Embed Size (px)

Citation preview

MARKET REPORT GERMANY 2019

Political and economic environmentPAGE 4

Office marketPAGE 6

Retail marketPAGE 8

Hotel marketPAGE 10

Logistics marketPAGE 12

Residential marketPAGE 14

Investment marketPAGE 16

Disclaimer PAGE 18

CONTENTS

3This market report has been compiled by the experts of KENSTONE Real Estate

Valuers (KENSTONE). The basis of the report is provided by data from valuations

evaluated centrally and publicly accessible information. KENSTONE was in charge

of putting together the evidence from these sources, evaluating it and presenting

the results of its analysis in the market report. It gives the reader a general

overview of the situation in the office, retail, hotel, logistics, investment and

residential markets in Germany. It focuses on eight German cities: Berlin (B),

Dusseldorf (D), Frankfurt (F), Hamburg (HH), Cologne (C), Leipzig (L), Munich (M)

and Stuttgart (S).

4 The year 2018 brought with it a phase of weaker economic growth. The growth rate at

1.4 % remained on the one hand extremely solid but fell, on the other hand, to its lowest

level since 2013. The trade conflict between the United States and China is an increasing

burden for the world economy including German industry which is heavily reliant upon

export. In addition there are problems with the automotive industry in terms of the new

emissions assessment procedure (WLTP) and the Brexit issue which is not concluded.

The main pillar of support for the economy is consumption, the construction sector and

also, to date, the service sector which is initially good news for the commercial property

markets. On the other hand industry has slipped into recession which, if one looks at weak

order books, should continue to prevail for the moment.

The ECB is steadfastly continuing with its policy of cheap money. The low interest environ-

ment with, in part, negative rates should therefore continue or, as a reaction of the ECB to

the weaker economic environment, become even more acute. At the same time inflation in

Germany should continue to be at approximately 1.5 % and below 2 % which is not really

helpful if one is looking for positive returns in real terms.

The labour market continues to be in very good shape. Unemployment is at a very low level.

However a slight increase in the seasonally adjusted unemployment rate in May 2019 was

recorded which shows that the labour market is not immune to an economic downturn.

On the other hand economic growth anticipated for 2019 and also 2020 should suffice to

provide the labour market with a continuing positive impetus. The number of people em-

ployed in jobs subject to social security charges jumps from one record to the next.

Following the state of the labour market wage growth also increased in tempo in 2018.

Wages and salaries grew, at approximately 4.7 %, more strongly than they did for at least

10 years which is a good sign, at least for consumption.

The Ifo-Index has been deteriorating significantly since the middle of last year and re-

cently fell to below 100. As of mid-2019 a change in the trend is not recognisable which

would indicate a moderate economy for the rest of the year. The growth forecasts at 0.4 %

for 2019 are accordingly very moderate and also for 2020 growth rate at approximately

1.3 % would on the one hand be sound but on the other hand would be below the level of

previous years.

The economic downturn will impact sooner or later on the German property market. How

severe this will be depends however on how long the phase of weakness lasts. Assuming

that the economy gradually finds its way out of the trough then the property market will

probably only experience a slight impact. On the other hand the economy will in the long

term lose steam not least due to falling competitiveness in the Eurozone. One can assume

therefore that the German property market, the commercial property market and also the

residential market will not be as lively as was the case in previous years.

Economic dynamism weaker

Consumption remains

fundamental growth driver

Interest rates and inflation stable

Labour market very strong

despite small hiccup

Early indicators rather weak

Wage growth gaining speed

Noticeable economic downturn –

preceding moderate growth

POLITICAL AND ECONOMIC ENVIRONMENT

3.000

5.000

7.000

9.000

11.000

13.000

15.000

Jun

11

Jun

13

Jun

15

Jun

17

Jun

19

Index

-1

0

1

2

3

4

Jun

11

Jun

13

Jun

15

Jun

17

Jun

19

%

90

95

100

105

110

Jun

11

Jun

13

Jun

15

Jun

17

Jun

19

Index

-2

0

2

4

11 Q

2

13 Q

2

15 Q

2

17 Q

2

19 Q

2

%

4

5

6

7

8

Jun

11

Jun

13

Jun

15

Jun

17

Jun

19

%

5GDP Annual growth rate (real)

%

IFO BUSINESS CLIMATE INDEX

Index

DAX

Index

UNEMPOYMENT RATE

%

INFLATION

%

FORECASTS

Sources: Kenstone, German Federal Statistics Office

Sources: Kenstone, Ifo

Sources: Kenstone, Deutsche Bundesbank, Deutsche Börse AG

Sources: Kenstone, German Federal Statistics Office

Sources: Kenstone, German Federal Statistics Office

Source: Commerzbank

Annual Change 2018 2019 2020

GDP % 1.4 0.4 1.3

Consumer Spending % 1.1 1.6 1.3

Inflation % 1.8 1.4 1.7

Absolute

Unemployment Rate % 5.2 4.9 4.7

Jun-

11

Jun-

13

Jun-

15

Jun-

17

Jun-

19

Jun-

11

Jun-

13

Jun-

15

Jun-

17

Jun-

19

Jun-

11

Jun-

13

Jun-

15

Jun-

17

Jun-

19

Jun-

11

Jun-

13

Jun-

15

Jun-

17

Jun-

19

The mood in the German office markets is still good. Irrespective of the economic weaken-

ing phase the service sector is still expanding and this promotes the demand for space.

In 2018 take-up for office space in the markets considered here missed the result of the

previous year by approximately 10 % – at approximately 4,000,000 m². In terms of long-

term comparisons it is still operating at a very high level. Ultimately take-up declined in

all markets albeit in a rather moderate manner. The first half-year 2019 recorded however

a rise in comparison to the previous year which underlines a stable market situation at a

high level.

With the backdrop of ongoing lively demand, the vacancy rate in the past 12 months has

fallen again and reached a weighted level of approximately 3.4 % which equates to a new

record in this century. In this regard the range is between 6.3 % in Dusseldorf down to

1.8 % in Berlin. If one defines full rental as a market with a vacancy rate of below 3 % then

four of the eight markets (Berlin, Cologne, Munich, Stuttgart) are fully rented.

Given the background of sound demand and low vacancy rates it is not surprising that

rents have risen further and that the speed of the rise has even accelerated. Berlin is still

in first place, unchallenged, as the number one followed now by Cologne and Hamburg.

Alongside Frankfurt, Munich traditionally records the highest rent and it has now

achieved the level of € 40 per square metre. Rental growth is not limited to prime sector

but is also to be ascertained across the board.

The recognisable increase in construction activity dating back to the end of last year has

continued in the past 12 months. In this regard Berlin, Munich and Frankfurt have shown

very lively developments in the long term and this is hardly noticeable in other markets.

In absolute terms, in relation to take-up, the former markets are showing values which

are above average. The proportion of space under construction is there between 5 % and

6.5 % of the existing stock. Thereof between 48 % and 57 % is already pre-let, which is

below average when compared to the other markets.

One cannot fail to recognise however that the lively development is accompanied by the

withdrawal of existing space with the consequence that in some markets total stock of

office space has hardly changed or, as in Frankfurt, is still negative.

If one assumes that, based on economic growth forecasts, the current economic weaken-

ing is limited in nature and that, at the latest, next year the direction of lower level but still

solid growth is achieved, then the effects of the economic weakening should remain lim-

ited and the outlook for the German office markets should remain fundamentally positive.

For the locations Berlin, Munich and Frankfurt on the one hand a considerable increase in

space available is to be anticipated and this requires for absorption solid demand and eco-

nomic support. However this space relates to markets which are currently characterised

by low levels of available supply and therefore from this one cannot ascertain a change

in the trend. What is critical for the further development is ultimately economic growth

which is currently affected by a number of uncertainties.

Upward trend on office

markets in tact

Lively take-up

Vacancy rates falling for the

8th year in succession

Rental increase accelerating

Building activity in part

at very high level

Outlook for office market remains

positive, with, however, uncertainties

OFFICE MARKET

6

2

4

6

8

10

12

0

1

2

3

4

5

11 12 13 14 15 16 17 18 19

%Mio. m²

B C D F HH L M S

Stock m m² 20.3 7.9 9.2 11.6 15.0 3.8 20.5 8.8

Take Up 1,000 m² 419 147 252 281 310 55 418 143

Vacancy 1,000 m² 372 206 573 701 505 211 494 188

Vacancy Rate % 1.8 2.6 6.3 6.1 3.4 5.6 2.4 2.1

Under construction 1,000 m² 1,047 194 222 622 338 84 1,288 n/a

Prime Rent € / m² 35.50 24.50 28.00 40.50 29.00 14.50 40.00 23.50

7OFFICE MARKET CONDITIONS and 12-months trend

TAKE UP / VACANCY RATE

m m² %

MARKET DATA MID-YEAR 2019

PRIME RENTS

€ / m²

Source: Kenstone

Sources: Kenstone, agents

Sources: Kenstone, agents

Sources: Kenstone, agents

To the advantage of Landlords

Tenants

Ber

lin –

Col

ogn

e –

Du

ssel

dor

f –

Fra

nkf

urt

–

Ham

bu

rg –

Lei

pzi

g –

Mu

nic

h –

Stu

ttg

art

–

12-months trend

Take Up, aggregated (ls) Vacancy Rate, weighted (rs)

2018 Mid-year 2019

Mid

-yea

r

10

15

20

25

30

35

40

45

B C D F HH L M S

€/m²

Data from the National office for statistics show that the turnover of German retail is

positive and also for stationary retail. The labour market is still in top shape, incomes are

rising clearly. Therefore the fundamental drivers for an expansion of retail remain intact

and give retail turnover the impetus it requires.

However clouds are increasingly gathering. The consumer confidence index is at a high

level with a slightly negative trend. The background to this is on the one hand a high

propensity to consume on the part of consumers and on the other hand a weakening as-

sessment of future income. After the labour market in the past only knew one direction

and words such as short time work or jobs cut almost disappeared in language, these have

now returned and are dampening the expectations of consumers.

In this environment retail turnover in 2018 in real terms grew more weakly than in the

previous year at approximately 1.7 %. The year 2019 started with comparable growth

rates too. What remained was also a difference in the development of the various retail

sectors. There are both winners and losers. As in previous years online business were

among the winners. Turnover there increased significantly at approximately 6.3 % even

if this is lower than in previous years.

Furthermore stationary, large-scale food retail and drugstores were among the formats

with an expansive development. The large market leading chains are investing in very

competitive conditions in new, efficient, high value space which provides for the demand-

ing customer an attractive local shopping experience. Therefore they contribute signifi-

cantly to the overall low level of growth in retail space.

Shopping centres, following years of growth, are now among the formats which are notic-

ing a difference in consumer behaviour and therefore face increasing pressure to adapt.

This is with the background that the classical centre concepts with a limited number of

anchor tenants and many smaller shops with a high proportion of textile providers are no

longer in such demand as in the past. The number of potential anchor tenants is declining

and space required of individual providers are falling given the pressure of online busi-

ness and fluctuation is increasing in the face of increasingly quicker product and fashion

cycles. The consequence is that the rental structure is under pressure although between

individual centres and formats at different locations and market positions there are sig-

nificant differences.

The classical business locations are developing dependent on the local retail structure in

very different manners. Attractive, competitive business locations are still enjoying the

corresponding level of attractiveness but the change in local providers is always apparent.

It is not infrequent that this is to the detriment of the classical owner managed business

model and also department stores whose number following the merger of Karstadt and

Kaufhof will probably decline.

In line with the differing market influences retail rents in traditional commercial locations

are showing a stable to slightly declining trend.

The trends recognisable in the past few years will probably continue in the near future

and economic weakness may accelerate the change process.

Ongoing positive

conditions for retail …

… with downsides however

Dynamism subsiding in retail

Food sector expanding

Different trends in traditional

commercial locations

Shopping centres under

pressure to adapt

Rents stable at best

Pressure to change will

remain high in retail

RETAIL MARKET

8

95

100

105

110

115

120

Jun

11

Jun

12

Jun

13

Jun

14

Jun

15

Jun

16

Jun

17

Jun

18

Jun

19

Index

0

5

10

15

Jun

11

Jun

12

Jun

13

Jun

14

Jun

15

Jun

16

Jun

17

Jun

18

Jun

19

Index

90

100

110

120

130

08 09 10 11 12 13 14 15 16 17 18

Index

9

RETAIL / SHOPPING CENTRE SPACE

Index

MARKET DATA

PRIME RENTS

€ / m²

100

150

200

250

300

350

400

B C D F HH L M S

€/m²

Sources: Kenstone, EHI, HDE

Sources: Kenstone, agents, Statistical Offices

Sources: Kenstone, JLL

Retail Shopping Centres Mid-year 2018 Mid-year 2019

RETAIL SALES Real

Index

CONSUMER SENTIMENT

Index

Sources: Kenstone, Federal Statistical Office Sources: Kenstone, GfK

B C D F HH L M S

Population 1,000 3,748 1,090 642 748 1,841 588 1,542 621

Population (2018 versus 2013) % 6.5 4.4 4.7 7.9 5.4 10.6 6.0 5.5

Prime Rent Mid-year 2019 € / m² 330 260 290 310 280 120 360 270

Jun-

11

Jun-

12

Jun-

13

Jun-

14

Jun-

15

Jun-

16

Jun-

17

Jun-

18

Jun-

19

Jun-

11

Jun-

12

Jun-

13

Jun-

14

Jun-

15

Jun-

16

Jun-

17

Jun-

18

Jun-

19

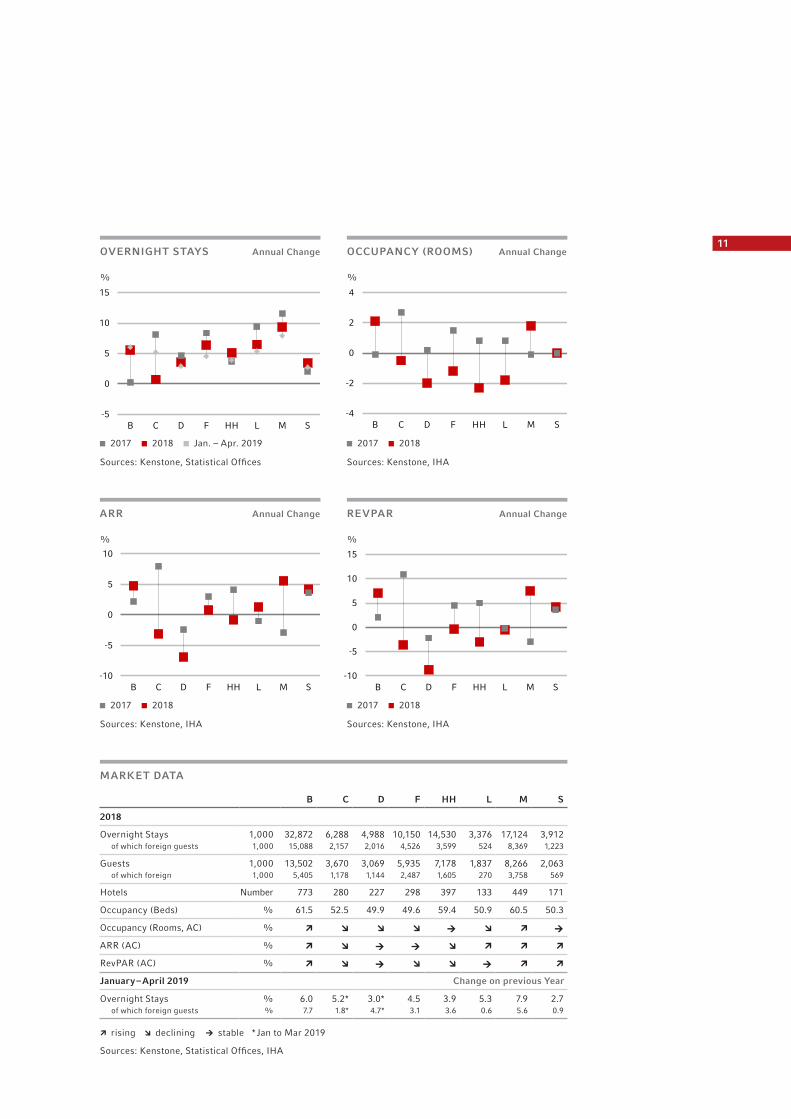

The German accommodation market is still in a growth phase. In comparison to the

previous year the number of overnight stays in 2018 increased by 4 % thus achieving the

highest level of growth since the year 2000. Guests from Germany (+3.9 %) and also from

abroad (+4.5 %) contributed to this good result.

The driver of this development was an overall positive economic environment with

increasing interest in short trips and, particularly in the year 2018, a long summer which

benefited holiday hotels.

City tourism as already in previous years contributed disproportionately to the market

development which is positive. Approximately 4.9 % additional overnight stays were

recorded in German cities, here in particular tourism hotspots such as Berlin, Hamburg

and Munich where growth at over 5 % was even higher and achieved in Munich 9 %, an

almost double digit growth rate.

The long and hot summer in 2018 benefited some regions with exceptional growth rates.

A not inconsiderable number of people seeking relaxation switched the south for the

north such that German sea resorts benefited with overnight stays growth of an extra-

ordinary 9.9 %.

Following the excellent development on the demand side, now the supply side develop-

ment is also gaining steam. The number of opportunities available for overnight stays

increased by approximately 1.9 % in classical hotels, the highest growth rate since the

mid-90s, if one disregards the year 2008. The trend towards large-scale hotels continues

unbroken. Irrespective of the growing numbers of beds, in 2018 the number of accom-

modations open fell again for the second time in succession at a rate of below 1 %. If one

looks at the number of hotel projects being planned then there are many indications that

the speed of growth on the supply side will even increase.

Capacity figures and also room prices in the hotel sector recorded, thanks to demand in

2018 growing rapidly, an overall positive trend. Room prices increased Germany wide

by 2.2 % and capacity numbers increased by 0.5 % to 71.9 % thus achieving a new

record. Since the last low point in 2009 (59.8 %) occupancy figures have increased by

approximately 12 %. As a result revenues per available room have continued their positive

upward trend.

For the cities considered there is however a rather more mixed picture. Based on demand

and the development of supply four cities have negative capacity numbers and two cities

recorded falling room prices.

One cannot fail to recognise in this regard however that irrespective of the long years

of growth in demand the competition situation in the hotel sector is extremely intensive

and the sector is confronted with a wide range of challenges. Lack of staff with increases

in costs, increasing regulation and changes in the context of the digitalisation of the

economy (sharing economy) are forcing some operators to run down their activities.

The success story on the accommodation market is continuing in the current year. In the

first four months the number of overnight stays increased by 4 % and shows the same

level of growth in comparison to the previous year. Unlike in previous years however the

larger contribution to growth stems from domestic tourism. Whilst overnight stays on

the part of domestic guests increased by 4.2 % the growth of overnight stays by foreign

guests was somewhat more moderate at 3 % and significantly lower than in the previous

year. The economic downturn and trade conflicts were able to dampen demand from

abroad. Both throw a shadow onto the further development of the accommodation sector

which, based on experience, reacts extremely sensitively to changes in the environment.

Overnight stays rising

and rising …

City trips generated demand …

Increase in supply accelerating

Occupancy and room prices

positive, local differences

… and climate change!

2019 got off to a sound start

HOTEL MARKET

10

11

B C D F HH L M S

2018

Overnight Stays 1,000 32,872 6,288 4,988 10,150 14,530 3,376 17,124 3,912of which foreign guests 1,000 15,088 2,157 2,016 4,526 3,599 524 8,369 1,223

Guests 1,000 13,502 3,670 3,069 5,935 7,178 1,837 8,266 2,063of which foreign 1,000 5,405 1,178 1,144 2,487 1,605 270 3,758 569

Hotels Number 773 280 227 298 397 133 449 171

Occupancy (Beds) % 61.5 52.5 49.9 49.6 59.4 50.9 60.5 50.3

Occupancy (Rooms, AC) %

ARR (AC) %

RevPAR (AC) %

January – April 2019 Change on previous Year

Overnight Stays % 6.0 5.2* 3.0* 4.5 3.9 5.3 7.9 2.7of which foreign guests % 7.7 1.8* 4.7* 3.1 3.6 0.6 5.6 0.9

rising declining stable * Jan to Mar 2019

MARKET DATA

ARR Annual Change

%

REVPAR Annual Change

%

-10

-5

0

5

10

B C D F HH L M S

%

-10

-5

0

5

10

15

B C D F HH L M S

%

Sources: Kenstone, IHA Sources: Kenstone, IHA

2017 2018 2017 2018

OCCUPANCY (ROOMS) Annual Change

%

Sources: Kenstone, Statistical Offices Sources: Kenstone, IHA

OVERNIGHT STAYS Annual Change

%

2017 2018 Jan. – Apr. 2019 2017 2018

-5

0

5

10

15

B C D F HH L M S

%

-4

-2

0

2

4

B C D F HH L M S

%

Sources: Kenstone, Statistical Offices, IHA

It was not really unexpected that the German logistics property market shone again in

2018 with a new record of space turnover. Users took up approximately 7,200,000 m²,

2,100,000 m² in the core centres and approximately 5,100,000 m² overall. Thus the dis-

tribution of surface area turnover shifted away from the five core centres in the direction

of peripheral regions which are however well-connected. There the surface area turnover

represents a new record. Building land which is becoming increasingly scarce is leading

to shifts in terms of area where availability is at least better.

2019 again appears to be a year in which the logistics sector expands and activities in the

corresponding property segment remain at a high level. However clouds are gathering.

Whether this trend continues at this level of dynamism is therefore not certain. The logis-

tics indicator of the BVL which reflects the mood within the logistics sector shows a clear

gap between the assessment of the situation and expectations within the logistics sector.

The current situation is still to be regarded as good, based on this, whilst expectations

have subsided to a level which was last recorded in 2012 in the context of the national

debt crisis.

The slightly more unfavourable economic environment is only reflected to a certain extent

in terms of turnover in the most significant transportation hubs. The turnover of goods at

German transportation airports increased in the past year by 1.4 % but showed in the first

few months of the current year a decline of 2.4 %. On the other hand container transport

at German seaports remains stable in 2018 and started with a slight rise in 2019.

The demand structure only changed slightly in 2018 in comparison to the previous year.

For the second year in succession logistics providers (approximately 38 %), followed by

industry and trade were the most active players. In terms of trading companies almost

50 % relates to e-commerce. The majority of users, as in previous years, are tenants but

the proportion of self users remains considerable at approximately 40 %.

In the expanding logistics market new developments represent a significant element to

cover growing demand for space. Approximately 43 % of requests were implemented in

new buildings and the remaining 57 % in existing properties which is however slightly

lower than in previous years.

New space entering the market remained high in 2018 when compared in the long

term but the result did not follow on from the two previous years as a result of limited

resources in terms of building land and construction capacity and fell below the level of

4,000,000 m². The total space is achieved in this regard in the typical formats such as

for example distribution centres or storage centres. Alternative formats such as for exam-

ple for city logistics remain the exception.

Driven by the high demand and rising construction costs a successive increase in rent is

to be recorded. The majority of the markets considered here showed rental increases.

It seems that developers can no longer absorb increasing building land prices and con-

struction costs by falling returns/increasing purchase prices.

The logistics sector will increase in significance not least because of the background of

changing social and economic structures. The dynamism with which this takes place

depends however on the economic environment which has recently experienced a setback.

One can therefore not rule out a lower level of dynamism in logistics markets.

Demand for logistics

space remains high

Environment has however

deteriorated

Transportation handling

figures show a mixed picture

New buildings essential

to meet demand

Signs of dynamism

subsiding increase

Completions at a high level

Prime rents increase

moderately overall

Demand structure unchanged

LOGISTICS MARKET

12

13

B C D F HH L M S

Take Up 1,000 m² 407.1 225.0 320.3 660.0 470.0 383.0 279.0 213.9

Prime Rents € / m² 5.50 5.10 5.40 6.00 5.80 4.50 7.10 6.15

MARKET DATA 2018

Sources: Kenstone, JLL, agents

TAKE UP By Region EXPORTS + IMPORTS 12-months-cumulative

bn. €

Sources: Kenstone, JLL Sources: Kenstone, Federal Statistical Office

Berlin Dusseldorf Frankfurt Hamburg Munich

PRIME RENTS

€ /m²

Sources: Kenstone, JLL Sources: Kenstone, agents

TAKE UP

m m²

Outside of the core areas Core areas (Big 5) 2017 2018

1,750

2,000

2,250

2,500

Apr

11

Apr

12

Apr

13

Apr

14

Apr

15

Apr

16

Apr

17

Apr

18

Apr

19

bn. €

Apr

-11

Apr

-12

Apr

-13

Apr

-14

Apr

-15

Apr

-16

Apr

-17

Apr

-18

Apr

-19

4

5

6

7

8

B C D F HH L M S

€/m²

0

2

4

6

8

11 12 13 14 15 16 17 18

Mio. m²

19 %

15 %

31 %

22 %

13 %

2018

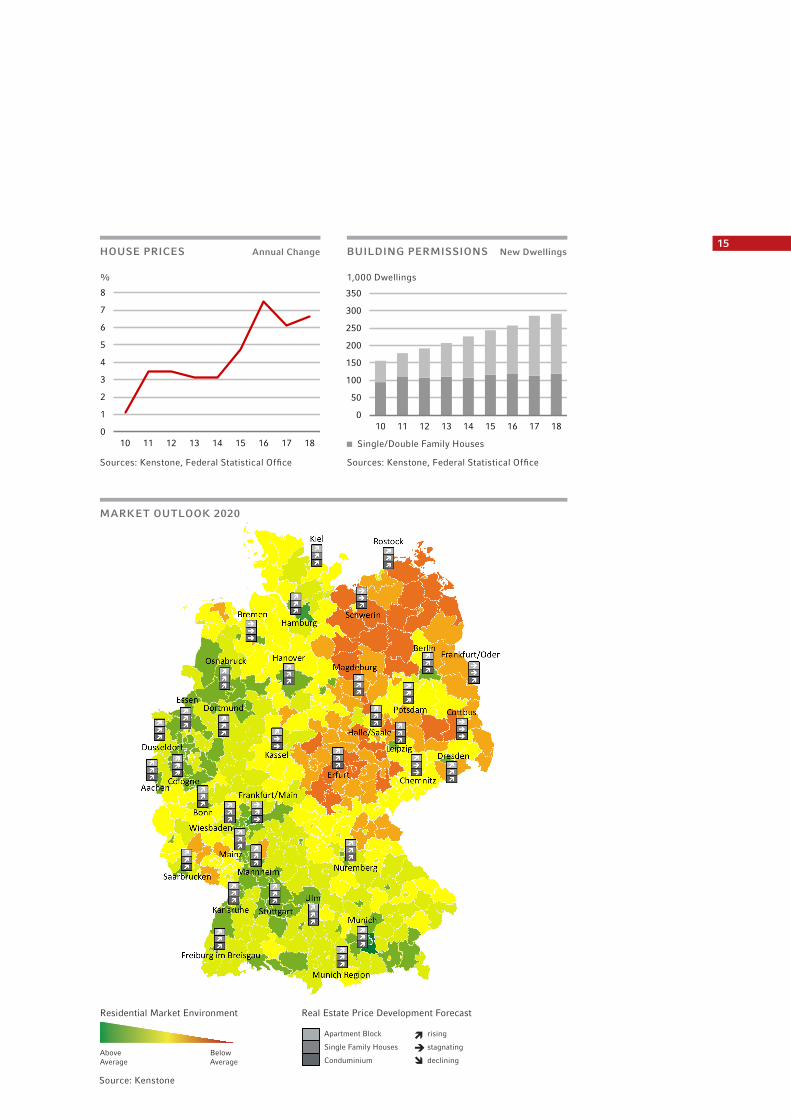

The German residential market is continuing its long-lasting upturn in 2019. The factors

which are driving price continue to apply. A record in the number of people employed

as employees, very sound growth in income and interest rate policy which has yet again

eased despite temporary fantasies of rising interest rates make for ongoing pressure on

price. In addition one has to consider increasing construction costs applying pressure on

the supply side.

Accordingly the price rises on the German residential market remain significant today.

According to the house price index of the Federal office for statistics prices increased

in 2018 by approximately 6.7 % and here price growth for existing properties is slightly

higher than for new buildings. As in the cycle as a whole price growth is driven by signi-

ficant increases in land value (+9 % in 2018) and a significant price increase for construc-

tion costs (+4.4 % in 2018).

Across the regions different growth rates are recorded. The highest price growth is to

be found in prospering agglomerations whereby in the majority of rural areas increasing

prices are also now to be recorded.

The financing environment remains favourable on the one hand for the potential purchas-

er and on the other hand non-critical from a macro economic point of view. The increase

in residential financing is slowly gaining speed for private households and the share of

mortgages is increasing as a share of GDP. Both indicators are however significantly below

historical levels and are therefore no cause for concern.

With respect to the development of rents the sources available do not indicate a common

conclusion. However the indications are mounting that new rents are increasing at a lower

level or are even in the process of stagnating. The cause for this could be several factors.

On the one hand the number of completions is increasing and on the other hand the ef-

fects of the “rental price brake” could be impacting. In addition rents have in part reached

a level which has limited the potential circle of users in the past few years.

Construction activity increased again in 2018 in comparison to the previous year. Approx-

imately 318,000 flats (only new buildings) were approved which represents an increase

of approximately 11 % and approximately 238,000 flats, approximately 4 % more, were

completed in comparison to the previous year.

Both for approvals and also for completions the growth results from an increase in apart-

ments which is to be found fundamentally in German growth centres.

On the other hand a careful analysis of planning approvals shows that the latter have

moved sideways since the middle of 2018. Clearly the availability of building land and also

resources in administration and the building sector are limiting further increases.

One cannot fundamentally ascertain that anything significant is changing in the upturn

of the residential market. Given the background that there is only a limited alternative for

investment, the acquisition of property for self usage also for rental purposes will remain

attractive. On the other hand the economic weakening may find its way to the residential

market through various channels and the continuous construction activity may close the

gap between demand and supply. These aspects considered, we assume that the residen-

tial market will continue to develop soundly without however achieving the recent very

high levels of growth for both rents and prices.

Boom and no end?

For buyers ongoing favourable

financing environment

Price rises continue at high level

Rental growth appears to be weakening

Lively building activity but

stagnation for planning approvals

Further development in

residential market more muted

RESIDENTIAL MARKET

14

15

Source: Kenstone

BUILDING PERMISSIONS New Dwellings

1,000 Dwellings

Sources: Kenstone, Federal Statistical Office

MARKET OUTLOOK 2020

HOUSE PRICES Annual Change

%

Sources: Kenstone, Federal Statistical Office

Apartment Block Single/Double Family Houses

Kiel Rostock

SchwerinHamburg

Bremen

Osnarbruck Hannover

Magdeburg

BerlinFrankfurt/Oder

Cottbus

Dresden

Chemnitz

Halle/Saale

Leipzig

Erfurt

Kassel

Essen

Dusseldorf

Aachen Cologne

BonnWiesbaden

Mainz

Frankfurt/Main

Mannheim

Saarbrucken

Karlsruhe

Stuttgart

Ulm

Nuremberg

Freiburg im Breisgau

Munich Region

Munich

PotsdamDortmund

Ruhrgebiet

Residential Market Environment

AboveAverage

BelowAverage

Real Estate Price Development Forecast

Apartment Block rising

Single Family Houses stagnating

Conduminium declining

0

50

100

150

200

250

300

350

10 11 12 13 14 15 16 17 18

1,000 Dwellings

0

1

2

3

4

5

6

7

8

10 11 12 13 14 15 16 17 18

%

The German investment market is still in great shape. For the top five cities in 2018 again

an increase in transaction volume was registered. Throughout Germany turnover in 2018

and also in the first half-year 2019 was below the level of the respective period in the

previous year. However, at € 24.4 billion it remains at, when compared in the long term,

a very high level. Irrespective of macro economic uncertainty domestic properties still

represents one of the few investment forms in which relatively secure, satisfactory returns

can still be achieved.

The user markets are providing largely sufficient tailwind to factor in rising rents into

investment calculations. If one disregards parts of retail then all other fundamental user

markets can be content with at least stable if not rising rents.

One cannot fail to recognise however that the circle of investors appears to be gradually

changing. In the first half-year the proportion of foreign investors fell to below 40 %, a

level last seen lower in 2013. Presumably the returns achievable here or the quality of the

stock available no longer meet the expectations of some investors.

Following the development of user markets, the proportion of office properties in terms of

turnover in 2018 and also in the first half-year 2019 increased. At above 47 % it is signifi-

cantly above the level achieved in previous years. The losers are however retail properties

whose share of transaction volume has settled at approximately 20 %. In addition other,

established usages such as hotels and logistics properties are sought after and the avail-

ability of these is increasing but not achieving by far the level of office or retail properties.

Irrespective of the increase in regulation in the market following the implementation

of the rental price brake and even a discussed rental price cap in Berlin, investments in

residential properties still remain attractive. For a large group of investors which are

predominantly German in origin it provides a geographically wide range of investment

opportunities with a low risk profile. Turnover increased in 2018 and achieved the second-

highest result of the last 10 years. Also in the first half-year 2019 significant transaction

activity was to be observed.

With respect to capital seeking a form of investment and also the financing market we

observe a solid environment even if the weakening economy is changing the view of banks

in terms of the risk perspective. On the other hand all fantasies of a gradual increase in in-

terest rates which were being discussed still before the end of the year have disappeared

in the meantime.

Since Berlin at approximately 2.9 % since the end of 2017 has had the top position in

office yields, the yields in the markets observed have slimmed down to a range between

2.9 % and 3.2 %. Only in Leipzig is this higher with a significant 4.3 %. Against expecta-

tions a continuing compression in yields is also to be observed for other property types

with the exception of shopping centres and inner-city commercial properties. The yields

there which are stable/rising reflect the disruption in retail which is increasingly reflected

in the rental income of such properties.

The environment for the German CRE-Investment market has deteriorated somewhat in

the light of the economic downturn but remains overall positive such that it is assumed

that market activity will continue at a level which is above average.

Investment turnover

remains at high level

Foreign investors less active

User markets mostly providing

impetus from the income side

Office buildings still

investors‘ favourite

Investment in residential

segments remain sought after

Capital availability non-critical

Varying yield development

CRE-Investment market

will remain dynamic

INVESTMENT MARKET

16

0

5

10

15

20

25

30

35

10 11 12 13 14 15 16 17 18 19

Mrd. €

17

CHANCES IN MARKET VALUES

Source: Kenstone

INVESTMENT VOLUME Annual Change

%

Sources: Kenstone, BNP Paribas Real Estate

2017 2018

INVESTMENT VOLUME (B, D, F, HH, M)

bn €

Sources: Kenstone, BNP Paribas Real Estate

Sources: Kenstone, agents

Sources: Kenstone, agents

PRIME OFFICE YIELDS

%

2017 2018 Q2 2019

Change on last 12 months

Outlook next 12 month

Office 10 % 5 %

Retail 0 % 0 %

Logistics 10 % 5 %

Residential(apartment blocks) 5 % 5 %

B C D F HH L M S

2018

Investment Volume of which m € 7,429 1,981 3,907 10,229 5,895 800 6,667 2,543Foreigners % 50.1 56.6 37.7 45.0 26.3 37.2 34.7 48.2Office % 56.8 46.4 65.1 82.4 51.9 32.5 63.8 59.2

Prime YieldsOffice % 2.90 3.15 3.20 3.15 3.05 4.30 3.20 3.05Retail % 2.90 3.20 3.20 3.10 3.00 4.20 2.90 3.20Logistics % 4.05 4.05 4.05 4.05 4.05 4.50 4.05 4.05

Mid-year 2019

Investment Volume m € 5,240 871 1,163 2,341 1,137 320 2,162 977

Prime YieldsOffice % 2.90 3.10 3.20 2.95 3.05 4.30 3.10 3.05

MARKET DATA

-50

0

50

100

B C D F HH L M S

%

Mid

-yea

r

2

3

4

5

B C D F HH L M S

%

DISCLAIMER

This publication serves exclusively to provide general information. The information contained in

this report is based on publicly accessible sources which we consider reliable. We cannot accept any

liability for the correctness or completeness of the information. All statements of opinion express the

author’s current assessment and do not necessarily represent the opinion of KENSTONE. The opinions

expressed in this publication may change without any prior announcement.

18

As

at O

ctob

er 2

019

· Pro

tect

ive

Ch

arg

e 50

,– €

CONTACT

KENSTONE GMBHREAL ESTATE VALUERSwww.kenstone.de

Dr. Michael BrandlManaging Director KENSTONE GmbH Real Estate ValuersLeopoldstr. 23080807 MünchenPhone +49 (0) 89.35 64-2456Fax +49 (0) 89.35 [email protected]

Martinus KurthManaging Director KENSTONE GmbH Real Estate ValuersLützowplatz 410785 BerlinPhone +49 (0) 30.26 53-2070 Fax +49 (0) 30.26 [email protected]