Embed Size (px)

Citation preview

Mega-merger of AB InBev – SAB Miller

Mergers & AcquisitionsCase Study

December 2015

NaCHANG

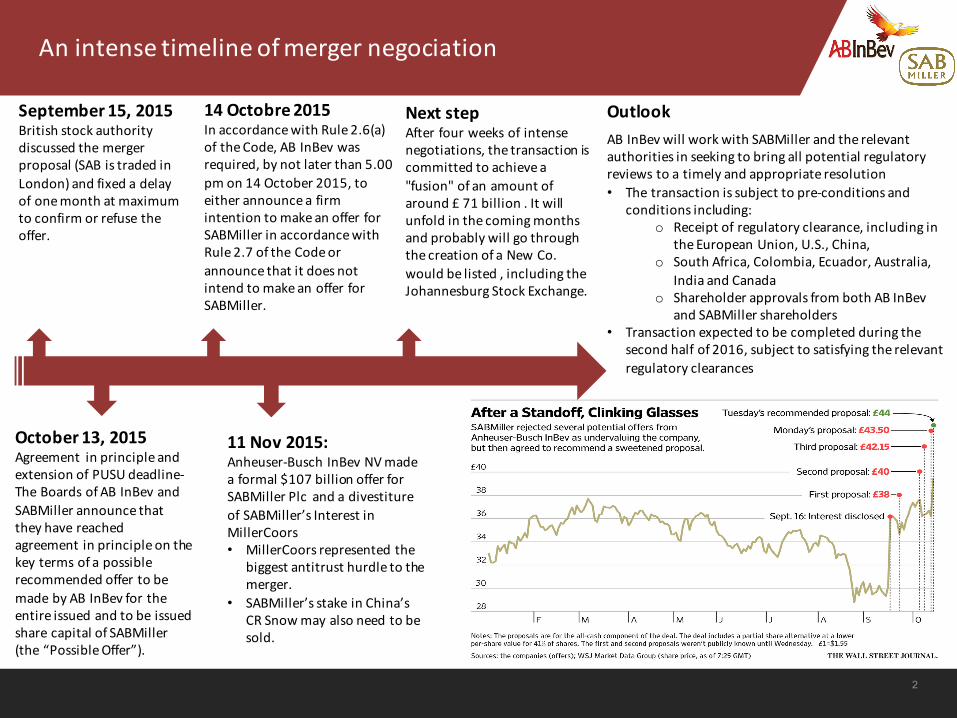

Anintensetimeline ofmerger negociation

2

September 15,2015Britishstockauthoritydiscussedthemergerproposal(SABistradedinLondon)andfixedadelayofonemonthatmaximumtoconfirmorrefusetheoffer.

14Octobre2015InaccordancewithRule2.6(a)oftheCode,ABInBev wasrequired,bynotlaterthan5.00pmon14October2015,toeitherannounceafirmintentiontomakeanofferforSABMillerinaccordancewithRule2.7oftheCodeorannouncethatitdoesnotintendtomakeanofferforSABMiller.

October13,2015Agreement inprincipleandextensionofPUSUdeadline-TheBoardsofABInBev andSABMillerannouncethattheyhavereachedagreementinprincipleonthekeytermsofapossiblerecommendedoffertobemadebyABInBev fortheentireissuedandtobeissuedsharecapitalofSABMiller(the“PossibleOffer”).

OutlookABInBev willworkwithSABMillerandtherelevantauthoritiesinseekingtobringallpotentialregulatoryreviewstoatimelyandappropriateresolution• Thetransactionissubjecttopre-conditionsand

conditionsincluding:o Receiptofregulatoryclearance,includingin

theEuropeanUnion,U.S.,China,o SouthAfrica,Colombia,Ecuador,Australia,

IndiaandCanadao ShareholderapprovalsfrombothABInBev

andSABMillershareholders• Transactionexpectedtobecompletedduringthe

secondhalfof2016,subjecttosatisfyingtherelevantregulatoryclearances

11Nov2015:Anheuser-BuschInBev NVmadeaformal$107billionofferforSABMillerPlcand adivestitureofSABMiller’sInterestinMillerCoors• MillerCoors representedthe

biggestantitrusthurdletothemerger.

• SABMiller’sstakeinChina’sCRSnowmayalsoneedtobesold.

NextstepAfterfourweeksofintensenegotiations,thetransactioniscommittedtoachievea"fusion"ofanamountofaround£71billion.ItwillunfoldinthecomingmonthsandprobablywillgothroughthecreationofaNewCo.wouldbelisted,includingtheJohannesburgStockExchange.

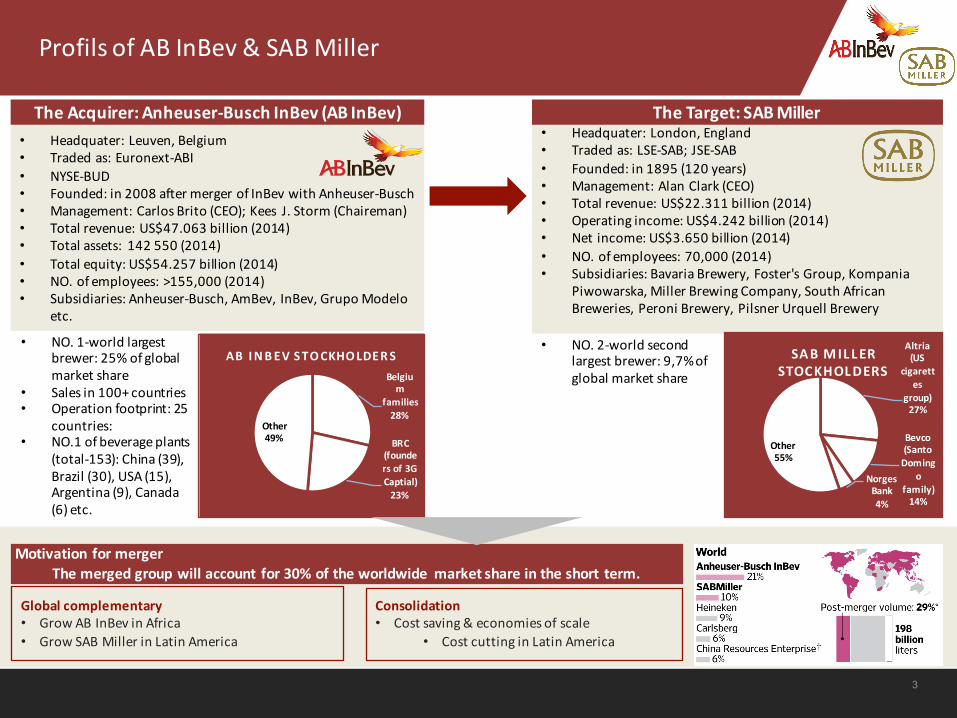

ProfilsofABInBev & SABMiller

3

Motivation formergerThemergedgroupwillaccount for30%oftheworldwide marketshareintheshort term.

TheAcquirer:Anheuser-BuschInBev (ABInBev) TheTarget:SABMiller• Headquater:Leuven,Belgium• Tradedas:Euronext-ABI• NYSE-BUD• Founded:in2008aftermergerofInBev withAnheuser-Busch• Management:CarlosBrito (CEO);Kees J.Storm(Chaireman)• Totalrevenue:US$47.063billion(2014)• Totalassets: 142550(2014)• Totalequity:US$54.257billion(2014)• NO.ofemployees:>155,000(2014)• Subsidiaries:Anheuser-Busch,AmBev,InBev,GrupoModelo

etc.

• NO.1-worldlargestbrewer:25%ofglobalmarketshare

• Salesin100+countries• Operationfootprint:25

countries:• NO.1ofbeverageplants

(total-153):China(39),Brazil(30),USA(15),Argentina(9),Canada(6)etc.

• Headquater:London,England• Tradedas:LSE-SAB;JSE-SAB• Founded:in1895(120years)• Management:AlanClark(CEO)• Totalrevenue:US$22.311billion(2014)• Operatingincome:US$4.242billion(2014)• Netincome:US$3.650billion(2014)• NO.ofemployees:70,000(2014)• Subsidiaries:BavariaBrewery,Foster'sGroup,Kompania

Piwowarska,MillerBrewingCompany,SouthAfricanBreweries,Peroni Brewery,PilsnerUrquell Brewery

• NO.2-worldsecondlargestbrewer:9,7%ofglobalmarketshareBelgiu

mfamilies28%

BRC(foundersof3GCaptial)23%

Other49%

AB INBEV STOCKHOLDERSAltria(US

cigarettes

group)27%

Bevco(SantoDoming

ofamily)14%

NorgesBank4%

Other55%

SABMILLERSTOCKHOLDERS

Globalcomplementary• GrowABInBev inAfrica• GrowSABMillerinLatinAmerica

Consolidation• Costsaving&economiesofscale

• CostcuttinginLatinAmerica

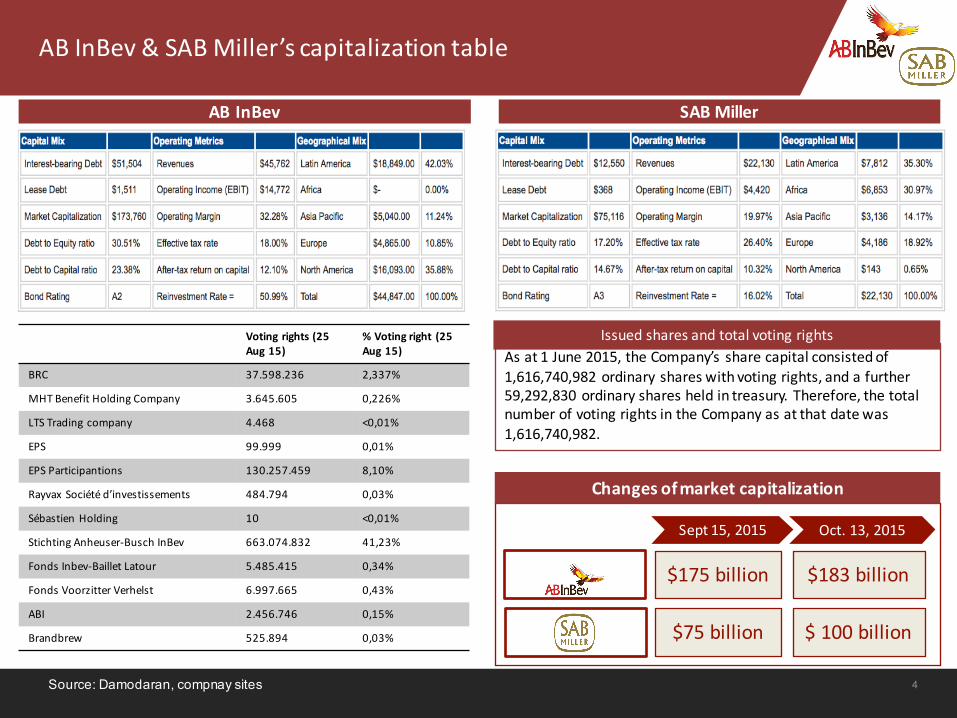

ABInBev &SABMiller’s capitalizationtable

4

ABInBev SABMiller

Voting rights(25Aug15)

%Voting right (25Aug15)

BRC 37.598.236 2,337%

MHTBenefitHolding Company 3.645.605 0,226%

LTS Tradingcompany 4.468 <0,01%

EPS 99.999 0,01%

EPSParticipantions 130.257.459 8,10%

Rayvax Société d’investissements 484.794 0,03%

Sébastien Holding 10 <0,01%

Stichting Anheuser-BuschInBev 663.074.832 41,23%

Fonds Inbev-Baillet Latour 5.485.415 0,34%

Fonds Voorzitter Verhelst 6.997.665 0,43%

ABI 2.456.746 0,15%

Brandbrew 525.894 0,03%

Sept15,2015 Oct.13,2015

$175billion

$75billion

$183billion

$100billion

Changesofmarketcapitalization

Asat1June 2015,theCompany’s share capitalconsistedof1,616,740,982ordinary shares with voting rights,andafurther59,292,830ordinary shares held intreasury.Therefore,thetotalnumber ofvoting rights intheCompany asatthat datewas1,616,740,982.

Issued shares andtotalvoting rights

Source: Damodaran, compnay sites

ABInBevSABMillerHeineken

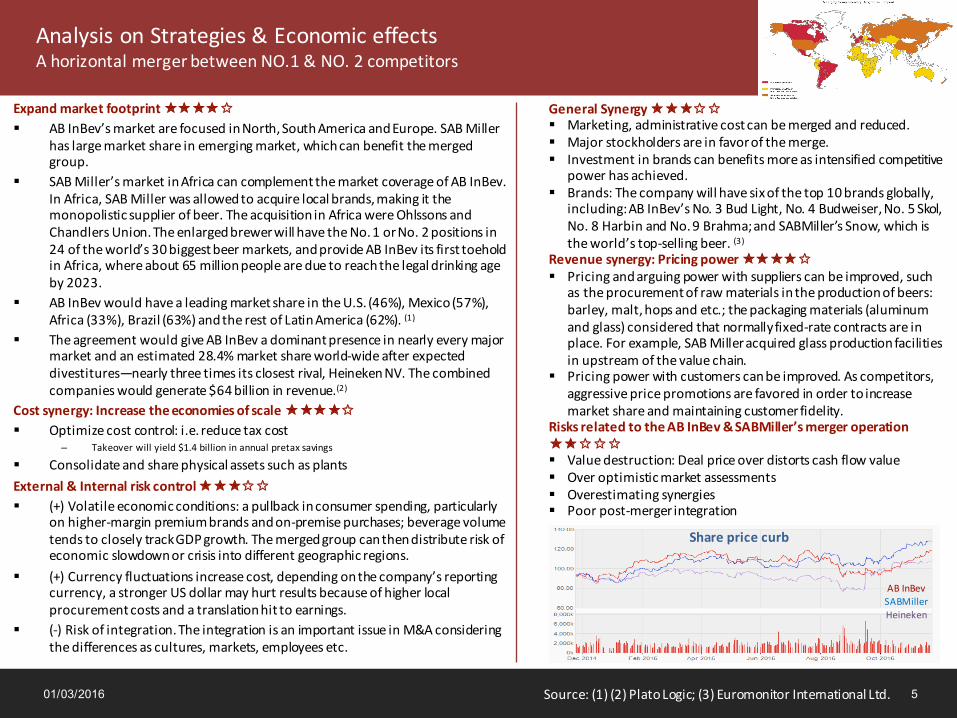

Sharepricecurb

AnalysisonStrategies&EconomiceffectsAhorizontalmergerbetweenNO.1&NO.2competitors

Expandmarketfootprint✭✭✭✭✩§ ABInBev’smarketarefocusedinNorth,SouthAmericaandEurope.SABMiller

haslargemarketshareinemergingmarket,whichcanbenefitthemergedgroup.

§ SABMiller’smarketinAfricacancomplementthemarketcoverageofABInBev.InAfrica,SABMillerwasallowedtoacquirelocalbrands,makingitthemonopolistic supplierofbeer.TheacquisitioninAfricawereOhlssons andChandlersUnion.TheenlargedbrewerwillhavetheNo.1orNo.2positionsin24oftheworld’s30biggestbeermarkets,andprovideABInBev itsfirsttoeholdinAfrica,whereabout65millionpeopleareduetoreachthelegaldrinkingageby2023.

§ ABInBev wouldhavealeadingmarketshareintheU.S.(46%),Mexico(57%),Africa(33%),Brazil(63%)andtherestofLatinAmerica(62%).(1)

§ TheagreementwouldgiveABInBev adominantpresenceinnearlyeverymajormarketandanestimated28.4%marketshareworld-wideafterexpecteddivestitures—nearlythreetimesitsclosestrival,HeinekenNV.Thecombinedcompanieswouldgenerate$64billioninrevenue.(2)

Costsynergy:Increasetheeconomiesofscale✭✭✭✭✩§ Optimizecostcontrol:i.e.reducetaxcost

– Takeoverwillyield$1.4billioninannualpretaxsavings

§ ConsolidateandsharephysicalassetssuchasplantsExternal&Internalriskcontrol✭✭✭✩✩§ (+)Volatileeconomicconditions:apullbackinconsumerspending,particularly

onhigher-marginpremiumbrandsandon-premisepurchases;beveragevolumetendstocloselytrackGDPgrowth.Themergedgroupcanthendistributeriskofeconomicslowdownorcrisisintodifferentgeographicregions.

§ (+)Currencyfluctuationsincreasecost,dependingonthecompany’sreportingcurrency,astrongerUSdollarmayhurtresultsbecauseofhigherlocalprocurementcostsandatranslationhittoearnings.

§ (-)Riskofintegration.TheintegrationisanimportantissueinM&Aconsideringthedifferencesascultures,markets,employeesetc.

01/03/2016 5Source:(1)(2)PlatoLogic;(3)Euromonitor InternationalLtd.

General Synergy✭✭✭✩✩§ Marketing,administrativecostcanbemergedandreduced.§ Majorstockholdersareinfavorofthemerge.§ Investmentinbrandscanbenefitsmoreasintensifiedcompetitive

powerhasachieved.§ Brands:Thecompanywillhavesixofthetop10brandsglobally,

including:ABInBev’s No.3BudLight,No.4Budweiser,No.5Skol,No.8HarbinandNo.9Brahma;andSABMiller’sSnow,whichistheworld’stop-sellingbeer.(3)

Revenuesynergy:Pricingpower✭✭✭✭✩§ Pricingandarguingpowerwithsupplierscanbeimproved,such

astheprocurementofrawmaterialsintheproductionofbeers:barley,malt,hopsandetc.;thepackagingmaterials(aluminumandglass)consideredthatnormallyfixed-ratecontractsareinplace.Forexample,SABMilleracquiredglassproductionfacilitiesinupstreamofthevaluechain.

§ Pricingpowerwithcustomerscanbeimproved.Ascompetitors,aggressivepricepromotionsarefavoredinordertoincreasemarketshareandmaintainingcustomerfidelity.

RisksrelatedtotheABInBev&SABMiller’smergeroperation✭✭✩✩✩§ Valuedestruction:Dealpriceoverdistortscashflowvalue§ Overoptimisticmarketassessments§ Overestimatingsynergies§ Poorpost-mergerintegration

Dealstructuresteps

M&AAnalysis

01/03/2016 6

v Negativeconsequencesthatfollowfromthisdeal:Thefirstisthatwhenantitrustregulatorsindifferentpartsoftheworldwillbepayingcloseattentiontothisdeal,anditseemslikelythatSABMillerwillbeforcedtosellits58%stakeinMillerCoors andthatMolsonCoors,theotherJVpartner,willbethebeneficiary.

§ RegulatoryhurdleinU.S.market,whereABInBev alreadyhasaroughly45%marketshareandSABMillercontrolsafurther25%throughitsMillerCoors LLCjointventurewithMolsonCoorsBrewingCo.

§ PotentialregulatoryhurdleisChina,whereABInBev hada14%marketsharelastyear*ChineseauthoritiescouldrequirethebrewertoexitSABMiller’sjointventurewithChinaResourcesEnterpriseLtd.,whichcontrols23%ofthemarketandproducesthetop-sellingSnowbrand.SomedivestiturescouldalsoberequiredinLatinAmerica.

Dealfeatures Strategicrationale &Motivations

Deallimits

v Dealtype:Amicable.ABInBev hasrecieved irrevocableundertakingsfrom Altria&BEVCO,whocollectively own approximately40,45%ofSABMIller’s issued share capital,tovoteinfavor ofthetransactionandtoelect forthePartialShareAlternative(PSA)fortheentirebeneficialholdingsofSABMiller shares.

v ABInBevReferenceShareholder(b),EPSParticipationsSˆrlandBRCSˆrl,who collectivelyhold approximately51.8%(c)oftheissuedshare capitalofABInBev,haveprovided irrevocableundertakings tovoteinfavorofthetransaction.

v SABMiller shareholderswill beentitledtoreceive foreachSABMillershareeither:£44.0in cash;or aPSAcomprised of 0,483969RestrictedShares plus £3,7788in cash.

v Financing:Structuring therequired fundingwill alsoprove complex,withABInBev workingwithabout10banks toarrangeasmuchas$70billioninfinancing.

v ABInBev turned toLazardforfinancial advice andits corporatebrokerDeutscheBankAG,aswell aslawyers fromFreshfields BruckhausDeringer andCravath Swaine&Moore.RobeyWarshaw,JPMorganChase&Co.,MorganStanleyandGoldmanSachs&Co.areadvising SABMiller,which sought legal advice fromLinklaters andHogan Lovells International.

v Brings together alargely complementary geographic footprint withaccess tohigh-growth regions (e.g.,Africa,AsiaandCentral&SouthAmerica).

v Builds onSABMiller’s SouthAfrican heritageandcommitment totheAfrican continent–acritical driverforthefuturegrowth ofthebusiness

v Generates significant growth opportunities forthecombinedportfolioofleading global,nationalandlocalbrands.

v Gainsfrom theexperience,commitment anddriveofthecombinedglobaltalentpool

v Benefits from revenue,cost andcashflowsynergies

1. Theshares ofSABMiller will beacquired byNewco(aBelgiancompanyformed forthepurposeofthis transaction)inexchangefortheissueofNewcoshares toSABMiller shareholders

2. ABInBev will acquireNewcoshares offormerSABMillershareholders tosatisfy thecashcomponents

3. ABInBevwill subsequently merge intoNewco,so that,following thecompletionofthetransaction,Newcowill be thenewholdingcompanyforthecombined group.

*Source:Euromonitor International

Recommendation forABInBev shareholders

01/03/2016 7

Merger effects

Shareholder price Shareholder vote

v Themerged groupcan complement thegeographic footprints particularly Africa andother emerging markets,which arepotentialgrowth engine inthe longrun.Shareprice islikely togoupward with positivegrowthprospect.

v Synergiesinterms ofcost control,operationefficiency,revenueimprovement,pricingpowerimprovement is likely toinputmorecapitalinto equity.Shareholders can thenbenefit from these operational profits.

v Theshareholders ofABInBev arelikely toexperience adilution inanewly combinedcompany ofvoting powerduetotheincreased number ofshares released duringthemerger process.

Inprinciple,theacquirer ABInBev can benefit frommerger synergiesindifferent aspectsinterms ofoperational profitsandmarket confidance,which is likely toenrich sharesholders’pockets.

Recommendation forSABMillershareholders

01/03/2016 8

Merger effects

Shareholder price Shareholder vote

v Theshareholders ofSABMillerarelikely toexperience adilutionofvoting powerinanewly combined company duetotheincreased number ofshares released duringthemerger process.

v AsSABMilleris likely toenlarge its brandportfolioandreduce thecompetition costsuch aslow pricing war,aswell asthetalentpoolanddistribution infrastructureofABInBev,theoperational revenuesarelikely tobenefit from themerger inthelongrun,which hasgreat potential toimprovemarketinsightandaugmentthestockprice.

Inprinciple,thetarget SABMilleris likely tobe involved inthedouble-win game,asthepreceedingperiod,theupwarded stockprice improve market confidance andincrease shareholders’profitsintheshortrun.Inthelongrun,thecombined groupwill benefit SABMillerequally.

Conclusion

01/03/2016 9

v 35%- 50%premiumofprice is relativehigh,causing pressureformanagementofnewcombined company todeliver very goodperformanceinorder tocover it.

v Horizontaloperation between these twocompanies might causecannibalization effects ofdifferent brands insame markets.

v Inpostmergephase, themerge oftwo differentcorporate cultureandgeneralmanagementneedextraattention.

v Facing authorities challengeregarding anti-trust.

Strengths Weaknesses

Keymessages

Theacquisitiondealis likely torestructuretheindustry toagreat extent interms ofgeographiccoverage,thepowerofnegociation inthevaluechain,theefficiency andcontrolofoperations,which leadtothepositiveprospectsofshareholders’benefits.

v Completion ofgeographic distribution- build uptruly globalpresence,with access tohigh-growthregions (Africa,Asia,Central&SouthAmerica)

v Improve therisk controlthanks toadiversifiedmarket distribution andbrands

v Generates significant growth opportunities forthecombined portfolio ofleading global,nationalandlocalbrands

v Benefits from revenue, cost,cashflowandtaxsynergies

References

§ http://www.ft.com/intl/cms/s/0/51bb21fa-6cba-11e5-8171-ba1968cf791a.html#axzz3sFk2nleJ§ http://www.wsj.com/articles/ab-inbev-seeking-finance-for-sabmiller-deal-1410779802§ http://www.sabmiller.com/investors§ http://www.ab-inbev.com/investors.html§ http://www.sec.gov/Archives/edgar/data/310569/000095013708009337/c30926cdefa14a.htm§ http://www.bloomberg.com/news/articles/2015-11-11/ab-inbev-to-buy-sabmiller-for-107-billion-as-u-s-deal-

agreed

01/03/2016 10