Embed Size (px)

Citation preview

Project co-finance by the FCH JU under FP7:

Market outlook for

Green Hydrogen

Daniel Fraile, Hinicio

CertifHy Public Launch, Brussels

April 23rd, 2015

Content

1. Hydrogen Global Outlook

2. Drivers for Green Hydrogen

3. Market outlook for H2Mobility

4. Market outlook for Power to Gas

5. Market outlook for Industry

6. Conclusions

Disclaimer: Figures presented here are still under consultation. They may be subjected to final review, after consultation with

stakeholders

INDUSTRY sector represents over 99% of all

hydrogen market

• The global demand in 2010

was approximately 43

Mtons and is foreseen toreach 53 Mtons by 2030,

• Europe represents 16% ofthe hydrogen global share35,87

44,31

6,83

7,09

0 10 20 30 40 50 60

2 0 1 0

2 0 3 0

MILLIONS TONS OF H2

H2 Demand Rest of the World Europe H2 Demand

23% Accumulated Growth

Ammonia accounts for over half of the total Industry consumption. Refineries are the second largest

consumer of hydrogen

80% of thedemand isconcentratedin two sectors(refineries andammoniaproduction forfertilizers)

Severalindustrialsectors count

for just 1% ofhydrogendemand.

Note: Market shares are based on global figures and are validated for Europe. H2 demand is

projected for Europe only.

Sources: Linde group, ICIS consulting, CEPS and Freedonia

Expected green hydrogen markets

All market segments will depend on a strong regulatory framework and

market incentives to valorise the added value of green hydrogen

Regulatory drivers are essential to create a

market for green H2

* These are drivers for penetration of FCV, regardless the type of fuel/hydrogen

Mobility and

transport Power to gas

Refineries

Amonia

(other

chemicals)

metal

processing

Food, Glass

production,

Semiconductors,

aerospace

H2 use inFCVs

Energy storage

and system

transformation

Fuel quality directive

RED (including. Renewables Transport

target)

Emissions Performance standards for

passenger cars

Low Emissions Zones*

Alternative fuel infrastructure

directive*

ETS (Cap, exemptions, CO2 price)

Industry

Regulatory drivers

Market drivers are also important and will play an important role in the long term, including, in

niche industrial sectors

Mobility and

transport Power to gas

Refineries

Amonia

(other

chemicals)

metal

processing

Food, Glass

production,

Semiconductors,

aerospace

H2 use

inFCVs

Energy storage

and system

transformation

Oversupply of variable

renewable energy/ Energy

storage market

Consumers choice- clean

transportation

CSR- Green marketing/ Company

image

cost competitive vs. SMR or vs.

ICE vehicles (pushed by

technology development,

pulled by market subsidies)

Industry

Market & Economic drivers

Certifhy’s Policy driven scenario to 2030

A clear policy framework for alternative vehicles and

low-carbon fuels after 2020

Power

• Renewable Energy directive

Transport

• Target for renewables in transport by 2030

• Fuel Quality directive (10-12% saving target by 2030)

• CO2 regulation in cars (70g/km in 2025)

• National targets for refuelling infrastructure

Energy Intensive

• ETS CO2 market

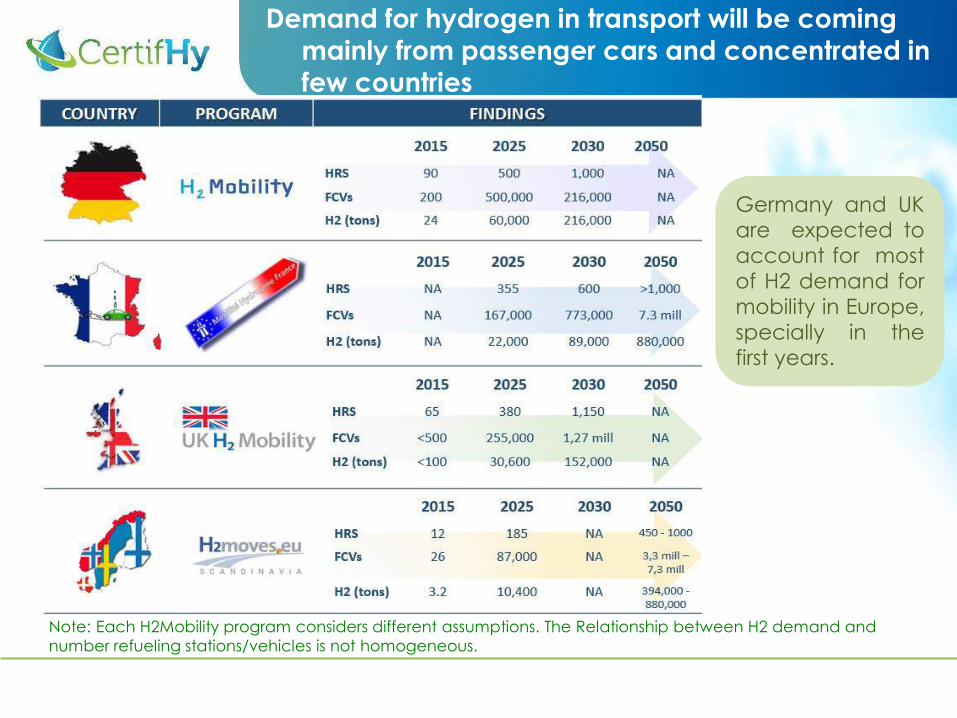

Demand for hydrogen in transport will be coming mainly from passenger cars and concentrated in

few countries

Germany and UK

are expected to

account for most

of H2 demand for

mobility in Europe,

specially in the

first years.

Note: Each H2Mobility program considers different assumptions. The Relationship between H2 demand and

number refueling stations/vehicles is not homogeneous.

Demand for FCV could lead to 0.8MTons of hydrogen by 2030, representing 6.5 million cars

H2mobility programsare more conservative& delaying the

penetration of FCV ascompared to previousstudies.

• We base our projections on the most recent H2mobility roadmaps.

• For 2015, demand is given by the UK, France, Germany and Scandinavia roadmaps.

• From 2025, we assumed these countries represents 60% of hydrogen demand forpassenger cars in Europe.

3 mill

0,0

0,5

1,0

1,5

2,0

2,5

3,0

2015 2020 2025 2030

H2

MTo

ns

H2 demand for road transport in Europe

Hinicio / H2 mobility Iniciatives Hyways scenario : high policy support-modest learning

Hyways scenario : high policy support-fast learning McKinsey power trains study

1.4 Mtons

0.8 Mtons

3 Mtons

Most demand in Mobility will need to come from green/low carbon sources

In the mid to

long-term, a

transition to FVCs

will only be

supported if

emissions saving

are significant.

By 2030, we

expect 75% to

be produced

from low-

carbon/RES

sources.

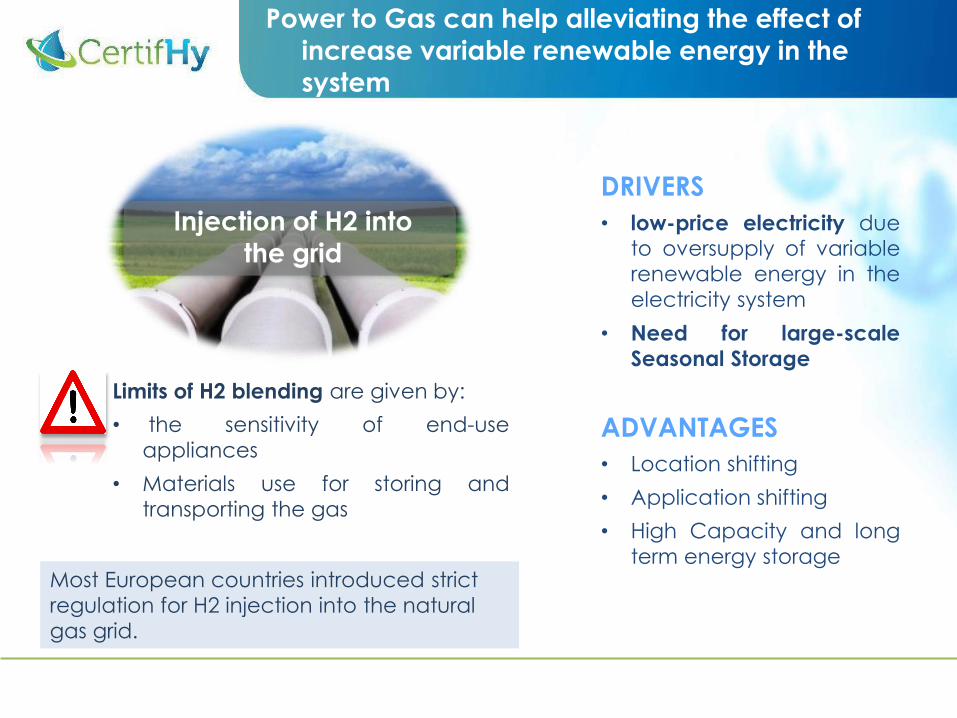

Power to Gas can help alleviating the effect of increase variable renewable energy in the

system

Injection of H2 into

the grid

Limits of H2 blending are given by:

• the sensitivity of end-use

appliances

• Materials use for storing and

transporting the gas

Most European countries introduced strict

regulation for H2 injection into the natural

gas grid.

DRIVERS

• low-price electricity dueto oversupply of variable

renewable energy in the

electricity system

• Need for large-scale

Seasonal Storage

ADVANTAGES

• Location shifting

• Application shifting

• High Capacity and long

term energy storage

Hydrogen injection could in theory allows

for a yearly absorption of up to 35TWh

• Bounded by the pipeline flow rate during low consumption periods, thus during

SUMMER

• 3 scenarios: Low (1%), Medium (2%) and High (5%) hydrogen volume blending

• We have only considered direct injection (no methanization)

Calculation

-

0,50

1,00

1,50

2,00

2,50

3,00

3,50

-

20.000

40.000

60.000

80.000

100.000

120.000

2020 2025 2030

Ton

s o

f H

2M

illio

ns

GW

h

P2G

1% H2 blending 2% H2 blending 5% H2 blending

Maximum Theoretical: 20%

Hydrogen injected in the natural gas grid will be mainly from renewable energy sources

2025 it is assumed 1% of H2 volume blending

2030 it is assumed 2% of H2 blending

• Largely depending on legal requirements (specially beyond

2020) and policy incentives:

• Potential new requirements (heavy oils for maritime transport)

• Substitution to low-carbon hydrogen will need to compete

againts other fuel CO2 reduction alternatives (biofuels,

electricity, upstream emissions, type of crude, etc.)

Refineries represent the industry sector with the largest potential for green hydrogen use

The main driver in other Energy-intensive

Industry might by CO2 prices

• Large uncertainty of CO2 prices. But we expect them to

increase in the long term

• Industry use of low carbon H2 will heavily depend on the cost

of producing that H2, or the price of a low-carbon GoO

• Substitution to low-carbon H2 will also depend on other CO2

emission reduction options (efficiency, renewable energy

input, etc.)

• Possible new requirements for Ammonia (fertilizers) producers

could lead to new drivers

Green hydrogen use in Industry

Under discussion…

Under a CO2 policy driven scenario, green hydrogen demand

could grow to significant levels in the mid-to long term (up to 17%by 2030)

If climate change and energy independence continue to dominate EU

action and national industry roadmaps for mobility materialize

Conclusions (I)

Provisional

Conclusions (II)

• Disconnecting the production site from the demand for green

hydrogen through the use of a GoO system will be essential for

an effective use of green hydrogen.

• Ideally, a good GoO scheme should be flexible enough to

serve both objectives: proof of renewable origin and of a low-

emission content.

• A clear long-term decarbonisation strategy is needed. EU

should set a concrete and ambitious legislative framework for

the post-2020 period.