Embed Size (px)

Citation preview

Market Discipline in Regulating Bank Risk: New Evidence from the Capital MarketsAuthor(s): Robert B. Avery, Terrence M. Belton and Michael A. GoldbergSource: Journal of Money, Credit and Banking, Vol. 20, No. 4 (Nov., 1988), pp. 597-610Published by: Ohio State University PressStable URL: http://www.jstor.org/stable/1992286 .

Accessed: 15/11/2013 08:08

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Ohio State University Press is collaborating with JSTOR to digitize, preserve and extend access to Journal ofMoney, Credit and Banking.

http://www.jstor.org

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

ROBERT B. AVERY TERRENCE M. BELTON MICHAEL A. GOLDBERG

Market Discipline in Regulating Bank Risk: New Evidence from the Capital Markets

THE DRAMATIC RISE IN BANK FAILURES over the past several years and the accompanying perception of increased bank risk taking have raised concerns about the current system of bank supervision and regulation. In response to these concerns, considerable attention has been given to the use of market discipline to complement bank examinations in regulating bank risk exposure. Recently, this attention has focused on holders of subordinated notes and debentures under a view that these investors-rather than equity holders or uninsured depositors-are best able to complement the current supervisory system.

The potential for bank subordinated notes and debentures (SNDs) to enhance bank supervision through market discipline is a key factor behind a recent proposal by the FDIC to increase total bank capital requirements from 6 to 9 percent of assets, with SNDs permitted to satisfy up to one-third of this requirement.l 2 This study attempts to evaluate the potential for SNDs to impose market discipline by analyzing

The authors gratefully acknowledge the comments of Mark Flannery, Christopher James, and especially George J. Benston. Excellent research assistance was provided by Oscar Barnhardt and Bryan Davis. This research was conducted while the authors were on the staff of the Board of Governors of the Federal Reserve System. The opinions in this paper are those of the authors and do not necessarily reflect the opinions of either the Board of Governors or the authors' current institutions or their staffs.

"'Market Discipline for FDIC-insured Commercial Banks," Federal Register, vol. 50, no. 87 (May 6, 1985), pp. 19088-89.

2Market discipline is also an important element for current proposals on a risk-based capital standard. Under this standard banks will have incentives to reduce portfolio risk (or increase capital) if the capital markets require sufficient premiums for bank risk. See "Capital Maintenance: Supplemental Adjusted Capital Measures," Federal Reserve System Docket No. RX567.

ROBERT B. AVERY is associate professor, Cornell University. TERRENCE M. BELTON is senior econo- mist at the Federal Home Loan Mortgage Corporation. MICHAEL A. GOLDBERG is vice president for f nancial analysis, Federal National Mortgage Association.

Journal of Money, Credit, and Banking, Vol. 20, No. 4 (November 1988) Copyright i' 1988 by the Ohio State University Press

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

598 : MONEY, CRED1T, AND BANKING

the default-risk premium on SNDs against generally accepted measures of bank risk, such as those found important in objective bank failure models. The study also seeks to determine whether market discipline imposed through SNDs is consistent with bank regulatory agency objectives-a basic premise of the FDIC proposal.

One aspect of SNDs that makes them an attractive source of market discipline is that holders of these instruments are typically subject to a larger risk of loss than uninsured depositors. Market discipline by uninsured depositors appears limited by (1) these depositors' ability to withdraw funds quickly once a problem situation becomes known, and (2) by the fact that they typically receive de facto insurance coverage when the FDIC uses the method of purchase and assumption (P/A) to resolve a problem situation. In contrast, subordinated debt can be a source of funding that cannot be withdrawn during adversity and is generally not assumed by the purchasing bank in a P/A transaction. Thus, subordinated lenders are generally subject to greater risk than uninsured depositors.

In addition to SND-holders, a bank's shareholders are also subject to risk. However, shareholders may beneElt at the expense of both the FDIC and SND- holders through increased risk exposure.3 As a consequence, because both the FDIC and SND-holders face moral hazard, and both have claims that, de facto if not de jure, are junior to those of uninsured depositors, one might expect that the discipline exercised by holders of bank subordinated debt should be comparable to that of the FDIC and consistent with the objectives of governmental regulation and prudential supervision. Indeed, this hypothesis would appear to be the primary factor under- lying the FDIC's proposal to allow subordinated notes and debentures to account for a signiElcant share of total bank capital requirements. The hypothesis will hold, of course, only if SND-holders believe they are not implicitly insured by bank regulators.

The potential for SNDs to enhance market discipline is examined in this study empirically by analyzing the interest rate spread between SNDs and Treasury securi- ties, with the latter constructed to be identical to the former in terms of maturity, coupon, and call privileges. This spread, or default-risk premium, is modeled as a function of various balance-sheet measures of risk, Moody's and Standard and Poor's bond ratings, and an index proposed by the FDIC for the pricing of risk-based deposit insurance. The FDIC Index is a weighted average of several ratios computed from an institution's statement of condition and income reports that presumably reflect the regulators' best estimates of those factors influencing bank risk. The weights were constructed by the FDIC so that the index is fairly highly correlated with conEldential examiner ratings of individual commercial banks. By way of preview, the study finds that SND risk premiums are weakly related to Moody's and Standard and Poor's ratings, but uncorrelated with the FDIC Index and any balance-sheet variables. Moreover, the FDIC Index of bank riskiness is found to be negatively related to the public bond ratings. These fIndings suggest that in the

3The FDIC and SND-holders face moral hazard in that greater risk taking by banks results in greater expected costs to these liability holders without offsetting gains. By contrast, shareholders receive expected returns that are in excess of their risk-adjusted levels. Kareken and Wallace (1978), Sharpe ( 1978), and others have analyzed this moral hazard problem from the perspective of the FDIC and the bank's shareholders.

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

ROBERT B. AVERY, TERRENCE M. BELTON, AND MICHAEL A. GOLDBERG : 599

current environment, the impact of the cost of SNDs on bank risk-taking behavior is unlikely to coincide with the directions desired by bank regulators.

RESEARCH METHODOLOGY

Bank-issued capital notes and debentures are forms of indebtedness that may qualify as secondary components of bank capital when (1) the note and debenture clearly states on its face that it is not a deposit and is not insured by the FDIC; (2) the instrument is subordinated to the claims of depositors; (3) the instrument has an original weighted average maturity of at least seven years; and (4) the instrument may not be redeemed early without the prior written approval of the appropriate bank supervisory agency. In addition to bank-issued subordinated debt that is sold in the capital markets, capital notes and debentures also may be issued by the bank's holding company (BHC) with the proceeds passed through, or "downstreamed," to the bank as either equity capital or as a SND. In either case, one would expect a relationship between the perceived riskiness of the issuer and the interest rate premium paid on this type of debt. Although SNDs appear to be an attractive instrument to evaluate the potential effectiveness of market discipline, surprisingly little academic attention (with the notable exceptions of Pettway [19761, Herzig- Marx [1978], and more recently Benston et al. [19861) has been paid to this liability to date.

The current study is differentiated from previous research in several ways: First, the data base includes bank problem loans, which were unavailable from call report information prior to December 1982. Second, this study introduces a methodology to measure the default premium on subordinated debt that controls for the fact that most bank or BHC debt is callable at some time prior to maturity. Because callability effectively represents a call option written by the lender and held by the borrower, the existence of such a privilege should result in the price of the bond being less than that of a noncallable bond, where the difference between the two reflects the option premium. To account for both callability and other factors related to maturity, a model is constructed to estimate the yield on a U.S. government security with maturity, coupon, and call features that identically match those of the bank-related debt. Selected market and balance-sheet measures that previous authors have found to be important in predicting the likelihood of bank failure are then used to explain the yield differential between the observed SND and its matched default-free security.4

An analysis of the sources of bank subordinated debt indicates that this type of liability is issued predominantly at the holding cornpany level with the proceeds downstreamed to the bank.5 Because of this practice, discipline from the capital markets can be imposed on banks only if it is first imposed on the BHC. Therefore, in

4In particular, Avery and Hanweck (1984) find their measures of returns on assets, capital-to-assets, and portfolio holdings of business loans to be of statistical and quantitative importance in explaining the probability of bank failure.

SFor example, as of year-end 1984 BHCs issued more than ten times the amount of debt issued by banks ($64.1 billion compared to $6.1 billion).

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

600 : MONEY, CREDIT, AND BANKING

order to evaluate the marketZiscipline potential of SNDs, we analyze the sensitivity of the cost of this type of debt to generally accepted measures of risk that apply to the issuer (i.e., risk variables that are computed from bank data when the issuer is a bank, otherwise generated from consolidated holding company data). When the SND issuer is a BHC, however, contractual agreements between the parent and its subsidiary can exist that also affect the BHC's cost of debt. In particular, when investors view a bank subsidiary as "too large to fail," then the existence of a restriction in the bond indenture that prohibits the holding company from selling shares in its bank subsidiary without prior approval (generally two-thirds) of its debtholders may limit the FDIC's ability to merge a failing bank with a healthy bank. This may increase the likelihood that the FDIC will provide the bank with direct financial assistance and may explain an interest rate premium on BHC debt that is less than that attributable to more traditional measures of holding company risk.6 These covenants are taken into account in all the empirical models estimated in this study.

A Model of the Call Feature To determine the value of a default-free bond's call feature, a bond pricing model

is employed that is similar to the single stochastic process models of Brennan and Schwartz (1977), and Dunn and McConnell (1981).

Assume that the capital markets are perfect, securities are traded on a continuous basis, and that bond prices (B) are a function only of the short-term interest rate (r), calendar time (t), the term to maturity of the bond ( T), and its coupon (c) and call features F(t), i.e., B(r,t, T,c, F(t)). Furthermore, assume the short-term interest rate can be represented by the Ito process,

dr = ,u(r, t)dt + a(r, t)dz, ( 1)

where ,u(r,t) is the instantaneous drift of the process, a(r,t) is the instantaneous standard deviation of r, and dz a Wiener process with dz = y(t) for y(t) distributed Normal (O, 1) and E(dz) = O, E(dz2) = dt. In equilibrium, the absence of arbitrage requires that all default-free noncallable bonds satisfy the partial differential equation7

1/2 Brr(r,t)a2(r) + Br(,u(r,t)-A(t)a(r,t))-BT-Br + c = ° (2)

where A(t) is the market price of risk, which can vary over time but must be the same for all securities in any given time period. The bond must also satisfy the boundary condition that at maturity B(r,t, T,c,F(T)) equals the face value of the bond.

The structure used here is differentiated from the research cited above in that it allows both F(.) and A(.) to vary over time and ,u(.) and a(.) to depend upon both

6This clause was present in Continental Illinois Corp.'s debt outstanding and may explain why these debt holders were not disadvantaged by the FDIC's actions to save the bank subsidiary in 1984.

7For more detail the reader is referred to Brennan and Schwartz (1985).

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

ROBERT B. AVERY, TERRENCE M. BELTON, AND MICHAEL A. GOLDBERG : 601

calendar time and the interest rate. These complications are necessitated by (1) the fact that the call provisions on most BHC debt involve multiple calls at different times and prices, and (2) a desire to estimate a structure that fully exploits the current yield curve by fitting all noncallable Treasury bond prices exactly. This was accomplished by fitting a discrete difference equation approximating equation (2) with the following procedure.

The first step was to employ historical data to estimate the expected drift and variability of the interest rate process. Using one month as the minimum unit of time, the drift of the 91-day Treasury bill rate was estimated by GLS using data from 1974 through 1984 as a mean-reverting process.

rl,+l= .0046 + .9595rl, R2 = .988 (3) (.0032) (.0356) N = 96

where rl, is the one-month Treasury bill rate (in annualized terms) in period t, with coefficient standard errors shown in parenthesis. The conditional standard devia- tion of the interest rate changes were estimated separately as

rl,+l-rl,+l | =- .0046 + .1149rl,. R2 = .24 (4) (.0020) (.0 1 94) N = 1 1 2

These two equations define the discrete analogs of ,u(r,t) and a(r,t). The discrete analogs of calendar time risk premiums, A(t)a(r, t), were then computed by solving the Treasury yield curve at the time BHC debt prices were measured (December 1983 and 1984) for a series of one-month forward rates, and subtracting the expected rates generated from formula (3) above, i.e., (1 + rtO)t/(l + r' 1O)' l-(1 + EO(rl,)), where rJ is the i-period bond rate in period j (in monthly terms) and Eo(rl) is the expected one-month rate at period t as forecast from period 0.

Finally, the price of a series of T-period default-free callable Treasury bonds was estimated by solving a series of T linked difference equations embedded with the above drift, variability, and risk-premium parameters using recursive dynamic sto- chastic programming. The solution relies on (1) the assumption that the bond is called whenever the bond price exceeds the call price, and (2) the one-period expected yield from a callable bond, taking into account the probability it will be called, is the same as the expected yield on a noncallable bond. The risk premium for a callable BHC security was then computed as the difference between the security yield to maturity and the yield estimated (as above) for the matched Treasury securities. The risk premiums for noncallable BHC securities were computed directly as the differ- ence between their yields to maturity and those of Treasury securities with the same maturity.

Ihe Empirical Model The empirical model estimated, while not derived explicitly from structural

assumptions, contains most features typically employed in past empirical studies of

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

602 : MONEY, CREDIT, AND BANK1NG

bank risk. Default premiums on publicly traded SNDs are modeled as functions of issue-related features-such as sinking fund provisions, maturity structure, issue size, and callability and variables representing the underlying risk of the holding com- pany. In addition, we include a dummy variable to control for the potential influence of restrictive bond covenants on the cost of BHC debt.8 The inclusion of the issue-related variables in the model is primarily to control for their impact on bond pricing, with the primary concern of the paper on variables representing bank risk.

By necessity the study focuses on the 100 largest U.S. BHCs, as these are the only ones with publicly traded SNDs. Data were gathered on all BHC or bank SNDs which were publicly traded (NYSE, AMEX, or OTC) with quoted sale or bid prices (by Moody's or Standard and Poor's) as of 12/31/83 or 12/31/84. This produced 168 issues for 85 BHCs. To make each BHC debt issue as homogeneous as possible, we dropped from the sample all zero coupon or issues subordinated to other SNDs. This reduced the sample to 137 issues drawn on 71 BHCs. Virtually all of these bonds were issued against the BHC rather than the bank and all were issued by a BHC in the top 100 in size as of 12/3 1/ 84. Although there was a fair amount of heterogeneity in terms of maturity, coupon, issue size, and callability, two-thirds of the issues were callable at some point and most of these had sinking fund provisions. The study's dependent variable was formed by first computing the price of a Treasury bond identical in maturity and callability to each issue and solving for the difference in yield to maturity from that actually quoted for each BHC issue. These premiums were computed using 12/31/83 and 12/31/84 SND prices and Treasury yields. The dependent variable used is the average premium of all outstanding issues for each BHC for each year. Hence, the data set is a pooled time series with two observations for each BHC. Issues were pooled in order to reduce the variability in premiums that is unrelated to holding company risk characteristics.

Variables representing BHC risk were drawn from three different sources. First, ratings data were gathered from two bond-rating companies Moody's and Stand- ard and Poor's-for the debt issues of each BHC.9 Second, balance-sheet and income data were drawn from the Bank Holding Company Financial Supplement (FR-Y9). These data represent the financial statements of the entire holding company including both bank and nonbank subsidiaries. Third, a few variables not available from FR-Y9 (e.g., past due and nonperforming loans, unconsolidated bank subsidiary assets) were constructed from bank Call and Income Reports by aggregating all banks within a holding company. Definitions of all variables used in the study with their sample mean statistics are shown in Table 1.

Of necessity, the selection of the specific set of variables used to measure bank risk is somewhat arbitrary. Previous reseach in two different areas was utilized to motivate the choice of balance-sheet variables. First, an index of bank risk proposed by the FDIC for use in setting risk-related deposit insurance premiums was used. This index which combines publicly available data on capital adequacy, loan quality,

8Fourteen BHCs, or 19.7 percent of the BHCs in our sample, had bond indentures containing these . .

restrlctlve covenants. 9Technically each issue could be separately rated. In reality, however, all notes and debentures of the

same BHC with equivalent subordination status had the same rating.

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

TABLE I

DEFINITIONS OF VARIABLES

Mean

YPREM' Mean risk premium on BHC debt defined, for each holding com- 129.2 pany, as the mean yield to maturity on all outstanding debt issues minus the mean imputed yield to maturity of a default-free Treasury bond with identical call provisions and maturity. Measured in basis points.

MATURlTYl Average months to maturity of outstanding issues of each holding 108.0 company.

MA TURl TY2 Equals 0 for all issues with remaining maturity less than 60 months; 51.7 equals MATURlTYI for all other issues.

SlNKING Average percent of issues required to be retired prior to maturity. 25.5 SALE Fraction of outstanding issues with quoted bid (versus sale) prices. .51 lSSUE Average issue size, $ millions. 53.1 COZNT EqualslifanySNDofaBHCcontainsarestrictionprohibitingthe .19

disposition of shares of bank subsidiaries without prior approval of debt holders; equals 0 otherwise.

LOGTA Natural logarithm of BHC total assets.2 16.2 D1983 Equals 1 in 1983; 0 in 1984. .50 FDIC lndex Calculated as .818-15.1 X CAPITAL + 21.1 X OD90 + 26.5 X .06

NA CC+ I 7.7 X RENEG + 15.1 X NCH-34.7 X ROA (See below variable deElnitions).

CAPlTAL Ratio of BHC primary capital (equity + loan loss reserves) to BHC .061 total assets.23

OD90 Ratio of consolidated bank loans and lease financing receivables .003 past due 90 days or more and still accruing to total bank assets.34

NACC Ratio of consolidated bank nonaccruing loans and lease financing .011 receivables to total bank assets.34

PCTBNK Ratio of the sum of individual bank subsidiary total assets including .875 intercompany transactions4 to the ratio of BHC total assets.2

RENEG Ratio of consolidated bank renegotiated troubled debt to total bank .001 assets.34

NCH Ratio of BHC net chargeoffs to BHC total assets.23 .003 ROA Annual rate of return on BHC assets.23 .007 FROA Estimated variance of BHC net income to total assets (estimated .071

using 14 semiannual observations over 1978- 1984.2 LlQUlD Ratio of consolidated bank U.S. Government and agency securities .135

plus cash items in process of collection, vault cash and reserves at Federal Reserve Bank, to total bank assets.34

C&l BHC ratio of commercial and industrial loans to total loans.23 .350 1. Each variable isconstructed fortwo pointsin time (yearwnd 1983and yearwnd 1984)foreach holdingcompany. Thefirst six variables were constructed for each holding company and each point in time by averaging over all issues outstanding at that point in time. 2. From FR-Y9. 3. Averaged over previous two years. 4. From Consolidated Call and Income Repons.

and earnings '° has been shown to reflect examiner ratings of individual commercial banks with a fairly high degree of accuracy.ll Second, variables shown in previous studies to be important explanatory variables in predicting bank failure are used.

"'The FDIC proposes to compute this index using bank data. This study constructs the index at the holding company level. See Table I for the exact definition.

"See Hirschorn (1986). The index is based on a probit model fit to predict which banks would be on the FDIC's problem bank list (banks with CAMEL ratings of 4 and 5). This problem list is confidential information available only to bank regulators. Hence, although the variables used in the FDIC Index are publicly available, the weights used in the index reflect confidential data. Hirschorn reports that the

ROBERT B. AVERY, TERRENCE M. BELTON, AND MICHAEL A. GOLDBERG : 603

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

604 : MONEY, CREDIT, AND BANKING

These include the variables used in the FDIC Index as well as measures of liquidity, earnings variability, and the ratio of commercial and industrial loans to total loans. 12

EMPIRICAL RESULTS

Table 2 presents some descriptive statistics on the mean risk premiums paid by bank holding companies on their notes and debentures in 1983 and 1984. Categories 1 to 4 shown in the table refer to the AAA, AA, A, and below-A-rated holding companies, respectively, for ratings made by Moody's and Standard and Poor's. For the FDIC Index, bank holding companies were rated according to the rating scheme proposed by the FDIC for purposes of its risk-based insurance program, and then ranked by quartiles. Mean premiums (in basis points) for the 25 percent of holding companies rated as least risky are shown in row 1; mean premiums for the second and third quartiles are shown in rows 2 and 3, respectively, while the holding companies rated in the most risky quartile are shown in row 4 of Table 2.

Although a fair amount of variability exists between the premiums paid by holding companies within each risk category, Table 2 indicates that the premiums are increasing in Moody's and Standard and Poor's categories and that mean differences between categories are generally statistically significant. No such conclusion holds for the FDIC Index which indicates that mean premiums actually decrease as the estimated riskiness of the holding company increases. The mean premium paid by holding companies ranked in the least risky FDIC category equals 168 basis points; the premium for holding companies in the most risky category equals only 110 basis points. The correlation coefficient between Moody's and the FDIC Index equals a statistically insignificant-.15; between Standard and Poor's and the FDIC Index equals-.18. The latter is significant at the 0.10 level suggesting that, if anything, a negative relationship exists between these two risk measures. By contrast, Moody's and Standard and Poor's ratings are positively related with a correlation coefficient equal to 0.85.

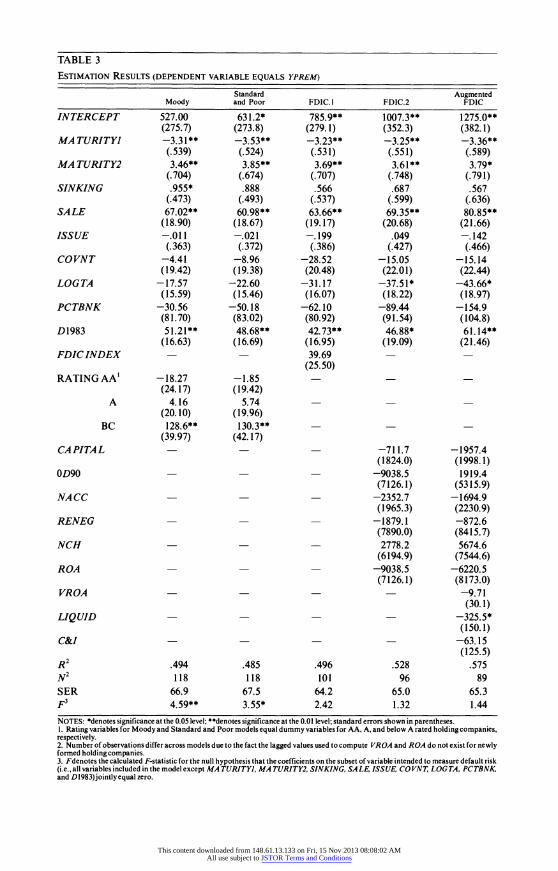

More general evidence on the determinants of risk premiums on bank subordi- nated debt is shown in Table 3 where generalized-least-squares estimates are pre- sented using several alternative methods for measuring holding company default risk. 13 Columns 2-3 of the table refer to models estimated using dummy variables for different Moody's and Standard and Poor's ratings, respectively. Column 4 is based on a model that uses the FDIC Index, while column 5 utilizes the set of variables proposed by the FDIC for its risk-based insurance premium proposal but allows the weights on these variables to be estimated. The last model (column 6) augments these

index correctly classifies 71 percent of the banks on the FDIC's problem bank list and 80 percent of the banks not on the list.

See Avery and Hanweck (1984) and Bovenzi, Marino, and McFadden (1983). I3Because two time periods were used for most BHCs, the models were estimated with standard

two-step modified GLS procedures under the assumption that a BHC's residuals were correlated with a common rho and residuals of different BHCs were uncorrelated. The GLS adjustment had virtually no effect on coefficients, their standard errors, or reported test statistics.

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

ROBERT B. AVERY, TERRENCE M. BELTON, AND MICHAEL A. GOLDBERG : 605

FDIC varlables with measures of the variability of earnings, liquid assets, and the percentage of commercial and industrial loans to total loans in the BHC's portfolio.

The estimates suggest that a fair amount of the variability in risk premiums remains unexplained in all of the estimated models. Furthermore, consistent with the findings of Pettway (1976), issue-related features of the bond, especially maturity (possibly reflecting preferred maturity habitats for government securities), and SA LE (reflecting the fact that quoted bid yields should exceed quoted ask yields) tend to dominate the explanatory power of the models. The coefficient on the measure of bank size (LOGTA ) is statistically insignificant in the Moody and Standard and Poor models but negative and statistically significant in all other models, suggesting that private-sector rating agencies may already account for size in formulating ratings. 14 The inclusion of a measure of BHC size in the model could capture two different effects. Subordinated notes and debentures of large BHCs may be more liquid because of a greater volume of secondary market trading in these issues. Larger banks also may be viewed by investors as having a greater degree of regulatory support because of the systemic impact of a large bank failure.l5

Covenants that restrict the ability of BHCs to dispose of shares of bank subsidiar- ies (COVNT) do not appear to have a substantial affect on SND premiums. The estimated coefficient on COVNTis negative, suggesting that BHCs with restrictive covenants tend to have lower premiums, but statistically insignificant in all the estimated equations. In addition, PCTBNK, the proportion of bank to total BHC assets, is negative but insignificant in all the regressions indicating that the market does not perceive nonbank assets as protecting debtholders from default.

Several of the individual coefficients of the dummy variables representing Moody's and Standard and Poor's ratings are also statistically insignificant. However, inclu- sion of the full set of ratings variables does significantly improve the explanatory power of the model. F-tests on the hypothesis that the coefficients of the ratings categories jointly equal zero are rejected in both models.l6

Consistent with the results of Table 2, important differences apparently exist between the market's assessment of default risk and the balance-sheet measures of risk taking currently evaluated and supervised by bank regulators. The coefllcient on the FDIC Index in column 4 of Table 3 is positive, as expected, but it is statistically insignificant at the 0.05 level. All coefficients of the individual components of the FDIC Index are also individually statistically insignificant (column 5). A test of the hypothesis that the coefficients on all components of the FDIC Index jointly equal zero cannot be rejected at the 0.05 level (a joint F of 1.32). A similar conclusion is supported by column 6 of the table which indicates that differences in premiums are not explainable by augmenting the components of the FDIC Index with factors such as the variability of earnings, liquidity, and the ratio of commercial and industrial

14Twenty-six percent of the variance in the Moody's ratings can be explained by BHC size (LOG TA) alone. Twenty-four percent of the Standard and Poor's rating can be similarly explained.

15Large BHCs may also have more diversified portfolios than small banks and therefore be subject to reduced volatility and earnings. Note, however, that this effect is already included in the augmented FDIC model by directly measuring the variance of earnings (VROA).

I6The calculated F-statistics (shown in the bottom row of Table 3) equal 4.59 for the Moody model and 3.55 for the Standard and Poor model.

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

TABLE 2

MEAN RISK PREMIUMS (IN BASIS POINTS) OF BANK HOLDING COMPANY NOTES AND DEBENTURES BY

RATING CATEGORY (STANDARD ERROR OF MEAN IN PARENTHESES)

Standard Category' Moody's2 and Poor's2 FDIC Index3

1 87.9 83.4 168.2 (16.9) (16.3) (25.5)

n=2 n=8 n=28

2 96.9 102.7 124.9 (1 1. 1) (6.4) (9.6)

n=44 n=43 n=28

3 128.5 133.0 1 14.2 (1 1.3) (16.2) (10.5)

n=58 n=48 n=28

4 239.4 269.3 1 10.3 (49.2) (108.9) (9 9)

n=6 n=3 n=29

1. Risk categories for Moody's and Standard and Poor's denote BHCs rated AAA, AA, A, and B or C, respectively. Risk categories for the FDIC Index rank BHCs by quartiles according to a formula proposed by the FDIC for assessing risk-based deposit insurance. 2. Mean differences between all Moody's categories are statistically significant at the 5 percent level except category I versus 2. For the Standard and Poor's rating categories, mean differences are not significant at the 5 percent level except for category I versus 3. 3. The difference between category I and category 4 mean premiums for the FDIC Index is statistically significant at the 5 percent level. Differences between other categories are not statistically significant.

606 : MONEY, CREDIT, AND BANKING

loans to total assets (calculated Fequals 1.44). Each of these variables has been found in previous work to be statistically significant indicators of bank failure (see Avery and Hanweck 1984) but surprisingly do not explain differences in subordinated debt risk premiums. The evidence seems to suggest that if market discipline currently exists in the subordinated debt market, it is not discipline concerning balance-sheet items traditionally supervised by regulators nor balance-sheet items elsewhere esti- mated to be important leading indicators of bank failure.l7

This result on the lack of a relationship between balance-sheet factors and the cost of bank debt appears to be quite robust with respect to model specifications. Because the results in Table 3 are surprising, three potential sources of specification error were examined. First, longer-term averages were employed in defining the balance-sheet measures of default risk. Second, measures of interest rate risk and off-balance-sheet activity were incorporated into the model to account for some potentially important omitted variables.l8 Finally, an attempt was made to model the change in risk premiums (from 1983 to 1984) as a function of changes in balance-sheet measures of bank risk.

In all three cases, results were obtained that support the conclusions suggested by Table 3. Models estimated using four-year-average data appear to fit slightly better than those based on one- or two-year averages but in no case could the hypothesis

17The basic result on the lack of market discipline holds whether or not interest rate premiums are adjusted for the value of the call option. However, the overall fit of the model is substantially worse when this adjustment is not made. Models estimated with premiums unadjusted for the value of the call option have R2 values that average 13 percent below those shown in Table 3.

I8The variables examined were standby and commercial letters of credit as a percent of total assets and the ratio of the absolute difference between interest-sensitive assets and interest-sensitive liabilities (maximum remaining maturity or longest repricing for both assets and liabilities is twelve months) to total assets.

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

TABLE 3

ESTIMATION RESULTS (DEPENDENT VARIABLE EQUALS YPREM)

Standard and Poor

631.2* (273.8) -3.53** (.524) 3.85**

(.674) .888

(.493) 60.98**

(18.67) -.021 (.372)

-8.96 (19.38)

-22.60 (15.46)

-50.18 (83.02) 48.68**

(16.69)

-1.85 (19.42)

5.74 (19.96) 130.3**

(42.17)

Augmented FDIC

1275.0 (382.1) -3.36 (.589) 3.79*

(.791) .567

(.636) 80.85

(21.66) -.142 (.466)

-15.14 (22.44)

-43.66* (18.97)

-154.9 (104.8) 61.14

(21.46)

Moody

527.00 (275.7) -3.31 (.539) 3.46

(.704) .955*

(.473) 67.02

(18.90) -.011 (.363)

-4.41 (19.42)

-17.57 (15.59)

-30.56 (81.70) 51.21

(16.63)

FDIC. I

785.9 (279.1) -3.23 (.531) 3.69

(.707) .566

(.537) 63.66

(19.17) -.199 (.386)

-28.52 (20.48)

-31.17 (16.07)

-62.10 (80.92) 42.73

(16.95) 39.69

(25.50)

FDIC.2

1007.3 (352.3) -3.25

(.551)

3.61 (.748) .687

(-599) 69.35

(20.68) .049

(.427) -15.05 (22.01)

-37.51* (18.22)

-89.44 (91.54) 46.88*

(19.09)

INTERCEPT

MA TURITYI

MA TURITY2

SINKING

SALE

ISSUE

COVNT

LOG TA

PCTBNK

D 1983

FDIC INDEX

RATING AA

A

BC

CAPITAL

OD90

-18.27 (24. 1 7)

4.16 (20. 10)

128.6 (39.97)

-711.7 (1824.0)

-9038.5 (7126.1)

-2352.7 (1965.3)

-1879.1 (7890.0) 2778.2

(6194.9) -9038.5 (7126.1)

-1957.4 (1998.1) 1919.4

(5315.9) -1694.9 (2230.9) -872.6 (8415.7) 5674.6

(7544.6) -6220.5 (8173.0)

NACC

RENEG

NCH

ROA

VROA 9.71

(30.1) LIQUID - - - - - 325.5*

(150. 1)

C&I - - - - -63.15 (125.5)

R2 .494 .485 .496 .528 .575 N2 118 118 101 96 89 SER 66.9 67.5 64.2 65.0 65.3 F3 4.59** 3.55* 2.42 1.32 1.44 NOTES: denotes significance at the 0.05 level; **denotes significance at the 0.01 Ievel; standard errors shown in parentheses. 1. Rating variables for Moody and Standard and Poor models equal dummy variables for AA, A, and below A rated holding companies, respectively. 2. Number of observations differ across models due to the fact the lagged values used to compute VROA and ROA do not exist for newly formed holdingcompanies. 3. Fdenotes the calculated F-statistic for the null hypothesis that the coefficients on the subset of variable intended to measure default risk (i.e., all variables included in the model except MA TURI TYI, MA TURI TY2, SINKING, SA LE, ISSUE, CO VNT, LOG TA, PCTBNK, and D1983)jointlyequal zero.

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

608 : MONEY, CREDIT, AND BANKING

that the coefficient on the FDIC Index (or its individual components) equals zero be rejected. Similar results were obtained when the volume of off-balance-sheet activity and alternative measures of interest rate risk were included in the model. Finally, when changes in risk premiums from 1983 to 1984were fit as functions of changes in balance-sheet measures of risk taking, the model fit even more poorly than in level form, with no evidence of statistical significance. Similar conclusions were found (1) when the model was estimated separately for each of the two years of data and (2) after an examination of outliers. I9 In no case was evidence found that measures of risk taking currently used by bank regulators were related to subordinated debt risk premiums.

CONCLUSIONS

The empirical findings in this study lead to the conclusion that risk premiums on bank-related long-term debt are virtually unrelated to traditional accounting mea- sures of bank performance and the index proposed by the FDIC for assessing risk-related insurance premiums. Even more surprisingly, the risk premiums are only weakly related to private-sector bond ratings (which are also uncorrelated or nega- tively correlated with the FDIC Index). Given the range of specifications examined, it seems unlikely that these fundamental conclusions would change with adjustments as simple as using different bond characteristics, balance-sheet measures, or time peri- ods of analysis.

Finding convincing explanations of these results presents a difficult problem. Putting aside the ever-present possibility of errors in the analysis, the apparent inconsistency between the regulators' rankings of the factors influencing bank risk and the market's suggests one of three possible explanations. First, regulators may not utilize publicly available data as efficiently as the market in assessing bank risk. However, this explanation implies that the market's assessment of bank risk should be more highly correlated with measures of bank performance than the regulators'. This is inconsistent with the fact that private sector ratings and market risk premiums appear to be unrelated to objective measures of bank performance while the regula- tors' assessment (e.g., the FDIC Index) is based on these measures. Second, differ- ences between the regulators' and the market's assessment of bank risk may be due to the fact that the market is not as efficient at evaluating bank risk as are regulators, or that superior information (reflected in the weights of the FDIC Index) is available to the regulator. However, this explanation of Zinside" or superior regulator informa- tion would not explain why public components of regulator evaluation, as reflected in the FDIC Index, are uncorrelated with market premiums or bond agency ratings.

A third possible explanation of these findings is that the market and the regulators have different objective or payoff functions. Although, as previously noted, SND- holders appear to bear risk comparable to the FDIC's, this may not be the case

19For example, the magnitude and significance of the coefficient on the FDIC Index were insensitive to the removal of any one observation from the sample. Even removing the observation with the greatest impact on this coefficient only reduces it by-.52 (about 1 percent) with no change in statistical

. .

slgnltlcance.

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

ROBERT B. AVERY, TERRENCE M. BELTON, AND MICHAEL A. GOLDBERG : 609

because most SND debt is issued at the BHC level whereas supervisory concerns are directed primarily at the bank level. Thus, holding company debt may be protected by nonbank assets, by the ability of bank management to reallocate assets (by dividends or other means) to the benefit of the BHC creditors, or by the existence of holding company bond indentures that contain restrictions prohibiting the disposal of the BHCs shares in its bank subsidiary without the approval of the bondholders. This explanation implies that restrictive covenants and/or the proportion of BHC assets invested in bank subsidiaries should affect BHC debt costs. However, the estimated coefElcients on these variables are insignificant in all the estimated equations.

Furthermore, payoffs to the capital markets and regulators may also differ because the FDIC may be reluctant to force P/A mergers with banks "too big to fail" and this may provide extra protection to their SND-holders (either at the bank or BHC level) for a given level of examiner risk. Indeed, as noted above, there is evidence that even after controlling for the size of bond issues and bank balance-sheet measures, both the bond risk premiums and Moody's and Standard and Poor's ratings are signifi- cantly correlated with bank size. However, even if it were perceived that the FDIC is providing implicit insurance for some very large bank SNDs, it still would not explain why the level of risk premiums for such banks is so high, nor why significant variation (with a standard deviation equal to 130 basis points) exists in the premium levels for banks of the largest size class. If these banks were truly too large to P/A, then they would be expected to have both low and similar premiums.

This study finds that the potential for market discipline to effectively and construc- tively augment regulatory controls via the subordinated note and debenture capital market is weak. The pricing signals that bankers receive from this market appear to be at odds with the directions desired by regulators. Given the surprising and disquieting nature of these findings, further research to disprove or better explain them would appear to be warranted before implementing policy changes, such as the FDIC's capital proposal, which rely upon SND market disciplines.

LITERATURE CITED

Avery, Robert B., and Gerald A. Hanweck. "A Continuous Time Analysis of Bank Failures." Bank Structure and Competition, Federal Reserve Bank of Chicago (April 1984), 380-401.

Benston, George J., Robert E. Eisenbeis, Paul M. Horvitz, Edward J. Kane, and George G. Kaufman. Safe and Sound Banking. Cambridge, MIT Press, 1986.

Bovenzi, John F., James A. Marino, and Frank McFadden. "Commercial Bank Failure Predictions Models." Economic Review, Federal Reserve Bank of Atlanta (November 1983), 14-26.

Brennan, Michael J., and Eduardo S. Schwartz. "Savings Bonds, Retractable Bonds and Callable Bonds." Journal of Financial Economics 5 (August 1977), 67-88.

"Determinants of GNMA Mortgage Prices." AREUEA Journal 13 (Fall 1985), 209-28.

Dunn, Kenneth B., and John J. McConnell. "Valuation of GNMA Mortgage-backed Securities." Journal of Finance 36 (June 1981), 599-616.

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions

610 : MONEY, CREDIT, AND BANKING

Herzig-Marx, Chaim. "Bank Soundness and Risk Premiums in Bank Debt." Federal Reserve Bank of Chicago working paper, 1978.

Hirschorn, Eric. "Developing a Proposal for Risk-related Deposit Insurance." Federal Deposit Insurance Corporation, Banking and Economic Review 4 (September/October 1986), 3-10.

Kareken, John H., and Neil Wallace. "Deposit Insurance and Bank Regulation: A Partial Equilibrium Exposition." Journal of Business (July 1978), 413-38.

Magen, S. D. The Cost of Funds to Commercial Banks. New York: Dunellen Publishing Co., 1971.

Pettway, Richard H. "Market Tests of Capital Adequacy of Large Commercial Banks." lke Journal of Finance 31 (June 1976), 865-75.

Sharpe, William F. "Bank Capital Adequacy, Deposit Insurance and Security Values." Journal of Financial and Quantitative Analysis 13 (November 1978), 701-18.

Silverberg, Stanley C. "Bank Holding Companies and Capital Adequacy." Journal of Bank Research (Autumn 1975), 202-207.

This content downloaded from 148.61.13.133 on Fri, 15 Nov 2013 08:08:02 AMAll use subject to JSTOR Terms and Conditions