Embed Size (px)

Citation preview

Meeting Your Income Needs in Retirement

12383 082608

Expectations

& Expenses

12383 082608

47% of workers have tried to

estimate how much money they’ll

need in retirement.

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2008 Retirement Confidence Survey®.

12383 082608

44% changed their retirement plans

59% started saving more

Source: Employee Benefit Research Institute and Mathew Greenwald & Associates, Inc., 2008 Retirement Confidence Survey®.

12383 082608

12383 082608

At this stage of your life,

what are your goals?

12383 082608

Financial Life Cycle

Source: Gail M. Gordon, “The Life Cycle of Financial Planning,” University of Wyoming Cooperative Extension Service, 2001.

12383 082608

Source: Gail M. Gordon, “The Life Cycle of Financial Planning,” University of Wyoming Cooperative Extension Service, 2001.

12383 082608

Goal 1

Protect Against Risks

What are your goals

in this category?

Source: Gail M. Gordon, “The Life Cycle of Financial Planning,” University of Wyoming Cooperative Extension Service, 2001.

12383 082608

Goal 2

Ensure Financial Security

What are your goals

in this category?

Source: Gail M. Gordon, “The Life Cycle of Financial Planning,” University of Wyoming Cooperative Extension Service, 2001.

12383 082608

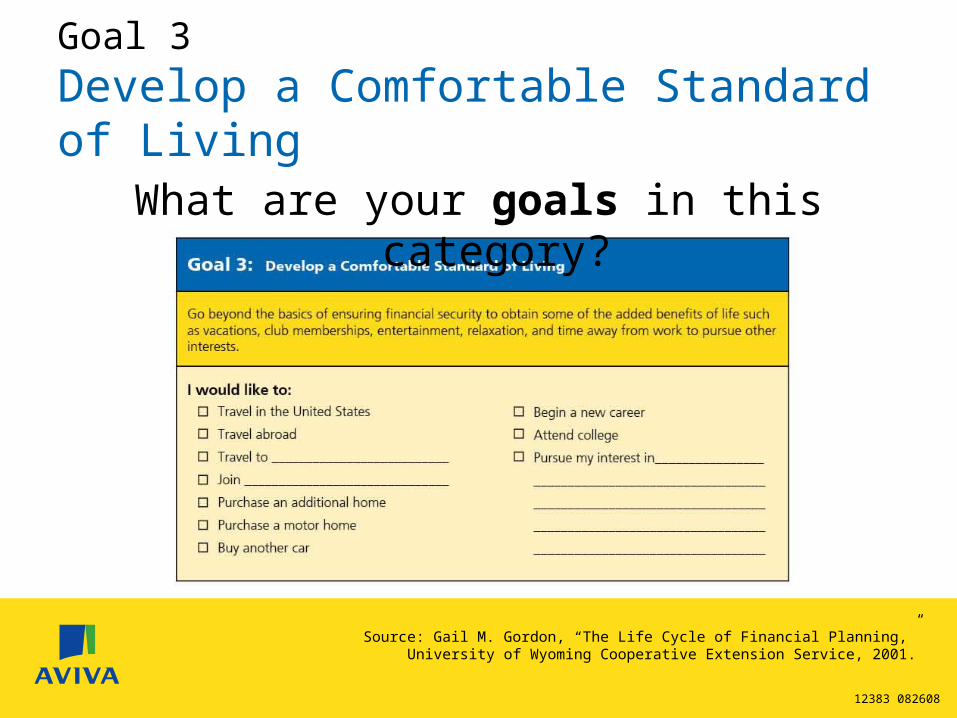

Goal 3

Develop a Comfortable Standard of Living

What are your goals in this category?

Source: Gail M. Gordon, “The Life Cycle of Financial Planning,” University of Wyoming Cooperative Extension Service, 2001.

12383 082608

What are your goals

in this category?

Goal 4

Create a Comfortable Retirement

Source: Gail M. Gordon, “The Life Cycle of Financial Planning,” University of Wyoming Cooperative Extension Service, 2001.

12383 082608

Goal 5

Manage Your Estate

What are your goals

in this category?

Source: Gail M. Gordon, “The Life Cycle of Financial Planning,” University of Wyoming Cooperative Extension Service, 2001. You should consult with a professional specializing in these areas regarding the applicability of this information to your own situation.

12383 082608

12383 082608

12383 082608

Source: U.S. Department of Labor, “Taking The Mystery out of Retirement Planning,” 2008.

12383 082608

12383 082608

12383 082608

12383 082608

Social Security Benefits

61-year-old man– Eligible at age 62

– $1,044 a year more at

age 63

Source: www.ssa.gov

12383 082608

www.ssa.gov/planners/calculators.htm

12383 082608

Pensions

89%

28%

Source: Watson Wyatt, “Large Employers Slow Changes to Retirement Plans, Watson Wyatt Finds,” Press Release, May 22, 2008.

12383 082608

Annuities

Fixed Annuity

Fixed IndexedAnnuity

VariableAnnuity

12383 082608

12383 082608

How does your amount of guaranteed income compare to your estimated annual retirement expenses?

Total Income Needed to Cover Annual Retirement Expenses......... $

Total Annual Income...................................................................... $

12383 082608

Fixed IndexedAnnuity

– The potential to earn interest credits based on changes in external market indices– Tax-deferred interest accumulation*– A death benefit for your beneficiaries– Principal protection– The ability to create an income stream you can never outlive– The security of a minimum guaranteed contract value– Options for when you decide to withdraw some or all of your money**

* Tax-deferral offers no additional value if an annuity is used to fund an IRA; purchase an annuity for reasons other than tax-deferral benefits beyond those inherently provided by an IRA, such as a lifetime income and a death benefit.** Taxable amounts withdrawn prior to 59 1/2 may be subject to a 10% IRS penalty. Withdrawals in excess of the free amount are not credited with index interest for that term, may be subject to Withdrawal Charges and a Market Value Adjustment and may result in the loss of principal if taken during the first 5-10 years of the Contract. Indexed annuities are not registered securities or stock market investments

and do not directly participate in any stock or equity investments.Annuities are products of the insurance industry; guarantees are backed by the claims-paying ability of the issuing company.

One of your choices for guaranteed retirement income

12383 082608

What are your options?

89%

28%

12383 082608

Next Steps

28%

12383 082608

Thank You

28%