Embed Size (px)

Citation preview

Measuring Oil’s Role in Latin American Economic Growth

Guillermo Perry

Chief Economist for Latin America & Caribbean,

The World Bank

Houston, TexasNovember 16, 1999

Relative Price of Oil (Index by Export Unit Value of OECD Countries)

0

0.1

0.2

0.3

0.4

0.5

0.6

Jan

-60

Jan

-62

Jan

-64

Jan

-66

Jan

-68

Jan

-70

Jan

-72

Jan

-74

Jan

-76

Jan

-78

Jan

-80

Jan

-82

Jan

-84

Jan

-86

Jan

-88

Jan

-90

Jan

-92

Jan

-94

Jan

-96

Jan

-98

Average Relative Price of Oil(With Standard Deviations)

0

0.1

0.2

0.3

0.4

0.5

Jan

-57

Jan

-59

Jan

-61

Jan

-63

Jan

-65

Jan

-67

Jan

-69

Jan

-71

Jan

-73

Jan

-75

Jan

-77

Jan

-79

Jan

-81

Jan

-83

Jan

-85

Jan

-87

Jan

-89

Jan

-91

Jan

-93

Jan

-95

Jan

-97

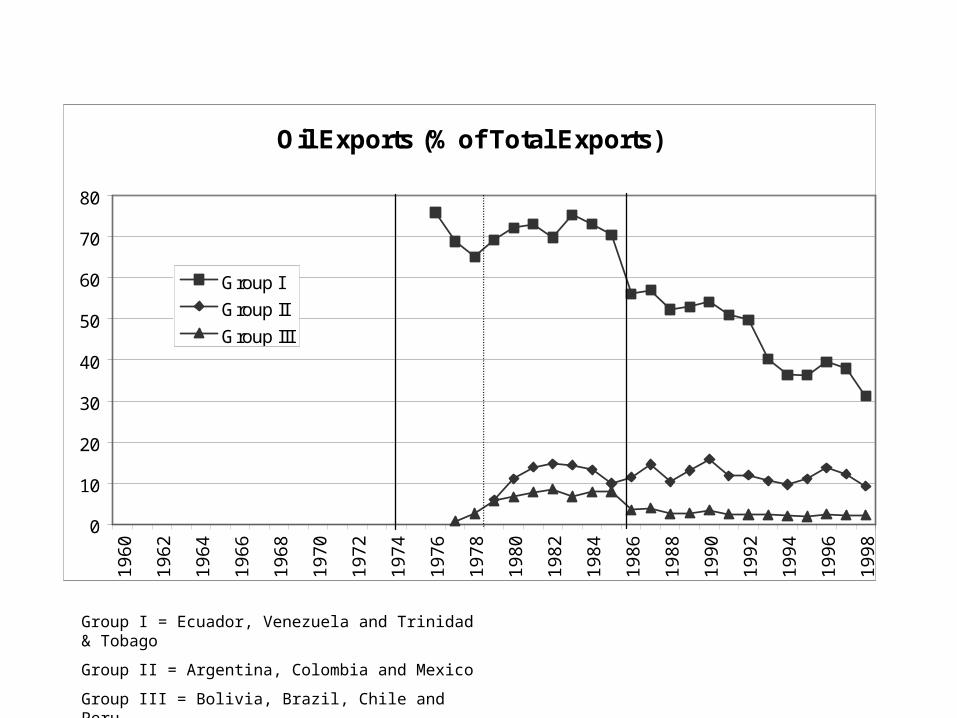

Group I = Ecuador, Venezuela and Trinidad & Tobago

Group II = Argentina, Colombia and Mexico

Group III = Bolivia, Brazil, Chile and Peru

Oil Exports (% of Total Exports)

0

10

20

30

40

50

60

70

80

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Group I

Group II

Group III

Non-Oil Exports (% of GDP)

0

5

10

15

20

25

30

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Group I

Group II

Group III

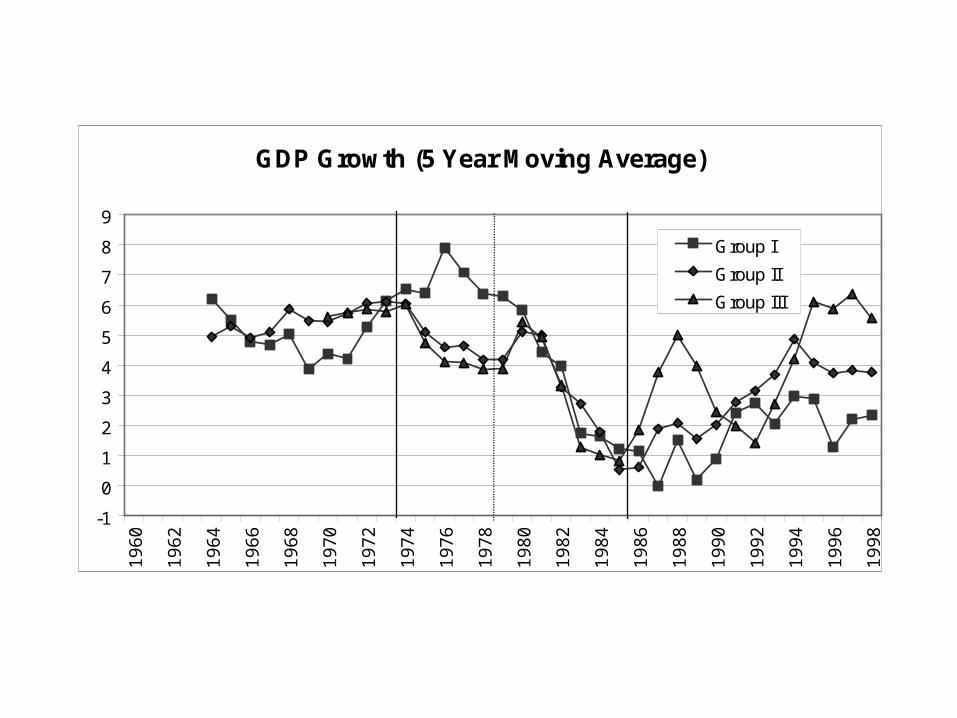

GDP Growth (5 Year Moving Average)

-1

0

1

2

3

4

5

6

7

8

9

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Group I

Group II

Group III

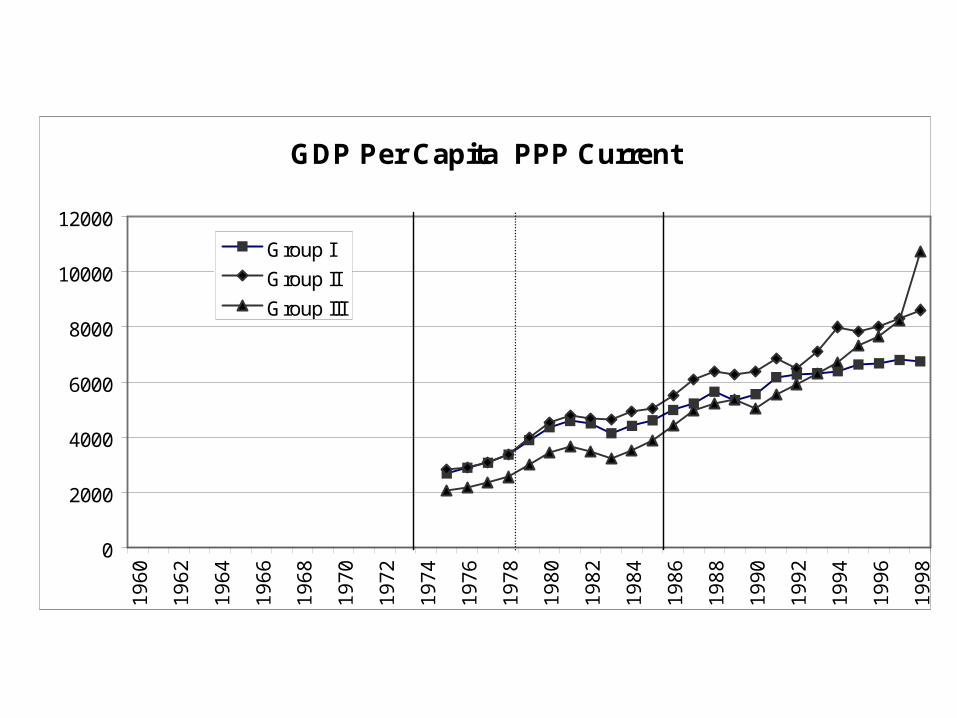

GDP Per Capita PPP Current

0

2000

4000

6000

8000

10000

12000

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Group I

Group II

Group III

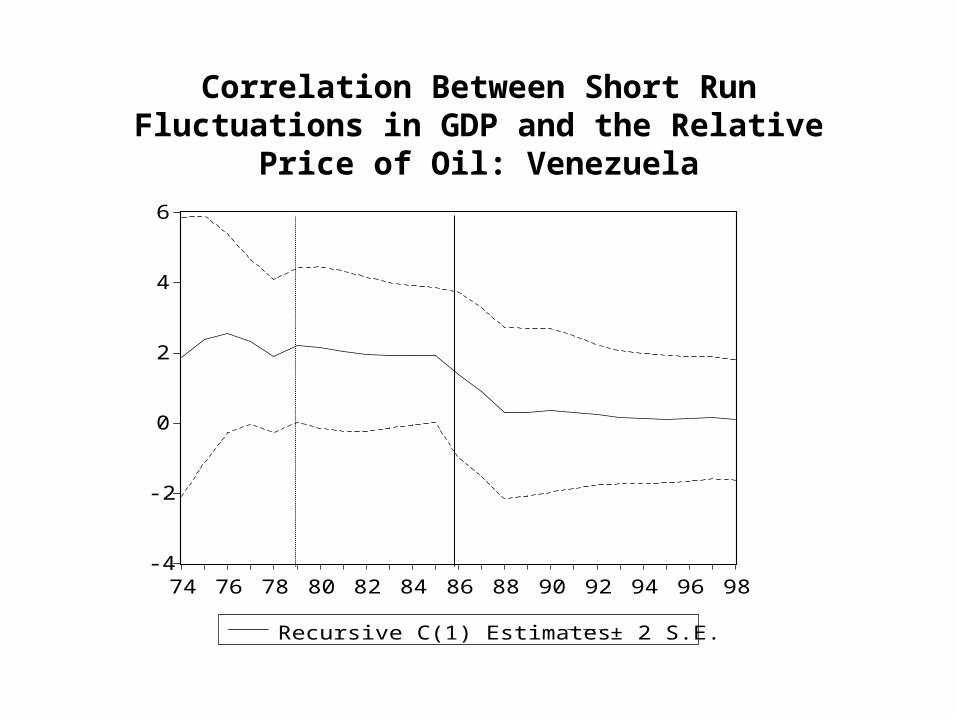

Correlation Between Short Run Fluctuations in GDP and the Relative Price of Oil: Venezuela

-4

-2

0

2

4

6

74 76 78 80 82 84 86 88 90 92 94 96 98

Recursive C(1) Estimates ± 2 S.E.

0.0

0.1

0.2

0.3

0.4

0.5

76 78 80 82 84 86 88 90 92 94 96

Recursive C(1) Estimates ± 2 S.E.

Correlation Between Short Run Fluctuations in GDP and the Relative Price of Oil: Mexico

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

74 76 78 80 82 84 86 88 90 92 94 96 98

Recursive C(1) Estimates ± 2 S.E.

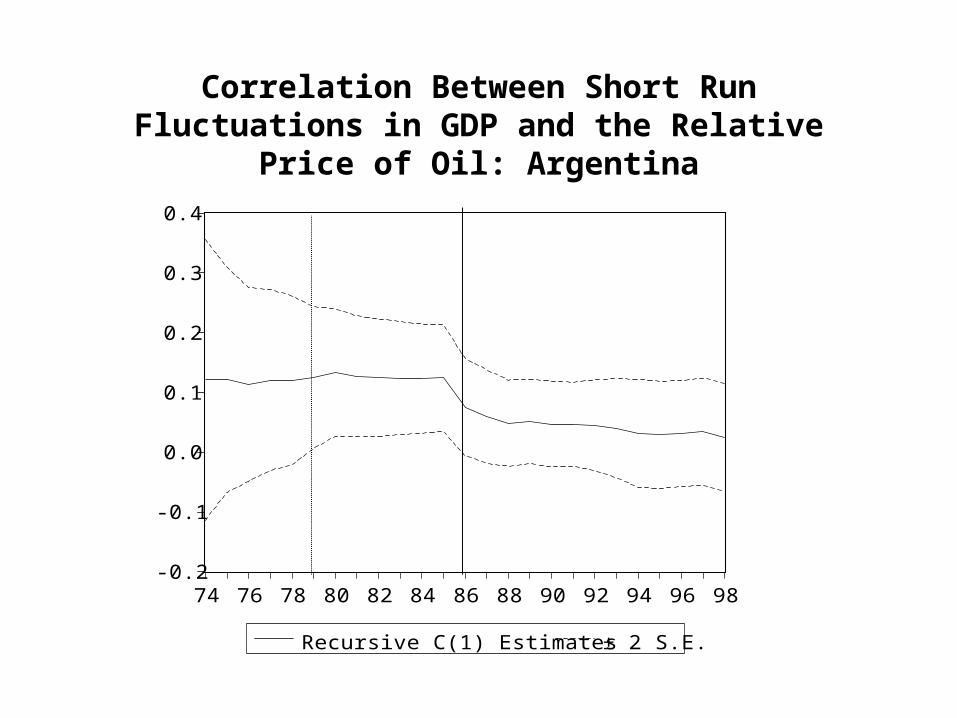

Correlation Between Short Run Fluctuations in GDP and the Relative Price of Oil: Argentina

-0.2

0.0

0.2

0.4

0.6

74 76 78 80 82 84 86 88 90 92 94 96 98

Recursive C(1) Estimates ± 2 S.E.

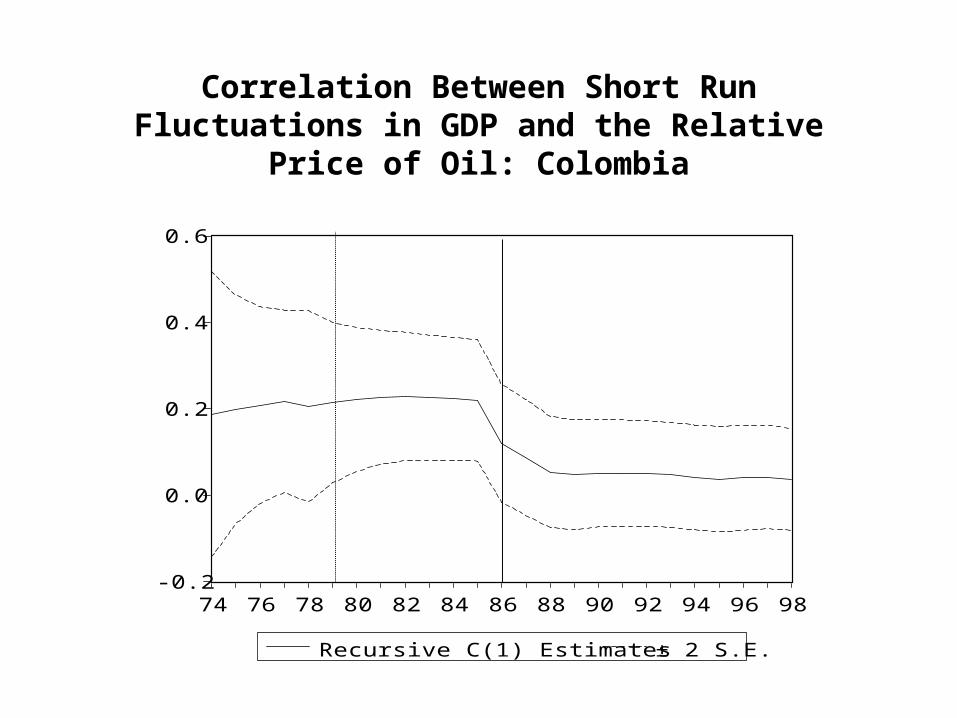

Correlation Between Short Run Fluctuations in GDP and the Relative Price of Oil: Colombia

Investments (% of GDP, 5 Year Moving Average)

0

5

10

15

20

25

30

35

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Group I

Group II

Group III

Savings (% of GDP, 5 Year Moving Average)

0

5

10

15

20

25

30

35

40

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Group I

Group II

Group III

NFPSB (% of GDP)

-30

-25

-20

-15

-10

-5

0

5

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

Group I

Group II

Group III

Note: Trinidad & Tobago is not included in Group I.

Note: Argentina not included in Group II.

Government Expenditures (% of GDP)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Group I

Group II

Group III

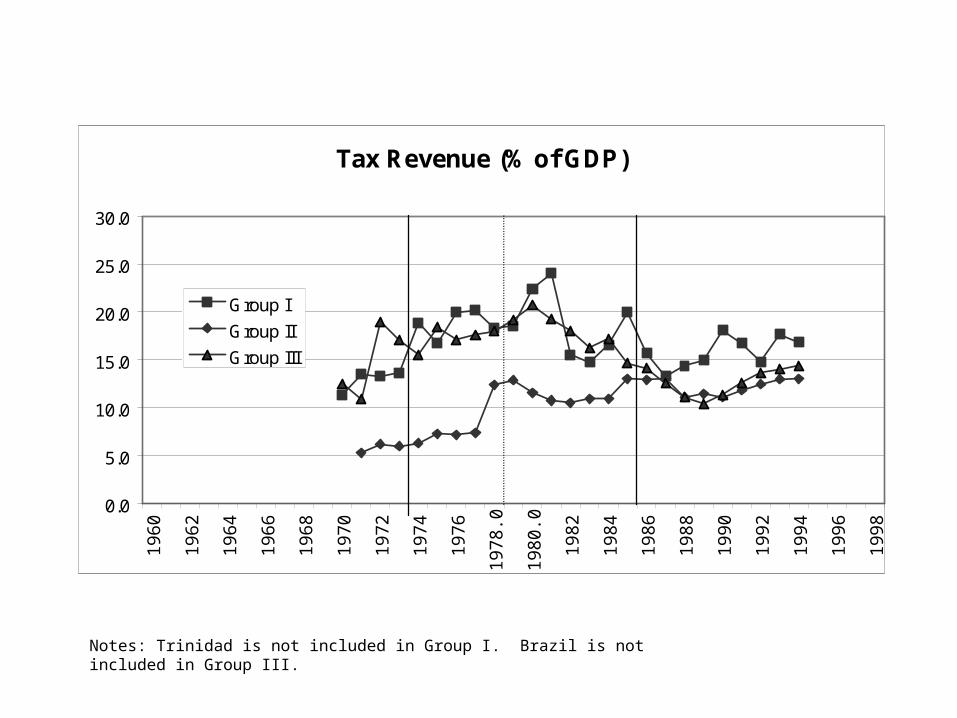

Tax Revenue (% of GDP)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

.0

1980

.0

1982

1984

1986

1988

1990

1992

1994

1996

1998

Group I

Group II

Group III

Notes: Trinidad is not included in Group I. Brazil is not included in Group III.

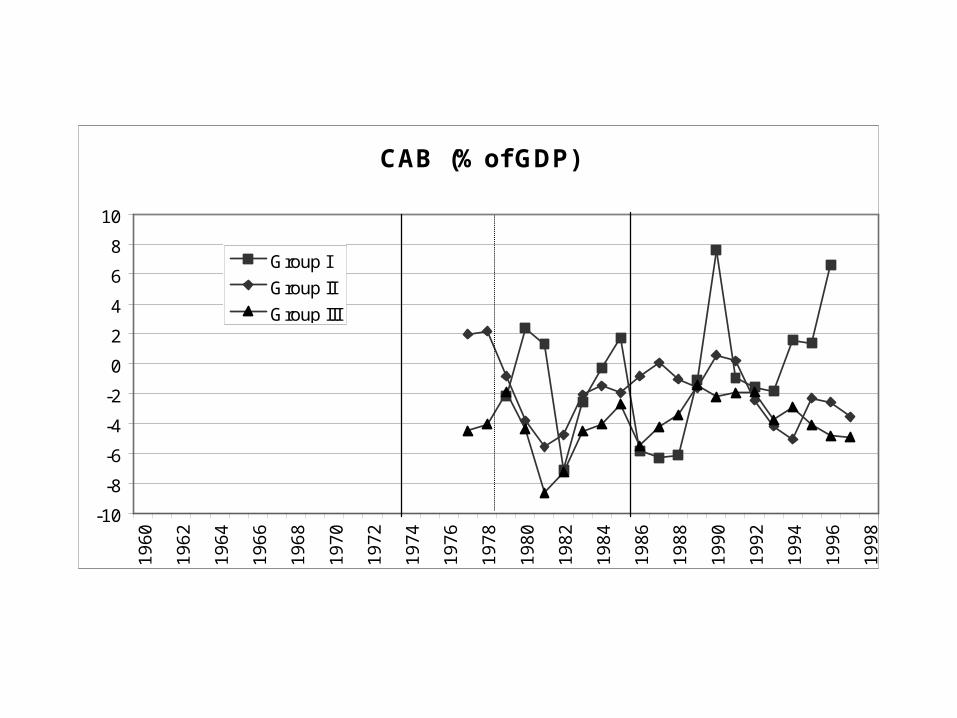

CAB (% of GDP)

-10

-8

-6

-4

-2

0

2

4

6

8

10

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Group I

Group II

Group III

External Debt (% of GDP)

0

10

20

30

40

50

60

70

80

90

100

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Group I

Group II

Group III

Latin America: External Factors and Growth

Deceleration,1999-1997

Due to externalfactors A

Due to externalfactors B

Argentina -11.5% -4.0% -1.6%Brazil -3.0% -5.5% -2.6%Chile -8.6% -4.7% -2.4%Colombia -6.6% -4.7% -2.7%Ecuador -10.4% -5.2% -3.1%Mexico -3.5% -1.5% -1.1%Peru -4.5% -3.2% -2.4%Venezuela -11.9% -5.2% -3.6%WeightedAvg. -5.5% -4.3% -2.2%

External Factors = U.S. Federal Funds Rate, terms of trade, “Non-Latin” Spreads, El Niño.

Weighted Avg. based on 1997 GDPs.

External Factors A = Estimated using 1998 and 1999 projections under 1997 external conditions.

External Factors B = Using 1997 external conditions for 1998 projection; 1998 conditions for 1999 projections

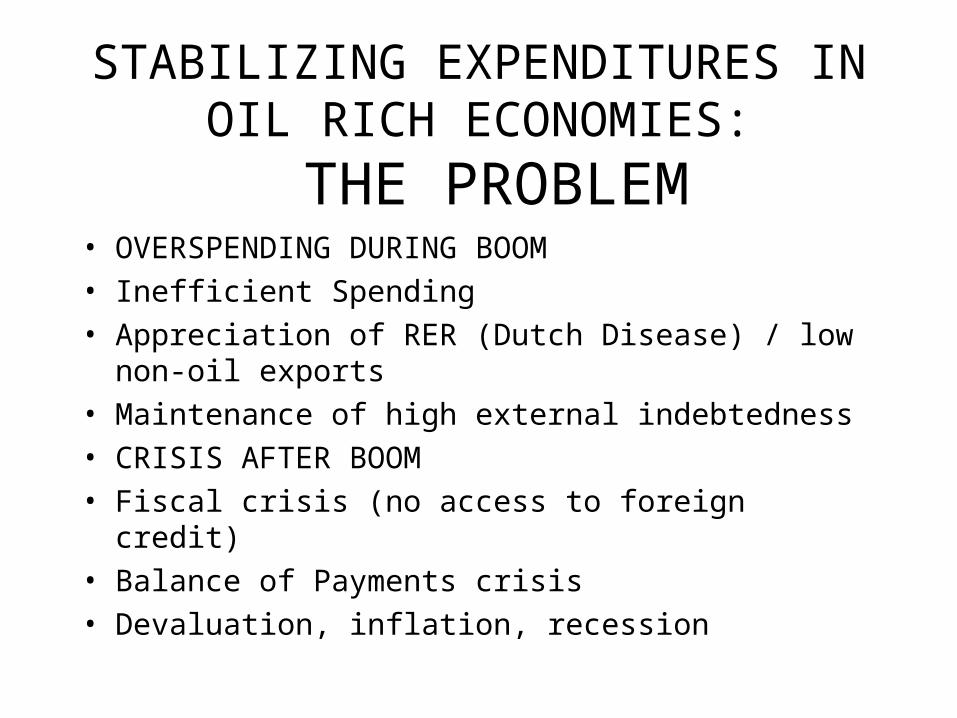

STABILIZING EXPENDITURES IN OIL RICH ECONOMIES:

THE PROBLEM• OVERSPENDING DURING BOOM

• Inefficient Spending

• Appreciation of RER (Dutch Disease) / low non-oil exports

• Maintenance of high external indebtedness

• CRISIS AFTER BOOM

• Fiscal crisis (no access to foreign credit)

• Balance of Payments crisis

• Devaluation, inflation, recession

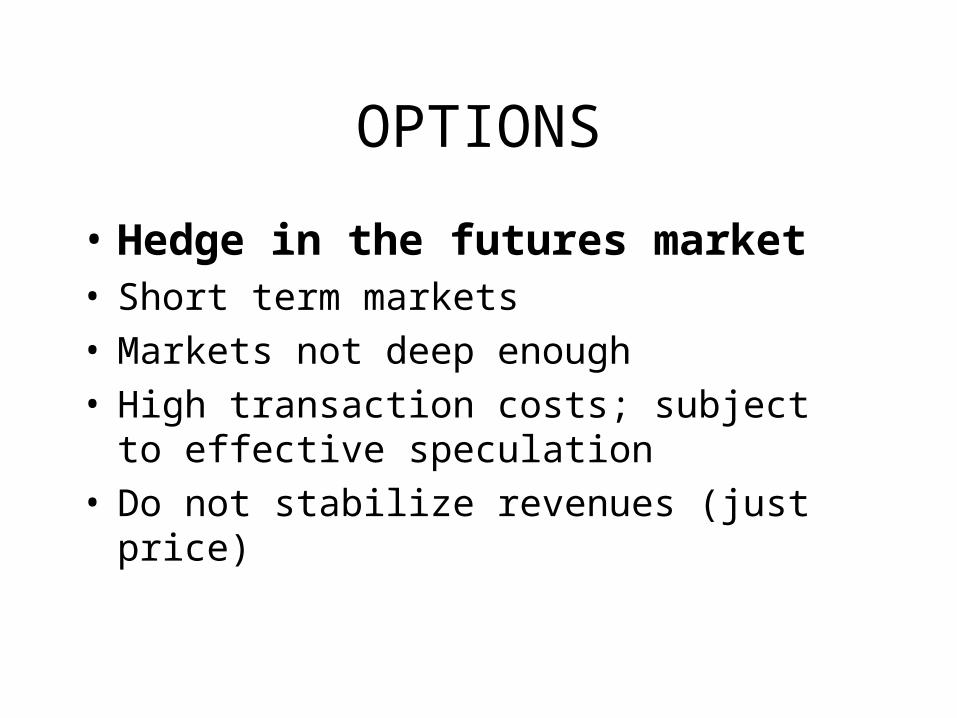

OPTIONS

• Hedge in the futures market• Short term markets• Markets not deep enough• High transaction costs; subject to effective

speculation• Do not stabilize revenues (just price)

OPTIONS

• Stabilization Fund

• To insulate from political pressures during boom

• Credibility for investors

Issues in the Design of Stabilization Funds

• Savings and withdrawal rules

• Reference price

• Fund can not be used as collateral

• Stabilization Fund is not enough to guarantee fiscal soundness

• Require coordination with exchange rate and monetary policies

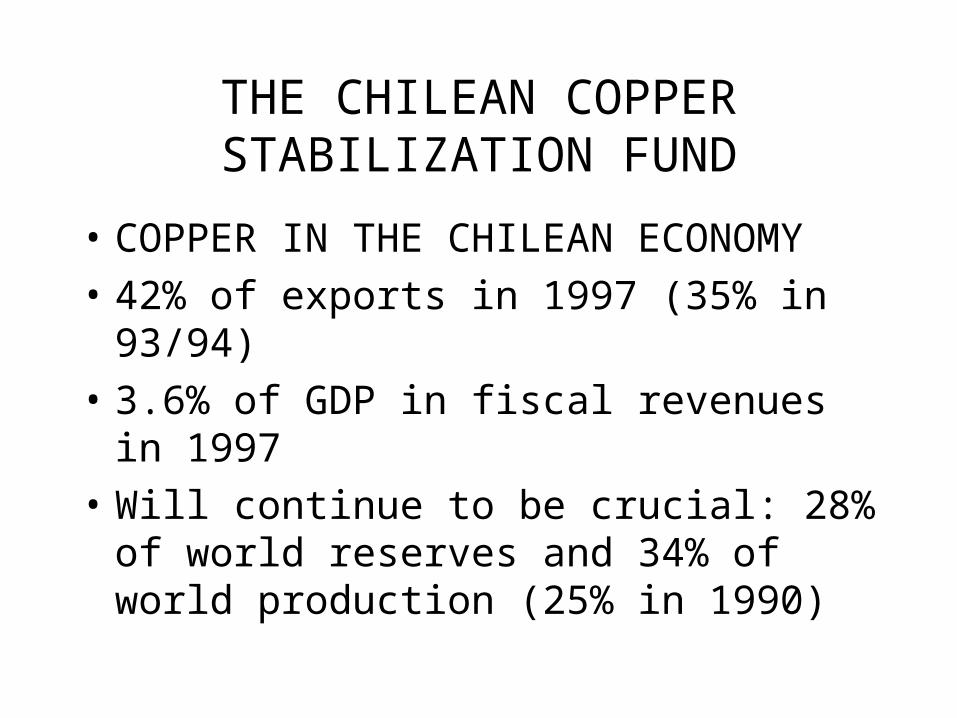

THE CHILEAN COPPER STABILIZATION FUND

• COPPER IN THE CHILEAN ECONOMY

• 42% of exports in 1997 (35% in 93/94)

• 3.6% of GDP in fiscal revenues in 1997

• Will continue to be crucial: 28% of world reserves and 34% of world production (25% in 1990)

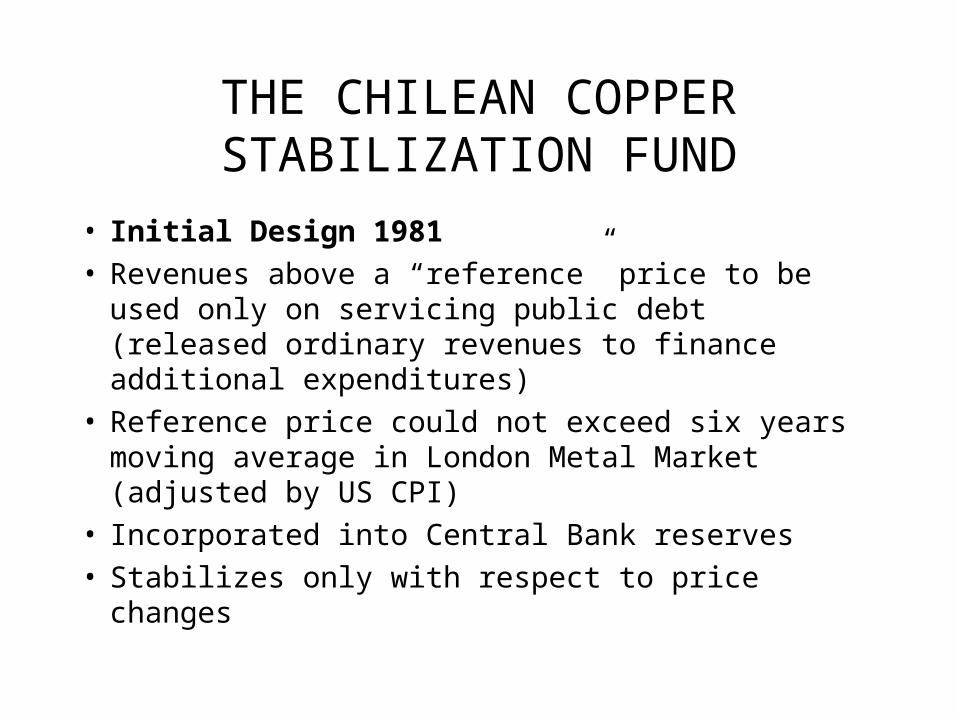

THE CHILEAN COPPER STABILIZATION FUND

• Initial Design 1981• Revenues above a “reference” price to be used only

on servicing public debt (released ordinary revenues to finance additional expenditures)

• Reference price could not exceed six years moving average in London Metal Market (adjusted by US CPI)

• Incorporated into Central Bank reserves• Stabilizes only with respect to price changes

THE CHILEAN COPPER STABILIZATION FUND

• Modifications

• 1985: CSF created as a separate Fund under WB Structural Adjustment Loan

• 1988: Proceeds can be used only for “extraordinary amortizations” of public debt

THE CHILEAN COPPER STABILIZATION FUND

• EVALUATION• Copper price cycles influence fiscal balance, but

less in last decade (Spilimbergo, IMF, April 1999)• Chile is one of the few LAC countries that has

achieved anticyclical fiscal policies (IDB)• Chile’s business cycle associated with copper

prices (3 out of 4 cycles since 1998), though last one less pronounced. Effect mainly through variations in investment

THE CHILEAN COPPER STABILIZATION FUND

• The CSF was crucial to contain political pressures for spending at beginning of democracy (Foxley)

• Recent downturn due to both sharp drop in copper prices and monetary overkill (Perry and Herrera -see graph-)

• About 640mUS$ (1%GDP), from accumulated 1500, used to ease fiscal adjustment in 1998 and 1999.

The Chilean Copper Stabilization Fund.

• Overall, it has contributed to Chile’s strong fiscal stance and anticyclical fiscal policy, and may have moderated but has not completely avoided effects of price on business cycle

THE COLOMBIAN OIL STABILIZATION FUND

• EVALUATION• The OSF has been less important than expected

due to delays in increased production and fall in oil prices (It accumulated around 200mUS against expected 600mUS$ -end 1998-)

• Fiscal balance deteriorated (in spite of it), due to deficits in social security and increased transfers to subnational governments

THE VENEZUELAN FUND FOR MACROECONOMIC

STABILIZATION• Created in 1998

• Savings rule: 80% of revenues from price in excess of five-year moving average.

• Uses: 40% to Social Investment Fund (expenditure!); 30% for public debt reduction; 30% for “Venezuelan Investment Fund” (abroad).

• Present Government may amend legislation.