Embed Size (px)

Citation preview

Corporate Presentation

March 2021

2

Disclaimer

Statements contained in this release relating to the business outlook of the Company, projections of operating/financial results, growth prospects of the Company and market

and macroeconomic estimates are merely forecasts and are based on the beliefs, plans and expectations of Management in relation to the Company’s future. These expectations

are highly dependent on changes in the market, Brazil’s general economic performance, the industry and international markets, and hence are subject to change.

3

GPA Consolidated GPA Brazil Grupo Éxito

3

4

GPA Consolidated GPA Brazil Grupo Éxito

5

We Are the #1 Food Retailer in South America, with a Diversified Portfolio of Leading Brands in Brazil, Colombia, Uruguay and Argentina

Food retailer andfood e-commerce inBrazil and Colombia

One of the largest retail employer in South America

98K employees

Food retailerin South America1

1,502 stores

R$ 50.4 bn2020 Net Revenue

R$ 3.9 bn (7.8% margin)2020 EBITDA

Source: Nielsen and Colombia market share from Supersociedades – Information of Dec/2020 for Brazil, Argentina and Uruguay; 2019 for ColombiaNote: 1) Leadership based on sales

o Stores: 25

o Net Revenue: R$1.2 bn

o EBITDA: R$16 mm

o EBITDA Margin: 1.4%

o Market share: 2%

o Stores: 91

o Net Revenue: R$3.7 bn

o EBITDA: R$372 mm

o EBITDA Margin: 10.3%

o Market share: 43%

o Stores: 873

o Net Revenue: R$28.3 bn

o EBITDA: R$2.3 bn

o EBITDA Margin: 8.0%

o Market share: 14%

2020

o Stores: 513

o Net Revenue: R$17.1 bn

o EBITDA: R$1.4 bn

o EBITDA Margin: 8.3%

o Market share: 31%

34% 56%

8% 9%

2% 0%

%

Share of Revenue

%

Shareof EBITDA

35% 56%

6

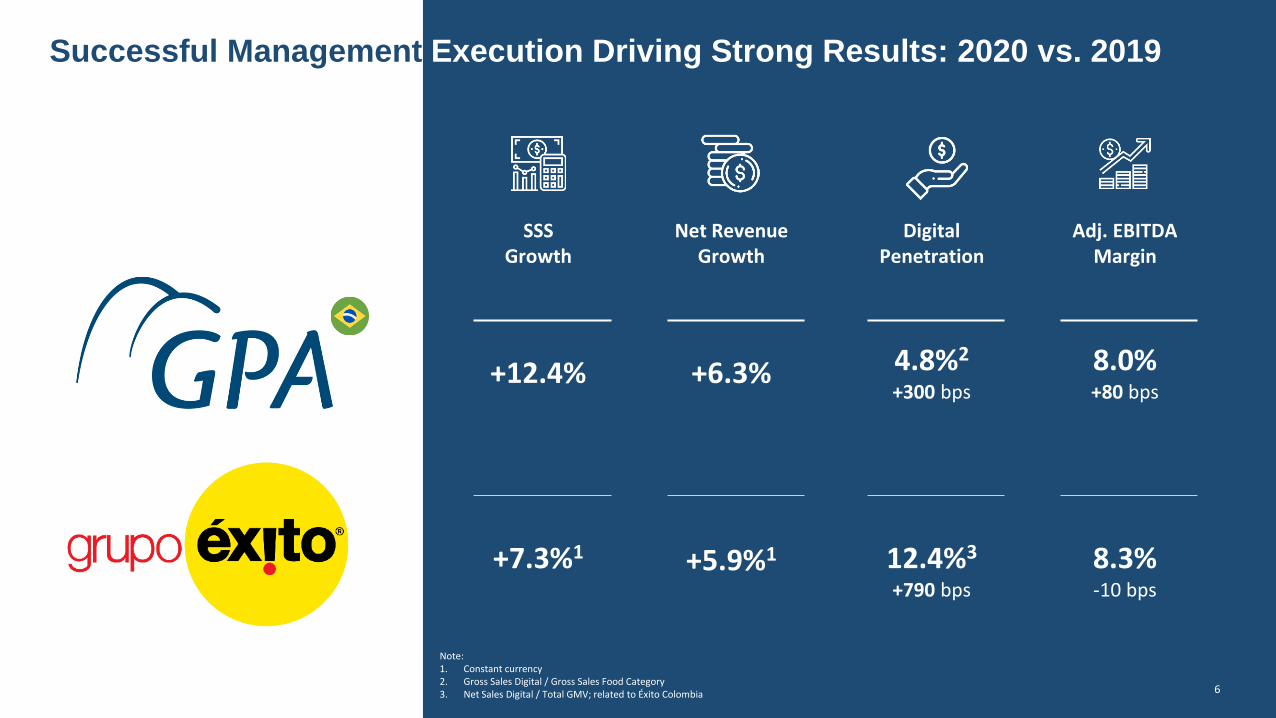

Successful Management Execution Driving Strong Results: 2020 vs. 2019

6

Net RevenueGrowth

+6.3%

+5.9%1

SSSGrowth

+12.4%

+7.3%1

Adj. EBITDA Margin

8.0%+80 bps

8.3%-10 bps

Digital Penetration

4.8%2

+300 bps

12.4%3

+790 bps

Note:1. Constant currency2. Gross Sales Digital / Gross Sales Food Category3. Net Sales Digital / Total GMV; related to Éxito Colombia

7

Our Group is Part of Key Sustainability Indexes Across the Globe

Highest Commitment to ESG Principles with Strong Market Recognition

Our Recent ESG Initiatives and Achievements

Carbon Efficient Index(ICO2)

Financial Times Stock Exchange(FTSE4GOOD)

B3 Corporate Sustainability Index(ISEB3)

The only food retailer

Morgan Stanley Capital International(MSCI)

Carbon Disclosure Programme(CDP)

A

B

7

8

Experienced Board

Top Management with Unique Experience in Food Retail and a Company with the Highest Governance Standards

Listed on Novo Mercado

Audit Committee

People and Remuneration Committee

Corporate Governance and Sustainability Committee

Financial Committee

Governance Highlights

Jean-Charles NaouriPresident

+ 3 5

# Y e a r s i n R e t a i l

Christophe Hidalgo

Member

+ 2 5

HervéDaudin

Member

+ 1 7

Renan Bergmann

Independent Member

Rafael Russowsky

Member

+ 8

Eleazar de Carvalho FilhoIndependent Member

+ 2 0

Luiz Augusto Castro NevesIndependent Member

+ 9

Arnaud Strasser

Co-VP

+ 2 0

Ronaldo Iabrudi

Co-VP

+ 8

Innovation and Digital Transformation Committee

# Years in Retail

Experience

Jorge FaiçalCEO GPA

+25

Guillaume GrasCFO GPA

+16

Luiz Henrique CostaCOO GPA

+7

Laurent CadillatCDO GPA

+20

Carlos Mario GiraldoCEO Éxito

+25

Jacky YanovichCOO Éxito

+20

Ruy SouzaCFO Éxito

+5

9

GPA Consolidated GPA Brazil Grupo Éxito

9

10

Focusing on Four Key Pillars

Increase Hyper Profitability

Growth andMaturation of Super Regional

Organic Expansion of Premium

Formats

10

Scale-up Our Digital Platform

Apps

1P

Ecommerce Stores

WebsitesMarketplace

Rewards Engagement

Solutions Frequency

Fulfillment GPA LOG

DCs

Last Mile

Data Insights

Media

43%of gross sales

17%of gross sales

27%of gross sales

44%of gross sales

12

Digital Ecosystem: Important growth lever

Evolution of food online sales

R$ 0.4 Bi

R$1.1 Bi

2019 2020

+3XCustomers

registered in theloyalty programs

Average omnichannel customer spend vs

B&M store customer

+ 21MM +2.7 x

Shipment from Stores / Click & Collect

Shipment from DCs

Last Milers

289 stores dec/20 vs 120 in dec/19, around52% of online sales

355 stores in 32 cities (vs 55 stores in 18 citiesin dec/19), +543% of GMV and +316% in

number of orders

6 DC´s by the country (4 new DC´s in 4Q20) in order to support sales growth of 128% in 4Q20

GPA Marketplace growth

Strengtheningverticals in 1P

Delivery radiusexpansion

5% share in food

2% share in food

Biggest coalition of Brazil retail market

+60 MM of potencial clientes with lowlevel of overlap between GPA and RD

Launched in October/2020and embraced by 1 million customersin the first 7 weeks

80% of activation and 30% oftransversal use in coalition (clientsnavigation in both companies) in earlystages of operation

New retail verticals planed for 2021

14%Market share

13

Strenghtening of GPA digital plataform| IDP doubles the number of omnichannelclients, who spend an average 2.7x more than a B&M store customer

• Complete basket experience

• Personalized recommendations

• Continuos geographical expansion

+4 DCs and +169 stores in 2020

+New sales regions for 2021

• Destination categories / complementary

• Target of 400k SKUs in 2021

• Accelerate Register Sellers / SKUs

• Strict control of Client Service

• Accelerate Media Performance

E-commerce 3P IN

+ COMPLETE ASSORTMENT IN FOCUS CATEGORIES

Core Business New Business

• Collaborative Platform: Be wherever the

customer is!

• Specialization as a Seller in other Market

Places

• Multiples Last Milers

E-commerce 3P OUT Change Business+ GMV

+ Market-share

+ Recorrência

+ Network effect

Grocery

Fresh

Craft Beers

Wines & Liquors

Auto Care

Personal Care

Cleaning

Pet Care

Baby Care

Home Care

E-commerce 1P

14

Distinguished B&M Portfolio Creating Economics Moats to Enhance the Largest Digital Food Retail Platform

Technology Capex Already Deployed

Reinvest FCF

Marginal Cost at Stores

Limited CAC (Mainly Retention)

Frequency + Recurrence

Nationwide Logistics in Place

Profitability Strategy to Deliver One-Stop-Shop

Top of Mind BrandsWe Already Own the Customer

(Massive Database)

Cashflow Dynamics

Food (mainly fresh) asOur Core

+800 Stores / Hubs

Last Mile Capabilities

21 mmcustomersregistered

Core /Higher Margin = 1P

Fulfillment / Take Rate = 3P

Agile Methodology

Talent Attraction & Retention

Partnership with Tech Companies

People: Our Most Valuable Asset

15

This is Our Platform Strategy

15

Network Effect

Digital Payment

LogisticsServices

Data Monetization

Customer Identity Platform

21+ mmCustomers

reig

PIX Enabled in all

stores12% penetration2

198% growth1

E-commerce+250mm annual visits

Coalition

60+ miclient base

FICR$1.1 bn

GMV

14% mkt share

Loyalty

6.4xavg. ticket4

82%penetration3

Open Banking

1 hour

delivery

Fulfillment

Services

Click & CollectIn 289 stores

(vs 120 in 2019)

+100 startups and scale-ups plugged

Relationship

Insights

Media

25 multidisciplinary squadsin digital

Innovation in the off environmentwith more than 200 self checkout

Note:

1. E-commerce 9M20 vs 9M19

2. Sales through digital channels at Pão de Açúcar as of 3Q20

3. Pão de Açúcar sales to loyal customers

4. Loyal customer using APP (with My Rewards and My

Discounts) vs loyal customer without APP

Consumption

2,7X higher

OMNICHANNEL CLIENTS

60%of multichannel

clients in e-

commerce

16

Expanding Our Digital Platform to Support Market Share Growth

16

VA

LUE

OF

OU

R P

LATF

OR

M

APPs(Cliente Mais and

Clube Extra)

Loyalty programs

Food e-commerce

GMV

Distinguish B&M assets with food as core (high frequency) contributing to a leading 1P platform

We Are Here Jan/21

Customer knowledge platform fully integrated generating network effects

Develop and complete ourvalue proposition

21mm

14% of mkt share

R$ 1.1bn

Multiple delivery solutions

• 289 stores click & Collect

• 32 cities last mile

BUILT ROADMAP

PLATFORM MATURITY

Launch 3P

Insights

Market share expansion

Boost 1P categories: strengthen existing verticals

to expand mkt share

Baby Products

Beer Cleaning Products

Wine

+ penetration in existing regions and expansion to

new regions

Enhance 3P:Huge potential to be captured

AutoPet

Homeware Toys Personal Care

+ new DCs+37 transit points

+170 same day / click & collect stores

+9 cities with last mile coverage

Data monetization:marketing of media - using

purchase frequency and customer base

New payment solutions:

digital wallet

Network effect

Fulfillment services

17

What is Our Strategy in Each Format?

Enhancing Value Proposition Organic ExpansionOrganic ExpansionRegional Positioning

Competitiveness in grocery

Quality in fresh

Streamline non-food & specialties

Stores strategically located in areas with high flow of people

Everyday Neighborhood Format

New stores concepts including coffee shop and wine house

31 closed or converted to Assaí(2016-2020)

23 repositioned in 2020

46 G7 stores

6 stores to be converted in 2021

Best shopping experience

Increased fresh offer

New payment and digital solutions

Better price positioning

Focus on fresh

Store layout similar to regional players

169 stores conversions (2018-20)

6 stores to be converted in 2021

Accelerated expansion

Maintenance of high profitability80 stores to be repositioned

Accelerated expansion

Maintenance of high profitability

Format maturation

Regional expansion (organic + M&A)

Value Proposition

Portfolio Repositioning

Strategy

Format Performance

(2020 vs. 2019)

11%Sales Growth

RepositionedStores Performance

19%Sales Growth

12%Sales Growth

7%Sales Growth

17

Strong growth in the first year and consistent growth in the

second year of operation

Growth above the control group on sales and on EBITDA

Relevant growth in its first year of operation followed by

acceleration in the second year

100% success in 2019 openings, with sales level above mature

stores and increased profitability

18

Key Takeaways

18

Focus on Executing Our StrategyStrategically Focused on Food Retail

Experienced & Engaged Management Team and High ESG Standards

Digital Platform StrategyIntegration of our Unique Omnichannel Portfolio with a Qualified and High recurrence Customer Base, Driving Growth

Improvement in All KPIsOperational Excellence, Continuous Innovation andStrengthening Value Proposition in Selected Formats

#1 Food Retailer and Food E-commerce, Serving All Client ProfilesThrough Our Multiformat Strategy

Multiple Levers of Growth and Low Leverage to Seize OpportunitiesStrong Organic Growth of Premium and Neighborhood Formats

19

GPA Consolidated GPA Brazil Grupo Éxito

19

20

Grupo Exito: an absolute food retail market leader in Colombia and Uruguay

Leading market position, with a comprehensive coverage of customers and marketsBrands and formats for all segments of the population

Premium

Mainstream

Low Cost

Diversified with a large footprintAbsolute market leader

#1 private employer in Colombia

Sizeable operationsAbsolute market leaderStrong cash generation

Dual retail/real estate modelDiversified real estate portfolio

45.8Brand Awareness

Highest score among food retailers in Colombia (~2x the second highest)

Corporate reputation

#1 in corporate reputation among retailers in Colombia. #8 overall

Reputable brand, with strong recognition

Source: Follow Brand

Revenues (R$bn) 18.8 4.4 1.4

EBITDA margin 8.3% 10.3% 1.4%

Cash flow conversion1 74% 74% 52%

Top-of-mind with customers

Source: Merco

1

1

Retail2

Real estate4

Highlights (2020)

Market shares

Brand portfolio

31% 43% 2%3

32% N/A 12%1 1

Notes: 1. Calculated as (EBITDA Pre IFRS 16 -Capex)/EBITDA Pre IFRS 16; 2. Colombia market share from Supersociedades, including discounters, as of 2019. Uruguay market share from IDretail/GDU, Dec, 2020. Argentina market share from Nielsen, Dec, 2020; 3. Refers to market share in the country. The market share for the areas Grupo Exito is present in is 14.5%; 4. Market share based on real estate AUM; 5. Includes: Tuya Pay, Paseo, Media business venture, Vehicle Rental business venture, Exito Móvil, among others

Comprehensive ecosystem

7,800/10,000

Sales area (‘000 sqm) 839 92 106

21

Leading retail through innovation and integration of BU´s across a comprehensive ecosystem with strong synergies

Comprehensive Ecosystem with Strong Synergies

Unmatched digital penetration in the

region

Including click & collect, digital

catalogue

735 vendors with 82% GMV growth in

2020

#1 food retailer, high margins and strong cash flow

generation

Dual Retail / Real Estate model

Absolute market leader, with 28%

retail market share

#1 loyalty coalition in Colombia with over

105 allied brands

Others

Brick & Mortar

Omni-channel

#4 travel agency in Colombia

#1 card issuer in Colombia

Launched in Mar/20 ~200k

digital accounts

#1 seller of micro insurance

in Colombia

#3 real estate player in

Argentina

#1 shopping mall operator in Colombia

Loyalty Coalition Complementary Businesses & Traffic

Monetization

Omniclient 1.1 M Tx. Target is to be the #1 ally of

money transfer network in Colombia

Alliance to centralize and

monetize electronic

transactions

+475K active lines and

triple digit growth in on-line channel

21

22

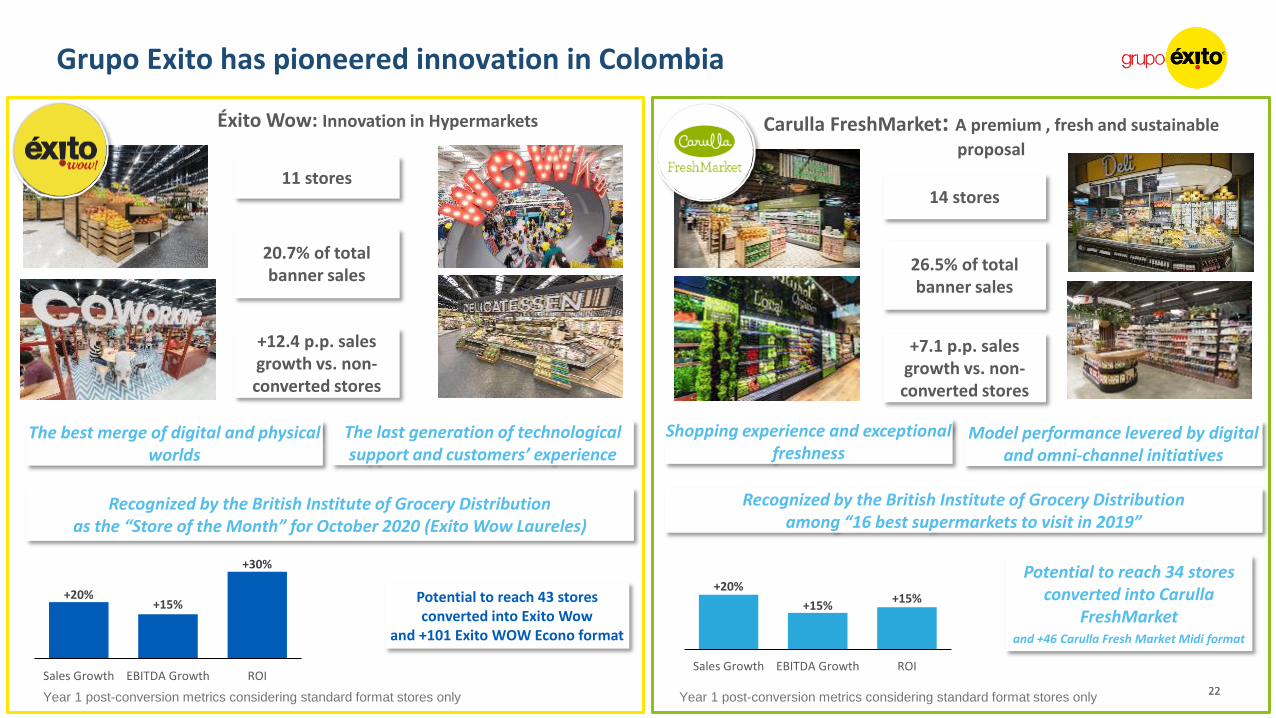

Grupo Exito has pioneered innovation in Colombia

22

11 stores

20.7% of total banner sales

+12.4 p.p. sales growth vs. non-converted stores

Éxito Wow: Innovation in Hypermarkets

The best merge of digital and physical worlds

The last generation of technological support and customers’ experience

Recognized by the British Institute of Grocery Distributionas the “Store of the Month” for October 2020 (Exito Wow Laureles)

14 stores

26.5% of total banner sales

+7.1 p.p. sales growth vs. non-converted stores

Carulla FreshMarket: A premium , fresh and sustainable

proposal

Shopping experience and exceptional freshness

Model performance levered by digital and omni-channel initiatives

Recognized by the British Institute of Grocery Distributionamong “16 best supermarkets to visit in 2019”

+20%+15%

+30%

Sales Growth EBITDA Growth ROI

Year 1 post-conversion metrics considering standard format stores only

Potential to reach 43 stores converted into Exito Wow

and +101 Exito WOW Econo format

Potential to reach 34 stores converted into Carulla

FreshMarket and +46 Carulla Fresh Market Midi format

+20%

+15%+15%

Sales Growth EBITDA Growth ROI

Year 1 post-conversion metrics considering standard format stores only

23

Strong and growing private label portfolio, with cross-synergies among our businesses in different countries

TaeqPositioned as the 3rd most important healthy brand in Colombia

FrescampoRelevant low-cost brand in the Colombian market

Food categories Non-Food categories

23

~6 thousand SKUs4Q20

ApparelArkitect, Bronzini and People are among the top 10 apparel brands in Colombia

HomegoodsRelevant homegoods brand, with international presence

~17% Private Label Penetration in Food Productsin 2020

~44 thousand SKUs4Q20

~36% Private Apparel & Homegoods Penetrationin 2020

24

4.5%

12.4%

2019 2020

There is no other Latin American player with such omnichannel penetration as Grupo Exito in Colombia

Positive contribution to the margin of the B&M business

E-commerce+240% in traffic

Marketplace735 vendors

Digital Catalogue+3.6% in sales

Last Mile & Delivery85% of total orders in

2020

Click & Collect800k+ orders in

2020

Unmatched omnichannel penetration

Notes: Data refers to Colombia. 1. Converted at a BRLCOP average FX rate for 2020 of 716.86; 2. 2020 vs. 20193. Include .com, marketplace, home delivery, Shop&Go, Click&Collect and digital catalogues

Exito to continue strengthening the omnichannel business in 2021

Increase platform monetization1

Increase apparel category penetration3

Maintain double digit growth and high penetration into 2021

2

2.8x food / 2.6x non-foodgrowth in 2020

164mm website visits in 2020, vs. 86mm in 2019

More than 8.5mm orders (+1.8X) in 2020

R$2.0bn1

2020 sales via omnichannel

Omnichannel highlights (2020)

Continue investing CAPEX in innovation and omnichannel (c. 30% of our total CAPEX in 2020)

4

2.7xOmnichannelsales growth2

Omnichannel share of sales (%)

9% food / 20% non-foodpenetration as of 2020

R$ 1 billion in food andR$ 1 billion in non food

3.1x Grupo Éxito(3) orders 70% share on sales

2525

Continued strong growth in omnichannel

Expansion of formats Wow, FreshMarket and Surtimayorista

Pioneer in innovation, including hypermarket, fresh market and real estate

Robust ecosystem, with clear customer monetization opportunities

Solid food retail leadership in Colombia and Uruguay, with robust operations and profitability

Key Takeaways

26

GPA Consolidated GPA Brazil Grupo Éxito

27

GPA - Main assets (value reserves)

• GPA paid aprox.

R$ 9.5 billion to acquire 96.57% of

Grupo Éxito through a tender offer.

Other Assets

• GPA holds 34% of Cnova, listed at Euronext: market

value of aprox. R$ 5.3 billion for GPA stake

(as of March 03, 2021)

Top of Mind Brands

• Lands and buildings in Brazil valued at

R$ 1.3 billion, book value

(as of Dec 31, 2020)

• Gas station and Drugstores

14%

Leadership in Market share

31%

43%