Embed Size (px)

Citation preview

McKinsey & Company 1

Independent Pricing

Review

NATIONAL DISABILITY INSURANCE AGENCY

Final Report | February 2018

McKinsey & Company 2

Contents

Executive Summary ........................................................................................... 3

The NDIS and pricing ................................................................................... 3

The Independent Pricing Review process .................................................... 3

Feedback from consultation ......................................................................... 4

Key findings and supporting evidence .......................................................... 5

Recommendations ....................................................................................... 6

Implications .................................................................................................. 7

1 Introduction ................................................................................................... 9

1.1 Overview of the NDIS and NDIA ........................................................... 9

1.2 The role of price .................................................................................... 9

1.3 Background and scope of the IPR ....................................................... 10

1.4 Phases of the IPR ............................................................................... 11

1.5 Acknowledgements ............................................................................. 12

2 Input from submissions and consultation .................................................... 13

2.1 Provider economics ............................................................................. 14

2.2 NDIA processes and systems ............................................................. 16

2.3 Market growth and development ......................................................... 17

2.4 Planning process ................................................................................. 18

3 Key findings and supporting evidence ........................................................ 20

3.1 Market development ............................................................................ 20

3.2 Analysis of provider economics ........................................................... 24

3.3 Benchmarking with comparable schemes ........................................... 28

4 Recommendations ...................................................................................... 33

4.1 Approach to price setting ..................................................................... 34

4.2 National vs regional pricing ................................................................. 40

4.3 Pricing of one-to-one services with different levels of complexity ........ 47

4.4 Pricing of Short term accommodation services .................................... 56

4.5 Thin and undersupplied markets ......................................................... 58

4.6 Provider efficiencies and adequacy of provider returns ....................... 63

4.7 Price deregulation ............................................................................... 86

Appendix A: Differences in cost drivers between attendant care providers ....... 92

Appendix B: Summary of IPR recommendations .............................................. 94

Appendix C: Variation in attendant care cost drivers across jurisdictions .......... 97

Appendix D: Existing definitions of participant complexity within the NDIA ....... 99

Appendix E: Opportunities for attendant care providers to innovate ............... 100

Glossary and Abbreviations ............................................................................ 102

McKinsey & Company 3

Executive Summary

THE NDIS AND PRICING

The National Disability Insurance Scheme (NDIS) is a new way of providing support for

460,000 Australians with permanent and significant disabilities (‘participants’). It represents a

fundamental shift in how disability support is delivered. Under the NDIS, participants can

exercise choice and control by purchasing their supports directly from providers. This means

funding of disability supports will no longer take place through block funding for providers, but

rather through individualised support funding for participants.

Once the NDIS reaches maturity, it is intended that the market itself will set the price of

supports. However, temporary price controls are needed to ensure participants can access

affordable supports, while the market is still growing. The National Disability Insurance Agency

(NDIA) uses price caps on many supports and services to regulate price, but striking the right

balance is challenging. If prices are set too high, this will encourage the supply of supports,

but reduce the purchasing power of participants and negatively impact the sustainability of the

NDIS. If prices are set too low, this could lead to a supply shortfall in the market and

compromise participant outcomes.

Some providers of disability supports and other stakeholders have expressed views that

current price caps are too low and are hindering market development. These issues have

been raised in submissions by providers to the NDIA, as part of the NDIA FY2017/18 Price

Review, as well as to the Productivity Commission as part of the review of NDIS costs.

THE INDEPENDENT PRICING REVIEW PROCESS

In June 2017, the Board of the NDIA commissioned McKinsey & Company to undertake an

Independent Pricing Review (IPR) to investigate the appropriateness of the NDIA’s pricing

strategy and approach, and the suitability of current price levels for supports and services.

The scope of the IPR was defined by the NDIA Board in the Terms of Reference (TOR):

1. Provide recommendations in relation to improved pricing effectiveness, including but not

limited to:

– National versus regional pricing

– Pricing of services with different levels of complexity

– Pricing of respite services

– Thin and undersupplied markets, particularly in regional and remote areas

– Relative provider efficiencies, including overheads

– Adequacy of provider returns

– Effectiveness of the Hourly Return approach used to set prices

McKinsey & Company 4

2. Provide recommendations in relation to the potential early deregulation of price in more

mature sub-markets and the glide path for the eventual deregulation of price more

generally.

Over the last six months the IPR team has conducted its review, including extensive

consultations with stakeholders – providers, peak bodies, the NDIA, academics, and state and

territory governments. Through the provider consultation process, the IPR team engaged with

over 1000 individuals across Australia through 10 open forums, 9 webinars and 45 one-on-

one interviews, to understand how providers have been responding to current price settings.

The IPR team also undertook detailed analyses of provider economics, market development

and NDIA data. This report provides a summary of the evidence gathered by the IPR team,

and 25 recommendations for changes to the NDIA’s pricing approach and policies.

Recommendations are grouped by the items in the Terms of Reference.

FEEDBACK FROM CONSULTATION

Key issues raised by providers and other stakeholders in submissions and during the

consultation process were:

■ The NDIS requires a significant change in providers’ operating models and there are

administrative costs associated with transition; as well as opportunities to improve the

efficiency of the NDIA’s systems and processes, for example, the online portal.

■ Current loadings for complex participants do not fully reflect the additional costs of

serving these participants, such as higher wages for a more skilled workforce, additional

time required for training and reporting, and higher supervision ratios. In addition, there is

no clear definition of what constitutes ‘complex’, and as a result the high intensity loading

is applied inconsistently.

■ Current travel allowances do not adequately cover the costs of provider travel and

participant transport in regional areas and isolated communities.

Other issues were raised in relation to specific support types:

■ In attendant care, some providers, who have historically been funded by state-

administered block funding, are struggling to adjust their business models to operate

under the NDIS unit-funding model and the current level of price caps. To operate

profitably within the price caps requires improved levels of utilisation and overheads; and

better matching of skills to participant needs.

■ In therapy, the existing single price point does not reflect the diversity in therapy supports

and the travel allowance is insufficient for some participants in regional areas. In

addition, limiting therapists to recover the costs from a maximum of 2 hours of

cancellations per year is imposing additional costs on some therapists.

Additionally, issues regarding the price setting process and the opportunity for innovative price

setting were raised, including:

■ The price setting process could be more transparent, and providers would appreciate

earlier communication of changes to price level and/or structure to refresh service

agreements and adapt operating models.

McKinsey & Company 5

■ Some providers and participants expressed the desire for the NDIA to explore outcomes-

based approaches to pricing on the basis that would create better incentives to improve

outcomes than the current hourly rate approach.

KEY FINDINGS AND SUPPORTING EVIDENCE

To address the issues raised by providers and other stakeholders during consultation, and

to assess whether current price caps are adequate, the IPR team looked at three sources of

evidence: evidence of market development/supply shortages; provider economics and

operating models; and benchmarks of comparable schemes.

The key findings of the IPR are:

■ While there is not yet evidence of generalised supply shortages, data on market

development is mixed and there are certain markets for which undersupply is a risk in the

future:

– Across support types, provider entry and exit data suggests market growth is keeping

pace with demand and utilisation data does not provide compelling evidence of supply

shortages:

□ The rate of growth of month-to-month provider registration outpaced the rate of

growth of participant registration throughout 2017.

□ Utilisation data from the trial sites suggests lower than expected utilisation was

driven by participants being unfamiliar with the NDIS and how to use their supports,

rather than a supply shortage.

– In the attendant care market, there is not yet compelling evidence of participants

being unable to access supports, but there are signals that are concerning, including

a significant proportion of providers that currently have unprofitable operating models.

– There are cohorts of participants for which supply shortages are high-risk due to the

increased cost of service provision and limited availability of workforce, including

those who: are in outer regional, remote or very remote areas; have complex needs;

are from culturally and linguistically diverse backgrounds; are Aboriginal and Torres

Strait Islander Australians; or have acute care needs such as in crisis situations.

■ While some providers have operating models that are profitable at current price points,

many are struggling, particularly traditional providers delivering attendant care supports:

– In the attendant care market, there is significant variation (from <$40 to $55+ per

hour) in the cost of service delivery between providers. There are examples of low

cost models that are profitable at current price points, including the online platform

model and lean-operating model. However, many traditional providers are struggling

to operate profitably at current price points. This is attributable to a combination of

factors: higher overheads; challenges in adapting to unit pricing and NDIA systems

improvement opportunities; lower utilisation of workers; and higher labour costs.

– In therapy, the single price point is working for some providers, such as physio and

speech therapy providers and many sole traders. However, it is not working so well for

some others, such as psychological therapy for more complex participants.

McKinsey & Company 6

– In Supported Independent Living (SIL), Support Coordination and Plan Management,

feedback indicates that most providers can operate profitably at current price

caps/benchmarks for lower complexity participants. However, the rollout of a more

accurate SIL pricing process may make it more challenging for providers to cross-

subsidise other supports in the future.

■ Benchmarking of NDIA support price caps against comparable schemes highlighted that

the NDIA price is broadly aligned with prices of accident compensation schemes,

including the Transport Accident Commission and WorkSafe, although market prices for

some similar aged care services are higher.

RECOMMENDATIONS

Ultimately, the test of whether the price caps set by the NDIA are adequate is whether

participants can access the quality supports and services required to achieve their goals.

While there is not yet evidence of widespread supply gaps occurring, the Scheme is in a state

of transition and rapid growth, and the situation could change quickly. Further, the absence of

supply gaps does not diminish the fact that the current price caps are challenging, and many

providers are unable to operate profitably within those price caps. Providers and participants

have raised concerns that where providers are unable to supply services at a given price

level, new supply will not be made available quickly enough to ensure that participants have

access to an adequate level of support.

To proactively manage the key risk of supply gaps, the IPR team proposes three steps for the

NDIA to undertake. Firstly, the NDIA should collect and analyse a broader set of indicators of

market development and participant outcomes to both better monitor the risk of supply gaps

and build institutional capacity to avert supply challenges through market intervention.

Secondly, the NDIA should implement appropriate amendments to price loadings and policies,

to improve the economics of efficient providers and reduce the risk of supply shortages in

high-risk markets – particularly rural and remote, and highly complex participants. Those

changes include:

■ Adding a third tier to the complexity loading of 10%, to account for higher level of

skills/experience of workers and additional training required.

■ Allowing providers to charge up to 45 minutes of travel time in rural areas, and quote for

services in isolated regions.

■ Changing the cancellation policy to allow providers to charge participants for

cancellations after 3pm on the day before the service.

■ Removing the $1000 travel cap for therapy supports and aligning the travel policy with

attendant care travel policy.

■ Changing the therapy prices to better reflect different therapy types, and introducing a

second tier of pricing for therapy assistants.

■ Addressing specific NDIA systems and processes, such as portal functionality and

quoting, to enable providers to reduce administrative tasks and overhead costs.

McKinsey & Company 7

Finally, the NDIA should assess the implementation of a temporary price supplement to the

attendant care price cap to address short-term issues with provider economics. The IPR

team’s assessment is that while generalised supply gaps have not occurred to date, there is

a material risk of gaps emerging over the next year. Demand will continue to rapidly increase

as new participants enter the Scheme, and many providers are struggling to operate a

surplus at the price cap with their current operating model. There is a risk that profitable

providers will not grow quickly enough to supply the services required. The IPR team

proposes a model of Transitional Support for Overheads (TSO) in the form of a 2-3%

increase in the price cap of 1:1 attendant care for the next 12 months. This would apply in

addition to the normal annual indexation of the price cap. This adjustment reflects what the

IPR team believes are reasonable cost improvement assumptions for most providers to

achieve in the near term. The exact quantum of the TSO should be a policy decision the

NDIA makes in view of other more targeted interventions government will undertake in the

next 12 months to mitigate the risk of supply shortages. There should be a review in 12

months to determine whether any level of temporary support is required for a further period.

The expectation is that 12 months is a reasonable timeframe for providers to make the

necessary changes to their business models, and for the NDIA to assist and encourage the

development of efficient and effective alternative supply options (e.g. e-marketplaces), so

that the TSO would not need to be renewed.

Longer term, the development of a competitive marketplace should enable changes to the

Scheme’s current pricing model of price caps and fee-for-service. The IPR team’s

recommendations include actions that the NDIA can take to pilot and prepare for different

pricing models. Firstly, the NDIA should conduct a trial of outcomes-based pricing. This is an

appealing alternative to input-based pricing as it encourages providers to maximise outcomes,

rather than the volume of services provided. However, it is significantly more complex and

requires strong baseline data and measurement systems. A trial would provide valuable

learnings on how this approach might be implemented in some supports.

Deregulation of pricing remains an appropriate goal, but there is not yet a clear path towards

reaching it. To better prepare the market and the NDIS for deregulation, the IPR team

proposes strengthening and monitoring provider and participant readiness, including investing

in key infrastructure, such as an e-market. Trialling price deregulation in one geography or

support type market will also help the NDIA collect more detailed information on the impact of

deregulation on market development and participant outcomes.

IMPLICATIONS

In developing its recommendations, the IPR team has sought to address provider concerns in

a way that best balances potential trade-offs between participant outcomes, market

development and Scheme sustainability. The effectiveness and efficiency of pricing

mechanisms and levels was considered, subject to available data. Some recommendations go

directly to changing the effective price, such as Temporary Support for Overheads (TSO) and

a new complexity loading for very complex participants; some target root causes of the

problems, such as changes to cancellation and travel policies; and some propose stronger

market monitoring and intervention capabilities. Each of these recommendation types will

have different impacts on the three Scheme aspirations: better participant outcomes; a

growing market with innovative supports; and a financially sustainable scheme.

McKinsey & Company 8

In the aggregate, the IPR team estimates that the above recommendations will have a

potential financial impact of ~$250-420m per annum over the next 12 to 24 months, will

alleviate some of the financial pressure currently placed on some providers, and will improve

participant outcomes by addressing challenges that are impacting some providers’ abilities to

deliver quality services. Cost estimates have been made on the best data available. However,

data will remain incomplete until the Scheme becomes more mature. As a result, the IPR has

made a number of assumptions leading to a wide range of estimates.

Beyond the next 24 months, the IPR team believe it is possible to implement the IPR

recommendations and manage the Scheme so that it is financially sustainable and within the

current budget estimates. Approximately 50% of the total cost implication of the IPR

recommendations is temporary and will therefore not have an adverse impact on the

Scheme’s longer-term financial sustainability. Also, as the Scheme matures, the NDIA should

be able to offset any financial impact of these recommendations by appropriately assessing

their effectiveness and efficiency. For example, as evidence develops as to which

interventions are most effective in reducing costs associated with complexity, it should be

possible to reduce the number of complex participants and provider costs and prices. It should

also be possible to encourage more local providers in rural and remote areas that will assist in

reducing travel costs. There should also be some savings from introducing tiered therapy

pricing.

McKinsey & Company 9

1 Introduction

1.1 OVERVIEW OF THE NDIS AND NDIA

The National Disability Insurance Scheme (NDIS) is a new scheme designed to change the

way supports and services are provided to Australians with significant and permanent

disabilities (‘participants’). By 2020, the NDIS will provide about 460,000 people with the

reasonable and necessary supports they need to live an ordinary life. The NDIS is currently

in the transition period, with participants entering the Scheme according to an agreed phasing

plan.

The National Disability Insurance Agency (NDIA) is the statutory authority responsible for

administering the NDIS. The NDIA has three external aspirations (NDIA aspirations):1

1. Facilitate outcomes of economic and social independence and deliver an exceptional

service for participants, and their families, carers and providers (‘better participant

outcomes’).

2. Work with participants and other stakeholders to facilitate the growth of a market of

adequate size, quality and innovation (‘a growing market with innovative supports’).

3. Deliver a financially sustainable scheme based on insurance principles within agreed

funding (‘a financially sustainable Scheme’).

1.2 THE ROLE OF PRICE

The NDIS represents a fundamental shift in the way disability supports are provided. Under

the NDIS, people with disability will be able to exercise choice and control over the supports

they receive. This way of providing supports and services requires a transition from a prior

model of block funding for providers, to individualised funding for supports for participants.

In a mature market, participants exercising choice and control will drive the price of supports,

and in turn drive competition and innovation among providers. This is an important feature

of the NDIS. However, where the market is not sufficiently mature and where there is an

imbalance in bargaining power between participants and providers, price regulation helps

ensure value for money for participants.

The NDIA sets price caps for many supports. The price of supports has implications for the

NDIA aspirations, and trade-offs may be required among them (see Exhibit 1). For example,

higher prices may encourage the supply of supports, but reduce the purchasing power of

participants and negatively impact Scheme sustainability, whereas lower prices may increase

value for money but lead to a supply shortfall in the market. Ultimately, the test of whether the

price caps set by the NDIA are adequate is whether participants can access quality supports

and services required to achieve their goals.

1 NDIA: Corporate Plan 2017-21. The Corporate Plan outlines four aspirations for the NDIA: three ‘external aspirations’ and one ‘internal aspiration’, which is to build a high performing NDIA.

McKinsey & Company 10

EXHIBIT 1

1.3 BACKGROUND AND SCOPE OF THE IPR

Some providers of disability supports and other stakeholders have expressed concerns that

some of the current price caps are constraining market development and outcomes for

participants. These concerns were raised in submissions to the NDIA, as part of the NDIA

FY2017/18 Price Review, as well as to the Productivity Commission as part of its review of

NDIS costs. In June 2017, the Board of the NDIA commissioned McKinsey & Company to

undertake an Independent Pricing Review (IPR) to understand the significance of provider

concerns, and create an evidence base to inform decision making and help to mitigate the risk

of future supply shortages as the NDIS transitions to full scheme. The objective of the IPR

was to investigate the appropriateness of NDIA’s current pricing strategy and approach, and

assess the suitability of current price levels for supports and services.

The scope of the IPR was defined by the NDIA Board in the Terms of Reference:

1. Provide recommendations in relation to improved pricing effectiveness, including but not

limited to:

– National versus regional pricing

– Pricing of services with different levels of complexity

– Pricing of short-term accommodation (respite) services

Facilitate outcomes of economic

and social independence and

deliver an exceptional service for

participants, and their families,

carers and providers

Better participant outcomes 1

V

Work with participants and

other stakeholders to

facilitate the growth of a

market of adequate size,

quality and innovation

A growing market with

innovative supports

2

Deliver a financially

sustainable Scheme based

on insurance principles and

within the agreed funding

A financially

sustainable Scheme

3

Speed vs cost

Price impacts pace of market

development and Scheme cost

Value vs speed

Price impacts pace

of market

development and

participant value

for money

Cost vs value

Price impacts

participant value for

money (quality and

quantity of services)

and Scheme cost

Impact of price on three Scheme aspirations

SOURCE: NDIS Corporate Plan 2017-21

McKinsey & Company 11

– Thin and undersupplied markets, particularly in regional and remote areas

– Relative provider efficiencies, including overheads

– Adequacy of provider returns

– Effectiveness of the Hourly Return approach used to set prices

2. Provide recommendations in relation to the potential early deregulation of price in more

mature sub-markets and the glide path for the eventual deregulation of price more

generally.

Pricing of specialist disability accommodation (SDA) was excluded from the scope of the IPR

on the basis that there was separate work being undertaken by the NDIA on this topic.

This report provides a summary of the evidence and findings from provider consultation and

analysis conducted by the IPR team (Sections 2 and 3), and presents recommendations

against each item of the IPR Terms of Reference (Section 4).

1.4 PHASES OF THE IPR

Phase 1 (Jul-Aug 2017): Review of submissions and NDIA documents and initial assessment

of provider economics

The first phase of work consisted of reviewing and analysing the NDIA’s market stewardship

role, building a provider economics/cost model, and analysing supply challenges likely to

emerge at the sub-market level. Submissions to the NDIA and the Productivity Commission

were reviewed and documented, to identify priority issues for further consultation.

The IPR team also conducted analysis of comparable schemes, e.g. Accident Compensation,

Aged Care, and State-funded disability – to assess NDIA prices versus other relevant sectors.

Phase 2 (Sep-Oct 2017): Provider consultation and evaluation of options

Phase 2 focussed on engaging with providers and other stakeholders. The IPR team held ten

provider forums in: Adelaide (SA), Townsville (QLD), Melbourne (VIC) (2), Darwin (NT),

Canberra (ACT), Sydney (NSW) (2), Newcastle (NSW) and Campbell Town (TAS), with

~800 individuals attending in total. In addition, nine online forums were held, with a total

of 270 individuals joining from across Australia.

The IPR team engaged individually with 45 NDIS and aged care providers, and participated in

working groups with providers, peak bodies, advisory groups, and state and territory

governments. This included multiple consultations with the Independent Advisory Council

(IAC) representing participants.

Though no formal written submissions were requested, many providers chose to submit

supporting evidence/documentation to the IPR. In total ~20 written submissions were received

from across the sector; this was in addition to the submissions made to the Productivity

Commission and NDIA FY2017/18 Price Review.

McKinsey & Company 12

Phase 3 (Oct-Nov 2017): Development of draft recommendations

The third phase of work focused on summarising findings, conducting further analysis and

developing draft recommendations. The consultation phase highlighted examples of providers

operating profitably at current price points, as well as examples of providers who find the

current price points very challenging. Phase 3 involved collecting data on different operating

models to identify features of models that are working, and key drivers of cost in models that

are not. The IPR team engaged with providers to identify options for solutions that would help

improve provider economics.

In considering solution options, the IPR assessed the appropriateness of options in achieving

NDIA’s three aspirations- better participant outcomes, a growing market with innovative

supports, and a financially sustainable scheme. Implications of the recommendations were

assessed, and the effectiveness and efficiency of pricing mechanisms and levels were

considered, subject to available data.

Phase 4 (Dec 2017): Syndication and refinement of recommendations and preparation of final

report

The final phase of the IPR involved testing of recommendations with providers and other

stakeholders and preparation of the final report. The implications of recommendations were

identified and quantified, where possible, in terms of impact on the three NDIA aspirations.

Estimates of costs were made based on the best information available. Given a lack of

appropriate data as the Scheme matures, the IPR made several assumptions to inform

estimates of costs, leading to wide ranges in estimates presented in this report.

1.5 ACKNOWLEDGEMENTS

The IPR team is grateful for the cooperation of many providers and representatives of peak

bodies, member groups and state and territory governments, who generously gave up their

time to meet with the team and provide input to the IPR. The IPR would like to especially

thank the 45 providers who met one-on-one with the IPR team and shared detailed financial

information, modelling and analysis, as well as the IAC that invited the IPR to join four of its

meetings.

The IPR team would also like to acknowledge the many individuals within the NDIA who

shared their expertise and helped the team understand current practices related to pricing and

work underway in the NDIA.

Further, the IPR team would like to thank AlphaBeta Advisors who provided support to

McKinsey & Company throughout the entirety of the IPR.

McKinsey & Company 13

2 Input from submissions and consultation

The IPR team examined input from various sources, including:

■ Written submissions to the Productivity Commission report on NDIS Costs; the NDIA

FY2017/18 Price Review; and the IPR team.

■ Face-to-face consultation with providers to the NDIS; providers in adjacent sectors such

as aged care; peak bodies including the Independent Advisory Council (IAC)

representing participants; state and territory governments; and academics.

Provider submissions to the Productivity Commission report on NDIS Costs and the NDIA

FY2017/18 Price Review had different areas of focus. The Productivity Commission sought

responses on pricing with a holistic view of the disability market, whereas the NDIA

FY2017/18 Price Review sought responses focused on specific modelling assumptions

detailed in the 2017 Price Review – Discussion Paper.

The objective of consultation undertaken through the IPR was to identify a comprehensive list

of issues and challenges faced by providers that the IPR team could test for significance and

impact on the NDIA aspirations: improving participant outcomes, growing a market with

innovative supports, and a financially sustainable scheme. To do this, the IPR team consulted

with over 1000 provider representatives through provider forums; and consulted individually

with 45 providers that are broadly representative of the disability market, including providers

across NDIS support types, large and small providers, providers with new service models,

providers delivering services in regional and remote areas, and new entrants with potential to

scale in size.

This section of the report records the challenges and opportunities raised by stakeholders –

as was committed to do during consultation, prior to testing their significance on the NDIA

aspirations. Actions being taken to address some of these challenges, as advised by the

NDIA, are also recorded. Section 3, Key findings and supporting evidence, details evidence

the IPR team sought to test, challenge and validate opportunities, including those raised by

providers, that are within the scope of the TOR. Section 4, Recommendations, outlines the

IPR team’s recommendations to address the challenges and opportunities raised by providers

and other stakeholders, underpinned by further analysis and data to support how these

recommendations assist the NDIA in achieving its three aspirations.

The IPR team recognises that not all challenges and opportunities raised by providers are

specifically within the scope outlined in the TOR. However, where these challenges are likely

to have a flow on impact on provider economics, they have been noted below. Other

challenges that are less likely to impact on provider economics, but could assist the NDIA to

improve participant outcomes, will be raised separately with the NDIA.

Feedback received during consultation can be summarised into four areas:

■ Increasing price loadings to adequately cover the cost of service delivery for rural and

remote geographies, participant cohorts, and support types (see Section 2.1 below).

■ Reducing the cost of administration for providers by improving the NDIA’s provider-facing

systems and processes (see Section 2.2).

McKinsey & Company 14

■ Increasing the emphasis on policies that support the development and growth of the

market, including a greater focus on participant outcomes (see Section 2.3).

■ Improving aspects of participant planning quality and consistency that would assist

provider economics as well as participant outcomes (see Section 2.4).

While discussions with providers centred around challenges they are facing, most expressed

their strong support for the reforms and objectives of the NDIS, and aspirations of the NDIA,

as well as the positive work underway by the NDIA to achieve these aspirations and address

provider challenges. Several providers were also excited about their success in developing

new business models that could work successfully in helping participants achieve their

objectives, and improve their outcomes, in a financially sustainable way.

The remainder of this section summarises provider and other stakeholder feedback on the

following topics:

■ 2.1 Provider economics

■ 2.2 NDIA processes and systems

■ 2.3 Market growth and development

■ 2.4 Planning process.

2.1 PROVIDER ECONOMICS

Many providers raised challenges with the assumptions included in the NDIA’s 2017 Price

review – Discussion Paper, which detailed the input assumptions to be used by the NDIA to

model the price of attendant care (a combined category comprising Assistance with Daily

Living and Assistance with Social and Community Participation). In Section 3 – Key findings

and supporting evidence, the IPR team tests these challenges by benchmarking against other

schemes, and examining effective models that are working in the market, as well as those that

are not working.

These providers considered that the NDIA should continue to refine the following

assumptions:

■ The wage assumption. The NDIA assumes that the disability support worker will be

employed at a level 2.3 under the Social, Community, Home Care and Disability Services

Industry Award (SCHADS Award). Some providers believe the assumption is low and

does not allow for career progression. Other providers commented that they pay higher

wages due to Enterprise Bargaining Agreements (EBA) or a more mature workforce. By

way of contrast, some providers commented that they are successfully operating in a

consistent way with the wage assumption, utilising different mixes of part-time/full-time

employee models, casual employment and accessing new talent pools.

■ The utilisation assumption for support workers. The NDIA assumes a utilisation level of

95% for disability support workers. Some providers believe this level of utilisation is

difficult to achieve. Some providers that consulted with the IPR reported that 80-85%

utilisation of direct support staff is typical. By way of contrast, some are achieving 95% to

100% utilisation.

McKinsey & Company 15

■ The utilisation assumptions for supervisors. The NDIA assumes a 1/15 supervision ratio,

and a utilisation level of 95% for supervisors. Some providers believe this level of

supervision is difficult to achieve, and that it does not allow sufficient time to undertake

quality/compliance requirements and support worker management. Others are finding

that they do not require the level of supervision of 1/15 to offer quality support to the

participants they serve.

■ The overhead assumption. The NDIA assumes an overhead level of 10%, which equates

to 15% if a provider is not subject to payroll tax. Some providers are finding it difficult to

achieve this level of overheads, particularly those with higher expenditure on training,

reporting and participant engagement during transition. While the Department of Social

Services (DSS) and states and territories have provided funding to support transition,

some providers claim this is insufficient – given that the participant-driven service model

requires most providers to make new investments in areas such as training, IT,

marketing, and recruiting. Further, some providers noted that NDIS processes contribute

to higher overheads, e.g. through lost administration time associated with information

and communication technology (ICT) challenges. By way of contrast, some providers

reported that they are currently able to achieve an overhead level of 10%.

Providers also raised issues related to the higher cost of service provision for certain cohorts

of participants. This includes participants living in remote areas, with complex needs, and

those requiring Assistive Technology (AT). More specifically, they considered that the NDIA

should consider the following:

■ Remote loadings are not sufficient for some remote areas where there are high costs-to-

serve due to factors including extra travel time, lack of infrastructure and facilities, and

the cost of deploying/housing a workforce. In some cases, such as for communities in

the Northern Territory, air travel and overnight accommodation is necessary to reach

participants, and this cannot be claimed from the NDIA.

■ Travel is also a concern in some regional areas, as providers are not being fully

remunerated for travel in all circumstances.

■ The differentiation in price levels for support workers serving participants with complex

needs is not sufficient to cover the costs of a higher skilled worker with increased

qualifications or experience, which some providers believe are required to provide high

quality support to these participants. Some providers expressed a view that the current

price could discourage providers, both existing and new entrants, from serving

participants with complex needs and instead focus on those that can be served with a

lower cost support model.

The NDIA has recently announced the development of an independent provider

benchmarking function to generate important strategic information both for providers and the

NDIA. The initiative seeks to collate and share market knowledge on the cost structures and

pricing of providers. Participating providers will receive information that enables them to

understand how they are performing relative to their peers, and where there are specific

opportunities for organisational improvement. The data generated by the project will be at an

aggregate and anonymised level, and will provide government with a clearer sense of what

is happening in the sector, and where intervention by the NDIA may be necessary.

McKinsey & Company 16

2.2 NDIA PROCESSES AND SYSTEMS

Providers raised challenges relating to additional overhead costs associated with operating in

the NDIS, which they believe are partly attributable to NDIA processes and systems.

Opportunities identified by providers for the NDIA to improve system and processes include:

■ Reducing the administrative load when providers interact with the NDIS, including the

one-time costs associated with pre-planning and quoting (where applicable) when a

participant enters the NDIS, and ongoing administration such as billing, invoicing, and

reporting. For example:

– Improve the functionality and efficiency of the Provider Portal, as they consider errors

are still occurring and can be time consuming to resolve.

– Increase the speed at which SIL quotes can be created and processed. Some

providers commented that they have submitted reports between 100-200 pages in

length as part of the additional information they consider is required for ‘above

benchmark’ SIL quotes, while other providers reported that they have waited up to 3

months to receive a response from the NDIA on SIL quote outcomes.

– The quoting process for Assistive Technology and home modifications can

disadvantage the provider developing the initial quote, as they are required to spend

more time and effort to develop a quote together with a participant, typically in-home,

and often an assessor, usually an occupational therapist. As the NDIA requires at

least 3 quotes, additional providers are sent the initial quote to develop their own

quote in isolation from the participant and assessor. This advantages subsequent

providers by giving them the opportunity to undercut the initial quote due to the

reduced cost of quote development.

■ Improving the clarity and consistency in communication of policies to providers. Some

providers commented that they spend significant amounts of time contacting the NDIA,

and become frustrated with the inconsistency of responses from NDIA staff. Others

commented that they’re increasingly satisfied with NDIA staff responses.

■ Increasing the transparency of the price setting process, and the timeliness of

communications relating to price changes, to allow providers sufficient time to update

service agreements prior to pricing changes coming into effect.

The NDIA has advised the IPR team that they have made several improvements in the

design and functionality of the Provider Portal in the last 12-18 months in response to

feedback from providers. However, the NDIA also recognises there are opportunities to

further improve functionality and provider experience, and will continue focusing on this as

part of its ongoing work. The NDIA also has two projects underway to address the

challenges providers are facing relating to SIL: the SIL Tool project, and the SIL Redesign

project. Data from the NDIA shows the SIL Tool has reduced the processing time for SIL

quotes by up to 50%, however additional improvements will be required for the NDIA to

achieve its target of a 14-day turnaround time.

McKinsey & Company 17

2.3 MARKET GROWTH AND DEVELOPMENT

Providers raised issues about price levels inhibiting the growth and development of a skilled

workforce. Some providers believe there is a risk of supply shortage as demand increases

towards Full Scheme, and there are anecdotal reports that some providers are choosing to

reduce their services or not grow beyond their existing service levels due to pricing

constraints. Some providers believe there is also potential that new participants and

participants with complex needs could have difficulty finding a service provider if the market is

not growing at the necessary rate to meet demand. At the same time, these providers

recognise there are also new providers entering the market and some other existing providers

are expanding their services. Providers suggested:

■ Setting prices at a point that allows providers to attract and retain a more skilled

workforce to care for participants with complex needs. Some providers serving

participants without complex needs also raised this as an issue, as they are having

difficulty attracting highly skilled workers necessary for some categories of service.

■ Explicitly allowing a provision for training, as some providers believe the utilisation

assumption used in modelling is not sufficient to cover enough time for training, in

addition to other non-client facing activities such as incident management, administration

and reporting. This issue is more pronounced for providers serving participants with

complex needs.

■ Developing market infrastructure to increase the ability for the market to grow. For

example, there is no functioning e-market, and participants vary in their abilities to

exercise choice and control.

Some participants and providers suggest that the hourly rate approach to pricing does not

provide sufficient incentives to improve outcomes and consistent adherence to insurance

principles. Specifically, they requested the NDIA to consider the following:

■ An approach to pricing consistent with an outcome focus. Prices are currently focused on

units of care in hours. The IAC and some providers would like to see an incentive in the

pricing structure for providers to reduce a participant’s support needs over time. While

the focus on units of care helps to ensure participants receive a defined number of

service hours, it can also inhibit innovation by limiting flexibility in how participant

packages can be spent.

■ A more consistent adherence to insurance principles that focuses on early investment to

reduce participant needs over time and reduce their lifetime cost to the NDIS. Participant

plans should be looked at more holistically to understand how a greater investment in

capital supports such as Assistive Technology and home modifications could reduce the

need for other supports. Looking at capital supports in combination with opportunities to

reduce other supports, and focusing on quality as well as price could improve outcomes

for participants, as well as assist the sustainability of the NDIS.

The NDIA has advised the IPR team that it has identified initiatives to expand its monitoring

and support of market development. It is developing a market assessment framework, which

seeks to bring together disparate data sources and metrics into a coherent assessment

process. It is also investing in a benchmarking function to share market knowledge and

identify opportunities for providers to improve their businesses. The NDIA is also focused on

McKinsey & Company 18

increasing its understanding of how the NDIS is affecting participant outcomes through

regular surveys and participant consultation. For example, the Short-form Outcomes

Framework questionnaire has helped the NDIA build a baseline understanding of participant

outcomes during the NDIS transition period.

2.4 PLANNING PROCESS

The planning process is not formally within the scope of the IPR, as defined in the TOR.

During consultation, issues were raised by providers about how the quality and consistency of

plans could be improved to positively impact both participant outcomes and provider

economics, both initial plans and plan reviews:

■ Improving the planning process to support NDIA planners and Local Area Coordinators

(LACs) to consistently capture all the needs of a participant to deliver quality plans for

participants. This can reduce the time and resources providers invest to help some

participants rectify issues with their plans such as correcting plan errors and submitting

additional documentation to justify the need for additional funding in participant budgets.

It can also help reduce the time providers spend educating participants and their families

on how to engage with the NDIA and LACs, including how to utilise their plans with

providers. These improvements will benefit participant outcomes by ensuring they have

sufficient funds for specific functions. It is recognised by providers that there will always

be more opportunities to improve plans, and the role of the NDIA is to improve the

capabilities of its planners over time in identifying and planning for all needs of

participants and how to improve outcomes.

■ Improving the consistency in timing and communications for plan reviews, to make sure

providers are aware reviews are taking place. This would help providers understand

when they may need to update service agreements with participants, and alert them to

when there could be service continuity issues if there are changes to a participant’s

funding allocation across different supports.

The NDIA has advised the IPR team that significant improvements are underway to the

planning process to address many of the challenges raised by providers, and are currently

being implemented as part of the Participant and Provider Pathways Review. Piloting has

commenced in Victoria in December 2017, with improvements including:

■ A significantly re-designed planning process to make it easier for participants to see how

their goals have been recorded and linked to community, other government services and

funded supports.

■ Face-to-face planning meetings with an LAC, an NDIA planner and a participant to

improve plan quality and educate participants and their families on how to utilise

participant packages.

■ Participants being able to see a working version of their plan as it is developed and the

opportunity to ask questions and provide feedback during the planning meeting, to allow

for any queries to be discussed and addressed before the plan is finalised.

■ The use of simple language to improve communication.

McKinsey & Company 19

Some providers argue that the challenges described in this section are having an impact on

their abilities to operate at a sufficient surplus in the sector. In Section 3 – Key findings and

supporting evidence, and Section 4 – Recommendations, the IPR team has worked with the

providers, the NDIA and other stakeholders to explore the challenges raised by providers that

are within the scope of the TOR, to provide a sufficient evidence base to justify the need for

action, and propose recommendations relating to pricing that can be adopted by the NDIA to

address these challenges.

McKinsey & Company 20

3 Key findings and supporting evidence

To address the issues raised by providers and other stakeholders during consultation, and to

assess whether current price caps are adequate, the IPR team looked at three sources of

evidence:

■ 3.1. Evidence of market development and shortages in supply, including analysis of

the available market data such as utilisation rates, rates of market entry and exit, and

market surveys.

■ 3.2 Provider economics and models, including detailed bottom-up analysis of

providers’ costs-to-serve and comparison with the hourly rate model.

■ 3.3 Benchmarks from other schemes, including comparison of NDIS prices to state

accident compensation schemes and the Commonwealth’s aged care and veterans’

support programs.

3.1 MARKET DEVELOPMENT

Close to 11,000 service providers have been approved to cater to participants in the NDIS,

with approximately 5,000 service providers already active in supplying support services.2

Many of these service providers are small suppliers, with 60% of active providers catering to

fewer than 10 clients each. The larger providers account for most of the Scheme expenditure

to date. Approximately 70% of NDIS payments have been to providers which cater to 100 or

more participants each.3

The IPR team recognises that the provider market landscape is likely to change significantly in

response to providers shifting to a new consumer-driven, unit funded environment. For

example, the current provider landscape for in-home attendant care, a significant support type

in the Scheme, is dominated by not-for-profits and medium to large providers.4 Going

forward, new providers, many of whom are likely to be for-profit organisations, and could

leverage technology innovatively, are expected to enter the market, having identified a

profitable niche or operating model. Some existing providers will exit the support category

because they cannot adjust to this new market landscape, while providers who successfully

adjust their operating models are likely to expand to meet demand. It is unclear how quickly

this market adjustment and new provider entry will occur. A dynamic and responsive approach

to monitoring the market will be critical to ensuring there is sufficient and quality supply to

allow participants to continue to receive safe and quality supports.

The key test of whether current prices are adequate is whether participants can access the

quality supports and services needed to achieve their goals, as defined and funded in their

2 National Insurance Disability Agency: National Insurance Disability Scheme COAG Disability Reform Council Quarterly Report (30 September 2017).

3 Analysis based on NDIS payment data. 4 Not-for-profits consist of 62% of the disability sector, while 88% of in-home attendant care service volume in

2016-17 was delivered by medium to large providers.

McKinsey & Company 21

plans. Market data on participant and provider behaviour and intent offers the most direct

evidence of whether current prices are consistent with this test. Analysis of provider entry and

exit rates, utilisation rates, and participant outcomes reveals a market that is, to date,

providing the supply required to match demand. However, this evidence is not unequivocal.

Gaps in the available data and the volatility of a transitional and rapidly growing market mean

that this data does not yet provide certainty as to whether participants will be able to continue

to access the supports they need into the future.

The remainder of this section examines the available data sources on market development:

Provider entry and exit data

Provider entry and exit data offer evidence of a market that is growing to meet demand.

The number of registered providers more than doubled in FY16/17. The rate of growth of

quarter-to-quarter provider registration has outpaced the rate of growth of participant

registration throughout 2017. In the latest quarter, provider registrations grew by 21%, with a

total of 10,507 providers currently registered in the Scheme.5

In the trial regions, less than 15% of providers decreased or ceased supply during the trial,

whereas 30% of providers increased supply or entered after the trial began (FY13/14 to

FY15/16).6 The existence of some provider exits is also not in itself an indication of

inappropriate prices. It is to be expected that as providers adjust to the NDIS, some will be

unable to make enough changes to their business models and operations to supply services

at an efficient price, while others will choose to specialise in some supports but exit other

supports. It is also important to recognise that providers may have been willing to invest in the

trial to test whether they could develop an effective model, so limited exits during trial may

also not be predictive of future provider behaviour.

Participant utilisation data

Another key data point – utilisation – also does not provide compelling evidence of supply

shortages. The utilisation rate is the share of a participant’s budgeted supports that has been

used. The average utilisation rate across the Scheme in FY16/17 was 66%, which is well

below the expected utilisation of the Scheme at maturity of 85-95%.7 However, the available

evidence suggests that it is more likely caused by participants being unfamiliar with the

Scheme and how to use their supports, rather than a supply shortage. In the trial sites, the

average utilisation rate also started low, at 64%, but increased to 75% in the final year,

reaching 80% in some sites. This change occurred without a reduction in the average size of

plans, discounting the possibility that individual plans simply became more restrictive, despite

the number of participants increasing as the trial progressed. Evidence from transition also

indicates that the utilisation rate increases as participants spend more time in the Scheme and

move onto their second and subsequent plans. The share of participants with high utilisation

rates (>75%) almost doubles from first to subsequent plans. There is little participant survey

5 National Insurance Disability Agency: National Insurance Disability Scheme COAG Disability Reform Council Quarterly Report (30 September 2017).

6 Analysis based on NDIS payment data. 7 Average utilisation rate for FY16/17 as at December 2017. Utilisation rates continue to increase after the end of

the period being measured due to delays in claims and payment processing, so it is likely the final average utilisation rate for FY16/17 will be higher.

McKinsey & Company 22

data to understand the drivers of this utilisation rate. Surveys during the NDIS trial showed

that 27% of NDIS participants had at least some difficulty in accessing supports for which they

had funding. More recently, baseline outcomes performance reported quarterly by the NDIA

shows that 68% of participants nominate having no difficulty in accessing health services they

require. However, a similar metric for NDIS services is not reported.

Analysis of utilisation by support type shows utilisation rates are highest in the largest support

types and supports using attendant care, with the category of core daily care support services

having a utilisation rate of 73% (Exhibit 2). This category includes support services such as

assistance with daily living. Other support types reliant on attendant care, like assistance with

social and community participation (‘Community’) and support for capacity building daily

activities, have the next highest utilisation rates. The lowest utilisation rates are in capital and

intermediary supports, which are of concern but are less likely to represent an imminent

shortfall in critical supports.

EXHIBIT 2

Average utilisation of daily care (core) supports was higher than any other

support type

OtherSupport

Coordin-

ation

Community

41%

Daily care (Core)

58%

44%

Daily care

(Capacity

Building)

73%

48%

Column width scaled to the support’s share of FY2016/17 Scheme expenditure

Uti

lis

ati

on

ra

te

Supports using attendant care

price cap

100%

Target

(85-95%)1

Utilisation rate by support type

Average utilisation rate by support type FY2016/17, %

1 Target utilisation rate estimated based on consultation with the NDIA and review of annual budget papers.

SOURCE: Scheme Actuary, FY17 utilisation data by support category

McKinsey & Company 23

Aggregate analysis of firm entry/exit and utilisation data is complemented by anecdotal

evidence of new private sector investment and innovation. For example, firms such as HireUp

and BetterCaring8 have made large investments to build new digital infrastructure to provide

services in the disability services market. Such upfront investments offer evidence of the

private sector’s willingness to invest in this market. Similarly, the state government in New

South Wales sold its Home Care business for $114 million, indicating the willingness of private

capital to enter the disability services market.

Participant survey data

An evaluation of the NDIS trial by the National Institute of Labour Studies (NILS) revealed

most participants found supports for which they had funding. This survey was initiated in 2014

and therefore covers more of the early experience of the Scheme. Approximately 73% of

participants responded that they were able to access all supports for which they had funding.

The average number of different supports accessed by participants has increased to 3.3 from

2.2 since the introduction of the Scheme, and 44% of participants report having greater choice

and control over the supports they do receive since their enrolment in the NDIS. 9

More recent measurement of participant outcomes reveals that 71% of participants believe

that the NDIS has helped the level of choice and control they experience. 75% of participants

identify the NDIS as having helped their daily living conditions, and 63% identify that it has

helped their social, community, and civic participation.10

Evidence of provider intent

Other factors point to significant challenges as the Scheme continues to grow. The

Productivity Commission acknowledged several studies that point to a potential future shortfall

in supply to meet projected demand, with current workforce growth rate estimated between 6-

13% versus a required growth rate of 18%. However, this can partly be explained by the

ramp-up in demand that is expected, i.e. future growth rates are expected to be higher than

current growth rates. The Productivity Commission also identified several participant cohorts

for which a shortfall in supply is a risk. These included participants in remote and very remote

areas and participants with complex needs. While there is not yet evidence of a shortfall in

supply occurring across the Scheme, this is a risk that needs to be closely monitored.

Furthermore, some providers reported to the IPR team during its consultation process that

they were drawing on surpluses and other funding sources, and cross-subsidising some

support types, to continue to serve participants while they transition. They are concerned as

to whether they can achieve a sustainable operating model in the future. Some major

providers also reported that due to challenging economics operating in the Scheme, they are

not accepting new participants for some services and are planning to reconsider their support

8 Better Caring is not a registered provider under the NDIS, but has a profitable operating model in the disability services market supporting self-managed participants.

9 National Institute of Labour Studies: NDIS Survey of people with disability, their family and carers (2014 – 2017), available at http://ndisevaluation.net.au/information/ndis-survey.cfm

10 National Insurance Disability Agency: National Insurance Disability Scheme COAG Disability Reform Council Quarterly Report (30 September 2017).

McKinsey & Company 24

offerings in 2018. Ongoing close market surveillance and liaison with providers will be

essential for identifying the intention of large providers to exit or reduce services.

3.2 ANALYSIS OF PROVIDER ECONOMICS

The financial sustainability of providers in the NDIS is critical to ensuring ongoing supply of

supports to participants. While providers may be able to absorb losses for a period, operating

in the NDIS needs to be attractive in the long term for enough providers to meet the growth in

demand.

To understand the economics of providers in the NDIS, the IPR team gathered evidence from

various sources, including a detailed cost-to-serve analysis of a sample of NDIS providers.

The IPR team is grateful for the cooperation of many providers, who generously shared

detailed financial information to enable the team to analyse their costs-to-serve.

The remainder of this section examines the evidence available on the following:

■ 3.2.1 Cost of transitioning to the NDIA

■ 3.2.2 Overview of provider economics across support types

■ 3.2.3 Provider economics in attendant care

Cost of transitioning to the NDIS

For providers across all support types, the cost of transitioning to the NDIS and interacting

with the NDIA’s systems and processes added materially to their cost base and affected their

short term financial position.

Moving to a unit-funded, consumer-driven environment has required providers to employ new

staff to process payments and invest in IT systems and marketing. Some providers estimate

that these costs have added 1.5% to their annual expenditure.11 This is detailed further in

Section 4.6.1.

Improving the NDIA’s systems and processes related to the portal and planning as articulated

in Section 4.6.2, would reduce administrative costs and cash flow risk. Anecdotal evidence

indicates that these improvements could amount to ~0.5% of total annual expenditure for

some providers.12 Anecdotal evidence also indicates that the cumulative effect of unapproved

SIL quotes, unresolved portal errors and expired plans has resulted in cash flow risk for some

providers; one large provider submitted that at one point they were owed ~10% of their total

revenue in services unclaimed. The IPR team has been advised by the NDIA that substantial

improvements to the portal have been made in the last 12-18 months, and the NDIA currently

has a significant program of work underway, the Provider Pathway Project, to review and

address the issues noted above.

11 Based on 45 one-on-one interviews with providers in September 2017, in which three large providers (revenue > 50 million in FY16/17) gave detailed evidence of these costs.

12 Based on 45 one-on-one interviews with providers in September 2017, in which three large providers (revenue > 50 million in FY16/17) gave detailed evidence of these costs.

McKinsey & Company 25

Overview of provider economics across support types

Across all support types there were examples of providers operating profitably, and examples

of providers struggling (see Exhibit 3).

EXHIBIT 3

In Supported Independent Living (SIL), Therapy, Support Coordination and Plan

Management, analysis indicated that most providers can operate profitably at current price

points/benchmarks. However, the costs involved in meeting quoting requirements and delays

in approving quotes in SIL are impacting provider overheads.13 In addition, the rollout of the

new SIL pricing process may reduce surpluses that providers are generating, and reduce their

ability to cross-subsidise other services.

In attendant care, there was a higher proportion of providers who submitted they were unable

to operate profitably. Given the emphasis from providers on the challenges associated with

profitably delivering attendant care, the IPR team conducted detailed analysis of provider

economics for this support type.

13 Anecdotal evidence from provider consultation indicates that SIL quoting requirements can be onerous: some providers have submitted reports of 100-200 pages in length to justify above benchmark quotes. NDIA data indicates that the average time to approve a SIL quote in Jul-Sept 2017 was 40 days, down from 107 days pre-July 2017.

SOURCE: Provider Consultation, Sep-Oct 2017

1 Numbers in brackets represent percentage of Scheme spend in FY17, based on payments data provided by the NDIA

Support type1 ChallengingWorking economically

Short term

accommodation

(1.7%)

▪ Providers serving complex participants

▪ Providers operating on weekends/

holiday periods/ overnight

▪ (Limited) Providers serving less complex

participants with lower care ratios

Assistance with daily

life and social/

community

participation

(36.1%)

▪ Providers serving complex participants

or operating in low density areas

▪ Providers with more qualified,

specialist or experienced workforces

▪ Providers with EBAs that are more

generous than the Award

▪ Tech-enabled for-profit providers serving

participants with lower complexity needs or

strong informal supports

▪ Some incumbents with economies of scale

▪ New entrants with lean operating models

Life skills and support

coordination

(5.3%)

▪ Providers serving complex participants,

where plans do not adequately cover

coordination activities undertaken

▪ Support coordination and plan management

providers for low complexity participants

▪ Some employment service providers

Supported independent

living (39.0%)

▪ Providers serving complex participants

with onerous quoting requirements

▪ Emergency/crisis situations

▪ Some SIL providers, as SIL is a quoted item

Therapy

(5.0%)

▪ Remote/rural areas where lots of travel

is required

▪ Some psychotherapy service providers

▪ Some therapy providers (e.g. sole traders in

physio, speech)

▪ Providers in high density, metro areas

Provider cohorts where pricing is working economically versus where it

is challenging

McKinsey & Company 26

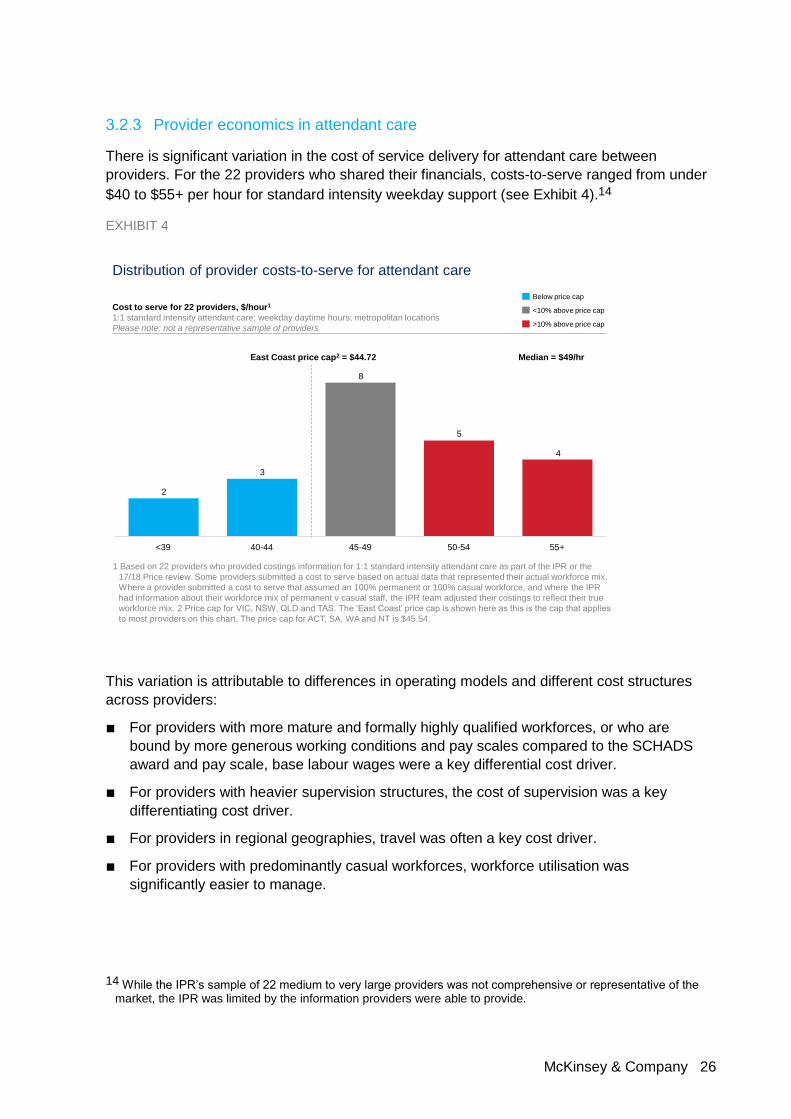

Provider economics in attendant care

There is significant variation in the cost of service delivery for attendant care between

providers. For the 22 providers who shared their financials, costs-to-serve ranged from under

$40 to $55+ per hour for standard intensity weekday support (see Exhibit 4).14

EXHIBIT 4

This variation is attributable to differences in operating models and different cost structures

across providers:

■ For providers with more mature and formally highly qualified workforces, or who are

bound by more generous working conditions and pay scales compared to the SCHADS

award and pay scale, base labour wages were a key differential cost driver.

■ For providers with heavier supervision structures, the cost of supervision was a key

differentiating cost driver.

■ For providers in regional geographies, travel was often a key cost driver.

■ For providers with predominantly casual workforces, workforce utilisation was

significantly easier to manage.

14 While the IPR’s sample of 22 medium to very large providers was not comprehensive or representative of the market, the IPR was limited by the information providers were able to provide.

4

5

8

3

2

45-4940-44<39 55+50-54

East Coast price cap2 = $44.72

1 Based on 22 providers who provided costings information for 1:1 standard intensity attendant care as part of the IPR or the

17/18 Price review. Some providers submitted a cost to serve based on actual data that represented their actual workforce mix.

Where a provider submitted a cost to serve that assumed an 100% permanent or 100% casual workforce, and where the IPR

had information about their workforce mix of permanent v casual staff, the IPR team adjusted their costings to reflect their true

workforce mix. 2 Price cap for VIC, NSW, QLD and TAS. The ‘East Coast’ price cap is shown here as this is the cap that applies

to most providers on this chart. The price cap for ACT, SA, WA and NT is $45.54.

Median = $49/hr

Distribution of provider costs-to-serve for attendant care

Cost to serve for 22 providers, $/hour1

1:1 standard intensity attendant care; weekday daytime hours; metropolitan locations

Please note: not a representative sample of providers

<10% above price cap

>10% above price cap

Below price cap

McKinsey & Company 27

■ There was significant variation in the cost of corporate or indirect overheads between

providers, with expenditure on corporate overheads as a percentage of direct labour

costs ranging from less than 10% to over 20%.15

For a more detailed summary of key drivers of differences in costs between providers, see

Appendix A.

Participant characteristics can also influence provider economics. Margins were more

compressed (or negative) for providers operating in areas with low density of participants, e.g.

rural, remote and very remote areas, and for those serving participants with complex needs.

On the other hand, the profitability of some providers can be in part attributed to their focus on

specific participant segments. Providers who serve participants at the lowest end of the

complexity spectrum often have lower labour and supervisory costs. These providers

submitted that it is not necessary to pay a highly qualified or trained worker to deliver

attendant care supports to participants that are not medically or behaviourally complex, for

whom the risk of incidents is extremely low. Rather what they focussed on ensuring was that

they had support workers with the right mindset, compassion and soft skills to deliver high

quality support.16 Providers who serve participants with predictable and high volumes of care

are also able to operate profitably in attendant care, because workforce rostering and

utilisation is easier to manage.

While a substantial number of providers assessed are not yet able to operate profitably at the

current price cap, there are some providers who submitted they are able to deliver

1:1 standard intensity attendant care at a sustainable surplus, while complying with their

award or enterprise agreement obligations. These providers often have lean operating

models, leverage technology successfully, or are sole traders. Some of these providers have

operated in the sector for some time, while others are new providers that entered the disability

space in response to the NDIS opportunity.

■ Traditional providers with lean operating models: Some traditional providers who run

extremely efficient operations and have achieved a degree of scale are able to operate

profitably. These providers exhibited some, or all, of the following characteristics: lean

corporate overheads facilitated by effective investments in IT systems; effective rostering

systems and a mix of casual and permanent staff to maximise staff utilisation; and/or a

supervision model where supervisors only focus on quality assurance and co-ordination,

while rostering work is done by a separate team. Providers in this group submitted they

can achieve corporate overheads of ~10% of direct labour costs. Providers in this group

who hire predominantly casual workers can maximise the amount of time their workers

perform client-charging work and achieve 95+% workforce utilisation rates. These

15 Data based on information from 22 providers who provided detailed financial information to the IPR. Corporate overheads refers to costs that are not directly attributable to client care (e.g. IT, HR, rent, marketing, business development, senior management salaries).