Embed Size (px)

Citation preview

MARKET ENVIRONMENT REPORT Winter 2013

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 2

About MercerMercer is a global provider of investment services, and offers customized guidance at each stage of the investment decision, risk management, and investment monitoring process. We have been dedicated to meeting clients’ needs for more than 40 years, and work with the fiduciaries of retirement funds, foundations, endowments, wealth management firms and other investors in more than 60 countries. We offer clients a continuum of services in order to tailor solutions specific to their unique requirements and governance objectives. Our services include:

For further information contact:Sue Crosby, Endowments and Foundations, [email protected] or at 212 345 9264John Nussbaumer, Retirement Plans and Health Care, [email protected] or at 404 442 3280David Eisenberg, Wealth Management Providers, [email protected] or at 617 747 9454

Missed our recent publications? Mercer Investment Forum – Boston June 13-14, 2013 - http://www.mercer.com/insights/investment-consulting Endowment and Foundations – Video with Richard Anderson – http://www.mercer-hammond.mercer.com/home Top Pension Risk Management Priorities for 2013 - http://www.mercer.com/press-releases/1494665 10 Steps for DC Plan Sponsors in 2013 - http://www.mercer.com/usdc Global Asset Manager Fee Survey - http://www.mercer.com/articles/1503475 Understand ETFs and Evaluation of their Uses - http://www.mercer.com/articles/understanding-exchange-traded-funds Building a Responsible Investment Portfolio - http://www.mercer.com/articles/building-a-responsible-investment-portfolio

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 3

Overview

Table of Contents

Market commentary 4

PerformanceGlobal equities climbed the wall of worry 5

Investors enjoyed strong returns in 2012 6

Macro environmentThe Fed expanded QE3 7

The tax deal reduced the risk of a recession 8-9

Global economic growth appears to have bottomed 10-11

Financial marketsMacro conditions should have less impact in 2013 12-13

Global equities: Valuations still attractive 14

US equities: Profits appear to be peaking 15

US equity style: Maintain quality focus, reduce growth bias 16

Emerging market equities topped developed markets for the year 17

International developed equity valuations remain more attractive than the US 18-19

Fixed income: Credit rallied in 2012, but little upside remains 20-21

Currencies: A race to the bottom 22-23

Fundamentals supportive of local currency debt 24

Global REITs produced strong returns in 2012 25Private equity stacks up well against public markets 26

Hedge funds lagged balanced portfolios in 2012 27

Liability driven investing: Maintain tactical under-hedge 28

Executive Summary

Global equity markets posted strong returns in 2012 as the MSCI ACWI index rose 16.1%. Treasuries returned a modest 2.0%, while investment-grade bonds gained 9.8% and high yield bonds rose 15.8%.

While the secular economic outlook for the developed world is weak and 2013 will likely bring more flare-ups, the macro environment appears to be stabilizing. The ECB has reduced left-tail risks in the Eurozone, although the crisis is likely to persist as a source of uncertainty. The Chinese economy appears to have avoided a hard landing and growth is improving. The US was able to avoid the full brunt of the fiscal cliff, but economic and employment growth is likely to remain subpar.

Expected returns on bonds have plunged as a result of the financial crisis and central bank actions. Meanwhile, equities and some other riskier assets offer significantly better valuations than they did before the crisis. Institutions that have not revisited their strategic allocations in some time may wish to do so as the long-term risk-reward trade- off between stocks and bonds has changed materially over the past five years.

Global equity valuations remain neutral to attractive on an absolute basis, but compelling relative to sovereign bonds and credit. US equity valuations are elevated on cyclically-adjusted measures, but high profit margins could persist for some time. International developed equities are attractively priced, especially against US equities. Emerging market equities are likely to remain highly sensitive to macro sentiment, but are priced to outperform developed equities.

Domestically, we continue to suggest tilts toward high quality stocks and away from small caps. Given the strong outperformance of growth relative to value over the past six years, we suggest adopting a more style neutral domestic equity portfolio. Outside the US, quality sectors appear less attractively priced. Investors that have distinct non- US quality allocation could consider reducing the size of quality overweights.

While we continue to favor credit over Treasuries, potential excess returns have fallen as spreads have narrowed. Yields on investment-grade bonds fell to record lows, although spreads relative to Treasuries remain above historical averages. The yield on high yield bonds also dipped to a record low. High yield bonds are reasonably attractive relative to Treasuries, but equities offer better risk-adjusted returns.

Spreads on illiquid debt securities have not compressed to the same extent as they have in public markets. This can be capitalized upon through private debt partnerships and some hedge funds. A diminishment in the importance of macro factors should result in a re-focus by the market on fundamental value, providing opportunities for alpha generation through asset allocation tilts and security selection.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 4

Market commentary January 2013Despite an uncertain macro environment and lackluster economic growth, global equities posted strong gains in 2012, with the MSCI ACWI index rising 16.1%. This came with significant intra-year volatility with two sell-offs greater than 10%. The S&P 500 finished 16.0% ahead for the year. Despite underperforming the S&P by 650 basis points in the first half of the year, the MSCI EAFE index edged ahead of the S&P with a 17.3% return for the year. Emerging market equities outperformed developed equities for the year with a gain of 18.2%. The reduction of macro risk was likely the primary driver of stock returns in 2012. The ECB showed its willingness to preserve the euro zone through the OMT program, reducing the likelihood of a disorderly break- up. In addition, fears of a hard landing in China receded as growth bottomed and began to recover. Finally, the US will avoid the brunt of the fiscal cliff in 2013, reducing the likelihood of a recession. Of course, macro risks remain. The developed world remains overly-indebted and is likely in for an extended period of slow growth. However, conditions seem to be stabilizing, and the likelihood of disaster scenarios have been reduced by policy actions. A diminished impact of macro on markets should mean lower correlations within and across asset classes, increasing the value of diversification. The injections of liquidity by the Federal Reserve and other central banks have fundamentally altered the outlook for fixed income. Yields on almost all types of fixed income instruments are at or near record lows. Cash rates will likely be near zero for at least two more years, and as measured by TIPS, Treasury investors will lose ground to inflation for maturities out to nearly 20 years. Investors reacted to this dynamic by shifting to credit, resulting in outsized gains in 2012. Investment grade bonds returned 9.8% on the year as the yield declined by 103 basis points to a meager 2.7%. High yield bonds jumped 15.8%, as yields declined from 8.4% to just 6.1%. Investment-grade corporate bonds yield 1.8% more than Treasuries, which remains above the historical average, and high yield bonds yield 5.2% more than Treasuries, which is in line with the historical average and reasonable in light of the short-term default outlook. We continue to favor credit over Treasuries, but with absolute yields so low, returns will largely be limited to income. Credit investors could look to private credit markets for higher returns. Spreads on illiquid debt securities have not compressed to the same extent as they have in public markets.The short-term outlook for equities is mixed. Stabilization of macro risk is a positive for equities, but short-term sentiment indicators hint a degree of complacency and investor surveys suggest excessive bullishness, raising the possibility of a pullback. In addition, the VIX index has dipped to the low teens in January, and the cost of portfolio protection has dropped. For investors with

longer time horizons, however, equities continue to offer compelling value versus Treasuries and credit. Despite their strong performance in 2012, global stocks appear reasonably priced. US equities are a bit rich when using cyclically-adjusted earnings measures. However, companies are benefitting from an accommodative Fed policy through lower interest rates. Non-US equities offer better valuations, but with greater risks.Corporate managements are signaling the attractiveness of equity relative to credit. US corporations are taking advantage of artificially low rates by issuing debt—over $1.5 trillion in the US in 2012. Over half of this was used to refinance existing debt at lower rates, which falls directly to the bottom line. However, companies are also increasing debt loads. In many cases, this is offering high quality companies a form of arbitrage, as debt costs are usually below earnings yields and often below dividend yields. In this low growth environment, companies are generally not investing with proceeds from debt issuance, but instead are returning money to equity shareholders through dividends, buybacks and cash mergers. Over the last two years (through 3Q12), non-financial companies have issued $840 billion in new debt securities (+18% of outstanding), while retiring $871 billion in equity (-6% of outstanding).While companies are reducing the supply of equities through buybacks and mergers, we may begin to see an increase in demand for stocks as investors rotate out of bonds. This could push valuations higher. Institutional investors have generally been reducing allocations to equities for more than a decade due to two brutal bear markets, high volatility and a remarkable bull market in bonds. However, the dismal return outlook for fixed income securities has become unavoidably clear, while prospective equity returns are reasonable even in a low-growth world. If macro conditions stabilize, investors may shift their focus toward meeting long-term needs, which in most cases will require a higher allocation to equities.In summary, while financial stress has receded over recent months, the macro environment remains uncertain; however, we suspect that these risks are well- recognized by market participants and discounted in prices. Given the paltry returns offered by fixed income securities, institutions should consider reexamining their strategic policies to determine the appropriate mix between defensive and risky assets. We endorse equity investments as an important tool to meet long-term objectives; however, we continue to recommend diversifying growth assets among a greater number of return drivers, such as private equity, private debt, hedge funds and real asset-oriented investments. Finally, a diminishment in the importance of macro should result in a re-focus by the market on fundamental value, providing opportunities for alpha generation through asset allocation tilts and active management.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 5

Global equities climbed the wall of worry

2012 Global Equity Market Performance

-10

-5

0

5

10

15

20

Dec

-11

Jan-

12

Feb-

12

Mar

-12

Apr-

12

May

-12

Jun-

12

Jul-1

2

Aug-

12

Sep-

12

Oct

-12

Nov

-12

Dec

-12

(%)

S&P 500 Russell 2000MSCI EAFE MSCI Emg Mkts

2012 Returns for Global Markets

15.617.3

8.2

18.2

24.6

16.0

19.1

17.3

21.622.5

17.016.0

0

5

10

15

20

25

US (S&P500)

MSCI EAFE Europe Japan Pacif ic ExJapan

EmergingMkts

(%)

US $

Local Currency

2012 Style Performance

18.118.515.8

17.020.2

12.814.615.1

0

5

10

15

20

25

Gro

wth

Valu

e

Gro

wth

Valu

e

Gro

wth

Valu

e

Def

ensi

ve

Dyn

amic

Russell Top 200 Russell Midcap Russell 2000 Russell 1000

(%)

2012 S&P 500 Sector Performance (%)

2.3

7.5

12.2

15.2

26.3

-2.9

12.5

12.5

21.9

13.2

-5 0 5 10 15 20 25 30

Utilities

Energy

Cons. Staples

Materials

Industrials

Telecom

Info Tech

Health Care

Cons. Disc.

Financials

Foreign equities made-up a large deficit to US in the second half.

Reduced macro tensions and central bank actions lifted equities in the second half of 2012.

Europe lagged the US in loca l currencies, but outperformed in US$ as the euro rallied. Since the end of May, Europe has outperformed the S&P 500 by 1530 bps in US$.

The plunge in the yen helped the Japanese market, bu t weighed on US$ returns.

Emerging currencies appreciated modestly.

An improving housing market helped to boost financials.

Oil prices declined 7%.

Tech stocks fell 5.2% in Q4.

Value outperformed growth across all capitalizations as financial stocks posted strong gains.

Cyclical, high-beta stocks outperform ed defensive stocks.

Despite tepid growth, consumer discretionary stocks outperformed staples.

Currency wa s neutral for EAFE.

Source: Bloomberg

Source: Bloomberg Source: Bloomberg, MSCI

Source: Bloomberg

The dispersion of cap and style returns was narrow in 2012.

Global equities finished the first quarter with strong returns, but tumbled in the second quarter.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 6

Fourth Quarter Performance (%)

3.3

4.1

6.6

6.0

1.9

0.7

-0.1

0.0

-6.3

-2.4

-0.4

-0.2

5.6

5.8

1.1

1.8

2.9

-3.1

-10 -5 0 5 10

Commodity Futures

Natural Res Stks

Intl Fixed

US Large-Cap Stks

US MBS

US Treasuries

T-Bills

US TIPS

US I/G Corp Bonds

Funds of Hedge Funds

US Small-Cap Stks

US Mid-Cap Stks

US High Yield Bonds

Emerg Mkt Debt (Local)

Emerg Mkt Stocks

Global REITs

Intl Sm-Cap Stks

Intl Large-Cap Stks

2012 Performance (%)

16.8

17.3

28.720.0

16.0

7.0

2.6

5.2

-1.1

1.5

2.0

2.2

17.3

18.2

9.8

15.8

16.3

0.1

-5 0 5 10 15 20 25 30

Commodity Futures

T-Bills

Intl Fixed

US Treasuries

Natural Res Stks

US MBS

Funds of Hedge Funds

US TIPS

US I/G Corp Bonds

US High Yield Bonds

US Large-Cap Stks

US Small-Cap Stks

Emerg Mkt Debt (Local)

US Mid-Cap Stks

Intl Large-Cap Stks

Emerg Mkt Stocks

Intl Sm-Cap Stks

Global REITs

Gold prices fell 6.7%, while oil prices were flat.

The intl fixed index, with a large weighting to Japan, was impacted by the sharp decline in the yen. The index was up 1.2% in hedged terms.

The S&P 500 did not participate in the fourth quarter rally.

Funds of hedge fund s outperformed US stocks and bonds in Q4.

Despite the expansion of QE3, the yield on the 10-year Treasury rose from 1.65% to 1.78% in Q4.

Europe gained 7% as financial tensions receded.

Small-caps outperformed large-caps by 270 bps in December.

The yield on junk bonds fell from 8.4% to 6.1% during the year.

Emerging currencies rallied against th e dollar in Q4.

US REITS earned 18.1% for the year.

Europe: 19.1%Japan: 8.2%

US large-caps were outperforming mids and smalls until December.

Emerging market US$ bonds were up 18%.

Europe/ME: 24.3% Asia: 20.8%Latin America: 8.7%

Financials: 14.6%Industrials: 7.6%

The Inflation breakeven rate on 10-year TIPS rose from 2.0% to 2.5%.

Commodity futures were the only major asset class to decline in 2012.

US Treasuries lagged credit.

Equity and credit investors enjoyed strong returns in 2012

Source: DatastreamSource: Datastream

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 7

The Fed expanded QE3 at its December meeting to include $45B a month in longer-term Treasury purchases on top of its existing $40B monthly MBS purchases. This puts the Fed on a pace to expand its balance sheet by more than a third in 2013, or $1 trillion. In addition, the Fed shifted its policy guidance from time-based to economic data-based. The FOMC stated that the Fed Funds target rate is likely to stay near

zero as long as unemployment is above 6.5% and forward looking intermediate-term inflation expectations are below 2.5%. At current labor participation rates and the recent pace of job creation, unemployment will not fall to 6.5% until late-2015 or early-2016. If participation rates return to pre-recession levels, unemployment could remain above the Fed’s target until early-2018. The FOMC’s December meeting minutes showed some disagreement

over when the current round of asset purchases should end, with some members suggesting they should conclude prior to year end.

Despite QE3, the yield on the 10-year Treasury increased slightly during the fourth quarter, rising from 1.65% to 1.78%. The real yield on 10-year TIPS rose from -0.77% to -0.67%, while inflation breakeven rates were relatively unchanged. TIPS price in inflation of 2.5% over ten years, in-line with historical averages. The economic impact of the Fed’s monetary policies is questionable at best

since borrowing costs are not what ails the economy. While risks of the Fed’s stimulus seem limited in the short-run, it carries significant longer-term risks. Over the near-term, inflation is likely to remain subdued and within the

Fed’s target range given economic slack. Labor costs, which are a substantial component of final goods prices, should be constrained by high unemployment. Inflationary pressures are most likely to arise from commodities since they are priced globally, and therefore less impacted by slack in the US economy and more sensitive to any weakening of the dollar. The larger the Fed’s balance sheet, the more difficult it will be to unwind

once economic conditions normalize. The bond market may struggle to absorb new Treasury debt plus Fed sales, which could lead to an unintended spike in rates and declining stock prices. However, if the Fed is too slow to sell bonds, inflationary expectations could rise, which would also lead to higher interest rates. The Fed might be powerless to end a negative feedback loop between inflation and interest rates.

The Fed expanded QE3

Decomposition of 10-Year Treasury Yield

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Real Yield on 10-Yr TIPSInflation Breakeven Rate

Fed Balance Sheet and Bank Excess Reserves

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Dec

-12

$ B

illio

ns

Fed Balance Sheet

Bank Excess Reserve

At the current rate of expansion, the Fed’s balance sheet could exceed $4T by the end of a year. The Fed currently owns 15% of Treasuries and 13% of agency and agency- backed debt. The Fed’s holdings of Treasury and agency debt exceeds those of China.

If bank excess reserves start to shrink, it would be good for growth, but it could generate inflation and force the Fed to unwind (sell) its holdings.

The inflation breakeven rate on 10-year TIPS is 2.5%, in-line with historical averages. It is just 2.1% on 5-year TIPS, suggesting benign inflation.

The real yield on Treasuries is sharply negative and unlikely to return to positive territory in the near future.

Source: Bloomberg

Source: Bloomberg

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 8

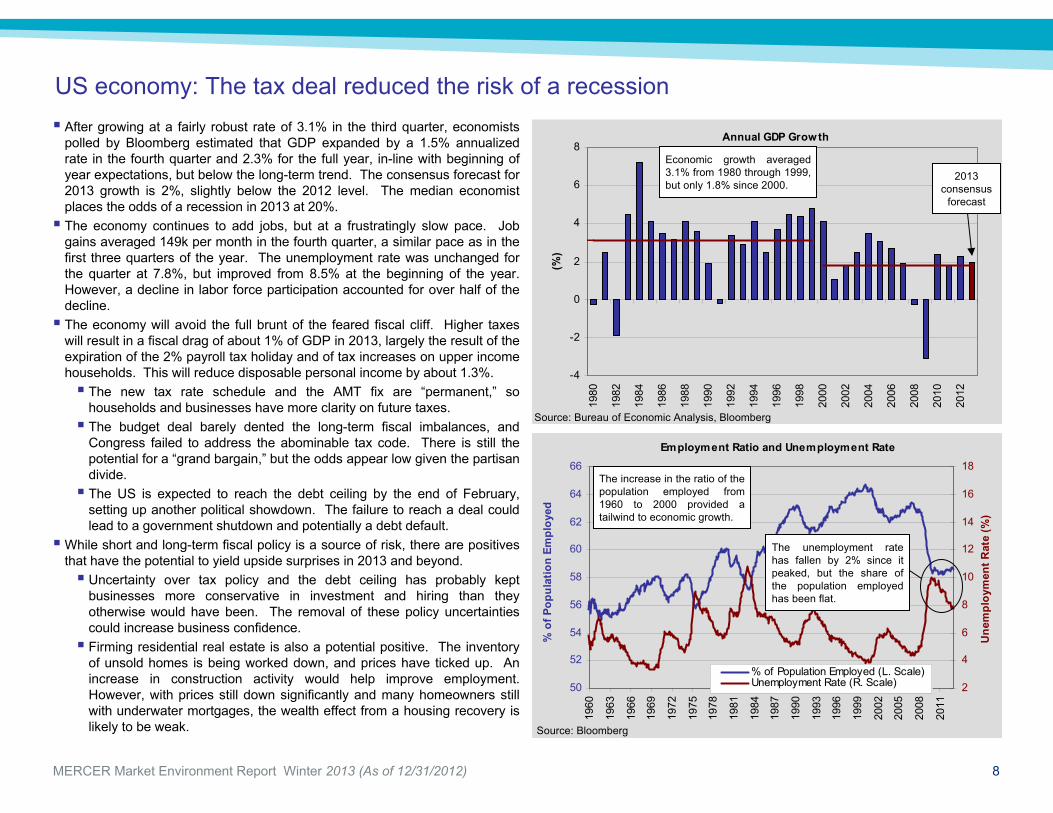

US economy: The tax deal reduced the risk of a recession After growing at a fairly robust rate of 3.1% in the third quarter, economists

polled by Bloomberg estimated that GDP expanded by a 1.5% annualized rate in the fourth quarter and 2.3% for the full year, in-line with beginning of year expectations, but below the long-term trend. The consensus forecast for 2013 growth is 2%, slightly below the 2012 level. The median economist places the odds of a recession in 2013 at 20%. The economy continues to add jobs, but at a frustratingly slow pace. Job

gains averaged 149k per month in the fourth quarter, a similar pace as in the first three quarters of the year. The unemployment rate was unchanged for the quarter at 7.8%, but improved from 8.5% at the beginning of the year. However, a decline in labor force participation accounted for over half of the decline. The economy will avoid the full brunt of the feared fiscal cliff. Higher taxes

will result in a fiscal drag of about 1% of GDP in 2013, largely the result of the expiration of the 2% payroll tax holiday and of tax increases on upper income households. This will reduce disposable personal income by about 1.3%. The new tax rate schedule and the AMT fix are “permanent,” so

households and businesses have more clarity on future taxes. The budget deal barely dented the long-term fiscal imbalances, and

Congress failed to address the abominable tax code. There is still the potential for a “grand bargain,” but the odds appear low given the partisan divide. The US is expected to reach the debt ceiling by the end of February,

setting up another political showdown. The failure to reach a deal could lead to a government shutdown and potentially a debt default.

While short and long-term fiscal policy is a source of risk, there are positives that have the potential to yield upside surprises in 2013 and beyond. Uncertainty over tax policy and the debt ceiling has probably kept

businesses more conservative in investment and hiring than they otherwise would have been. The removal of these policy uncertainties could increase business confidence. Firming residential real estate is also a potential positive. The inventory

of unsold homes is being worked down, and prices have ticked up. An increase in construction activity would help improve employment. However, with prices still down significantly and many homeowners still with underwater mortgages, the wealth effect from a housing recovery is likely to be weak.

Annual GDP Growth

-4

-2

0

2

4

6

8

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

(%)

Employment Ratio and Unemployment Rate

50

52

54

56

58

60

62

64

66

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

% o

f Pop

ulat

ion

Empl

oyed

2

4

6

8

10

12

14

16

18

Une

mpl

oym

ent R

ate

(%)

% of Population Employed (L. Scale)Unemployment Rate (R. Scale)

The unemployment rate has fallen by 2% since it peaked, but the share of the population employed has been flat.

The increase in the ratio of the population employed from 1960 to 2000 provided a tailwind to economic growth.

Source: Bureau of Economic Analysis, Bloomberg

Source: Bloomberg

Economic growth averaged 3.1% from 1980 through 1999, but only 1.8% since 2000.

2013 consensus

forecast

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 9

Net Business Investment(% of GDP)

0

1

2

3

4

5

6

1947

1951

1955

1959

1963

1967

1971

1975

1979

1983

1987

1991

1995

1999

2003

2007

2011

(%)

Net Business Investment

Rolling 10-yr Average

US economy: The tax deal reduced the risk of a recession (cont.)

NFIB Small Business Optimism Index

75

80

85

90

95

100

105

110

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

Business investment is a key driver of long-term economic growth. The low level of investment over the last decade helps explain weak growth.

Business investment has recovered, but remains far below normal levels.

Small businesses have been dour since the financial crisis, which is a concern since they tend to drive employment growth. Sentiment took a hit following the election. It remains to be seen whether avoiding most of the fiscal cliff will improve sentiment.

Case-Shiller 10-City Housing Index

50

100

150

200

250

300

350

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

1996

= 1

00

Residential Real Estate Investment as % of GDP

0

1

2

3

4

5

6

7

8

1950

1954

1958

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

2010

(%)

The Case-Shiller housing index has recovered somewhat. However, it remains nearly a third below its peak, suggesting underwater mortgage s remain rampant. The prospects of a renewed wealth effect appear dim.

Real estate prices nearly tripled from 1996 to 2006.

Prices are currently at 2004 levels.

Source: Bureau of Economic Analysis

Source: Bureau of Economic Analysis

Source: Bloomberg

Source: Bloomberg

Residential real estate investment’s share of GDP reached an unprecedented low in this cycle. The inventory of unsold homes is slowly being cleared and household formation is improving, which should contribute to a recovery, although it will likely take years to get back to average.

Investment increased by 9% over the last four quarters.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 10

Global economic growth appears to have bottomed

2012 was another turbulent year for the global economy, but there are signs that global growth has bottomed. The willingness of the ECB to act as lender of last resort helped ease financial stress in the Eurozone, reducing the risk of an imminent break-up. Two-year Spanish bond yields fell from 6.6% in July to 2.8% at year-end, and the credit spread on banks declined. However, the structural issues are largely unresolved and the region remains in a shallow recession. The ECB’s actions have reduced near-term risk and bought fiscal policy makers more time, but the crisis is likely to remain a source of uncertainty and the recent calm could lead to complacency. Economists polled by Bloomberg project that the Eurozone economy

shrank 0.4% in 2012 and will contract further in the first half of this year. However, some leading economic indicators point to stabilization and analysts anticipate a mild recovery beginning in the second half of 2013. The periphery has made solid progress in reducing labor costs and

adjusting public finances. Current account deficits have fallen and several countries now have or are approaching primary budget surpluses. Nevertheless, deleveraging and improving competiveness will be long and painful, particularly in the absence of growth. High unemployment in the periphery is likely to persist, creating intense social and political pressures.

Fears of a hard landing in China was another source of anxiety in 2012. The Chinese economy grew an estimated 7.7% in 2012, its slowest rate since 1998. However, the slowdown appears to be ending, reducing fears of a hard landing. The HSBC manufacturing PMI hit a 19-month high in December and exports grew 14.1% year-over-year in December. While weak developed world growth will continue to weigh on growth through trade links, economists project that the economy will expand 8.1% this year. Policy makers have room to further loosen monetary and fiscal policies to support growth, but must avoid worsening existing investment and credit excesses. From a long-term perspective, China must rebalance its economy away from fixed investment and toward local consumption. The global macro environment in 2012 was dominated by the Eurozone debt

crisis and the Chinese slowdown and those issues are likely to remain the key issues in 2013 and beyond. The secular economic outlook for the developed world is likely to be weak for the foreseeable future given debt and demographic issues, while the outlook for emerging economies remains bright due to their structural advantages, although they will not be able to fully decouple from the developed world.

Consensus Economic Growth Expectations

3.5

1.0

2.2

-0.1

0.9

-1.4

1.7

7.7

5.3

-2.1

2.0

-0.8

-1.5

0.7

5.6

8.1

1.1 0.8

-4

-2

0

2

4

6

8

10

US

UK

Ger

man

y

Italy

Spai

n

Japa

n

Chi

na

Indi

a

Braz

il

(%)

2012 (e)2013 (f)

India is struggling with a bloated budget and current account deficits.

Slowing commodity demand weighed on Brazil.

The Italian and Spanish economies are projected to contract a cumulative 7.4% and 5.4%, respectively, between 2008-2013, while Germany grew 4.4%.

2013 GDP GrowthConsensus Expectations

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

May

-11

Jul-1

1

Sep-

11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

(%)

US EurozoneUK Japan

Economists have become much less sanguine for 2013 growth forecasts since 2011, although forecasts for the US and UK have stabilized.

The new Japanese government proposed a round of stimulus and encouraged the BoJ to adopt a 2% inflation target.

Source: Bloomberg

Source: Bloomberg

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 11

Global economic growth appears to have bottomed (cont.)

Bond Yields

0

1

2

3

4

5

6

7

8

9

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

(%)

Italy 2-yr Spain 2-YrItaly 10-yr Spain 10-yr

Bank Credit Default Swap Pricing

0

100

200

300

400

500

600

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Per $

10,0

00 o

f Pro

tect

ion

Europe US Asia

Chinese Retail Sales Growth

0

5

10

15

20

25

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

(%)

Chinese retail sales grew a robust 15% in 2012. Importantly, the growth rate has increased over the last four months. Chinese imports grew just 6% y-o-y in December, but import growth has improved relative to the summer months.

LTRO Draghi’s save the euro speech.

LTRODraghi’s save the euro speech.

Banking sector risk in Europe has declined, but remains elevated due to risk of further debt restructurings.

With financial stress reduced, the focus in 2013 will likely be on economic growth, implementation, and greater integration.

Citigroup Economic Surprise Index

-150

-100

-50

0

50

100

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

G-10

Emerging Markets

Economic surprise indexes spent a good part of 2012 in negative territory. However, the index has returned to positive territory in developed markets and the index fo r emerging markets is close to neutral.

Source: BloombergSource: Bloomberg

Source: BloombergSource: Bloomberg

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 12

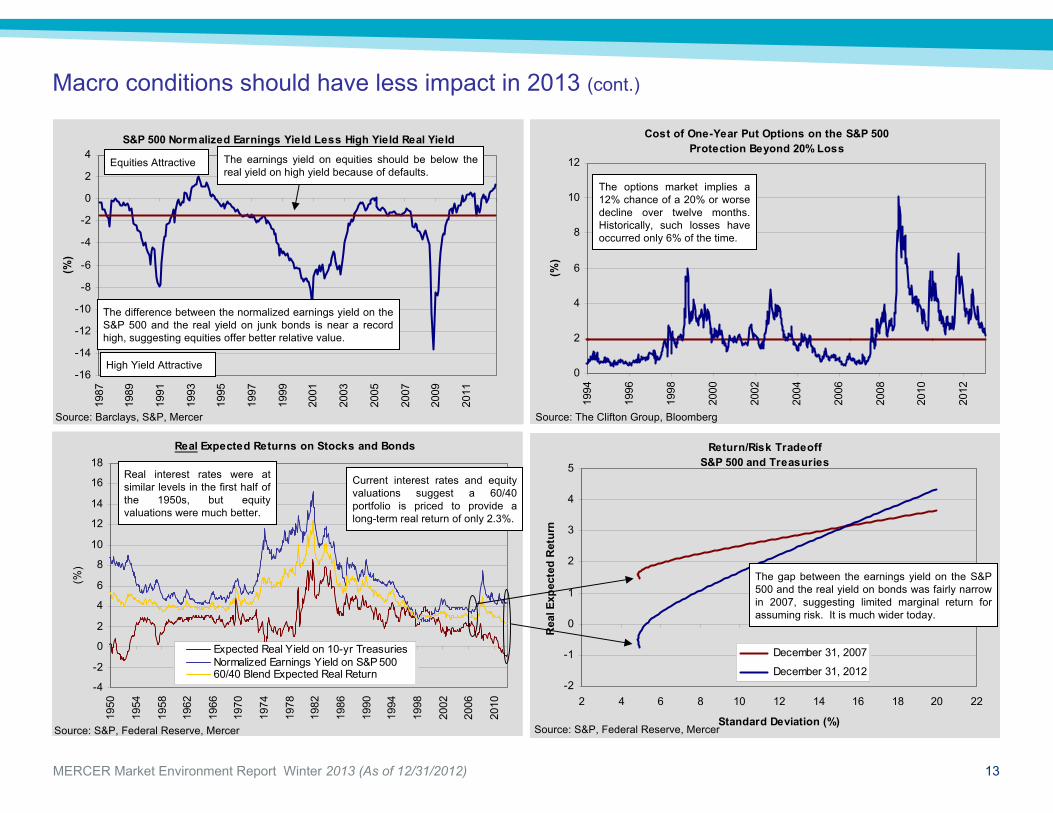

Macro risks abound; however, conditions appear to be stabilizing and we suspect the risks are well-recognized by market participants and discounted into prices. While 2013 will likely bring more flare-ups, macro factors should be a less important driver of returns. This could mean lower correlations within and across asset classes, increasing the value of diversification. Loose central bank policies in the US and in most overseas economies

assure poor real returns from safe assets. Investors desiring to preserve or grow purchasing power must prudently accept risk. Credit strategies enjoyed strong returns in 2012 as spreads plummeted.

Nevertheless, we continue to favor credit within fixed income strategies because spreads to Treasuries offer a favorable risk-to-reward. Yet with absolute yields so low, investors should not expect capital gains. Returns will largely be limited to income. While public market credit securities have limited upside, illiquidity is still

well rewarded in private credit markets. Spreads on illiquid debt securities have not compressed to the same extent as they have in public markets. Private debt partnerships and some hedge funds can capitalize on this. In this low rate world, global equities continue to offer attractive risk

premiums relative to Treasuries and credit. While equity volatility could remain high, stocks are very likely to outperform bonds over the intermediate-term even in a risky, low-growth world. Despite the strong returns from equities over the past year, we favor overweight positions to equities versus bonds. The price of tail risk protection is at a post-financial crisis low, although it

is not cheap by longer-term historical standards. Investors with long time horizons could consider selling protection should premiums rise in 2013 as a result of a market correction. A diminishment in the importance of macro should result in a re-focus by

the market on fundamental value, providing opportunities for alpha generation through asset allocation tilts and security selection.

Expected returns on bonds have plunged as a result of the financial crisis and central bank actions. Meanwhile, equities and some other riskier assets offer significantly better valuations than they did before the crisis. Institutions that have not revisited their strategic allocations in some time may wish to do so as the long-term risk-reward trade-off between stocks and bonds has changed materially over the past five years.

Macro conditions should have less impact in 2013

Average Correlation Among Risky Assets(Daily Correlation of Rolling 90-day Returns)

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2005

2006

2007

2008

2009

2010

2011

2012

Pre- and post-Lehman

S&P 500 - Equity Risk Premium Versus Long-Term Treasuries

-2

-1

0

1

2

3

4

5

6

7

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

(%)

The prospective equity risk premium over long-term Treasuries remains healthy by historical standards at 4%.

This calculation uses normalized earnings, which assumes earnings 22% less than current levels. Based on reported earnings, the risk premium exceeds 5%.

We estimate global equities price a risk premium of over 5%.

The correlation of risky assets has been much higher post-Lehman. Correlations should decline if macro worries recede.

Source: Bloomberg, Datastream, JP Morgan, Mercer

Source: Mercer, S&P, Bloomberg

Median since 1956

Note: Includes MSCI World, MSCI Emerg, Barclays High Yield, GSCI, DXY (inverse), EM fx

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 13

Macro conditions should have less impact in 2013 (cont.)

Cost of One-Year Put Options on the S&P 500Protection Beyond 20% Loss

0

2

4

6

8

10

12

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

(%)

S&P 500 Normalized Earnings Yield Less High Yield Real Yield

-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

(%)

The options market implies a 12% chance of a 20% or worse decline over twelve months. Historically, such losses have occurred only 6% of the time.

Real Expected Returns on Stocks and Bonds

-4

-2

0

2

4

6

8

10

12

14

16

18

1950

1954

1958

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

2010

(%)

Expected Real Yield on 10-yr TreasuriesNormalized Earnings Yield on S&P 50060/40 Blend Expected Real Return

Return/Risk TradeoffS&P 500 and Treasuries

-2

-1

0

1

2

3

4

5

2 4 6 8 10 12 14 16 18 20 22

Standard Deviation (%)

Rea

l Exp

ecte

d R

etur

n

December 31, 2007

December 31, 2012

The gap between the earnings yield on the S&P 500 and the real yield on bonds was fairly narrow in 2007, suggesting limited marginal return for assuming risk. It is much wider today.

Source: S&P, Federal Reserve, Mercer Source: S&P, Federal Reserve, Mercer

Source: Barclays, S&P, Mercer Source: The Clifton Group, Bloomberg

The difference between the normalized earnings yield on the S&P 500 and the real yield on junk bonds is near a record high, suggesting equities offer better relative value.

Equities Attractive

High Yield Attractive

The earnings yield on equities should be below the real yield on high yield because of defaults.

Current interest rates and equity valuations suggest a 60/40 portfolio is priced to provide a long-term real return of only 2.3%.

Real interest rates were at similar levels in the first half of the 1950s, but equ ity valuations were much better.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 14

Global equities: Valuations still attractive after 2012 gains

Global Valuations

24.6

20.7

1.5 1.1 1.73.7

2.2

12.7

14.613.3 13.212.112.8

9.58.07.27.6

2.2 2.72.3

0

5

10

15

20

25

30

MSCI US MSCI Europe MSCI Japan MSCI EM

P/E TrailingP/E NormalizedP/CFP/BDividend Yield

The earthquake stil l impacts the trailing 12 month earnings.

Source: MSCI, Bloomberg, Mercer

Return-On-Equity for Global Markets

-5

0

5

10

15

20

25

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

(%)

MSCI Emerg Mkts MSCI EuropeMSCI Japan MSCI US

Profitability in Europe and emerging markets is in-line with historical averages, while margins remain elevated in the US.

The dividend yield on Japanese stocks is particularly attractive relative to miserable local bond yields.

Europe trades at a sizable discount to the US on all valuation measures.

Global equities enjoyed a very good year despite the macro headwinds, an example of the unreliable link between economic growth and equity returns. The MSCI ACWI index surged 16.1% for the year, although it followed a poor 2011. MSCI ACWI earned an annualized 3.7% for the two-year period, and the five-year return, which includes the financial crisis, was -1.2%. Valuations on global equities were attractive at the beginning of the year, but

they are clearly higher now after the strong 2012. Nonetheless, valuations remain neutral to attractive on an absolute basis. In comparison to sovereign bonds and credit, the valuation of equities is compelling. The earnings outlook is an ongoing concern. In the US, profit margins are

unsustainably high. Outside the US however, margins are at or below normal levels. While earnings in Europe and emerging markets declined in 2012, it appears they have bottomed. Short-term sentiment indicators suggest that confidence has improved

considerably, which could be interpreted as a contrarian indicator. However, retail and institutional investors have been slow to move back into equities. This is a medium-term positive as the low rate environment and high risk premiums could spark a rotation back into equities, especially if the perception of macro risk declines.

MSCI World Valuations

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

P/B

0

2

4

6

8

10

12

14

16

18

20

P/C

F

P/B

P/CF

Source: MSCI, Datastream

Source: MSCI, Datastream

The P/B ratio on MSCI World is in the bottom 36% of observations since 1975, while P/CF is near the median.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 15

S&P 500 Profit Margin on Sales

0

1

2

3

4

5

6

7

8

9

10

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

(%)

Trailing 12-Months

10-Yr Moving Average

Average Since 1956

S&P 500 - P/E Ratio

0

5

10

15

20

25

30

35

40

45

50

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

Shiller's (10-yr Avg. Real Earnings)Normalized EarningsReported Earnings

US equities: Profits appear to be peaking The S&P 500 declined as much as 5.8% in Q4, but pared losses as a deal

emerged on the fiscal cliff, finishing the quarter down 0.4%. For 2012, the S&P 500 added 16.0%, marking its fourth consecutive year of gains and strongest year since 2009. There are growing signs that earnings and profit margins are topping. The

profit margin on sales ticked down from 8.5% to 8.2% during the year. Based on estimated fourth quarter earnings, reported earnings were virtually flat in 2012, while operating earnings increased only 3%. We suspect 2013 will be another lackluster year for profit growth. Productivity gains have lost steam, signaling that companies have

exhausted cost cutting as a source of profit growth. Future aggregate earnings growth will need to increasingly come from investment and hiring, which will put downward pressure on margins. Companies continue to buy back shares, which can increase earnings

per share without aggregate profit growth. Stock analysts expect double-digit operating earnings growth in 2013,

which is exceedingly optimistic. Analysts are widely-recognized as an overly optimistic bunch, so it’s doubtful that the market is pricing in such high growth.

The strong return from the S&P 500 lifted valuations in 2012. The P/E ratio on reported earnings increased from 14.5 to 16.4 for the year. This is still below the median of 17.1 since 1956. With margins so high, cyclically- adjusted earnings show a much less favorable picture for equity valuations. Based on normalized earnings, which assume profit margins decline by 22%, the P/E ratio on the index stood at 20.7, which is above the historical median of 17.1 (since 1956). Based on average 10-year real earnings (Shiller’s methodology), the P/E finished the quarter at 21.1 compared to a median of 18.9 (since 1956). While we expect profit growth to remain constrained, margins could stay

above historical norms for quite some time. The Fed’s monetary policy provides a substantial subsidy to corporations, allowing them to slash interest costs. This effect will continue to help profitability as companies re-finance higher rate debt. Further, the slack in the labor market should keep a lid on wages, which is usually the most significant cost for companies. Despite elevated cyclically-adjusted valuations, we consider US equity

valuations as neutral since high profit margins could persist for some time. We find equity valuations attractive when viewed against bond yields.

Profit margins tend to mean revert.

Margins have been trending upwards over the past two decades.

Source: S&P, Bloomberg

Source: S&P, Mercer

The trailing P/E on the S&P 500 is attractive at 16.4, but profit margins are near historical highs. The P/E on cyclically-adjusted earnings measures is higher.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 16

US equity style: Maintain quality focus, reduce growth bias In 2012, large-cap value stocks slightly outperformed growth, but since the

start of 2007, large-cap growth trounced value by a cumulative 29.7 percentage points (30.4 vs. 0.7%). At the start of the run, large-cap growth offered compelling relative valuations; however, the valuation gap has closed. While styles have a tendency to overshoot, suggesting that growth’s run could extend, we have less conviction in our previous call to overweight growth and suggest moving towards a style neutral domestic equity portfolio. We continue to suggest an overweight to quality stocks. Valuations remain

attractive, and they are well-positioned to take advantage of the Fed’s policies. Many of these companies can borrow at rates less than their dividend yields. The broader low volatility universe has less appeal because high dividend plays appear pricey relative to the market. Stocks with moderate dividend yields and growth potential offer better value than those with high yields. We continue to suggest underweighting small-caps due to relative valuations.

While small-caps slightly outperformed large-caps in 2012, they trailed on a beta-adjusted basis. Momentum appears to be shifting in favor of large-caps and given relative valuations, we suspect that this is the start of a multi-year period of small-cap underperformance.

Valuation of Russell 1000 Growth to Valueand Subsequent Performance

0.0

0.3

0.5

0.8

1.0

1.3

1.5

1.8

2.0

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

R10

00G

/R10

00V

Rel

ativ

e to

Mea

n

-20

-15

-10

-5

0

5

10

15

20

Subs

eque

nt 5

-Yr R

elat

ive

Perf

orm

ance

(%)

Valuation of R1000G/R1000VSubsequent 5-Yr Relative Return (R1000G - R1000V)

Sector Valuations - Ratio of High Quality to Low Quality(Based on Average of P/B, P/E and P/CF)

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

2.7

1995

1997

1999

2001

2003

2005

2007

2009

2011

Rel

ativ

e Va

luat

ion

ofH

igh

Qua

lity

/ Low

Qua

lity

US Equity Valuations by Capitalization

10.513.0

16.7

2.4

15.2

10.18.8

11.5

24.4

14.6

1.7

19.9

6.9

13.215.1

1.5

23.8

0

10

20

30

P/E - TrailingReported

P/E - 5 YrAverageEarnings

P/CF P/E - 1Yr.Forw ard(I/B/E/S)

DividendYield

EPS Grow th -Last 10 Yrs

Russell Top 200

Russell Midcap

Russell 2000

Quality stocks appea r attractively valued, trading below their historical premium.

Small-caps appear expensive relative to large caps based on most valuation measures. Small-caps' trailing P/E of 24 is 60% higher than that of large caps, and they trade at a 30% premium on P/CF. On forward earnings, small-caps traded at a 15% premium to large-caps.

Growth and value are trading at normal relati ve valuations.

Large-caps have grown earnings faster.

Source: Russell, Mercer

Source: Russell Source: Datastream, Mercer

There was a -0.7 correlation between the relative valuation and subsequent 5-yr return.

56.4

Value attractive Growth outperforms

Growth attractive Value outperforms

Quality attractive

Quality unattractive

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 17

Emerging market equities topped developed markets for the year

After tumbling 18.4% in 2011, emerging market stocks rebounded 18.2% in 2012, outperforming the S&P 500 by 220 basis points. Regional performance showed some dispersion, with Asian stocks rising a robust 20.8%, while Latin American equities returned just 8.7%. The macro outlook for emerging economies appears to be improving.

Earnings declined about 3.5% over the last twelve months, but appear to have bottomed after gaining 3% over the prior three months. Even after the strong rally, emerging market valuations remain compelling. Based on P/B and P/CF, emerging stocks are trading 7% below their historical median since 1996. Based on our measure of normalized earnings, they trade at a P/E of 13, a 40% discount to the US. The best values in emerging markets come from the more cyclical, globally-

sensitive sectors, such as energy. Locally-focused sectors (e.g., consumer staples) trade at large premiums to developed markets. Emerging market equities are likely to remain highly sensitive to the macro

sentiment given their high beta. However, they appear attractively valued in absolute and relative terms and remain priced to outperform developed market equities. We continue to suggest an overweight.

MSCI Emerging MarketsP/E Ratios

0

5

10

15

20

25

30

35

40

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Normalized P/ETrailing P/E

Valuation of MSCI Emerging Markets to Developed Markets(Based on an average of P/E, P/B and P/CF)

-60

-50

-40

-30

-20

-10

0

10

20

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

(%)

Emerging markets are trading in-line with their historical median since 1996. However, they traded at a normalized of P/E of just 13, which is 15% below our estimate of fair value.

Based on a mix of valuation measures, EM stocks are trading at a 10% discount to developed equities. They are trading in-line with Japanese and European stocks, but at a 28% discount to US stocks.

The historical discount has been larger, but developing economies are structurally more sounder than they were in the 1990s, and developed economies are less stable.

Discount/Premium of MSCI Emerging Markets Sectors to Developed Markets Sectors

(Based on an average of P/B, P/CF, and P/E)

-30-20-10

010203040506070

Hea

lth C

are

Con

s. S

tapl

es

Tele

com

Fina

ncia

ls

Indu

stria

ls

Con

s. D

isc.

Mat

eria

ls

Utili

ties

I.T.

Ener

gy

Inde

x

(%)

Investors might be overpaying for exposure to local consumption. Sectors that have more exposure to local growth are trading at significant premiums to developed world equities, while more cyclical, global sectors are trading at discounts.

Source: BloombergSource: Datastream, Mercer

Source: Bloomberg, Mercer

Health care and consumer staples trade at P/E ratios of 29 and 26, respectively, in emerging markets.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 18

European Equity Valuations

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

P/B

0

2

4

6

8

10

12

14

16

18

P/C

F

P/B

P/CF

International developed equity valuations remain more attractive than US

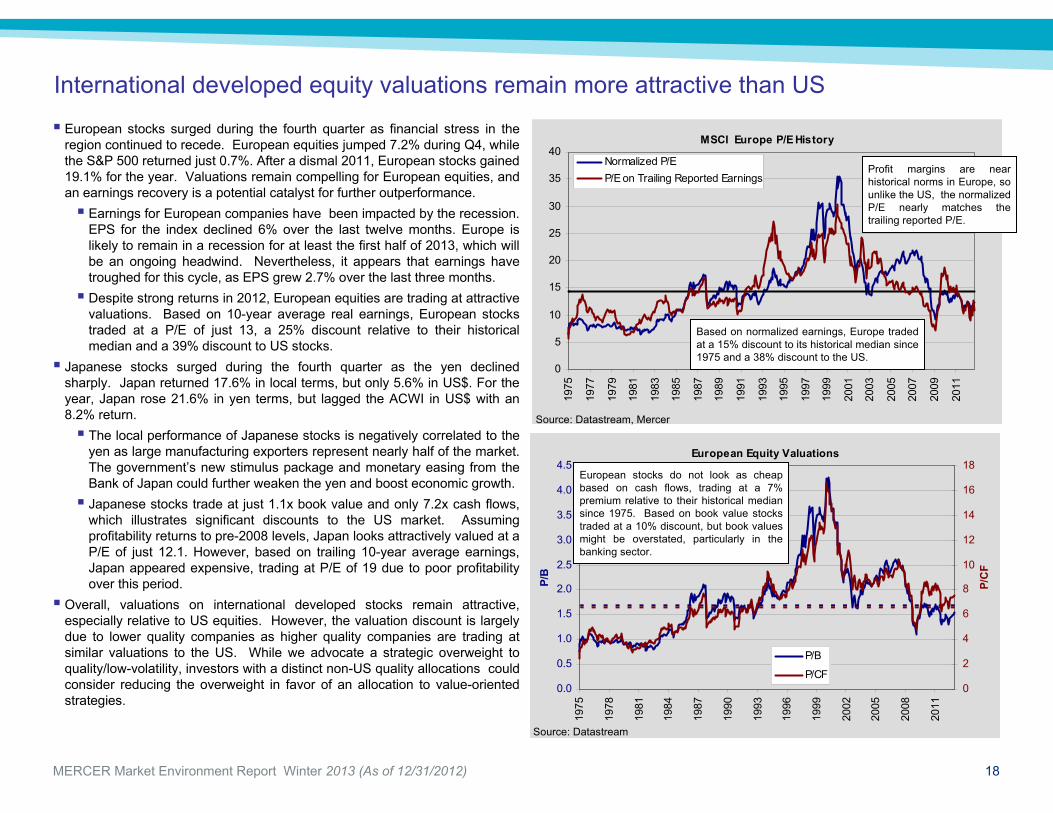

European stocks surged during the fourth quarter as financial stress in the region continued to recede. European equities jumped 7.2% during Q4, while the S&P 500 returned just 0.7%. After a dismal 2011, European stocks gained 19.1% for the year. Valuations remain compelling for European equities, and an earnings recovery is a potential catalyst for further outperformance. Earnings for European companies have been impacted by the recession.

EPS for the index declined 6% over the last twelve months. Europe is likely to remain in a recession for at least the first half of 2013, which will be an ongoing headwind. Nevertheless, it appears that earnings have troughed for this cycle, as EPS grew 2.7% over the last three months. Despite strong returns in 2012, European equities are trading at attractive

valuations. Based on 10-year average real earnings, European stocks traded at a P/E of just 13, a 25% discount relative to their historical median and a 39% discount to US stocks.

Japanese stocks surged during the fourth quarter as the yen declined sharply. Japan returned 17.6% in local terms, but only 5.6% in US$. For the year, Japan rose 21.6% in yen terms, but lagged the ACWI in US$ with an 8.2% return. The local performance of Japanese stocks is negatively correlated to the

yen as large manufacturing exporters represent nearly half of the market. The government’s new stimulus package and monetary easing from the Bank of Japan could further weaken the yen and boost economic growth. Japanese stocks trade at just 1.1x book value and only 7.2x cash flows,

which illustrates significant discounts to the US market. Assuming profitability returns to pre-2008 levels, Japan looks attractively valued at a P/E of just 12.1. However, based on trailing 10-year average earnings, Japan appeared expensive, trading at P/E of 19 due to poor profitability over this period.

Overall, valuations on international developed stocks remain attractive, especially relative to US equities. However, the valuation discount is largely due to lower quality companies as higher quality companies are trading at similar valuations to the US. While we advocate a strategic overweight to quality/low-volatility, investors with a distinct non-US quality allocations could consider reducing the overweight in favor of an allocation to value-oriented strategies.

MSCI Europe P/E History

0

5

10

15

20

25

30

35

40

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

Normalized P/EP/E on Trailing Reported Earnings

Based on normalized earnings, Europe traded at a 15% discount to its historical median since 1975 and a 38% discount to the US.

European stocks do not look as cheap based on cash flows, trading at a 7% premium relative to their historical median since 1975. Based on book value stocks traded at a 10% discount, but book values might be overstated, particularly in the banking sector.

Source: Datastream

Source: Datastream, Mercer

Profit margins are nea r historical norms in Europe, so unlike the US, the normalized P/E nearly matches the trailing reported P/E.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 19

International developed equity valuations remain more attractive than US (cont.)

Discount/Premium of MSCI EMU to MSCI US (Based on average of P/E, P/B, P/CF)

-70

-60

-50

-40

-30

-20

-10

0

10

Tele

com

Utili

ties

Con

s. D

isc.

Ener

gy

Mat

eria

ls

Fina

ncia

ls

Indu

stria

ls

Hea

lth C

are

Con

s.St

aple

s

Info

. Tec

h

Inde

x

(%) Cyclical and “local” stocks are

trading at a significant discount to the US. These stocks are most exposed to break-up risk and the recession. Given these discounts, deep value managers hold some appeal.

Defensive sectors and those with a global orientation are trading in-line with their US counterparts.

The index trades at a sizable discount to the US based on a mix of valuation measures

Global Equity Valuations

11.5

1.43.7

18.913.3

n/a

24.6

13.612.9

14.4

7.67.17.2

8.4

0.81.11.5

2.3

2.22.9

0

5

10

15

20

25

30

Large Small Large Small

Europe Japan

P/E Trailing P/E Forw ard

P/CF P/B

Div. Yield

Japanese Equity Valuations

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

P/B

0

5

10

15

20

25

30

P/C

F

P/B

P/CF

Shiller's P/E Ratio for MSCI Japan (Based on 10-year Average Real Earnings)

0

20

40

60

80

100

120

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

PE

0

2

4

6

8

10

12

RO

E (%

)

PE (L. scale)

ROE (R. scale)

Historical valuation comparisons must be made with caution for Japan due to the enormous bubble that inflated in the 1980s. Still, the P/B ratio is in the bottom decile of historical observations, while the P/CF ratio is in the bottom third.

As in the US, European small-caps appear richly-valued relative to large- caps. Japanese small-caps, however, are relatively attractive.

Source: Bloomberg

Source: Datastream

Source: Datastream

Source: Datastream

Shiller’s P/E ratio on Japan remains high at 19 due to low profitability. Profitability is slowly recovering, but has not yet reached pre-bust norms.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 20

Bond Yields

0.9

1.7 2.32.7

6.1

2.2

5.5

3.7

1.0

2.22.7

8.4

2.8

6.6

1.9

3.83.73.0

4.0

7.56.7

0

2

4

6

8

10

Agg. Treas GSE MBS I/G Corp HY Corp Munis Local EMD

(%)

Dec-12 Dec-11 Dec-10

Treasury Yield Curve

-2

-1

0

1

2

3

4

5

3 mo 6 mo 1 yr 2 Yr 3 Yr 5 yr 7 yr 10 yr 20 yr 30 yr

(%)

Treasuries at 12/31/10 TIPS at 12/31/10Treasuries at 12/31/11 TIPS at 12/31/11Treasuries at 12/31/12 TIPS at 12/31/12

Fixed income: Credit rallied in 2012, but little upside remains The Barclays Treasury index returned 2.0% in 2012, its lowest annual return

since 2009. Several macro factors in Europe and the US contributed to yield volatility throughout the year. The 10-year Treasury yield reached a record low of 1.47% in June and rose to 1.78% by year end, only 9 bps lower than where it started the year. While nominal yields did not move much in 2012, real yields on TIPS plunged

deeper into negative territory on higher inflation expectations. At year end, 10-year TIPS yielded -0.67%, down from -0.07% at the start of the year. The inflation breakeven rate on 10-year TIPS increased by 49 bps to 2.45%. Extremely low yields mean Treasury investors are all but certain to lose

purchasing power over the intermediate-term. The Fed does not intend to raise short-term interest rates until unemployment reaches 6.5% or inflation climbs above 2.5%, which should anchor the yield curve, and the Fed will absorb a third of the new Treasury supply in 2013. While we do not expect a significant increase in rates over the short-term, the risks are decidedly asymmetric. Over 1-year, the 10-year Treasury’s yield only needs to rise to 2.0% for capital losses to offset the yield. Apart from liability hedging purposes, there is little reason to take significant duration risk in Treasuries. A big story in 2012 was the continued improvement in credit strategies.

Investment grade bonds surged 9.8% for the year, as the yield on the Barclays I/G Corporate index fell by 103 bps, finishing the year at only 2.7%. It’s unlikely that yields will decline materially from present levels, meaning that future upside will be limited to the current yield less the impact of downgrades/defaults. Credit still offers reasonable value relative to Treasuries, as the spread of 1.4% is above the 1% historical median. We continue to favor credit over Treasuries. Should Treasury yields rise, we expect the spread to narrow further, cushioning losses for credit. The credit rally led to a 15.8% return for high yield bonds in 2012. The yield

on junk bonds finished at a record low 6.1%. Net of full cycle typical default losses, high yield bonds are priced to return only 3% to 4%. High yield bonds still appear reasonably attractive relative to Treasuries with a spread of 5.1%, and the short-term default outlook is favorable. An intermediate-term concern is that new issuance quality has worsened. Of course, high yield tends to behave more like equities than bonds, and equities currently offer a much better risk-to-reward for longer-term investors. Private credit investments still have appeal. Spreads on illiquid debt

securities have not compressed to the same extent as they have in public markets.

Source: Federal Reserve

The premium for extending duration remains small by historical standards. Real yields on TIPS are negative out to nearly 20 years.

Source: Barclays

Yields in several fixed income markets finished the year at or near record lows.

Yields declined across all fixed income sectors during 2012.

Despite the Fed’s purchases of MBS under QE3, the yield increased during the fourth quarter.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 21

High Yield Bond Credit Spread

0

2

4

6

8

10

12

14

16

18

20

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

(%)

Investment-Grade Corporate Bond Credit Spread

0

1

2

3

4

5

6

7

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

(%)

Fixed income: Credit rallied in 2012, but little upside remains (cont.)

Although absolute yields on investment grade are near record lows, the spread remains 39 bps above the historical median.

Source: Barclays

Ultra-low yields give investors little cushion to protect against future interest rate increases. Tilting toward corporate bonds improves the picture, but they suffer from the same dynamic as well.

Fed policy is likely to anchor rates over the next few years. However, if the 5-year returns to its 2011 high of 2.3% over three years, it would mean losses of 0.3%, annualized.

Source: Bloomberg, Mercer

Source: Barclays

The spread on junk bonds decreased 188 bps in 2012 to 5.1%, only 0.2% above the historical median. A benign default outlook and a continued search for yield should support low spreads.

Corporate Bond Issuance by Year

613696

1,020

843

132

1,114

880

1,074

809750

977

733

59 132 101 149 148 66

288

163244

354

0

500

1,000

1,500

2,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$ B

illio

ns Investment Grade

High Yield

EndingYield (%) 1 Yr (%) 2 Yr (%) 3 Yr (%)

5-Year Treasury (YTM = 0.72)0.3 2.4 1.3 1.00.8 0.3 0.6 0.71.0 (0.4) 0.3 0.51.5 (2.3) (0.4) 0.22.0 (4.2) (1.2) (0.1)2.5 (6.1) (1.9) (0.5)

Breakeven Yield 0.9 1.2 1.810-Year Treasury (YTM = 1.78)

1.5 4.2 2.8 2.41.9 0.7 1.3 1.52.0 (0.1) 0.9 1.32.5 (4.1) (0.9) 0.23.0 (8.0) (2.7) (0.9)3.5 (11.7) (4.5) (2.0)

Breakeven Yield 2.0 2.3 2.6

Annualized Return Over Period

2012 saw record issuance of both investment grade and high yield bonds. Much of this was used to refinance existing debts at lower rates, which improves cash flow.

Source: Bloomberg

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 22

2012 Performance of Foreign Currencies Versus the Dollar

-15

-10

-5

0

5

10

Mex

ican

Pes

o

Kore

an W

on

New

Zea

land

Dol

lar

GB

Poun

d

Taiw

an D

olla

r

Can

adia

n D

olla

r

Swis

s Fr

anc

Aust

ralia

n D

olla

r

Euro

Chi

nese

Yua

n

Indi

an R

upee

Braz

ilian

Rea

l

Japa

nese

Yen

(%)

Currencies: A race to the bottom

Source: Bloomberg

The yen declined 10.1% in the fourth quarter alone, while the euro added 2.6% in Q4.

On a trade-weighted basis, the dollar declined 0.8% in the fourth quarter and finished the year down 2.0%. The euro appreciated by 2.6% against the dollar during the quarter, reflecting the further easing of financial tensions. The most notable action was for the yen, which plunged 10.1% in Q4 as newly elected Prime Minister Shinzo Abe introduced fiscal stimulus and pressured the Bank of Japan to increase its inflation target. It was generally a good year for emerging market currencies, with the Indian rupee and Brazilian real being notable exceptions. Central bank policies are likely to continue to heavily influence currency

markets in 2013. While the Fed pursued an aggressive QE program in 2012, the negative effect on the dollar was relatively muted as other major central banks took part in monetary easing programs. The expansion of QE3 reinforces monetary policy risks for the dollar.

The Fed continues to be among the most aggressive of global central banks. On the other hand, the dollar remains undervalued against most developed currencies based on relative purchasing power parity. The US still has a very high current account deficit, but the boom in natural gas should help reduce this due to falling net energy imports. The long-term bearish case for the yen is compelling in light of the

country’s weak growth, oppressive debt loads and rising trade deficit. However, the country is still experiencing mild deflation (which is bullish) and it is unclear how aggressive the Bank of Japan will actually be in attempting to hit its new 2% inflation target. We also caution that the short yen trade has quickly become a favorite among currency speculators, hinting the potential for a reversal. The outlook for the euro is mixed, with a bias toward weakness. The ECB

has stepped up and reinforced its role as lender of last resort, which has reduced systemic risk, but unlike the Fed, it has resisted monetary stimulus and still has a 0.75% overnight lending rate. Of course, the economic challenges facing the Eurozone are daunting. Further, the euro appears fairly expensive once again on purchasing power parity. These factors are likely to leave the currency susceptible to declines. The Australian dollar has been a favorite among speculators and carry

traders because it is one of only a few developed economies offering a positive real return. However, the overvaluation based on purchasing power parity exceeds 30% relative to the US dollar.

Central Bank Balance Sheet Growth

50

100

150

200

250

300

350

400

450

500

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

(1/2

008=

100)

US EMUUK JapanSw itzerland

Source: Bloomberg

The central bank balance sheets of the US, UK and Switzerland have more than tripled since the crisis. The ECB and BoJ have been more restrained.

The euro’s modest appreciation for the year bucked the consensus call for depreciation.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 23

Net Speculative Positioning in Euro and JPY

-250

-200

-150

-100

-50

0

50

100

150

200

2005

2005

2006

2006

2007

2007

2008

2008

2009

2009

2010

2010

2011

2011

2012

2012

Bill

ion

Con

trac

ts

EURJPY

Currency Valuation Versus US Dollar(Based on Relative PPP)

-30

-15

0

15

30

45

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

(%)

Euro UK PoundYen Sw iss Franc

Source: Bloomberg

The euro trades at about a 14% premium to the dollar based on relative purchasing power parity.

Dollar Cheap

Dollar Expensive

Global Central Bank Rates

0

2

4

6

8

10

12

14

16

2007

2008

2009

2010

2011

2012

(%)

US EuropeJapan UKChina IndiaBrazil

Real Interest Rates and Current Account Balances

-4

-3

-2

-1

0

1

2

3

4

Switz

erla

nd

Taiw

an

Chi

na

Kore

a

Japa

n

Euro

zone

Mex

ico

Braz

il

US

UK

Can

ada

Indi

a

Aust

ralia

Rea

l Int

eres

t Rat

e (%

)

-12

-9

-6

-3

0

3

6

9

12

Cur

rent

Acc

ount

Bal

ance

(% o

f GD

P)

Real 3M rate (LS)

Current Account Balance (2012F, RS)

Currencies: A race to the bottom (cont.)

Speculative short positions in the yen are at their highest since the carry trade craze in 2006/07.

Traders have slashed their short positions in the euro since the OMT program.

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

The Eurozone current account balance is close to flat.

All but three countrie s shown here have negative real interest rates.

Japan’s real interest rates are higher than those in most other developed economies due to low inflation.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 24

Fundamentals supportive of local currency emerging debt Local currency emerging market debt posted strong returns in 2012. The

JPMorgan GBI-EM Global Diversified index appreciated 16.8% as declines in local yields and currency appreciation boosted returns. The 5.45% yield on local emerging debt is at an all time low; however,

fundamental factors remain supportive relative to developed economies. Emerging governments are less indebted than developed governments

and the credit quality of their debt has been steadily improving. While inflation risks are higher in emerging economies relative to most

developed peers, the credibility of many emerging central banks has improved as a result of successful policies targeted at containing inflation. Volatile commodity prices could have an outsized effect on short-term inflation; however, in the long run, the trend of converging inflation in emerging and developed economies should continue. Strong growth rates, favorable current account balances and currency

reserves could lead to currency appreciation for emerging economies. A cause of concern is that yields are now approaching levels that may cause

“growth asset” investors to question the use of emerging debt as a substitute for equities.

Local Currency EM Debt Yields and Inflation

0

2

4

6

8

10

12

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

(%)

Yields

Inflation

Real yields on local currency EM debt are positive; however, they have contracted to approximately 1% based on projected 12- month inflation.

Source: Datastream, IMF, JPMorgan, Mercer

Government Debt (% of GDP)

0

20

40

60

80

100

120

2000

2002

2004

2006

2008

2010

2012

2014

2016

(%)

Developed

Emerging

Emerging market debt burdens are likely to decline over the next several years given fast GDP growth rates.

Source: IMF

Emerging Market Debt Credit Spread(US$ Denominated)

0

2

4

6

8

10

12

14

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

(%)

Source: Barclays

Credit spreads on US$ denominated EM debt have fallen below historical averages, although credit quality has been improving. We continue to favor local currency EM debt over US$ debt.

MERCER Market Environment Report Winter 2013 (As of 12/31/2012) 25

The global real estate securities market performed well during the fourth quarter of 2012 with all regions posting positive returns. The FTSE EPRA NAREIT Developed index gained 5.8% during the fourth quarter and ended up 28.7% for 2012. The US REIT benchmark gained 2.6% for the quarter and 18.1% for the year. As of December 31, 2012, the US REIT dividend yield stood at 3.7% while

the global property securities dividend yield was 3.6%. Movements in REIT share prices continued to be influenced by the risk-

on/risk-off shifts of the broader equity market. According to Green Street Advisors, US REITs trade at a 13% premium