Embed Size (px)

Citation preview

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 1/40

MeralcoNovember 18, 2013

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 2/40

MERALCO SERVES A STRATEGIC MARKET

Powers more than five (5)million customers in 33cities and 78municipalitiesThe country’s center ofcommerce & industry

About 50% of the country’sGDP

An estimated 60% ofmanufacturing outputMore than 30 manufacturingeconomic zones

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 3/40

HUB OF GOVERNMENT SERVICES & INFRASTRUCTURE

Providers of outsourced businessprocessesHQ of shared services of globalcompanies

Deustche Bank, Chevron, etc.

Hotels & hospitalsTelecoms & transportation

Internet backbone, LRT & MRT,airport, etc.

All major media companies

Malacañang, Senate & House ofRepresentatives, Supreme Court,Armed Forces, National Police &Office of Civil DefensePAG-ASA

Providers of outsourced businessprocesses

HQ of shared services of globalcompanies (e.g., Deustche Bank,Chevron, etc.)

Hotels & hospitals

Telecoms & transportation: internetbackbone, LRT & MRT, airport

All major media companies

Malacañang, Senate & House ofRepresentatives, Supreme Court

Armed Forces, National Police &Office of Civil Defense

PAG-ASA

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 4/40

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

23,83424,660 24,806 25,078

26,21927,049 27,516

30,247 30,592

32,771 GWh7.1%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

4.054.21 4.32 4.39 4.46

4.574.70

4.855.03

5.19 mln3.2%

ENERGY SALES

CUSTOMER COUNT

CONSOLIDATED

Ave. Growth: 2003-09: 2.7%2009-12: 5.0%2003-12: 3.7%

Ave. Growth: 2003-09: 2.6%2009-11: 3.2%

2003-12: 2.8%

MARKET HAS BEEN STEADILY GROWING

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 5/40

DRIVERS OF GROWTH (1 ST HALF 2013)

13,11814,950 14,781

16,215 16,863

2009 2010 2011 2012 2013

4,956 5,174

6,261 6,557

4,933 5,067

4.4%

4.7%

2.7%

4.0 % Total, in GWh

Share of

2013 Sales:Details:

• Food & Beverage• Electrical Machinery (semicon)• Miscellaneous Manufactures

• Real Estate (condominiums, BPO office space)• Private Services (hotels, malls, hospitals)• Trade

Movers for 1H 2013

• Increased household consumption mainly due to warmertemperature and benign inflation

30.0%

38.9%

30.7%

Industrial

Commercial

Residential

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 6/40

ON POWER PRICES

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 7/40

SUPPLY CHAIN OF THE POWER SECTOR

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 8/40

1H 2013 Share per component

Generation Charge56.9%

Meralco17.6%

NGCP9.0%

Taxes, UnivCharge11.5%

System LossCharge5.0%

BILL COMPONENT1H 2013Overall Ave,

P/kWh

Generation Charge 5.38Distribution Charge(MERALCO) 1.66

Transmission Charge(NGCP) 0.85

System Loss Charge 0.47

Taxes, Univ Charge* 1.09

Total 9.45

GENERATION CHARGE: SINGLE LARGEST COMPONENT

* Breakdown :Universal Charges 0.25VAT 0.77Others (Local Franchise Tax, etc.) 0.07

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 9/40

REGIONAL COMPARISON OF ELECTRICITY PRICESFINDINGS OF THE INTERNATIONAL ENERGY CONSULTANTS

Philippine tariffs are “fully cost -reflective, which issound economic policy”

Policy is similar to Singapore, Japan, and Australia

Rates in Thailand, Malaysia, South Korea, Taiwan,& Indonesia are low due to “government subsidies”

“Tariffs remain well below the cost”

“Poor economic policy … unsustainable”

John Christopher Morris, Ph.D.Managing Director

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 10/40

COMPARISON OF AVERAGE RETAIL ELECTRICITY TARIFFS

0.00

15.00

30.00

U S c / k W h

Bundled excl taxesUnbundled Generation

Unbundled Transmission

Unbundled Distribution

Other Taxes & Charges

Notes:1. Weighted average tariff (all customer categories), excluding VAT2. Tariffs are for January 2012

Source: International Energy Consultants

“Cost -reflective” “Government subsidized”

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 11/40

GOVERNMENT SUBSIDIES IN OTHER COUNTRIES

• Subsidy is up to 54% of the power cost• Subsidies are through: sub sidized fuel , cash grants , addi t ion al debt ,

deferred expend i tures

Source: International Energy Consultants

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 12/40

OTHER FINDINGS OF THE INTERNATIONALENERGY CONSULTANTS

Dependence on the price of imported fuel“Fuel is the largest component of the tariff.Approx. 80% of generation on Luzon is fuelledwith imported coal & oil (at full internationalmarket prices) & domestic gas (pegged tointernational prices)” “Several (but not all) other countries with lowertariffs provide fuel to their utilities at below-market rates”, or Their government-owned power generation,transmission, and/or distribution companies aresubsidized, absorb costs, and/or incur losses

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 13/40

Historical Fuel Costs vs. Tariffs

0

25

50

75

100

125

150

0.00

5.00

10.00

15.00

20.00

25.00

30.00

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

$ / t o n n e - $ / b

b l

c / k W h

Coal Oil Australia Singapore Indonesia Korea Meralco

Source: IECNB. Meralco, Indonesia & Korea are averages of all tariff classes; Singapore, Australia are residential tariffs only

June, 2012

Over the past decade, some markets have passed rising fuel costs on to customers(eg. Singapore, Australia, Philippines) but others have not (eg. Indonesia, Korea)

Page 13

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 14/40

• VAT• Royalty/Tax on

indigenous fuels or

Duty/Tax onimported fuels• Real Property Tax• Other taxes & fees

• 3% franchise tax,in lieu of all othertaxes

Transmission

• VAT• Local Franchise Tax on pass

through gen/ trans/ system loss

charges *• Local Franchise Tax ondistribution charges

• Real Property Tax• Energy Tax on residentials• Universal Charges incl FIT•

Other taxes & fees* not applicable to electric coops

DistributionDELIVERYGENERATION

Phl Power Market is a fully priced market No Subsidies and heavily “taxed”

THE POWER SECTOR IS HEAVILY TAXED

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 15/40

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 16/40

POWER PLANT /LOCATION

GENERATINGCOMPANY FUEL

INITIALCONTRACTED

CAPACITYILIJAN,

Batangas

South Premiere

Power Corp.

Nat Gas /

Diesel1,180 MW

CALACA,Batangas

SEM-Calaca PowerCorp. Coal 210-420 MW

MASINLOC,Zambales

Masinloc PowerPartners Co. Ltd. Coal 330-430 MW

PAGBILAO,Quezon Therma Luzon Inc. Coal 350 MW

SUAL,Pangasinan

San Miguel EnergyCorp. Coal 200-500 MW

Combined capacity:> 2,270 – 2,880 MW

MERALCO &South Premiere Power Corp. MERALCO &

SEM-Calaca Power Corp.MERALCO &

Masinloc Power Partners.

MERALCO &Therma Luzon Inc. MERALCO &

San Miguel Energy Corp.

Completion in 2012 of negotiations for new Power Supply Agreements

MERALCO RECENTLY SECURED TIGHTLY PRICEDPOWER FOR ITS CUSTOMERS

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 17/40

LOWER GENERATION CHARGES IN 2013 VS. 2012

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 18/40

Generation Charges also went up duringpast major Malampaya maintenance works

6.77 6.74

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

J a n - 1 0

F e b

- 1 0

M a r - 1 0

A p r - 1 0

M a y - 1 0

J u n - 1

0

J u l - 1 0

A u g - 1 0

S e p - 1 0

O c t - 1 0

N o v - 1 0

D e c - 1 0

J a n - 1 1

F e b

- 1 1

M a r - 1 1

A p r - 1 1

M a y - 1 1

J u n - 1

1

J u l - 1 1

A u g - 1 1

S e p - 1 1

O c t - 1 1

N o v - 1 1

D e c - 1 1

J a n - 1 2

F e b

- 1 2

M a r - 1 2

A p r - 1 2

M a y - 1 2

J u n - 1

2

J u l - 1 2

A u g - 1 2

S e p - 1 2

O c t - 1 2

N o v - 1 2

D e c - 1 2

J a n - 1 3

F e b

- 1 3

M a r - 1 3

A p r - 1 3

M a y - 1 3

J u n - 1

3

J u l - 1 3

A u g - 1 3

S e p - 1 3

O c t - 1 3

N o v - 1 3

Malampayamaintenance(Jul 13-21)

Malampayamaintenance

(Feb 10-Mar 9)

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 19/40

IMPACT OF THE MALAMPAYA AND POWERPLANT MAINTENANCE

Generation Charge will rise

Will affect December and January bills to customers

After conclusion of maintenance works, GenerationCharge will normalize in February

Malampayamaintenance

Use of alternate, but more expensive,liquid fuels

Power plantmaintenance

• Tighter generation supply situation• Greater dependence on WESM

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 20/40

Meralco's Peak / Off-Peak (POP)rates program

Formerly "Time of Use" or "TOU"Alternative energy pricing scheme:based on the cost of supplying

electricity during a period of timeMeralco customers can avail oflower generation costs in theirtotal electricity rate during pre-defined off-peak hours

DAYS PEAK OFF PEAK

Monday to Saturday 8 am to 9 pm (13 hours) 9 pm to 8 am (11 hours)

Sunday 6 pm to 8 pm (2 hours) 8 pm to 6 pm (22 hours)

CUSTOMER OPTIONS TO LOWER THEIRGENERATION CHARGE

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 21/40

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 22/40

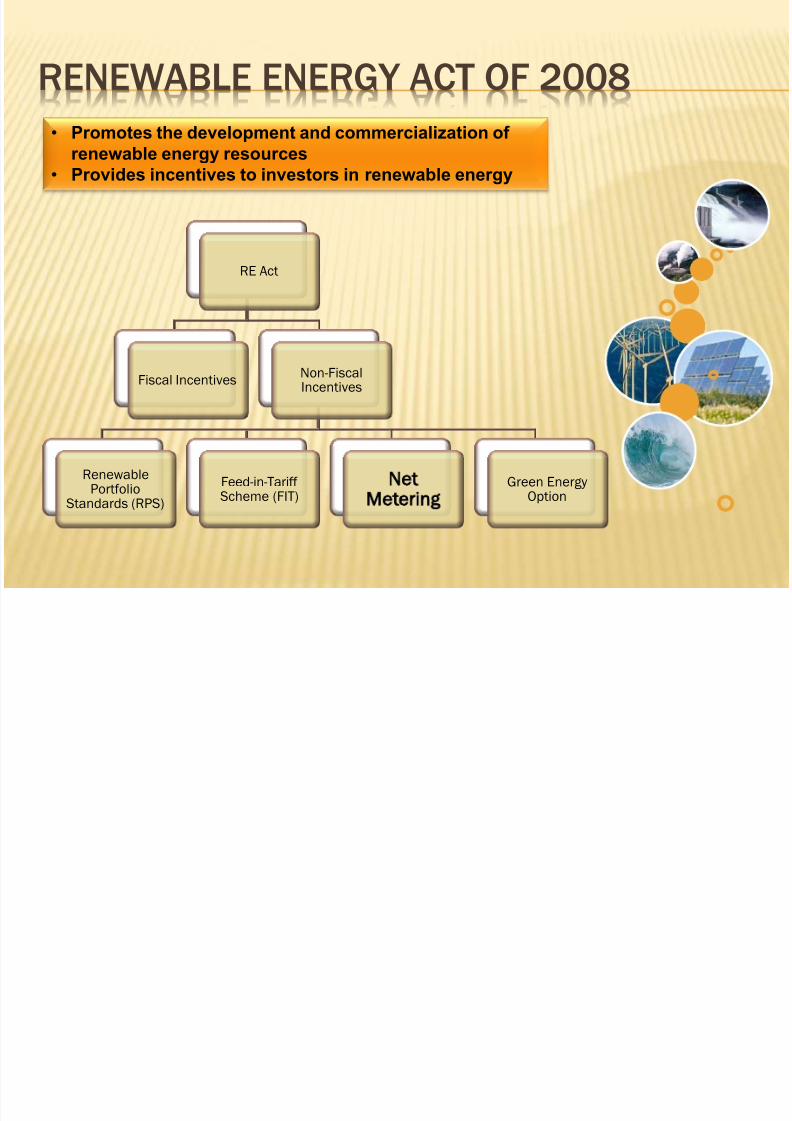

RENEWABLE ENERGY ACT OF 2008

RE Act

Fiscal Incentives Non-FiscalIncentives

RenewablePortfolio

Standards (RPS)

Feed-in-TariffScheme (FIT)

NetMetering

Green EnergyOption

•Promotes the development and commercialization ofrenewable energy resources

• Provides incentives to investors in renewable energy

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 23/40

Customer Exports Energy to the Distribution Network• Daytime with Energy generated by the Solar PV•

Household uses up a portion of the Energy generated by Solar PV for basic load• Energy generated in excess of the Household load is exported to the Distribution Network

Customer Imports Energy from the Distribution Network• E.g., Night time with no Energy generated by the Solar PV• Household Energy demand is supplied by the Distribution Network

EnergyImported

EnergyExported

₱ kWh Imported

₱ kWh Exported

₱ Net Billed Amount

l e s s

Import Meter

Export Meter

Import Meter

Export Meter

NET METERING: CUSTOMER AS SUPPLIER

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 24/40

April 2013 Lifeline Data Customer

Count(in millions)

EnergyConsumption

(gWh)

Lifeline 1.88 96.6Non-Lifeline 2.90 846.6TOTAL 4.79 943.2

39.36%

60.64%

Customer Count

10.24%

89.76%

Energy Consumption

Lifeline Non-lifeline

Lifeline Non-lifeline

SUPPORT TO MARGINALIZED SECTORS

KWhConsumption Lifeline Discount

( of Charges*)

1-20 100%

21-50 50%

51-70 35%

71-100 20% * Applied to sum of Generation,

Transmission, Distribution, Supply,Metering, and System Loss charges

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 25/40

POWER SECURITY AND ROBUSTDISTRIBUTION INFRASTRUCTURE

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 26/40

STRATEGIC IMPERATIVES

Given the strategic nature of Meralco’s market,power security and competitiveness are verycritical concerns

Adequate, reliable and reasonably pricedpower supply

Customer-centric processes and systemsHighly robust and customer responsivenetwork and service infrastructure

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 27/40

6668

5430 5339

60996869

9175 8890 9053 8748

10,321

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

INVESTING TO SUPPORT DEVELOPMENT

CPIP 115 kV Line, Calamba PremiereIndustrial Park (CPIP), Calamba, Laguna

Laguna Bel-Air Substation, Sta. Rosa, Laguna

Carmelray 83-MVA Bank No. 2, CarmelrayIndustrial Park, Calamba, Laguna

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 28/40

REDUCING THE SYSTEM LOSS CHARGE

10.85 11.1010.21 10.10

9.65

9.28

8.61 7.947.35 7.04

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

System Loss Cap8.5%

9.5%

1 . 4

6 %

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 29/40

I F R ( t i m e s ) / C I T

( h o u r s )

Total IFR (Reliability) improved by 23%, at 2.84 times

Forced CIT (Availability) improved by 29%, at 1.75 hoursPre-Arranged CIT (Availability) improved by 20%, at 1.11 hours

IMPROVING SYSTEM AVAILABILITY AND RELIABILITY

IFR: Interruption Frequency RateCIT: Cumulative Interruption Time

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 30/40

Ave. Time to Process Application

improved by 14%, at 4.6 days Ave. Time to Connect Applicationimproved by 31%, at 2.12 days

11.42

8.185.94 5.34

4.6

2008 2009 2010 2011 2012

Ave. Time to Process Application(Days)

4.253.42 3.38 3.06

2.12

2008 2009 2010 2011 2012

Ave. Time to Connect Application(Days)

IMPROVING CUSTOMER SERVICE

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 31/40

Country% Families with

Access toElectricity

Families withAccess

Total Number ofFamilies

Luzon 91.52 % 9,639 10,532

Visayas 81.55 % 3,010 3,691

Mindanao 75.04 % 3,172 4,227

Source: NSO - Number of Families by Presence of Electricity, Main Source of Water Supply, and Toilet Facilities and by Region: 2009

Meralco and the Philippines

Major Island Groups

MERALCO (2012) Philippines (2012)

Household 96.56% 77.60%

Barangay 100% 99.98%Source: DOE Accomplishment Report, 2012

Survey Population, in thousands

IMPROVING ACCESS TO SERVICE

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 32/40

Fast response and isolation ofhazardous and life threateningincidents

Timely and accurate informationon restoration efforts and power

situation

Ready 24 x 7 to respond to ourcustomers’ concerns

ENHANCING DISASTER PREPAREDNESS

“ Habagat ” in Au gu st , 2012

“ Habagat ” in Au gu st , 2013

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 33/40

MAKING A DIFFERENCE BEYOND OUR FRANCHISE

ASSISTANCE TO CABANATUAN ELECTRIC CORPORATION

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 34/40

ASSISTANCE TO CABANATUAN ELECTRIC CORPORATION(CELCOR) ON THE REPAIR OF DAMAGED ELECTRICFACILITIES DUE TO TYPHOON SANTI (OCT 18-22, 2013)

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 35/40

Meralco contingent in

Aklan, Capiz and Iloilo

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 36/40

Assessment

Meralco assessment team with CAPELCO Gen. Manager Edgar Diaz

Meralco Sector heads Gary Festin and Bernard Castro at assessmentsites

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 37/40

Arrival

Meralco Panay contingent line up along Aklan West Road on their way to theirrespective assignments in Kalibo in

Aklan, Roxas City in Capiz, and Sara inIloilo.

Meralco Sector heads give an overall briefing to the Panay contingent

Meralco crews arrived at the CaticlanPort in Aklan after almost 24 hours of

travel.

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 38/40

Efforts Meralco crews at work in different areas in Panay Island

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 39/40

MERALCO SMART GRID VISION 2021

7/21/2019 Meralco Presentation Nov 18

http://slidepdf.com/reader/full/meralco-presentation-nov-18 40/40