Embed Size (px)

Citation preview

Mechanics of Financial Accounting

BUS512M

November 20, 2014 Session 1 1:00-4:30

Susan Crosson

Draw an Accountant…. Who/What Information needs for business/financial decisions

Syllabus, Calendar, Website Questions?

Adobe Connect sessions in December and January-best days and times?

Tentative schedule: 12.13.14 10-11AM Atlanta time

12.15.14 8-9PM Atlanta time 1.5.15 8-9PM Atlanta time

Look for Announcement with a link in Blackboard.

Midterm will be distributed electronically before December 1 and will be Due before 8AM

(Atlanta time) Monday December 15, 2014.

Today’s Learning Outcomes

• Financial Statements and account classifications

• Daily transactions-journal, T account ledger

• Period end transactions-adjusting and closing

• What happened? Reverse T account analysis

• Why Financial Statements and where do they come from?

Accounting tells the story!

Once upon a time, long, long ago,

accounting began to reduce events to

numbers to capture and bring meaning to

data and it was good! Concepts were

agreed upon and accounting techniques

evolved to analyze & resolve business

issues.

Measurement

Accounting Records

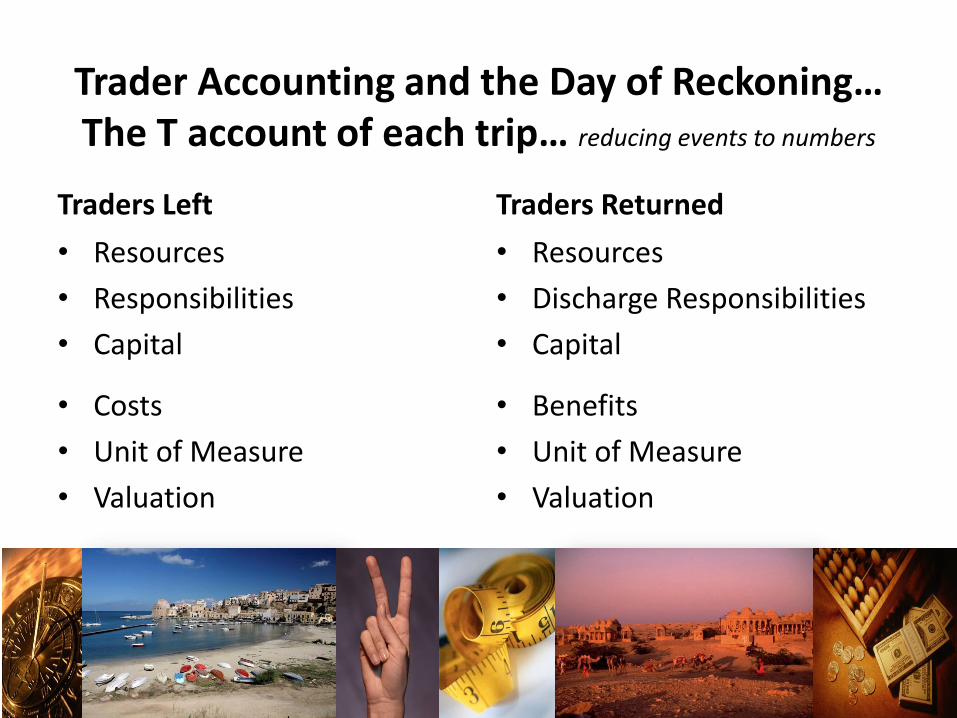

Trader Accounting and the Day of Reckoning… The T account of each trip… reducing events to numbers

Traders Left

• Resources

• Responsibilities

• Capital

• Costs

• Unit of Measure

• Valuation

Traders Returned

• Resources

• Discharge Responsibilities

• Capital

• Benefits

• Unit of Measure

• Valuation

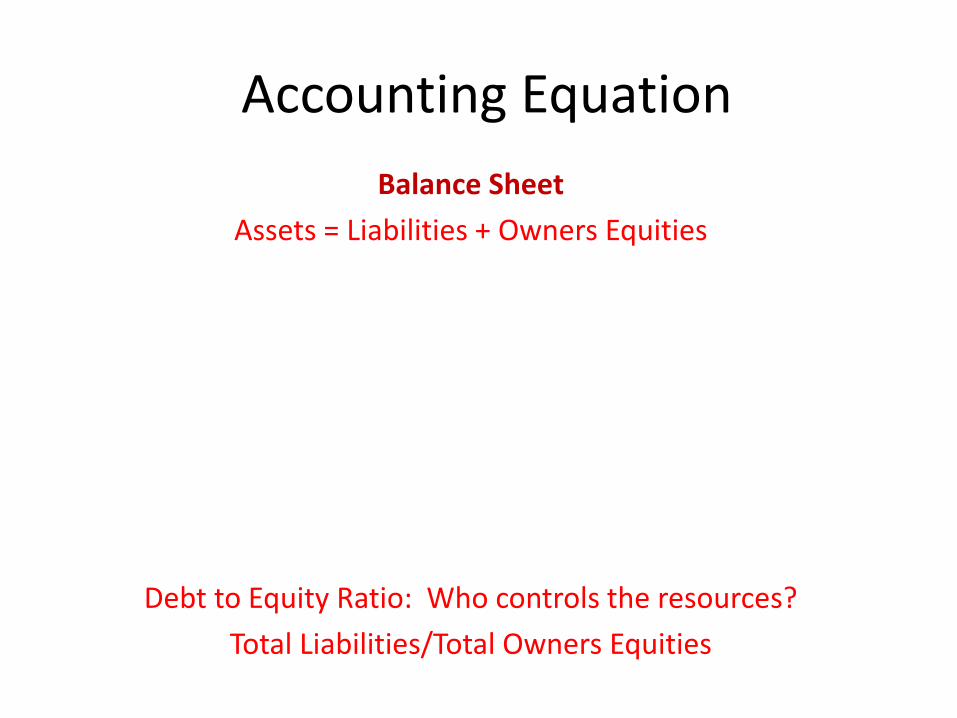

Accounting Equation

Balance Sheet

Assets = Liabilities + Owners Equities

Debt to Equity Ratio: Who controls the resources?

Total Liabilities/Total Owners Equities

Balance Sheet Basics

• A=L+OE for Sole Proprietorships and Partnerships

• Key numbers: – Current assets – Net property, plant, & equipment – Other assets – Total assets – Current liabilities – Long-term liabilities – Total liabilities – Total owners equity

• Prove Assets=Liabilities + Owners Equity

Balance Sheet Basics-Corporations

• A=L+SHE • Snapshot of financial health at a moment in time

• Other names: Statement of Financial Position

• Key numbers: – Current assets

– Net property & equipment

– Other assets

– Total assets

– Current liabilities

– Total liabilities

– Total stockholders’ equity

• Prove Assets=Liabilities + Stockholders’ Equity

Self Reporting QUIZ: Find the following key numbers for the most current year and report your answers

• Current assets_________

• Net property & equipment__________

• Other assets__________

• Total assets__________

• Current liabilities_________

• Total liabilities__________

• Total stockholders’ equity_________

• Prove Assets=Liabilities + Stockholders’ Equity

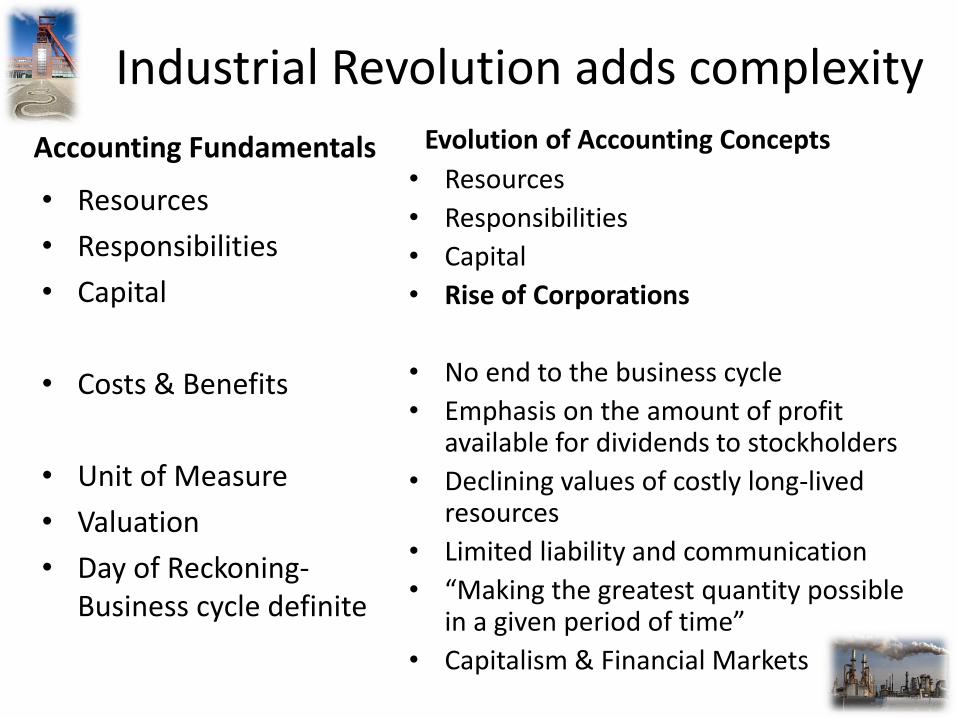

Industrial Revolution adds complexity

Accounting Fundamentals

• Resources

• Responsibilities

• Capital

• Costs & Benefits

• Unit of Measure

• Valuation

• Day of Reckoning- Business cycle definite

Evolution of Accounting Concepts

• Resources

• Responsibilities

• Capital

• Rise of Corporations

• No end to the business cycle

• Emphasis on the amount of profit available for dividends to stockholders

• Declining values of costly long-lived resources

• Limited liability and communication

• “Making the greatest quantity possible in a given period of time”

• Capitalism & Financial Markets

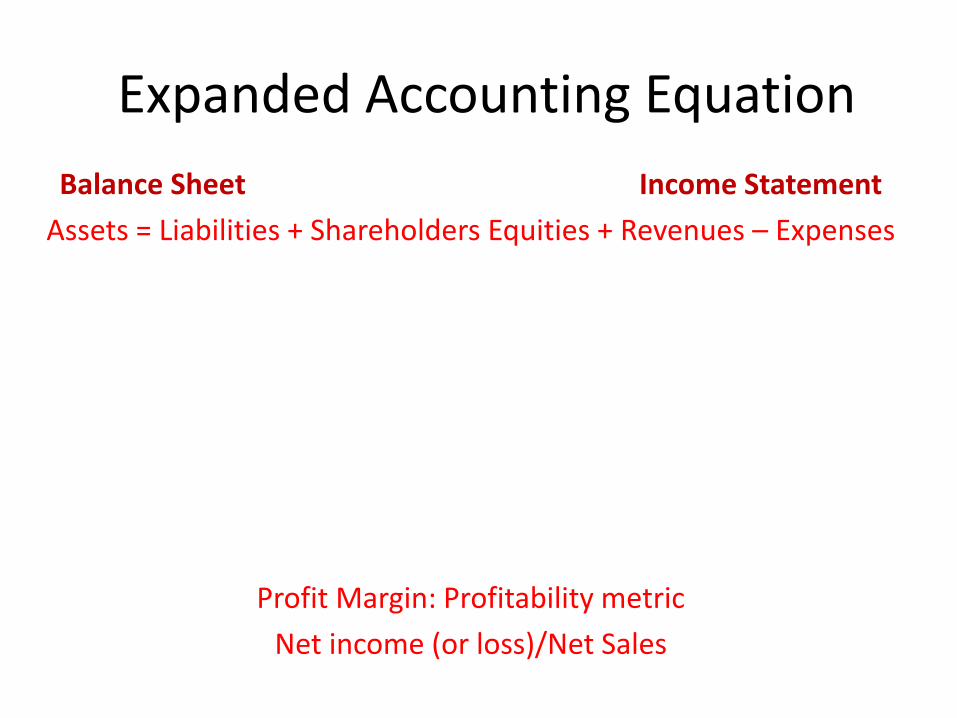

Expanded Accounting Equation

Balance Sheet Income Statement

Assets = Liabilities + Shareholders Equities + Revenues – Expenses

Profit Margin: Profitability metric

Net income (or loss)/Net Sales

Income Statement Basics

• Matches benefits and efforts of business for a period of time

• Single step format • Multi-step format • Key numbers:

– Revenue or Net sales – Cost of goods sold or

cost of sales – Operating expenses – Operating income – Other revenue and

expenses – Income taxes – Net income or Net

earnings

Self Reporting QUIZ: Find the following key numbers for the most current year and report your answers

• Total Revenue________ • Cost of revenues_______ • Expenses __________ • Income from operations__________ • Other revenue and expenses________ • Income taxes________ • Net income from continuing operations_________ • Net income________ • How profitable is this business in the last 3 years?

Learning Outcome: Financial Annual Reports-Identify the Key Numbers

• Assets (A)

• Liabilities (L)

• Stockholders’ Equity (SHE or SE)

• Revenues (R)

• Expenses (E)

Prove the Accounting Equation

Assets=Liabilities+SHE + Revenues-Expenses

Balance Sheet

Income Statement

Today and Tomorrow

Industrial Revolution • Resources • Responsibilities • Capital • Rise of Corporations • Going Concern & Business Entity • Net Income, Contributed Capital,

Retained Earnings, & Dividends • Depreciation, Amortization, &

Depletion • Financial reporting & Auditing • Product & Service Costing • Accounting kept the books

(locked the data up) and interpreted the data for others.

Transformative Technologies

• Now data unlocked with 24/7 access to anyone via Internet & Cloud.

• Massive quantities of financial and nonfinancial data. BIG DATA

• Comprehensive Income Statement • Making sense of business to an

audience-what info important? • Point of view of who’s telling the story-

single entity or helicopter? • Accountants still can be the

storytellers by bringing meaning to data through the process of:

Understanding the Concepts first

Then applying the best Accounting Tools To analyze and make Business Decisions

Financial Statement Basics • Accounting Equation

• Order of preparation: – Income Statement

– Stockholders’ Equity and Other Comprehensive Income

–Balance Sheet

–Cash Flow Statement

–Comprehensive Income

–Nonfinancial Metrics

Homework

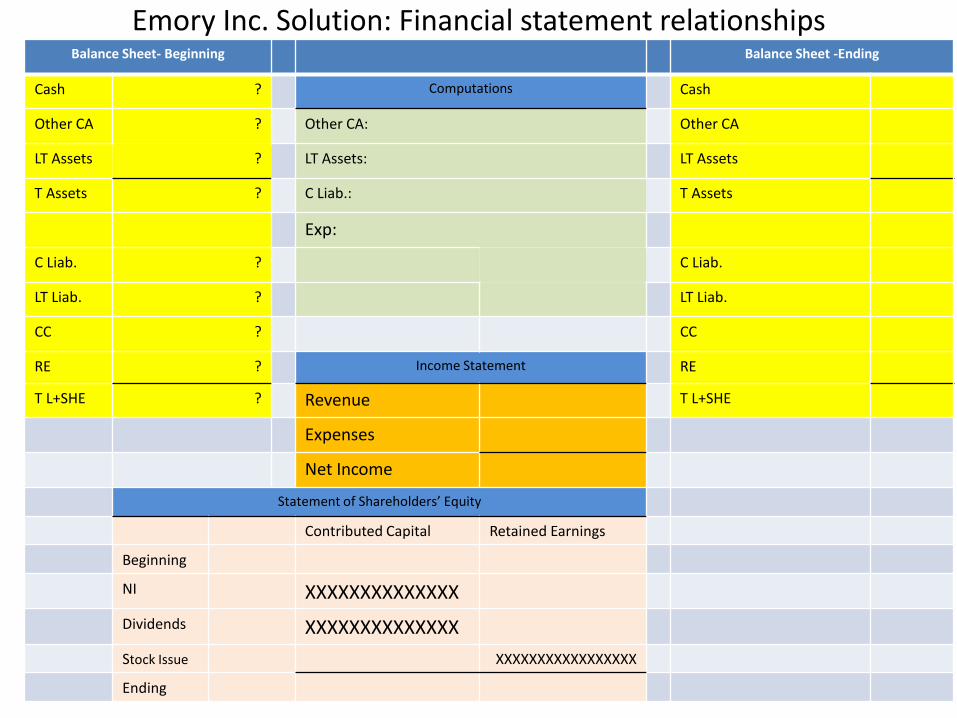

SOLUTION Emory Inc.

Emory Inc. Solution: Financial statement relationships Balance Sheet- Beginning Balance Sheet -Ending

Cash ? Computations Cash

Other CA ? Other CA: Other CA

LT Assets ? LT Assets: LT Assets

T Assets ? C Liab.: T Assets

Exp:

C Liab. ? C Liab.

LT Liab. ? LT Liab.

CC ? CC

RE ? Income Statement RE

T L+SHE ? Revenue T L+SHE

Expenses

Net Income

Statement of Shareholders’ Equity

Contributed Capital Retained Earnings

Beginning

NI XXXXXXXXXXXXXX

Dividends XXXXXXXXXXXXXX

Stock Issue XXXXXXXXXXXXXXXXX

Ending

What do you know?

Classifications • Assets: Current & Long-term (Property, Plant, &

Equipment; Investments; Intangibles)

• Liabilities: Current & Long-term

• Shareholders Equities: Contributed Capital and Retained Earnings

• Revenues: Sales, Income, Gains, & Losses

• Expenses: Operating (selling, administrative, & General), Other

Current Ratio: Liquidity metric

Current assets/current liabilities

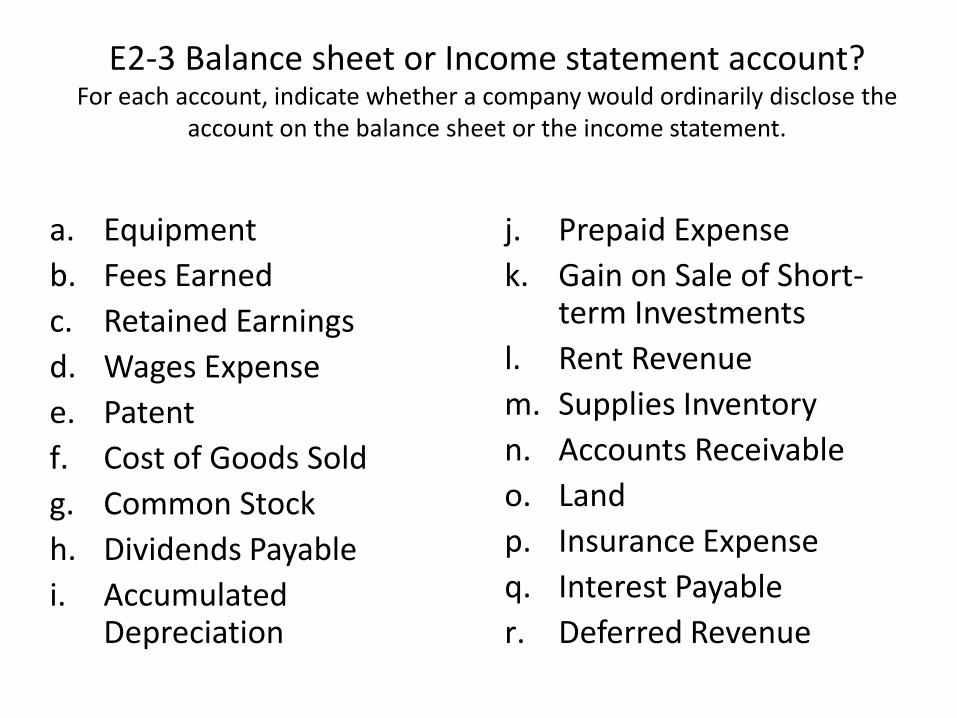

E2-3 Balance sheet or Income statement account? For each account, indicate whether a company would ordinarily disclose the

account on the balance sheet or the income statement.

a. Equipment

b. Fees Earned

c. Retained Earnings

d. Wages Expense

e. Patent

f. Cost of Goods Sold

g. Common Stock

h. Dividends Payable

i. Accumulated Depreciation

j. Prepaid Expense

k. Gain on Sale of Short-term Investments

l. Rent Revenue

m. Supplies Inventory

n. Accounts Receivable

o. Land

p. Insurance Expense

q. Interest Payable

r. Deferred Revenue

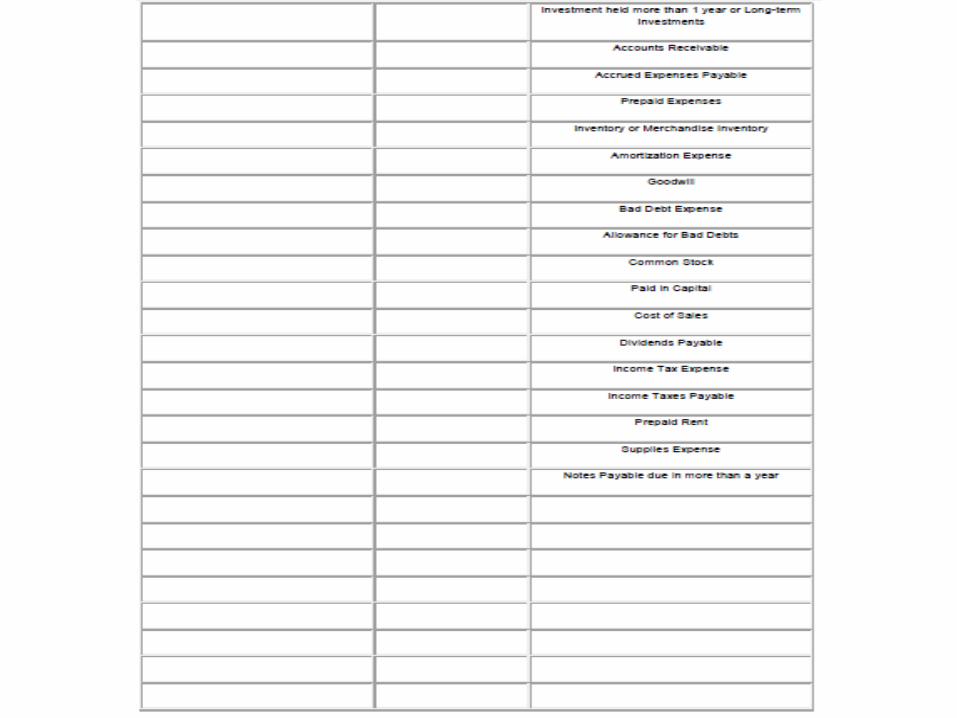

P2-1 Classifying balance sheet accounts Presented below are the main section headings of the balance sheet: a. Current assets; b. Long-term investments; c. Property, plant, & equipment; d. Intangible assets; e. Current liabilities; f. Long-term liabilities; g. Contributed capital; h. Retained earnings

1. Dividends payable 2. Payment received in advance 3. Allowance for uncollectible

accounts 4. Inventories 5. Capital stock 6. Accumulated depreciation-

building 7. Bond payable 8. Machinery and equipment 9. Accounts receivable 10. Short-term investments 11. Buildings 12. Patents

13. Property 14. Investment fund for plant

expansion 15. Wages payable 16. Cash 17. Accumulated depreciation-

equipment 18. Prepaid rent 19. Trademarks 20. Land held for investment 21. Current portion due of long-

term debt 22. Accounts payable 23. Short-term notes payable

Financial statement relationships Balance Sheet 12.31.Begin Balance Sheet 12.31.End

Cash Statement of Cash Flows 12.31.End Cash

Other CA Cash-Operating IS, changes in CA&CL Other CA

LT Assets LTInvt, PP&E, Intan. Cash-Investing Changes in LTA LT Assets

T Assets Cash-Financing Changes in LTL, CC T Assets ?

Change in Cash ?

C Liab. Cash-12.31.Begin ? C Liab.

LT Liab. Cash-12.31.End ? LT Liab.

CC CC

RE Income Statement (year ending 12.31.) RE

T L+SHE Revenue Sales,Earned,Other T L+SHE ?

Expenses COGS,Oper.,Other

Net Income ?

Statement of Shareholders’ Equity (year ended 12.31.)

Contributed Capital Retained Earnings

12.31.Begin

NI XXXXXXXXXXXXXXX

Dividends XXXXXXXXXXXXXXX

Stock Issue XXXXXXXXXXXXXXXXX

12.31.End ? ?

P2-3 Financial statement relationships-find missing numbers Balance Sheet 12.31.2010 Balance Sheet 12.31.2011

Cash 420 Statement of Cash Flows 12.31.2011 Cash ?

Other CA 1,300 Cash-Operating 275 Other CA 1,550

LT Assets 1,400 Cash-Investing (200) LT Assets 1,600

T Assets 3,120 Cash-Financing 330 T Assets ?

Change in Cash ?

C Liab. 620 Cash-12.31.2010 ? C Liab. 995

LT Liab. 1,000 Cash-12.31.2011 ? LT Liab. 1,200

CC 1,000 CC 1,200

RE 500 Income Statement (year ending 12.31.2011) RE ?

T L+SHE 3,120 Revenue 4,200 T L+SHE ?

Expenses 4,050

Net Income ?

Statement of Shareholders’ Equity (year ended 12.31.2011)

Contributed Capital Retained Earnings

12.31.10 1,000 500

NI ?

Dividends (70)

Stock Issue 200

12.31.11 ? ?

P2-5 BS and IS relationships across 5 years 2014 2013 2012 2011

Assets:

Cash 500 200 300 300

Acct receivable 700 ? 300 200

Inventory 400 400 ? 500

Land 400 400 200 100

PP&E 800 700 600 700

Liabilities & SHE

Accts payable ? 500 300 200

Bonds payable 700 800 600 500

Contrib Capital 600 600 400 ?

RE 600 300 800 400

Sales ? 700 1,100 1,000

Expenses 600 ? ? 400

Net Income ? (100) 400 ?

Dividends 200 ? ? ?

Accounting Equation or FS Missing Numbers

Salaries expense $4,000 Commissions Earned $20,000

Accounts payable $7,000 Retained Earnings

December 31, 20XX c= ?

Dividends $6,000 Utilities expense $2,000

Accounts receivable $8,000 Inventories $22,000

Cash a= ? Salaries Payable $1,000

Net income b= ? Retained Earnings January

1, 20XX $25,000

Total assets d= ? Common stock $1,000

Use the following information to calculate at, or for the year ended, December 31, 20XX (a) cash, (b)

net income, (c) retained earnings, and (d) total assets.

E4-7 Preparing financial statements Taken from the 2012 annual report of Bristol-Myers Squibb, a world-leading

drug company (dollars in millions), reconstruct the financials.

Cost of goods sold $ 4,610

Net cash from operations 6,941

Accounts receivable 3,083

Impairment expense 1,830

Net cash from financing (4,333)

Shareholders’ equity 13,638

Net cash from investing (6,727)

Research & dev. expense 3,904

Other noncurrent assets 21,043

Other expenses/(gains) (241)

Marketable securities 1,173

Cash and equivalents $ 1,656

Short-term borrowings 826

Adv. & product expense 797

Accounts payable 2,202

Long-term liabilities 13,980

Net sales 17,621

Property, plant, & equip. 5,333

Other current assets 3,609

Other current liabilities 2,678

Sell. & adm. expenses 4,220

Accrued payables 2,573

E4-7 Financial statement relationships Income Statement for 2008 Balance Sheet –End of 2008

Revenue Statement of Cash Flows for 2008 Cash

COGS Cash-Operating Mkt Sec

S&A Exp Cash-Investing AR

Adv Exp Cash-Financing Other

R&D Exp Change in Cash Total CA

Rest. Exp Cash-12.31.2007 PP&E

Other Exp Cash-12.31.2008 Other NCA

Total Exp Total Assets

Net Income

AP

Acc. Pay

ST Borrow

Other

Total CL

LTL

SHE

TL+SHE

Accounting Cycle

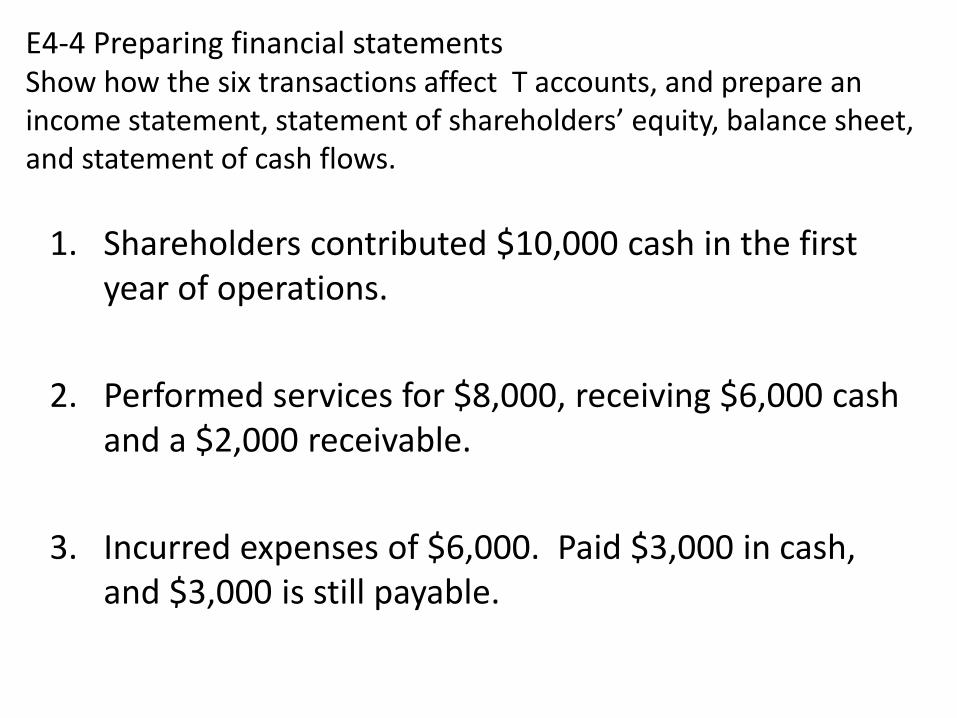

E4-4 Preparing financial statements Show how the six transactions affect T accounts, and prepare an income statement, statement of shareholders’ equity, balance sheet, and statement of cash flows.

1. Shareholders contributed $10,000 cash in the first year of operations.

2. Performed services for $8,000, receiving $6,000 cash and a $2,000 receivable.

3. Incurred expenses of $6,000. Paid $3,000 in cash, and $3,000 is still payable.

E4-4 Preparing financial statements Show how the six transactions affect the T accounts, and prepare an income statement, statement of shareholders’ equity, balance sheet, and statement of cash flows.

4. Purchased land for $12,000. Paid $2,000 in cash and signed a long-term note for the remainder.

5. Paid shareholders $400 in the form of a dividend.

6. Sold one-half of the land purchased in (4.) for $7,000 cash.

T account

E4-4 Financial statement relationships Balance Sheet- Beginning Balance Sheet -Ending

Cash Statement of Cash Flows Cash

Other CA Cash-Operating Other CA

LT Assets Cash-Investing LT Assets

T Assets Cash-Financing T Assets ?

Change in Cash

C Liab. Cash-Beg C Liab.

LT Liab. Cash-End ? LT Liab.

CC CC

RE Income Statement RE

T L+SHE Revenue T L+SHE ?

Expenses

Net Income ?

Statement of Shareholders’ Equity

Contributed Capital Retained Earnings

Beginning

NI XXXXXXXXXXXXXX

Dividends XXXXXXXXXXXXXX

Stock Issue XXXXXXXXXXXXXXXXX

Ending ? ?

Matching & Accrual Accounting

• Basic to financial reporting of corporations. • Concerned with the timing of revenue and expense

recognition. • Purpose is to accurately measure revenues and

expenses (and profits) for each accounting period. • Accrual accounting’s Income Statement attempts

to match revenues earned and the expenses incurred, NOT cash flows.

• Accrual accounting’s Statement of Cash Flows reports the cash inflows and outflows for the period.

Adjusting Entries: 4 Kinds

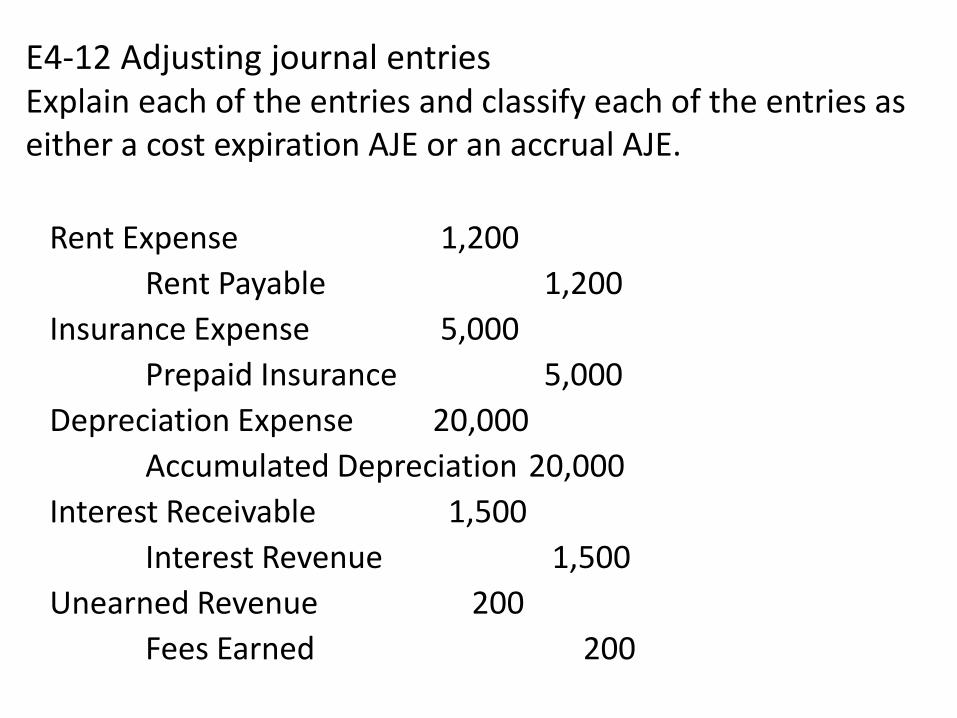

E4-12 Adjusting journal entries Explain each of the entries and classify each of the entries as either a cost expiration AJE or an accrual AJE.

Rent Expense 1,200

Rent Payable 1,200

Insurance Expense 5,000

Prepaid Insurance 5,000

Depreciation Expense 20,000

Accumulated Depreciation 20,000

Interest Receivable 1,500

Interest Revenue 1,500

Unearned Revenue 200

Fees Earned 200

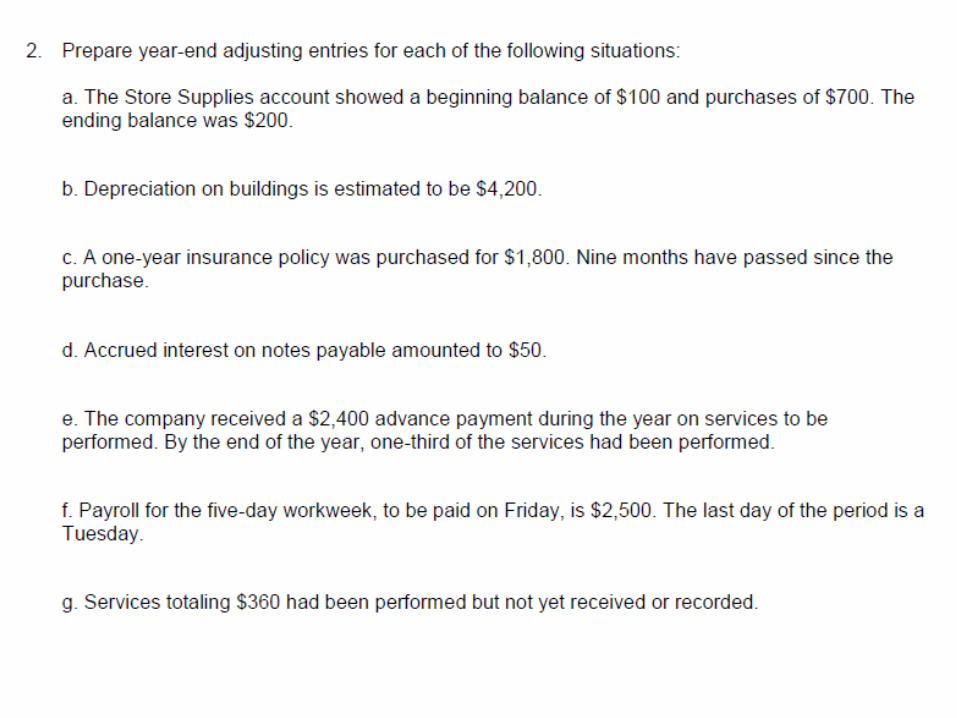

P4-8 Preparing adjusting journal entries a. The 12.31.14 supplies balance is $85,000. A count of supplies reveals that

the company actually has $30,000 of supplies on hand.

b. As of 12.31.14 the company had not paid the rent for the month. The monthly rent is $2,400.

c. On 12.20.14 the company collected $18,000 in customer advances for the subsequent performance of a service. As of 12.31.14 two-thirds of the service had been performed.

d. The total cost of fixed assets is $500,000. The company estimates that the assets have a useful life of ten years and used straight-line depreciation.

P4-8 Preparing adjusting journal entries e. The company borrowed $10,000 at an annual interest rate of

12% on 7.1.14. The first interest payment will be made 1.1.15.

f. The company placed several ads in newspapers during the month. On 12.31.14 the company received a $28,000 bill for the ads, which was not recorded at the time.

g. On 7.1.14 the company paid the premium for a one-year life insurance policy. The $350 cost of the premium was capitalized when paid.

Closing Entries: Income Statement and Dividend Accounts

Prepare closing entries from the adjusted trial balance shown above.

Accounts Payable $62,800

Accounts Receivable $50,000

Accumulated Depreciation $3,000

Building $163,200

Cash $220,480

Common Stock $400,000

Depreciation Expense $3,000

Design Income $140,000

Dividends $30,000

Income Taxes Expense $8,000

Income Taxes Payable $8,000

Office Supplies $36,600

Office Supplies Expense $15,400

Prepaid Rent $16,000

Rent Expense $16,000

Unearned Income $1,680

Utilities Expense $6,800

Wages Expense $55,200

Wages Payable $7,200

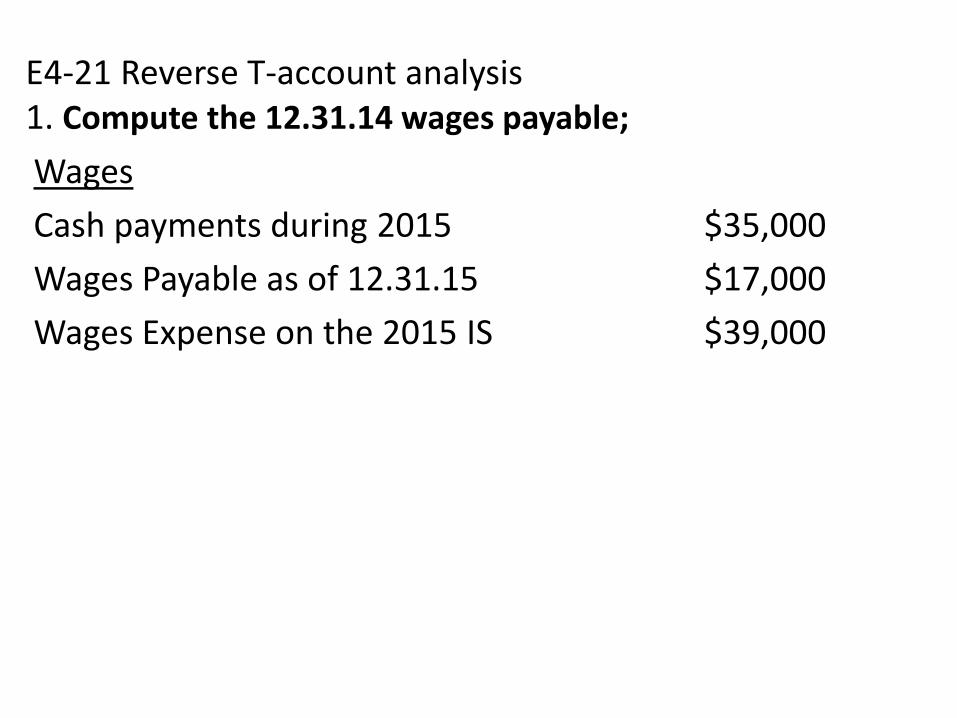

E4-21 Reverse T-account analysis 1. Compute the 12.31.14 wages payable; Wages

Cash payments during 2015 $35,000

Wages Payable as of 12.31.15 $17,000

Wages Expense on the 2015 IS $39,000

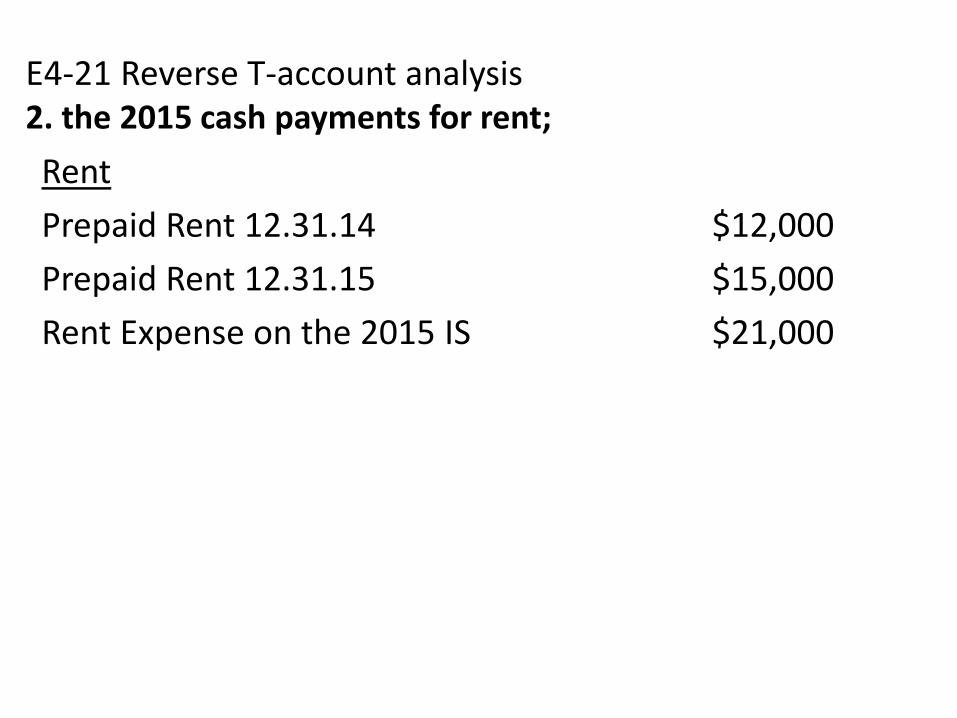

E4-21 Reverse T-account analysis 2. the 2015 cash payments for rent; Rent

Prepaid Rent 12.31.14 $12,000

Prepaid Rent 12.31.15 $15,000

Rent Expense on the 2015 IS $21,000

E4-21 Reverse T-account analysis 3. the accounts receivable as of 12.31.15.

Accounts Receivable

Cash collected from customers during 2015 $38,000

Accounts Receivable as of 12.31.14 $14,000

Sales Revenue on the 2015 IS $45,000

P4-9 Inferring adjusting journal entries from changes in T-account balances

Account Balance before AJE Prepaid rent 14,500

Prepaid insurance 8,500 Accum. Deprec. 36,000

Salaries payable 1,300 Unearned revenues 800

Fees earned 87,600 Rent expense 6,500 Insurance expense 5,500

Depreciation expense 0 Salary expense 3,500

Balance after AJE 11,800

7,800 38,400

2,500 600

87,800 9,200 6,200 2,400 4,700

P4-20 Reverse T-account analysis

You are a credit analyst for a bank. Badger Business has applied for a loan. The company claims to have more than tripled profits from 2014 to 2015 and believes that it should be given prime credit terms. In addition, you note that Badger has expanded its operations, recently paying $37,000 for new equipment that replaced old equipment, which was sold that same year. No other transactions affected the company’s equipment account. Excerpts from the 2015 financial statements are provided below. Balance sheet: 2015 2014 Equipment $97,400 $84,800 Acc. Depreciation (26,400) (24,300) Income statement: Net income $5,200 $1,500 Depreciation expense $8,700 $7,600 Statement of cash flows: Proceeds from equipment sale $23,400 0

Today we learned about… • Revenue • Expenses • Assets-4 categories • Liabilities-2 categories • Stockholders’ Equity-2 categories Proved the Accounting Equation Accounting Cycle CSI Accounting: Reverse engineering T accounts 3 Ratios:

Current ratio Debt to Equity Profit Margin

What questions do you have?

Company X

WHAT ARE YOUR THOUGHTS?

Company X

Company X