Embed Size (px)

Citation preview

Measuring Economic Policy Uncertainty

Scott R. Baker (Northwestern)Nick Bloom (Stanford & NBER)Steve Davis (Chicago & NBER)

AEA, January 2015

This paper tries to investigate two questions

• Uncertainty: Does policy uncertainty matter?

• News: Can text search create data (back to 1880s)?

2

We approach policy uncertainty methodically

1) Measuring policy uncertainty

2) Evaluating our measure

3) Estimating the impact of policy uncertainty

Our policy uncertainty index is based on computer search of Newspapers

• For 10 major US papers get monthly counts of articles with:{economic or economy}, and{uncertain or uncertainty}, and {regulation or deficit or federal reserve or congress or legislation or white house}

• Divide the count for each month by the count of all articles

• Normalize each to SD=1, then sum all 10 papers to get the U.S monthly index

Newspapers: • Boston Globe• Chicago Tribune • Dallas Morning News • Los Angeles Times• Miami Herald

• New York Times• SF Chronicle• USA Today• Wall Street Journal• Washington Post

5

Note: We use Access World News Newsbank Service when constructing a daily EPUIndex, because the daily index requires a higher density of news sources.

Constructing our US News-Based EPU Index

5010

015

020

025

0

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

US News-based policy uncertainty index: Jan 1985-Aug 2014

Source: “Measuring Economic Policy Uncertainty” by Scott R. Baker, Nicholas Bloom and Steven J. Davis, all data at www.policyuncertainty.com. Data normalized to 100 prior to 2010.

GulfWar I

9/11

Clinton-Election

Gulf War II

Bush Election

Stimulus Debate

Lehman and TARP

Euro Crisis and 2010 Midterms

Russian Crisis/LTCM

Debt Ceiling; Euro Debt

Black Monday

Fis

cal C

liff

Shu

tdow

n

Note: Analysis uses Newsbank coverage of around 1000 US national and local newspapersSee Table 1 in the Baker, Bloom and Davis (2013) for a more detailed analysis.

Category EPU analysis – look for category terms alongside our economic policy uncertainty terms

Notes: Index of Policy-Related Economic Uncertainty composed of quarterly news articles containing uncertain or uncertainty, economic or economy, and policy relevant terms (scaled by the total number of articles) in 6 newspapers (WP, BG, LAT, NYT, WSJ and CHT). Data normalized to 100 from 1900-2011.

Can run the index back to 1900 using 6 newspapers(Jan 1900 – Dec 2012)

100

200

300

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Po

licy

Un

cert

ain

ty In

dex

Versailles conference

9/11 and Gulf War II

Debt Ceiling

OPEC II

Lehman and TARP

Great Depression, New Deal and FDR

Truman-Deweyelection

Great Depression Relapse Gulf

War IBlack Monday

Start of WW I

OPEC I

Asian Fin. Crisis

Watergate

Assassination of McKinley

Gold Standard Act

Berlin Conference

McNary Haughen farm bill

010

020

030

0

2003 2005 2007 2009 2011 2013

India Economic Policy Uncertainty IndexIn

dia

Bas

ed P

olic

y U

nce

rtai

nty

Ind

exExchange Rate

Fluctuations and WorryLokpal Bill

Source: www.policyuncertainty.com. Data from 7 Indian newspapers (Economic Times, Times of India, Hindustan Times, Hindu, Statesman, Indian Express, and Financial Express)

Congress Party wins National Election

Bear Sterns

Lehman Bros

India-US Nuclear Deal

Price Hikes

010

020

030

040

0

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

China Economic Policy Uncertainty IndexC

hin

a B

ased

Po

licy

Un

cert

ain

ty In

dex

9/11

Political Transition and new National

Congress

Rising Interest Rates

Inflation and Export Pressure

Eurozone Fears and Protectionism

China Stimulus

China Deflation and Deficit

Source: www.policyuncertainty.com. Data until August 2014. Based on newspaper articles from the South China Morning Post.

5010

015

020

025

0

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

North Korean Economic Policy Uncertainty IndexP

olic

y U

nce

rtai

nty

Ind

ex

Source: www.policyuncertainty.com. Data from 0 North Korean newspapers

1992 10 1994 1 1995 4 1996 7 1997 10 1999 1 2000 4 2001 7 2002 10 2004 1 2005 4 2006 7 2007 10 2009 1 2010 4 2011 7 2012 10 2014 10

50

100

150

200

250

300

350

400

450

Orange Revolution in Ukraine

Duma elections and protests

against election fraud

Kizlyar hostage crisis;PM Chubais resigns

Cons

tituti

onal

Cr

isis

Russian financial

crisis

First Chechen

War

Second Chechen

War

Acting PM Gaidar resigns

Russian military

exits Chechnya

Timoshenko resigns;

Terror attack in Nalchik

Parliament dismissedIn Ukraine

Terror attacks in Nalchik & Stavropol

Med

vede

d el

ectio

n

Putin becomes

PM

Lehm

an B

roth

ers

Failu

re

Ukr

aine

Con

flict

Tape

r Tan

trum

Putin

ele

ction

Kiev Euromaidan;

Crimea annexation

12

Russian Economic Policy Uncertainty Index (beta)

Source: Data from Kommersant daily newspaper (1992-2014)

We approach policy uncertainty methodically

1) Measuring policy uncertainty

2) Evaluating our measure

3) Estimating the impact of policy uncertainty

4) Why policy uncertainty changes over time

A) Market Use

Market suggests informational value in the data

I) We have also tracked numerous institutions using the data like Goldmans, Citibank, JP Morgan, Blackrock, Wells Fargo, IMF, Fed, ECB etc (see www.policyuncertainty.com)

II) This has led Bloomberg, FRED, Reuters and Haver to stream the data for their financial and policy users

1020

3040

5060

VIX

(re

d)

5010

015

020

025

0E

co

no

mic

Po

licy

Un

cert

ain

ty In

de

x (B

lue)

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

9/11WorldCom & Enron

Gulf War II

Credit Crunch

Asian crisis

Gulf War I

Obama Election, Banking Crisis

Debt Ceiling

LTCM default

B) Comparison: stock market implied volatility (the VIX)

Correlation 1-month VIX and EPU index = 0.55Correlation 10-year VIX synthetic and EPU index = 0.73

Large interest

rate cuts

Clinton election

Source: www.policyuncertainty.com. Data until October 2012

C) Running Detailed Human Audits10 undergraduates read ≈ 9,098 newspaper articles to date using a 63-page audit guide to code articles if they discuss “economic uncertainty” and “economic policy uncertainty”

16

010

020

030

040

0

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010year

Human index based on audit of 3727 articles (ave=34 per year) in the LA Times and New York Times (the two papers we could audit from 1900 to 2012) versus the historical index for these two papers.

Find humans and computers give similar results in large samples: yearly from 1900

Computer

Human

Correlation=0.837

050

100

150

200

250

1985 1990 1995 2000 2005 2010year

Human index based on audit of 3891 articles (34.7 per month) in the LA Times, New York Times, Miami Herald and SF Chronicle (the five papers we could audit from 1985 to 2012).

Computer

Human

Correlation=0.721

Find humans and computers give similar results in large samples: quarterly from 1985

The human-computer differences are uncorrelated with real outcomes: e.g. GDP growth

-.2

-.1

0.1

.2Y

ea

rly G

DP

gro

wth

-10

12

Co

mpu

ter

hu

man

EP

U %

diff

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Computer human EPU % diff Yearly GDP growth

Yearly economic policy uncertainty index based on human audit of 3727 articles in the LA Times and New York Times (the two papers we could audit from 1900 to 2012) in a 3-year moving average to yield an average of 121 articles per year.

Correlation=0.071

010

020

030

040

0

1985 1990 1995 2000 2005 2010

Papers sorted into 5 most ‘Republican’ or ‘Democratic’ groups using the media slant measure from Gentzkow & Shapiro (2010).

D Bias test: compare 5 most Republican and 5 most Democrat papers – they looks similar

Reagan, Bush I

Bush IIClinton Obama

We approach policy uncertainty methodically

1) Measuring policy uncertainty

2) Evaluating our measure

3) Estimating the impact of policy uncertainty

- Firm-level regressions

- Macro VARs

Microdata: Firm-level estimates exploit differences in industry exposure to government

Use the Federal Registry of Contracts and match this to Compustat firms (using Compustat parent & D&B subsid names)

Generate average industry contracts/revenue (1999 to 2012)

Yit = Fi + Pt + α*Expj*Govt + β*Expj*EPUt + εi,t

Microdata: Run firm level panel regressions

Firm stock price volatility

Firm fixed effects

Period fixed effects

Firm government exposure × government expenditure(1st moment effect)

Firm government exposure × policy uncertainty(2nd moment effect)

i=firm, j=industry, t=quarterEstimated firm by quarter 1996-2012, standard-errors clustered by j

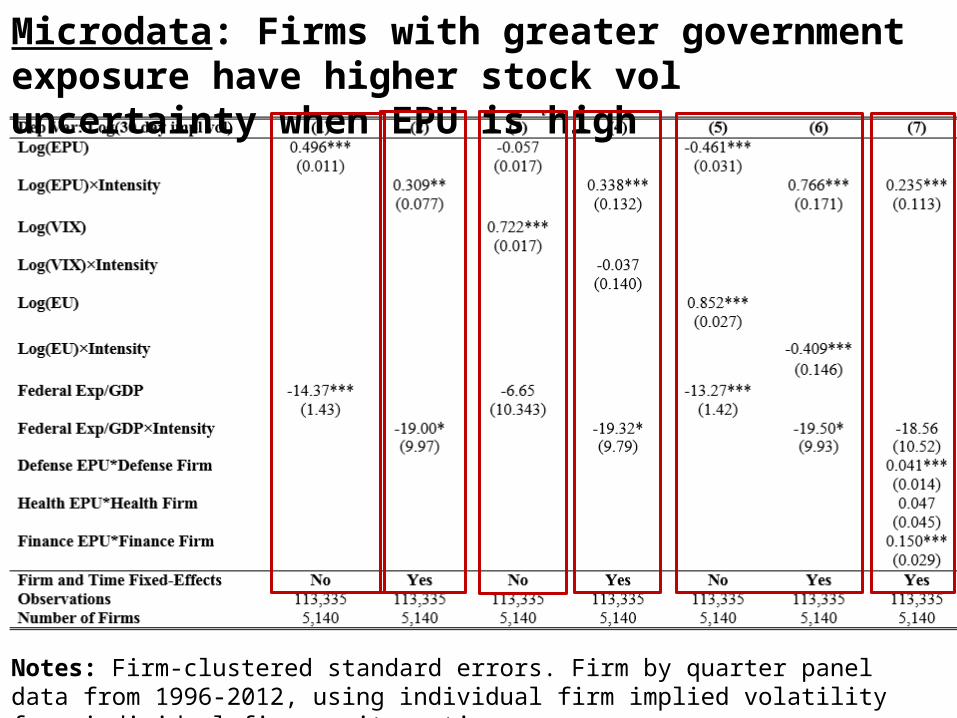

Microdata: Firms with greater government exposure have higher stock vol uncertainty when EPU is high

Notes: Firm-clustered standard errors. Firm by quarter panel data from 1996-2012, using individual firm implied volatility from individual firm equity options.

Microdata: Stock vol uncertainty results are very robust to different measures, samples and controls

Notes: Firm-clustered standard errors. Firm by quarter panel data from 1996-2012, using individual firm implied volatility from individual firm equity options.

Microdata: Firms in sectors with higher government exposure cut investment & hiring when EPU is high

Notes: Firm-clustered standard errors. Firm by quarter panel data for investment and firm by year for employment from 1985-2012.

27

Magnitude for Investment and Employment v. large

in exposed sectors (health, defense & construction)

• Consider EPU increase from 2005/6 to 2011/12 (84%) for firm with govt. exposure of 0.25 (health, defense & constr.).

• Results suggest reduce investment by 9% (similar to average recessionary drop in NIPA investment of 8.5%)

• Results suggest reduce employment by 12% (much larger than average recessionary drop in employment of 2%)

We approach policy uncertainty methodically

1) Measuring policy uncertainty

2) Evaluating our measure

3) Estimating the impact of policy uncertainty

- Firm-level regressions

- Macro VARs

VAR for US industrial production and employment after a 2005/6 to 2011/12 sized EPU shock

Ind

ust

rial

Pro

du

ctio

n, (

%)

Months after the economics policy uncertainty shock

Notes: The impulse response function for Industrial Production and Employment to a rise in the policy-related uncertainty index from the 2005-2006 average value to the 2011-2012 average value. The central (black) solid line is the mean estimate, the dashed (red) outer lines are the one SE bands. Estimated using a monthly Cholesky Vector Auto Regression on: the EPU index, log(S&P 500), federal funds rate, log employment, log industrial production. Monthly data from 1985M1 to 2012M12, using 3 lags.

Em

plo

ymen

t Im

pac

t, (

%)

-1.5

-1

-.5

0.5

1

0 6 12 18 24 30 36year

-.6

-.4

-.2

0.2

0 6 12 18 24 30 36year

-1.5

-1-.

50

.5

0 6 12 18 24 30 36year

VAR robustness

Months after the policy uncertainty shockNotes: This shows the impulse response function for GDP and employment to an increase in the policy-related uncertainty index from the 2005-2006 average to the 2011-2012 average. Estimated using a monthly Cholesky Vector Auto Regression (VAR) of the uncertainty index, log(S&P 500 index), federal reserve funds rate, log employment and log industrial production with 3 lags unless otherwise specified. Data from 1985 to 2012, except for the pre-1985 data spec which uses EPU and IP data from 1920 to 1984.

Ind

ust

rial

Pro

du

ctio

n Im

pac

t(%

dev

iati

on

)

Baseline Bivariate (EPU and industrial production)

Six months of lags

1920-1984 historical data

Adding EU(after EPU)

Adding VIX(after EPU)

Reverse bivariate (industrial production & EPU)

11 Country Panel VAR, with Country & Period FEsIn

du

stri

al P

rod

uct

ion

, (%

)

Months after the economics policy uncertainty shock

Notes: Shows the impulse response function for Industrial Production and employment to an increase in the policy-related uncertainty index from the 2005-2006 average value to the 2011-2012 average value. The central (black) solid line is the mean estimate while the dashed (red) outer lines are the one-standard-error bands. Estimated using a monthly Cholesky Vector Auto Regression (VAR) with 3 lags on the EPU index, log(S&P 500 index), unemployment rate, and log industrial production, plus a full set of country, year and month fixed-effects. Country data weighted by the number of newspapers used to make the EPU series. Fit to monthly data from 1985M1 to 2012M12 where available. Estimated on data from Canada, China, France, Germany, India, Italy, Japan, Russia, Spain, UK and the USA.U

nem

plo

ymen

t Im

pac

t, (

%)

-1.5

-1

-.5

0

0 6 12 18 24 30 36year

0.1

.2.3

.4

0 6 12 18 24 30 36year

-1.5

-1-.

50

0 6 12 18 24 30 36year

11 Country Panel VAR robustness

Months after the policy uncertainty shock

Ind

ust

rial

Pro

du

ctio

n Im

pac

t(%

dev

iati

on

)

Baseline

Bivariate (EPU and industrial production)

Six months of lags

Adding stock volatility

Reverse bivariate (industrial production & EPU)

Dropping stock-price

Notes: XXXX This shows the impulse response function for GDP and employment to an increase in the policy-related uncertainty index from the 2005-2006 average to the 2011-2012 average. Estimated using a monthly Cholesky Vector Auto Regression (VAR) of the uncertainty index, log(S&P 500 index), federal reserve funds rate, log employment and log industrial production with 3 lags unless otherwise specified. Data from 1985 to 2012, except for the pre-1985 data spec which uses EPU and IP data from 1920 to 1984.

No country or time FEs

Conclusions

1. Policy uncertainty fluctuates at a high frequency, driven by the business cycle, the political factors, & shocks (e.g. wars)

2. Policy uncertainty appears to have risen since the 1960s (maybe from political polarization & larger government)

3. Firm-level (and VAR) evidence suggests EPU can:• Substantially increase stock-volatility and reduce hiring &

investment, in defense, healthcare & construction• Moderately reduce overall output and employment

Data available at: www.policyuncertainty.com

Finally, should note all the data is online

Back-Up

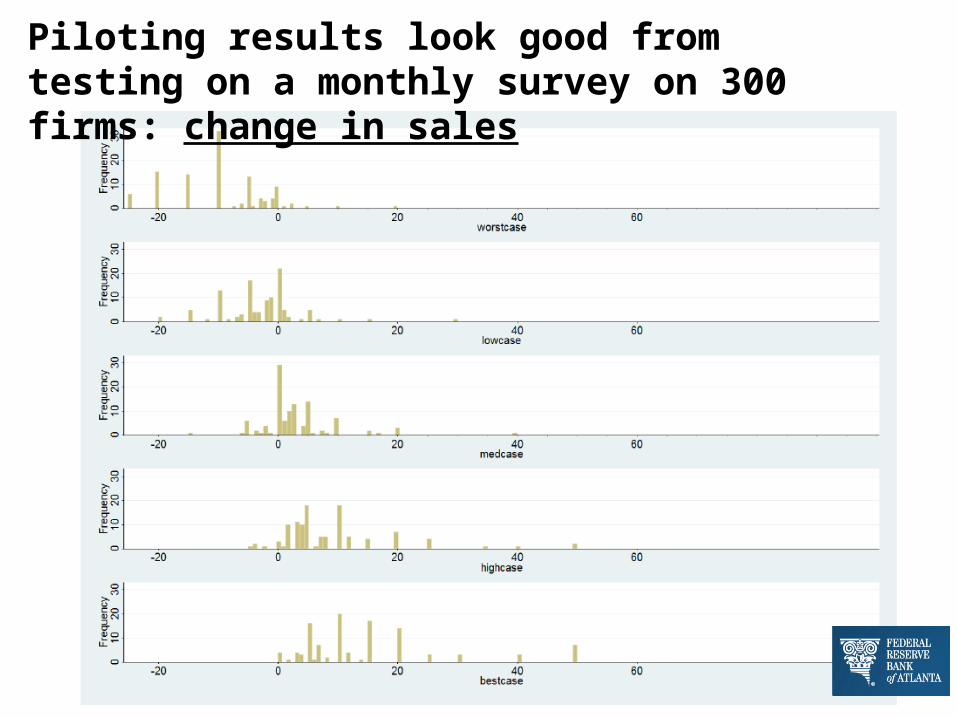

Future Work: working on firm-level surveys

Projecting ahead over the next twelve months, please provide the approximate percentage change in your firm's SALES LEVELS for:

• The LOWEST CASE change in my firm’s sales levels would be: -9 %• The LOW CASE change in my firm’s sales levels would be: -3 %• The MEDIUM CASE change in my firm’s sales levels would be: 3 %• The HIGH CASE change in my firm’s sales levels would be: 9 %• The HIGHEST CASE change in my firm’s sales levels would be: 15 %

Numbers in red are the average response from the pilot on 300 firms

Piloting results look good from testing on a monthly survey on 300 firms: change in sales

Please assign a percentage likelihood to these SALES LEVEL changes you selected above (values should sum to 100%)

• 10 % : The approximate likelihood of realizing the LOWEST CASE change• 18 % : The approximate likelihood of realizing the LOW CASE change• 40 % : The approximate likelihood of realizing the MEDIUM CASE change• 23 % : The approximate likelihood of realizing the HIGH CASE change• 9 % : The approximate likelihood of realizing the HIGHEST CASE change

Numbers in red are the average response from the pilot on 300 firms

Can also ask about probabilities

Piloting results look good from testing on a monthly survey on 300 firms: probabilities

Notes: Data from “The buzz: Links between policy uncertainty and equity volatility”, by Krag Gregory and Jose Rangel, Goldman Sachs, November 12, 2012.

Correlation EPU and 1 month=0.578Correlation EPU and 10 years=0.855

1020

3040

5060

5010

015

020

025

0E

cono

mic

pol

icy

unce

rtai

nty

2002 2004 2006 2008 2010 2012

Implied volatility

1 Month Implied Volatility (♦)

10 Year Implied Volatility (+)

Economic Policy

Uncertainty (•)

Stock market data: More similar to 10 year index of implied volatility on the S&P500 (correlation 0.73)

Jan-85

Jan-86

Jan-87

Jan-88

Jan-89

Jan-90

Jan-91

Jan-92

Jan-93

Jan-94

Jan-95

Jan-96

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

0

20

40

60

80

100

120

140

160 Monetary Fiscal Health Security Regulation

The key sources of policy uncertainty from 1985

Note: This quarterly chart shows the 5 most important sources of economic policy uncertainty based on frequency counts of newspaper articles.

GulfWar I

Clinton Election

Gulf War II

9/11

Lehman and TARP

Black Monday

Fiscal cliff, Europe and DebtCeiling

Gingrich Shutdown

Why is not fully clear – but looking into this along with Jonathan Rodden and Brandice Canes-Wrone

Notes: Frequency of the triple of “economy/economic”, “uncertain/uncertainty” and one of a collection of financial market terms (stock price, equity price, stock market) in 10 major US papers and normalized by the total number of articles, by month and paper. Both series scaled to same mean. Each series set to mean of 100 over entire period.

43

Correlation=0.733

Also tested by fitting events we know - VIX

44

Note: Plots the frequency of the word “uncertain” in each quarter of the Federal Open Market Committees’ (FOMC) Beige Book. Data from 1983Q4 (when the Beige book started) to 2013Q1. The Beige Book is an overview of economic conditions of about 15,000 words in length prepared two weeks before each FOMC meeting. The count of “Policy Uncertainty” uses a human audit to attribute each mention of the word uncertain to a policy context (e.g. uncertainty about fiscal policy) or a non-policy context (e.g. uncertainty about GDP growth). See the paper for full details.

05

10

15

20

25

30

35

40

45

50

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

Uncertainty Policy Uncertainty

Surveys: e.g. compare to the FOMC Beige Book’s mentions of uncertainty and policy uncertainty

Correlation with our EPU index=0.72

1990 Q4 - 1991 Q1

Gulf War I

1993 Q2 - 1993 Q3

Clinton Tax Reforms

2001 Q4 - 2002 Q2

9/11 Attacks

2002 Q4 - 2003 Q2

Gulf War II

2004 Q2 - 2004 Q4

Bush/Kerry Election

2008 Q3 - 2009 Q4

Lehman's and recession

2010 Q1 - 2013 Q1

Debt-ceiling crisis

1983 Q3 – 2013 Q1 Overall Average

Overall Economic Uncertainty 11 8.8 7.7 13.5 5.2 10.2 15.8 5.5Economic Policy Uncertainty 5.5 6.3 1.2 4.8 2.8 0.8 6.8 1.7All Fiscal Matters 1 5.5 1.5 0 0 0.4 3.3 1.0

Taxes Only 0 3.3 0.2 0 0 0.3 1.4 0.4Spending Only 0.5 1 1 0 0 0.2 1.2 0.3

Monetary Policy 0 0 0 0 0 0 0 0Health Care 0 2 0 0 0 0.2 0.5 0.1National Security and War 5.3 0.3 0 2 0 0 0.1 0.2Financial Regulation 0 0 0 0 0 0.2 1.2 0.2Sovereign debt, currency crisis 0 0 0 0 0 0 0.8 0.1U.S. Elections and Leadership Changes 0 0 0 0.2 2.2 0 0.9 0.2Other Specified Policy Matters 0 0.5 0.7 0 0.2 0 0.5 0.2Politics, Unspecified 0.5 1 0 3 0.7 0 1.6 0.3Sum of Policy & Politics Categories 6.8 9.3 2.2 5.2 3.0 0.8 10.0 2.5

Beige Book breakdown also points to similar factors