Embed Size (px)

Citation preview

Max India LimitedMax India Limited

I t P t tiInvestor PresentationNovember 2013

1

BSE Scrip Code: 500271, NSE Ticker: MAX, Bloomberg: MAX:INwww.maxindia.com

MAX GROUP - OVERVIEW

2

www.maxindia.com

Max Group Vision“To be the most admired corporate for service excellence”

Sevabhav• Positive social impact • Culture of Service

Excellence

• Helpfulness • Mindfulness

• Expertise • EntrepreneurshipExcellence

• Dependability • Business performance

• Transparency • RespectCredibility

• Integrity • Governance

3

Our Businesses

M lti b i t F d l d i

“ IN THE BUSINESS OF LIFE ”

Multi-business corporate Focused on people and service

Life InsuranceProtecting Life

HealthcareCaring for Life

Health InsuranceEnhancing Life

Senior LivingProtecting Life Caring for Life Enhancing Life

74:26 JV* with Mitsui Sumitomo;

Largest non bank lead private life insurer

74:26 JV* with Life Healthcare, SA;

2,000 beds

74:26 JV with BUPA Finance Plc, UK

100% Owned;Continuing Care

Retirement Community in Dehradun

Focus on healthcare, children and the environment

Corporate Social ResponsibilityNiche high barrier polymer films & Leather

Finishing Foils

Speciality FilmsClinical Research100% owned;

540+ active sites

4* Max India currently holds 71.1% in Max Life and 65.86% in Max Healthcare

INR 100 Bn+ Revenue* 5 Mn+ Customers 15 000 Employees 50 000^ Agents 1 900+

A unique investment opportunity and a resilient business model

INR 100 Bn+ Revenue .. 5 Mn+ Customers..15,000 Employees.. 50,000^ Agents.. 1,900+ Doctors

Strong growth trajectory even in challenging times; a resilient & diversified business model

1

2

Steady revenue growth and cost rationalization leads to strong financial performance

Well established board governance….internationally acclaimed domain experts inducted

3

4

Diversified ownership…..marquee investor base

Superior brand recall with a proven track record of service excellence

5

6

Strong history of entrepreneurship and nurturing successful business partnerships7

Pharma Electronic Mobile Communication Plating Medical Life Pharma Component Telephony Services Chemicals Transcription

HutchisonCOMSAT

ATOTECH

Insurance

5*Total Revenue for FY13, ^Across Life and Health Insurance

Growth potential recognized by the market….high pedigree investor base

Others9 4%

Shareholding Patternas on Sep 30, 2013

• Reliance MF• Fidelity• Blackrock• Temasek

First State

Shareholding Concentrated

Promoter38.9%

Mutual Funds11.2%

9.4%

• First State• Matthews• Norwegian Govt.

Pension Fund• ICICI Prudential MF• Cresta

Concentrated with Marquee

Investors

IFC

FII (Others)21.1%

IFC3.9%

Goldman Sachs15.5%

Number of outstanding shares : 26.6 Cr.

6

Rs Cr

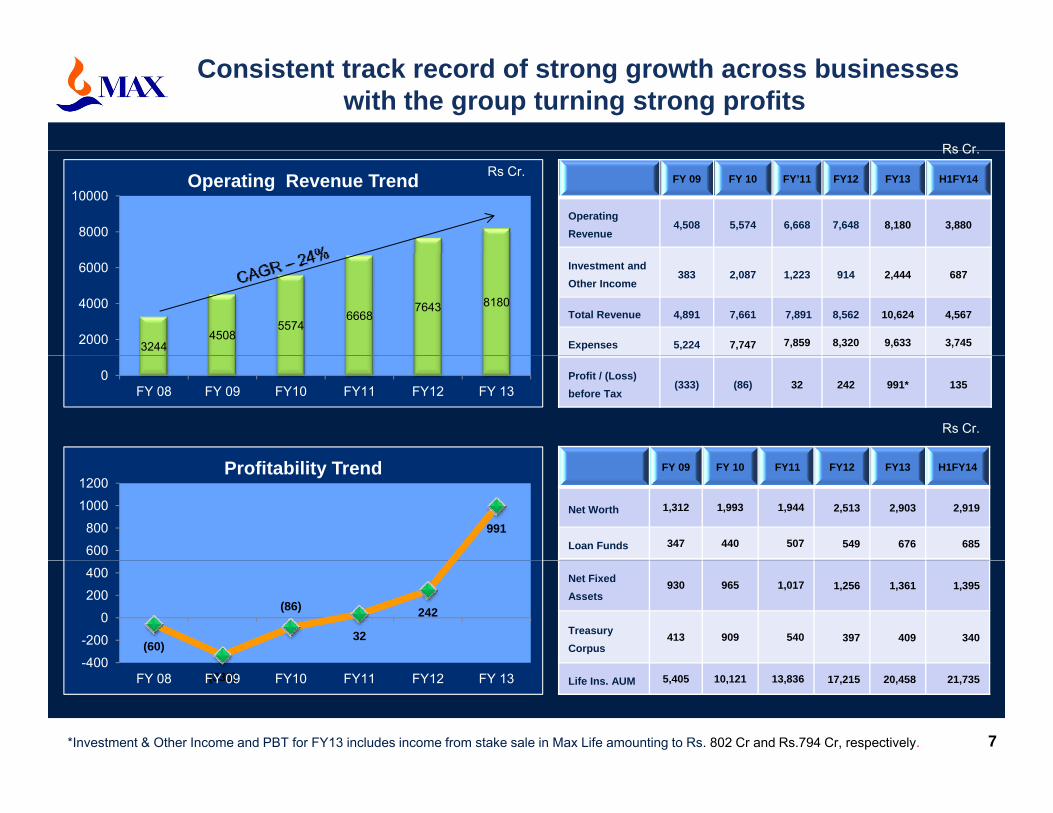

Consistent track record of strong growth across businesses with the group turning strong profits

8000

10000Operating Revenue Trend

Rs Cr.

Rs Cr. FY 09 FY 10 FY’11 FY12 FY13 H1FY14

Operating Revenue

4,508 5,574 6,668 7,648 8,180 3,880

32444508

55746668

7643 8180

2000

4000

6000 Investment and Other Income

383 2,087 1,223 914 2,444 687

Total Revenue 4,891 7,661 7,891 8,562 10,624 4,567

Expenses 5,224 7,747 7,859 8,320 9,633 3,745

0FY 08 FY 09 FY10 FY11 FY12 FY 13

Profit / (Loss) before Tax

(333) (86) 32 242 991* 135

Rs Cr.

FY 09 FY 10 FY11 FY12 FY13 H1FY14

Net Worth 1,312 1,993 1,944 2,513 2,903 2,919

Loan Funds 347 440 507 549 676 685991

600

800

1000

1200Profitability Trend

Net Fixed Assets

930 965 1,017 1,256 1,361 1,395

Treasury Corpus

413 909 540 397 409 340(60)

(86)

32

242

-400

-200

0

200

400

7

Life Ins. AUM 5,405 10,121 13,836 17,215 20,458 21,735(333)-400

FY 08 FY 09 FY10 FY11 FY12 FY 13

*Investment & Other Income and PBT for FY13 includes income from stake sale in Max Life amounting to Rs. 802 Cr and Rs.794 Cr, respectively.

MAX LIFE INSURANCE COMPANY (Max Life)

8

www.maxnewyorklife.com

The Essence of our chosen StrategySources of competitive advantageTo be the most admired life insurance Our objective

company in India with sharp focus on financial metrics

”Build a robust multi-channel distribution

To serve the long-term savings and protection needs of mass affluent+

customers through a high quality agency supplemented by our privileged

Our approach architecture while Max Life’s proprietary high

quality agency will remain the core

distribution channel.”bancassurance partnership

RECREATE GROW TURBOCHARGE OPPORTUNISTIC REDUCE

Key choices

High quality “platinum standard” agency that we were kno n for

Privileged banc-assurance relationship with Axis Bank

Product development process

Change

New PD deals

Group business

Discover growth options for the

Cost

– Driving cost management

Lo eringknown for Enter another bancassurancearrangement

gmanagement and governance

Persistency management

options for the future

– Lowering costs of agency

9

Traditional products continue to dominate ULIPs

Product MixProduct MixApr‐Sep’12 Apr‐Sep’13

9% 42% 49%ICICI Pru

Par Non Par ULIP

4% 42% 54%

39%

32%

3%

28%

58%

40%

M Lif

HDFC Life

SBI Life

42%

27%

11%

35%

47%

38%

63%

71%

76%

17%

4%

11%

20%

25%

12%

Reliance Life

Bajaj Allianz

Max Life

55%

68%

68%

30%

7%

21%

15%

25%

11%

25%

0%

35%

57%

40%

43%

Kotak Life

Birla Sunlife

18%

4%

40%

56%

42%

40%

Most insurers focused on the major segments which were being phased out on 30th Sep – NAV Guaranteed ULIPs& Index linked non‐par products

Relaunch of closed products: Postponement of implementation date will lead to relaunch of some of the

10SOURCE: Market Intelligence

withdrawn products (withdrawn only from field) till

Product closures & continued agency rationalization lead to an increase in agency efficiency parameters

Average Agent Productivity

Average Agent Case Rate

Average Branch Productivity

Apr‐Sep 2013 2012 2013 2012 2013 2012

Insurer Rs. 000s Rs. 000s # # Rs. Lakhs Rs. Lakhs

Bajaj Allianz 4.0 4.3 0.17 0.20 5.9 6.4

Birla Sunlife 3 8 3 4 0 19 0 20 6 7 7 1Birla Sunlife 3.8 3.4 0.19 0.20 6.7 7.1

HDFC Life 4.9 3.9 0.23 0.16 6.9 7.8

ICICI Prudential 4.5 4.9 0.10 0.14 12.1 8.1

Kotak Life 5.2 4.3 0.19 0.15 8.4 7.2

Max Life 10.7 10.4 0.40 0.45 19.8 19.2

Metlife 4.7 6.1 0.16 0.20 6.4 8.1Metlife 4.7 6.1 0.16 0.20 6.4 8.1

Reliance Life 4.6 3.5 0.25 0.26 5.1 3.5

SBI Life 10.5 8.6 0.38 0.37 14.8 10.8

11SOURCE: News Reports, Quarterly Public Disclosures & Market IntelligenceNote: Agency productivity calculated using FYP (100% SP)

Tata AIA 3.9 3.5 0.14 0.13 7.4 6.5

Hi hl d ti Agency base at 39,000+ agents, average case size at ~Rs. 28,000 with average case rate ~0.45

Max Life well positioned for the transformation

Highly productive agency model and best in class training

New Work System under implementation, 23% y-o-y growth in NWS offices, recruitment up 32%

Need based insurance sales

400+ trainers on board

Comprehensive product P d t i f H1FY14 P 69% N 20% ULIP 11%p p

portfolio with an enduring customer base

Product mix for H1FY14: Par 69%, Non-par 20%, ULIP 11%

Long tenor products (21 Yr) & a young customer profile (35 Yr)

Disclosures ahead of competition

First life insurer to disclose Embedded Value; EV for FY13 at Rs. 3,756 Cr. grows 10% y-o-y pre-dividend

Implied NBM on APE* for FY13 at 21 8% v/s 17 8% in FY 12competition Implied NBM on APE for FY13 at 21.8% v/s 17.8% in FY 12

Max Life’s share of private sector grows to 10.4% in H1FY14;

Assets under Management at Rs. 21,735 Cr. as at Sep 30, 2013, grow 13% y-o-y

Over 3.5 million polices in-force with Sum assured touching Rs. 187,000 Cr.Other key drivers

Business capitalised at Rs. 2,127 Cr. as at Sep 30, 2013; solvency surplus of Rs. 1,941 Cr. and solvencymargin of 520%

Pays interim dividend of Rs.128 Cr to shareholders for H1FY14 after paying dividends of 259 Crdividends for FY 13 (post DDT)

Accreditations & Awards

Ranked 2nd in Insurance Industry for India's Best Companies to Work for 2012 by Great Place to Work and Economic Times

Won the 6th National Conference & Competition on Six Sigma, 2012, held by the Confederation of Indian Industry (CII) for the Green Belt project "Power of Speed - Settlement of Claims within 10 days”

Awarded the 6th AIMIA Loyalty Award in the category 'Financials - Non Banking Financial Services Sector'.

12

Silver EFFIE Award in 2012, for the 'Aapke Sachche Advisor' campaign. Organized by The Advertising Club Bombay in India,

QCI DL Shah Awards for Best Six Sigma Project on economics of Quality - 2012

**APE – Adjusted Premium Equivalent (Annualized First Year Premium adjusted for 10% of Single Premium; Limited Premium valued at 50%).

MAX HEALTHCARE (MHC)

13

www.maxhealthcare.in

Indian healthcare industry poised for exponential growth

KEY HIGHLIGHTS• Indian Health Industry is poised to double to USD 125 bn by 2015E, driven by a combination of ageing population, growing

lifestyle diseases and medical insurance penetration as well as increasing ability to afford quality healthcare.

• Realization of latent demand through growth in insurance & consumer education likely to be a key growth driver

• Private hospitals to contribute USD 45 Bn by 2012

• Share of top tier private hospitals (>100 beds) is expected to grow to 40% of the total hospital segment by 2015

• Specialty hospitals are estimated to grow faster than overall industry due to rise in lifestyle diseases

14Sources: Research on India Report , 2010, Healthcare India Report, Fitch Ratings, 2010, FICCI E&Y Report, 2008

• Specialty hospitals are estimated to grow faster than overall industry due to rise in lifestyle diseases

• India needs an investment of USD 86 Bn by 2025 to increase bed density to 2 per 1,000 population

Growing Health Insurance Market...

Increasing prevalence and propensity are key market drivers

Comparative medical cost

11160

80

100

120

billion

g

100

48

65

Comparative medical cost

India UK US

’000

s)

14 17 22 3251

6684

0

20

40

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

Rs

8.5 7 4.5 9.8

3224

6.419.218

Open Heart Knee replacement Lap Cholcystectomy Obesity Surgery

(US

D

Rising health insurance penetration will make healthcare affordable

Cost differentials provide a huge untapped market for medical tourism related business opportunities

International Healthcare Expenditure (as a % of GDP) Per Capita Spending (PPP)

2.9

3.4

1.2

3.3

4.2

3.6

Mexico

Brazil

India

PublicP i

7285

2992

8632000

4000

6000

8000

6.8

6.4

8.4

3.1

0 5 10 15 20

US

Australia Private233

837109

863

0

2000

China Brazil India USA UK Global

China Brazil India USA UK Global

15Sources: FICCI & E&Y Report, 2007, IRDA, B&K report, 2009, Crisil, Research on India Report, 2010

On a per capita basis , both in terms of USD and PPP, India’s Healthcare spend is amongst the lowest globally. However India'shealthcare spending is growing at a healthy CAGR of 14%, rising from 5.5 % of GDP (2009) to 8% (2012)

MHC, with its unique model* is well positioned to deliver high quality of care to patients

Quaternary /Tertiary Care- Max Super Speciality Hospitals – Saket - Max Super Speciality Hospital – Patparganj- Max Super Speciality Hospital – Mohali- Max Super Speciality Hospital – Bhatinda

•Organ Transplant•Neurosciences•Oncology•Cardiac CareMi i ll I i & M t b li SMax Super Speciality Hospital Bhatinda

- Max Super Speciality Hospital – Shalimar Bagh-Max Super Specialty Hospital – Dehradun

Secondary CareSecondary Care

•Minimally Invasive & Metabolic Surgery•Joint Replacement and Orthopedics•Aesthetics and Reconstructive surgery

•Medicine & Allied SpecialtiesMother and Child

Max Hospitals – 3Specialty Centre – 2

•Mother and Child•High-end diagnostics•Infertility and IVF•Eye and Dental care

Primary CareClinics / Implants – 10

•PHP•Specialist doctor consult•Basic diagnostics like pathology collection

•Home Care

• Max Super Specialty Hospitals, SaketM S S i lt H it l P t jNABH & NABL

16

• Max Super Specialty Hospital, Patparganj• Max Hospital, Gurgaon

NABH & NABL Accreditations

*The above model is for MHC’s Network of hospitals and includes Max Super Speciality Hospital , Saket, unit of Devki Devi Foundationand Max Super Speciality Hospital, Patparganj, unit of Balaji Medical and Diagnostic Research Centre

C

Extensive focus on service excellence –a key strength for MHC

• Complete service profile, cutting edge technology and state of the art infrastructure• North India centric strategy allows leveraging of medical capabilities

Comprehensive and integrated healthcare services

Well established brand name throughout India• Patient centric healthcare delivery model with focus on highest quality of care• High operational and clinical efficiency• Won numerous accolades including accreditations by the NABH, NABL and awards by FICCI• Comprehensive range of services offer primary, secondary, tertiary and quaternary care

Well established brand name throughout India

p g p y, y, y q y

•Team of 1,900 doctors complemented by 2,400 nurses and 900 other trained medical personnel*

Network of highly respected and leading specialists

T iti f T ti t Q t C• Foray into Stem cells – service profile enhanced to include Organ Transplant• Revolutionary change in healthcare operations by introducing Electronic Health Records (EHR)• Centres of excellence in cardiac, minimal access, metabolic and bariatric, orthopedics & joint replacement,

neurosciences, pediatrics, obstetrics & gynecology, oncology and aesthetic & reconstructive surgery

Transitions from Tertiary to Quaternary Care

, p , gy gy, gy g y• Research focus- Only centre in Indian subcontinent to conduct basic research in the field of diabetic and

cardiology genetics in collaboration with Imperial College, London

• DNB (Diplomate of National Board) & fellowship programs

Extensive emphasis on medical training and education

17

• DNB (Diplomate of National Board) & fellowship programs• High quality nursing and paramedic care supported by nursing and paramedic college

MHC delivering superior performance across all key metric

56.5%57.2%

59.2% 59.6%61.2%

57 0%

59.0%

61.0%

63.0%

600

750

Revenue and Contribution Margin

18914 19433 2043121558 23585 25126

20000

25000

30000

1000

1200

1400

Avg. operational beds and Avg. revenue per occupied bed day*

372 423 534 685 824 1149

53.1%

49 0%

51.0%

53.0%

55.0%

57.0%

0

150

300

450

662 712 751926 992

1302

0

5000

10000

15000

20000

0

200

400

600

800

49.0%0FY 08 FY 09 FY10 FY11 FY12 FY13

Revenue (Rs cr) Contribution Margin

00FY 08 FY 09 FY10 FY11 FY12 FY13

Avg. operational beds Avg Revenue per bed day (Rs)

Inpatient Trends Outpatient Trends

95114

64785 64390 6880676838

84635 87522

60000

80000

100000

45000

60000

75000

90000

105000Inpatient Trends

3636

446 493565 594

676735

350

500

650

800

20002500300035004000

Outpatient Trends

46532 51103 59130 64335 6937595114

0

20000

40000

0

15000

30000

45000

FY 08 FY 09 FY10 FY11 FY12 FY13

1593 1900 22502906 3103

3636

-100

50

200

0500

10001500

FY 08 FY 09 FY10 FY11 FY12 FY13

18

Inpatient Transactions Avg. revenue per patient (Rs) Outpatient transactions (000's) Avg. revenue per patient (Rs)

*Average revenue per occupied bed day has been calculated on inpatient revenue

MAX BUPA HEALTH INSURANCE (Max Bupa)

19

www.maxbupa.in

A symbiotic partnership in the health insurance space

India’s leading conglomerate Gl b l H lth I id• India’s leading conglomerate• Successful track record of

building businesses • Expertise in life insurance,

• Global Health Insurance provider with market leadership in UK, Spain & Australia

• 12 million customers in over 190 Expertise in life insurance, health insurance and healthcare businesses

• Group revenues in FY 2013 –Rs 10 624 crores

countries• Group revenues in 2012 - £8.5

billion and PBT of £600 millionEmployee base of over 52 000Rs 10,624 crores

• Local perspective of the Indian market

• Culture of service excellence

• Employee base of over 52,000 • Recently voted as best

international health care provider

Leveraging the strengths of both partners to build a robust and profitable

20

Leveraging the strengths of both partners to build a robust and profitable enterprise with focus on service excellence

Industry is poised for an exponential growth

Key drivers of growth

▪ Increase in affordability– Increasing affordability with rise

i i l l d h lth305

351404

464

350400450500

Bill

ion)

Indian Health Insurance Market (Rs. In Billion)

in income levels and healthcare spend per capita

▪ Increase in willingness– Rapid scale-up of hospitals and

i t id t 22 3251 66 83 111

131160

192231

266

100150200250300350

GW

P (R

s. in

expansion outside metros– Take-off of comprehensive

insurance coverage products e.g. secondary healthcare, out-patient etc

17 22 32

050

patient etc.– Higher need with rise in

incidences of chronic diseases (viz. cancer, heart disease)

– Acceptability of insurance with

• Industry grew by 17% in Apr’12-Feb’13 period• CAGR last 5 years at 34%• Expected CAGR of 20 - 25% for next 5-10 years

p yincreasing awareness

▪ Increase in ticket size– Rise in healthcare costs with

market inflation

• Insurers focusing on containing loss ratio’s and improvingprofitability• Standalone health insurers growing aggressively

21SOURCE: Team analysis, WHO statistics, NCAER, McKinsey Urbanisation report, Government economic survey, BRIC report

Relationship

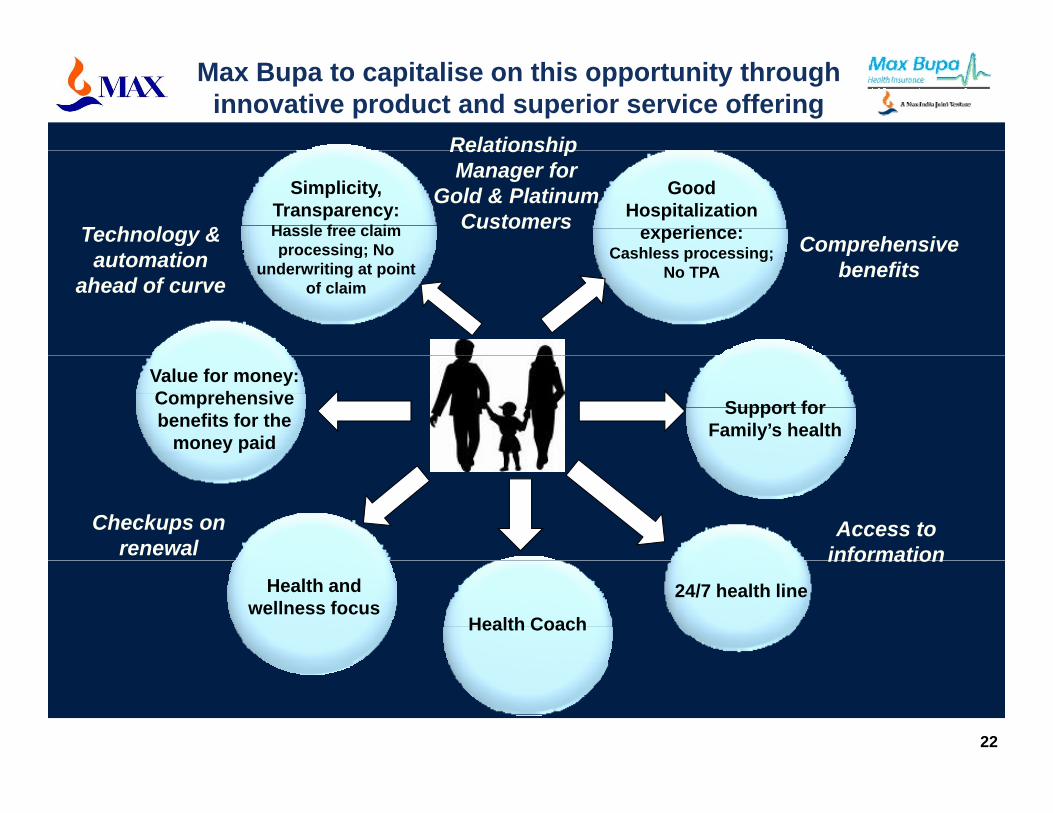

Max Bupa to capitalise on this opportunity through innovative product and superior service offering

Good Hospitalization

experience:Cashless processing;

Simplicity, Transparency:Hassle free claim processing; No Comprehensive

Relationship Manager for

Gold & PlatinumCustomersTechnology &

t ti Cashless processing; No TPA

processing; No underwriting at point

of claim

pbenefitsautomation

ahead of curve

Value for money: Comprehensive benefits for the

money paid

Support for Family’s health

Access to information

Checkups on renewal

Health and wellness focus

Health Coach

information24/7 health line

22

Extensive focus on key growth levers to maximize long-term value

• Max India - strong understanding of Indian Insurance landscape,learning's from Max Life’s success and leverage synergies withMax Life and MHC

• BUPA – Product design, underwriting and clinical expertise

Leveraging Max India and BUPA capabilities

Factsheet* – Max Bupag g p

• Opened up to Standalone Health insurers in February 2013• Tie-up with Deutsche Bank finalised; significant traction on other

discussions

Bancassurance would catapult growth Gross Written Premium^ INR 130 Cr.

Customer Base^ 580K+

• Value based pricing based on data and analysis• Selective targeting of profitable Group business

Pricing for profitability

Customer Base 580K+

Number of Employees 1270+

• Build a culture of innovation and expertise.• Focus on wellness and specialized products with no age limit and

high sum assured.G P l A id t (GPA) d b IRDA 1 t M ’13

Continuous product innovationNumber of Agents 10,000+

• Group Personal Accident (GPA) approved by IRDA on 1st May’13;launched on 15th May’13

• Focus on the mass affluent+ customer base

Focussed customer profile

Number of Offices 21

Partner Hospitals 2,800+

23

• Robust underwriting procedure

* For half-year ended Sep 30, 2013 ^Excludes 781K+ lives under RSBY scheme

MAX SPECIALITY FILMS (MSF)

24

www.maxspecialityfilms.com

Industry marked by robust global and domestic demand

BOPP Global Demand and Supply

6480 6750 7130 7500 7900

77% 76% 77% 77% 78%

60%

80%

100%

6000

8000

10000

(KTA

)

4950 5150 5500 5800 63000%

20%

40%

0

2000

4000

2007 2008 2009 2010 20112007 2008 2009 2010 2011

Capacity Production Utilization

Key Highlights•Growth of flexible packaging Industry ~ 17-18% in India and 7 - 8% globally

•Per capita consumption of BOPP in India relatively lower

•Growth in FMCG and organized retail and changing urban life styles & rural demand.

•Competitive pricing and costs spurs exports from India and restricts imports.

•Shift from PET to BOPP (Indian BOPP:PET products ratio around 1:2 against 3:1 globally)

•BOPP films are recyclable and have a competitive advantage over other plastic and traditional products

25* Surplus absorbed by industry exports, given cost & productivity edge; Source- EY Analysis , AMI BOPP Report-2010

•Convertor industry growing & India becoming global hub for supplies of Flexible Laminates

MSF uniquely positioned to create value

Commodity Speciality(Preferred)

MetallisedFilms Coated Films Foils

End UsePackaging,Industrial,

Textiles

Packaging,Lamination

Packaging,Lamination,Industrial,

Packaging, Industrial

Lifestyle,Apparels

Ma Specialit Films is m ch more than packagingOur Focus

Max Speciality Films is much more than packaging… Manufacturer of niche (high margin) and high barrier speciality polymer films

Pioneer in introduction of value added products/technology in India

Value added products account for 60-70% of total sales

Customer Base in India / Exports

New product development – 6 to 8 per year

26

New product development 6 to 8 per year

Long term relationship with blue chip customers; Preferred Vendor

Visibility in Top Brands

You will FindYou will Find MSF films in…

27

MAX NEEMAN MEDICAL INTERNATIONAL (MNMI)

28

www.neeman-medical.com

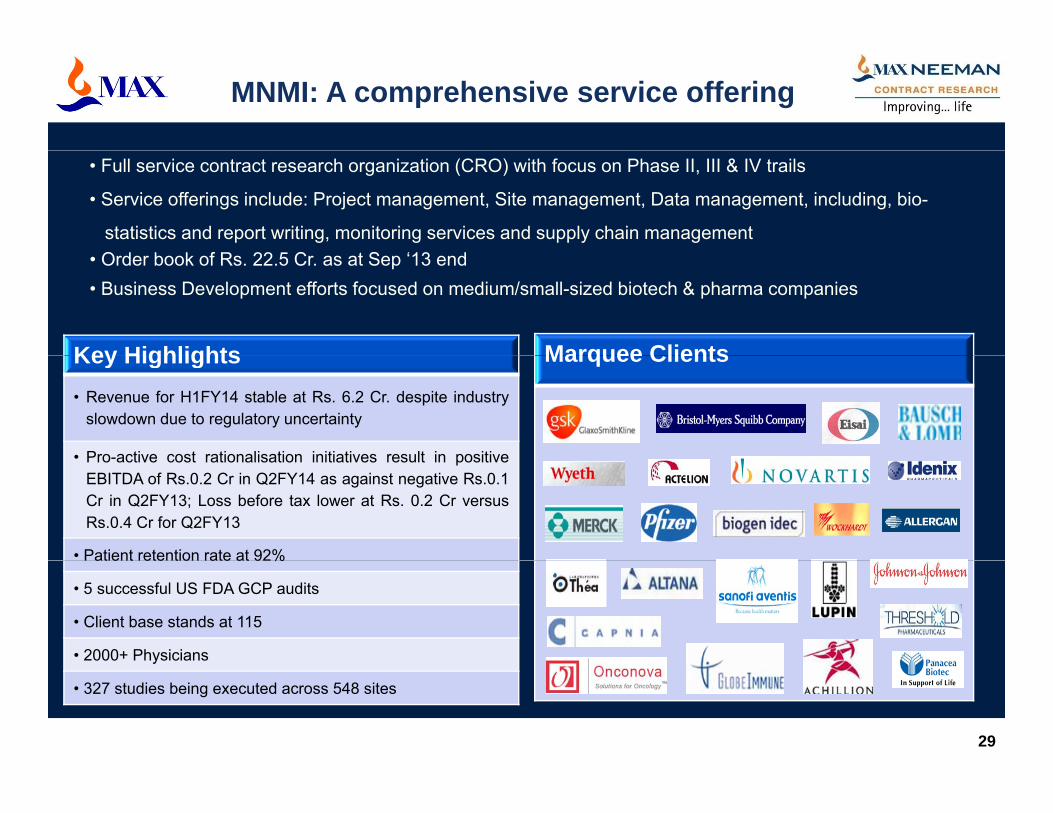

MNMI: A comprehensive service offering

• Full service contract research organization (CRO) with focus on Phase II, III & IV trails

• Service offerings include: Project management, Site management, Data management, including, bio-

statistics and report writing, monitoring services and supply chain managementO d b k f R 22 5 C t S ‘13 d

Key Highlights Marquee Clients

• Order book of Rs. 22.5 Cr. as at Sep ‘13 end• Business Development efforts focused on medium/small-sized biotech & pharma companies

Key Highlights• Revenue for H1FY14 stable at Rs. 6.2 Cr. despite industry

slowdown due to regulatory uncertainty

• Pro-active cost rationalisation initiatives result in positive

Marquee Clients

• Pro-active cost rationalisation initiatives result in positiveEBITDA of Rs.0.2 Cr in Q2FY14 as against negative Rs.0.1Cr in Q2FY13; Loss before tax lower at Rs. 0.2 Cr versusRs.0.4 Cr for Q2FY13

• Patient retention rate at 92%Patient retention rate at 92%

• 5 successful US FDA GCP audits

• Client base stands at 115

• 2000+ Physicians

29

y

• 327 studies being executed across 548 sites

MAX INDIA FOUNDATION (MIF)

30

www.maxindiafoundation.org

MAX INDIA FOUNDATIONMaking a difference… to life

Factsheet* – MIF

Locations 369

Max India Foundation

• Corporate Social Responsibility (CSR) Arm of theMax India Group focused on providing quality Locations 369

NGO Partners 317

Max India Group focused on providing qualityhealthcare to the underprivileged, facilitatingawareness of health related issues, and promotingand fostering an eco-friendly healthy environment.

Beneficiaries 4,80,433

• Immunization• Artificial Limbs & Polio

Awards Received:-•Golden Peacock Global CSR Award 2011•Global CSR Awards at the World CSR Day 2012G ld P k A d f CSR 2012

Initiatives

Callipers• Health Camps• Surgeries & Treatment

•Golden Peacock Award for CSR 2012•“Best CSR Practices 2013” at 7th Indy’s Award •“Best CSR Practices 2013”at the World CSR Day,

• Palliative Care• Lifeline Express Camps• Multi-speciality Camp• Cancer Awareness

31

• Cancer Awareness• Environment Awareness

* Till October, 2013

Thank You

32

Road Map to Becoming India’s Most Admired Life Insurance Company

Key Public MessagesKey Public MessagesKey Public MessagesKey Public Messages

A trusted life insurance specialist Customer centric Financially responsible and strong A great place to work An admired member of the community

VISIONVISION Become the most admired Life Insurance Company in India

MISSIONMISSION

Part of top quartile newLife Insurance Companies National Player Brand of FIRST choice

An admired member of the community

KEY KEY WHAT –Comprehensive suite ofproducts, competitive pricing, extensive distribution, persistency customer service excellence

Employer of Choice Principal of Choice for AgentsKey DifferentiatorsKey Differentiators

Financial Strength & Security Quality of agents Flexible Products

OBJECTIVESOBJECTIVES

STRATEGIESSTRATEGIES

persistency, customer service excellence, profitable portfolios

HOW –TalentedPeople, Professional & Productive Agents, Performance Metrics, Leverage Technology, Teamwork, Customer Centric Innovative Distribution and Marketing

e b e oduc s Service Excellence Fair Terms of Business

Customer Centric, Innovative Distribution and Marketing

INITIATIVESINITIATIVES What-When-Who-How-Cost linkage plans at Departmental and Individual levels

VALUES & BELIEFS OPERATING PRINCIPLES METRICS & PERFORMANCE

Excellence Honesty Knowledge Caring Integrity

VALUES & BELIEFSSTANDARDS MGMT PROCESS Customer comes first

International quality standards Do it right the first time Fact based decisions Bias for result oriented action Financial strength & discipline

Input Output External Internal

Ab l t

GMPR Ratings TEC/TTR – Templates Primary, Shared and

ContributoryB l d dIntegrity

TeamworkFinancial strength & discipline

Direct and open communication Respect Max & NYLI values & parentage Fun at work

Absolute Ratios

Balanced scorecard Core, Functional and

Leadership Competencies

33

Protection Oriented, Longer Tenor Life InsurancePROPORTION OF POLICIES (% b

PRODUCT TYPE Tenure (Y )

Age of Insured(Y )

34

3218.4WHOLE LIFE

POLICIES (%, by number)

(Years) (Years)

44

16

34

34

1.4TERM 25

ENDOWMENT 31.316

0.2DEFERRED ANNUITY

6.6MONEY BACK

18

3015

40

UNIT LINKED 39.8

30

3615

15

HEALTH 0 7HEALTH 0.713 38

GUARANTEED INCOME 1.7 4419

34

21 35Max Life Average Max Life Average

As on 30th Sep 2013

Market Position Insurance Sales

S. No. Company Individual New Business Premium (Rs. Cr) Premium Adjusted for 10% single premium

Apr‐Sep’13 Apr‐Sep‘12 Growth (%) Market Share

1 ICICI Prudential 1 357 1 224 11% 19 9%1 ICICI Prudential 1,357 1,224 11% 19.9%

2 SBI Life 985 711 38% 14.4%

3 HDFC Life 864 1,139 ‐24% 12.7%

4 Max Life 709 635 12% 10.4%

5 Reliance Life 522 410 27% 7.6%

6 Bajaj Allianz 389 427 ‐9% 5.7%

7 Birla Sunlife 383 421 ‐9% 5.6%

8 PNB MetLife 262 242 8% 3.8%

9 ING Life 200 209 ‐4% 2.9%

10 Kotak Life 165 158 4% 2.4%

hOthers 986 1,123 ‐12% 14.5%

Private Total 6,823 6,700 2%

LIC 12,150 13,931 ‐13%

Grand Total 18 973 20 631 ‐8%

35

Grand Total 18,973 20,631 ‐8%

Market Share of Pvt. Players 36.0% 32.5%

Source: IRDA website; Max Life Sales are as reported to IRDA (Cash basis)

Max Life – Embedded Value

Amount in Rs. Crore392^

23

19315March 31, 2013

302

Unwind of Di t

Other Operating Variance

Non Operating Variance

213

3,684

Cost Overrun*

3,756

Value of New Business

Discount

1,973

1,858SH

dividend payouts

Implied NBM** is 21.8% on APE***

(17.8% in 2011-12)1,712 1,898

Opening EV Closing EV

Denotes increase to EV Net Worth

36

Denotes decrease to EV* Cost Over-run includes over-runs that are relevant to Embedded Value. ^ Unwind calculated on the expected basis where the Net Worth earns 8.15% and the VIF earns 13%.**VNB includes shareholders’ interest in the residual estate from participating business aggregating Rs. 32 Cr. Implied NBM is on a structural basis.***APE – Adjusted Premium Equivalent (Annualized First Year Premium adjusted for 10% of Single Premium; Limited Premium valued at 50%).

Value of In-force business

Max Life – Key Assumptions to Embedded Value

Economic Assumptions

Cash/Money Market/TB 7.50%

G Secs 7.96%

Economic Assumptions

Corporate Bonds 8.76%

Equities 13.00%

Unit Linked Fund Growth Rate 10.50%

Interest Rate on Non Unit Reser es 8 15%Interest Rate on Non‐Unit Reserves 8.15%

Inflation 6.50%

Risk Discount Rate 13.00%

Service Tax 12.36%Service Tax 12.36%

Tax Rate 13.52% (12.5% + 5% surcharge + 3% education cess)

Sensitivity

• For change in risk discount rate by 1%, the value of in-force business would change by 4-5%.

Operating Assumptions

• Operating Assumptions like mortality morbidity and lapses are based on our own experience and

37

• Operating Assumptions like mortality, morbidity and lapses are based on our own experience and validated with industry / reinsurers experience.

• Expense assumptions are in line with experience and are unchanged from that used last year.

Max Life – Basis of Preparations for Embedded Value

Max Life’s EV guided by European Embedded Value principles

“Top down” allowance for risk including allowance for time value of financial options and guarantees

Explicit allowance for cost of capital where capital is the higher of the required solvency margin and internal capital requirements

Actuarial assumptions based on past experience and on management’s views of future trends in experiencep

Results not audited nor subject to external review but the EV methodology is in line with accepted international practices

38

is in line with accepted international practices

New Business Growth – Adjusted FYP 1 and

Track record of strong performanceRenewal premium and conservation ratio 2

1308 159513836

1721520458

15000

20000

25000

1500

2000

jAUM

83% 82% 83% 81% 81%78%

90%

30003500400045005000

p

1584 1724 1506 1513

35755405

10,121

0

5000

10000

0

500

1000

1117 2014 3011 3751 4489 473930%

60%

0500

1000150020002500

FY 08 FY 09 FY10 FY11 FY12 FY 13

AFYP (Rs cr) AUM (Rs cr)

FY 08 FY 09 FY10 FY11 FY12 FY 13

Renewal Premium (Rs cr) Conservation Ratio

5180

In force business and No. of policies100%

Distribution Mix

123

155

152169

1 72.6

33.4 3.5 3.6

2.533.544.55

80100120140160180

14%8%

67% 75% 71%50%

36% 34%

60%

80%

100%

70 94

1231.7

00.511.52

020406080

FY 08 FY 09 FY10 FY11 FY12 FY 132% 1% 3% 6% 9% 9%6% 3% 4%

23%41% 49%

25%22% 22%

22%

0%

20%

40%

FY08 FY09 FY10 FY11 FY12 FY13

39

Sum Asssured (Rs 000's cr) Policies million

1. Individual First Year Premium adjusted for 10% single pay2. Conservation ratio = Renewal premium for the current period / (First Year + Renewal Premium for the previous period)

Group Bancassurance Partnership Distribution Own Channel

Max Life Insurance - Financials

Key Business Drivers Unit Quarter Ended Y-o-Y Growth

Half year ended Y-o-Y Growth Sep-13 Sep-12 Sep-13 Sep-12

a) Gross written premium income Rs. Crore

First year premium 416 370 13% 718 644 12%

Renewal premium 1,160 1,095 6% 2,101 2,089 1%

Single premium 103 93 12% 185 168 10%

Total GWP 1,679 1,557 8% 3,005 2,901 4%

b) Shareholder Profit (pre‐tax) Rs. Crore 136 114 20% 248 242 3%

c) Expenses of Management % 18 3% 19 4% 6% 20 1% 20 6% 2%c) Expenses of Management % 18.3% 19.4% 6% 20.1% 20.6% 2%

d) Individual Adjusted Premium (APE*) Rs. Crore 415 366 13% 709 635 12%

e) Conservation ratio** % 79.0% 77.0% 3% 77.0% 77.0% ‐

f) A i R 28 877 24 407 18% 27 884 23 578 18%f) Average case size Rs. 28,877 24,407 18% 27,884 23,578 18%

g) Case rate per agent per month No. 0.43 0.44 ‐2% 0.40 0.45 ‐11%

h) Number of agents No. 39,233 40,021 ‐2% 39,233 40,021 ‐2%

*Individual First Year Premium adjusted for 10% single pay **Conservation Ratio = Renewal Premium for the current period / (First Year + Renewal Premium for the previous period) 40

i) Paid up Capital Rs. Crore 2,127 2,127 0% 2,127 2,127 0%

j) Individual Policies in force No. Lacs 35 35 1% 35 35 1%

k) Sum insured in force Rs. Crore 186,841 158,054 18% 186,841 158,054 18%

MHC – Vision / Mission

B ild T tPASSIONK Diff ti t

VISIONDeliver international class healthcare with a total service focus, by creating an institution committed to the highest standards of medical & service excellence, patient care, scientific knowledge, research and medical education.

• Create exceptional standards of Medical & Service Excellence• Care provider of FIRST CHOICE• Principal Choice for Physicians

Build TrustPASSIONKey Differentiators Focused NCR centric delivery – for operational excellence Leadership in 5 super-specialties in tertiary care

- ‘Star’ physicians supported by a group of high quality physicians Ethics Memorable brand experience

- ‘Star’ and quality physiciansMISSION

GOALS • Profitable without profiteering.• Seamless linkage between secondary and tertiary care.

• Principal Choice for Physicians• Ethical Practices • Create International Centre of Excellence for select Super Specialties.• Safety – Patient, Customer, Staff

Star and quality physicians- Infrastructure and equipment- No surprises – cost of care, pricing, medication- Signage- Look – feel – smell - touch

High quality nursing and paramedic care supported by nursing and paramedic college

KEY OBJECTIVES

STRATEGIES

WHAT –Medical USP’s ; Best in class ; Comprehensive care ; Convenience & accessibility ; Seamless service ; Patient records ; Consistent and customised care ; Service excellence ; Preventive health ; Caring place to work.

HOW –Train train train ; Partnership with Medical community ; Principalchoicefor physicians ; Never ending focus on medical and service excellence ; Build lasting customer relationships ;No franchising.

• WHAT- HOW - WHEN - COST - LINKAGE

Technology and IT

VALUES & BELIEFS OPERATING PRINCIPLESMETRICS &

STANDARDSPERFORMANCEMGMT PROCESS

INITIATIVESWHAT- HOW - WHEN - COST - LINKAGE

• Shared responsibility with single accountability.• Unique approach through: - International benchmarking. - Walk the Talk - IT Capability- Medical – Management Alignment. - Rehearse rehearse - Cost Efficiency- Train train train. - Mystery customers - Attrition Management

Key Public Messages Medical Excellence Service Excellence – Total Experience In your community - near you STANDARDS MGMT PROCESS

• Competence rating• Potential analysis• PSC model• Balanced scorecard• Performance / Risk linked

reward.

• Caring • Excellence• Integrity• - Personal• - Professional• Accountability• Openness/Transparency

• Courtesy & Caring always• Customer comes first• Do it right first time• International image standards• Direct & open communications • Create trust• Compliance• Fun at work

• JCIA Accreditation • ISO 9001 : 2000• Integrated Management System• Credentialing / Grant ofprivileges• Employee productivity• Employee Engagement survey• Service Dashboard - Sparsh

In your community near you High-end tertiary care in Private sector Comprehensiveness Referral system – National & International Value for money

41

p p y• Teamwork• Win-win partnerships

• Fun at work• Reward & Recognition

Service Dashboard - Sparsh• NABH/NABL Accreditation• Adverse event Measurement.

Corporate Social Responsibility

Padma Shri Dr. Rustom Phiroze Soonawala Eminent and Internationally renowned Obstetrician & Gynaecologist

MHC – Key Physicians

MD, FRCS, FRCOG

Chairman, Obstetrics & Gynaecology

Eminent and Internationally renowned Obstetrician & Gynaecologist.

Former President of the Federation of Obstetricians and Gynaecologists

Padma Shri Dr. Pradeep K Chowbey

MBBS, MS, FIMSA, FAIS, FICS, FACS,

Prior to joining MHC, he was Chairman of the Minimal Access Metabolic & Bariatric surgery

center, Sir Ganga Ram Hospital. He has been visiting faculty to the best Medical Institutions like, , , , , ,

Doctor of Science (Honoris Causa)

Chief- Surgery & Allied Surgical Specialties

Director - Minimal Access, Metabolic & Bariatric Surgery

g p g y

Memorial Sloan Kettering Cancer Hospital, NewYork, John Hopkins Institute in USA & Royal

Marsden Cancer Hospital, in U.K. Dr. Chowbey has done his MBBS followed by MS, General

Surgery(1977) from Govt. Medical College, Jabalpur & MNAMS, National board of Examination.

Renowned Joint Replacement Surgeon having 30 years experienceDr. S.K.S. Marya (M.S., DNB, Mch, FICS)

Chairman - Orthopaedics & Joint Replacement

Renowned Joint Replacement Surgeon having 30 years experience.

Pioneered bilateral Hip and Knee Joint replacement.

Author and teacher par excellence.

Renowned Neuro Surgeon having 40 years experience.

Pioneer in the field of neurosurgery credited with many ‘firsts’ in India Median CorpectomyDr. A.K.Singh (M.S., Mch, Diploma WFNS)

Director – Max Institute of Neurosciences, Dehradun

Pioneer in the field of neurosurgery, credited with many firsts in India - Median Corpectomy

for Cervical Spondylosis; Direct Trans Nasal Trans Sphenoidal removal of Pituitary Tumors

and many others. Also won BC Roy Award amongst others

Author and teacher par excellence.

H i 2 f i i S i l O lDr. Harit Chaturvedi (MS, MCH)

Chief Consultant & Director – Surgical Oncology

Having 25 years of experience in Surgical Oncology.

Served institutions of repute like Rajiv Gandhi Cancer Institute, Indraprastha Apollo Hospitals,

Batra Hospital & Medical Research Centre, New Delhi.

Dr. Anurag Krishna 20 years experience in Paediatric surgery -complex congenital malformations

MS, MCh., FAMS

Director, Paediatrics and Paediatric Surgery

Published 50 scientific papers in leading national and international journals

Served as Member of the Board of Management of Sir Ganga Ram Hospital.

42

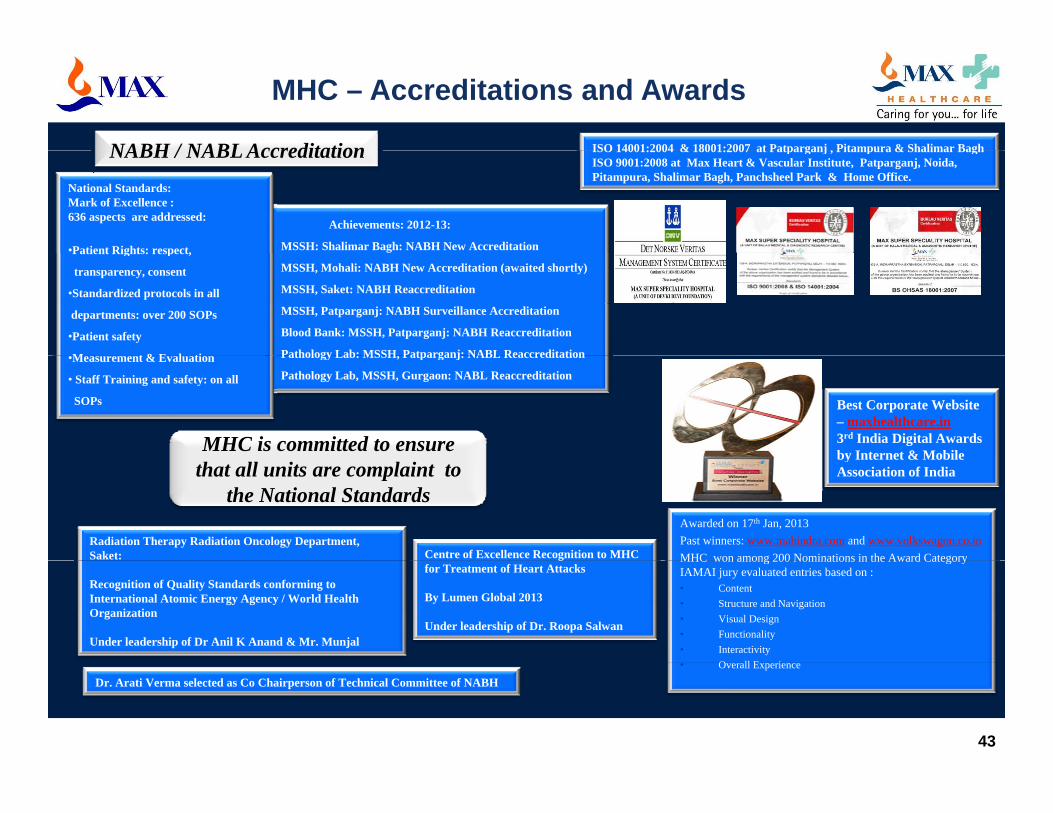

MHC – Accreditations and Awards

NABH / NABL Accreditation ISO 14001:2004 & 18001:2007 at Patparganj , Pitampura & Shalimar Bagh

Achievements: 2012-13:

MSSH: Shalimar Bagh: NABH New Accreditation

National Standards: Mark of Excellence :636 aspects are addressed:

•Patient Rights: respect,

NABH / NABL Accreditation ISO 14001:2004 & 18001:2007 at Patparganj , Pitampura & Shalimar Bagh ISO 9001:2008 at Max Heart & Vascular Institute, Patparganj, Noida, Pitampura, Shalimar Bagh, Panchsheel Park & Home Office.

MSSH, Mohali: NABH New Accreditation (awaited shortly)

MSSH, Saket: NABH Reaccreditation

MSSH, Patparganj: NABH Surveillance Accreditation

Blood Bank: MSSH, Patparganj: NABH Reaccreditation

Pathology Lab: MSSH Patparganj: NABL Reaccreditation

Patient Rights: respect,

transparency, consent

•Standardized protocols in all

departments: over 200 SOPs

•Patient safety

M t & E l ti Pathology Lab: MSSH, Patparganj: NABL Reaccreditation

Pathology Lab, MSSH, Gurgaon: NABL Reaccreditation •Measurement & Evaluation

• Staff Training and safety: on all

SOPs

MHC is committed to ensure

Best Corporate Website – maxhealthcare.in3rd India Digital Awards by Internet & Mobile

that all units are complaint to the National Standards

Centre of Excellence Recognition to MHC Radiation Therapy Radiation Oncology Department, Saket:

Awarded on 17th Jan, 2013Past winners: www.mahindra.com and www.volkswagon.co.inMHC won among 200 Nominations in the Award Category

by Internet & Mobile Association of India

gfor Treatment of Heart Attacks

By Lumen Global 2013

Under leadership of Dr. Roopa Salwan

Recognition of Quality Standards conforming to International Atomic Energy Agency / World Health Organization

Under leadership of Dr Anil K Anand & Mr. Munjal

MHC won among 200 Nominations in the Award CategoryIAMAI jury evaluated entries based on :• Content• Structure and Navigation• Visual Design• Functionality• Interactivity

O ll E i

43

Dr. Arati Verma selected as Co Chairperson of Technical Committee of NABH • Overall Experience

MHC Tertiary Care Facility, Saket [South Delhi]

MAX DEVKI DEVI HEART & VASCULAR INSTITUTE(East & South)

MAX SUPER SPECIALITY HOSPITAL (West)(May 2006)(East & South)

( East :- December 2004, South :- February 2010) Patient beds – (East ; 207 beds) & (South ; 83 beds) 11 OTs, 2 Cardiac Catheterization Labs Tower Specialties – Cardiac Sciences, Minimal Access,

(May 2006) 184 beds (including 71 critical care beds) 7 OTs, 20 Consult Chambers Tower Specialties– Orthopedics, Neuro Sciences,

Obstetrics & Gynecology, Pediatrics and Aesthetic &pMetabolic & Bariatric Surgery, Comprehensive Oncology (Surgical, Medical and Radiation)

Nuclear Diagnostic Services Advanced CT Scan Imaging

C t li d E C d ith Ad d C di Lif

Reconstructive Surgery Brain Suite (first in Asia) and Intra Operative MRI DSA Lab (for Neuro Sciences) Emergency Services High end Radiology facilities with 64 slice Cardiac CT

44

Centralized Emergency Command with Advanced Cardiac Life Support Ambulances and Air Evacuation Service

High end Radiology facilities with 64 slice Cardiac CT

MHC Tertiary Care Facility, Patparganj [East Delhi]

PATPARGANJ BALAJI HOSPITAL (PPG I ) (May 2005)

PATPARGANJ SUPER SPECIALITY HOSPITAL (PPG II) (Feb 2010)(May 2005)

154 inpatient beds 3 OTs General Surgery & MAS Nephrology

(Feb 2010) 259 inpatient beds 7 OTs, 1 Cardiac Catheterization Labs Invasive & Non Invasive Cardiology Cardio Thoracic Vascular SurgeryNephrology

Mother and child care Plastic Surgery & Gastroenterology Other allied specialties

Cardio Thoracic Vascular Surgery Comprehensive Oncology

(Surgical, Medical and Radiation) Orthopedics & Joint Replacement Neurosciences Urology

45

Urology Critical Care & Other allied specialties Ambulatory Care

MHC Tertiary Care Facility [ North India]

Mohali (September 2011)

Bhatinda (September 2011)

142 inpatient beds and 45 Critical Care Beds 5 OTs Oncology Cardiac Sciences Orthopedics

141 inpatient beds and 42 Critical Care Beds 5 OTs Oncology Cardiac Sciences OrthopedicsOrthopedics

Neuroscience Mother and Child Care Urology ENT & Dialysis Plastic and Reconstructive Surgery

Orthopedics Neuroscience Mother and Child Care Urology ENT & Dialysis Plastic and Reconstructive Surgery

46

Plastic and Reconstructive Surgery Dentistry & Day Care

Plastic and Reconstructive Surgery Dentistry & Day Care

MHC Tertiary Care Facility [ North India]

Shalimar Bagh Dehradun (May 2012)(November 2011)

196 inpatient beds and 80 Critical Care 7 OTs Cardiology , Cathlab and Oncology

(May 2012) 166 inpatient beds and 39 Critical Care 4OTs Neurosciences Cardiac Care

Orthopedics and Neuroscience Mother and Child Care and Urology ENT and Dialysis Plastic Surgery and Reconstructive Dentistry & Day Care

Cardiac Care Orthopedics Mother and Child Internal Medicine General Surgery ENT and Dialysis

47

Ophthalmology ENT and Dialysis Eye & Dental Care

MHC Secondary Care Facility [ Suburb of Delhi ]

NOIDA (August 2002)GURGAON (July 2007) PITAMPURA (February 2002)(North Delhi)

32 inpatient beds 2 OTs Mother and child care Non-invasive cardiology

80 inpatient beds 3 OTs Orthopedics & Trauma Ophthalmology (anterior and posterior) Woman and child (including infertility)

(North Delhi) 90 inpatient beds 2 OTs Lithotripsy Mother and child care

Laparoscopic surgery Orthopedics ENT, ophthalmology Urology and nephrology Full range diagnostics

( g y) Medical & surgical intensive care Nephrology and urology Aesthetic and reconstructive surgeries General and minimally invasive surgeries PHP and OPD

Aesthetic & Reconstructive Surgery Non-invasive cardiology Physiotherapy Pediatric & Neonatal Intensive Care Full range diagnostics

48

PHP, OPD and Dentistry Pediatric & Neonatal Intensive Care Full range diagnostics PHP, OPD and Dentistry

MHC Speciality Centres – Panchsheel [South Delhi]

OPTHALMOLOGY AND DENTAL CARE (November 2005)

SPECIALIST CONSULTS AND HIGH END DIAGNOSTICS(November 2005)

Lasik, OPD and diagnostics Dental – 5 chambers Support services and offices

HIGH-END DIAGNOSTICS (August 2006)

GP and specialist consults Diagnostics Neurology (EEG and EMG) Neurology (EEG and EMG) Preventive health and chronic care Physiotherapy Minor procedures and emergencies IVF

H C

49

Home Care

Max Healthcare* – FinancialsQuarter Ended H lf d d

Key Business Drivers UnitQuarter Ended Y-o-Y

Growth

Half year ended Y-o-Y Growth Sep-13 Sep-12 Sep-13 Sep-12

a) Revenue (Gross) Rs. Crore

Inpatient Revenue 262 198 32% 496 387 28%

Day Care Revenue 12 9 36% 22 18 28%Outpatient Revenue 78 65 19% 148 128 16%Other Operating Income (1) 2 ‐ ‐ 4 ‐Total 351 274 28% 667 537 24%

b) ProfitabilityContribution Margin Rs. Crore 217 168 30% 413 326 27%Contribution (%) % 61.8% 61.2% ‐ 62.0% 60.8% ‐EBITDA Rs Crore 31 5 512% 48 24 97%EBITDA Rs. Crore 31 5 512% 48 24 97%EBITDA (%) % 8.9% 1.9% ‐ 7.2% 4.6% ‐

c) Patient Transactions (No. of Procedures) No.

Inpatient Procedures 28,796 23,820 21% 54,254 45,350 20%

D P d 4 465 3 572 25% 17%Day care Procedures 4,465 3,572 25% 8,580 7,362 17%

Outpatient Registrations 994,938 907,999 10% 1,870,773 1,773,450 5%

d) Average Inpatient Operational Beds No. 1,440 1,261 14% 1,417 1,225 16%

e) Average Inpatient Occupancy % 77.7% 70.2% 11% 73.7% 69.3% 6%

50*The above results are for MHC Network of hospitals and includes results for Max Super Specialty Hospital, Saket, unit of Devki Devi Foundation and Max Super Speciality Hospital, Patparganj, unit of Balaji Medical and Diagnostic Research Centre

f) Average Length of Stay No. 3.58 3.42 ‐4% 3.53 3.43 ‐3%

g) Avg. Revenue/Occupied Bed Day (IP) Rs. 25,392 24,278 5% 25,922 24,874 4%

Max Bupa Health Insurance - Financials

Key Business Drivers Unit Quarter Ended Y-o-Y Growth

Half year ended Y-o-Y Growth Sep-13 Sep-12 Sep-13 Sep-12

a) Gross written premium income Rs Crorea) Gross written premium income Rs. Crore

First year premium 39.2 27.8 41% 71.2 52.6 35%

Renewal premium 31.6 13.0 142% 59.1 24.4 142%

Total 70.7 40.8 73% 130.3 77.0 69%

b) Net Earned Premium Rs. Crore 57.8 29.5 96% 105.5 54.5 93%

c) Average premium realization per life Rs. 5,241 4,880 7% 5,308 5,040 5%

d) Conservation ratio % 83% 80% 4% 82% 77% 6%

e) Number of agents No. 10,124 7,415 37% 10,124 7,415 37%

f) Paid up Capital Rs. Crore 556.0 448.5 24% 556.0 448.5 24%

51

g) No. of Lives (excl Rural & Social) No. 162,310 88,491 69% 291,592 186,780 67%

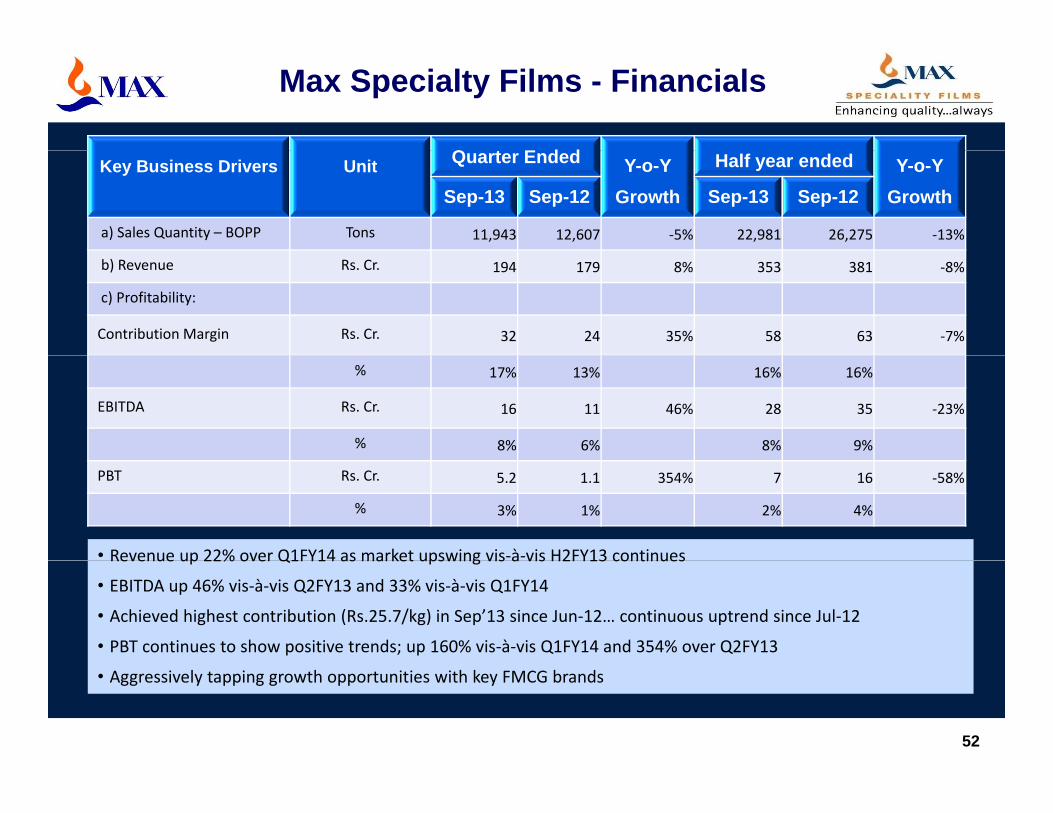

Max Specialty Films - Financials

Q t E d dKey Business Drivers Unit Quarter Ended Y-o-Y Growth

Half year ended Y-o-Y Growth Sep-13 Sep-12 Sep-13 Sep-12

a) Sales Quantity – BOPP Tons 11,943 12,607 ‐5% 22,981 26,275 ‐13%

b) Revenue Rs. Cr. 194 179 8% 353 381 ‐8%

c) Profitability:

Contribution Margin Rs. Cr. 32 24 35% 58 63 ‐7%

% 17% 13% 16% 16%

EBITDA Rs. Cr. 16 11 46% 28 35 ‐23%

% 8% 6% 8% 9%

• Revenue up 22% over Q1FY14 as market upswing vis‐à‐vis H2FY13 continues

PBT Rs. Cr. 5.2 1.1 354% 7 16 ‐58%

% 3% 1% 2% 4%

Revenue up 22% over Q1FY14 as market upswing vis à vis H2FY13 continues

• EBITDA up 46% vis‐à‐vis Q2FY13 and 33% vis‐à‐vis Q1FY14

• Achieved highest contribution (Rs.25.7/kg) in Sep’13 since Jun‐12… continuous uptrend since Jul‐12

• PBT continues to show positive trends; up 160% vis‐à‐vis Q1FY14 and 354% over Q2FY13

52

• Aggressively tapping growth opportunities with key FMCG brands

Disclaimer

This presentation has been prepared by Max India Limited (the “Company”). No representation or warranty, express or implied, is made and nop p p y ( p y ) p y, p p ,reliance should be placed on the accuracy, fairness or completeness of the information presented or contained in the presentation. The pastperformance is not indicative of future results. Neither the Company nor any of its affiliates, advisers or representatives accepts liabilitywhatsoever for any loss howsoever arising from any information presented or contained in the presentation. The information presented orcontained in these materials is subject to change without notice and its accuracy is not guaranteed.

The presentation may also contain statements that are forward looking. These statements are based on current expectations and assumptionsthat are subject to risks and uncertainties. Actual results could differ materially from our expectations and assumptions. We do not undertakeany responsibility to update any forward looking statements nor should this be constituted as a guidance of future performance.

This presentation does not constitute a prospectus or offering memorandum or an offer to acquire any securities and is not intended to provideThis presentation does not constitute a prospectus or offering memorandum or an offer to acquire any securities and is not intended to providethe basis for evaluation of the securities. Neither this presentation nor any other documentation or information (or any part thereof) delivered orsupplied under or in relation to the securities shall be deemed to constitute an offer of or an invitation.

No person is authorised to give any information or to make any representation not contained in and not consistent with this presentation and, ifi d h i f ti t ti t t b li d h i b th i d b b h lf f th C fgiven or made, such information or representation must not be relied upon as having been authorised by or on behalf of the Company any of

its affiliates, advisers or representatives.

The Company’s Securities have not been and are not intended to be registered under the United States Securities Act of 1993, as amended (the“Securities Act”), or any State Securities Law and unless so registered may not be offered or sold within the United States or to, or for thebenefit of, U.S. Persons (as defined in Regulations S under the Securities Act) except pursuant to an exemption from, or in a transaction notsubject to, the registration requirements of the Securities Act and the applicable State Securities Laws.

This presentation is highly confidential, and is solely for your information and may not be copied, reproduced or distributed to any otherperson in any manner. Unauthorized copying, reproduction, or distribution of any of the presentation into the U.S. or to any “U.S. persons” (as

53

defined in Regulation S under the Securities Act) or other third parties ( including journalists) could prejudice, any potential future offering ofshares by the Company. You agree to keep the contents of this presentation and these materials confidential.

54

55

MAX INDIA LTD.Max House, Okhla, New Delhi – 110 020

Phone: +91 11 26933601-10 Fax: +91 11 26933619Website: www maxindia com

56

Website: www.maxindia.com