Embed Size (px)

Citation preview

March 9, 2017 | 1

March 9, 2017 | 2

01

2016 OVERVIEW AND OUTLOOK

March 9, 2017 | 3

Carrefour, the reference in food retail

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 3

March 9, 2017 | 4

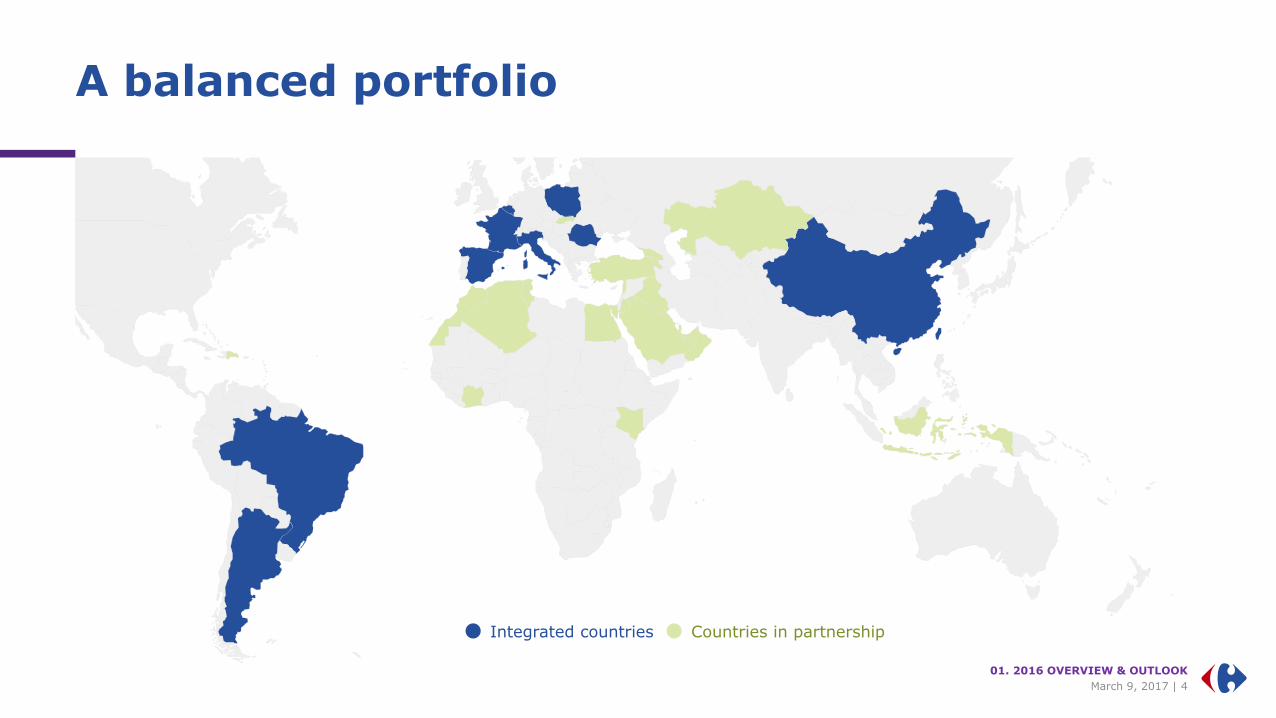

A balanced portfolio

Integrated countries Countries in partnership

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 5

Carrefour: The reference in food retail

Food represents 83% of the Group sales in 2016(growth of over 4% in 2016)

01. 2016 OVERVIEW & OUTLOOK

Quality

accessible to all

Unique know-

how

in fresh produce

Pioneer

in organic food

and Quality Lines

Powerful

exclusive brands

Sourcing

expertise

March 9, 2017 | 6

CSR is at the heart of Carrefour’s know-how

Fight wastage Biodiversity Partnerships

Food

Climate – Energy

Packaging

Waste

Agroecology

Sustainable fishing

Sustainable forestry

Beekeeping

Diversity

SMEs and Producers

Nutrition/Health

Solidarity

Included in the Dow Jones Sustainability Index Europe in 2016Present in the DJSI Europe, Stoxx Global ESG, FTSE4Good, Ethibel

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 7

Carrefour, pioneer in organic products

ROLL-OUT OF ORGANIC FOOD AREAS IN STORE

DEVELOPMENT OF OFFER ACQUISITION OF GREENWEEZ

PROGRAM TO ACCELERATE ORGANIC FARMING

PARTNERSHIPS WITH 300 FARMS BY 2020

3,000 ORGANIC FOOD SKUs

OF WHICH MORE THAN 800 UNDER

PRIVATE LABELS

+32%

ORGANIC FOOD SALES IN 2016:

LEADING ONLINE ORGANIC FOOD RETAILER

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 8

A multiformat Group: “Everyone under one roof”

First hypermarket Promodès Atacadão

Accelerationin convenienceBilla, Dia, Eroski

1999 20072012

to 20151963

Rue du Commerce

2016

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 9

The center of gravity is shifting towards convenience

BREAKDOWN OF STORES UNDER BANNERS BY FORMAT

5,4797,075

9,000

2,986

3,227

3,700

1,366

1,328

1 450

164

305

350

2012 2016 2019e

9,995 stores

11,935stores

14,500stores

Evolution 2012 vs. 2019e

+100%

+6%

+24%

+ 64%

Cash & CarryHypermarketsSupermarketsConvenience

GROSS SALES BREAKDOWN – (%)

58%51%

<50%

42%49%

>50%

2012 2016 2019e

Hypermarkets Other formats

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 9

March 9, 2017 | 10

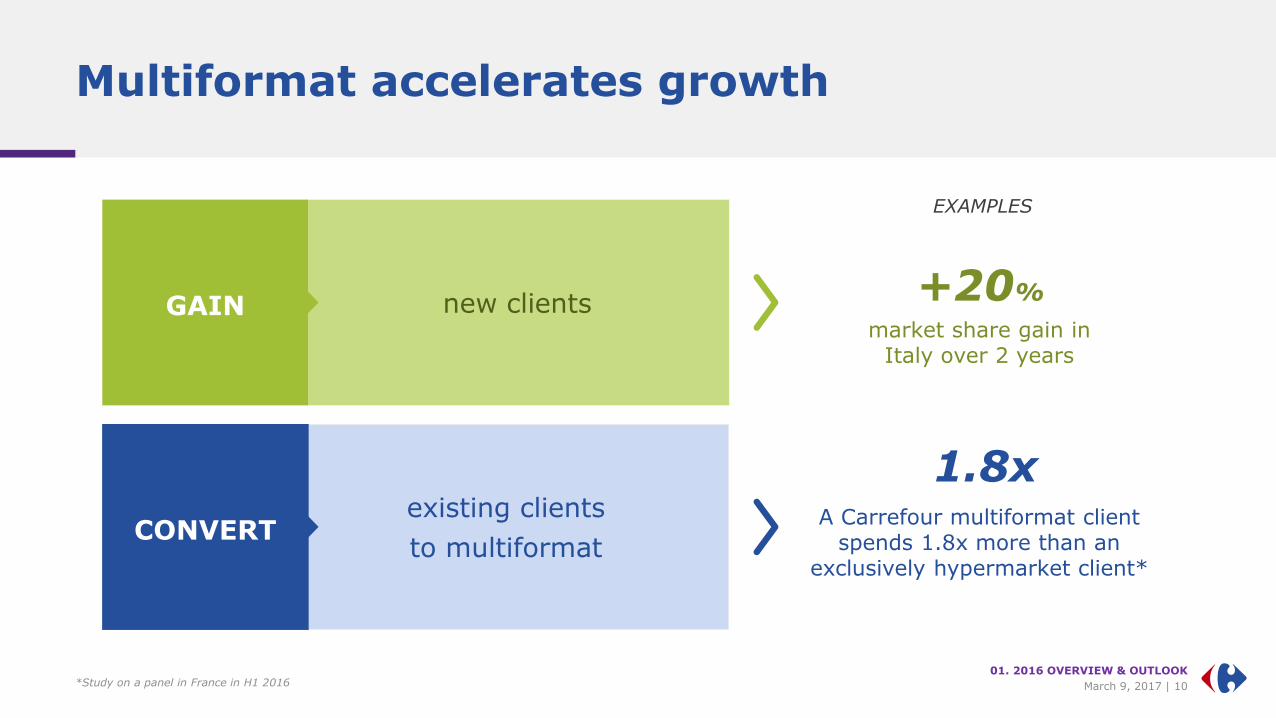

Multiformat accelerates growth

*Study on a panel in France in H1 2016

+20%GAIN

1.8x

CONVERTexisting clients

to multiformat

market share gain in Italy over 2 years

A Carrefour multiformat client spends 1.8x more than an

exclusively hypermarket client*

new clients

EXAMPLES

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 11

E-commerce, an additional format

HYPERMARKETS SUPERMARKETS

CONVENIENCE

CASH &CARRY

E-COMMERCE

Selected banners

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 12

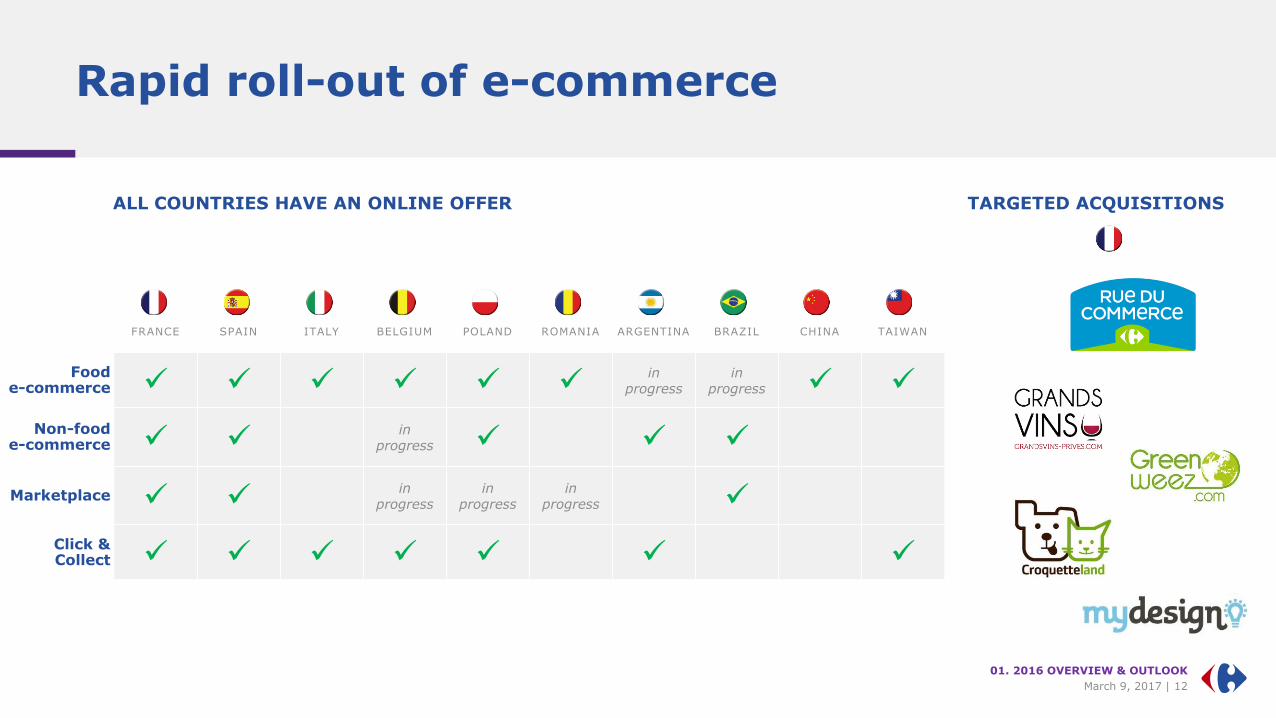

Rapid roll-out of e-commerce

ALL COUNTRIES HAVE AN ONLINE OFFER

FRANCE SPAIN ITALY BELGIUM POLAND ROMANIA ARGENTINA BRAZIL CHINA TAIWAN

Foode-commerce

in progress

in progress

Non-foode-commerce

in progress

Marketplace in

progressin

progressin

progress

Click & Collect

TARGETED ACQUISITIONS

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 13

€4bnTarget

x3

2020 e-commerce prospects

€1.2bn

in 20162020 target

GROSS MERCHANDISE VOLUME

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 14

Omnichannel reinforces multiformat

Increasein average basket

Growthof traffic

Gainnew clients

Rejuvenateclient base

+20% +10%

Hyper-market

Hyper-market

+Drive

Hyper-market

Hyper-market

+Click & Collect

A CLIENT WHO ADOPTS DRIVE OR CLICK & COLLECT SPENDS MORE

01. 2016 OVERVIEW & OUTLOOK

Source : 2016 study based on a panel in France and Spain

March 9, 2017 | 15

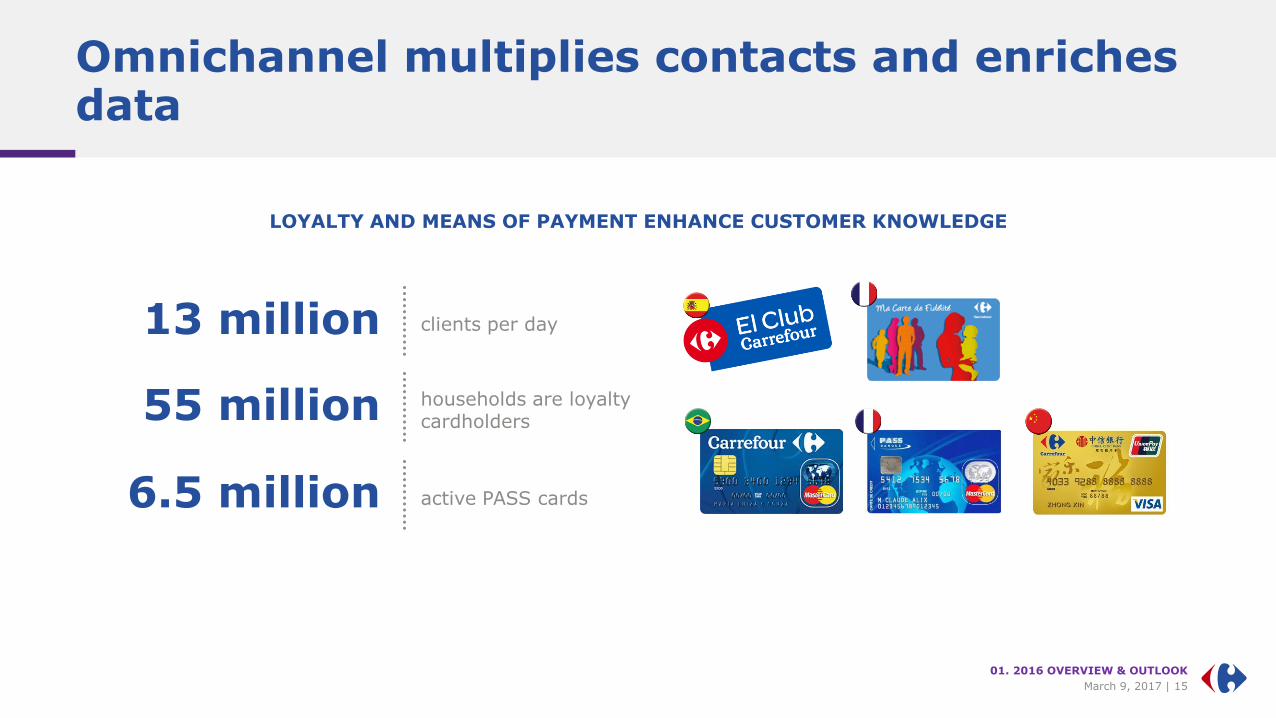

Omnichannel multiplies contacts and enriches data

55 million households are loyalty cardholders

6.5 million active PASS cards

13 million clients per day

LOYALTY AND MEANS OF PAYMENT ENHANCE CUSTOMER KNOWLEDGE

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 16

Non-food and services dynamized by omnichannel

A differentiated assortment

Powerful exclusive labels

Services rolled out online

E-commerce:

A complementary and additional offer

3 million SKUs

3 countries have a Marketplace

6 countries by end 2017

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 17

Carrefour, a culture of innovation

ProductsFormats

ServicesConcepts

Experiment

Iterate

Deploy

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 18

SUPECO: C&CFORMAT INSPIRED BY ATACADÃOAND ROLLED OUT IN 4 COUNTRIES TO DATE

FRANCE:MARKET

ST MARCEL

Differentiated formats

ITALIE: CLUSTERIZATION

URBAN ATTRACTIONGOURMET

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 19

Innovative concepts

ITALY: TERRE D’ITALIA RESTAURANT FRANCE: BULK WALL SPAIN: NEW LAYOUT FOR APPLIANCES

SPAIN: NEW FMCG LAYOUT BELGIUM: BEER CELLAR FRANCE: ORGANIC FOOD AREA

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 20

Products that make a difference

FRESH PRODUCE: REAL KNOW-HOW REFLETS DE FRANCE: 600 SKUs ORGANIC FOOD SALES:+32% IN 2016

VEGGIE: THE 1ST VEGETARIAN PRIVATE LABEL « REPACKAGING » OF OWN BRAND

800 CARREFOUR BIO SKUs

TEX: 22% MARKET SHARE IN HYPERS & SUPERS

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 21

Services that facilitate daily life

01. 2016 OVERVIEW & OUTLOOK

BELGIUM: BRINGR

FRANCE: LIVRAISONEXPRESS.FR

FRANCE: LAUNDROMAT IN-STORE POST OFFICE CORNERFINANCIAL SERVICES

March 9, 2017 | 22

A new collaborative and agile spirit of innovation

Innovation team dedicated to identifying innovative start-ups.

OptiMiam: Fight against food waste

2 HACKATHONSin 2016

129 participants

15 projects

6+ incubations

Cargo

Creation of a dedicated real estate company

for logistics

01. 2016 OVERVIEW & OUTLOOK

France – PIKIT

Connected object allowing to shop online from home

March 9, 2017 | 23

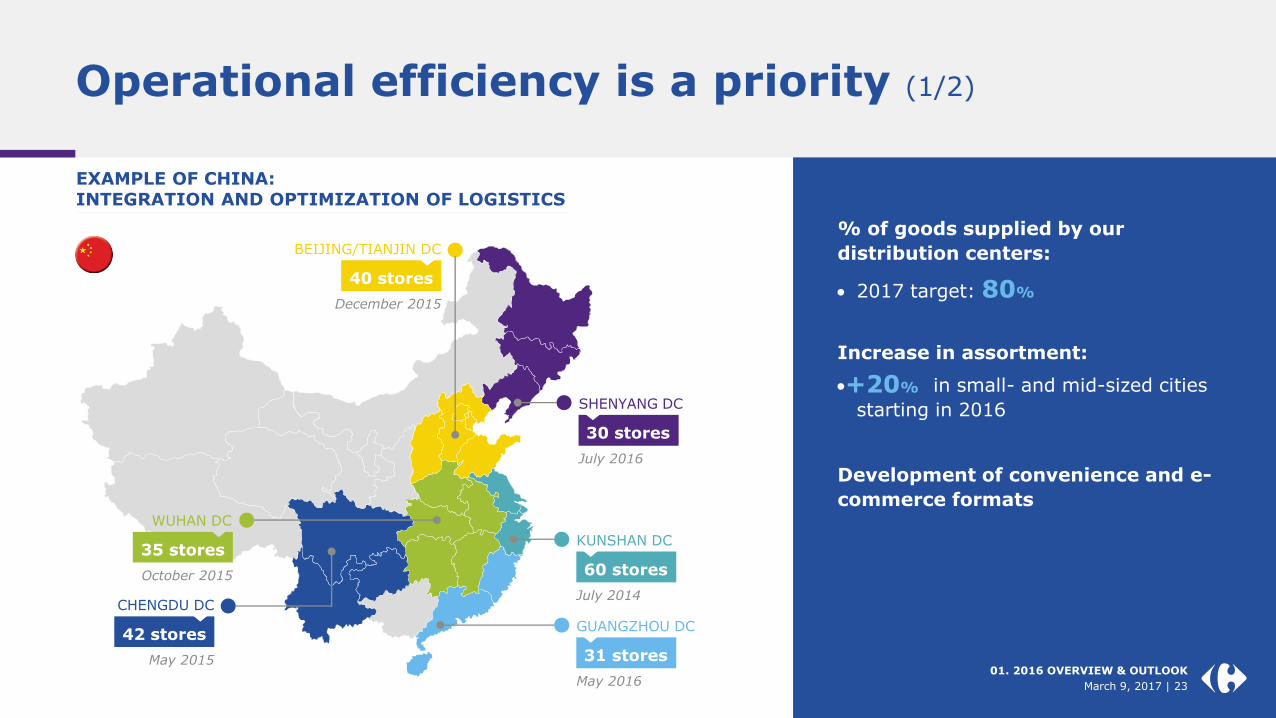

Operational efficiency is a priority (1/2)

EXAMPLE OF CHINA:INTEGRATION AND OPTIMIZATION OF LOGISTICS

30 stores

SHENYANG DC

July 2016

60 stores

KUNSHAN DC

July 2014

31 stores

GUANGZHOU DC

May 2016

40 stores

BEIJING/TIANJIN DC

December 2015

42 stores

CHENGDU DC

May 2015

35 stores

WUHAN DC

October 2015

% of goods supplied by our

distribution centers:

2017 target: 80%

Increase in assortment:

in small- and mid-sized cities

starting in 2016

Development of convenience and e-

commerce formats

+20%

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 23

March 9, 2017 | 24

Operational efficiency is a priority (2/2)

EXAMPLE OF FRANCE: REINFORCED NETWORK OF MULTIFORMAT WAREHOUSES 2018 CARAVELLE TARGETS*

From 67 to 55 warehouses in France

of which 34 are multiformat

Number of Km -20%

Cost of package -5%

Product availability +2%

2013 2018

*2018 targets versus 2012

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 24

March 9, 2017 | 25

CSR:Doing our

job well

CSR contributes to operational efficiency

Reducing wastage

Reduce food waste by 50%

by 2025

Biodiversity

Increase sales of products from Quality Lines and organic farming every year

Training

New skills: data scientists, innovation, job training

Energy

Energy consumption reduced by -9.3% in 2016

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 26

A model strongly focused on value-creation

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 26

March 9, 2017 | 27

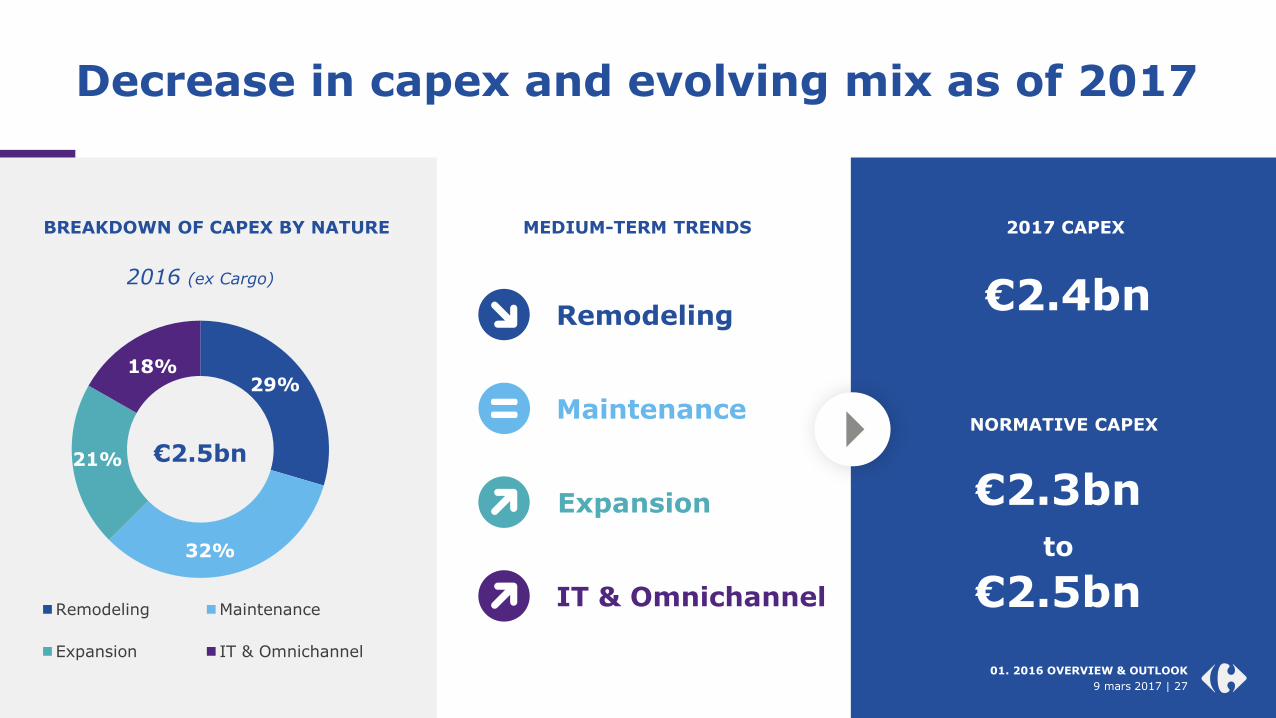

Decrease in capex and evolving mix as of 2017

01. PRÉSENTATION DE L’ANNÉE 2016 & PERSPECTIVES

29%

32%

21%

18%

Remodeling Maintenance

Expansion IT & Omnichannel

€2.5bn

2016 (ex Cargo)

€2.3bn to

€2.5bn

Remodeling

Maintenance

Expansion

IT & Omnichannel

2017 CAPEX

€2.4bn

NORMATIVE CAPEX

9 mars 2017 | 27

01. 2016 OVERVIEW & OUTLOOK

BREAKDOWN OF CAPEX BY NATURE MEDIUM-TERM TRENDS

March 9, 2017 | 28

Value-creation drivers

Solid generation of

operating cash flow

linked to improved results

Disciplined Capex

between €2.3bn and €2.5bn per year (€2.4bn in

2017), with strict Return on Investment criteria and an

evolution in the mix

Control of Working Capital

Requirements

Balanced capital

allocation,

combiningcontinued targeted

acquisitions,

45-50% payout*,

maintaining a BBB+ rating

*of the adjusted net income, Group share

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 29

Financial outlook – 2017 & medium-term

Payout of between 45% and 50% of adjusted net income,

Group share

Capex decrease in 2017 to €2.4bn, and normative capex between €2.3bn and €2.5bn

Planned IPOs of Carmilaand Brazilian operations in 2017,

market conditions permitting

Continued tactical acquisitions

Total sales growth of 3% to 5%

at constant exchange rates in 2017

Continued increase in Free Cash Flow, with a new increase in 2017

01. 2016 OVERVIEW & OUTLOOK

March 9, 2017 | 30

02

2016 FINANCIAL RESULTS

March 9, 2017 | 31

2016 key figures

02. FULL-YEAR 2016 RESULTS

(1) At constant exchange rates

(2) EBITDA: Recurring operating income before depreciation and amortization (including supply chain depreciation)

€76,645m

up

+2.7%(1)

€2,351m

a margin of

3.1%

€1,039m

up

+9.2%

€4,531m

an improvement of

€15m

NET SALES

RECURRING

OPERATING

INCOMEFREE CASH FLOWEX. EXCEPTIONAL ITEMS NET DEBTEBITDA MARGIN(2)

5.1%

a

Stable margin

€1,031m

or

1.39 €/per share

ADJUSTED

NET INCOME,GROUP SHARE

March 9, 2017 | 32

Organic growth of 3.0% in 2016

02. FULL-YEAR 2016 RESULTS

2016 SALES EVOLUTION – (in €m and %)

€76.9bn

+3.0% 0.0%

-0.5%

+0.2%

-3.1%

-0.4%

+3.0%

€79.2bn

+2.7%

€79.0bn €76.6

bn

2015net sales

2016 organic net salesex petrol

ex calendar

2016 net salesat constant exch. rates

2016 net sales

Scope effect1 Petrol & calendar effect

Acquisitions/disposals

Currenciesimpact

LFLex petrol

ex calendar

(1) Scope effect includes store openings/closings and temporary store closures

March 9, 2017 | 33

+1.0%

+2.3%

+3.9%

+3.0%

+3.0%

2012 2013 2014 2015 20162016

Further sales growth

ORGANIC SALES GROWTH EVOLUTION EX PETROL - 2012 TO 2016 – (in %)

02. FULL-YEAR 2016 RESULTS

March 9, 2017 | 33

CAGR2012 – 2016

+2.6%

March 9, 2017 | 34

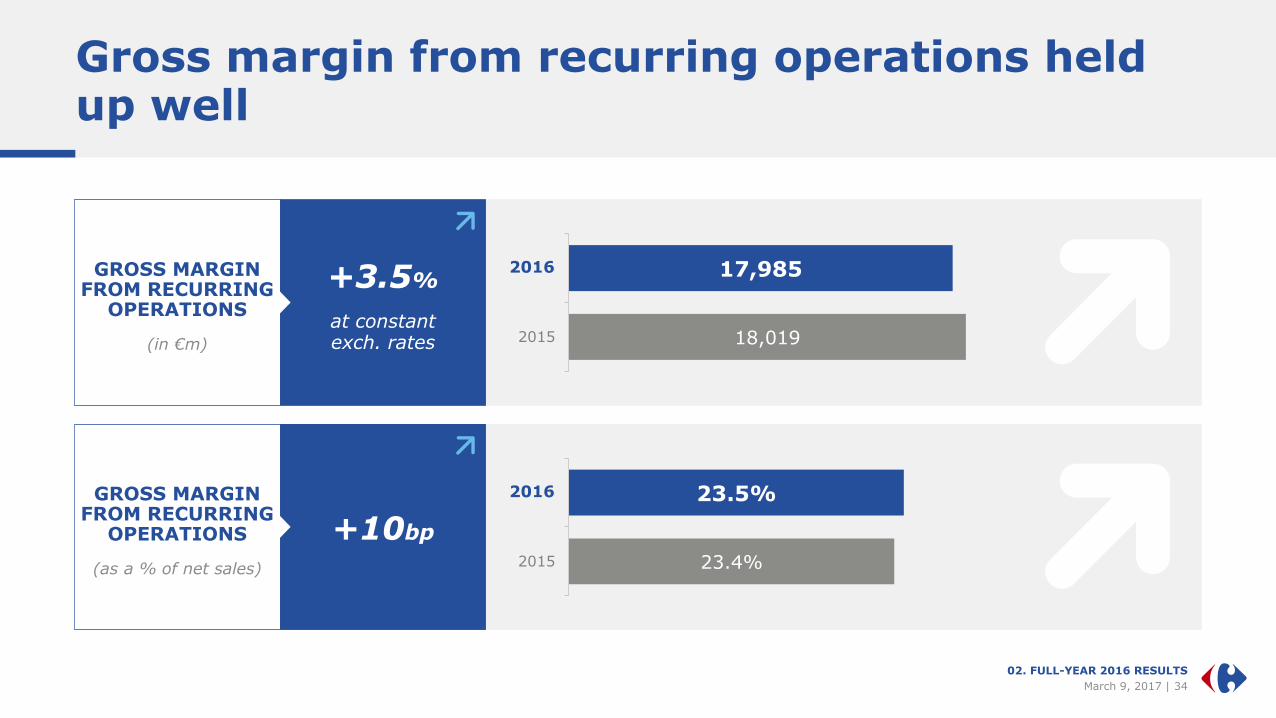

Gross margin from recurring operations held up well

02. FULL-YEAR 2016 RESULTS

+3.5%

at constantexch. rates

GROSS MARGINFROM RECURRING

OPERATIONS

(in €m) 18,019

17,985

2015

20162016

+10bp

GROSS MARGINFROM RECURRING

OPERATIONS

(as a % of net sales) 23.4%

23.5%

2015

20162016

March 9, 2017 | 35

Good control of operating costs

02. FULL-YEAR 2016 RESULTS

+4.9%

at constantexch. rates

OPERATINGCOSTS

(in €m) 13,070

13,125

2015

20162016

+10bpOPERATING

COSTS

(as a % of net sales,ex. petrol) 18.6%

18.7%

2015

20162016

March 9, 2017 | 36

Stable asset costs as a percentage of sales

02. FULL-YEAR 2016 RESULTS

+2.8%

at constantexch. rates

ASSET COSTS

(in €m) 2,505

2,509

2015

20162016

StableASSET COSTS

(as a % of net sales,ex. petrol) 3.6%

3.6%

2015

20162016

March 9, 2017 | 37

France: ROI reflecting investmentsto prepare for the future

NET SALES

€35,877m

ROI

€1,031m

LFL (1)

+0.3%

MARGIN

2.9%

(1) ex. petrol, ex. calendar 02. FULL-YEAR 2016 RESULTS

March 9, 2017 | 38

Other European countries: Strong increase in profitability

NET SALES

€20,085m

ROI

€712m

LFL (1)

+2.0%

MARGIN

3.5% +70 bps

+ 25.7%at constant exch. rates

(1) ex. petrol, ex. calendar 02. FULL-YEAR 2016 RESULTS

March 9, 2017 | 39

Latin America: Continued strong momentum, driven by Brazil

NET SALES

€14,507m

ROI

€711m

LFL (1)

+13.5%

MARGIN

4.9% Stable

+ 3.7%at constant exch. rates

(1) ex. petrol, ex. calendar 02. FULL-YEAR 2016 RESULTS

March 9, 2017 | 40

Asia: Continued transformation in China and further growth in Taiwan

NET SALES

€6,176m

ROI

€(58)m

LFL (1)

-5.0%

MARGIN

-0.9%

(1) ex. petrol, ex. calendar 02. FULL-YEAR 2016 RESULTS

March 9, 2017 | 41

Adjusted net income, Group share

02. FULL-YEAR 2016 RESULTS

(in €m) 2015 2016

EBITDA (1) 3,955 3,886

Recurring operating income 2,445 2,351

Net income from associates and JVs 44 -36

Non-recurring income -257 -372

EBIT 2,232 1,943

Net financial expenses -515 -515

Net interest expense -347 -377

Other net financial expenses -168 -138

Income before taxes 1,717 1,428

Income tax expense -597 -494

Effective tax rate 34.8% 34.6%

(in €m) 2015 2016

Net income from continuing operations 1,120 934

Minority share of net income from continuing operations

-143 -148

Net income from continuing operations, Group share

977 786

Net income from discontinued operations, Group share

4 -40

Net income, Group share 980 746

Adjusted net income, Group share 1,113 1,031

Notes : (1) Recurring operating income before depreciation and amortization (including supply chain depreciation)

March 9, 2017 | 42

2016 Free cash flow

02. FULL-YEAR 2016 RESULTS

(in €m) 2015 2016

Gross cash flow 2,733 2,964

Change in working capital 81 351

Discontinued activities 3 -11

Operating cash flow 2,818 3,305

Capital expenditure (ex. Cargo) -2,378 -2,492

Net capital expenditure (Cargo) - -249

Change in net payables to fixed asset suppliers 136 -78

Asset disposals (business-related) 104 118

Discontued operations 7 -

Free cash flow 687 603

Impact of Cargo - -249

Impact of exceptional items -265 -186

Free cash flow from continuing operations, excluding exceptional items 951 1,039

March 9, 2017 | 43

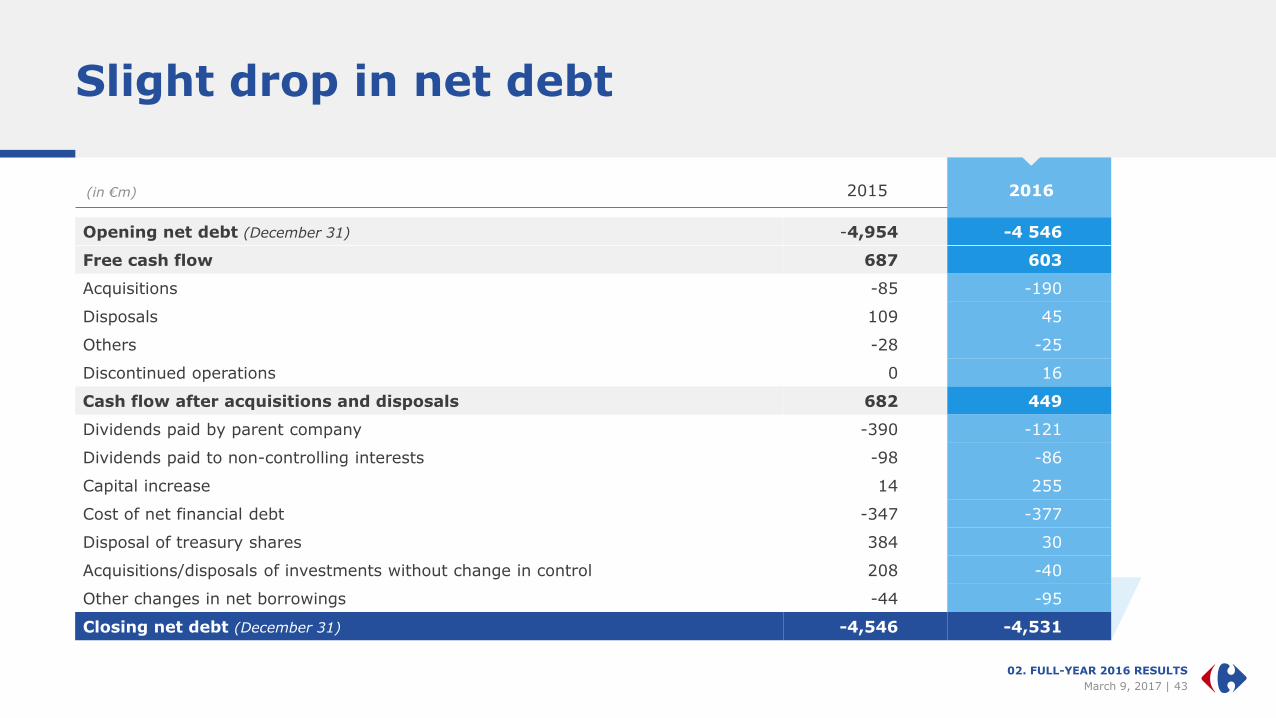

Slight drop in net debt

02. FULL-YEAR 2016 RESULTS

(in €m) 2015 2016

Opening net debt (December 31) -4,954 -4 546

Free cash flow 687 603

Acquisitions -85 -190

Disposals 109 45

Others -28 -25

Discontinued operations 0 16

Cash flow after acquisitions and disposals 682 449

Dividends paid by parent company -390 -121

Dividends paid to non-controlling interests -98 -86

Capital increase 14 255

Cost of net financial debt -347 -377

Disposal of treasury shares 384 30

Acquisitions/disposals of investments without change in control 208 -40

Other changes in net borrowings -44 -95

Closing net debt (December 31) -4,546 -4,531

March 9, 2017 | 44

Credit rating and debt maturity maintained

On April 26, 2016, issua issuance of a €750m bond with a maturity of 8 years and a 0.75% coupon

In 2016, €667m of bonds reached maturity

At end 2016, the debt maturity was 4.1 years

02. FULL-YEAR 2016 RESULTS

1,250

279

1,000 1,000 1,000 1,000

750 750

2.44%

5.25%

1.75%4.00% 3.88%

1.75%0.75% 1.25%

2017 2018 2019 2020 2021 2022 2024 2025

Average annual coupon

DEBT REDEMPTION SCHEDULE – (in %)

2016 issuance

Credit rating maintainted: BBB+

March 9, 207 | 44

March 9, 2017 | 45

Stable proposed dividend: €0.70 per share

02. FULL-YEAR 2016 RESULTS

Dividend of €0,70proposed

to the General Shareholders’

meeting on June 15, 2017

Payout of 51% of

adjusted net income, Group share, in line with our distribution

policy

Payment in

shares or in cash

March 9, 2017 | 46

APPENDIX

March 9, 2017 | 47

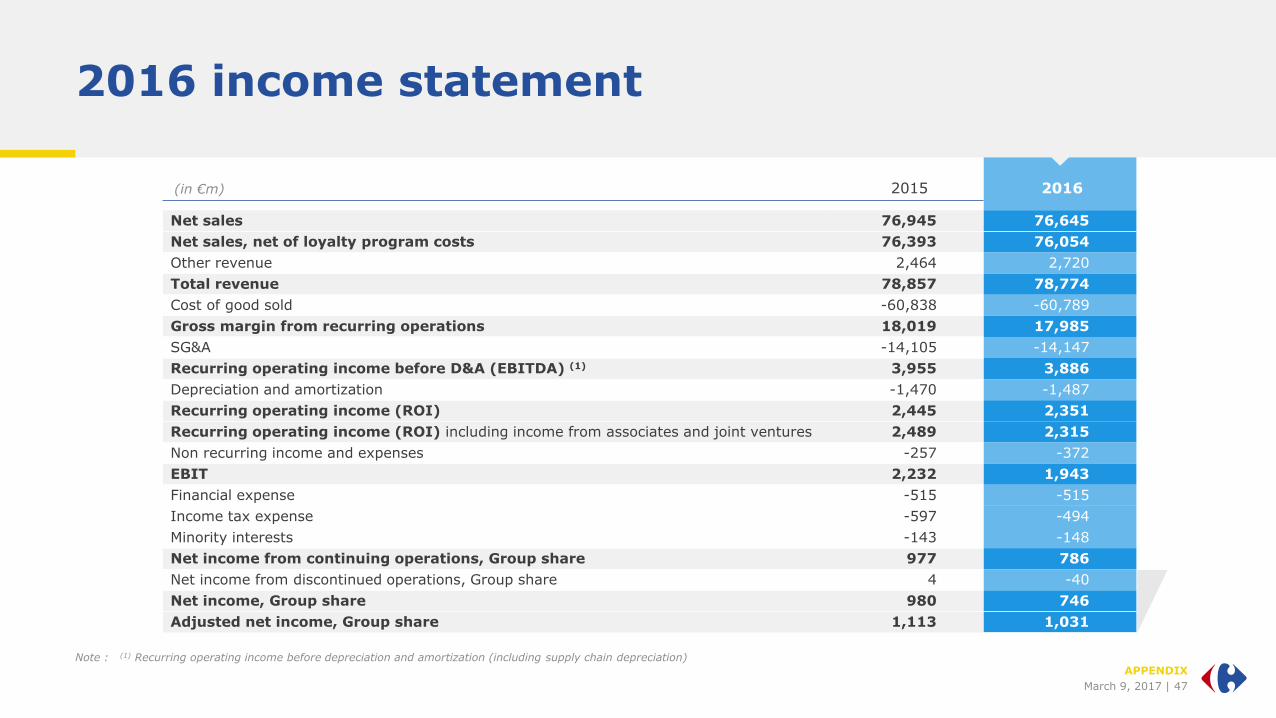

2016 income statement

APPENDIX

Note : (1) Recurring operating income before depreciation and amortization (including supply chain depreciation)

(in €m) 2015 2016

Net sales 76,945 76,645

Net sales, net of loyalty program costs 76,393 76,054

Other revenue 2,464 2,720

Total revenue 78,857 78,774

Cost of good sold -60,838 -60,789

Gross margin from recurring operations 18,019 17,985

SG&A -14,105 -14,147

Recurring operating income before D&A (EBITDA) (1) 3,955 3,886

Depreciation and amortization -1,470 -1,487

Recurring operating income (ROI) 2,445 2,351

Recurring operating income (ROI) including income from associates and joint ventures 2,489 2,315

Non recurring income and expenses -257 -372

EBIT 2,232 1,943

Financial expense -515 -515

Income tax expense -597 -494

Minority interests -143 -148

Net income from continuing operations, Group share 977 786

Net income from discontinued operations, Group share 4 -40

Net income, Group share 980 746

Adjusted net income, Group share 1,113 1,031

March 9, 2017 | 48

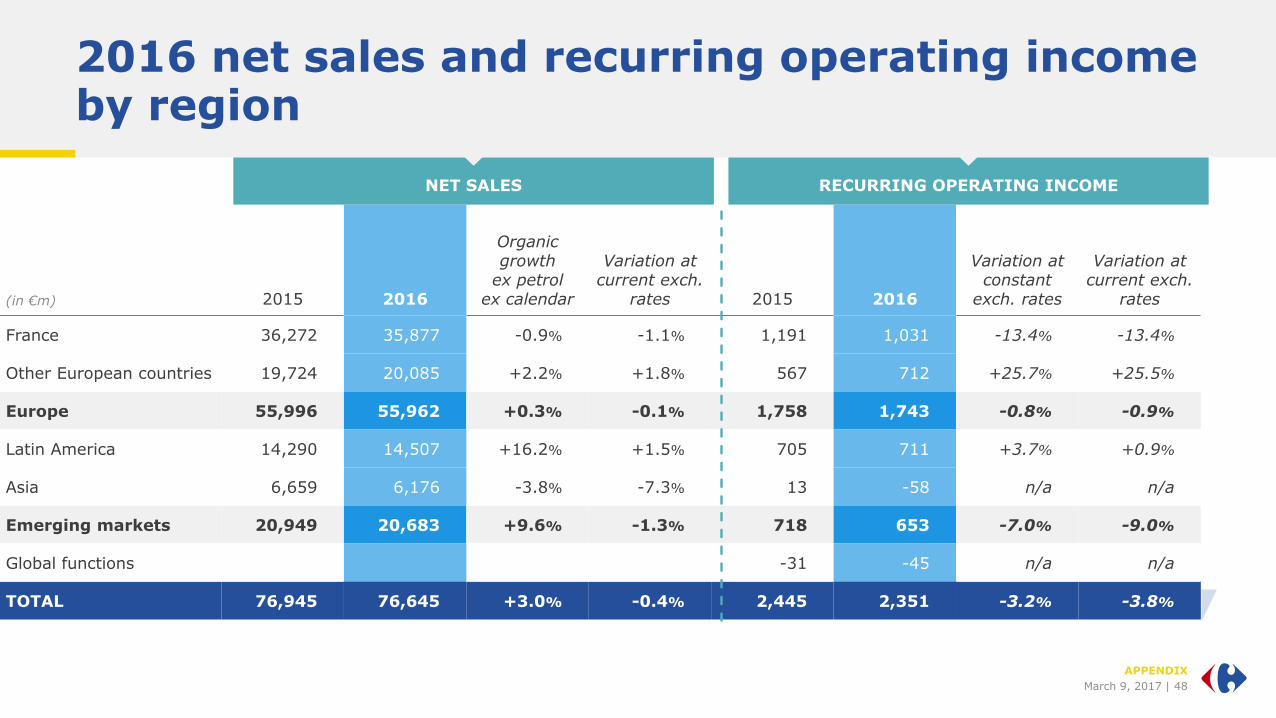

2016 net sales and recurring operating income by region

APPENDIX

(in €m) 2015 2016

Organicgrowth

ex petrolex calendar

Variation at current exch.

rates 2015 2016

Variation at constant

exch. rates

Variation at current exch.

rates

France 36,272 35,877 -0.9% -1.1% 1,191 1,031 -13.4% -13.4%

Other European countries 19,724 20,085 +2.2% +1.8% 567 712 +25.7% +25.5%

Europe 55,996 55,962 +0.3% -0.1% 1,758 1,743 -0.8% -0.9%

Latin America 14,290 14,507 +16.2% +1.5% 705 711 +3.7% +0.9%

Asia 6,659 6,176 -3.8% -7.3% 13 -58 n/a n/a

Emerging markets 20,949 20,683 +9.6% -1.3% 718 653 -7.0% -9.0%

Global functions -31 -45 n/a n/a

TOTAL 76,945 76,645 +3.0% -0.4% 2,445 2,351 -3.2% -3.8%

NET SALES RECURRING OPERATING INCOME

March 9, 2017 | 49

Adjusted net income, Groupe share

APPENDIX

Note : (1) Tax impact of restated items (from non-recurring income and expenses and financial expenses) and non-recurring tax items

(in €m) 2015 2016

Net income from continuing operations, Group share 977 786

Restatement for non-recurring income and expenses (before tax) 257 372

Restatement for exceptional items in net financial expenses 65 30

Tax impact(1) -159 -179

Restatement on share of income from minorities and companies consolidated by the equity method

-27 22

Adjusted net income, Group share 1,113 1,031

March 9, 2017 | 50

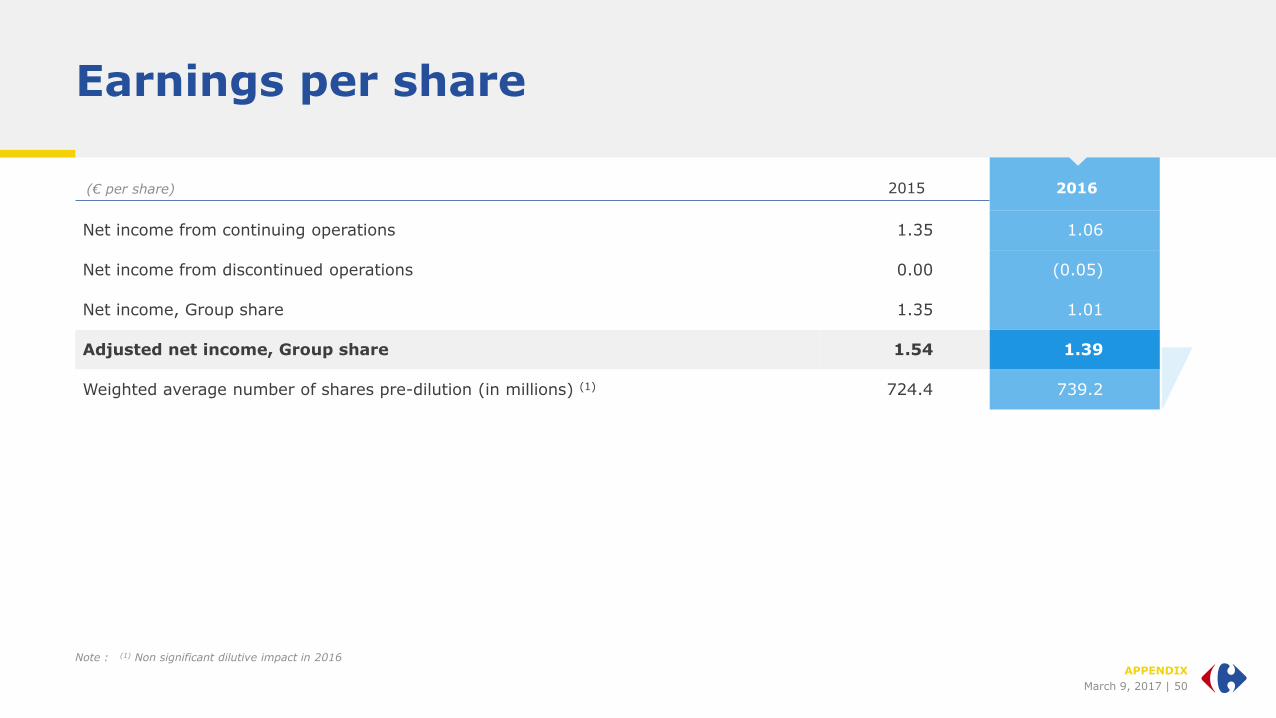

Earnings per share

APPENDIX

Note : (1) Non significant dilutive impact in 2016

(€ per share) 2015 2016

Net income from continuing operations 1.35 1.06

Net income from discontinued operations 0.00 (0.05)

Net income, Group share 1.35 1.01

Adjusted net income, Group share 1.54 1.39

Weighted average number of shares pre-dilution (in millions) (1) 724.4 739.2

March 9, 2017 | 51

Stores under banners1 at end 2016

APPENDIX

Notes : (1) including franchisees and partners; (2) Maghreb, Middle East and Dominican Republic

(#) Hypermarkets Supermarkets Convenience Cash & Carry Total

France 243 1,062 4,222 143 5,670

Spain 175 129 545 849

Belgium 45 442 285 772

Italy 57 412 586 13 1,068

Poland 86 159 641 886

Romania 32 213 53 298

Others 44 422 202 668

Other European countries 439 1,777 2,312 13 4,541

Argentina 79 126 398 603

Brazil 237 42 70 349

Latin America 316 168 468 0 952

China 229 25 254

Taiwan 64 30 94

Others 81 8 2 2 93

Asia 374 38 27 2 441

Others (2) 90 182 46 13 331

Total 1,462 3,227 7,075 171 11,935

March 9, 2017 | 52

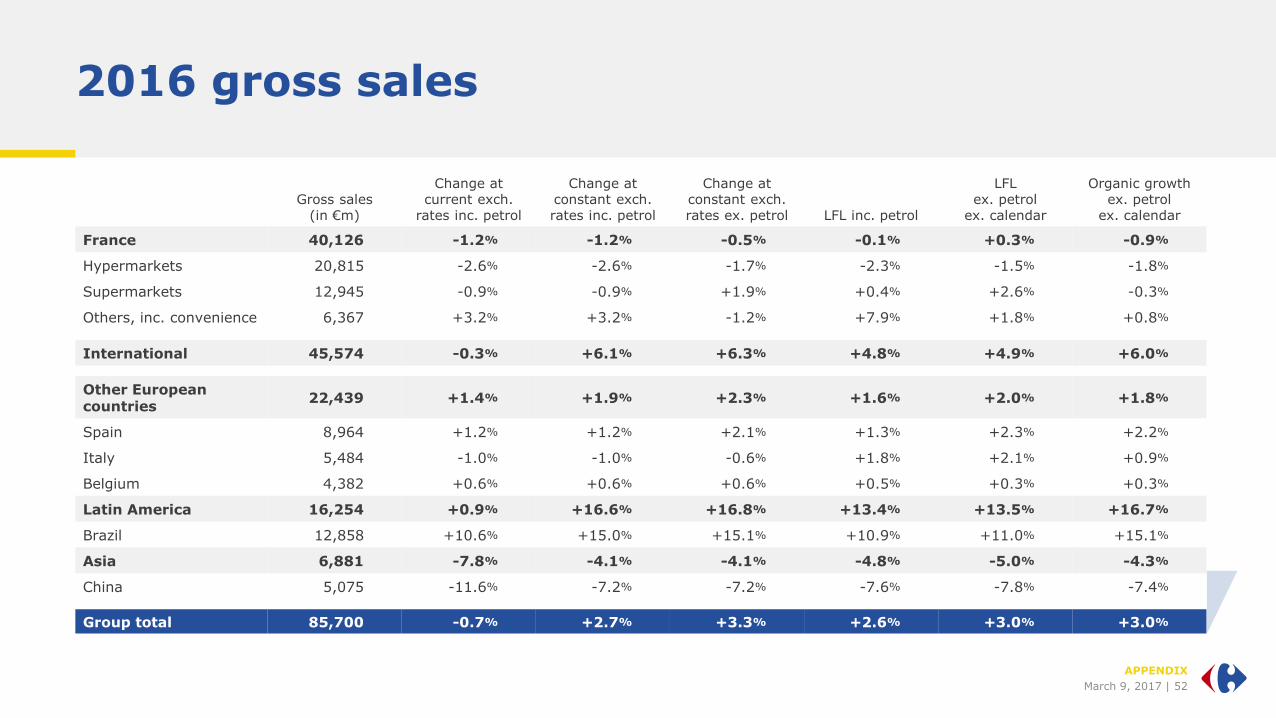

2016 gross sales

APPENDIX

Gross sales(in €m)

Change at current exch.

rates inc. petrol

Change at constant exch. rates inc. petrol

Change at constant exch. rates ex. petrol LFL inc. petrol

LFLex. petrol

ex. calendar

Organic growthex. petrol

ex. calendar

France 40,126 -1.2% -1.2% -0.5% -0.1% +0.3% -0.9%

Hypermarkets 20,815 -2.6% -2.6% -1.7% -2.3% -1.5% -1.8%

Supermarkets 12,945 -0.9% -0.9% +1.9% +0.4% +2.6% -0.3%

Others, inc. convenience 6,367 +3.2% +3.2% -1.2% +7.9% +1.8% +0.8%

International 45,574 -0.3% +6.1% +6.3% +4.8% +4.9% +6.0%

Other Europeancountries

22,439 +1.4% +1.9% +2.3% +1.6% +2.0% +1.8%

Spain 8,964 +1.2% +1.2% +2.1% +1.3% +2.3% +2.2%

Italy 5,484 -1.0% -1.0% -0.6% +1.8% +2.1% +0.9%

Belgium 4,382 +0.6% +0.6% +0.6% +0.5% +0.3% +0.3%

Latin America 16,254 +0.9% +16.6% +16.8% +13.4% +13.5% +16.7%

Brazil 12,858 +10.6% +15.0% +15.1% +10.9% +11.0% +15.1%

Asia 6,881 -7.8% -4.1% -4.1% -4.8% -5.0% -4.3%

China 5,075 -11.6% -7.2% -7.2% -7.6% -7.8% -7.4%

Group total 85,700 -0.7% +2.7% +3.3% +2.6% +3.0% +3.0%

March 9, 2017 | 53

2016 capex breakdown

29%

32%

21%

18%

41%

6%25%

21%

7%

2016 CAPEX

€2,492m(ex Cargo)

Remodelling Maintenance

Expansion IT & omnichannel

France Europe

LatinAmerica

Asia

DIA

APPENDIX

BREAKDOWN OF CAPEXBY NATURE

BREAKDOWN OF CAPEXBY REGION

March 9, 2017 | 54

Hypermarkets: The format for routine shopping needs

With low prices all year round, in-store animations and promotions

1,328 stores ranging from 2,400 m² to 23,000 m²

Banner : 439 stores in other European countries

182 stores in Latin America

243 stores in France

374 storesin Asia

90 stores in other countries

APPENDIX

March 9, 207 | 54

March 9, 2017 | 55

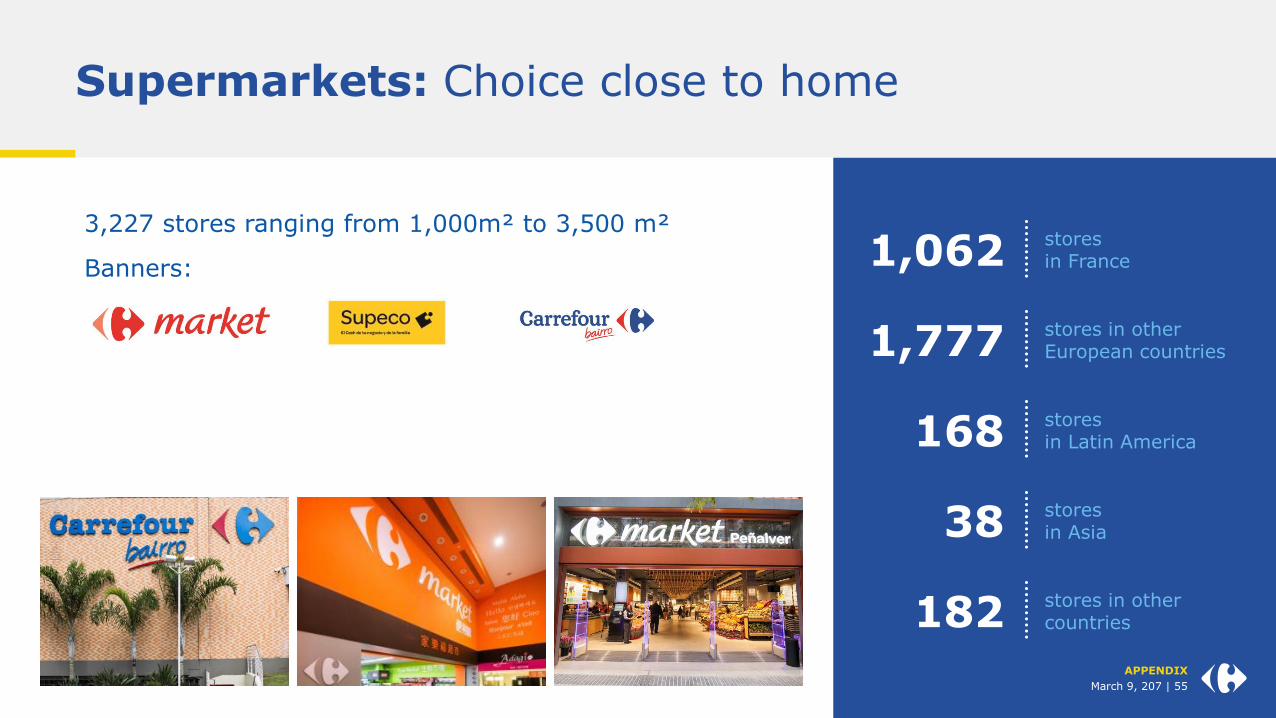

Supermarkets: Choice close to home

APPENDIX

3,227 stores ranging from 1,000m² to 3,500 m²

Banners:

1,777 stores in other European countries

168 stores in Latin America

1,062 stores in France

38 storesin Asia

182 stores in other countries

March 9, 207 | 55

March 9, 2017 | 56

Convenience: Essential daily products

APPENDIX

Catering to daily shopping needs with extended shopping hours

7,075 stores ranging from 200 m² to 900 m²

Banners: 2,312 stores in other European countries

468 stores in Latin America

4,222 stores in France

27 storesin Asia

46 stores in other countries

March 9, 207 | 56

March 9, 2017 | 57

Cash & Carry: Wholesale prices and customized services

APPENDIX

305 stores

Banners:

13 stores in other European countries

134 stores in Latin America

143 stores in France

2 storesin Asia

13 stores in other countries

March 9, 207 | 57

Disclaimer

This presentation contains both historical and forward-looking statements. These

forward-looking statements are based on Carrefour management's current views and

assumptions. Such statements are not guarantees of future performance of the

Group. Actual results or performances may differ materially from those in such

forward-looking statements as a result of a number of risks and uncertainties,

including but not limited to the risks described in the documents filed with the Autorité

des Marchés Financiers as part of the regulated information disclosure requirements

and available on Carrefour's website (www.carrefour.com), and in particular the

Annual Report (Document de Référence). These documents are also available in the

English language on the company's website. Investors may obtain a copy of these

documents from Carrefour free of charge. Carrefour does not assume any obligation

to update or revise any of these forward-looking statements in the future.