Embed Size (px)

Citation preview

Market Report

SDN Market Sizing

Presented by:

April 2013

SDN Market Sizing Report

Copyright 2013 All Rights Reserved. April 2013

Executive Summary The impact of software-defined networking (SDN) will exceed $25B per annum by 2018, and could grow as high as $35B annually. Even conservative models show SDN-related spend exceeding 30% of total networking in that timeframe, with more aggressive models topping out at 40%. The effects on purchasing will be felt across virtually every customer segment within the networking space. Service Providers, Web 2.0 companies, and the Global 500 will lead the charge, with more than 16% of their annual networking spend being influenced by the nascent technology by 2018. Even the least impacted market segments (small and medium businesses) will contribute as much as $2.5B in annual SDN-related purchases within five years. While SDN will heavily impact existing markets, new market creation should follow a trajectory more similar to server virtualization in the mid 2000s. Driven primarily by network virtualization, the emerging datacenter controller and applications market could grow to $1B annually within six years. The rapid emergence of SDN as an influencer in network purchasing decisions will dramatically impact what has been a largely stagnant network vendor competitive landscape. New SDN use cases could open the market to new entrants for the first time in more than a decade. Combined with the trend towards converged IT organizations, SDN could enable a new type of networking decision maker that has less experience with and weaker ties to incumbent vendors.

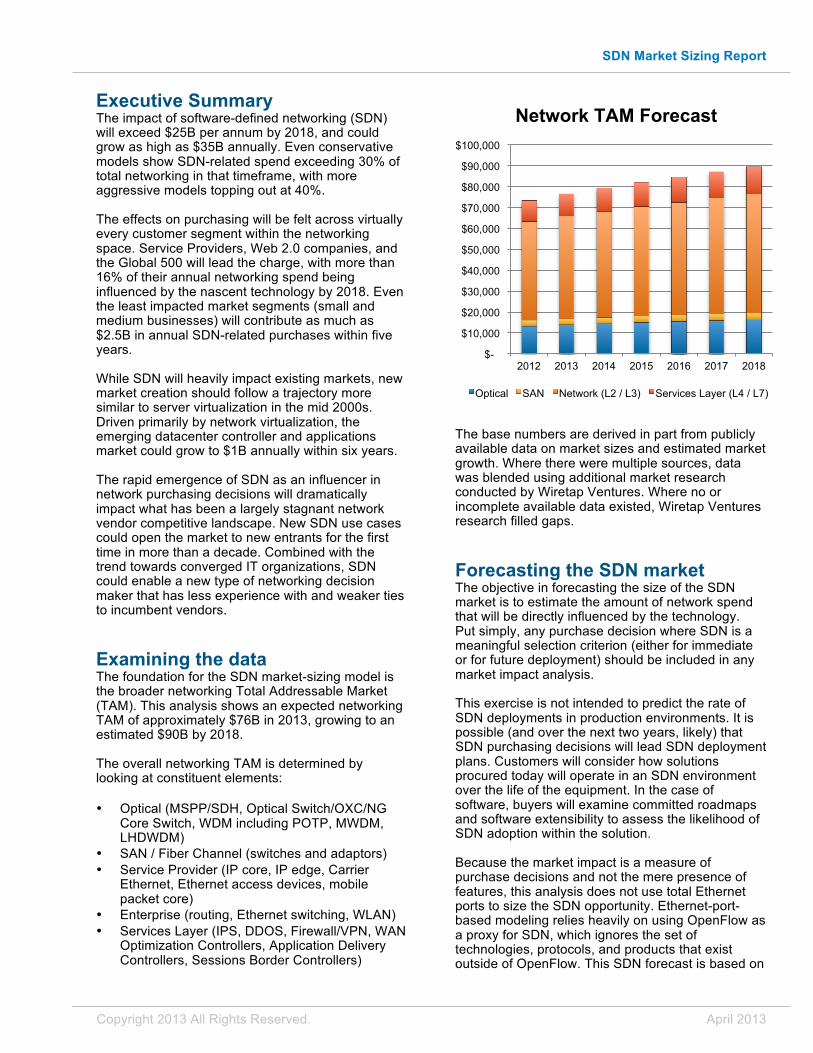

Examining the data The foundation for the SDN market-sizing model is the broader networking Total Addressable Market (TAM). This analysis shows an expected networking TAM of approximately $76B in 2013, growing to an estimated $90B by 2018. The overall networking TAM is determined by looking at constituent elements:

• Optical (MSPP/SDH, Optical Switch/OXC/NG Core Switch, WDM including POTP, MWDM, LHDWDM)

• SAN / Fiber Channel (switches and adaptors)

• Service Provider (IP core, IP edge, Carrier Ethernet, Ethernet access devices, mobile packet core)

• Enterprise (routing, Ethernet switching, WLAN)

• Services Layer (IPS, DDOS, Firewall/VPN, WAN Optimization Controllers, Application Delivery Controllers, Sessions Border Controllers)

The base numbers are derived in part from publicly available data on market sizes and estimated market growth. Where there were multiple sources, data was blended using additional market research conducted by Wiretap Ventures. Where no or incomplete available data existed, Wiretap Ventures research filled gaps.

Forecasting the SDN market The objective in forecasting the size of the SDN market is to estimate the amount of network spend that will be directly influenced by the technology. Put simply, any purchase decision where SDN is a meaningful selection criterion (either for immediate or for future deployment) should be included in any market impact analysis. This exercise is not intended to predict the rate of SDN deployments in production environments. It is possible (and over the next two years, likely) that SDN purchasing decisions will lead SDN deployment plans. Customers will consider how solutions procured today will operate in an SDN environment over the life of the equipment. In the case of software, buyers will examine committed roadmaps and software extensibility to assess the likelihood of SDN adoption within the solution. Because the market impact is a measure of purchase decisions and not the mere presence of features, this analysis does not use total Ethernet ports to size the SDN opportunity. Ethernet-port-based modeling relies heavily on using OpenFlow as a proxy for SDN, which ignores the set of technologies, protocols, and products that exist outside of OpenFlow. This SDN forecast is based on

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

2012 2013 2014 2015 2016 2017 2018

Network TAM Forecast

Optical SAN Network (L2 / L3) Services Layer (L4 / L7)

SDN Market Sizing Report

Copyright 2013 All Rights Reserved. April 2013

product architectures that are shifting to central control and use programmatic APIs for flow-based control for vendor and 3

rd-party applications.

Beginning with assumptions This SDN market forecast is predicated on three foundational assumptions:

• SDN-related spend is largely substitutive to existing network spend.

• Different product types will be impacted by SDN in different ways.

• Uptake of SDN use cases dictates how much and when spend shifts from traditional to SDN solutions.

It is unlikely that SDN will increase network spend on its own; network spend tends to be tightly correlated with IT spend, which, at a macro level, is more closely tied to GDP than individual technologies. This means that any SDN spend must come at the expense of either non-SDN equipment spend or by swapping operational savings for additional equipment purchase. SDN impact cannot be modeled as a flat percentage that is applied equally to all product types in all market segments. Some products and markets will lend themselves to SDN use cases more than others, and some buyers will be more or less predisposed to adopting new technologies. Ultimately, the specific SDN use cases will dictate when markets move towards SDN, and to what extent they make the transition. Those use cases that have the most potential will drive technology development, which will determine where SDN spend is focused.

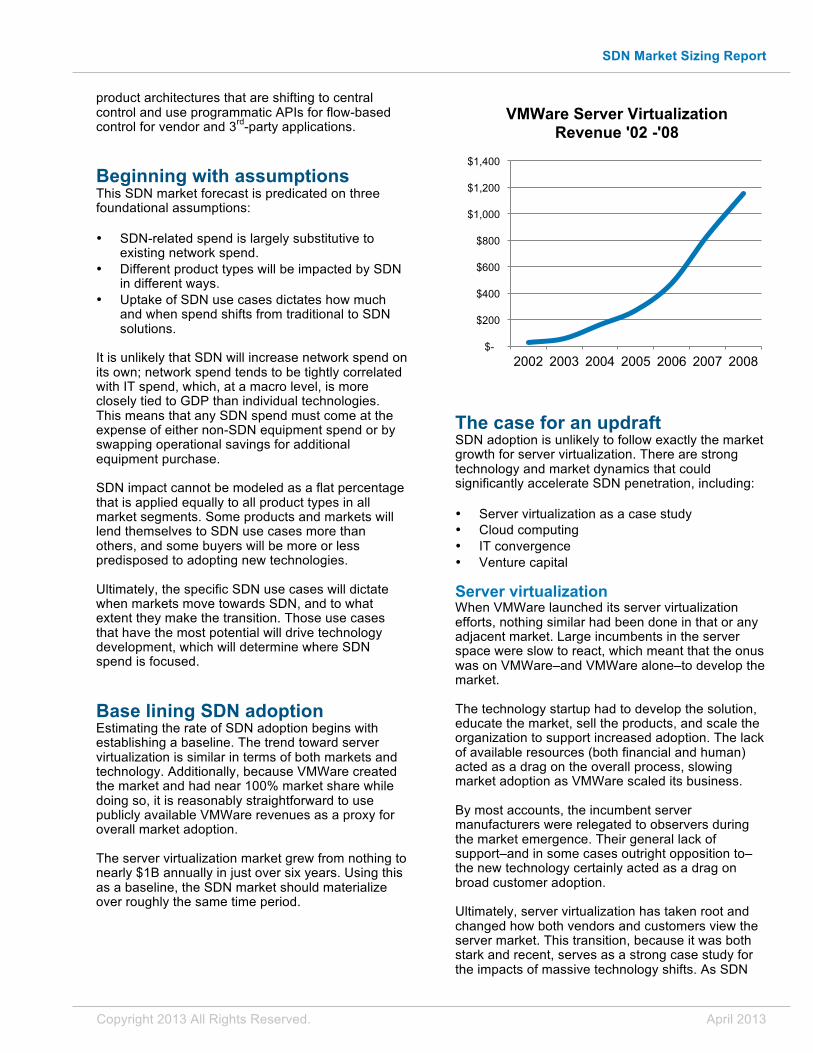

Base lining SDN adoption Estimating the rate of SDN adoption begins with establishing a baseline. The trend toward server virtualization is similar in terms of both markets and technology. Additionally, because VMWare created the market and had near 100% market share while doing so, it is reasonably straightforward to use publicly available VMWare revenues as a proxy for overall market adoption. The server virtualization market grew from nothing to nearly $1B annually in just over six years. Using this as a baseline, the SDN market should materialize over roughly the same time period.

The case for an updraft SDN adoption is unlikely to follow exactly the market growth for server virtualization. There are strong technology and market dynamics that could significantly accelerate SDN penetration, including:

• Server virtualization as a case study

• Cloud computing

• IT convergence

• Venture capital

Server virtualization When VMWare launched its server virtualization efforts, nothing similar had been done in that or any adjacent market. Large incumbents in the server space were slow to react, which meant that the onus was on VMWare–and VMWare alone–to develop the market. The technology startup had to develop the solution, educate the market, sell the products, and scale the organization to support increased adoption. The lack of available resources (both financial and human) acted as a drag on the overall process, slowing market adoption as VMWare scaled its business. By most accounts, the incumbent server manufacturers were relegated to observers during the market emergence. Their general lack of support–and in some cases outright opposition to–the new technology certainly acted as a drag on broad customer adoption. Ultimately, server virtualization has taken root and changed how both vendors and customers view the server market. This transition, because it was both stark and recent, serves as a strong case study for the impacts of massive technology shifts. As SDN

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

2002 2003 2004 2005 2006 2007 2008

VMWare Server Virtualization Revenue '02 -'08

SDN Market Sizing Report

Copyright 2013 All Rights Reserved. April 2013

follows a similar trajectory, it seems unlikely that the major networking incumbents will be similarly complacent, and in fact every major vendor has announced plans to support SDN. Broad incumbent support could accelerate the maturation of the SDN market.

Cloud computing The trend towards cloud computing has been ever present for the past several years. Much of the value in this movement is in orchestrating workloads across both public and private resource pools. This creates an untethering of applications and underlying infrastructure that requires a level of dynamism that simply does not exist in networks today. As cloud initiatives continue to grow, there will be increased pressure on networking to provide a more flexible transport that can adjust in real-time to the needs of users and applications. This should provide ample use cases for SDN technologies, and help accelerate customer demand for SDN.

IT convergence Increasingly, IT silos are being broken down, and infrastructure is being consolidated into a smaller number of organizations. This is part of broad efforts to manage infrastructure more holistically, removing hard organizational edges between teams that ultimately rely on each other. A major part of the SDN draw is the ability to orchestrate the network centrally and offer programmatic interfaces with which applications can provide inputs into the underlying network. This bridging of the network-application divide could be particularly attractive to organizations looking to remove boundaries and rally around the applications that ultimately drive the business.

Venture capital The rise of server virtualization was notable for the lack of companies that emerged during a disruptive technology phase. More typically, the opportunity to disrupt incumbents in sizable markets attracts new entrants. These startups identify new pain points, pursue new ideas, sell into new niche markets, and generally accelerate the move away from legacy solutions. If VC funding is any indication, the SDN arena appears to be more typical than server virtualization.

VC funding in SDN-focused companies has increased from less than $10M in 2009 to nearly $500M in 2013. The astonishing 50X increase in VC funding should accelerate the growth of the SDN market.

The case for a downdraft There are likely to be three primary drags on the emergence of SDN:

• Complexity

• Skill sets

• Incumbent behavior

Complexity Where server virtualization was confined to a single element in the broader IT stack (compute), SDN is much more pervasive. The very nature of the network is to act as connective tissue between compute, storage, and services. Accordingly, the reach of SDN is significantly greater. With greater reach comes greater complexity. The number of devices, protocols, and technologies with which SDN solutions must be compatible certainly increases the technological challenges of migrating, for both vendors and customers.

0

100

200

300

400

500

600

Mar-

07

Jul-07

Nov-0

7

Mar-

08

Jul-08

Nov-0

8

Mar-

09

Jul-09

Nov-0

9

Mar-

10

Jul-10

Nov-1

0

Mar-

11

Jul-11

Nov-1

1

Mar-

12

Jul-12

Nov-1

2

Mar-

13

SDN Funding ($M) Mar '07 - Mar '13

SDN Market Sizing Report

Copyright 2013 All Rights Reserved. April 2013

Finally, because networks act as central resources between pools of IT infrastructure, they are subject to stricter uptime requirements than servers. If a virtual machine or even an entire server fails, some number of applications might be less performant or unavailable. If the network fails, many racks of servers and storage can be taken offline. The potential impact is orders of magnitude greater. The higher risk could slow down SDN adoption. It is worth noting that risk is more likely to slow down SDN deployment than SDN emerging as an actual purchase criterion. As a means of ensuring investment protection, customers will likely demand SDN support even if they are months or years from deploying it in production.

Skill sets Today’s networks are designed and managed by a large number of certified network engineers operating on command-line interfaces. However, part of the SDN lure is the promise of programmatic interfaces that allow for more application-driven behavior. The drive toward automated, highly programmable behavior represents a significant shift in skill sets away from the highly specialized network engineer. As companies move to a more programming-savvy workforce (often called DevOps), there will be a requirement to either train existing employees, or replace some network engineers with software developers. Retooling the workforce could slow SDN penetration.

Incumbent behavior Ultimately, disruption favors those with lower market share as it serves to level the playing field for all. Strategically, this means that companies in a dominant incumbent position are less likely to fully embrace disruptive technologies, preferring instead to either slow progress or steer development in a favorable direction. As SDN is still in its early stages, it is difficult to know how the networking incumbents will shape the technology landscape. While it is true that every major networking vendor has publicly embraced SDN, it is difficult to know how those plans will manifest themselves in actual product. Additionally, some vendors will market more traditional networking solutions as SDN solutions, which could serve to confuse the marketplace and stall momentum.

Quantifying the SDN impact Assuming that SDN is largely substitutive to existing networking spend, the general networking TAM provides the overall market from which SDN will pull. And the server virtualization market provides a timeframe in which the SDN market is likely to emerge.

The model shows potential SDN revenues growing from less than $200M in 2012 to more than $35B by 2018. This growth is driven primarily by the network (L2/3) and service layer (L4/7) categories. The L2/3 contribution will exceed $3.5B by 2015 and grow to more than $21B by 2018, while the services layer will add roughly $2.3B in 2015 and more than $10B by 2018.

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

2012 2013 2014 2015 2016 2017 2018

'12 - '18 Market Forecast by Product Category

Services Layer (L4 / L7) Network (L2 / L3)

Optical SAN

SDN Market Sizing Report

Copyright 2013 All Rights Reserved. April 2013

Mapping impact to customer segments To map the product categories to actual markets, consider the following customer segments and sub segments:

• Enterprise

• Global 500

• Very Large (>10000 employees)

• Large (>1000 employees)

• Medium (>100 employees)

• Small (<100 employees)

• Public Sector

• Service Providers

• SP Carrier (major telcos)

• SP Cloud (cloud providers)

• Cloud and SAAS

• Massive Datacenter (Google, Facebook, etc.)

• Web 2.0 (ecommerce, content, social, etc.)

• SP Managed Services The impact of SDN in these customer segments will not uniformly felt. The service provider, Web 2.0, and Global 500 companies will lead growth.

Annual SDN purchases led by the Global 500 will grow from $20M in 2012 to more than $6B by 2018. In the same timeframe, service provider and Web 2.0 spend will increase to a combined $11B annually. Even the smallest market segments will see a sizable increase in SDN spend by the year 2018. The small and medium business segments, accounting for less than $20M in SDN spend in 2013, will contribute close to $2.5B annually–a remarkable 125X increase over six years.

Translating customers to use cases The overall SDN spend can be translated from customer segments to specific use cases. The SDN use cases are aggregated into the following categories and subcategories:

• Enterprise Access

• Enterprise Datacenter

• Enterprise Datacenter (private cloud)

• Enterprise Datacenter (regulated)

• Cloud Service Provider Datacenter

• Hyper-scale Datacenter

• Web 2.0 Datacenter

• Service Provider

• WAN Edge

• Mobile Backhaul

• Metro Aggregation

• Wired Edge (REN)

• Mobile Packet Core

• Wired Core By studying known SDN trials and deployments, and by engaging with SDN customers, the spend by customer segment can be modeled into a more use-case-specific distribution.

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

2012 2013 2014 2015 2016 2017 2018

SDN Spend by Customer Segment

Enterprise Public Sector

Service Provider Cloud & SAAS

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

2012 2013 2014 2015 2016 2017 2018

SDN Spend by Use Case

Service Provider Cloud Service Provider DC:

Enterprise DC Enterprise Access

SDN Market Sizing Report

Copyright 2013 All Rights Reserved. April 2013

The use case model reflects fairly broad SDN applicability. Of the 12 use case categories, 7 of them will contribute more than $3.5B annually by 2018, with the four datacenter categories (Hyper-scale, Web 2.0, private cloud, and regulated) contributing a combined $19.3B. The SDN impact in the Mobile Packet Core, Wired Core, and Wired Edge is significantly lower, with less than $400M in combined annual purchases by 2015.

Emerging datacenter controller and applications market In addition to the traditionally tightly coupled hardware/software networking solutions, there will be an emergence of controllers and orchestration applications in the datacenter.

As a baseline, consider again the rise of the server virtualization market. If the controller and applications market emerges over the next six years, it could contribute as little as $1B annually, or as much as $2.4B annually with a more aggressive model. The emergence of a datacenter controller and applications market will be slowed somewhat by a dependence on the underlying hardware. Before controllers and orchestration applications can be deployed en masse, the underlying network must be SDN-capable. So while SDN should shape hardware decisions in the short term, until those decisions translate to deployed SDN architectures, the market for controllers and applications will remain small.

The notable exception to this is network overlays (including technologies like VXLAN). These technologies do not have a direct dependence on the underlying hardware, which means this part of the market will not experience the same drag.

The qualitative impacts of SDN The quantitative impacts of SDN are substantial, but the qualitative aspects of this market transition could be even more important. SDN marks the first time since the Internet Boom of the late 1990s that there has been a significant inflection point in both networking technologies and overall business landscape. The result should shape how IT evolves for the next 20 years. While SDN’s impacts will be felt across the entire industry, the datacenter will make up more than half of the SDN market by 2018. New technology, new venture capital, and new players in the datacenter could disrupt what has been a virtual monopoly for the past 20 years. This will change how the major incumbents have to compete, and it could spur a massive consolidation of companies–both new entrants and established entities. Additionally, SDN appears to be just one of several infrastructure movements towards a more software-based, tightly-integrated, highly-automated IT ecosystem. The rise of programmatic interfaces and infrastructure orchestration will require a new level of system integration–one that extends well beyond individual silos and demands deeper reach into support systems and processes. This will require a change in skill sets, which is helping to drive the DevOps movement. If the underlying workforce changes, vendors will no longer be able to rely on their certified engineering base as a source of competitive advantage, which could disrupt the competitive landscape still more. Finally, given the number of systems that must integrate and the sheer complexity of the interactions between them, DevOps is unlikely to be sufficient for many IT organizations. There will be an increased need for professional services to handle these integrations. If professional services do emerge as a competitive weapon, this will change even more how major IT vendors compete, opening the door for those who have strong systems integration practices.

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

2012 2013 2014 2015 2016 2017 2018

SDN Controller + Apps Forecast '12 - '18

SDN Market Sizing Report

Copyright 2013 All Rights Reserved. April 2013

Regardless of the specific technology and strategic directions that the industry collectively pursues, the impacts of SDN will be profound on both the competitive landscape and the bottom line.

Conclusion The movement towards software-defined networks is the kind of change that happens once in a generation. But to think that the impact is primarily a technological shift would hugely underestimate the transformational impact that this will have on not only the networking space but also the entire IT infrastructure landscape. At a minimum, the introduction of a disruptive way to build networks will lessen the value of more than two decades of incumbency. With a level playing field, markets that have been impenetrable to new entrants will be opened. For the first time in 20 years, market share in some of the most lucrative, high-margin businesses will be up for grabs. The impact could be double-digit share movement as vendors compete. Exactly how crowded is the space? SDNCentral, the leading content and corporate directory site in the SDN arena, has approximately 225 companies registered. Now consider that this number was near 0 in 2009. The race towards SDN (whether a marketing or a product race) is on.

With so much at stake, start-ups are being funded at an incredible rate. These new entrants bring with them not just new ideas but also new ways of thinking. New ideas are the lifeblood of innovation, and SDN is fueling those. The resulting change will extend well beyond the products, potentially lifting the entire space from slow-moving incrementalism to rapid evolution that is more typical of adjacent technology markets. As the large players try to adjust to a swifter competitive environment, there will undoubtedly be a round of industry consolidation. Some companies will fail, others will break through, and still others will be acquired. These acquisitions will be driven by the larger players, which can potentially fracture partnerships, as friends become foes. VMWare and EMC fired the first shot when they acquired Nicira, which put them on a collision course with long-time partner Cisco. Further consolidation could see peripheral players like Oracle and IBM enter the fray. With this sea change brewing, 2013 should be the breakout year for SDN. Venture capital will continue to flow into new companies. Start-ups will continue to emerge from stealth mode. Existing players will continue to announce SDN products and production deployments. The industry will continue its acquisition spree. But ultimately, the measure of SDN progress will be the amount of revenue that is directly attributed to SDN as a primary selection criterion.

Acedemic, 35

Private Technology

Company, 90

Public Technology

Company, 65

Customer, 35

Organizations Associating with SDN