Embed Size (px)

Citation preview

Meg LassaratCFO

Mustang

Meg LassaratCFO

Mustang

Thought Leadership onRisk and ChangeThought Leadership onRisk and Change

Plenary Session ThreePlenary Session Three

Session ModeratorECC Board Member

Thought Leadership on Risk and ChangeThought Leadership on Risk and Change

Jerry R. StrawserDean,Mays Business School

Texas A&M University

Jerry R. StrawserDean,Mays Business School

Texas A&M University

Thought Leadership on Risk and ChangeThought Leadership on Risk and Change

Dr. William H. GlickDean and H. Joe Nelson III Professor of Management at the Jesse H. Jones Graduate School of Business

Rice University

Dr. William H. GlickDean and H. Joe Nelson III Professor of Management at the Jesse H. Jones Graduate School of Business

Rice University

Doing Business in the “Reset” Economy

Doing Business in the “Reset” Economy

Jerry Strawser, DeanKPMG Chair in Accounting

Mays Business SchoolTexas A&M University

Jerry Strawser, DeanKPMG Chair in Accounting

Mays Business SchoolTexas A&M University

Doing Business in the “Reset” Economy

Doing Business in the “Reset” Economy

In the last 6 months, have things:In the last 6 months, have things:

4%

44%

22%

22%

8%

1. Gotten much better

2. Gotten a little better

3. Stayed about the same

4. Gotten a little worse

5. Gotten much worse

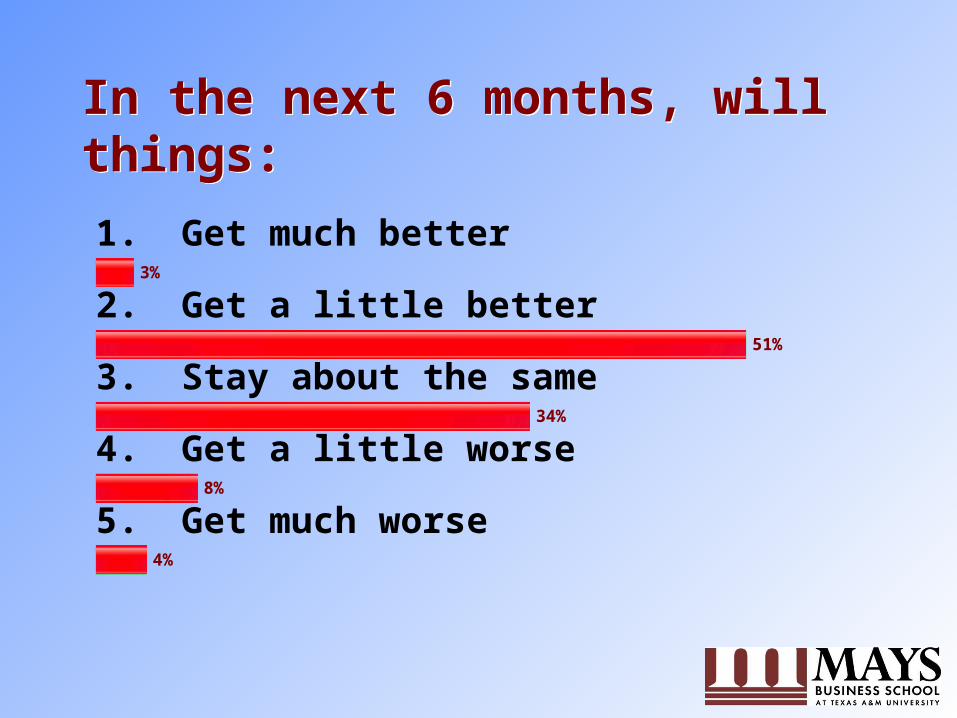

In the next 6 months, will things:In the next 6 months, will things:

3%

51%

34%

8%

4%

1. Get much better

2. Get a little better

3. Stay about the same

4. Get a little worse

5. Get much worse

When do you think things willget back to “normal”?When do you think things willget back to “normal”?

0%

16%

64%

20%

1. Within the next 6 months

2. Sometime during 2010

3. Sometime after 2010

4. Never

So What Happened?So What Happened?

Source: The Conference Board

Consumer Confidence IndexConsumer Confidence Index

30405060708090

100110120130140150

Aug-00

Feb-01

Aug-01

Feb-02

Aug-02

Feb-03

Aug-03

Feb-04

Aug-04

Feb-05

Aug-05

Feb-06

Aug-06

Feb-07

Aug-07

Feb-08

Aug-08

Feb-09

30405060708090

100110120130140150

Aug-00

Feb-01

Aug-01

Feb-02

Aug-02

Feb-03

Aug-03

Feb-04

Aug-04

Feb-05

Aug-05

Feb-06

Aug-06

Feb-07

Aug-07

Feb-08

Aug-08

Feb-09

Source: www.conference-board.org/

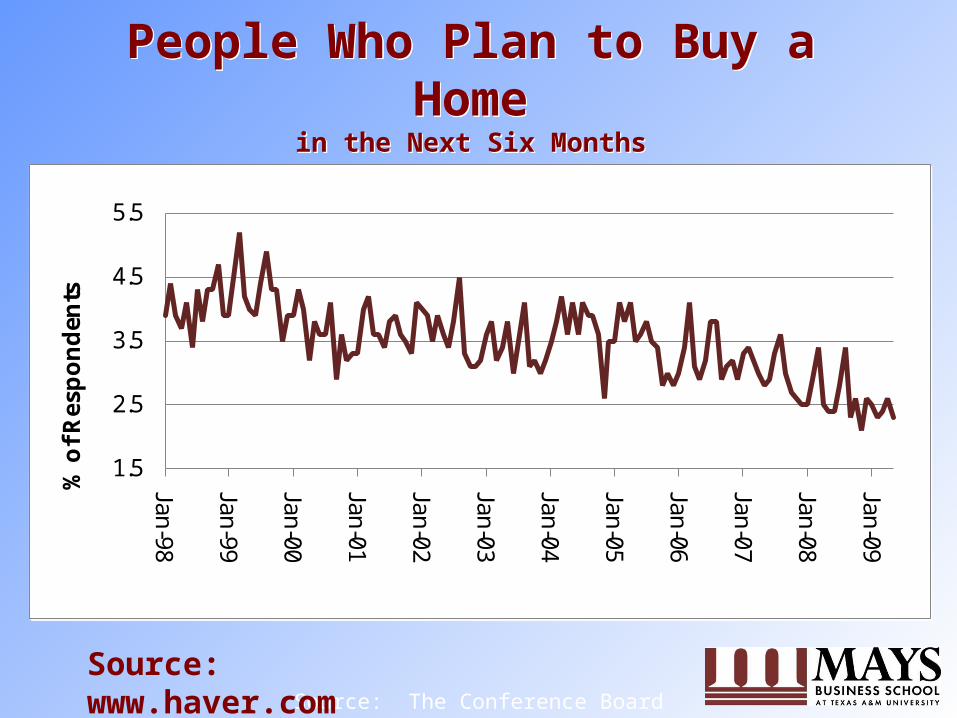

People Who Plan to Buy a Homein the Next Six Months

People Who Plan to Buy a Homein the Next Six Months

Source: The Conference Board

1.5

2.5

3.5

4.5

5.5

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09%

of

Res

po

nd

ents

1.5

2.5

3.5

4.5

5.5

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09%

of

Res

po

nd

ents

Source: www.haver.com

0

5

10

15

20

25

30

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09%

of

Res

po

nd

ents

0

5

10

15

20

25

30

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09%

of

Res

po

nd

ents

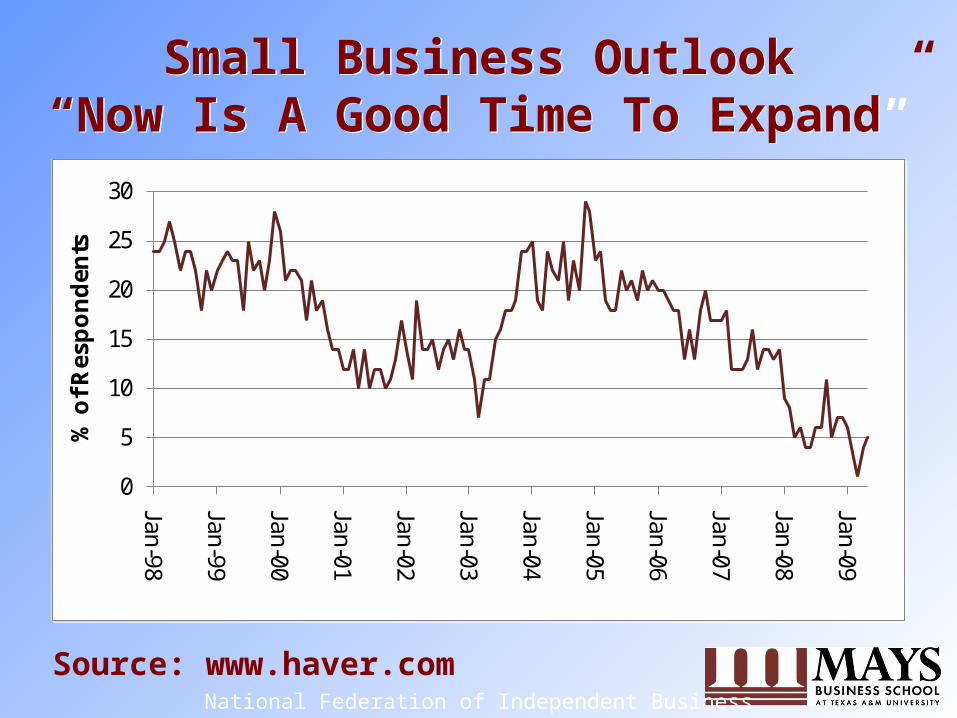

Small Business Outlook“Now Is A Good Time To Expand”

Small Business Outlook“Now Is A Good Time To Expand”

National Federation of Independent Business

Source: www.haver.com

National Federation of Independent Business

-10

-5

0

5

10

15

20

25

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09N

et %

of

Res

po

nd

ents

-10

-5

0

5

10

15

20

25

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09N

et %

of

Res

po

nd

ents

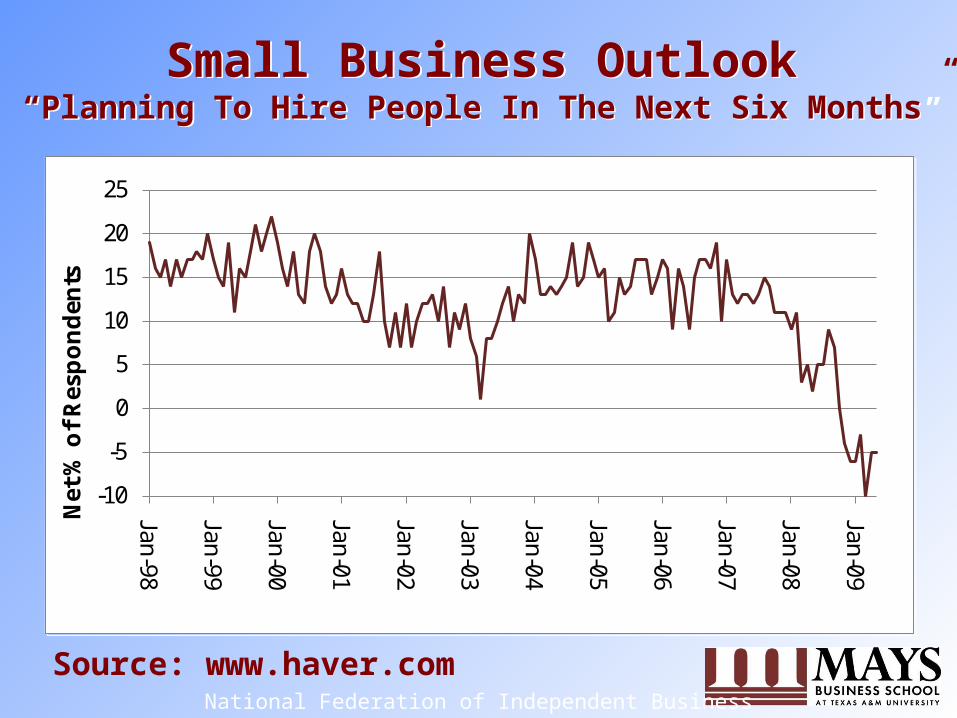

Small Business Outlook“Planning To Hire People In The Next Six Months”

Small Business Outlook“Planning To Hire People In The Next Six Months”

Source: www.haver.com

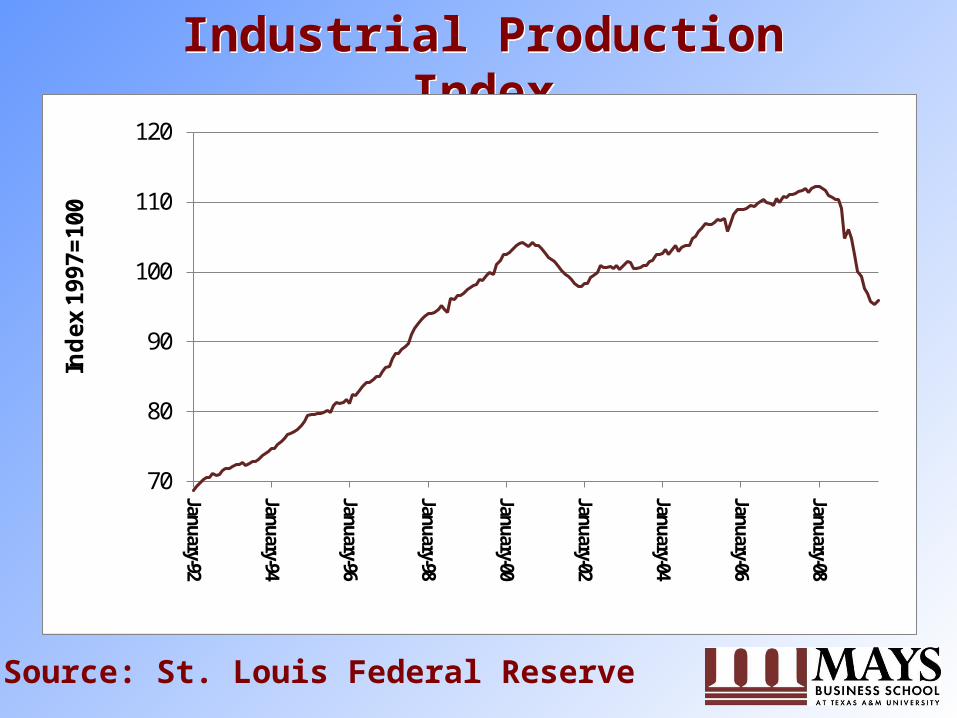

Industrial Production IndexIndustrial Production Index

70

80

90

100

110

120

January-92

January-94

January-96

January-98

January-00

January-02

January-04

January-06

January-08

Ind

ex

1997=

100

Source: St. Louis Federal Reserve

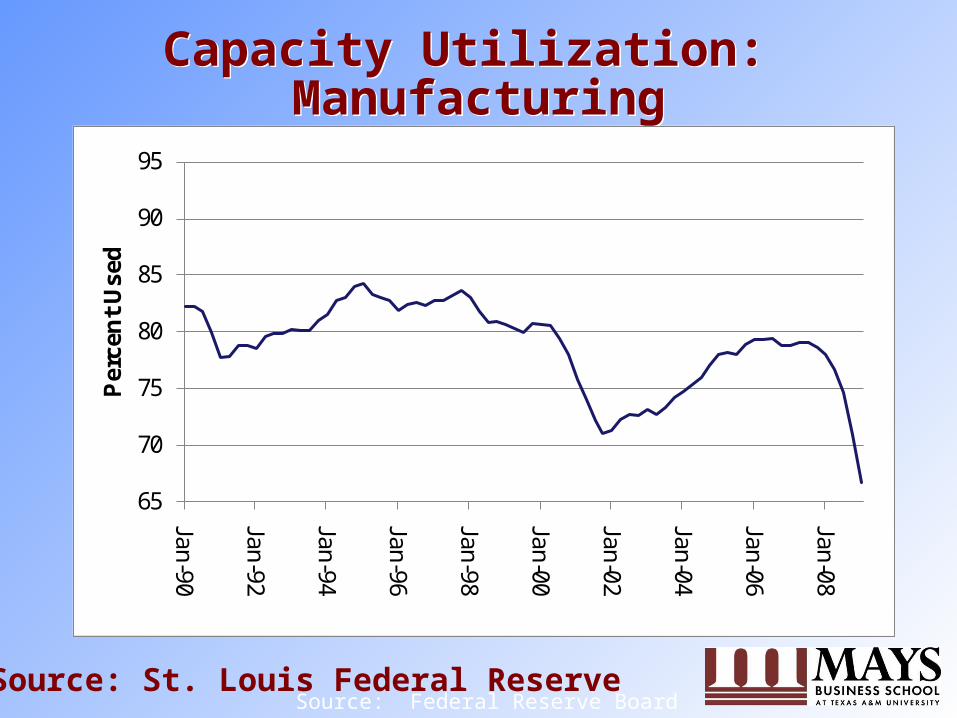

Capacity Utilization: Manufacturing

Capacity Utilization: Manufacturing

Source: Federal Reserve Board

65

70

75

80

85

90

95

Jan-90

Jan-92

Jan-94

Jan-96

Jan-98

Jan-00

Jan-02

Jan-04

Jan-06

Jan-08P

erce

nt

Use

d

Source: St. Louis Federal Reserve

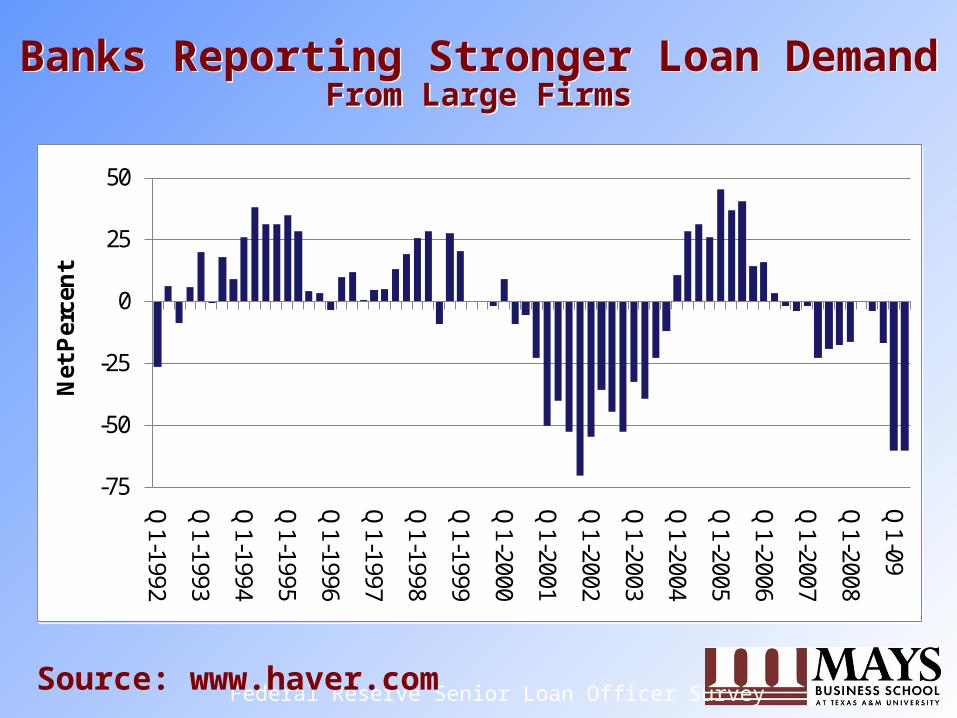

Banks Reporting Stronger Loan DemandFrom Large Firms

Banks Reporting Stronger Loan DemandFrom Large Firms

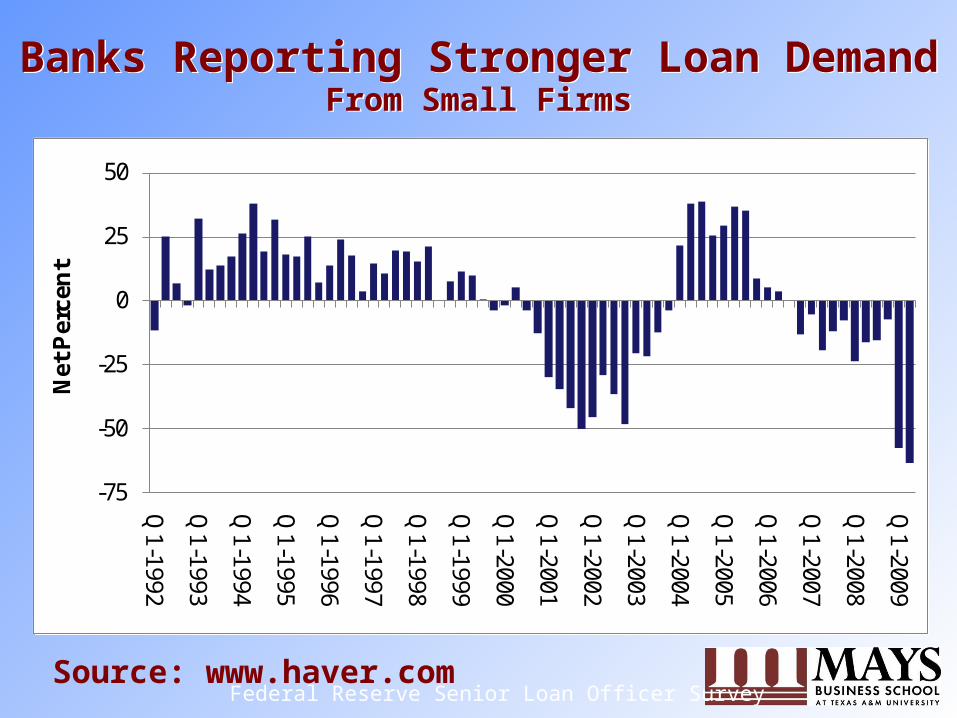

Federal Reserve Senior Loan Officer Survey

-75

-50

-25

0

25

50

Q1-1992

Q1-1993

Q1-1994

Q1-1995

Q1-1996

Q1-1997

Q1-1998

Q1-1999

Q1-2000

Q1-2001

Q1-2002

Q1-2003

Q1-2004

Q1-2005

Q1-2006

Q1-2007

Q1-2008

Q1-09

Net

Per

cen

t

-75

-50

-25

0

25

50

Q1-1992

Q1-1993

Q1-1994

Q1-1995

Q1-1996

Q1-1997

Q1-1998

Q1-1999

Q1-2000

Q1-2001

Q1-2002

Q1-2003

Q1-2004

Q1-2005

Q1-2006

Q1-2007

Q1-2008

Q1-09

Net

Per

cen

t

Source: www.haver.com

Federal Reserve Senior Loan Officer Survey

-75

-50

-25

0

25

50

Q1-1992

Q1-1993

Q1-1994

Q1-1995

Q1-1996

Q1-1997

Q1-1998

Q1-1999

Q1-2000

Q1-2001

Q1-2002

Q1-2003

Q1-2004

Q1-2005

Q1-2006

Q1-2007

Q1-2008

Q1-2009

Net

Per

cen

t

-75

-50

-25

0

25

50

Q1-1992

Q1-1993

Q1-1994

Q1-1995

Q1-1996

Q1-1997

Q1-1998

Q1-1999

Q1-2000

Q1-2001

Q1-2002

Q1-2003

Q1-2004

Q1-2005

Q1-2006

Q1-2007

Q1-2008

Q1-2009

Net

Per

cen

tBanks Reporting Stronger Loan Demand

From Small FirmsBanks Reporting Stronger Loan Demand

From Small Firms

Source: www.haver.com

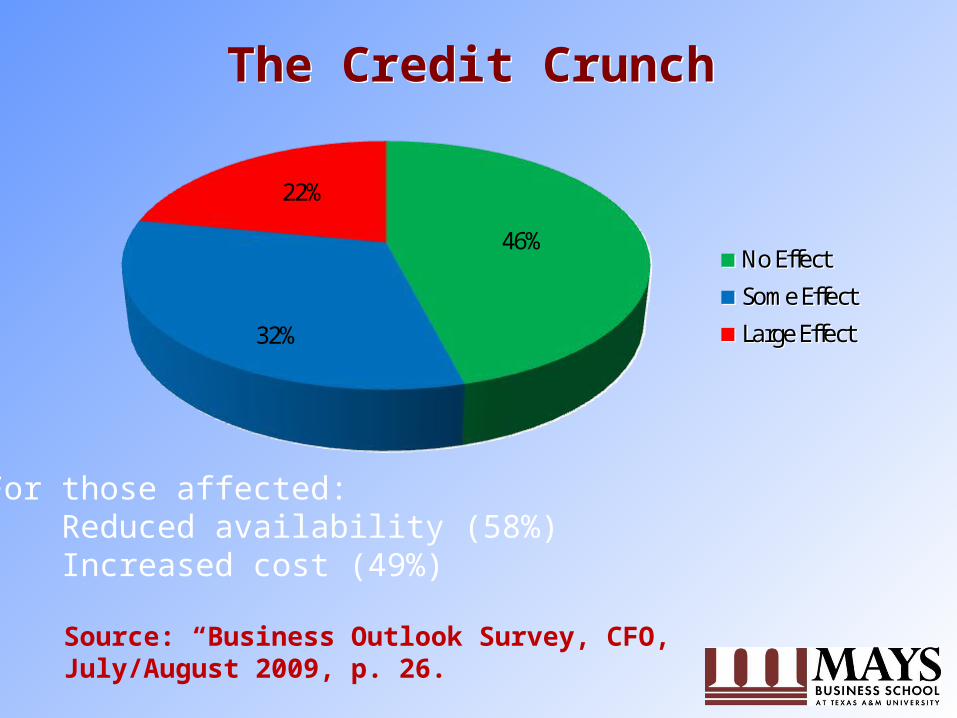

The Credit CrunchThe Credit Crunch

46%

32%

22%

No Effect

Some Effect

Large Effect

46%

32%

22%

No Effect

Some Effect

Large Effect

For those affected:• Reduced availability (58%)• Increased cost (49%)

Source: “Business Outlook Survey, CFO, July/August 2009, p. 26.

US Civilian Unemployment RateUS Civilian Unemployment Rate

0

2

4

6

8

10

12

Jan-81

Jan-83

Jan-85

Jan-87

Jan-89

Jan-91

Jan-93

Jan-95

Jan-97

Jan-99

Jan-01

Jan-03

Jan-05

Jan-07

Jan-09(P

erce

nt)

Source: St. Louis Federal Reserve

US Employment:Construction

US Employment:Construction

Source: Bureau of Labor Statistics

NAICS 23Building, developing, construction of

Houses, buildings, power lines, highways, streets and bridges

4,000

5,000

6,000

7,000

8,000

Jan-90

Jan-92

Jan-94

Jan-96

Jan-98

Jan-00

Jan-02

Jan-04

Jan-06

Jan-08

Th

ou

san

ds

of

Wo

rker

s

Source: St. Louis Federal Reserve

US Employment:Government

US Employment:Government

Source: Bureau of Labor Statistics

Sector 92: Executive, legislative, justice, public safety, humanResources, environmental quality, planning, national security.

National, state and local government.This includes civilian employees only, military personnel are excluded.

18,000

19,000

20,000

21,000

22,000

23,000

Jan-90

Jan-92

Jan-94

Jan-96

Jan-98

Jan-00

Jan-02

Jan-04

Jan-06

Jan-08T

ho

usa

nd

s o

f W

ork

ers

Source: St. Louis Federal Reserve

Oil PricesOil Prices

Source: http://tonto.eia.doe/gov/dnav/pet/hist

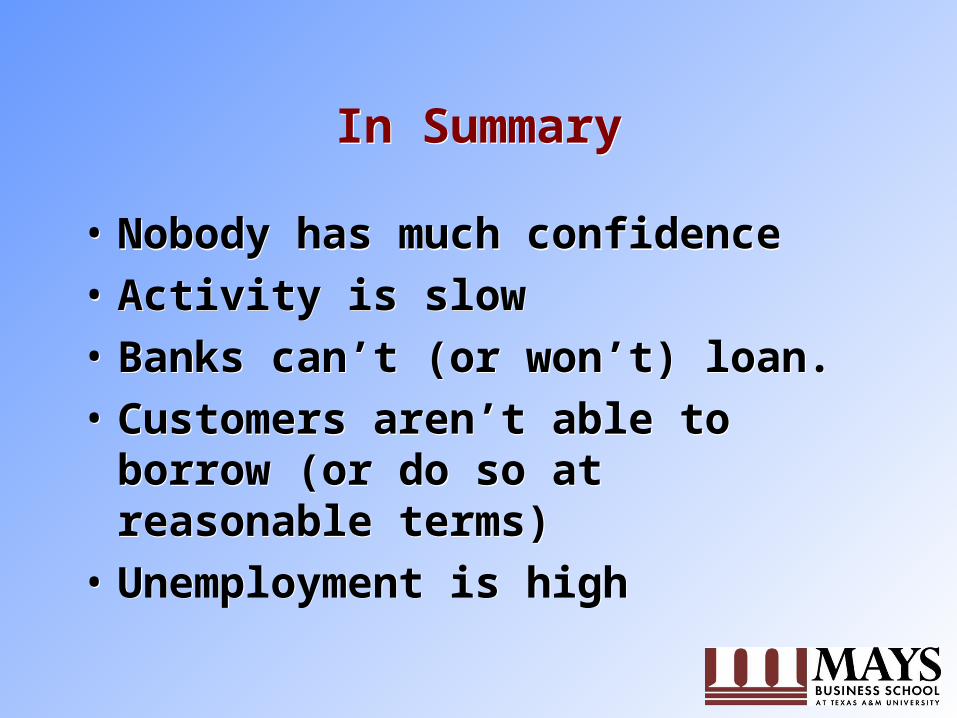

In SummaryIn Summary

• Nobody has much confidence

• Activity is slow

• Banks can’t (or won’t) loan.

• Customers aren’t able to borrow (or do so at reasonable terms)

• Unemployment is high

• Nobody has much confidence

• Activity is slow

• Banks can’t (or won’t) loan.

• Customers aren’t able to borrow (or do so at reasonable terms)

• Unemployment is high

The Best Case ScenarioThe Best Case Scenario

• Rise in stock price followed by favorable corporate earnings 4Q09

• Consumer confidence rises with stocks

• Foreclosure pressure continues to be heavy

• More spending results in higher profits

• Layoffs end by the end of the 2009

• “Jobless recovery” in 2010• Higher interest rates and

inflation in 2010-11

• Rise in stock price followed by favorable corporate earnings 4Q09

• Consumer confidence rises with stocks

• Foreclosure pressure continues to be heavy

• More spending results in higher profits

• Layoffs end by the end of the 2009

• “Jobless recovery” in 2010• Higher interest rates and

inflation in 2010-11

The Worst Case ScenarioThe Worst Case Scenario

• No effective fiscal package gets passed

• Treasury and Fed continue to stumble

• Bad banks and businesses propped up

• No price discovery for “toxic” mortgages

• Political risk for business stays high

• Business / investors “sit on their hands”

• Unemployment goes well over 10%

• Commodity deflation and price deflation

• No effective fiscal package gets passed

• Treasury and Fed continue to stumble

• Bad banks and businesses propped up

• No price discovery for “toxic” mortgages

• Political risk for business stays high

• Business / investors “sit on their hands”

• Unemployment goes well over 10%

• Commodity deflation and price deflation

Which is it?Which is it?

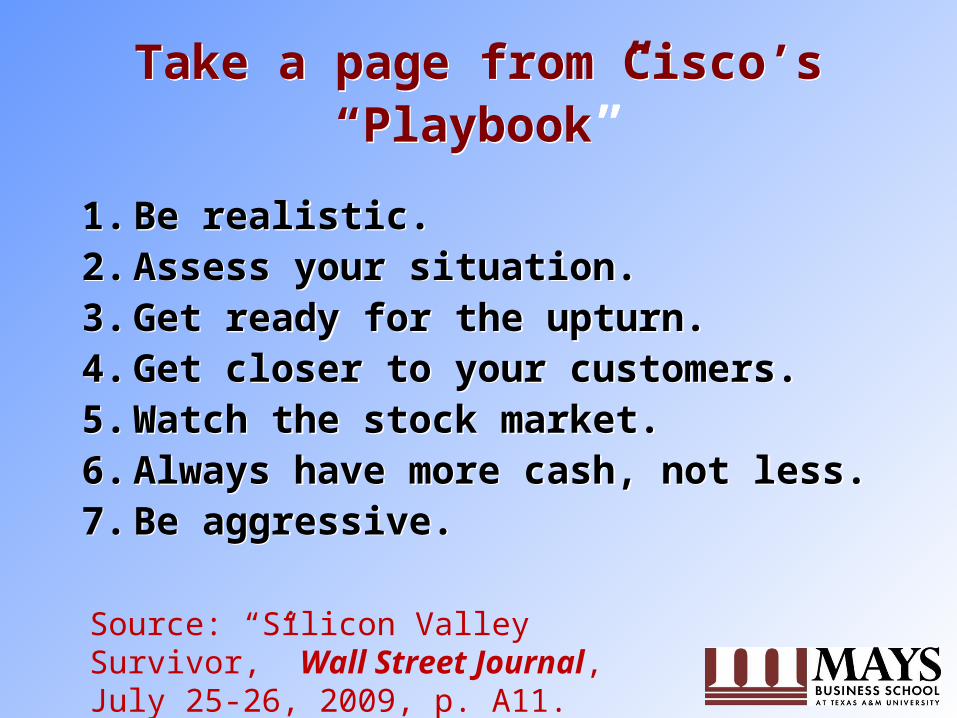

Take a page from Cisco’s “Playbook”

Take a page from Cisco’s “Playbook”

1. Be realistic. 2. Assess your situation. 3. Get ready for the upturn.4. Get closer to your customers.5. Watch the stock market.6. Always have more cash, not less.7. Be aggressive.

1. Be realistic. 2. Assess your situation. 3. Get ready for the upturn.4. Get closer to your customers.5. Watch the stock market.6. Always have more cash, not less.7. Be aggressive.

Source: “Silicon Valley Survivor,” Wall Street Journal, July 25-26, 2009, p. A11.

Three more ... Three more ...

1. Tough economies will pare the field of weak competitors

2. Tough economies provide cover for certain behaviors and decisions (customers, suppliers, and employees)

3. Everything is up for grabs. Use this as a business development opportunity.

1. Tough economies will pare the field of weak competitors

2. Tough economies provide cover for certain behaviors and decisions (customers, suppliers, and employees)

3. Everything is up for grabs. Use this as a business development opportunity.

How Others Have CopedHow Others Have Coped

• GE: Communicating inside and outside• Nalco: Motivating employees to cut costs• Avon: Changing marketing to reflect the

times• Waste Management: Getting customers to

share the pain

• GE: Communicating inside and outside• Nalco: Motivating employees to cut costs• Avon: Changing marketing to reflect the

times• Waste Management: Getting customers to

share the pain

Source: “My Recovery Playbook,” Fortune, August 31, 2009, pp. 61-66.

What is your Company Doing?What is your Company Doing?

0% 10% 20% 30% 40% 50% 60% 70%

Excuse to restructure

Reducing R&D

Streamlining offerings

Changing terms with suppliers

Reengineering processes

Deferring new hiring

Layoffs

Limiting travel

0% 10% 20% 30% 40% 50% 60% 70%

Excuse to restructure

Reducing R&D

Streamlining offerings

Changing terms with suppliers

Reengineering processes

Deferring new hiring

Layoffs

Limiting travel

Source: “How Bleak is the Landscape?,” Harvard Business Review, July-August 2009, 92-93.

What Opportunities is your Company Considering?

What Opportunities is your Company Considering?

0% 10% 20% 30% 40% 50%

Creating new products/services

Improving current products/services

Negotiating better terms w/suppliers

Encouraging entrepreneurial …

Targeting new customers

Restructuring for efficiency

0% 10% 20% 30% 40% 50%

Creating new products/services

Improving current products/services

Negotiating better terms w/suppliers

Encouraging entrepreneurial …

Targeting new customers

Restructuring for efficiency

Source: “How Bleak is the Landscape?,” Harvard Business Review, July-August 2009, 92-93.

What can Happen During a Recession?

What can Happen During a Recession?

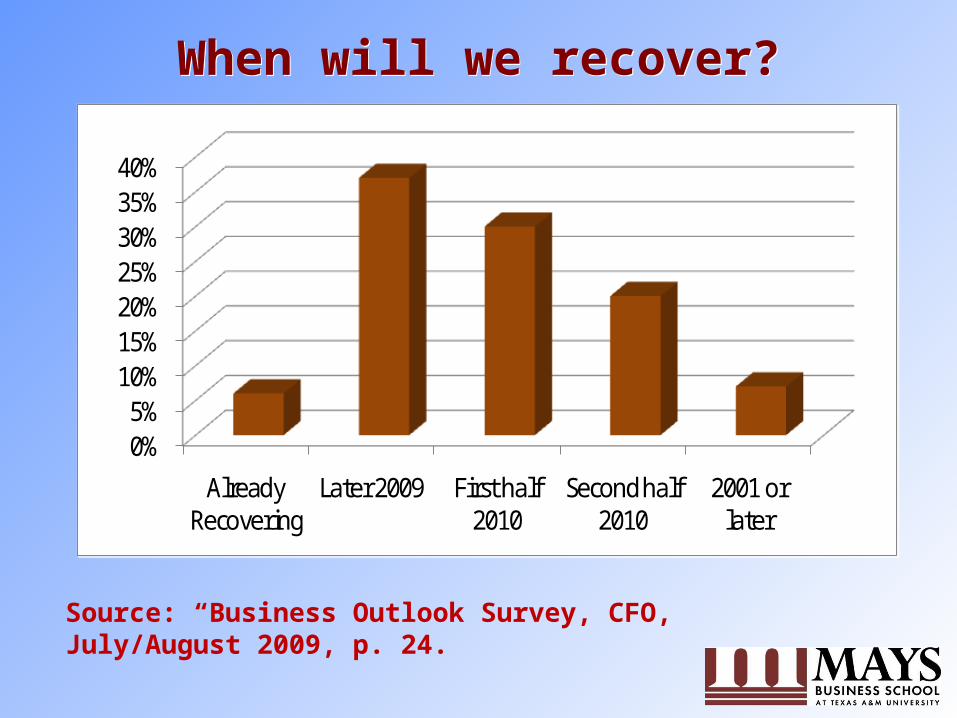

When will we recover?When will we recover?

0%5%

10%15%20%25%30%35%40%

Already Recovering

Later 2009 First half 2010

Second half 2010

2001 or later

0%5%

10%15%20%25%30%35%40%

Already Recovering

Later 2009 First half 2010

Second half 2010

2001 or later

Source: “Business Outlook Survey, CFO, July/August 2009, p. 24.