Embed Size (px)

Citation preview

Maria O. Hart (Montana Bar No. 13155)PARSONS BEHLE k, LATIMER800 West Main Street, Suite 1300Boise, Idaho 83702Telephone: 208.562.4900Facsimile: 2 0 8 [email protected]

Attorney for Plaintiff

gV

' ' ~ ~ > I '.7:! > " t; j'!';„:> .' v pgF 0!, '' -,. e~Qpg.

"' " "-7 "O-!'777-JE!!,",l'EE;, p „ ,

„

'J!5 J!'! 6 Rfgg gq

C'EpU7 y

MONTANA KIGHTKKNTH JUDICIAL DISTRICTGALLATINCOUNTY

SALAD DAYS PRODUCTIONS, INC., d/b/aTHE PLAYMILL THEATRE,

Plaintiff,

Case No.

COMPLAINT

P/$5gddArd/ld /~ fdd~THE TOWN OF WEST YELLOWSTONE,

Defendant.

COMES NOW Plaintiff, Salad Days Productions, Inc., d/b/a the Playmill Theatre, by and

through its undersigned counsel of record, Parsons Behle & Latimer, and hereby alleges causes

of action against Defendant, the Town of West Yellowstone as follows:

PARTIES

1. Pl a i nt iff Salad Days Productions, Inc. is an Idaho corporation, doing business as

the Playmill Theatre ("the Playmill").

2. A t al l r e levant times hereto, the Playmill has been operating in West Yellowstone,

Gallatin County, Montana.

3. Defe n dant the Town of West Yellowstone ("the Town") is a subdivision of the

state of Montana.

COMPLAINT - 1

JURISDICTION AND VENUE

4. This C ourt has jurisdiction over the parties because the Town of West

Yellowstone is located in Gallatin County, and that is the county wherein the acts requiring relief

took place.

5. Ven ue is proper in this Court pursuant to Mont. Code Ann. $$ 25-2-118, 122 and

126.

GENERAL ALLEGATIONS

The Pla mill's Histo

6. The P l aymill has operated in West Yellowstone, Montana since 1964.

7. Sal ad Days Productions, Inc. purchased the Playmill Theatre in January 2005 and

has owned and operated it since that date. Roger and Heidi Merrill manage the Playmill.

8. The P laymill performs live musical theatre and other theatre every summer

between May and September. It sells tickets to the theatre performances as well as concessions-

style food, themed clothing, and other souvenir items.

Montana's Resort Tax Statute

9. Pur suant to Mont. Code Ann. $ 7-6-1501 et seq., certain designated municipalities

and geographic areas in Montana may enact a resort tax ordinance for the assessment and

collection of taxes associated with the tourism industry.

10. I n particular, Mont. Code Ann. $ 7-6-1503(2)(a) permits the taxing of "all goods

and services sold... within the resort communi o r are a" by s pecifically enumerated

establishments including hotels, motels, camping facilities, restaurants, bars, ski resorts, and

other recreational facilities. (Emphasis added). L ive theatres are not included in this list of

establishments for which all goods and services are subject to the resort tax.

COMPLAINT - 2

11. M o nt. Code Ann. $ 7-6-1503(2)(b) states "[e]stablishments that sell luxuries shall

collect a tax on such luxuries."

12. "Luxuries" are defined by Mont. Code Ann. $ 7-6-1501 as "any gift item, luxury

item, or other item normally sold to the public or to transient visitors or tourists."

13. R egarding a resort area's obligation to provide notice to businesses detailing the

goods and services subject to the resort tax, Mont. Code Ann. $ 7-6-1504(6)(a) states:

Before the resort tax question is submitted to the electorate of aresort community or a rea, the governing body o f the resortcommunity or the board of the county commissioners in the countyin which the resort area is located shall publish notice of the goodsand services subject to the resort tax.

14. M o nt . Code Ann. $ 7-6-1505(4)(a) further allows each resort area may pass an

administrative ordinance for the effective administration of the resort tax ordinance "which may

include further clarification and specificity in the categories of goods and services that are

subject to the resort tax consistent with 7-6-1503."

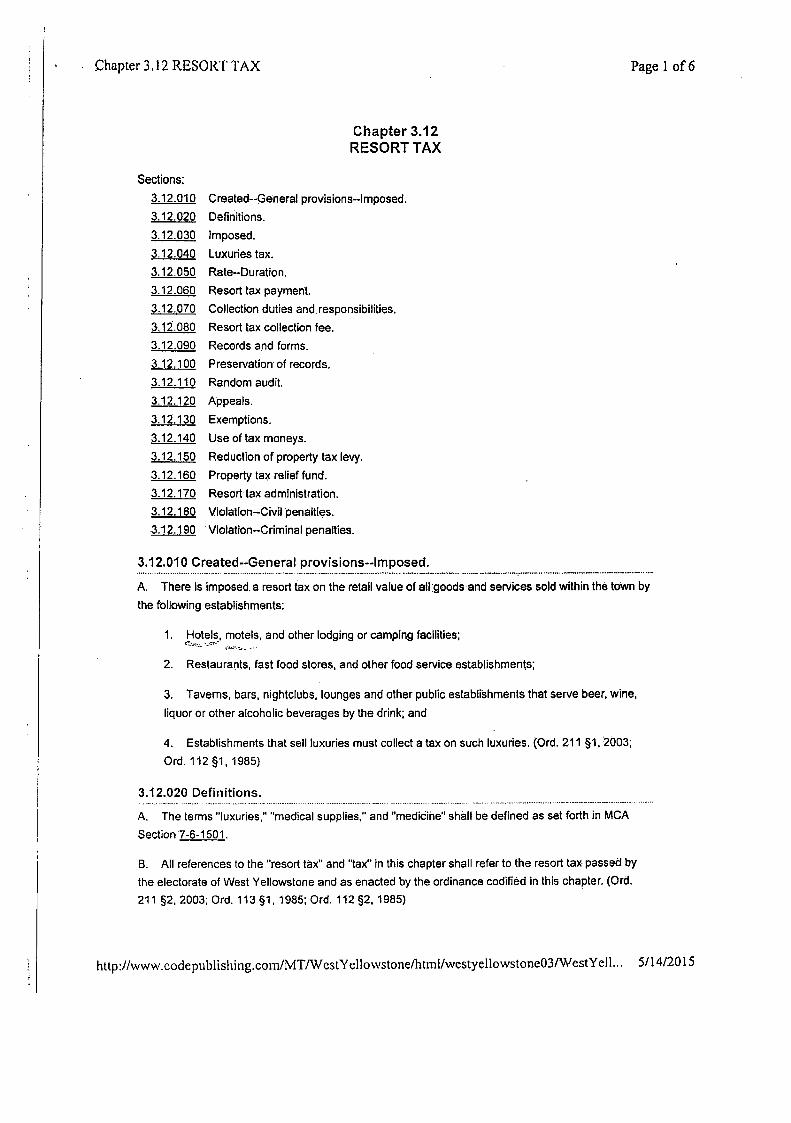

The Town's 2003 Resort Tax Ordinance

15. T h e Town enacted Ordinance No. 3.12.010 et seq., entitled "Resort Tax," in 1985.

The Town renewed Ordinance No. 3.12.010 et seq. in 2003 without any amendments (the "2003

Ordinance"). A true and correct copy of the 2003 Ordinance is attached hereto as Exhibit A.

16. The 2003 Ordinance, putatively enacted under the authority of Mont. Code Ann. $

7-6-1501 et seq., purports to impose a resort tax on the retail value of certain defined and

specified goods and services "sold within the Town." See 2.12.010 (emphasis added).

17. Se c t ion 3.12.020 of the 2003 Ordinance defines luxuries subject to the resort tax

"as set forth in MCA Section 7-6-1501."

18. Se c t ion 3.12.040 of the Ordinance further states:

COMPLAINT - 3

Luxuries shall be further defined to mean sporting goods, rentalson snowmobiles, automobiles, all-terrain vehicles, motorcycles,bicycles, skis, boats, campers, boat motors; recreational services,including float trips, guided trips and tours; all souvenir andlocalized items such as imprinted hats and T-shirts and curios; allnonfood items such as cleaning supplies, housewares (other thanhousehold appliances), automotive supplies and parts; ice; retailliquor, beer and wine, except that sold at state stores.

19. L iv e theatre tickets are not specified or included in the 2003 Ordinance's list of

luxury items.

20. In a dd i t ion, section 3.12.110 of the 2003 Ordinance grants the Town the authority

to conduct random audits of businesses to determine the accuracy of resort taxes paid and to

"determine[] a deficiency."

21. And , section 3.12.130 of the 2003 Ordinance exempts certain services from the

resort tax including "[a]11 nonrecreational labor, services and nonrecreational state licensed

profession and trades."

The Pla mill's Ticket Sales

22. T h e Playmill has paid to the Town all resort tax collected on all ticket sales as

well as food and souvenir sales which occurred within the Town at the Playmill box office, in

person or over the telephone.

23. I n 2005, the Playmill began selling tickets online to its live theatre performances.

24. T h e Playmill utilizes a third-party online vendor called Vendini to handle all

online ticket sales. Vendini is located and provides its activities from San Francisco, California.

Purchasers of the tickets are located throughout the United States and abroad.

25. The P laymill has never collected nor paid resort tax on any ticket sales which

occurred over the internet, as these sales were not made "within the Town."

COMPLAINT - 4

The 2007 Audit

26. De l l inger 8c Gallagher, CPA's, located in Manhatten, Montana ("Dellinger") is an

agent or employee of the Town authorized to conduct audits of resort tax payments to the Town.

27. In 2 007, pursuant to the Town's request, Dellinger conducted an audit of the

Playmill's resort tax payments for the preceding fiscal year. During this audit, Dellinger

requested and reviewed the Playmill's bank statements, internal financial records, tax returns,

spreadsheets, and other sales information, including all records for the Playmill's internet ticket

sales (the "2007 Audit").

28. U p on information and belief, Dellinger is directed to review all business records

and activities in light of the resort tax ordinance to determine whether a business is complying

with the ordinance or whether a violation has occurred. Dellinger makes recommendations to

the Town Council regarding all findings of compliance or non-compliance so the Town can

"determine a deficiency" or otherwise.

29. A ft e r reviewing the records and business activities of the Playmill for all items

and ticket sales, including both box off ice and online ticket sales, during the 2007 Audit,

Dellinger concluded that there existed uncertainty as to whether the 2003 Ordinance applied to

online ticket sales and as a result, did not recommend any action to the Town.

30. N ei t her Dellinger nor the Town assessed or required payment of the resort tax

relating to the online ticket sales, nor did the Town issue any finding of non-compliance to the

Playmill for failure to collect and remit the resort tax on online sales. Rather, the Town did not

provide any communication to the Playmill, written or otherwise, following the 2007 Audit.

COMPLAINT - 5

31. Acc o rdingly and in specific reliance on the absence of a directive from the Town

or Dellinger pursuant to the 2007 Audit, the Playmill continued to collect and remit to the Town

only those resort taxes associated with box office ticket sales made within the Town.

The 2014 Audit

32. In 2 0 14, the Town notified the Playmill that it was conducting an audit for the

2013 resort tax year, and again required the Playmill to provide bank statements, internal

financial records, tax returns, spreadsheets, and other sales information for the year 2013 to

Dellinger for review.

33. The P laymill provided all requested financial documents to Dellinger.

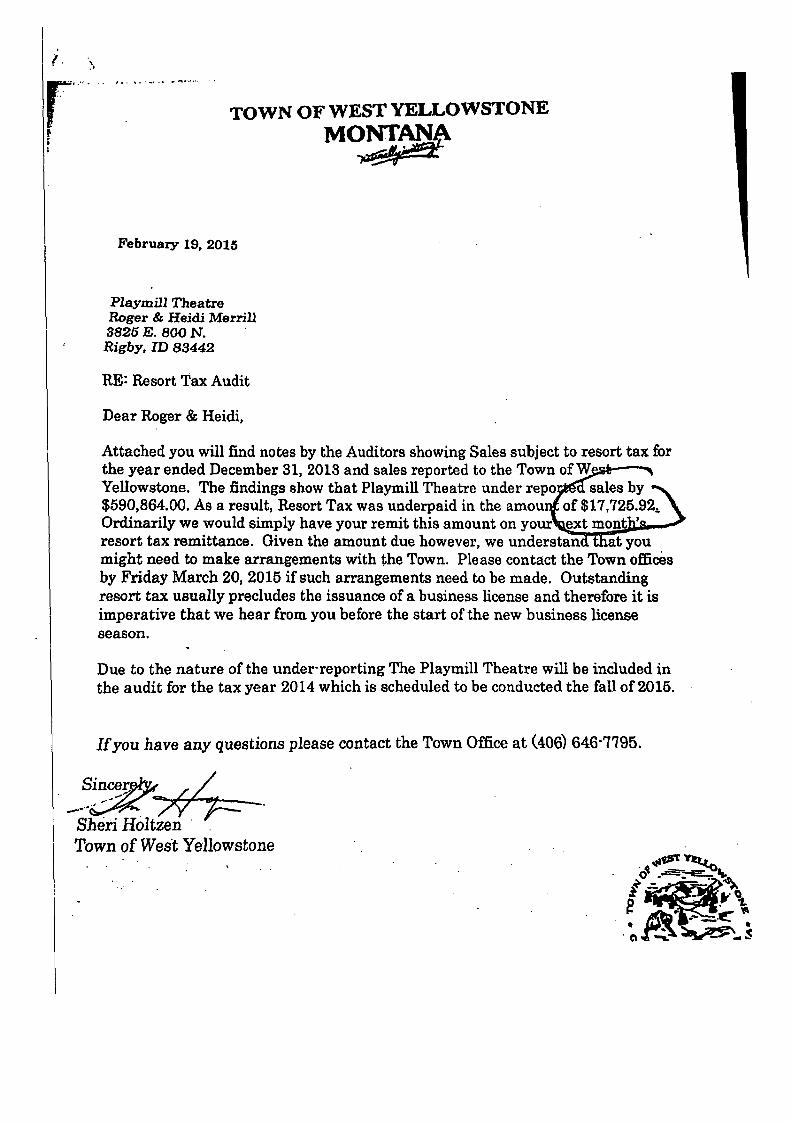

34. O n or about February 19, 2015, the Town sent a letter to the Playmill claiming

that the Playmill had underreported sales in the amount of $590,864.00, and therefore owed

$17,725.92 in resort tax. The letter asserts the underreported sales relate exclusively to online

ticket sales. A true and correct copy of the February 19, 2015 letter is attached hereto as Exhibit

The Pla mill's A eal to the Town

35. A ft e r receiving the February 19, 2015, letter from the Town, the Playmill filed an

appeal with the Town clerk, contesting the amount of resort tax claimed by the Town.

36. O n A pri l 7, 2015, the Playmill, through its manager Roger Merrill, appeared

before the Mayor and the Town Council at a council meeting to request information regarding

the Town's interpretation of the 2003 Ordinance and to request that the Town not impose the tax,

especially in light of the 2007 Audit findings. The Town Council deferred the interpretation of

the 2003 Ordinance to its legal counsel, Jane Mersen. A true and correct copy of the April 7,

2015 Town Council Meeting Minutes is attached hereto as Exhibit C.

COMPLAINT - 6

37. D u r ing the April 7, 2015 Town Council meeting, Ms. Mersen stated that the 2003

Ordinance needed to be updated, primarily because the 2003 Ordinance does not provide a

method for appealing the amount or imposition of resort tax, but rather only provides for a

method to appeal any penalties and interest imposed along with the resort tax.

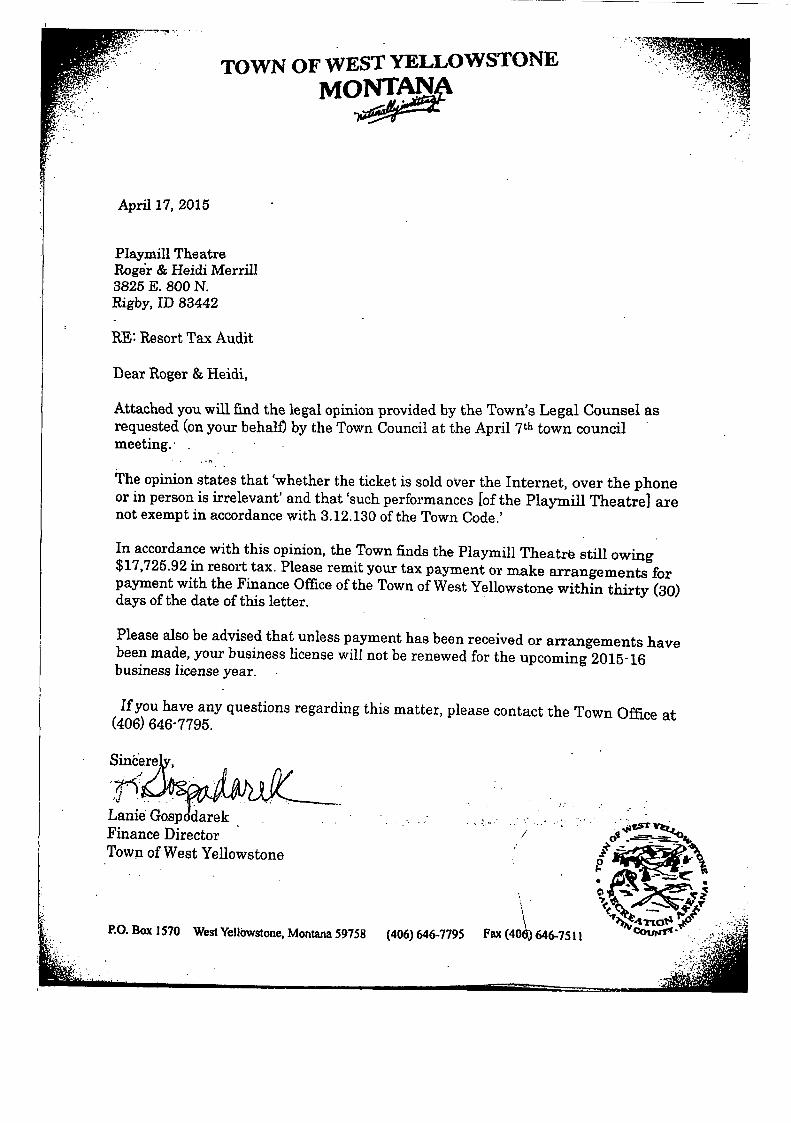

38. On A p r i l 13, 2015, Ms. Mersen sent the Playmill a letter reiterating the Town's

position stating that online ticket sales for a theatrical performance are "a service" subject to the

resort tax and the "service... is a luxury under the definition in both the Town's ordinance and

also Section 7-6-1503, MCA." A t rue and correct copy of the April 13, 2015 letter is attached

hereto as Kxhibit D.

39. On A p r i l 17, 2015, the Town Clerk, Lanie Gospodorek, sent the Playmill a letter

stating that unless the Playmill remitted the tax payment or made arrangements for the same, the

Town would not renew the Playmill's business license for the 2015-16 license year. A true and

correct copy of the April 17, 2015 letter is attached hereto as Exhibit E.

The Town's 2015 Amendment of the Resort Tax Ordinance

40. O n A p r i l 21, 2015, the Town Council proposed amendments to the 2003

Ordinance setting forth certain revised and additional terms of its resort tax.

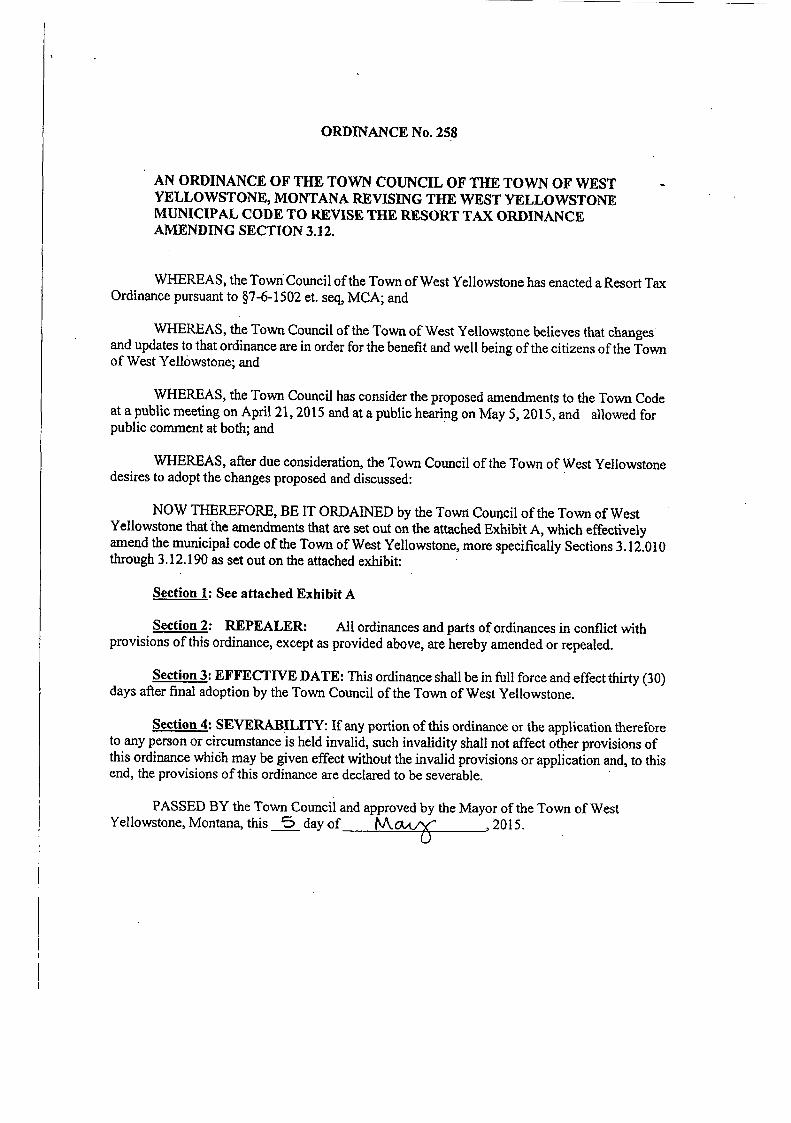

41. On M a y 5, 2015, the Town adopted Ordinance No. 258 ratifying the previously

proposed amendments to the Town's resort tax ordinance (the "2015 Ordinance"). A true and

correct copy of the 2015 Ordinance is attached hereto as Exhibit F.

42. The 2 0 1 5 O rdinance expands the definition of " l uxuries" to i nc lude "al l

attractions such as arcades, bowling centers, concerts, movie/theater tickets and all concession;

event and entertainment tickets (regardless of the method or location of purchase)."

COMPLAINT - 7

The Town's Refusal to Issue the Pla mill a Business License

43. O n May 15, 2015, the Playmill applied for a renewal of its business license, as

required by local ordinance, submitting payinent along with the application.

44. M s . Gospodorek informed the Playmill that the Town would not grant the

business license until the Playmill paid the resort tax claimed by the Town in its February 19,

2015 letter.

45. As of t h e date of this f i l ing, the Town has refused to renew the Playmill 's

business license on the grounds that the Playmill has outstanding resort tax payments due for the

2013 year.

46. In addition, the Town has designated the Playmill as a business automatically

subject to a (third) resort tax audit for the year 2014.

COUNT ONK(Deciaratory Judgment and Injunctive Relief)

47. T h e Playmill repeats and incorporates by reference each and every allegation set

forth in the preceding paragraphs.

48. A dispute has arisen between the Playmill and the Town concerning the

applicability and validity of the Town's interpretation of the 2003 Ordinance, which was the

operative ordinance during the 2007 Audit as to online ticket sales and all other ticket sales for

live theatre performances at the Playmill.

49. An a c tual and substantial legal controversy exists between the parties with respect

to whether the Town can (a) impose a resort tax on live theatre tickets absent express authority

pursuant to state statute or the applicable ordinance; (b) expand the definition of "luxuries" under

the 2003 Ordinance to include live theatre tickets without engaging in the legislative process; and

(c) impose a resort tax on live theatre tickets sold via the internet.

COMPLAINT - 8

50. The Town's 2015 actions amending and expanding the 2003 Ordinance in order

to add previously missing terms including a definition of "luxuries" which now expressly

includes live theatre tickets and a clarification that goods and services sold via the internet are

sold "within the Town" for purposes of the resort tax, provides a direct admission from the Town

that relevant terms at issue in this lawsuit were not clear and/or present in the 2003 Ordinance.

51. The Town's reliance upon the 2003 Ordinance as a basis for demanding payment

of resort taxes for online ticket sales or any live theatre tickets sales 'violates Montana law and

the Town's own ordinance. See Canbra Foods Ltd. V. Montana Dept. of Revenue, 278 Mont.

368, 373, 925 P.2d 855, 858-59 (1996) (holding that "It]ax statutes are to be strictly construed

against the taxing authorities and in favor of the taxpayer.").

52. Mont. Code Ann. $$ 27-8-201 and 27-9-202 gives this Court the power to declare

(1) the respective rights of the Playmill and the Town under the 2003 Ordinance and (2) the

validity of the 2003 Ordinance, particularly as applied to live theatre tickets and online ticket

sales.

53. Ac cordingly, the Court should determine by declaratory judgment that:

a. The Town's interpretation and enforcement of the 2003 Ordinance is illegal

pursuant to Montana statute and local ordinance;

b. Mont. Code Ann. $ 7-6-1501 et seq. does not impose a resort tax on l ive

theatre establishments;

c. Online ticket sales are not sales "within a resort community or area" under

Mont. Code Ann. $ 7-6-1503;

d. The Town's 2003 Ordinance does not impose a resort tax on l ive theatre

establishinents;

COMPLAINT - 9

e. The Town's 2003 Ordinance does not identify live theatre tickets as a luxury

which is subject to the resort tax;

f. Online ticket sales are not sales "within the Town" under the 2003 Ordinance;

and/or

g. The Town's collection of resort taxes from the Playmill for all l ive theatre

tickets violates the express terms of the taxing authority granted to the Town

pursuant to Montana statute and local ordinance.

54. I n addition to the declaratory relief requested, the Court should enjoin the Town

&om refusing to grant the Playmill the business licenses necessary and required for legal

business operations.

55. The Town conducted the 2007 Audit and did not assess any resort tax against the

Playmill for its online ticket sales. Upon completion of the 2007 Audit, the Town did not assert

a claim for payment of resort taxes for online ticket sales. Accordingly, the Town implicitly

concluded the Playmill correctly interpreted the 2003 Ordinance as not applying to online ticket

purchases.

56. The Playmill continued its practice of not collecting and remitting the resort tax in

reliance on the 2007 Audit which made no findings or adjustment for the Playmill's failure to

collect and remit the resort tax for online ticket sales.

57. T h e T own has reversed and materially altered its position regarding the

applicability of the 2003 Ordinance to the Playmill's online ticket sales, to the detriment and loss

of the Playmill.

COMPLAINT - 10

58. T h e Town should be estopped &om materially altering its own 2007 interpretation

of the 2003 Ordinance or seeking payment from the Playmill for online ticket sales prior to the

enactment of the 2015 Ordinance in May, 2015.

COUNT TWO(Bad Faith)

59. T h e Playmill repeats and incorporates by reference each and every allegation set

forth in the preceding paragraphs.

60. To t h e Playmill's detriment the Town has reversed the findings and position it

took during the 2007 Audit regarding the applicability of the 2003 Ordinance to the Playmill's

online ticket sales and has relied solely on its 2014 re-interpretation of the 2003 Ordinance to

support its demand for payment of resort taxes and refusal to issue a business license.

61. A s s t a ted herein, the Town has acted frivolously and without legal basis to

deprive the Playmill of the value of its ticket sales and has threatened to substantially interfere

with the Playmill's sole source of income by refusing to grant the business license necessary to

operate as a legal business in the Town.

62. B y demanding payment of a resort tax for online ticket sales and refusing to grant

the essential and necessary business license to the Playmill as leverage to force the Playmill to

submit to the Town's changed interpretation of its ordinance without due process of law, the

Town has acted with bad faith and with the specific intent to deprive the Playmill of the value of

its primary income source.

63. The T own has continually and repeatedly asserted positions that it knew or

reasonably should have known were lacking in legal basis under the 2003 Ordinance or Montana

statute.

COMPLAINT - 11

PRAYER FOR RELIKF

WHEREFORE, the Playmill prays for entry of judgment against the Town as follows:

1. Tha t judgment be entered in favor of Playrnill on all claims for relief raised

herein, specifically, that declaratory judgment be entered as follows:

a. The Town's interpretation and enforcement of the 2003 Ordinance is illegal

pursuant to Montana statute and local ordinance;

b. Mont. Code Ann. $ 7-6-1501 et seq. does not impose a resort tax on live

theatre establishments;

c. Online ticket sales are not sales "within a resort community or area" under

Mont. Code Ann. $ 7-6-1503;

d. The Town's 2003 Ordinance does not impose a resort tax on l ive theatre

establishments;

e. The Town's 2003 Ordinance does not identify live theatre tickets as a luxury

which is subject to the resort tax;

f. On l ine ticket sales are not sales "within the Town" under the 2003 Ordinance;

g. The Town's collection of resort taxes fiom the Playmill for all l ive theatre

tickets violates the express terms of the taxing authority granted to the Town

pursuant to Montana statute and local ordinance;

h. The Playmill does not have to pay the resort tax as demanded by the Town for

online ticket sales for the year 2013 in the amount of $17,725.92; and/or

i. The Town illegally assessed and collected resort taxes from the Playmill for

the its sales of ticket in the theatre box office of the Playmill since at least

2005, in an amount to be determined at trial; and/or

COMPLAINT - 12

2. The Town is estopped from refusing to renew the Playmill's business license

pending the Court's decision on the interpretation of the 2003 Ordinance as requested herein;

3. Dama ges in an amount to be determined at trial for resort taxes the Playmill

overpaid to the Town in relation to ticket sales made at the box office;

4. All c osts associated with briny'ng this suit pursuant to Mont. Code Ann. $$ 25-

10-101 and 27-9-311;

5. Atto rney's fees pursuant to Mont. Code Ann. $f 25-10-711 and 27-8-313;

6. For s uch other and further relief as the Court deems just and proper.

DATED THIS 2nd day of July, 2015.

PARSONS BEHLE <0 LATIMER

ByMaria O. Hart

Attorney for Plaintiff

COMPLAINT - 13

Exhibit A

Chapter 3.12 RESORT TAX Page 1 of6

Chapter 3.12RESORT TAX

Sections;3.12.0103.12.0203.12.0303 12 0403.12.0503 12.0603.12.0703.12.0803.12.0903.12 1003.12.1103.12.1203.12 1303.12.1403.12.1503.12.1603.12.1703.12.1803 12.190

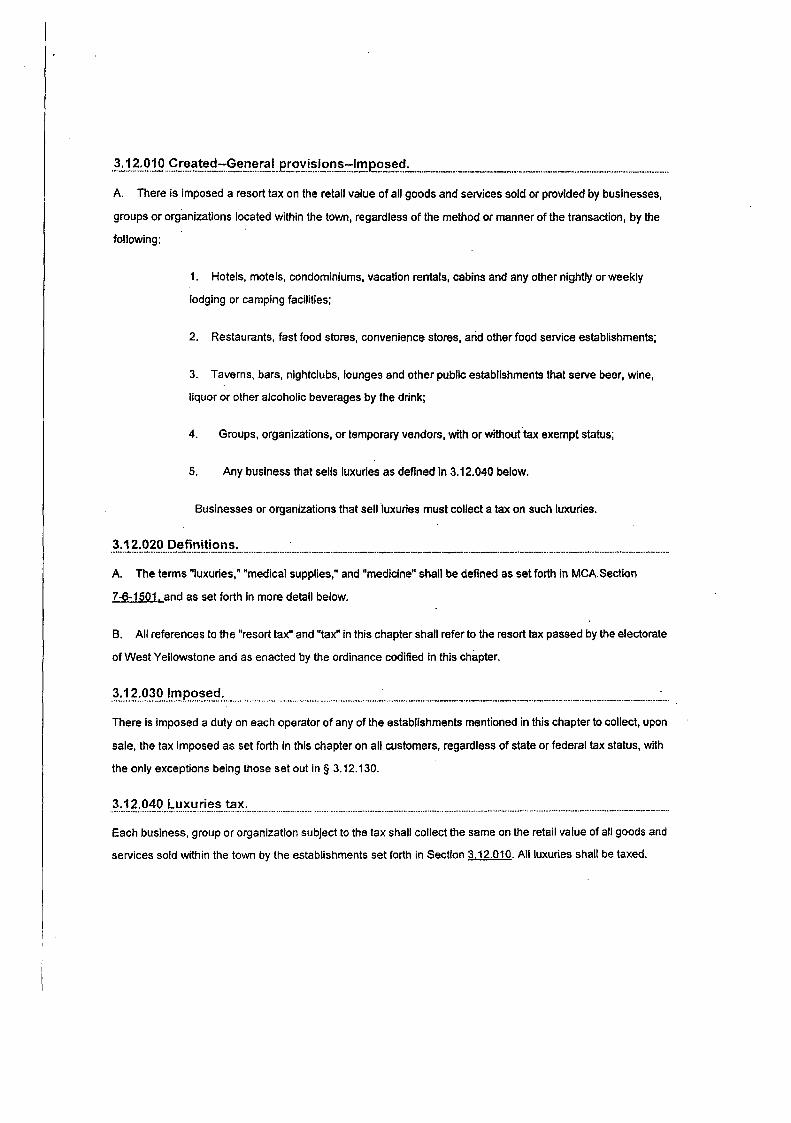

3.12.010 Created-General provisions-Imposed

A. There is imposed. a resort tax on the retail value of all goods and services sold within the town bythe following establishments:

Created — General provisions-lmposed.Definitions.Imposed.Luxuries tax.Rate-Duration.Resort tax payment.Collection duties and responsibilities.Resort tax collection fee.Records and forms.Preservation of records.Random audit.Appeals.Exemptions.Use of tax moneys.Reduction of property tax levy.Property tax relief fund.Resort tax administration.Violation-Civil perialties.Violation-Criminal penalties.

1. Hotels, motels, and other lodging or camping facilities;

2. Restaurants, fast food stores, and other food service establishments;

3. Taverns, bars, nightclubs, lounges and other public establishments that serve beer, wine,liquor or other alcoholic beverages by the drink; and

4. Establishments that sell luxuries must collect a tax on such luxuries. (Ord. 211 $1. 2003;Ord. 112 g1, 1985)

3.12.020 Definitions

A. The terms "luxuries," "medical supplies," and "medicine" shall be defined as set forth in MCASection 7-6-1501.

B. All references to the "resort tax" and "tax" in this chapter shall refer to the resort tax passed bythe electorate of West Yellowstone and as enacted by the ordinance codified in this chaptei'. (Ord.211 g2, 2003; Ord. 113 g1, 1985; Ord. 112 ll2, 1985)

http://www.codcpublishing.con1/MT/WestYellowstone/html/westyellowstone03/WestYell... 5/14/2015

.Chapter 3.12 RESORT TAX Page2of6

3.12.030 lmposed.

There is imposed a duty on each operator of any of the establishments mentioned in this chapter tocollect, upon sale, the tax imposed as set forth in this chapter. (Ord. 113 g2, 1985)

3.12.040 Luxuries tax

Each business subject to the tax shall collect the same on the retail value of all goods and servicessold within the town by the establishments set forth in Section 3.12.010. All luxuries shall be taxed,and luxuries shall mean any gift item, luxury item, or other item, or other itern normally sold to thepublic or to transient visitors or tourists; but the term does not include food purchased unprepared orunserved, medicine, rnedicai supplies and services, or any necessities of life. Luxuries shall be.furtherdefined to mean sporting goods, rentals on.snowmobiles, automobiles, all-terrain vehicles,motorcycles; bicycles; skls, boats; campers, boat motors:; i'ecreational services;-including float trips,.guided trips and tours; all souvenir.arid localized'items'such as;imprinted hats and T-shirts andcurios; all nonfood items such as/cleaning'supplies, ho'usewares (other than household appliances),automotive supplies and parts; ice retail liquor, beer and:wine,.except that sold at.state stores; (Ord.211 g3,2003; Ord. 113tJ12, 1985)

3.12.050 Rate-Durat ion.

A. The exact rate of the resort tax is three percent.

B. The duration of the resort tax as approved by the voters on November 5, 1985 is twenty yearsfrom its effective date. The.effective date of the resort tax is January 1, 1986.

C. The duration of the resort tax renewal as approved by the voters on November 5, 2002, is twentyyears from its effective date. The effective date of the resort tax renewal is January 1, 2006. {Ord. 211g4, 2003; Ord. 112 Q3, 4, 5, 1985)

3.12.060 Resort tax payment

The resort taxes collected by a business in any month are to be paid to the town on or before thetwentieth day of the following month, or if such day falls on a Saturday, Sunday or holiday, then onthe next business day. Resort tax payments sent by mail or private courier must be received by thetown on or before the twentieth day ofeachmonth, or if such day falis on a Saturday, Sunday orholiday, then on the next business day. (Ord. 224 $1, 2007: Ord. 219 $1, 2006: Ord. 113 g3, 1985)

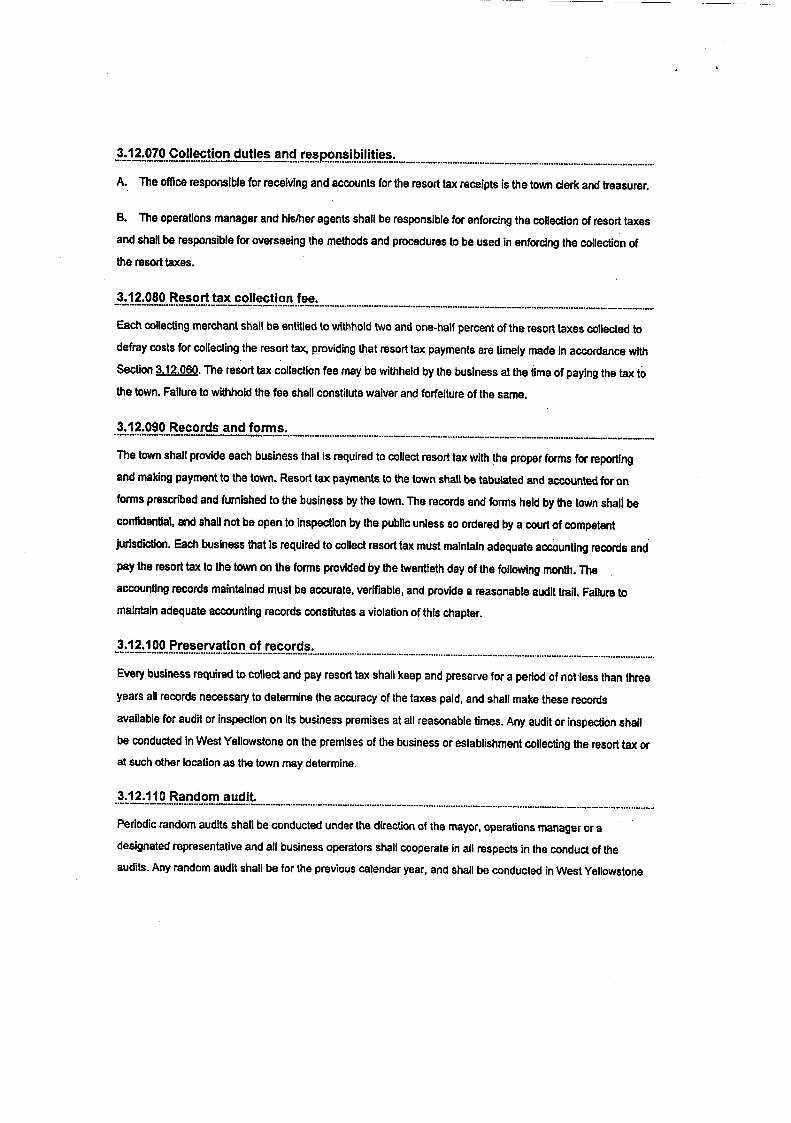

3.12.070 Coilection duties and responsibi l it ies

A. The office responsible for receiving and accounts for the resort tax receipts is the town clerk andtreasurer.

B. The operations manager and his/her agents shall be responsible for enforcing the collection ofresort taxes and shall be responsible for overseeing the methods and procedures to be used inenforcing the collection of the resort taxes. (Ord. 172 $1, 1995: Ord. 113 Q4, 5, 1985)

3.12.080 Resort tax collection fee.

http://www.codepublishing.com/MT/WestYellowstone/htrnl/westyellowstone03/WestYell... 5 /14/2015

Chapter 3.12 RESORT TAX Page3 of 6

Each collecting merchant shall be entitled to withhold two and one-half percent of the resort taxescollected to defray costs for'collecting the resort tax, providing that resort tax payments are timelymade in accordance with Section 3.12.060. The resort tax collection fee may be withheld by thebusiness at the time of paying the tax to the town. Failure to withhold the fee shall constitute waiverand forfeiture of the same. (Ord. 222 $1, 2007: Ord. 21S g2, 2006: Ord. 113 $7, 1985)

3.12.090 Records and forms

The town shall.provide each business that is required to collect resort tax.with the proper forms forreporting and making payment to the town. Resort tax payments to the town shall be tabulated andaccounted for on forms prescribed and furnished to the business by the town. The records and formsheld by the town shall be confidential, and shall not be open to inspection by the public unless soordered by a court of competent jurisdiction. Each business that is required to collect resort tax must'maintain adequate accounting records and pay the resort tax to the town on the forms provided bythe twentieth day of the following month. The accounting records maintained must be accurate,venTiable, and provide a reasonable audit trail. Failure to maintain adequate accounting recordsconstitutes a violation of this chapter. (Ord. 219 g3, 2006: Ord. 201 g1, 1999: Ord. 119 g1, 1986; Ord.113 58, 1985)

3.12.100 Preservation of records

Every business required to collect and pay resort tax shall keep and preserve for a period of not lessthan three years all records necessary to determine the accuracy of the taxes paid, and shall maketheserecords available for audit or inspection on its business premises at all re'asonable times. Anyaudit'or inspection shall be conducted in West Yellowstone on the premises of the business orestablishment collecting the resort tax or at such other location as the town may determine. (Ord. 21Sf4, 2006: Ord. 201 g2, 199S: Ord. 113 $10, 1985)

3.12.110 Random audit.

Periodic random audits shall be conducted under the direction of the mayor or his designatedrepresentative and all business operators shall cooperate in all respects in the conduct of the audits.Any random audit shall be for the previous calendar year, and shall be conducted in WestYellowstone on the premises of the business or establishment collecting the resort tax or at suchother location as the town may determine. If the audit determines a deficiency it will be at thediscretion of the town to audit the previous two years and require a follow up audit on the nextreporting year. Failure to cooperate in any audit or inspection of records, including the failure to makethe appropriate records available on the business premises in West Yellowstone, shafl constitute aviolation of the provisions of this chapter. (Ord. 201 g3, 1999: Ord. 113 g9, 1985)

3.12.120 Appeals

Any business may appeal to the town council any.assessment of penalty,or interest;.provided, thatnotice of appeal in writing is filed with the town clerk within thirty days of the serving or mailing of thedetermination of the amount of penalty and interest due. The town council shall on the nextimmediate regular town council meeting fix the time and place for hearing the appeal and the townclerk shall cause notice in writing to be personally served by a peace officer upon the operator; Thefindings and decision of the town council shall be final and conclusive and shall be served upon the

http://www.codepublishing.com/MT/WestYellowstone/html/westyellowstone03/WestYell... 5 /14/20.15

Chapter 3.12 RESORT TAX Page 4 of 6

appellant in the manner prescribed for service of notice of hearing or by certified mail directed to thebusiness operator's last known address. Any amount found to be due shalt be immediately payableupon service of the findings and decision. (Ord. 113 g11, 1985)

3.12.130 Exemptions.

Notwithstanding Section 3.12.040, however, the following goods and services shall be exempt fromthe tax.

A. Utilities and utility services;

B. Medical supply services and medicine;

C. Wholesale merchandise for resale at retail or used in the purchaser's bdsiness as supplies;

D. Gasoline and other motor vehicle fuel;

E. Liquor sold at state liquor stores;

F. Propane and similar home fuels;

G. Automobiles, trucks, snowmobites, motorcycles, all-terrain vehicles, bicycles, boats, outboardmotors and chain saws;

H. Labor on automobiles, trucks, snowmobiles, motorcycles, all-terrain vehicles, bicycles, boats,outboard motors and chain saws;

. I: All nonrecreatiohal,labor, services.and nonre'creational,state'licensed professions.and trades;::

J. All payroll and business and labor costs;

K. Lumber, building supplies and tools, and other tools;

L. Household appliances;

M. Any hotel, rnotel, campground or other lodging facility occupancy, with respect to any person orpersons who occupy a room or a space for a period longer than thirty consecutive calendar days;provided, that such person certifies prior to occupancy that the occupancy will exceed thirtyconsecutive calendar days and does in fact exceed thirty consecutive calendar days;

. N. .AII sales of,goods from catalogs paid for from.outside of th'e boundaries of the town; that is;catalog sales of goods shail be.exempt.except,to.the extent that the goods ar'e'paid for and.the„„exchange,is made within.the.,bou'ndaries,of the town; (Ord. 117 H2, 3, 1986; Ord. 113 $13, 1985)

3.12.140 Use of tax moneys

A. The tax moneys derived from the resort tax may be appropriated by the town council for anyactivity, undertaking, or administrative service that the municipality is authorized by law to perform,including costs resulting frorn the imposition of the tax.

z:-' t

http:/hvww.codepublishing.com/MT/West Yellowstonc/html/westyellowstone03/WestYell... 5 /14/2015

Chapter 3.12 RESORT TAX Page5 of6

B. There is established a marketing and promotion (MAP) fund for the town. Two and one-halfperceht of the three percent resort tax c'ollected by the collecting merchant shall be dedicatedexclusively to the MAP fund, which fund shall'be used solely for the marketing and promotion of WestYellowstone and the surrounding area, as well as the associated costs of administering the fund, The.town council may appropriate additional resort tax receipts to the MAP fund.

C. The town council shall by resolution establish a board of not less than three nor more than sevenqualified persons to oversee the MAP fund. At least one member of this board shall be a sittingmember'of the town council or the council's designee. The board shall establish policies andprocedures for its operation and the general rnanagement of the fund in accordance with the council'sresolution establishing the board. The board shall also select individual marketing and promotionprojects and approve expenditure of funds for such projects, subject to approval by the town council..(Ord. 222 g2, 2007: Ord. 112 g6, 1985)

3.12.150 Reduction of property tax levy

Annually anticipated receipts from the resort tax must be applied to reduce the municipal property taxlevy for the fiscal year in an amount equal to five percent of the resort tax revenues derived during thepreceding fiscal year. (Ord. 112 $7, 1985)

3.12.160 Property tax relief fund

In the'.event the town receives more resort tax revenues than had been included in the annualmunicipal budg'et; it shall establish a mu'nicipal property tax relief fund, and all resort tax revenuesreceived in excess of the budget amount must be placed in the fund. The entire fund must be used toreplace municipal property taxes in the ensuing fiscal year. (Ord. 112 g8, '1985)

3.12.170 Resort tax administration

The town shall administer resort tax collections according to the following rules

A. Resort tax payments shall be made to the town finance office by the established deadline.

B. Failure to report or make resort tax payments by the payment deadline shall result in forfeiture ofthe resort tax collection fee for the month in which the payment is due.

O':.. Failure to pay resort tax before the end of the month in which the payment is due shall result inan administrative fee of either: (1) twenty-five dollars for businesses with gross sales of one thousandfive hundred dollars or less for the reported month; or (2) fifty dollars for businesses with gross salesin excess of one thousand five hundred dollars for the reported month, which shall be in addition toany civil penalties awarded to the town in a suit for collection of resort tax.

D. At the end of each subsequent month after the original payment is due, the town will assess anadditional administrative fee equal to ten percent of the sum of any delinquent resort tax andpenalties, which shall be assessed on the first business day of the subsequent month. This and alladministrative fees shall be assessed in addition to any civil penalties awarded to the town in a suitfor collection of resort tax.

http://wv~.codepublishing.com/MT/WestYellowstone/html/westyellowstone03/WestYell... 5/14/2015

• .Chapter 3.12 RESORT TAX Page6of6

; E. . The,'town:rnay ievoke the busiriess license.of any person or business that violates any provisionof this chapter; The town may revoke a violator's.'business license either through the administrativeprocedure described in Chapter 5;04ior,"through a court order>oijjudgment in accordance,with Section

. 3.1'2.186. (Ord. 250 $1, 2010: Ord. 219 g5, 2006: Ord. 211 g5, 2003; Ord. 112 g9, 1985)

3.12.180 Vlolation-Civil penalties.

For failure to report taxes when due, failure to pay taxes when due, and other violations of thischapter, the town may seek the following penalties or remedies:

A. A court judgement in the amount of all unpaid resort taxes, including any unpaid administrativefees assessed under Section 3.12.170 and any resort tax collection fees forfeited in accordance withSection 3 12.080;

B. Interest at the rate of ten percent per annum on unpaid resort taxes or administrative fees fromthe due date or assessment date until paid;

C. A civil penalty in the amount of fifty percent of the unpaid resort taxes, which includes forfeitedresort tax collection fees, plus all costs and attorney's fees incurred by the town in any court action;

D. An order requiring the delinquent business to undergo a financial audit by the town or itsrepresentatives to determine the proper amount of resort taxes due, including payment by thebusiness of all audit costs and expenses incurred by the town or its representatives;

E. Revocation of the violator's town business license, either. throu'gh judicial order 'or the:administrative procedure described in Chapter 5.0'4;

F. Any other penalty, remedy or judicial relief to which the town is entitled. (Ord. 219 g6, 2006: Ord.207 g3, 2000: Ord. 113 g6. 1985)

3.12;190 Violation-Criminal penaltiesA'p'erson'.or-busin'ess violating"any provision of this chapter is guilty'of a misdemean'or and subject toa fine.not exceed.one thousand dollars.for each violation, or imprisonment'not to exceed.six monthsfor'each violation, oi both. (Ord. 219 g7, 2006)

The West Yellowstone Town Code ls current throughOrdinance 257, passed November 20, 2012.Disclaimer: The Town Clerk's Office has the official version of theWest Yellowstone Town Code. Users should contact the TownClerk's Office for ordinances passed subsequent to the ordinancecited above.

http://www.codepublishing.com/MT/WestYellowstone/html/westyellowstone03/WestYell... 5/14/2015

Kxhibit B

TOWN OF WEST YELLOWSTONEMaNTAN

Februa~ 19, 2015

Playmill TheatreBoger 4 He idi Merr i l l3825 E. 800 N.Rigby, ID 83442

RE- Resort Tax Audit

Dear Roger 8r, Heidi,

Attached you will find notes by the Auditors showing Sales subject to resort tax forthe year ended December 31, 2013 and sales reported to the Town of WYellowstone. The Gndings show that Playmill Theatre under repo sal e s by$590,864.00. As a result, Resort Tax was underpaid in the amou of $17,725.92.Ordinarily we would simply have your remit this amount on your ex t mont 'resort tax remittance. Oiven the amount due however, we understan t a t youmight need to make arrangements with the Town. Please contact the Town ofacesy Friday March 20, 2015 if such arrangements need to be made. Outstanding

resort tax usually precludes the issuance of a business license and therefore it isimperative that we hear from you before the start of the new business licenseseason.

Due to the nature of the under-reporting The Playmill Theatre will be included inthe audit for the tax year 2014 which is scheduled to be conducted the fall of 2015.

If you have any questions please contact the Town Office at (406) 646 7'195.

Sincer,

Sheii HoltzenTown of West Yellowstone

Playmill TheatreNotes to Schedule of Sales

Note 1 -Q asis of Accounhng

The schedul

accounting principles;

Note 2 - Reconciiiation of Sales

. for federalnera11 accepted.

ule of sales have been prepared on the accounting basis used by the Cornpanyincome tax p~rposes, which is a comprehensive basis of accounting,other than gene

~,,ofr1aThe followi g is a econciliation between s«s as ratre and e ort tax sales as they are defined un«

881,341Sales per the financial recordsfor the year ended December 31, 2013

Less exempt sales:

Sales subject to resort taxfor the year ended December 31, 2013

Sales reported to the Town of West Yellowstonefor the year ended December 31, 2013

(Over) under reported sales

881,341

290 477.

$ 59 0 864

Sch D

Kxhibit C

Town of West YellowstoneTuesday, April 21, 2015

West Yellowstone Town Hall, 440 Yellowstone Avenue7:00 PM

TOWN COUNCIL MEETING AGENDA

April 14, 2015 Work Session 0o

Pledge of AllegiancePurchase OrdersTreasurer's Report/Securities Report mClaims ~Consent Agenda: Apri l 7, 2015 Work Session & Town Council Meeting ao

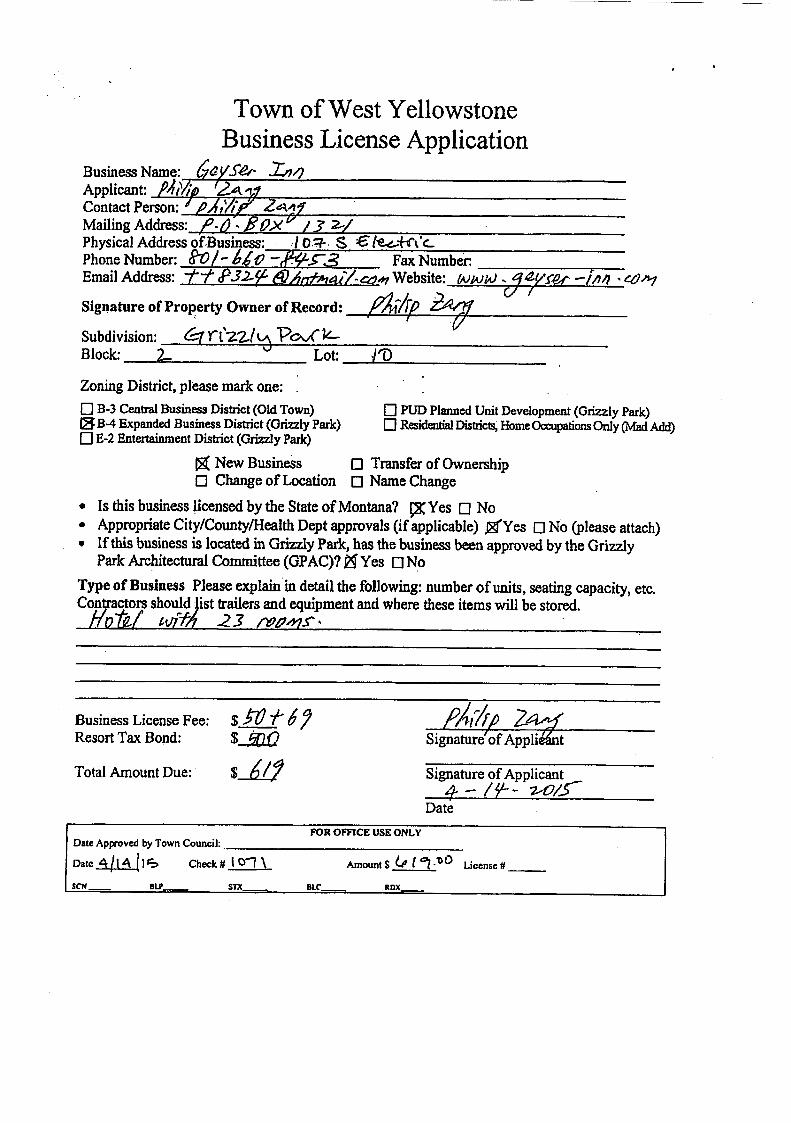

Business License Applications

Advisory Board Report(s)Operations Manager & Department Head ReportsAssignments ReportComment Period

Geyser Inn ~

• Public Comment• Council Comments

UNFINISHED BUSINESS

Proposal from Hebgen Basin Fire District to purchase the Emergency ServicesBuilding at 400 Yellowstone Avenue for $200,000 (Tabled 1/20/15)

NEW BUSINESS

Ordinance No. 258, Resort Tax, 1" Reading

Resolution No. 661, Public Records Request Policy

Recruitment Services Contract, Prothman Company

Executive Session with Town Attorney to discuss pending litigation, Closed to the Public

Correspondence/FYIMeeting Reminders

Discussion/Action a>

Discussion/Action m

Discuss>on/Acbon ao

Discussion/Action ~

Policy No. 16 {Abbreviated)Policy on Public Hearings and Conduct at Public Meetings

Pu I' earin u l i c MeetinA public hearing is a formal opportunity for citizens to give their views to the Town Council for considerationin its decision making process on a specific issue. At a minimum, a public hearing shall provide for submissionof both oral and written testimony for and against the action or matter at issue.

Oral CommunicationIt is the Council's goal that citizens resolve their complaints for service or regarding employees' performanceat the staff level. However, it is recognized that citizens inay from time to time believe it is necessary to speakto Town Council on matters of concern. Accordingly, Town Council expects any citizen to speak in a civilmanner, with due respect for the decorum of the meeting, and with due respect for all persons attending.

• No member of the public shall be heard until recognized by the presiding officer.• Public comments related to non-agenda items will only be heard during the Public Comment portion of

the meeting unless the issue is a Public Hearing. Public comments specifically related to an agenda itemwill be heard immediately prior to the Council taking up the item for deliberation.

• Speakers rnust state their naine for the record.• Any citizen requesting to speak shall limit him or herself to matters of fact regarding the issue of

• Comments should be limited to three (3) minutes unless prior approval by the presiding officer.• If a representative is elected to speak for a group, the presiding officer may approve an increased time

aflotment.• If a response from the Council or Board is requested by the speaker and cannot be made verbally at the

Council or Board meeting, the speaker's concerns should be addressed in writing within two weeks.• Personal attacks made publicly toward any citizen, council member, or town employees are not

allowed. Citizens are encouraged to bring their complaints regarding employee performance through thesupervisory chain of command.

concern.

Any member of the public interrupting Town Council proceedings, approaching the dais without permission,otherwise creating a disturbance, or failing to abide by these rules of procedure in addressing Town Council,shall be deemed to have disrupted a public meeting and, at the direction of the presiding officer, shall beremoved from the meeting room by Police'Department personnel or other agent designated by Town Council orOperations Manager.

General Town Council Meetin Information• Regular Town Council meetings are held at 7:00 PM on the first and third Tuesdays of each month at

the West Yellowstone Town Hall, 440 Yellowstone Avenue, West Yellowstone, Montana.• Presently, informal Town Council work sessions are held at 12 Noon on Tuesdays and occasionally on

other mornings and evenings. Work sessions also take place at the Town Hall located at 440Yellowstone Avenue.

• The schedule for Town Council meetings and work sessions is detailed on an agenda. The agenda is alist of business items to be considered at a meeting. Copies of agendas are available at the entrance tothe meeting room.

• Ag endas are published at least 4S hours prior to Town Council meetings and work sessions. Agendasare posted at the Town Offices and at the Post Office. In addition, agendas and packets are availableonline at the Town's website: www.townofwestyellowstone.com. Questions about the agenda may bedirected to the Town Clerk at 646-7795.

• Of fi c ial minutes of Town Council meetings are prepared and kept by the Town Clerk and are reviewedand approved by the Town Council. Copies of approved minutes are available at the Town Clerk'soffice or on the Town's website: www.townofwestyellowstone.com.

04/17/1512 (32(54

'IQWN OF WSST TELLONSIQNR Pagel 1 of 3Report ID( L160Cash Report

For the Accounting Periodl 3/15

saginning Trsnsf srsSalaaoa Reosivsd In

rransfers SndingDiebursed Out BalanceFund/Aooount

1000 General Fund101000 CASH101100 Investmeats - CD's101300 Investments -' Noney Narket Accou

101500 Investment-STIP103000 Petty Cash103100 Town Ofi'ice

103200 Petty Cash/WY Police Dept103400 Petty Cash-Recreation

Total Fund

598,883.560.00

158,9$1.13286. 12

0.000.000.000.00

758, 150. 81

299.990.000.000.000.000.000.000.00

299.99

159,398.710.00

200,000.00179,000.00

0.000.000.000.00

538,398.71

25$,624.11O.000.000.000.000,00O. 000. 00

258,624.11

1,170.27214,344.63529,041.86655,742.86

50.0050.0050.00

150.001,400,699.62

-179. 890. 46114,344 • 63570, 060.13$34,456.14

50.0050.0050.00

15D.DD1,439,271.64

2100 Local Option Taxation-Resort Tax101000 CASH101300 Investments - Noney Narket Accou101500 Investment-STIP102200 Bond Reserve Caeh Acct-104102215 STIP Investment-Rev Bond current101225 STIP Reserve Acct Town Hall 101

56,300.760.28

263,620.0011, 329.6276, 414. 32

135r 996. 31544,671,29

213, 113.290.00

130,000.000 19

11.0$7.2430.70

364 <231.42

O.DD0,000.000.000.000.00

278,46$.3S0.00

11,0'70.000.00

65 • 21$.470.00

354,756.85

0.000.000. 000.000.000.00

945.670.2$

3$1, 550. 0012, 329. $131,293.09

136,027.01S54, 145. 86Total Fuad

2101 Narketing 6 promotlone (NAP)101000 CASH101300 Investments - Noney Narket Accou101500 Investamnt-STIP

41, 070. 892,015,37

65,900.00109,9$6.26

3,872•000.300.00

3,$72.30

0. 00O.OD0.00

0. 000.000.00

9,904.250.000.00

9,904,25

36.038.642,015.61

65,900.00103,954.31Total Fuad

strict)2102 TSID (Tout'ism Suainese Ielprovelaent Di101DOO CASH

2111 Of f Street Parkiag11,580.00 0. 00 341.40 9,665.08 11,619.8910,052.37

101000 CASH101500 lnvestment-STIP

1,$20.766$,735.3370,556.09

0.0315.5115. 55

0. 000.00

0.000.00

0.000 • 00

I, $20.1968,750.8570(571. 64Total Fund

2210 Parks 4 Recreation5,737.36 1,700.0D 0.00 0.00 0.00 7,437.36101000 CASH

2211 Parks/Rec Donations - Teea Center5,15S.41 0.0$ 0. 00 0 00 0.00 5, 15$.491010DD CASH

2211 Parks - Volleyball Court3, $$1. 77 0.06 0.00 0.00 0.00 3.8$2.$3101000 CASH

2211 CCmlaunity Garden551 76 0.01 0.00 0.00 0.00 551.77101000 CASH

1214 Smoking Waters Day Camp -scholarehips2,360.31 0,04 0.00 0.00 0.00 2,360.35101000 CASH

1220 L(brary101000 CASH102130 Donations for Rxteneion Svcs Lib103000 Petty Cash

6,264.601,4S0.09

50.007,794.69

47,217,300.020.00

47,217.32

0. 000.000.00

0.000.000.00

16,568.19O.OD0.00

16,56$.29

36r 913 ' 611,4$0.11

50.0038,443.72Total Fu nd

2240 Cemetery101000 CASH101500 Investment -sTIp

5,211.846,$31.15

12,042.99

0.0$0.000.0$

0. 000. 00

0.000.00

0.000.00

5,211. 926,831.15

12,043.07Total Fund

Di/17/1512:32>54

IOMN OF MEST YELLGHSTOMS Psge> 2 ot IRepo'rt ID > L140Cash RepOrt

F or the Accounting Period: 3 / 15

SogianingSalanco ReceivadFund/Account In

Tsauatosa Tronetase SndingSslanoaDiebureed

2390 Dxug Forfeiture101000 CASH101500 Investment-6TIP

2,233.$427,858.$530,092.69

I•000•000.00

1,000.00

0. 000. 00

0. 001.000.001,000.00

1.000,000,00

3,000.00

231.$426,85$.8527>092.•9Total Fund

2392 CDSG-Local Source101000 CASH101500 Inveetmeat STIP

11,S05.1168, 822 .1280,628.49

175.1$0.00

175.18

0.000.00

0.000.00

0.000.00

11, 980. 954$, 822.1280,803.67Total Fund

2101 Cemetery Perpetual Care (7050)

101000 CASH101540 Inveetment-STIP

1,846.9535,924.8237>191.77

0.034.118 • li

0.000.00

D. 000.00

O.000•00

1,866.9$35,932.9337,799.91Total Fuod

2820 Gas Taa Appcrtionment101000 CASH101300 Investmenta - Noney Narket Ac101500 Investsent-STIP

9>092.9310,027.3645,005.•184,125. 90

2,487.041.48

li • 672,503.19

0. 000.000.00

0.000.000.00

O.DO0.000•00

11,579.9710.028.$465,020.2$86.629.09Totel Fuud

2850 911 smsrgency101000 CASH101500 Inveetsmnt-STIP

-10, 044.770•84

-10,043.93

D.DD0•00

0.000.00

D.DD0.00

l. 112.210.00

1,112.2'1

11. 157. 040.$4

11, 156.20Total Fund2917 Crlme Victime Assistance

101000 CASM3050 GO Sond

101000 CASH101300 Investments - Noney Narket Accou101500 Inveetment-STIP

20.053.67

90,494.07$4,223.4247,464.32

222, 381. 81

414 • 5412.4710 • 76

437. 71

0.00 0.00

0.000 000,00

0.00

0.00D.OD0.00

0.00

0.000.000.00

90, 908. 6184.235.8947,675.08

222,$19.58

20,053.61

Total Snnd4000 Capital Projects/Hquipment

101000 CASH101900 Investment -STIP

6. 70S • 4188,135.0594,S43.46

0.0$19. 9019. 98

0.000.00

0.000.00.

1.200.000.00

1,200.00

5,508.4 •SS, 154,95 .93,6$3:44Total Fund

4060 puhlic Horks Eguipment Replacemeu101000 CASH101500 Inveatamnt-STIP

1,255.75238. 01

1,•93.76

0.000.050.05

D. 000.00

0.000.00

0.000.00

1,255.15236.06

1, • 93.81'total Fund4010 Parkway Construction/Ntn

101300 Investments - Noney Narket101500 Investment"8?IP

Accou 2. 761. 654,058.296,819. 94

0 • 410.921.33

0.000.00

0. 000,00

0. 000.00

2,762.064,059.216. 821. 27Total Fund

4075 Street Conetruction /Maintenance244,214.2$ 55.58 0.00 0.00 0.00 246.269.86101500 Investment -STIP

5210 Mster Operating Fund1D1000 CASM101300 Inveatsmnts - Noney Narket1D1500 Investment-STIP102245 Replacaueut 6 Oepreciation Ra

Accou67,553.1110,027.36

182,193.24148,701.49408,477.40

17.525.701.48

41 • 1333.5&

11, 601.87

0.00D.DO0.000.00

0.000.000.000.00

9,899.640.000.000.00

9,899.84

75,178.9710,028.$4

182.234.3714$>737.25416, 179. • 3xotal Fund

04/17/1511i33c54

TOWH OF WEST YELLOWSTONE Fagec 3 ot 3Report IDc LlloCaeh Report

For the Accounting Pericdi 3 / 15

Transters TranatereFund/Account Reoeived Xn OutOfabursad

5220 Water Replacement Depreciation Fund101000 CASH101500 Investment-sTIP

11. 077,00111,839.23222,916.23

0.0047.5347,83

0. 000. 00

0.000.00

0.00 11, 0' 7 7 .000 • 00 111, 687. 06

222,964.06Total Fund5310 Sawer cperating Fund

101000 CASH101300 Investments - Iloney Narhet Accou101500 Investmsnt-STIP101510 Had Add construction-sTlp102245 Replaceaent 6 Depreciation Ent.

130,399.5464, Osl.36

365,999.7560, 487. 16

129, 921. 61750,892.62

41,535.369.49

50,082.6213.6629.32

91,670.45

1, 027 • 300.000•00o.oo0•00

1,027.30

50,000.000.000.000.000.00

So,ooo.oo

12, IC7.66O. 000. 00O.00O. 00

22,l67.66

100, • 94. 5464.O91.95

416,082.3760.501.02

129,950,93771, 122. 71Total Fund

5320 Sewsr Replacement oeqreciation Fund101000 CASH101500 Inveatment•STIP

322.00270,185.59270•507 59

0. 0060.9960.99

O.oo0.00

0. 000.00

0.00 312.000 .00 270, 24 6 . 58

270,568.58lotal Fund7010 Social Services/Help Fund

101000 CASH 1,079.41 0.00 0.00 329. 80 26, 61 4 . • I25,866.207195 Court Collections Trust Acct

101000 CASH 0.00 0.00 0.00 0 • 00 11, 80 C • 4911,806.4974 58 Court Surcharge HB17C

101000 CASH7467 HT Lacc Entorcument Academy (NLEA)

O. 00 0.00 0. 00 0 .00 15, 100. 0 015, 100. 00

101000 CASH 0.00 0.00 0. 00 14,984.00I • , 9 84 . 0 07465 publ)c oetender Fee

101000 CASH7469 City Court - Judge Srandis

0. 00 0. 00 0.00 O. 00 2, 461. 002,461. 00

101000 CASH7910 Payroll Fund

1,765.00 0.00 0.00 1,420•00 6,881.00C,$36.00

101000 CASH O. 00 197, 615. 99 232,271.86 0 00 -6,697.8727,960.007930 Claims Fund

101000 CASH 0.00 135r248.02 144,066•57 9,016.4617.835.01

Tatals 4,S01,810.32 1,303,193. ll 334, 191. 30 I,320,843.39 334, 191. 30 •,784,1CO.37

• ~ • Transtera In and Transters Out columns should match. There are a couple exceptfona to thisc 1) Canceled Electronic Checha and1) Payroll Jouznal vouchera that include local deductions set up with receipt accounting, please aee cash rsconciliatfon procedurein manual or call to r more details.

84/13/2815 86 :58 4866 464977 FIRST SECLIRITY BAM< PAGE 81/Bl

IFlreg Secll~ I

REPURCHASE CONFlRMATION

Treasurer's OfficeTown of West YellowstoneP.O. Box 1570.West Yellowstone, MT59758vla Fax: 646-7511

Tax IO Number: 81-0299400

REPURCHASE CONFIRbhATION

ABreement Number:Trade Date:

Settlement Oate:Maturlty Oate:

Repurchase Rate:

Current Balance:ued lnterest:

607229004/10/20154/10/20154/18/2015

0,036% tThe avarage invastrnent rtta for Bl-day T-BPls, adjusted weekly.)

$541,286.26$5.16

SECURITIES DESCRIPTlON

allatln County, MT SD 044Madison County, MT K-12 SDLake County, MT SD tttM

MarketCUSIP Rats Matu Par Value

36370NBL8 3.00' 6I15 I2016 $2 00,000 $202, 98955734RAZO 2.00% 7I1/2017 $376,000 ' $388,801509405872 2.00% 7l1 /2016 $300 ,000 $30 2 871

82 661

Fractional Interest in Securities': N4A

"Froctional Interest c ((Current Balance)/(Marlret Value)J 8'

This Repurchase Agreement ls not a deposltand is not covered by FDIC depositinsurence or the FDICTransaction Account Guaranty Program. In the event of a bank fallvre, the Town of M/est Yellowstone wlllbecome the owner of the Securltles, or obtalns o perfected securlty Interest in these Securitles.

Operatlng Account InformationAccount Number:

Date:Balance;

Current Rate:Accrued Interest:

607228924/13/2015$9,565.54

$0.00

Money Market Account lnformationAccount Number:

Date:Balance:

Current Rate:Accrued Interest:

606062854/13/2015

$702,207.290.19%

$43.866.00%i

04/17/1515I5$I09

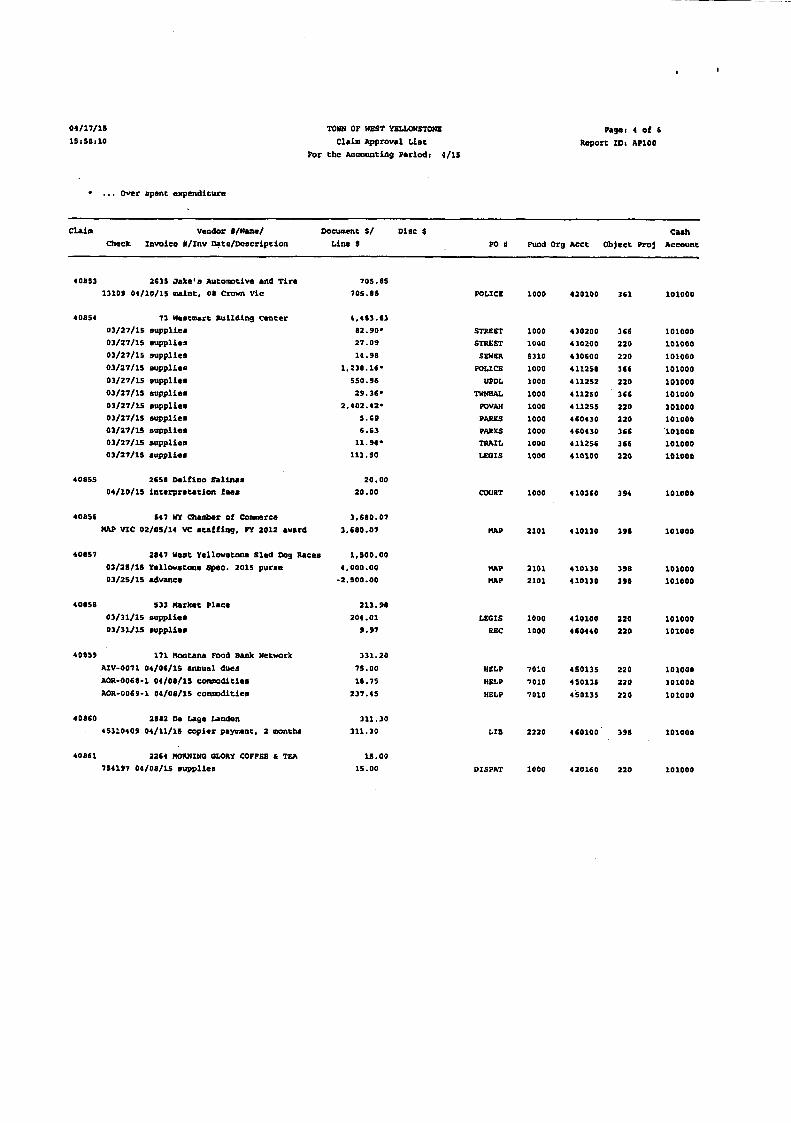

TOWN OP NEST IELLOWSTONEClaim Approval List

PageI 1 of 6RepOrt ID: AP100

For the Accouncing periodi • /15

.. . over speat expendicure

Claim vendor 6/Name/ Document 8/ Di sc 8

Line 8Cash

po 8 Fund org Acct object Proj Accountcheck Invoice 8/Inv Dare/Dascription

4079$ 155L Thyssenkrupp ElevaCor Corp3001754829 04/OL/15 elevator mainc-Povah

38$•273$$.17 • POVAW 1000 411155 350 101000

40791 246 Utilities Underground Location5035295 03/31/15 axcavation notifications

5035295 03/31/15 excavation notifications

20.0210.0110.01

NATERSEWER

430500 357 101000• 30600 357 101000

52105310

4 07 9'2 2$4$ Eaeting, Xauffman 8 Mersen, PC

bill spans services for 3 months04/D5/15 legal sarvices04/05/15 postage/copies04/05/15 phone/f ax04/05/15 travel

19,500.49

LEGALLEGALLEGALLEGAL

1000100010001000

• 11100411100411100411100

351S70345373

1010DO101000101000101000

19, 317.5080 • 41

3. 90• $.6$

40797 255$ Rebgea Basin Pire District

04/15/15 April 2015•5,563.00

45.563.00 1000 410400 357 101000FIRE

40798 146 Morrison-Maierle, Inc20843 04/07/15 po online backup20$44 04/07/15 Tova offices online backup20863 04/06/15 Netvork maint/support

707.5070.0060.00

577.50

1000 420160 399 1010001000 410510 356 1010001000 • 20160 39$ 10100D

DISPATFINADM

40799 154C Century Link OCC 48.'3348,23 f inadm 1000 410510 345 10100003/23/15 IOag diet Chg 40CvAC-7COO

40$0104/01/1504/01/1504/01/1504/Oi/15Oi/01/15

04/01/150 • /01/1504/01/1584/01/1504/01/1504/01/1504/01/1504/01/1504/01/1504/01/1504/01/1504/01/1504/01/1504/01/1504/01/15

1789 NEX Bank07 Pord Expedition C-545C3A06 Dodge Durango c-137410 Ford Crovn Vic 6-34157A0$ Ford Crcwn Vic C-143710 Pord Expeditica 6 •0000•611 Ford Expediticn • -21425A77 Intl Dumptruck78 chevy oueptruck7$ Autocar Dumptruck•5 Pard F-350140 G GraderCAT 936 Losder93 Dodge 4•58295 MObile 6vaeper97 Athey SveCper99 SS Snovblover00 Preightliner Dump 6-40700$Snovmohile01 Freighcliner Dump 6-54564Aoe Ford Pickup • - 1 450

1,132.1039.7789.05•5.6913.44

177,12307. 51

0.000.000.00

55.39119.29186.32

'IS. 400.000.000.000.000.000.00

87. 11

SSPOLICEFOLICEPOLICEPOLICEPOLICESTREETSTREETSTREETSTREETSTREETSTREETSTREETSTREETSTREETSTREETSTREETSTREETSTREETSTREET

450135•302004201004201004201004101004301004302004302004302004302DO4301DO• 30100430200430200430200430200420100430100430100

131231131231131'231231131231131231231131131131

131231131231131

1010001010081010001010001010001010001010DO101000101000101000101000101000101000101000101000101000101000101000101000101000

10001000100010081000LOOO1000100010001000100010001000 .1000100010001000LOOO10001000

04/17/1$Is>50110

TOWN OF WEST YELLOMSTOMEClaim Approval Lisr

lagei 2 of 6Raport ID: AP100

For the Aeeounting Periodi 4/1S

• •.. Over spent expenditure

Claim vendor 8/Name/ Document 8/ Disc 8line 8

CashPO 8 F und Org Aect Object Proj AceountCheck Invoice 8/Inv Date/Descriptlon

04/01/15 00 GNC Pickup 6-14$404/01/15 00 CAT 930H Loader04/01/1S 00 904$ MiniLoader

04/01/15 TNP Truek 8104/01/1S YNP Truck 8204/01/15 00 Ford Rseape (multi-use)04/01/15 14 Police Intercsptor

129.36391.92189.10

0.000.00

31.03139. 62

STREETSTREETSTREE1'STREETSTRSETDISPATPOLICE

1.000100010001000100010001000

430200430200430200•30200430200• 10510420100

231231231231231310231

101000101000101000101000101000101000101000

40$33 2613 Pirst Bankcard03/03/1S carrot Top, flags03/03/15 Carrot Top, flags03/09/15 Rossiter Elec, svltch, motor03/10/15 NF Gov online. regis Arnado

03/12/15 Home Depot, supplies, vac03/20/ls Home Depot, schlage csms

I .S80.0342 004

268. 12560 00

15. 0015$.91• 16. 00 •

POVAHTWNHAL

SEWERSLDINS

POVAHTRAILH

100010005310100010001000

4112$5411250•30600420531411255411256

220220369380366366

101000101000loloaa101000101000101000

40034 999as Departsmnt of Revenue

04/02/15 tax vithholding pmt penalty

270.00270.00~ FINADM 1000 410510 870 101000

• 0035 54 Soseman Daily Chzonicle

04/Ol/15 subscziption, Police Dept04/ol/ls subscrlption, Tovn Mall

451. 60220 Oo i

228. 00 i

ADMINDISPAT

1000 410210 333 loloao1000 420160 333 101000

40036 2601 chemnet Consortium. Inc.0203$ 03/24/15 random dzug test fea

35.0035.00 AOMIN 1000 410210 3S1 101000

40837 29aO Joel Feterson Appraisal, Inc.

715 04/03/15 ESS appzaisal2g500.00

2,500•00 101000ADMIN 1000 •1 0210 3SS

04/01/15 supplies04/01/15 supplies

04/01/15 credit

40030 135 Food Roundup 3. 393•592.67

-2.87

FINADMSEMERLEGIS

1000 410510 220 . 1010005310 430640 351 1010001000 410100 220 101000

40$39 1404 VS SANK3933017 03/25/15 paying agent fee. GO bond

350.00350.00 GO 30$0 4 90100 630 101000

40840 2140 MMIA MONTANA

315016 a4/oa/15 deductible zecover, A. Frank1,310.00

1,310.00 • I H8 1000 510330 512 101000

40041 1454 sozeman chroniele/Blg Sky12$9934 03/15/15 J. serger Retire ad

110.7S110.75 ADMIN 1000 410210 327 101000

01/17/1515<5 • ilo

TOWN OP WSST YELLOWSTDNS

Claim Approval ListPage> 3 of 6

Report ID: AP100Por the Accounting Periodi 4/15

• .. . Over speat expendicure

Claim Vendor 8/Name/ Docuamnt 5/Line 8

Disc 8 Cashpo 8 pund Org Acct ob3ecc Proj Accountcheck xnvoice 8/Inv Date/Description

10842 1331 west Yellovstone Foundation01/07/16 Sus funding, 2nd half PY 15

7,500.007,500.00 LEQIS 1000 410 100 870 ID1000

40813 40 Jerry's Enterprises03/13/15 mouse03/13/15 compucer accessories

65.9717. 9947.98

1000 420160 220 1010001000 420160 220 101000

OISPATDISPAT

1081• 1241 Saf eguard 321. 32321.32 DXSPAT 10OO 12O16O 22O 1OIOOD30579551 03/20/15 parking tickete

10815 2507 Silvertip Pharmacy

03/1$/15 Rx04/01/15 Rx04/03/15 Rx01/09/15 Rx

133.0050.0025.0D25.0033.00

HEIPWELPNELPRELP

7010701070107010

368358358358

1010001010001010001010DD

450135450135450135450135

40$46 1$9 NSE ANALYTICAL iAEORATORY 396.0019$.0D198.00

WATERWATER

5210 1 30500 357 1010005210 430500 357 101000

15020$4 02/16/15 vater samples150307$ 03/15/18 vacer samples

40847 2761 ND Supply Watervorks. Ltd. 183.521$3.52» SEWER 6310 430600 369 101000D172621 D4/08/15 sever eupply

40$4 • 2686 Waxie Sanitary Supply75206283 01/10/15 cuscodial supplies

$26.35$26.35 PARES 1000 160430 220 101000

40849 951 Sarnee 6 Noble 202.9113.4967. 9535•57$5•90

LIB 2220 215LIS 2220 215

LIB 2220 215LIS 2220 215

•60100460100460100160100

101000101000101000101000

2999434 04/01/15 books2999435 01/01/15 booke2997S19 03/28/1.5 books2997978 03/2$/15 books

40850 761 oeneral Distributing Co. 43.7113. 71 STREET 1000 430200 220 1D1000319110 03/31/15 compressed 02

40$51 151 Oallatin Councy WY TS/Compoet 435.75435.75 PARKS 1000 460430 534 1D100003/31/16 cransfer station charges

40$52 379 Energy Laboratoriee. Inc350460628 04/10/15 vasrevater eamples

297. 5019'7 • 50 SEWER 5310 430640 357 101000

04/17/1515PSSP10

TOMN OF MEST YELLOMSTONE

Claim Approval L is tPagei 4 of 6

RePort IDP AP100Por che Accounting Periodi 4/15

• .. . Over spenc expenditure

Claim vendor 5/Name/ Document S/Line 5

Disc 6 CashPo 8 Fund org Acct object Pro) AccountCheck Invoice 8/Inv Date/Description

• 0$53 2635 Jake'8 Autosotive and Tire131D9 04/10/15 maint, 0$ Crovn Vic

705.85705.$5 POLICE 1000 410100 361 101DOO

4085403/27/1503/27/1503/27/1503/27/1503/2'P/1503/27/1503/27/3503/27/1503/27/1503/27/1503/27/15

71 Mastmart Building Centersupplies•uppliessuppliessupplies•uppliessuppliessuppliessuppliessuppliessupplies• upplies

• >4•3 . 6 382.90•27.0914.9$

1 138.16 •550.9629.36•

1 401. • 1 •5.696.63

11. 94 •113.50

STRESTSTREET

SEMSRPOLICE

UPDl

10001000531010001000100010001000100010001000

43020043020043060041125$411252411250•112554 60430460430411256410100

36611022036622036622022036636C220

101000101000101000101000101000101000101000101000101DOO101000101000

PARKSPARKSTRAILLEGIS

40$55 2CSO Delfino Salinas

04/10/15 interpretation fees20. 00

20.00 COURT 1000 • 103CO 394 101DOO

40856 547 MY chasher of CossmrceNAP VIC 02/05/14 VC Staffing, FY 1012 avard

3.680.073,680.07 MAP 2101 • 10130 39$ 101000

40857 2$47 Nest Yellowatona Sled Dog Races

03/15/15 Yellovscone spec. 1015 purse03/25/15 advance

1,500.004,0OD.OO

-2,500.00MAP 2101 410130 398 101000MAP 1101 410138 39$ 101000

4o$5$ S33 Market Place03/31/15 supplies03/31/15 supplies

213. 98204.01

9•97LEGIS

RSC1000 410100 220 1010001000 460440 220 101000

40$59 171 Mcntana FOO4 Bank NetwerkAIV-0071 04/06/1S annual duesAOR-006$-1 04/0$/15 cosmodiciesAOR 0069-1 04/OS/15 commodities

331.2075.001$.75

137.45

HE1 P 7010 450135 220 101000MELP 'POlO 450135 220 101000HELP 7010 450135 220 101000

40$60 2882 De Lage Landen45310409 04 /11/15 copier payment, 2 monchs

311. 30311.30 LIB 2120 4C0100 39$ 101000

40861 2264 FIPRNING GLORY COFPSS 6 TEA

75419'p 04/0$/15 supplies15.00

15. 00 DISPAT 1000 420160 120 101000

04/17/1515fSof10

TONN OF WEST ISLLOESTONE

claim Apyroval ListPagei 5 of 6

Report ID: AP140For the Accountfng Pertodi 4/15

• ... Over spent expenditure

vendor 5/Nacc/ Document 8/Line 6

Disc 5 cashPO 5 pund Org Acct object proj AccountCheck Invoice 5/Inv Date/Descriytion

40861 2813 STAPLES Credit P l a n03/12/15 supplies03/12/1S supplies

427.6947.47

360.221000 410230 210 1010001000 420160 220 101000

JAILDISP

40863 2835 Corner Cenex 15. 7615.76 LEGIS 1000 410100 220 101000849 03/31/15 supplies

44864 1331 west Yellowstonc Foundation04/07/15 bus vouohers

3D. 0030.00 7410 • 50135 220 101000

4086S 29 Terrell's Office Machines Inc $2.%0%2.50 LIS 2220 460100 398 141000299545 04/01/15 maint contract, copier

40SSS 331 Allegra 77,9077. 90 FINADM 1000 410510 390 1D100022820'2 04/15/ls yerforate paper, hus licensee

40867 2707 MSQ Extension 890.00390.00250.002%0.00

FINADMFINADMPINADM

1000 410510 335 1010001000 41051 0. 33$ 1010001000 4105 10 335 1010DD

04/16/1% Institute regls. Holtren04/16/ls Institute regis, Gospodsrek

04/16/1% Institute regis. Roos

40868 1140 Sagebrush Floral • 0. 0040.00 REC 1000 460440 110 101000591431 04/07/15 flowers, dance recital

40869 2%14 Kathy Arnado 276.00176.00 SOCSER 1004 4 50135 370 10100044/17/1% motel + meals, Hissoula, Arnad

40870 2291 American ExpressAmason, phone accessoryCostco, wire racks 6 boxesCabela's, gift card, Dittmann

Xbix, console repair/replaceXhix, console repair/reylaceXhix, return. credit next mo.walmart, microwaveWild Nest, suppliesMslwarebytes, vi r us softwareMalwarebytes, virus software

2,777.6831. 74

549. 95 •500.00781. 22250.00410. 06116.7971.0724.9541. 90

DISPATDRDG

LEGISDISPATDISPATDISPATDISPAT

LEGISLI8LIS

1000239010001000100010001040100022201110

4 2oloa Eo a420141 220410100 2104 20160 361410160 369420160 362420160 220410100 120460100 2164601ao 216

1410001010401D1000101000101004101000141000101000101000101040

03/10/1%43/12/1503/13/1%43/13/1%03/13/1503/13/1%03/17/1543/17/1504/04/1504/04/ 1%

Total : 101 , 1 3 8 . 978 of Cla ims 4%

04/17/1515a55ilO

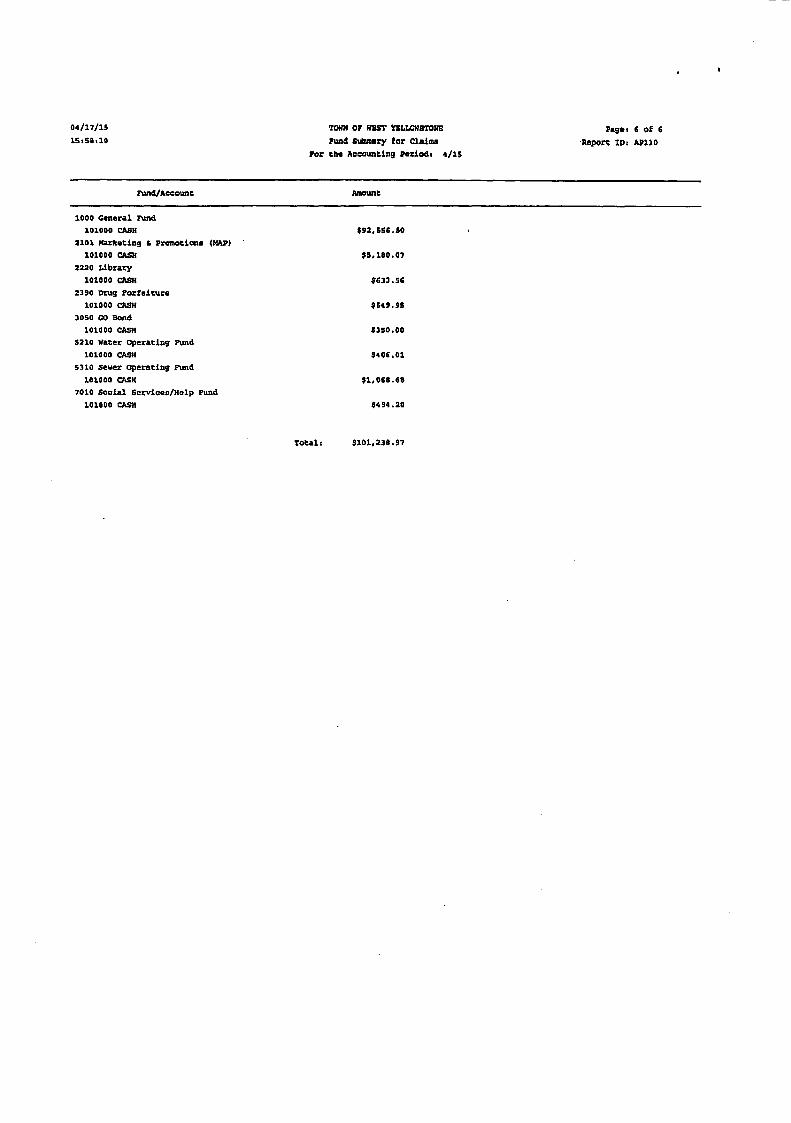

TOHN OF HSST YSLLOHSTOHE

Fund s|99nary ior claimePaget 6 09 6

Report Ipc ApllDpor the Accounting periodi 4/15

Fund/Account

1000 General Fund1010DO CASH

2101 Harheting 5 pzoaotione (HAP)101000 CASH

2320 Librazy101000 CASH

2390 nrug Forteiture101000 CASH

3050 GO Bond101000 CASH

5210 Hater operating Fund101000 CASH

5310 sewer operating Fund

592,556.50

55, 150.07

0549.95

535D.OO

6633.56

5406.01

101000 CASH7010 Social Services/Help Fund

101000 CASH

51,065.65

6494.20

Total < 5 101, 2 3$ • 97

WEST YELLOWSTONE TOWN COUNCILTown Council Meeting 4k Work Scssion

Aprll 7, 2015

COUNCIL MEMBERS PRESENT: Mayor Brad Schmier, Jerry Johnson, John Costello, ColcParker, Greg Forsythe

OTHERS PRESENT: Finance Dircctor Lanie Gospodarck, Assistant Pubiic ServicesSuperintcndent David Arnado, Social Services Assistant Kathi Arnad, Town Attorncy JaneMcrsen

The meeting is called to order by Mayor Brad Schmier at 7:00 PM in the West YellowstoncTown Hall, 440 Yellowstone Avenue, West Yellowstonc, Montana

Portions of thc meeting are being rccordcd.

The Trcasurcr's Rcport with corresponding banking transactions is on file at the Town Officesfor public rcvicw during regular business hours.

WORK SESSION

lvfayor Schmier calls thc meeting to order and explains that thc first itcm of discussion is theCollective Bargsining Agreement for the West Yellowstone Employecs Unit of thc MontanaPublic Employees Association. Schmicr asks Council Mcmbcr Johnson and Financc DiiectorLanie Gospodarc,k to describe thc agrcement and answer any questions from the Councll. Thcagrecment has becn approved by the Employces Unit and is on thc agenda for considcration bythe Council latcr this evening. Johnson explains the language changes madc to the section thataddresses the use of floated holidays. Other changcs were made in the agrcement that affecttaking vacation timc, pay out of sick leavc, steward release during work hours, probation,scniority, advance leave time requcsts, grievance process, unifonn provisions, health andwellncss, and compensation. Johnson and Gospodarck answcr multiple questions from theCouncil, Mayor Schmier points out that thc language about thc treadmill in thc bascment of theTown Hall may conflict with Pollcy No. 31. Johnson points out that tlds contract is only for twoyears, unlike thc prcvious contract that was for six years. He says that was easily agreed on andno one was happy about the fact that it took so long to ncgotiatc this contract. Johnson thanksevcryone that workcd on the agrcement for their time and efforts, hc also thanks Town AttorneyJane Merscn for her advice and guidancc through the process.

Mayor Schmier says they have two major employee recruitments underway, the OperationsManagcr and Social Services Director. Thc Council discusses the proposal thcy recentlyreccivcd fiom thc Prothman rccruiting firm, a firm out of Washington statc that specializes inrecruiting management positions fbr iocal governmcnts. The Prothman proposal offers toconduct the recruitment for $18,000 plus expcnscs. Schmier points out that othcr jurisdictions inthe rcgion lncluding Belgrade and Red Lodge have used this firm. Alter further discussion, theCouncil indicates th'at they would likc to procced with thc process and direct thc staff to rcquest aspccific contract for action by thc Council at the ncxt mceting.

Thc Council discusses thc job announccment, salary, and job description for the Social ScivicesDirector. Thc Council makes rccoinincndations for minor changes to the job description andMcrscn agrccs. The Council directs the staff to start advertising for the position.

The Council adjoums thc work scssion at 7:15 PM and the regular meeting starts at 7:30 PM.

ACTION TAKEN

I) Mot ion carried to approvc the claims which total $71,131.74. (Forsythe, Parker)

2) Mot ion carried to approvc the Consent Agends, which includes thc minutes of thc March17, 2015 Town Council Meeting and March 31, 2015 Town Council Work Scssion.(Forsythe, Parkcr)

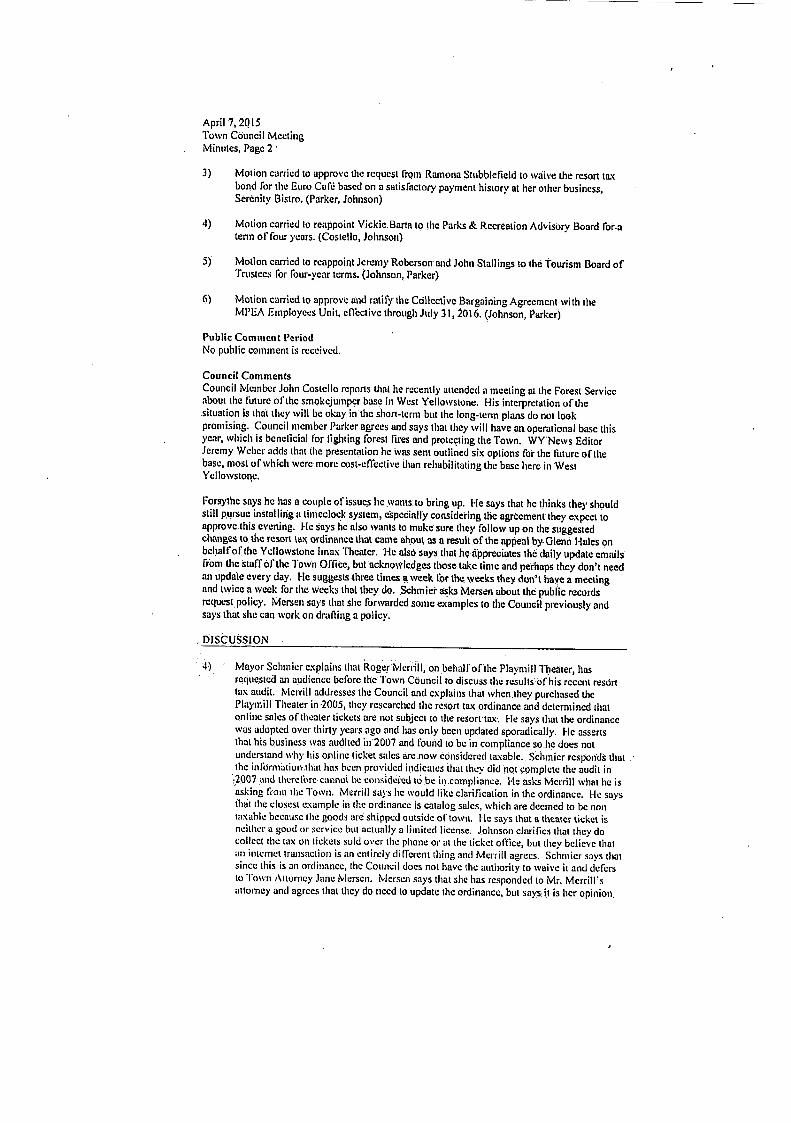

April 7,20I5Toivn Council Mectingiulinutcs, Pagc 2

3) Mot i on carricd to approvc thc rcqucst Irom Ramona Stubblefield to waive the resort taxbond for the Euro Cafd based on a satisfactory payment history at her other busincss,Sercnity Bistro. (Parker, Johnson)

temi of four ycars. (Costello, Johnson)

Trustees for four-ycar terms. (Johnson, Parker)

4) iMotion carried to reappoint Vickie.l3arta to the Parks <Ik Recreation Advisory Board for.a

5) hl o t ion carried to rcappoint Jeremy Roberson and John Stallings to the Tourism Board of

6) iblotion carricd to approvc and ratil'y the Collcctive Bargaining Agreetnent with theMPEA Employees Unit, elTectivc through July 3I, 2016. (Johnson, Parker)

Public Camntcnt PcriodNo public commcnt is rcccivcd.

Council Comments

Ycllowstonc.

Council lvlcmbcr John Costello rcports that he rccently aucndcd a mceting at the Forest Serviccabout the Ibturc ofihc smokcjumper base in West Yellowstone. His interpretation ol the.situation is that tliey will be okay in thc short-term but the long-term plans do not lookpromising. Council mcmbcr Parker agrces and says that they will have an operational basc thisyear, which is bcnclicial for lighting forest fires and protecting the Town. WY News EditorJeremy Wcbcr adds that thc presentation hc ivas sent outlined six options for thc future ol'thebase, most of which werc morc cost-elTcctive than rehabilitating thc basc here in West

Forsythc says hc itas a couple of issucs he wants.to bring up. I.le says that he thinks they shouldstill pursuc installing a timcclock system, e'spccialfy conside'ring tlie agrccment they expeci toapprovc.this cvening. I-le says he also wants to make' sure thcy follow.up on the suggestedchanges to the resort tax ordinancd that came about as a result of the appebl by. Glenn Hales onbehalf of the Ycllowstone Imax Thcater. He also says that hc a'ppreciates thg daily update cmails'fi'om thc 'staff'of thc Tow'n OAicc, but acknowledges those takc time and perhaps they don't needan update cvery day. I-Ic sugg>ests three times a week for the weeks they don't have a mectingand nvice a week for the weeks thal they do. Schmier asks Mersen about the public recordsrequest policy. Mersen says that shc fonvardcd sonie examples to the Counc'il previously andsays that shc can work on dralling a policy.

, DISCUSSIOiq'

) lvl ayor Schmicr cxplains that Roger ivlcrrill, on behalfof'the Playmill Tlieater, has

tax audit. <Mcrrill addresses thc Council and explains that when.they purchased thcPlaymill Theater in 2005, they rcscarched the resort tax ordinancc and dctcrmincd thaionline salcs of theater tickets are not subjcct to the resort tax; I-le says that the ordinanccwas adoptcd over thirty years ago and has only becn updated sporadically. I-Ie asscrtsthat his business was auditcd in 2007 and found to bc in compliance so.hc does notunderstand why his onlinc ticket salcs arc.now considcrcd taxable. Schmicr rcsponds that ..the inl'ormation tliat luis b«cn providcd indicates that th«y did hot complctc the audit in;2007 pttd thcrcforc-cannoi bc considcinl to be in.compliance. Ide asks lvlcrrill ivhat hc isusking from the Town. Mcrrill sayshc ivould likcclarilicationin theordinancc. Hi'. Saystliat ihc closest cxamplc in thc ordinance is catalog salcs, which are dccmcd to be liolttaxahlc bccausc the goods are shippcd outsidc of town. I-Ic says that a theaicr tickct isneither a g>ood ur scrvicc but actually a limited license. Johnson claiilics thai they docollcct thc tax on tickeis sold over the phone or at the tickct office, but they bclicvc thatan inicrnct triuisaction is an entirely dilferent thing and Merrill agrecs. Schinicr says thatsincc this is an orctinancc, the Council docs not havc thc authority to waive it and dct'crsto 'I'oivn Aitomcy Jane ivlerscn. Ivlcrscn says that shc has responded to ivlr. iVlcrrill<sattorney and agrees that thcy do nced to updatc thc ordinance, bui says it is hcr opinion

requested an audiencc bclorc thc Town Council to discuss tlic rcsults'ofhis rcccnt reson

April 7, 2015Town Council MeetingMinutes, Page 3

'thai purchasina a.ticl;ct over tlie iiiternci is'mcrcly'a prc-paymeni-foi the cxperience.i'riIVcst.Yelloivstone and therefore is subject to the tax .-

appreciates their elforts. Johnson asks the rest ol'ihe Council if thcy w'ould likc them tomove fonvard with negotiating thc collective bargaining agreement with the Policc unit.1 he Council agiees and designatcs Johnson and Gospodarek to proceed with thatncgotiation,

6) Cos tello says that hc would likc to crcdit both sidcs for working on this agreement and

A) Adv i sory. Board Reports: Coimcil Member Cola Parkbrrcport's that the Planiiing Board

reports that he talked to Glen Loomis.who has closcly been monitoring klousc Hill 262.The bill is inde'finitely frogen biit the majority leadcr from Dillon has the option olbringiiig it back to the t1oor for'another vote. Loomis is optimistic that this is a realpossibility.

Guay about the two appraisab thcy arc waiting for. ChicfofPolice Scott Neivell reportsthat Officer Kearncy is doing vcry wcll and hc is working with thc Operations Managerto draA an offer of employmeni for a sccond agrcemem. He says that remodeling isgoing well.at the Policc Dcpartment. Mayor Schmier asks about the agreement withGallatin County.Shcriff Ddpartment is going and il'thcy will be able to release theCounty deputies from that.obLigation in the near future. Neivell says that Officer Couitisis on vacaiion right now but as soon as hc returns he thinks thcy will be able to cover allof thcir shifts and no lo'nger require thcir assistancc.by the timc the summer season takes.,Social Services.Assistant Kathi Arnado says that things are going vvell in hcr departmcntand slie is getting assistancc Irom Public Services io pick up food. They will, however,lose the assistancc of Frank Bdzold as a voluriti:cr on the 17'" of thc month. FinanceDirector Lanie Gospodarek says that shc'is starting to work on budgct prcparation.Schmier notes that the sewer fund is ovcrdraw'n. Gospodarek says that they did notanticipate the substantial increase in the elcctric hills for the new blowers at the lagoonsand that line is over budget. Assistant Public Serviccs Superintendent Dave Arnado saysthat they are nearly finished wiih thc carpet projcct at thc Povah'Center and will be ablcto focus on finishing at the Policc station. 1-lc indipatcs hc iviB also talk to represcntativesfrom DOT.about the Canyon Street project tomorrovv.

has bccn mccting regularly dnd is making progrcss on the Grosvth Policy. Johnson

B) Oc p artment Head Reports: Schmier reports on behalt'of Operations Manager Becky

CORRESPONDENCE/FYI

Dated March 11, 20'15, the West Yellowstonc Brownic Troop ivrites io express a concern andimpr'ovement suggestion for thc playground at Pioncer Paih:. Dated March 23; 2015, GayleGifford, CEO of the Montana Foodbank Network, ivrites to announce that the MarketPlacegroccry store and volunteer Frank Bczold are being recognizcd by the hiontana First Lady LisaBullock at the State Capitol on Friday, April 17, 2015.

The mecting is adjourned..(8:)5 PM)

ivlayor

ATTEST:

Town Clcrk

WEST YELLOWSTONE TOWN COUNCILWork SessionApril I4, 20IS

COUNCIL MEMBERS PRESENT: Mayor Brad Schmier, Jerry Johnson, Grcg Forsythe, ColeParker, John Costello

OTHERS PRESENT: Finance Director Lanie Gospodarek, Public Services SuperintendentJames Pattcrson, Town Attorney Jane Mersen, Jercmy Weber-Editor, West Yellowstone Ncws,Hclene Rightenour