flow forecast for e-commerce 67

Appendix C : Interest rate changes over time 68

Appendix D : Mercedes-Benz Claremont detailed marketing plan 72

xi

List of acronyms and abbreviations

CC close corporation

CEO chief executive officer

CRM customer relationship management

CSI corporate social investment

EFT electronic funds transfer

F&I Finance and Insurance (representative)

FCPA Foreign Corrupt Practices Act

IT information technology

LSM Living Standards Measurement

MBSA Mercedez-Benz South Africa

MPC Monetary Policy Committee

NAAMSA National Automobile Association of Manufacturers of South Africa

NCA National Credit Act

NYSE New York Stock Exchange

PC passenger car

SA South Africa(n)

SARB South African Reserve Bank

SARS South African Receiver of Revenue

SMH Sandown Motor Holdings (Pty) Ltd

SMS short message service

VAPs value-added products

VAT value-added tax

1

CHAPTER 1INTRODUCTION

1.1 BRIEF INTRODUCTION TO THE COMPANYSandown Motor Holdings (Pty) Ltd (hereinafter referred to as SMH) is a large motor group

controlling various dealerships across the country. Most notably SMH owns franchises

associated with Daimler-Chrysler brands such as Mercedes-Benz, Chrysler, Jeep, Dodge

and Mitsubishi.

SMH had its roots in the Gauteng Province under the guidance of its founder Mr. Roy

McAlister who, to date, still actively manages the group. Through rapid acquisitions, SMH

has grown to a well-respected organisation with operations that can be classified as being

SMH Gauteng and SMH Western Cape.

Table 1.1: Sandown Motor Holdings (Pty) Ltd Shareholding

Daimler Chrysler (Pty) Ltd 50.1% of issued shares

Roy McAllister 9.9% of issued shares

True Class Consortium 2 (Pty) Ltd 40% of issued shares

Total 100 % of issued shares

Source: Interview with Roy Marcus, FD: Passenger Cars

In 2002 DaimlerSA purchased the majority shareholding in SMH, which makes SMH quite

a rare occurrence. Manufacturers rarely become involved with dealership shareholding.

2007 saw SMH entering into a black economic empowerment deal with the TrueClass

Consortium by selling 40 per cent shareholding. DaimlerSA in turn, is owned by Daimler

AG, which is noted on the New York Stock Exchange (NYSE). This implies that SMH has

to conform to the Foreign Corrupt Practices Act (FCPA) as is expected of all companies

whose holding companies are listed in the NYSE. SMH quickly developed from an owner-

managed business to a fully-fledged corporate. This transformation to becoming a

corporate has not been without teething problems and has forced SMH to revise its

corporate governance to stay within the regulations set forth by the FCPA and the new

National Credit Act. To drive this down to the operational level, this revised corporate

governance model had to set more stringent boundaries especially relating to the

delegation of authority.

2

As can be expected by such change, middle and even senior management greatly resisted

these changes. The new governance model now restricts their decision-making powers

and diminishes their ability to operate quickly and decisively.

SMH has operated in the Western Cape for the last forty years and currently employs 683

people. Port Elizabeth is also included under SMH Western Cape even though it is located

in the Southern Cape. Mr. Owen E. Bell acts as Managing Director for SMH Western Cape

and is regarded as an icon in the Cape motor industry.

Western Cape dealerships include:

Mercedes-Benz Century City;

Eikestad Motors;

Orbit Boland;

Orbit Culemborg;

Mercedes-Benz Claremont;

Mitsubishi Port Elizabeth;

Chrysler Century City;

Mitsubishi Tygerberg;

Paarl Motors (the most recent acquisition).

The projected annualised turnover for SMH Western Cape is R2.2 billion and can be

broken down into the following business lines and their percentage contribution to

turnover:

75% new and pre-owned vehicle sales;

6% parts sales;

10% vehicle servicing;

3% finance and insurance operations;

2% driveway sales;

4% other.

The above percentages clearly illustrate that SMH is largely driven by vehicle sales, which

at 75 per cent of total turnover, is considered to be its core business. It therefore makes

sense to assume that the Board of Directors place great emphasis on sales and that it lies

at the centre of company strategy.

3

1.2 MANAGEMENT ROLE OF THE AUTHOR IN THE COMPANY The author of this research report, Jaco van Zyl, is a 29-year old male and has been

involved in the motor vehicle industry since June 2003. In January 2005, he started as a

sales executive with one of SMH’s Mercedes-Benz dealerships in N1 City, Cape Town.

April 2007 saw him being promoted to new-vehicles sales manager during which time he

developed the strategy aimed at new-vehicle sales. Upon completion of the strategy for

new-vehicle sales, he was appointed as pre-owned sales manager and this period forms

the basis for the pre-owned strategy as set forth in this report.

In both the new and pre-owned sales departments of Mercedez-Benz, he was involved

with the day-to-day running of the departments and interaction with customers. Further to

the day-to-day management of these departments, he is also involved with advertising

strategy, overall departmental strategy, budget setting and reporting these results directly

to the dealer principle, Mr. Keith Steele and Western Cape managing director, Mr. Owen

E. Bell.

Jaco van Zyl has the authority to make business decisions except in cases where vehicles

will be sold at a loss. In such instances authorisation needs to be obtained from Mr. Steel,

the dealer principle. The decision-making culture in Claremont can be considered to be

collective with Mr. Steele reserving the right to make all final decisions.

From a leadership point of view, Jaco van Zyl’s biggest challenge lies in the constant

motivation of the sales force reporting directly to him. Currently his pre-owned sales team

consists of three highly experienced individuals and another with average experience.

Sending the sales executives on the appropriate training to ‘fill the gaps’ also forms part of

motivation, as a well-trained and capable sales force tends to be more motivated than

untrained sales executives.

1.3 BACKGROUND SETTING TO THE OBJECTIVE OF THE REPORT May 2008 saw the board of directors unveil Sandown Motor Holdings’ new vision: “The

vision of the company is to become the finest motor group in the world.” Anyone would

agree this to be quite a bold vision, but it is certainly not impossible. In 2007, SMH

purchased three of the most successful Mercedes-Benz dealerships in London, United

Kingdom, and therefore SMH really has no other choice than to strive toward this bold new

vision. The question most observers in the motor retail industry would ask is: How does

4

SMH plan to become the finest motor group in the world, given the current economic

climate in South Africa?

On the 8th of June 2006, the South African Reserve Bank started a fierce campaign

against inflation and has since consistently raised the prime-lending rate, starting from a

low at 10.5 per cent prime to the 15.5 per cent prime of today (South African Reserve

Bank, 2008).This has placed great pressure on all South African consumers to decrease

expenditure and as a consequence has brought about a 26 per cent drop in vehicle sales

in May 2008, compared to May 2007.

The passenger car segment is usually the most sensitive to any negative developments in

the market relating to a decline in business and consumer confidence.

Motor groups and independents are finding it tougher to cover costs and return acceptable

profits to its shareholders.

The aim of this research report is to critically analyse the environment affecting the new

and pre-owned sales of Mercedes-Benz Claremont. Once analysis is complete, the

research report will set forth a deliverable strategy that supports the new company vision

and should be acceptable by SMH’s four, equally important shareholders, namely

customers, suppliers, employees and shareholders.

In simple terms, the strategy will be aimed at keeping Mercedes-Benz Claremont, the

dealership employing the author of this research report, profitable through the period of

constraining macro-economic policy expected over the next 24 months.

1.4 RESEARCH DESIGN AND METHODOLOGYSMH have only really developed from being a family-type business to a full-blown

corporate in 2006 with the opening of a ‘flagship dealership’ in Century City and Daimler-

SA becoming a shareholder.

These developments have necessitated change and therefore the report will focus on

strategy development as the key driver of success for SMH and more specifically,

Mercedes-Benz Claremont. This report will look at various models developed by leaders in

the field of strategy and therefore starts off by looking at some definitions on what strategy

5

is and why a sound strategy is crucial for survival and profitability. Michael Porter’s work is

used quite extensively as he is considered to be a subject matter expert in strategy

Thereafter different tools are used to develop the individual departments’ strategies. A

different model is used for each of the departments to obtain a feel for the variety of

models that exist, but to also benefit from synergies between the different models. This

minimises the ‘gaps’ in the different approaches and some form of cross-pollination should

occur.

These strategies focus on process management to ensure consistency throughout their

operations in all smaller dealerships. Managers are caught up in red tape and paperwork

and are often removed from customer interaction. They have lost the continuity of staff

training and creating the value inherent to customer interaction and relationship

management.

SMH therefore aims to benchmark against the top companies in the industry, but in doing

so they will inevitably increase their costs. How do they go about actually curbing costs

without losing value for the customer?

1.5. FRAMEWORK FOR THE PROPOSED STUDYHaving already given a brief overview of Sandown Motor Holdings and it operations in the

Western Cape, the study starts off by examining Mercedes-Benz Claremont in broad

terms.

Next the focus turns towards examining the pre-owned vehicle sales department, because

a strong pre-owned strategy forms the backbone of an effective new-vehicle sales

department. Without the ability to trade in customers’ old vehicles, high levels of new

vehicle sales cannot be achieved consistently over time. To supplement the pre-owned

strategy further, the report then moves towards establishing an e-commerce platform to

further support the pre-owned strategy.

Finally the report shifts its focus to the new-vehicles sales strategy by examining the

environment in which new-vehicles sales are conducted and then lays down an aggressive

but realistic strategy that will support the overall business strategy of SMH.

6

1.6 PROVISIONAL LIST OF SOURCESThe scope of the research report demands sources of knowledge from both academic and

experiential sources.

The National Automobile Association of Manufacturers of South Africa, more commonly

known as Naamsa, is another source of industry specific information that is accurate and

audited. This information is easily accessible through their website on www.naamsa.co.za.

Websites such as Statistics South Africa are also useful in spotting trends in the economy.

Conversations with representatives from financial institutions such as ABSA and Wesbank

also offer great insight into what the market is doing.

Online sources such as the Harvard Business Review is utilised to obtain articles relevant

to strategy definition and crafting. Various books such as Changing Paradigms by Clarke

and Clegg (2000) also form the basis of thoughts in the report.

Clive Howe’s C@ps model is also used as a management tool to translate strategy into

practical daily activities

7

CHAPTER 2DEVELOPING A STRATEGY FOR CLAREMENT PRE-OWNED

2.1 BACKGROUND ON MERCEDES-BENZ CLAREMONTIt is important to understand how Mercedes-Benz Claremont is financially supported by its

different departments. To simplify this concept, one can analyse the gross profit

contributions of the different departments as it stood at the end of July 2008.

Table 2.1: Gross profit contributions by department

%

% Total gross profit contribution: New vehicle sales 85

% Total gross profit contribution: Pre-owned vehicle sales 12% Total gross profit contribution: Service 38

% Total gross profit contribution: Parts 15

% Total gross profit contribution: Finance & Insurance 10

Cumulative profit contribution 160

Source: Mercedez-Benz Claremont Financials, 2008.

The table illustrates that new vehicle sales is by far the biggest contributor of profit in the

business with pre-owned sales contributing far less than expected. Based on this

information, one needs to ask three important questions:

Is this desirable?

Why does Claremont new and pre-owned profit contribution differ so dramatically?

What can be done about it?

It is not advisable to have so much of a business’ survival riding on the success of one

department. Claremont is very exposed to new vehicle market risks such as factory

strikes, raw material shortages, price increases or transportation risks inherent to getting

the vehicles from the factory to the showroom. The reason for the large difference in profit

is due to the past strategy undertaken by Claremont management.

To date, the pre-owned department was utilised in a supporting role of new vehicle sales.

The following example illustrates this point: The new vehicle department has a customer

wanting to trade in a high value exotic CLS500 worth R500 000. The new vehicle

8

department will initially earn a R30 000 profit, but in reality this transaction amounts to a

net cash outflow of R470 000 carried by the pre-owned department. Assuming that the

floor-plan interest rate is 9 per cent and the CLS500 remains unsold for 90 days, then the

pre-owned department would pay R11 250 in interest. Over time the market value of the

vehicle might also have dropped dramatically and by day 90 can only be sold for

R495 000. The end result is that the pre-owned department shows a loss of

R11 250+5 000=R16 250 so that the new vehicle department can make R30 000 profit.

Good for new sales, bad for pre-owned.

In a purely pre-owned driven business, management would have opted not to do the

transaction knowing the risks inherent to trading in the CLS500. A business with its main

focus on pre-owned would only do a transaction where they will profit on the vehicle sold

and at worst, break even on the trade-in.

However, in the case of Mercedes-Benz Claremont, it is necessary from time to time to

enter into such transactions in an effort to protect the brand image. After all, a large part of

Mercedes-Benz brand loyalty stems from the perception that Mercedes-Benz vehicles hold

their re-sell value better than those of other manufacturers. Mercedes-Benz Claremont

management should aim to find a better balance between new and pre-owned. Careful

consideration needs to be given to new vehicle transactions where high profile trade-ins

are present. Tough decisions on whether or not to do certain transactions need to be taken

with the longer term view in mind.

So what should be done in future to avoid being overexposed to new vehicle sales risks?

The real source of advantage are to be found in management’s ability to consolidate

corporate-wide technologies and production skills into competencies that empower

individual businesses to adapt quickly to changing opportunities (Clark & Clegg,

2000:206). Clearly the pre-owned department is not operating at its optimum and Clark

and Clegg highlight a possible reason for this. Obviously the pre-owned department

management have not consolidated corporate-wide technologies such as using the

customer relationship management (CRM) database on Kerridge and bulk short message

service (SMS) computer systems which the new vehicle sales department have been

using with great success over the last few years.

9

Dr. Norris Dalton, chief executive officer (CEO) of The South African Institute of

Management states that a company is only as good as its management which need to

understand that a company is a community of people, with independent wills of their own,

and that the primary job of management is to align that group of discordant wills with the

corporate will to achieve the goals of the organisation. On time results, not, excuses, is the

clarion call of effective management (Dalton, 2008:23). Pre-owned sales executives have

been known to be proud of being traditional and tend to reject new technology that

requires initial effort to master. The ‘I have been doing this for the last fifteen years and I

do not intend to change’ reflects this sentiment. This is a prime example of where

management need to align the wills of the pre-owned sales executive with the corporate

will of the company by making them understand that professionalism is the key driver of

competitive advantage in the pre-owned business arena.

Pre-owned managers have also not been able to leverage corporate-wide production

skills. Pre-owned sales executives are not being exposed to product training as do the new

vehicle sales executives and are not being subjected to stringent requirements for their

daily activities and can relax knowing that they are protected. In fact, this means the pre-

owned department needs to find alternative ways to get rid of unwanted stock. Chapter 3

will deal with this subject in more detail, especially, from an e-commerce strategy point of

view.

As mentioned, Mercedes-Benz Claremont needs to improve its pre-owned contribution by

selling more vehicles at acceptable margin levels. Section 2.2 deals with this strategy.

2.2 STRATEGY DEFINEDMany definitions exist about what strategy really is and should be, but does not give a

clear idea of what a company should actually do to create a strategy that fits with the

particular company. Michael Porter (1996:1) argues that three key principles exist for a

company aiming to strategically position itself:

‘Strategy is the creation of a unique and valuable position, involving a different set of

activities.’

‘Strategy requires you to make trade-offs in competing; to choose what not to do.’

‘Strategy involves creating ‘fit’ among a company’s activities.’

10

This view from Porter suggests that strategy is a clear statement of future intent. This

means that any manager looking to reach a certain goal needs to lay down a definite

roadmap for his/her department. This requires that the manager needs to have an in-depth

understanding of the environment in which the department operates. It is only possible to

create a unique position for your own business if you know what activities are creating the

value that your opposition is offering customers in that segment.

This knowledge of the environment is also crucial in deciding on which trade-offs to make.

Of course part of the decision on what not to do, involves having knowledge of what trade-

offs the competition are making.

Lastly, the knowledge required of the internal environment of the business, will be what

allows management to create ‘fit’ among the business’ activities. Understanding the

internal processes and capabilities within a large, geographically dispersed business is

easier said than done, as the different functions are often located in different geographic

regions and decisions around processes are made without proper consultation with all the

departments or business units involved.

Porter is saying here that knowledge of both the internal and external environment of a

business is necessary to craft a strategy for any business and Mercedes-Benz Claremont

is no different.

These principles form the basis of the strategy for Mercedes-Benz Claremont in this

research report, specifically relating to the pre-owned department. These principles

illustrate that there is a difference between strategy and operational effectiveness as

management often tend to confuse these two concepts.

Management of Mercedes-Benz Claremont should start by defining how they are going to

position the business differently from the competition. This implies taking decisions on

targeting a different market with a different type of product line backed up by a different set

of activities. Note that the emphasis is on ‘different’ and not on ‘better’ just yet.

It also means that management need to decide on what customers not to target, what

products not to stock and what activities not to engage in. Trading-off certain options, will

11

help them to keep focus on what it is they intended to do and sticking to it, at least until

they make a conscious decision to change their initial strategy.

Knowing exactly what they have planned in terms of strategic positioning allows them to

see how to create fit amongst the company’s activities. How should the pre-owned

department’s activities fit into the bigger picture in supporting new vehicle sales and how

should new-vehicles sales be supporting the pre-owned effort? It also gives management

an idea of why an e-commerce strategy is important and what company-wide activities can

support this strategy?

Only once there is absolute clarity on these three principles, should management look at

improving operational effectiveness, that is, what are the processes involved in admin,

marketing, finance and sales. Then only should the questions be asked on how to do

those things better, faster and at a lower cost. Certainly this does not mean that

operational effectiveness should not be considered as a strategic point of reference, but it

is advisable to see it as a support mechanism to solidify the strategic intentions.

Therefore Claremont’s success will be based on doing many different things well, not just

a few and integrating among them. If there is no fit among them, then there is no

distinctive strategy and little sustainability (Porter, 1996:15).

Realising that a new strategy is needed and then developing it is wonderful. But more

important is the ability to implement it. Asbury (2008:2) notes that South African

companies are often guilty of not being able to implement effective strategies and has

become a source of frustration for directors, shareholders, employees and even

customers. It is all well to not implement a new strategy in buoyant times, but in a

downturn such as the one facing the South African economy at present, failure to do so is

career-threatening for Claremont management and life-threatening for SMH itself.

2.3 ORIGIN OF CLAREMONT’S STRATEGIC POSITIONINGThe strategy for Claremonts’s strategic positioning should be based on a subset of the

industry’s products. The reason for this is that the Claremont management do not have the

authority to start another business in another industry or related industry. A clear mandate

exists from head office to keep trading in vehicles and to maintain existing customers’

vehicles. Therefore the only real activity difference can be created by targeting vehicle

12

sales to different customers than what the competition is targeting. The easiest way to do

so is through a completely different value offering as is shown in the following sections.

2.4 PRODUCT PROFILEMass customisation is the ability of a company to meet each customer’s requirements

(Kotler & Keller, 2006:152). It therefore makes sense to base the backbone of any pre-

owned business strategy rooted in the decision on what product to sell. Invariably this

decision is influenced by the following factors:

Buying preferences of the target market;

Competitors; and

Availability of certain product lines.

2.4.1 Buying preferences of the target market Claremont is considered to be one of the most affluent areas in Cape Town with the

following buyer profile:

Relatively conservative buying habits;

High customer service expectations: Emphasis on value and quality;

Living Standards Measurement (LSM) 8-10;

Financially secure;

Highly educated and well informed about market trends;

Well traveled; and

Petrol engines are preferred over diesel.

It is quite easy to assume that based on the above customer profile, Claremont pre-owned

should sell exotic and highly expensive vehicles. Year to date 2008, Claremont sold

vehicles with an average selling price of R212 000. Compared to an average selling price

of R257 000 in 2007, one could argue that the customer profile does not accurately reflect

the buying habits when it comes to pre-owned vehicles. This decline in average selling

price could be attributed to the economic slowdown experienced in South Africa.

Another interesting attribute of the motor vehicle industry is how customers’ buying

patterns and preferences change over time. Seasonality plays a big role in cabriolet (SL,

CLK and SL-Classes) sales. Cape Town has lovely sunny weather in summer which

means everybody yearns to drive down Camps Bay Boulevard with the vehicle roof

13

dropped. Conversely, cold winter months bring heavy rainstorms that last for weeks on

end and as can be expected, vehicle dealers hardly receive any enquiries on cabriolets.

‘The flavour of the month’ is another phenomenon that has pre-owned dealers scratching

their heads. As soon as a pre-owned dealership recognises that a certain product line is

selling well, he will attempt to stock up on that particular vehicle or colour, only to discover

that the trend has changed. Often these cycles last about two weeks at a time and are

completely unpredictable. This drawback of the pre-owned industry compared to the new

vehicle industry is something to take note of and anticipate.

2.4.2 CompetitorsAlthough Mercedes-Benz Claremont is part of SMH, it finds its biggest competitors to be

within the same group. Most notably, Eikestad Mercedes-Benz, Mercedes-Benz Century

City, Orbit Pre-Owned and Paarl Motors.

Eikestad Pre-Owned has a customer base that closely mimics Claremont Pre-Owned

based on its LSM levels as well as demographics. However, subtle differences do exist

especially with regard to taste and usage. A large wealthy farming community exists there

and they tend to drive smaller distances on a day-to-day basis. They also prefer diesel

vehicles to petrol due to the fact that farmers are allowed to buy diesel in bulk and at big

wholesale discounts. It is therefore essential that Eikestad Pre-owned specialise in low to

medium mileage vehicles in the 40 000-60 000kms range. They also have a strong light

commercial market in Stellenbosch which means that they sell quite a few Mitsubishi pick-

ups; however, they have to do this at deep discounts to compete against aggressively

priced Toyotas and Isuzu’s.

Paarl Motors Pre-Owned is Eikestad’s biggest competitor as they have an almost identical

target market as well as the close proximity to one another. They stock and price their

products with much consideration of what the other is doing and with little consideration of

what the Cape Town dealers such as Claremont, Culemborg or Century City is doing.

However, they are worth mentioning as Claremont should not compete with them in the

higher mileage category Mercedes-Benz category.

Culemborg Pre-Owned has been set up as an outlet to sell off other vehicle brands

ranging across the spectrum of South African manufacturers. It is a rare occurrence that

14

Culemborg and Claremont compete head-to-head on the same deal as they differ

completely on the market they are trying to capture.

The Century City branch is seen as the flagship dealership in the Western Cape and its

strategy is to stock vehicles of very low mileage (2 000-30 000 kms). Their range varies

from A-Class to the most exclusive and expensive models up to the R1.2 million mark. In

doing so, they established themselves firmly in the eyes of customer as the place to go

when you are looking to buy top end exotics. Customers looking to see the latest and

greatest in Mercedes-Benz vehicles therefore go there to shop. Their pricing is quite

optimistic and customers are willing to pay premiums just to be able to say that they buy

their vehicles there. Therefore Claremont Pre-Owned should not aim to compete directly

with Century City in the exotic car range.

“Where absolute superiority is not attainable, you must produce a relative one at the

decisive point by making skillful use of what you have”. Von Clausewitz (1832) in his book

On War made strategic sense and is even applicable to Claremont Pre-Owned. This does

not mean that Claremont should never stock more expensive exotics. As market

circumstances improve and pre-owned vehicle sales increases toward the end of 2009 as

is expected, Claremont will be well known for its medium level profile and will have

established itself a business beachhead. It will then be possible to aim the sharp end of

the spear where rivals such as Century City will be uninterested in what Claremont is

doing (Harvard Business School Press Books, 2006:4). By stocking and selling some high

level exotics Claremont will be able to successfully move beyond the medium level

beachhead for some time before the competition notices and retaliates. Figure 2.1 depicts

this possible strategy.

15

Figure 2.1: Moving beyond the beachhead: Exotic vehicles

2.4.3 Availability of certain vehicle (product) linesSourcing appropriate vehicles for any pre-owned sales department is certainly the most

important aspect of the selling function. Aligning specific vehicle supply with an ever-

changing customer demand is a fine balancing act based on experience, market

predictions and a good dose of luck. Another factor to be considered is the availability of

certain products. When the demand for vehicles increase, so too do the prices at which

these vehicles can be sourced. This causes dealers to pay more for vehicles and more

often than not this premium cannot be passed on the customer as the ‘flavour of the

month’ theory lasts too short for customers to realise that that specific vehicle is in short

supply in the market place. By the time they do realise it and become willing to pay the

premium for the product, the flavour of the month has changed and they start searching for

a different car.

2.5 OPTIMUM STOCK LEVELSIt is unlikely that a dealership such as Claremont can perform at a much higher level than

30 units per month, given its size and the current economic climate. Space constraints

only allow Claremont Pre-Owned to display 25 vehicles at any given time. The targets as

set out by Sandown Motor Holdings head office at 26 units per month are slightly

optimistic. A more realistic figure would be to aim for 24 units per month.

A, B C SLK, CLK, SL

High end

Mid range

Low end

16

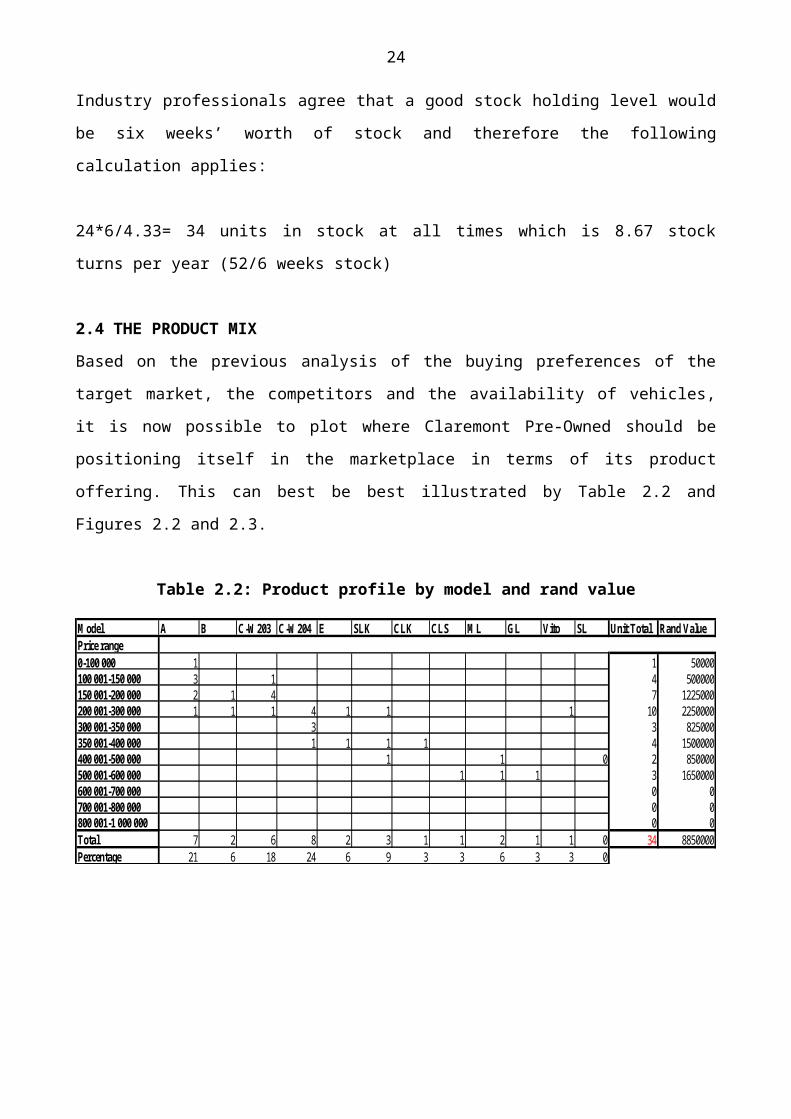

Industry professionals agree that a good stock holding level would be six weeks’ worth of

stock and therefore the following calculation applies:

24*6/4.33= 34 units in stock at all times which is 8.67 stock turns per year (52/6 weeks

stock)

2.4 THE PRODUCT MIXBased on the previous analysis of the buying preferences of the target market, the

competitors and the availability of vehicles, it is now possible to plot where Claremont Pre-

Owned should be positioning itself in the marketplace in terms of its product offering. This

can best be best illustrated by Table 2.2 and Figures 2.2 and 2.3.

Table 2.2: Product profile by model and rand value

Model A B C-W203 C-W204 E SLK CLK CLS ML GL Vito SL Unit Total Rand ValuePrice range0-100 000 1 1 50000100 001-150 000 3 1 4 500000150 001-200 000 2 1 4 7 1225000200 001-300 000 1 1 1 4 1 1 1 10 2250000300 001-350 000 3 3 825000350 001-400 000 1 1 1 1 4 1500000400 001-500 000 1 1 0 2 850000500 001-600 000 1 1 1 3 1650000600 001-700 000 0 0700 001-800 000 0 0800 001-1 000 000 0 0Total 7 2 6 8 2 3 1 1 2 1 1 0 34 8850000Percentage 21 6 18 24 6 9 3 3 6 3 3 0

17

A, 7

B, 2

C-W203, 6

C-W204, 8

E, 2

SLK, 3

CLK, 1 CLS, 1

ML, 2

GL, 1 Vito, 1

SL, 00

1

2

3

4

5

6

7

8

No. of veheicles

A B C-W203 C-W204 E SLK CLK CLS ML GL Vito SLModel

Stock by model

Figure 2.2: Bar Chart: Number of units per model

1025000

425000

1075000

2350000

625000

1075000

375000

550000

1000000

550000

250000

00

500000

1000000

1500000

2000000

2500000

Rand value

A B C-W203 C-W204 E SLK CLK CLS ML GL Vito SLModel

Stock Value by Model

Figure 2.3: Bar Chart: Stock value by model

18

2.7 BUYING POLICYFurther to trading vehicles in from customers, it is also possible to buy vehicles from

auctions as well as other dealers. This is the ideal situation as the pre-owned manager can

choose which stock to buy and at a price that is acceptable. These decisions are very

strategic and often involve significant complexity and uncertainty (Coughlan, 2002:7). Will

this stock sell quickly? Also to be considered is the short time frame in which decisions are

to be made, especially at auctions where the air is electric and full of stimuli that diverts the

buyer’s attention from making sound decisions.

Currently, Claremont Pre-Owned has surplus funds available to buy extra prime stock, but

is limited by the amount of floor space it has and therefore it is not always possible to buy

in vehicles on top of the ones traded in. This problem can be easily overcome by simply

selling off unwanted stock to other dealers and wholesalers who are willing to pay the

asking price.

2.8 SELLING (WHOLESALING) POLICYA problem with Sandown Motor Holdings Western Cape is that it has a ‘rigid wholesaling

policy’ when having to dispose of unwanted stock when that stock reaches the 60 and 90

days period. This is a much debated policy within SMH Western Cape and could easily be

called the ‘The Classical Clash of Heads’.

The emotional or bullish view advocates never selling stock to the trade even if stock

levels become high or even undesirable. This view believes that the market will change

and those vehicles will eventually become flavour of the month. Every vehicle has profit

opportunity and must not be given away.

The other view is much more conservative. Stock should be bought in at the right price

where possible but in cases where circumstances necessitates paying a bit too much, then

pre-owned managers must not be prohibited from dumping stock to other dealers who will

make the profit on those vehicles. Claremont Pre-Owned should follow this strategy as

opposed to following the bullish approach. Vehicles in stock up to 60 days should be

priced bullish in an attempt to make good margins.

All stock older than 60 days should be marked-down to ensure it is sold by the 90-day

mark. Thereafter the pre-owned manager should get three bids from other dealers or put it

19

on an auction and dump the stock to make cash flow available to buy fresh desirable stock

even if it results in a loss.

2.9 HUMAN CAPITALIt is important to consider that there also needs to be alignment between the company’s

strategy and its human capital. Few executives take the time to examine the alignment

between their business strategies and their people practices and policies (Nalbantian,

Guzzo, Kieffer & Doherty, 2003:17-21).

This is very important when involved with Mercedes-Benz. Daimler SA has taken a hard

stance with their recently updated Dealer Standards at the end of 2007. These standards

are forcing dealerships to take responsibility for vehicle preparation before delivery to

customers, accurate administration of deal files and post delivery contacts with pre-owned

customers. And whilst these measures are necessary for customer satisfaction, they place

much pressure on sales staff and sales managers considering the financial penalties on a

dealership if an audit finds that these standards have not been adhered to.

From a human capital point of view, management need to take note that aligning this

dealer standards strategy with the correct human capital requirements will be crucial for

Claremont Pre-Owned. In the past successful pre-owned sales executives and sales

managers were considered to be individuals who were able close any deal anywhere and

to ‘shoot from the hip’. These individuals were not famous for their systematic approach to

selling or their administrative abilities.

Circumstances have since changed as careful consideration needs to be taken to only

recruit and employ people who will be able to master the Dealer Standards and still be

able to close and make the sale. Some managers still prefer to recruit these so-called

‘closers’ whilst employing another administrative person to do the Dealer Standard

cleaning up after the sales executive. This makes sense in a perfect world where cutting

costs are unnecessary. Unfortunately Mercedes-Benz Claremont needs to keep its costs

down and it therefore makes sense to employ only those executives who are systematic

and administratively sound.

20

In the past Dealer Standards only forced new vehicle sales executives to go on new

product training as well as take on some soft skills training in the form of two-day

workshops with elaborate assignments to be handed in before being considered

competent. From July 2008 this is now compulsory for all pre-owned sales executives and

pre-owned sales managers dealing with the Mercedes-Benz brand. From a human capital

strategy point of view this is great as all sales executives are being trained and developed.

It does however place pressure on the recruitment of sales executives for the pre-owned

department who have a willingness to be trained as well as the ability to do the

assignments in order to be declared competent on that unit standard.

The strategy necessary to align the human capital in the pre-owned department with the

Dealer Standard strategy of the dealership lies in the ability of management to

communicate the importance of their contribution toward Dealer Standards. Management

will also need to coordinate and train them in this new work process to ensure that they

develop the administrative and systematic skills employed by the new vehicle sales

executives. As consultants George Labovitz and Victor Rosansky (1997: 13) once wrote,

“Imagine working in an organisation where every member, form top management to the

newly hired employee, shares an understanding of the business, its goals and purpose.”

Imagine working in a department where everyone knows how he or she contributes to the

company’s business strategy. That’s alignment!

The same applies to the goals of the pre-owned department not relating to dealer

standards. Pre-owned sales executives need to be given a clear brief on their own sales

targets, gross profit targets and the financial implications of their debtor levels. They need

to be shown how these factors impact the business and the long-term sustainability

thereof. They need to understand where they are part of the activities which make

Claremont different from its competitors.

Most importantly, they need to understand that they are a part of the competitive

advantage and therefore need to take responsibility for that.

21

2.10 PROCESSESSatisfied customers constitute the company’s customer relationship capital. It forms a very

important base of monetary value in Mercedes-Benz Claremont and because of this, long-

term profitability and increasing cost pressures forces SMH management to ensure that no

deals are lost. It is important to understand the value and the importance of customer

retention. It costs five times more to acquire new customers than satisfying current

customers. The average company loses 10 per cent of its customers per year. A five per

cent reduction in the customer defection rate can increase profits from 25 per cent to 85

per cent, depending on the industry. The customer profit rate increases over the life of the

retained customer. (Kotler & Keller, 2006:156).

Kotler and Keller’s statement holds great value for Claremont Pre-Owned and it therefore

makes sense to make sure that existing customers are well looked after. For the months of

June, July and August 2008, Claremont Pre-Owned spent R26 415 per month on

advertising and promotion and retailed an average of 20 units per month. This implies that

Claremont spent R1 320,75 per unit retailed on advertising.

Further investigations revealed that over the same three months in question, an average of

four ‘offers to purchase’ were signed by customers but these deals were never completed

due to customers defecting. A big reason for these defections lie in sales executives failing

to promptly follow up these customers in terms of finance and other promises made. In

some cases customers only informed the sales executives up to 15 days after the original

offer was signed. Strictly speaking these customers should be seen as existing customers

as soon as they sign.

If Claremont pre-owned had retained those four customers per month, it would mean that

the advertising spend per unit retailed would drop to R1 100,63. This amounts to a 17 per

cent reduction in advertising spend per unit.

The strategy laid out above, however much it may create warm fuzzy feelings, is at best a

cloud of hot air if not translated into everyday actions. Clive Howe (2006:87) in his book,

Simple Solutions to Strategic Success, states that once strategic plans and business plans

have been established, it should be translated into doable goals and ultimately measurable

activities. Clive Howe has developed his C@ps model which emphasises simplicity and

practicality.

22

The aim behind his model is to keep things simple and to the point. Most strategic plans of

more than one page are often not read thoroughly and are often cluttered with superficial

information. This document is a one-pager which really expresses a company or

department’s critical success path. It can be circulated to all employees involved and can

be used as a guide for all their actions.

The model starts by stating the vision of the company, in this case being the vision to

become the finest motor group in the world. From this vision, the values of the department

flows followed by the critical success factors. Next the model aims to define what strategic

objectives are necessary to achieve those critical success factors. This is crucial. These

strategic objectives are really what bring the strategy to life. This is the part of the model

that needs to be religiously adhered to in order for the strategy to be implemented

successfully.

Executing the strategy is often easier said than done as many organisations have found

over time. The ability to measure whether the strategy is being implemented is just as

important as the conception of it. The C@ps model emphasises this ability to measure and

advocates a key performance measurement for each of the strategic objectives. Figure 2.4

shows the C@ps Model devised for Claremont Pre-Owned. The values aspire to high

levels of integrity and critical success factors are both financial and activity based. The

performance indicators relating to pre-owned sales are provided to measure whether or

not the strategic objectives are being met are simple and easy to measure on a day-to-day

basis.

The model is a great tool for the pre-owned department and is the final step to getting the

pre-owned department to world-class level.

23

Figure 2.4: C@PS Model for Claremont Pre-Owned

24

CHAPTER 3DEVELOPING AN E-COMMERCE STRATEGY TO SUPPORT THE

MERCEDES PRE-OWNED EFFORT

3.1 INTRODUCTION With the proliferation of the internet and online auctioneering technology in South Africa, it

makes sense to embark on an e-commerce project to support the efforts of the pre-owned

department.

The pre-owned market is marked by great fluctuations in the demand and supply of pre-

owned vehicle stock and understanding how to cope with these fluctuations is the key to

success for small and larger motor groups.

SMH as one of the largest motor groups in South Africa, is no stranger to these

fluctuations. In the period spanning March 2007 to December 2007, Sandown Motor

Holdings Western Cape alone had been overstocked by about R17 million. This problem

has since grown to roughly R22 million and has to be funded by an interest-bearing

overdraft. It therefore comes as no surprise that SMH requires an urgent strategy to curb

these dangerous levels of cash-consuming stock.

Although this research report aims to focus on Mercedes-Benz Claremont, it makes sense

to develop an e-commerce strategy that can be used throughout the group, as Claremont

does not have enough vehicles to sell via an e-commerce platform to make it financially

viable and successful. The next section will therefore explore the viability of an e-

commerce platform for the Western Cape region from which to trade these units to

wholesalers and stop stock from ageing.

This chapter starts by analysing SMH at industry level by drawing heavily on the work of

Michael Porter (1996, 2001). Again it is relevant to discuss the mission of the business

within the context of an e-commerce strategy, the industry structure and possible

competitors. Again Michael Porter’s work in the form of his Resource-Based View is

utilised by looking at SMH unique competencies, sustainability and timing. These insights

lead to strategy formulation and implementation, specifically related to an e-commerce

solution.

25

3.2 PORTER’S APPROACHPorter’s Competitive Forces Model, however outdated it may seem, still serves as a useful

tool in helping to sculpt the correct strategy for SMH’s e-commerce business. In doing so

one is able to draw a distinct line between strategy and performance by specifically looking

at the mission of the business, the industry structure and competitive positioning.

3.3 SANDOWN MOTOR HOLDINGS OVERALL STRATEGYSMH aims to derive satisfy its four equally important shareholders in the following ways:

a) Shareholders“Some smaller previously profitable dealerships were losing money after sales had

dropped by 40 to 50 percent.The decline in sales volume coincided with severe sales

margin erosion resulting in a double whammy…The operating margins of good dealerships

are 2.5 per cent before interest and tax, so they are sailing very close to the wind”

(Cokyane, 2008). This statement certainly holds true for SMH.

Generating enough revenue in an attempt to cover all overheads and give SMH

shareholders maximum return on investment and exceed the industry norm is the vision

for the foreseeable future.

b) CustomersSMH strives to provide customers with the highest quality service. In doing so, SMH aims

to provide world-class sales consultants, superior after sales service and trade-in prices

that are market related and fair. In the current economic climate, it is high quality trade-in

prices that will allow SMH to enter into new transactions. This however, is easier said than

done as high levels of pre-owned stock forces SMH to pay less than fair prices for trade-

ins. Included in the definition of customers are the wholesalers who buy those unwanted

trade units that SMH does not intend to retail.

The cornerstone of the e-commerce strategy is to also provide the wholesalers with

superior service such as unit availability, ease of posting a bid on any particular unit and

fair pricing. This problem lies at the heart of this chapter and is the motivation for the e-

commerce strategy to be discussed.

26

c) SuppliersSMH aims to build lasting relationships with suppliers. Daimler SA is the biggest supplier

of SMH as they supply SMH’s primary stock in the form of new vehicles. The longevity of

SMH directly translates into the longevity of Daimler SA. SMH’s ability to trade in pre-

owned vehicles has a direct influence on their ability to sell new vehicles that is the

commodity of Daimler SA.

d) EmployeesHowever cliché it may seem, SMH really does care about its employees. The success of

SMH is the direct result of SMH’s employees’ success and vice versa. SMH therefore aims

to provide job security to its employees. In times of financial strain, SMH will seek to

minimise costs of a non-human nature and try to cut costs and maximise profits

elsewhere. An e-commerce strategy aimed at increasing turnover and profit will ultimately

allow SMH to cover expenses which would otherwise have been subsidised by the

retrenching of staff.

3.4 INDUSTRY STRUCTUREFrom a vehicle sales point of view, motor groups have different manufacturer franchises

with different strengths and weaknesses. As mentioned in the first chapter, SMH is

involved with Mercedes-Benz, Chrysler, Mitsubishi and Jeep, whereas Barloworld and

McCarthy are very much involved with Toyota as well as some Daimler Franchises. These

differences serve to differentiate their operations, but one thing all these groups have in

common is the ever-changing levels and mix of trade-in vehicles they deal with.

Depending on market circumstances, the abundance or the lack of trade-in-stock, largely

determines the success of a dealership in that it allows the new car department to trade-in

unwanted vehicles from customers. If a dealership is overstocked in its used car

departments, it will find it difficult to front the cash to buy in the trade units, which means

that the dealer is limited to deals containing no trade-ins and will therefore lose business to

rival dealerships.

Having just launched the new Mercedes-Benz C-Class, SMH finds itself in a position

where it is trading in large volumes of trade units that exceeds pre-owned sales levels at

SMH outlets. By the same token, other motor groups such as Audi are launching their new

models and also experiencing increased pre-owned stock levels. It therefore makes

27

strategic and financial sense to find another channel from which to sell the excess stock to

other vehicle traders who have a demand for that stock and will consequently be willing to

pay slightly higher prices to ensure they receive the unit.

3.5 COMPETITIVE POSITIONINGClay Christensen (1997: 141-156) insists that any strategy should start with a strengths,

opportunities and threats analysis. In the pre-owned strategy this route was not taken due

to the inherent knowledge and experience already built into the department as it stands.

Considering that an online auction is a brand new field for most managers at SMH, it is

relevant if not crucial, to analyse the environment which SMH plans to enter in this fashion.

3.5.1 SMH strengthsa) The most distinguishable characteristic of SMH lies in its ability to attract a top

workforce, especially in the Western Cape. This translates into a rare ability to attract

people in top positions in competing companies as these people aspire to work at

SMH to a large degree. In doing so SMH is able to gain insight into what other

successful companies are doing. In pre-owned terms it means that SMH

management know management in other companies on an intimate level and can

therefore leverage this ability to sell pre-owned vehicles to these dealers within the

scope of the proposed e-commerce strategy.

e) Due to its size, SMH has access to relatively large financial resources. This allows

SMH to carry pre-owned stock levels of size and mixture that allows it to trade with

almost any customer.

f) The number of outlets over which SMH has control is a great advantage in terms of

its pre-owned retailing strategy. Should a unit be deemed not retailable at a specific

outlet, it can easily be moved to another SMH outlet elsewhere in the Western Cape.

When an outlet requires a specific vehicle for a customer, then that pre-owned

manager can access the consolidated stock list and transfer the vehicle to where it is

necessary.

g) The size of SMH operations presents the opportunity to centralise certain functions

and departments. Administrative functions such as payroll, vehicle stocking, financing

and marketing can be centralised. Mass clearance sales are often held at one central

location for all the outlets and the advertising budget for these sales are split between

the various pre-owned departments. It would therefore make sense to centralise the

e-commerce strategy by using the various outlets’ inputs electronically. Costs can be

28

easily allocated based on usage of the system which, in this case would be directly

tied to the number of units sold via e-commerce.

h) Proximity of the various Western Cape outlets also brings great advantages.

Paarl Motors: Mercedes-Benz and Mitsubishi, Chrysler Jeep

Eikestad Motors: Mercedes-Benz and Mitsubishi

Orbit Boland: Mercedes-Benz and Mitsubishi, Chrysler Jeep

Mercedes-Benz Claremont: Mercedes-Benz

Mercedes-Benz Culemborg: Mercedes-Benz

Lifestyle Centre Century City: Mercedes-Benz, Chrysler Jeep

Mitsubishi Paarden Eiland

Mitsubishi Durban Road

All these dealerships are within a 100km radius of one another. Even though an e-

commerce strategy is usually associated with vast geographical dispersion, the pilot

Western Cape project would benefit from this proximity by allowing dealers to easily drive

to the precise location of the vehicle on offer for a thorough inspection. More often than

not, e-commerce strategies in the motor vehicle industry fail due to the sheer distances

between the seller and the buyer. When it comes to high value goods such as vehicles,

buyers definitely prefer to physically inspect the goods they are purchasing, especially if

the vehicle is pre-owned.

3.5.2 SMH weaknessesa) Under strengths it was noted that SMH has access to vast financial resources. At this

point it should be noted that McCarthy’s, Imperial and Barloworld are much larger

companies and have much deeper pockets. If they do decide to take on SMH in a

price war on pre-owned vehicles, they would most probably be the victors.

i) SMH lacks diversity in its businesses. All SMH eggs are packed into the motor

vehicle basket. The threat obviously exists that a severe industry recession could

jeopardise the future of SMH. In contrast McCarthy’s, Imperial and Barloworld have

diversified their operations into logistics, vehicle and plant hire, finance and

insurance, to name but a few. In the case of vehicle rentals, they are able to buy the

vehicles from their own dealerships, rent them out and end up selling them from their

own outlets and auctions. They are also able to cross subsidise between industries

when a specific industry suffers from severe recession. This creates longevity and

security for all stakeholders.

29

j) SMH dealerships tend to differ from region to region. One will find that Gauteng

dealerships give away larger discounts than the Western Cape dealerships. This

means that a lack of communication often sees Western Cape dealerships losing

business to its Gauteng counterparts. Such undercutting taking place within regions

is a source of much conflict at most management meetings at regional level. Such

inter-company competition results in margin erosion through cannibalization. Luckily

for SMH, so do McCarthy’s, Imperial and Barloworld. In this instance, it is much

better to be in the shoes of a smaller vehicle group. The proposed e-commerce

strategy will hopefully eliminate this form of detrimental inter-company competition by

using a single auctioneering platform in what will initially be the Western Cape only,

but later on, countrywide.

3.5.3 SMH threats Strong competitors (see Appendix A for screen shots of competitors’ sites)

a) Wesbank, ABSA, Standard Bank, Nedbank, MFC etc. all have their own auctions

selling repossessed vehicles to traders and the public. Smaller auctions by privately

held companies include Aucor, Burchmores and CMA. Their auctions occur

frequently (once or twice a month) and they generally sell at very competitive prices

as they are only looking to recover their costs. It should be noted however that their

auctions are still traditional auctions and they do not yet have a real online presence.

By having an online auction, SMH will be able to compete with bank auctions as it

appeals to the timing needs of vehicle traders requiring stock to sell.

b) McCarthy Call-A-Car is the second biggest threat and provides a marketing service

for not only McCarthy Limited dealers but also for dealers that are not part of

McCarthy. All participating dealers list their vehicles on the Call-A-Car website and

customers’ inquiries are thereafter channeled to the relevant dealers via Call-A-Car.

SMH does not form part of this network.

c) Barloworld also has an online auction which is really aimed at selling vehicles to end

customers called autoteam.co.za. Appendix A clearly shows the large list of

participating dealers. Whilst their sites are mostly aimed at retailing units to

customers instead of vehicle traders, they still remain a threat to take notice of.

d) Other auctions such as Claremart, Surf4Cars and Auction Alliance are also sources of

competition for the SMH site. Once again these sites and auctions are mostly aimed

at selling retail units.

30

3.6 ACHIEVING SUSTAINABLE COMPETITIVE ADVANTAGEIn the motor vehicle industry, most bankruptcies are caused by unmanageable interest

bills on increasing stock levels and lack of sales and resulting margins to cover this

interest.

Interest rate levels are the biggest determinant of sales in the motor vehicle industry.

These need to be monitored closely as possible rate hikes need to be anticipated and pre-

owned stock levels need to be dropped as soon as possible. Interest rate hikes give

dealers a triple whammy as sales drop, stock levels of unwanted stock rise and

dealerships have to then fund those stock levels at the higher interest rate.

Once again the proposed e-commerce strategy will be an ideal way to lower stock levels in

anticipation of rate hikes and getting a head start on the competition. By pumping out

unwanted pre-owned stock before other motor groups and smaller dealers do, means that

SMH would be the ones saturating the market and realising relatively decent prices before

the market slumps.

In times where the normal revenue lines are under pressure, it makes sense to keep the

use of current capital as low as possible in order to make strict return on net assets

requirements from the shareholders. Being able to manage sales levels and the interest

therefore lies at the core of business sustainability in the motor industry and will be the

departure point for SMH’s e-commerce strategy.

3.7 STRATEGY FORMULATIONGaining competitive advantage does not require a radically new approach to business; it

requires building on the proven principles of effective strategy (Porter, 2001). This implies

that SMH should not reinvent the wheel. Instead they need to focus on what they have

been doing well all these years, which is selling cars, and just modifying those channels

and the methods of selling through them.

The answer lies in establishing a lower-cost and higher-profit business based on e-

commerce in the pre-owned departments. SMH will create synergies with its existing

businesses like the new vehicle departments as well as service and parts. Such synergies

will also benefit SMH by allowing the smaller dealerships in rural areas to trade out of their

unwanted stock that might be more appropriate for metropolitan areas.

31

A well planned e-commerce strategy will generate value for all SMH stakeholders by

freeing up cash flow to trade, thereby making it financially stable for investors,

shareholders, customers and employees alike.

3.8 TAKING THE RESOURCE-BASED VIEW ON THE SITUATION The resource-based view is another approach advocated by Michael Porter. It is more firm

specific and is therefore the next logical step in formulating an e-commerce strategy for

SMH. This framework should be used to build a picture around the unique competencies

of SMH, the appropriability of retaining value created inside the firm, sustainability of a

proposed strategy and timing required to build competitive advantage.

SMH in the Western Cape already has a well-developed information technology (IT)

department with all the necessary expertise and infrastructure to embark on the

development of an online auctioning platform. Further capital expenditure required will be

minimal. All pre-owned managers are fully computer literate and will require only minor,

focused training in order to operate the software relating to the auction. It is also clear that

the product to be sold is quite unique to SMH as other motor groups and individual dealers

have different trade-in profiles. One can say with conviction that SMH has the necessary resources to embark on this strategy.

As mentioned earlier in the paper, SMH managers all come from different companies and

therefore have the necessary contacts which are built over years. These levels of trust with

other dealers will be the toughest unique competency for competitors in the Western Cape

to imitate. It will also be very hard for competitors to imitate the stock mix that SMH will

have on offer. The only competitor that will really be able to match the product mix will be

the bank auctions.

At this point one can once again point out that the timing of SMH auctions will be better

than those of banks as it will be online and the auction can be run as often as is necessary

to stay competitive with bank auctions.

As SMH will continue to have high stock levels over the foreseeable future, it remains

certain that the resources will consistently be available and therefore sustainable.

The competitive advantage will therefore be derived from a technical and financial ability to

see the strategy through. SMH will continue to have appropriate stock available for sale

32

and has the necessary contacts and relationships in place with its dealer customers. All of

the above-mentioned factors are value that is already being generated inside the firm and

has to date never been exploited. It makes sense to start utilising the value by turning it

into revenue.

3.9 THE STRATEGYAccording to Johnson, Clayton and Kagerman (2008:1), very little formal study has been

done into the dynamics and processes of business model development. Second, few

companies understand their existing business model well enough: the premise behind its

development, its natural interdependencies, and its strengths and limitations. So they do

not know when they can leverage their core business and when success requires a new

business model. Based on their opinion and the findings of the previous sections, it is

apparent that there is a need for SMH to re-look its business model to some extent. Whilst

an e-commerce strategy will not reinvent the way SMH does business currently, it will be a

good starting point to start creating a core competency for commerce in the future. Baby

steps are required.

It is also clear that SMH has the necessary resources to embark on such a strategy. The

aim would be to develop an alternative channel from which to market its unwanted pre-

owned vehicles. An e-commerce approach is seen as the most viable and approach with

the least cost implications to optimise profits.

The immediate tactic would be to set up an interactive auctioning website that will allow

SMH to auction off unwanted units at financially sound prices starting at a regional level in

the Western Cape. Only once the business model has been fine-tuned, can it be rolled out

to other regions in South Africa, eventually establishing it at a national level.

33

According to Turban, King, Viehland and Lee (2006: 58), the advantages of an online

auction would be the following:

a) Increased revenue from broadening the bidder base and shortening the cycle time.

SMH will have more vehicle traders showing interest in vehicles for which SMH

otherwise might not even have had a prospective buyer in the first place. By

shortening the time from when SMH owns the vehicle to when they sell the vehicle

(cycle time), they will be able to keep the interest bill to the minimum.

b) Optimal price setting becomes possible. It will also give SMH a true indication of the

true value of a vehicle for future purposes of pricing certain models.

c) SMH are able to cut out intermediaries such as wholesalers who in the past used to

buy trade units from SMH and sell it onto other dealerships who will eventually retail