Embed Size (px)

Citation preview

Markets for Ecosystem Services: International

Experience

Sara J. Scherr

Forest Trends

Ecoagriculture Partners

May 2005

International Trends in Payments for Ecosystem Services: Key Messages

1) PES strategies are emerging because conservation finance is in crisis just as broader ecosystem conservation needs are identified; conservation investment must be part of the mainstream economy

2) Innovative market and ‘market-like’ mechanisms are emerging all over the world that seek to convert major “sources of threat” to sources of conservation stewardship (U.S. leads in some market developments, lags in others)

3) The rules and strategies developed over the next decade will influence patterns of conservation and investment globally over the next century; the U.S. can play a leadership role

Investing in “Natural Infrastructure’

The Forest Climate Alliance

Strategic Advice to National Policy Initiatives

Biodiversity Offsets

Carbon sequestration and storage

Soil formation and fertility

Decomposition of wastes Landscape beauty

Wilds species & habitat protection Plant pollination

Watershed protection and regulation

Air quality Pest & disease control

• Failures of traditional regulatory approaches

• Limits of protected areas and broadened ecosystem approach

• Financial markets reward short-term returns over long-term ones

• Financial value of natural area conversion is much

higher than for conservation

Motivations to Use Market-Type Instruments

• Stagnant public and civic funding forconservation

THE FOREST CLIMATE ALLIANCEWho Buys Ecosystem Services? Direct Beneficiaries

• Watershed protection– Industrial, agricultural water users – to secure stable supply, flow– Municipal water utilities, consumers (reduce costs, water quality)– Agencies managing environmental risks (e.g.,floods)

• Biodiversity conservation– Conservation agencies and organizations working on private lands– Tourist industry, for landscape beautify or protection of key species– Land developers (offsets for damage, or for amenity values)– Farmers (to protect pollinators, sources of wild products)

• Carbon emission offsets or avoided deforestation– Industries required to comply with carbon rules (offsets for emissions)– Agencies, municipalities seeking to improve air quality– Businesses providing carbon offsets

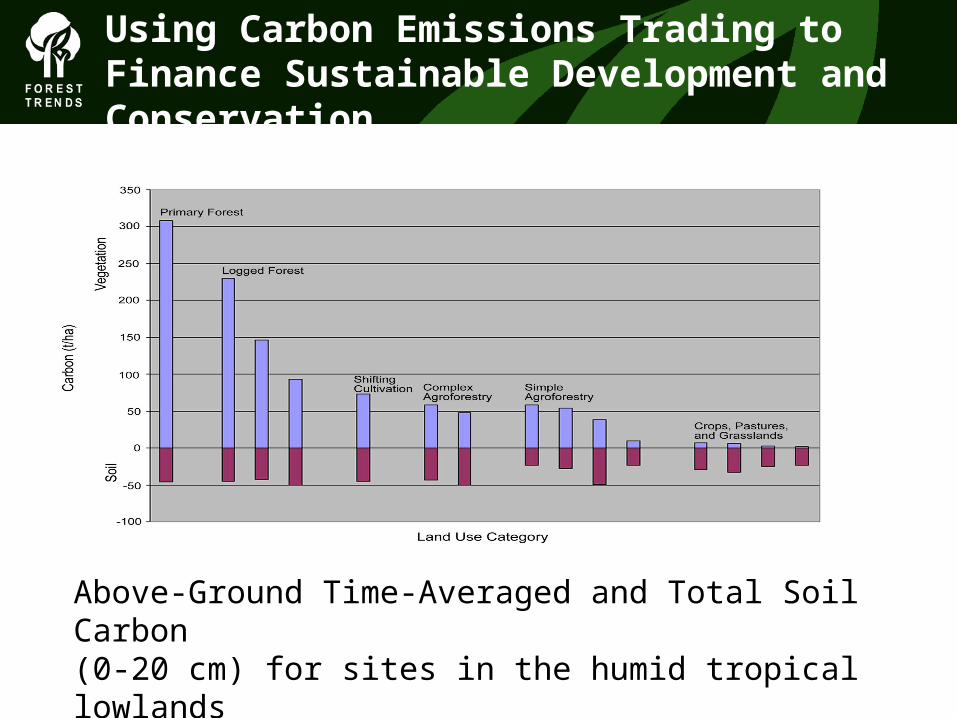

Using Carbon Emissions Trading to Finance Sustainable Development and Conservation

Above-Ground Time-Averaged and Total Soil Carbon(0-20 cm) for sites in the humid tropical lowlands of Brazil, Cameroon and Indonesia

THE FOREST CLIMATE ALLIANCEWho Buys Ecosystem Services? Indirect Beneficiaries

• Consumers: “green” values

• Companies: “green” branding

• Investors: ”green” filters

Types of Markets and Payment Schemes for Ecosystem Services

• Self-organized private deals Private entities pay for private services

• Public payments to private land and forest owners Public agency pays for service

• Open trading of environmental credits under a regulatory cap/floor Landowners either comply directly with regulations, or buy compliance credits

* Eco-label of forest, farm products Consumers prefer certified sust. supplies

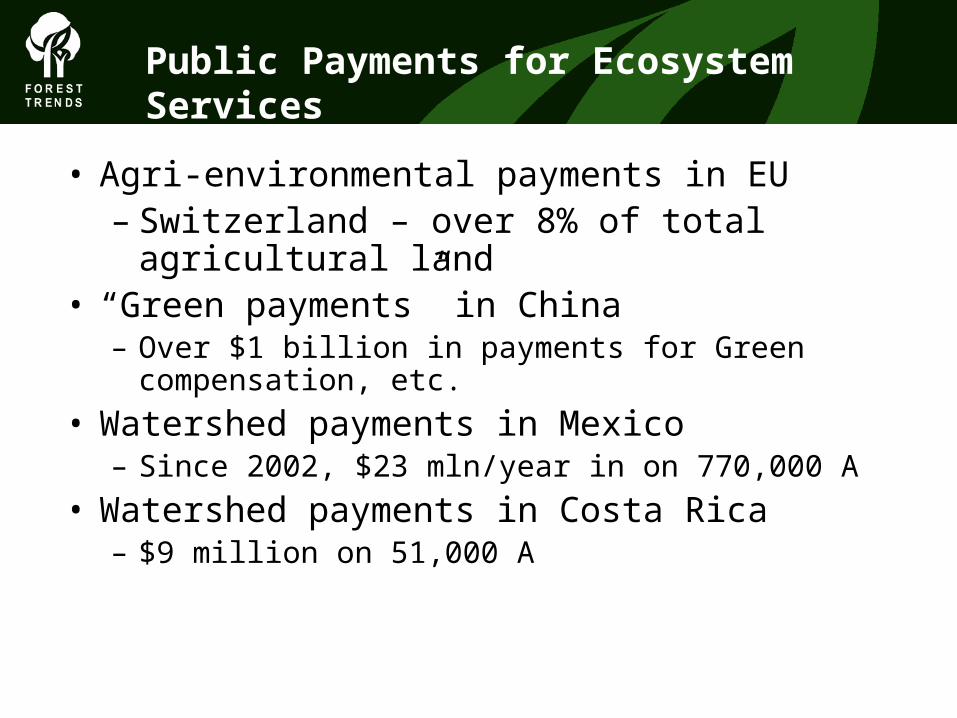

Public Payments for Ecosystem Services

• Agri-environmental payments in EU– Switzerland – over 8% of total agricultural land

• “Green payments” in China– Over $1 billion in payments for Green compensation,

etc.

• Watershed payments in Mexico– Since 2002, $23 mln/year in on 770,000 A

• Watershed payments in Costa Rica– $9 million on 51,000 A

Private Deals

• Retail carbon market – Now 0.7m t/CO2; expected to grow to 15m 2008-2012

• Payments for water quality protection– Perrier bottling plants in France

• Payments for landscape beauty/tourism value– Chile’s private Protected Area Network – 2.5 million A

• Conservation NGO payments for habitat and biodiversity conservation– Latin America - $100,000,000’s

Trading Under a Regulatory Cap or Floor

• The Kyoto-compliant carbon market – Was 1.16m t/CO2 in 2002 and is expected to grow to a

at least 15m t/CO2 in 2008-2012 ( LULUCF under $50 million)

• European Trading System– 20 million tons CO2 @ 16.7 euros/t (not yet LULUCF)

• New South Wales, Aust. GHG Abatement– Aus$11-14/tCO2e

• Tradable development rights in Brazil

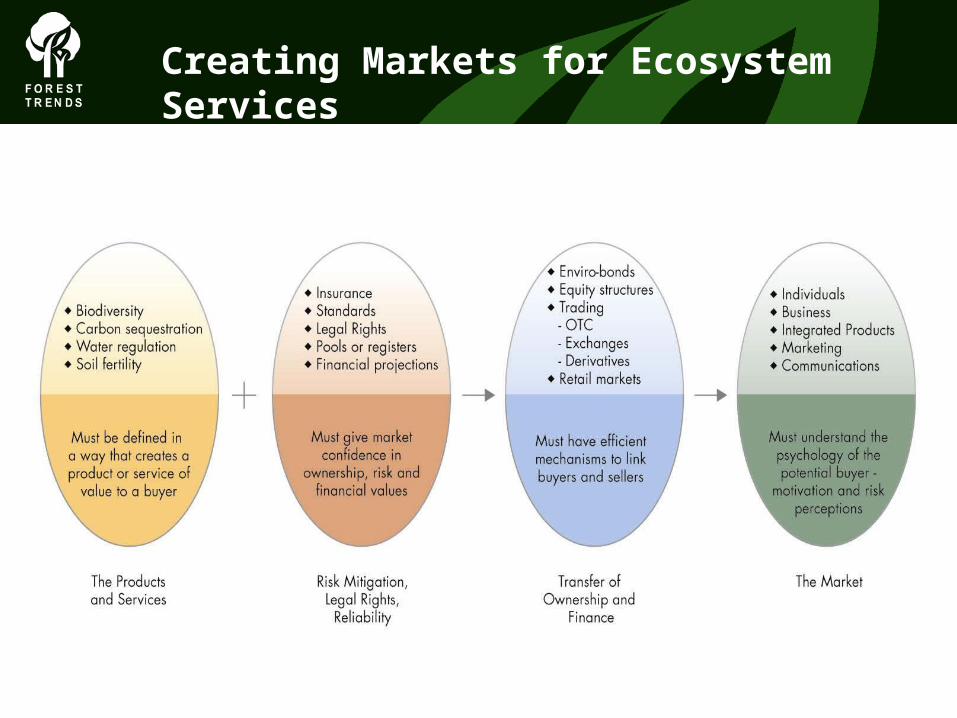

Creating Markets for Ecosystem Services

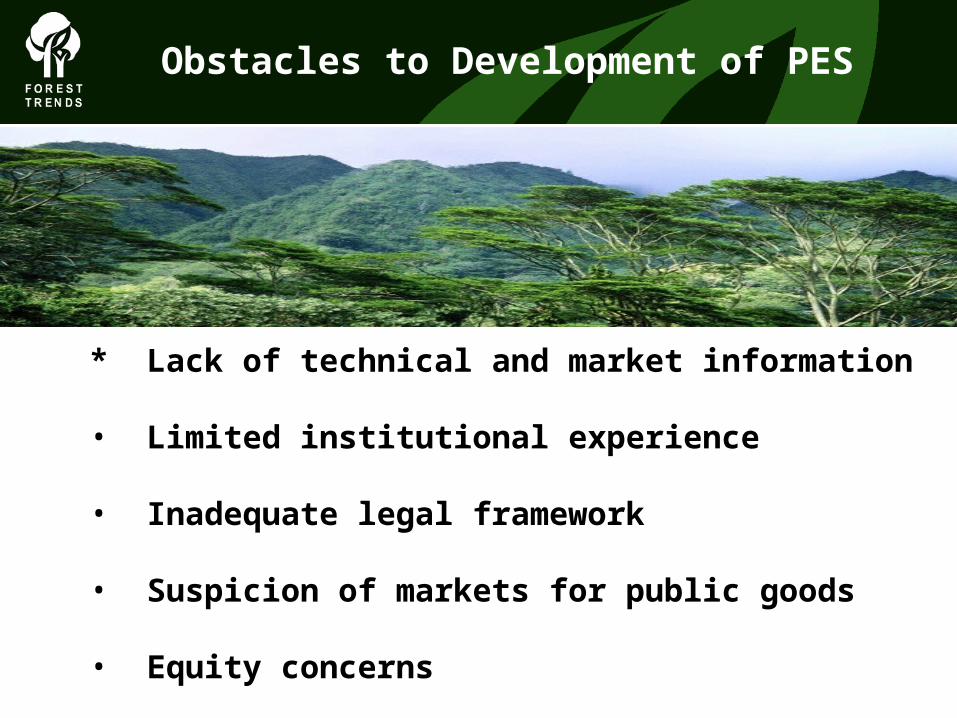

Obstacles to Development of PES

* Lack of technical and market information

• Limited institutional experience

• Inadequate legal framework

• Suspicion of markets for public goods

• Equity concerns

Priorities for Action

• Democratize information about ecosystem service markets

• Encourage broad participation in policy dialogue about the rules and shape of ecosystem service payments (local, national, international)

• Reduce learning costs for new entrants to these markets; through training programs and enterprise support

• Reduce transaction costs through institutional innovations like suitable intermediaries, ‘bundling’, large-area programs, integrate with economic activities

The Katoomba Group– Linking Global Innovators

“The Katoomba Group has become the incubator for the development of new environmental markets, providing the intellectual capital supporting the boldest new economy experiments.” – G. Daily

The Katoomba Group’s “Ecosystem Marketplace”

The first global information service to report on and track developments in new

ecosystem service-based markets for:

• Water quality and flow related to land use decisions• Carbon sequestration and storage• Conservation of biodiversity and endangered species• Other conservation-related transactions

Run a Search

Vol. 1. No.1

http://www.forest-trends.org/staff/Marketplace/Index.htm

Ecoagriculture Partners

International Learning Network: Paying/rewarding farmers and farmingcommunities for stewardship ofecosystem services

Steering Committee: Forest Trends, Winrock Int’l, IUCN, NEMA-Uganda, EcoTrust, IFAD, REBRAF, ICRAF, Katoomba Group, UNDP/GEF

• Nairobi meeting, September 2004• Uganda meeting, September 2005

(with Katomba Group)

Thank you!

www.forest-trends.orgwww.ecoagriculturepartners.orgwww.ecosystemmarketplace.com

Ecoagriculture Partners