Embed Size (px)

Citation preview

Leslie Fay Case

March 30, 2010

Keith CappsTyler Davidson

Ying Zhou

Paul Polishan

◦ Graduated with accounting degree in 1969

◦ Started working for Leslie Fay after graduation

◦ Became friends with John Pomerantz

◦ Became CFO after John became president

Poliworld

◦ Accounting offices of Leslie Fay

◦ Strictly run by Polishan

16 hour shifts

One picture on a desk

Demands of why information was needed

Leslie Fay

Donald Kenia

◦ Polishan’s quiet lieutenant

◦ Accepted responsibility for $80 million fraud

◦ No incentive-based compensation package

◦ Pomerantz and Polishan claim to not know of fraud

◦ Many felt it didn’t add up

Leslie Fay

Fred Pomerantz started Leslie Fay after WWII

Quite a “character”

◦ Gambling

◦ Extravagant parties

◦ Knife wounds

◦ Red Rolls Royce

Company focused on conservative dresses

◦ Largest supplier to department stores in 80s

Red Rolls Royce

Leslie Fay investing

◦ Leslie Fay goes public in 1952

◦ Goes private in 1980s

◦ Goes public again in 1986

John Pomerantz becomes CEO after Fred’s death

The “old-fashioned way”

◦ Continues operations like his father

◦ Shuns market tests, trusts in-house designers

◦ Is slow to integrate computers

Red Rolls Royce

In the early 1970s, annual dress sales began gradually declining.

During the 1980’s, Leslie Fay’s targeted consumer-base (30-55 year-old

women) preferred casual attire.

Recession of the late 1980’s and early 1990’s:

◦ Caused decline in retail spending.

◦ Department store chains weakened.

Leading competitor, Liz Claiborne faced slowing sales, took large

inventory write-downs.

Despite weak market, Leslie Fay reported impressive sales and

earnings.

Fashion Becomes Unfashionable

Leslie Fay forced to markdown its wholesale prices.

◦ Also, granted large rebates to customers who where “stuck”

with excess Leslie Fay product.

Lobbied financial analysts to remain positive in

regards to Leslie Fay’s financial outlooks.

Fashion Becomes Unfashionable

In January of 1993, Polishan informed Pomerantz that Kenia admitted

to masterminding a fraud.

Pomerantz and Polishan denied having any suspicion of wrongdoing.

◦ Pomerantz: “In my heart of hearts, I feel that I’m a victim”

Audit Committee launches an investigation

◦ Retained Arthur Andersen & Co. to help investigate the impact of the fraud.

BDO Seidman, Leslie Fay’s audit firm since the mid-1970’s, issued

unqualified opinions for the years preceding the fraud.

BDO withdrew their 1990 and 1991 audit opinions.

Houston, We Have a Problem

BDO resigned as Leslie Fay’s auditor.

◦ Encouraged by SEC

◦ Lawsuits were launched by investors and creditors

BDO, Leslie Fay, Leslie Fay Executives named codefendants

◦ Independence deemed to have been jeopardized

Upon conclusion of the investigation, a 600 page

report was submitted to the SEC

Houston, We Have a Problem

Inventory: Key focus of Fraudulent Activity

◦ Inflated inventory

Reduced per unit cost of finished goods, increasing GPM on sales.

Other Gimmicks

◦ Pre-recording sales

◦ Failing to accrue period-ending expenses

◦ Failing to write-off uncollectibles, ignoring discounts on receivables

Kenia allegedly decided what amount of profit should be reported each

period.

◦ Ratios

1990-1992 $80 million in overstated profits

Andersen 600 page Report

In April 1993, Leslie Fay filed Chapter 11 Bankruptcy.

Lawsuits charged BDO for at least recklessness in their audits of Leslie Fay.

Howard Schilit’s red flags:

◦ Implausible trend lines in financial data

◦ Implausible relationships between key financial statement items.

◦ Unreasonably generous bonuses paid to top execs

◦ Bonuses linked directly to earnings

BDO contends accusations were based on incomplete information from the

investigative reports released by Leslie Fay’s audit committee.

New investigation underway

BDO Seidman: Odd Man Out

Stillman Report:

◦ Largely exonerated Leslie Fay’s Top execs (including Pomerantz)

◦ “Viable claims” against Kenia and Polishan.

◦ “Claims worth pursuing against…BDO Seidman”

◦ “Likely BDO Seidman acted negligently”

Leslie Fay’s stockholders filed a large civil suit against BDO

Seidman

BDO in turn filed suit against Leslie Fay’s principal officers.

BDO, “…we are the victims of this fraud.”

BDO Seidman: Odd Man Out

July 1997 - $34 million settlement

BDO contributes $8 million to the settlement pool

Kenia admits that Polishan had been the architect of the

fraud.

Polishan convicted on 18 of 21 counts of fraud against

him, 9 years of prison

Key factor: Polishan’s dominance and intimidation of

Kenia

Epilogue

Q1: Prepare common-sized financial statements

The Leslie Fay CompaniesConsolidated Balance Sheets 1987 - 1991 (in millions)

Normal BS Common Size BS

Assets 1991 1990 1989 1988 1987 1991 1990 1989 1988 1987Current Assets:

Cash $ 4.7 $ 4.7 $ 5.5 $ 5.5 $ 4.1 1.2% 1.1% 1.4% 1.5% 1.3%

Receivables(net) 118.9 139.5 117.3 109.9 82.9 30.0% 31.8% 30.3% 30.3% 27.1%

Inventories 126.8 147.9 121.1 107.0 83.0 32.0% 33.7% 31.3% 29.5% 27.2%

Prepaid Expenses & Other

Current Assets 19.7 22.5 19.5 16.4 15.9 5.0% 5.1% 5.0% 4.5% 5.2%

Total Current Assets 270.1 314.6 263.4 238.8 185.9 68.2% 71.7% 68.0% 65.8% 60.9%

Property, Plant, and Equipment 39.2 30.0 27.2 25.9 24.1 9.9% 6.8% 7.0% 7.1% 7.9%

Goodwill 81.3 88.1 91.2 94.1 90.3 20.5% 20.1% 23.5% 25.9% 29.6%

Deferred Charges and Other Assets 5.2 6.2 5.5 4.2 5.1 1.3% 1.4% 1.4% 1.2% 1.7%

Total Assets $395.8 $438.9 $387.3 $363.0 $305.4 100.0% 100.0% 100.0% 100.0% 100.0%

Liabilities and Stockholders' Equity 1991 1990 1989 1988 1987 1991 1990 1989 1988 1987

Current Liabilities:

Notes Payable 35.0 48.0 23.0 29.0 15.5 8.8% 10.9% 5.9% 8.0% 5.1%

Current Maturities of

Long-term Debt 0.3 0.3 0.3 0.3 1.4 0.1% 0.1% 0.1% 0.1% 0.5%

Accounts Payable 31.9 43.3 38.6 45.6 31.6 8.1% 9.9% 10.0% 12.6% 10.3%

Accrued Interest Payable 3.0 3.8 4.1 3.9 3.7 0.8% 0.9% 1.1% 1.1% 1.2%

Accrued Compensation 16.9 14.9 19.5 16.6 10.6 4.3% 3.4% 5.0% 4.6% 3.5%

Accrued Expenses & Other 4.3 6.4 5.8 7.2 7.4 1.1% 1.5% 1.5% 2.0% 2.4%

Income Taxes Payable 1.4 2.3 4.6 6.1 1.8 0.4% 0.5% 1.2% 1.7% 0.6%

Total Current Liabilities 92.8 119.0 95.9 108.7 72.0 23.4% 27.1% 24.8% 29.9% 23.6%

Long-term Debt 84.4 129.7 129.0 116.3 116.6 21.3% 29.6% 33.3% 32.0% 38.2%

Deferred Credits & Other

Noncurrent Liabilities 2.8 2.6 2.7 4.2 4.9 0.7% 0.6% 0.7% 1.2% 1.6%

Stockholders' Equity:

Common Stock 20.0 20.0 20.0 20.0 20.0 5.1% 4.6% 5.2% 5.5% 6.5%

Capital in Excess of Par Value 82.2 82.2 82.1 82.2 82.2 20.8% 18.7% 21.2% 22.6% 26.9%

Retained Earnings 156.9 127.6 98.5 72.8 50.5 39.6% 29.1% 25.4% 20.1% 16.5%

Other -34.3 -31.5 -31.9 -32.0 -31.7 -8.7% -7.2% -8.2% -8.8% -10.4%

Treasury Stock -9.0 -10.7 -9.0 -9.1 -9.1 -2.3% -2.4% -2.3% -2.5% -3.0%

Total Stockholders' Equity 215.8 187.6 159.7 133.8 111.9 54.5% 42.7% 41.2% 36.9% 36.6%

Total Liabilities and

Stockholders' Equity $395.8 $438.9 $387.3 $363.0 $305.4 100.0% 100.0% 100.0% 100.0% 100.0%

The Leslie Fay Companies

Consolidated Income Statements 1987 - 1991 (in millions)

Normal IS Common Size IS

1991 1990 1989 1988 1987 1991 1990 1989 1988 1987

Net Sale $ 836.6 $ 858.8 $ 786.3 $ 682.7 $ 582.0 100.0% 100.0% 100.0% 100.0% 100.0%

Cost of Sales 585.1 589.4 536.8 466.3 403.1 69.9% 68.6% 68.3% 68.3% 69.3%

Gross Profit 251.5 269.4 249.5 216.4 178.9 30.1% 31.4% 31.7% 31.7% 30.7%

Operating Expenses:

Selling, Warehouse, General

and Administrative 186.3 199.0 183.8 156.2 132.5 22.3% 23.2% 23.4% 22.9% 22.8%

Amortization of Intangibles 2.7 2.9 2.6 3.3 3.8 0.3% 0.3% 0.3% 0.5% 0.7%

Total Operating Expenses 189.0 201.9 186.4 159.5 136.3 22.6% 23.5% 23.7% 23.4% 23.4%

Operating Income 62.5 67.5 63.1 56.9 42.6 7.5% 7.9% 8.0% 8.3% 7.3%

Interest Expense 18.3 18.7 19.3 18.2 18.4 2.2% 2.2% 2.5% 2.7% 3.2%

Income Before Non-recurring

Charges (Credits) 44.2 48.8 43.8 38.7 26.2 5.3% 5.7% 5.6% 5.7% 4.5%

Non-recurring Charges (Credits) -5.0 -0.9%

Income Before Taxes on Income 44.2 48.8 43.8 38.7 31.2 5.3% 5.7% 5.6% 5.7% 5.4%

Income Taxes 14.8 19.7 18.0 16.4 11.5 1.8% 2.3% 2.3% 2.4% 2.0%

Net Income $ 29.4 $ 29.1 $ 25.8 $ 22.3 $ 19.7 3.5% 3.4% 3.3% 3.3% 3.4%

Q1: Key Financial Ratios Comparasion

Industry Leslie Fay1991 1991 1990 1989 1988 1987

Liquidity:Current Ratio 1.8 2.9 2.6 2.7 2.2 2.6Quick Ratio 0.9 1.5 1.4 1.5 1.2 1.4

Solvency:Debt to Assets 0.53 0.45 0.57 0.59 0.63 0.63Times Interest Earned 4.2 2.6 2.6 2.3 2.2 2.1Long-term Debt to Equity 0.14 0.4 0.7 0.8 0.9 1.0

Activity:Inventory Turnover 6.7 6.6 5.8 6.5 6.4 7.0Age of Inventory 53.7 days 55.3 62.9 56.2 57.2 52.1Accounts Receivable Turnover 8 6.5 6.7 6.9 7.1 7Age of Accounts Receivable 45.5 days 56 54 53 51 52Total Asset Turnover 3.1 2.1 2.0 2.0 1.9 1.9

Profitability:Gross Margin 31.5% 30.1% 31.4% 31.7% 31.7% 30.7%Profit Margin on Sales 2.2% 3.5% 3.4% 3.3% 3.3% 3.4%Return on Total Assets 6.0% 15.8% 15.4% 16.3% 15.7% 16.2%Return on Equity 14.0% 13.6% 15.5% 16.2% 16.7% 17.6%

Net Sales: The sales has been growing steadily except the slight drop in 1991,

which is contrary to the recession.

Inventory: Leslie Fay has been known for not catching up the fashion; Also,

the recession caused the slow down on retails. There should be inventory

write-off issue in the apparel industry, which haven't been reflected in the

inventory account.

A/R: Because of its nature of hiding fraud; Continue weakness in the retail

sector, Leslie Fay supposed to incur some substantial loss for receivable write

off; Age of A/R is 10 more days than industry norm. (56 vs 45.5days in 1991)

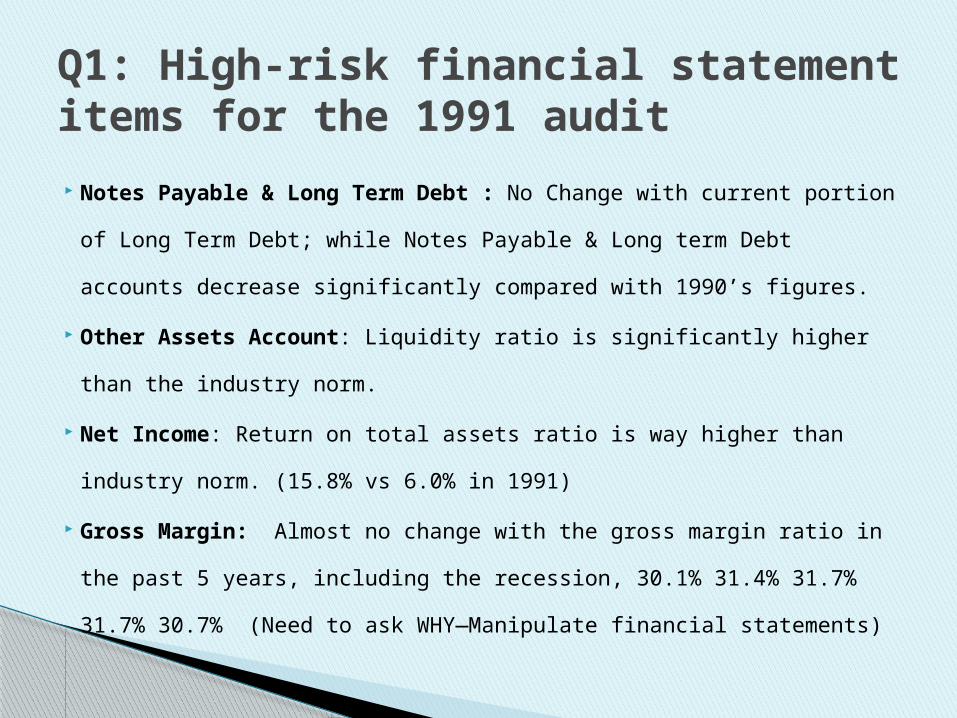

Q1: High-risk financial statement items for the 1991 audit

Notes Payable & Long Term Debt : No Change with current portion

of Long Term Debt; while Notes Payable & Long term Debt accounts

decrease significantly compared with 1990’s figures.

Other Assets Account: Liquidity ratio is significantly higher than the

industry norm.

Net Income: Return on total assets ratio is way higher than industry

norm. (15.8% vs 6.0% in 1991)

Gross Margin: Almost no change with the gross margin ratio in the

past 5 years, including the recession, 30.1% 31.4% 31.7% 31.7%

30.7% (Need to ask WHY—Manipulate financial statements)

Q1: High-risk financial statement items for the 1991 audit

Industry reported modest quarterly sales increases during

recession. But the companies that benefited the most from those

increases were not the leading apparel manufacturers but rather

firms sold to discount merchandisers.

We would like to obtain some key financial ratios from Leslie

Fay’s direct competitors who were also the leader of the industry,

such as Liz Claiborne. This information may make more sense for

analyzing Leslie Fay’s performance compared using the industry

benchmark.

Q2: Other financial information for planning 1991 audit

SAS 59: evaluate company as a going concern

◦ Auditor should consider management’s plans

Conservative clothing line

◦ Plans to continue with traditional clothing line

◦ Industry trend moving to casual clothing

Economy

◦ The overall economy was down when the fraud was perpetrated

◦ Had an industry wide effect

◦ Leslie Fay seemed immune

Q3: List nonfinancial variables that auditors should consider.

SAS 65: Auditor’s consideration of Internal Audit

◦ Discuss internal audit function with management

◦ Assess competence and objectivity

Determine internal auditor’s role through

discussions with management

◦ If it objectivity appears suspect:

Carefully evaluate internal audit’s work

Q4:How should auditors take the role of internal auditor into consideration?

SAS 65: Evaluating Internal Auditors

◦ Scope of work is appropriate to meet the objectives

◦ Audit programs are adequate

◦ Working papers adequately document work

For Leslie Fay

◦ Through testing of internal auditor’s work

◦ Ensure controls are in place and followed

Q4:How should auditors take the role of internal auditor into consideration?

AICPA Rule 101-6

◦ CPA – client relationship must be “one of complete candor”

◦ When threatened or actual litigation exists between management and the CPA,

complete candor may not be possible.

If management intends to file suit against the auditor, an adversarial

relationship would exist.

Given the circumstances, in litigation, Leslie Fay would likely attempt

to shift the burden of responsibility to BDO, and vice versa.

Such an adversarial relationship caused the SEC to end this auditor-

client relationship.

Q5 - SEC Ruling – BDO’s Independence Jeopardized

End.Questions?

Anyone?Anyone not named Rajendra?