Embed Size (px)

Citation preview

Copyright 2009, CAIA AssociationSM. All rights reserved.

No part of this publication may be copied or reproduced, electronically or mechanically, without a prior written consent of the CAIA Association.

March 2010 CAIA Level II Sample Questions

Chartered Alternative Investment Analyst®

These questions are designed to be representative of the format and nature of actual CAIA Level II examination questions in March 2010. The sample questions are not a facsimile of the actual questions. The sample questions do not cover all of the study materials that comprise the CAIA Level II curriculum and accordingly should not be used to assess a candidate’s level of preparedness for the exam. Section 1: Provide the best answer to the following 50 questions Questions 1 through 11 Venture Capital and Private Equity Questions 12 through 17 Commodities Questions 18 through 22 Managed Futures Questions 23 through 27 Real Estate Questions 28 through 32 Hedge Funds Questions 33 through 50 Integrated Topics and Applications Section 2: Provide constructive responses to each part of these two essay questions. Question 1 Professional Standards of Practice Question 2 Current Topics

Copyright 2009, CAIA AssociationSM. All rights reserved. 1

Section 1: Provide the best answer to the following 50 questions Use the following scenario to answer questions 1 and 2

Tambourine Partners is a private equity firm that manages a series of private equity funds. Tambourine was established over twenty years ago by four co-workers who left a major private equity firm having been locked-out of senior management. The four founders of Tambourine worked hard through years of difficulty raising capital and laboring to identify the best potential investments. In the last half of their history, the fund has been able to participate in the best deals, attract large investors and generate enormous returns.

Mr. J. Jangle is considering recommending that his institution allocate capital to the latest offering from Tambourine Partners. He is focused on understanding the partnership agreement since he has limited experience with such agreements regarding private equity investments. 1. In reviewing the limited partnership agreement used by Tambourine and comparing

it with other agreements, Jangle notes the use of the term “preferred return” in describing the cash flows of the fund. Which of the following most accurately describes the concept of a preferred return with respect to partnership agreements?

A. It’s a hurdle rate that describes the return needed to trigger secondary funding B. It’s a hurdle rate that must be met for general partners to earn performance fees C. It’s a pump rate that triggers automatic cash distributions to limited partners D. It’s a pump rate that targets the highest return that general partners can earn

2. In further reviewing the limited partnership agreement used by Tambourine and

comparing it with other agreements, Jangle notes the use of the term “qualified majority” in describing the process by which the General Partner can be removed “without cause” by the limited partners. Which of the following most accurately describes “without cause” clauses with respect to partnership agreements?

A. Agreements that are standardized with well defined conditions B. Agreements that require both a dollar-weighted and investor-weighted majority C. Agreements that cause a cease in funding and generally require a high approval

vote (e.g., 75%) D. Agreements that require approval by “qualified partners”

Copyright 2009, CAIA AssociationSM. All rights reserved. 2

Use the following scenario to answer questions 3, 4, and 5 Niles Foundation has been slowly increasing the percentage of its endowment invested in private equity. The Foundation is now establishing revised and expanded guidelines for their private equity program. Susan Brick is heading up the effort to draft the proposed guidelines. It has been established that the program will continue to be managed internally and invested entirely in private equity funds, but that the allocations must be made consistently in line with policies determined by the investment committee. Ms. Brick is investigating three specific issues with regard to the guidelines: the timing of the investments, the allocation of the investments amongst private equity categories and the method of selecting funds. 3. Ms. Brick has initially advocated a guideline that establishes a fixed mix of

institutional quality private equity funds and newer, emerging funds that offer niche strategies. Which of the following terms most accurately reflect this aspect of the allocation process?

A. Core-satellite approach B. Top–bottom approach C. Investment grade–speculative grade approach D. Diversified–mixed approach

4. Ms. Brick has criticized the Foundation’s historic approach to private equity

investment as being a market timing approach rather than a cost averaging approach. Which of the following most accurately characterizes a key difficulty with using a market timing approach rather than a cost averaging approach?

A. Market timing causes much greater market risk from market panics B. Market timing substantially increases transactions costs and taxes C. Market timing in private equity funds runs afoul of regulatory constraints D. Market timing can cause vintage year concentration

5. Ms. Brick reviewed previous investment decisions and attempted to categorize

them as “top down” or “bottom up.” Which of the following decisions would most clearly be categorized as reflecting a top down strategy?

A. The fund was selected for having the highest estimated alpha B. The fund was selected for having a manager consistently performing in the top

quartile C. The fund was selected to fill voids in the portfolio’s allocation to healthcare D. The fund was selected for having the best protected intellectual property rights

Copyright 2009, CAIA AssociationSM. All rights reserved. 3

6. Which of the following statements apply more to buyout funds than to venture capital funds?

A. Their valuation risk is high because heroic assumptions are required with

traditional valuation methods B. Their source of returns comes primarily from leverage and company building C. They are invested in rapidly growing sectors or cutting edge technologies D. Their returns’ sensitivity to public markets is high

7. Which of the following features most applies to cost averaging in the private equity

markets?

A. Cost averaging can be viewed as part of an asset allocation strategy B. There is a consensus in the industry that cost averaging doesn’t work C. Cost averaging can be seen as naïve diversification over time D. Cost averaging requires forecasting which vintage year will present the best

opportunities 8. Which of the following observations is TRUE about applying an over-commitment

strategy by limited partners?

A. The strategy seeks to equate commitments to available resources B. The strategy seeks an over-commitment ratio of greater than 100% C. The strategy seeks to concentrate the limited partner’s portfolio into one or two

vintage years D. After a build-up of the portfolio, the strategy seeks a short-term orientation

9. What are two main exit routes prior to private equity funds’ maturity?

A. Secondary transactions and securitization B. Realizations and limited partner default C. Liquidity lines and selling maturing investments D. Securitization and limited partner default

10. Which method of estimating private equity betas involves calculating an

unleveraged beta?

A. Bottom-up beta B. Quoted comparables C. Relative risk measures D. Beta based on modified and corrected data

Copyright 2009, CAIA AssociationSM. All rights reserved. 4

11. Which of the following statements most accurately describes the benefits and costs of using a fund of funds structure relative to an in-house private equity investment program?

A. The additional layer of management fees charged by fund of funds is inefficient

relative to in-house private equity investment programs B. The scale economies provided by fund of funds are almost always cheaper than

in–house private equity investment programs C. Fund of funds avoids the burden of research and due diligence associated with

in-house private equity investment programs D. Fund of funds requires a subscription-based funding approach that leads to

inefficient liquidity management compared with in-house private equity investment programs

12. Under what condition does an investor who has established a long position in a 3-

month oil futures contract profit from this position?

A. When the spot price of oil is lower than today’s futures price in three months B. When the spot price of oil is higher than today’s futures price in three months C. When the spot price of oil increases over the next three months D. When the spot price of oil decreases over the next three months

13. How can we describe the average risk premium on commodities since 1959?

A. It’s been about the same as the risk premium on bonds B. It’s been lower than the risk premium on bonds C. It’s been higher than the risk premium on stocks D. It’s been about the same as the risk premium on stocks

14. Investors can gain exposure to commodities through owning bonds issued by firms

that derive a significant part of their revenue from the sale of commodities. Which of the following types of bonds is likely to offer the highest exposure to the commodity market in which the companies are involved?

A. Triple-A rated bonds B. Single-B rated bonds C. Single-C rated bonds

Copyright 2009, CAIA AssociationSM. All rights reserved. 5

15. The exponential moving average of a commodity’s closing price was $48 yesterday and is $50.4 today. Given that the exponential smoothing parameter λ is 0.6, which of the following prices is closest to today’s close price?

A. 50 B. 52 C. 54 D. 56

16. Which of the following factors is MOST likely to have significantly contributed to

the tightening of light sweet crude oil markets in 2008?

A. US and EU government requirements to improve the quality of diesel fuel B. US and EU government regulations regarding bioethanol usage targets C. Supply side disruptions caused by a surge in militant activity in Iraq D. Supply side disruptions caused by economic sanctions imposed on Iran

17. In “Do Professional Currency Managers Beat the Benchmark?”, Pojarliev and

Levich investigated a subset of returns from 34 individual currency fund managers over the 1990-2006 period. Which of the following observations is most consistent with their findings regarding the post 2000 period?

A. Profitability of trend-following rules declined while alpha generation persisted B. Alpha generation and profitability of trend-following rules declined C. Profitability of trend-following rules persisted while alpha generation declined D. Alpha generation and profitability of trend-following rules persisted

18. Suppose that a particular futures trader reports a high level of margin to equity.

What would this ratio indicate?

I. Highly levered trading II. Diversification across several exchanges III. Calendar spread trading IV. Backwardated markets

A. I or III B. I or II C. I only D. I, II, or IV

Copyright 2009, CAIA AssociationSM. All rights reserved. 6

19. Under what circumstance is the “Capital at Risk” measure MOST likely to underestimate the real risk of loss?

A. When the stop loss level is set close to (1% and less) the current market price

and the main exposure is oil futures B. When the stop loss level is set close to (1% and less) the current market price

and the main exposure is agricultural commodities C. When the stop loss level is set at 5% to the current market price and the main

exposure is oil futures D. When the stop loss level is set at 5% to the current market price and the main

exposure is agricultural commodities 20. What distinguishes the managed futures strategy from other hedge fund strategies?

A. An absence of directional bias B. An elevated credit risk C. An elevated counterparty risk D. A negative correlation to inflation

21. Amy Templeton, CAIA, is trying to determine how the established, systematic

managed futures program known as “Global Trends” is performing relative to its peers. Which of the following comparisons would be most appropriate for her?

A. The historical return volatility of the fund to the MLM Index B. The historical return volatility of the fund to the Barclay Hedge CTA Index C. The historical risk adjusted returns of the fund to the MLM Index D. The historical risk adjusted returns of the fund to the Barclay Hedge CTA Index

22. Which of the following areas is the least regulated of the managed futures industry?

A. Agricultural commodities B. Long term US Treasury note futures C. Foreign exchange D. Energy futures

23. Why do Real Estate Investment Trusts (REITS), as an industry, have a relatively

low potential for growth?

A. Because they must pay out a minimum of 90% of their taxable income as dividends

B. Because they have limited investment opportunities C. Because they generate most of their income from mortgage investments D. Because their size is limited by law

Copyright 2009, CAIA AssociationSM. All rights reserved. 7

24. Which of the following methods is used to construct the Case-Shiller Home Price Indices, an index group that tracks values of US residential real estate properties?

A. Repeated-sales pricing B. Appraisal based valuation C. Hedonic-price method

25. With respect to REIT residual cash flow valuation, which of the following features

distinguishes the Adjusted Funds from Operations (AFFO) method from the Funds from Operations (FFO) method?

A. AFFO accounts for recurring capital expenditures B. AFFO accounts for depreciation C. AFFO accounts for gain or loss on depreciable property sales D. AFFO accounts for REIT stock price appreciation

26. Identify the distinctive feature of the Lien Theory, one of the two main systems of

managing mortgage deeds in the US.

A. The ownership of the property is transferred to the lender if default occurs B. The borrower has the right to partially or fully pre-pay the principal before the

due date C. The mortgagee has the right to force a foreclosure if default occurs

27. At the end of month 27, a hypothetical mortgage-backed security’s conditional

prepayment stands at 5.50%. The beginning mortgage balance for month 28 is $475,000,000 while the scheduled principal payment is $400,000. Which of the following numbers comes closest to the projected prepayment for month 28?

A. $1.6 million B. $1.8 million C. $2.0 million D. $2.2 million

28. Which segment of the convertible profile graph is described by a convertible option

that is “at-the-money?”

A. Distressed B. Busted C. Hybrid D. Equity

Copyright 2009, CAIA AssociationSM. All rights reserved. 8

Use the following information to answer the next question. Consider the very front end of the following binomial convertible pricing tree: Current Year 1 109.55 132.63 86.75 Upper half of node = parity 119.99 Lower half of node = convertible theoretical value 57.37 99.25 29. Using this tree, which comes closest to the convertible's delta?

A. 0.55 B. 0.64 C. 0.73 D. 0.90

30. Why would we expect convertible bonds to have negative values for rho at most

points along the convertible price track?

A. Because changes in interest rates have little impact on the price of convertibles B. Because as interest rates increase, the convertible value decreases C. Because interest rates cannot go negative D. Because most convertibles have options that are out-of-the-money

31. What does a Hurst exponent of 0.2 imply about a hedge fund manager’s

performance?

A. The performance is mean-reverting B. The performance is persistent C. The performance is random

32. Distressed hedge funds tend to perform best in what market environment?

A. When credit spreads widen B. When credit spreads are stable C. When credit spreads tighten

Copyright 2009, CAIA AssociationSM. All rights reserved. 9

33. Consider an equity market where prices are volatile but are not trending, and an

investor who is in both cash and equity. What would be TRUE in this case?

A. A simple buy-and-hold will outperform a simple constant-mix strategy B. A simple constant-mix strategy will outperform a simple buy-and-hold strategy C. A simple constant-mix strategy will underperform a constant-proportion

portfolio insurance strategy D. A constant-proportion portfolio insurance strategy will outperform a simple

buy-and-hold strategy 34. What does a convex trading strategy refer to?

A. A strategy where past winners are purchased and past losers are sold B. A strategy that replicates the payoff from a covered call strategy C. A strategy that holds a constant mix of assets D. A buy-and-hold strategy

Use the following scenario to answer the next three questions Geoffrey Peck is a consultant and is currently reviewing the investment policies and practices of a major pension fund. The fund is exploring infrastructure investing and has retained Peck to provide an initial report. 35. Which of the following is LEAST accurate with regard to the conceptual

characteristics of infrastructure?

A. Large, monopolistic assets with high initial fixed costs B. Public goods that are non-rivalrous and non-excludable C. Moderate duration with elastic demand for its services D. Stable cash returns that serve as inflationary hedges

36. Peck is interested in describing the weightings of listed infrastructure investment

opportunities throughout the world and within sectors. Peck used the UBS Global Infrastructure & Utilities index to estimate geographic weightings and the Moody’s Economy.com Infrastructure Index to estimate weightings by sectors (both using market capitalizations). Which of the following most accurately characterizes the largest weightings geographically and largest weightings in terms of sectors, respectively, using these sources?

A. Asia and the US; water and gas B. Australia and Asia; transportation and communications C. Asia and the US; electricity and water D. The US and Europe; electricity and communications

Copyright 2009, CAIA AssociationSM. All rights reserved. 10

37. Peck notes that the UBS Global Infrastructure & Utilities index has been used to estimate listed infrastructure returns for the ten year ending in 2007. The performance has been compared to other investments such as equities, bonds and hedge funds. Which of the following most accurately characterizes the return and risk of infrastructure over this time interval and according to this source?

A. Moderately low returns (7%-8%) and low volatility (6-8%) B. Moderate returns (9%-10%) and moderately low volatility (8%-10%) C. Moderately high returns (13-14%) and moderately high volatility (18%-20%) D. High returns (16%-17%) and moderate volatility (13%-14%)

38. Which of the following characteristics makes the infrastructure asset class an

appealing addition to a diversified traditional asset portfolio of a pension fund?

A. Strict regulatory oversight B. Elastic demand C. Asset-liability duration match D. Low leverage

39. Consider the Goldman Sachs Commodity indices (GSCI indices). Regardless of

market direction, which of the following index and volatility period combinations would be expected to perform BEST under frequent portfolio rebalancing?

A. Low correlation, high volatility B. High correlation, high volatility C. Low correlation, low volatility D. High correlation, low volatility

40. Since the inception of the Goldman Sachs Commodity Index (GSCI) in 1992, GSCI

has been in backwardation as often as it has been in contango. In “The Strategic and Tactical Value of Commodity Futures”, Erb and Harvey investigated the effectiveness of various GSCI tactical allocation strategies. According to their research, which of the following strategies has historically provided the highest return?

A. Maintain a long position in the index when backwardated; switch to cash in

other markets B. Maintain a long position in the index when in contango; switch to cash in other

markets C. Maintain a long position in the index when backwardated; a short position when

in contango D. Maintain a buy and hold long position in the index both in contango and

backwardated markets

Copyright 2009, CAIA AssociationSM. All rights reserved. 11

41. A bank has two loans outstanding. The first is a $100 million 1-year loan at the rate

of 15% to a client with a BBB credit rating. The second is a $60 million 1-year loan at the rate of 20% to a client with C credit rating. Historical data shows that the 1-year probability of default for firms with a BBB rating is 4% while the same probability for firms with a rating of C is 7%. Investors are typically able to recover 35% and 20% of the notional value of an unsecured loan to BBB and C rated firms respectively. Which of the following values comes closest to the expected credit loss of the bank?

A. $ 3 million B. $ 7 million C. $11 million D. $15 million

Use the following information and the one-step binomial process approach to firm value estimation (discrete time compounding) to answer the next three questions Suppose the current value of the XYZ Corporation’s assets is £200, and that the value of the firm’s assets is expected to increase or decrease by 25% over the next year. The firm has one-period zero coupon debt outstanding with the notional value of £180. 42. If the one-year riskless rate is 1%, which of the following values comes closest to

the risk-neutral probability (π) of an up-move?

A. 0.48 B. 0.50 C. 0.52 D. 0.54

43. If the one-year riskless rate is 4% and the risk-neutral probability π is 0.58, which

of the following amounts comes closest to the fair value of for the risky loan?

A. £154 B. £161 C. £168 D. £175

44. If the one-year riskless rate is 10% and the fair value for the risky loan is £156,

which of the following values comes closest to the risky loan’s credit spread?

A. 4.6% B. 5.0% C. 5.4% D. 5.8%

Copyright 2009, CAIA AssociationSM. All rights reserved. 12

45. Which of the following statements MOST accurately identifies a major benefit offered by credit default swaps (CDS)?

A. CDS allow for separation of default and interest rate risks B. CDS greatly improve public risk transparency C. CDS offer protection against market overreaction to news releases D. CDS eliminate credit market counter-party risk

46. Similar to the term structure of interest rates, one can depict the term structure of

credit default swap (CDS) spreads for a given reference entity. Which of the following credit curve shapes is consistent with the notion that the cumulative probability of defaulting increases over time?

I. Downward sloping II. Flat III. Upward sloping

A. I and II B. I, II and III C. II and III D. III only

47. Consider a CDO portfolio that consists of 100 loans, each having the notional value

of $10 million. A mezzanine tranche of this structure has a notional value of $50 million with an attachment of 5% and width of 2%. The spread is 150 basis points. Assume the recovery rate is 45%. Which of the following percentages comes closest to the loss of this tranche if 11defaults happen?

A. 33% B. 43% C. 53% D. 63%

48. A long/short equity hedge fund exhibits average monthly returns of 0%, monthly

historical volatility of 7% and skewness of -0.50. Which of the following percentages comes closest to the monthly 99% confidence Value at Risk (VaR) (α = 2.326) for this fund? Account for skewness, and use the Cornish-Fisher expansion in your VaR calculations!

A. 14% B. 16% C. 18% D. 20%

Copyright 2009, CAIA AssociationSM. All rights reserved. 13

49. Daily return volatility for stock X was estimated to be 1.5% yesterday while its

historical average daily return has been 0%. After a negative news release, the stock price fell 10% today. Which of the following percentages comes closest to the daily return volatility at the market close today? Use the Exponentially Weighted Moving Average model in your calculations and assume that the decay factor λ = 0.95.

A. 1.8% B. 2.1% C. 2.4% D. 2.7%

50. The daily return volatility for stock X was estimated to be 1.5% yesterday while its

historical average daily return has been 0%. After a negative news release, the stock price fell 20% today. Which of the following percentages comes closest to the daily return volatility at the market close today? Use the Generalized Autoregressive Conditional Heteroskedastic (GARCH) model in your calculations and assume that the long run daily return volatility %25.1 , ω = 0.000005, and the innovation weight α = 0.05.

A. 4.2% B. 4.7% C. 5.2% D. 5.7%

Copyright 2009, CAIA AssociationSM. All rights reserved. 14

Section 2: Essay Provide constructive responses to each part of these 2 questions. Responses should be clear and concise. Full sentences are not required. Not all questions require the same length of response. Be guided by the notion that complete responses that call for discussion, explanation, or description can be written in one or two paragraphs. Guideline answers are provided after each question. The guideline answer represents a complete and comprehensive response to each question. Candidates will not be expected to provide responses of this length on the exam.

Copyright 2009, CAIA AssociationSM. All rights reserved. 15

Question 1 Rui Gomes holds a professional designation that requires all members to adhere to the Code and Standards. He has created a website and discussion room in order to attract new clients to the firm with which he is employed and to publish his recommendations. In a recent forum he placed a buy recommendation on a particular merger arbitrage fund based upon a study of the performance of the targets of three large takeovers between September and November of 2009. A. Describe the violation of the Code and Standards. You need not quote the number

and/or letter of the standard, but must provide an explicit description as it applies to this situation.

(3 Points)

B. Provide two recommended procedures for compliance to support the principles of

the standard that was violated.

(2 Points) Question 2 In September of 2006, a large hedge fund named Amaranth collapsed. Ensuing research and investigations indicated that Amaranth had massive positions in energy derivatives, particularly natural gas. The dominant Amaranth trading strategy involved taking short positions in natural gas futures contracts with delivery in non-winter months and long positions in natural gas futures contracts with delivery in winter months. A. Common positions involving multiple derivatives are often referred to with specific

terminology such as “straddles,” “strangles,” or “bull call spreads.”

i. Identify the name of the main strategy that Amaranth employed (described above).

ii. State the name of the relationship wherein nearby futures prices are lower than more distant futures prices.

(2 Points)

Copyright 2009, CAIA AssociationSM. All rights reserved. 16

Question 2 (Continued) B. It is believed that natural gas storage operators took futures positions offsetting

many of the positions held by Amaranth (described above). These storage operators have been described as holding a position in real options.

i. Describe the options that the storage operators hold. ii. Describe the mechanics of how storage operators would use futures contracts

with their decision to exercise or not to exercise these options. iii. Discuss whether these storage operators would prefer high or low volatility in

natural gas prices and why.

(3 Points)

C. It is believed that Amaranth relied principally upon the historical volatility of the natural gas futures prices in analyzing the risks of its positions. Till (Amaranth Lessons Thus Far, 2008) suggested a risk measurement technique that may have better captured the true likelihood of incurring large losses.

i. Name and describe the risk measurement approach recommended by Till. ii. Provide an explanation of how that methodology may have more accurately

reflected the true risks assumed by Amaranth.

(2 Points) D. As Amaranth collapsed, it was forced to liquidate its major positions due to margin

calls.

i. In addition to using the traditional markets, Amaranth employed another method to exit its final positions. Describe this method.

ii. Describe how this exit strategy affected their profitability. iii. Explain “nodal liquidity” and how this concept relates to the success or failure

of the second exit strategy employed by Amaranth.

(3 Points)

Copyright 2009, CAIA AssociationSM. All rights reserved. 17

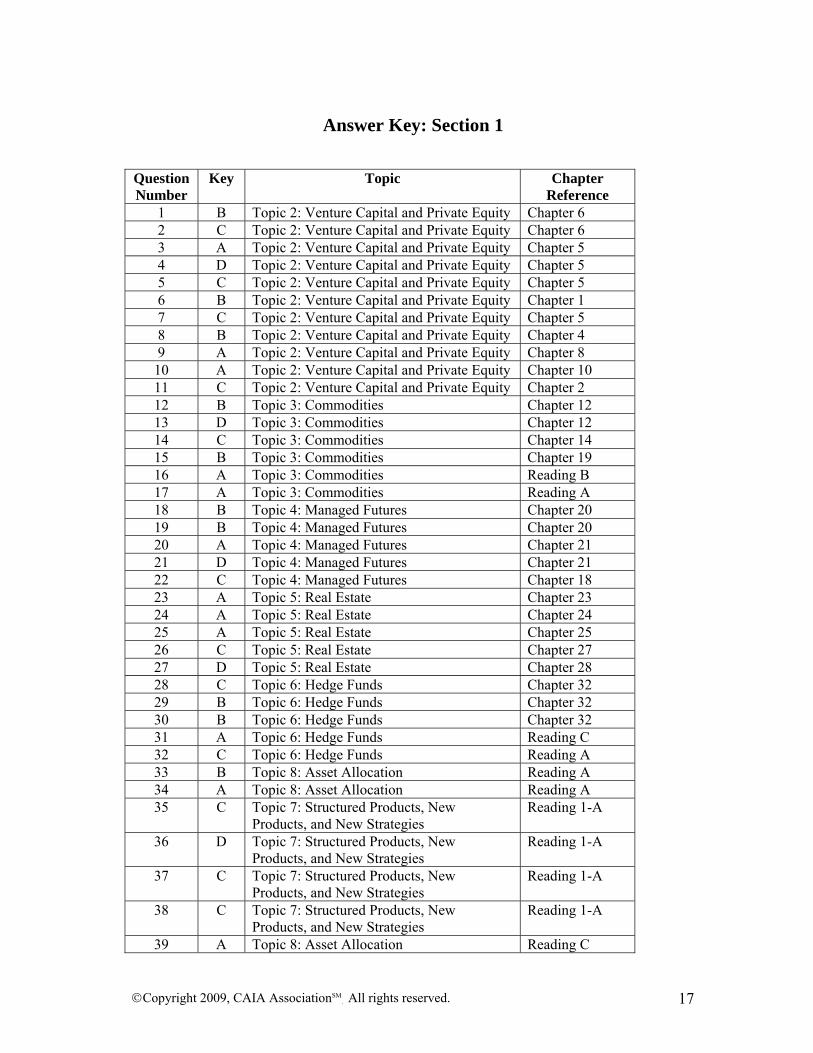

Answer Key: Section 1

Question Number

Key Topic

Chapter Reference

1 B Topic 2: Venture Capital and Private Equity Chapter 6 2 C Topic 2: Venture Capital and Private Equity Chapter 6 3 A Topic 2: Venture Capital and Private Equity Chapter 5 4 D Topic 2: Venture Capital and Private Equity Chapter 5

5 C Topic 2: Venture Capital and Private Equity Chapter 5 6 B Topic 2: Venture Capital and Private Equity Chapter 1 7 C Topic 2: Venture Capital and Private Equity Chapter 5 8 B Topic 2: Venture Capital and Private Equity Chapter 4 9 A Topic 2: Venture Capital and Private Equity Chapter 8

10 A Topic 2: Venture Capital and Private Equity Chapter 10 11 C Topic 2: Venture Capital and Private Equity Chapter 2 12 B Topic 3: Commodities Chapter 12 13 D Topic 3: Commodities Chapter 12 14 C Topic 3: Commodities Chapter 14 15 B Topic 3: Commodities Chapter 19 16 A Topic 3: Commodities Reading B 17 A Topic 3: Commodities Reading A 18 B Topic 4: Managed Futures Chapter 20 19 B Topic 4: Managed Futures Chapter 20 20 A Topic 4: Managed Futures Chapter 21 21 D Topic 4: Managed Futures Chapter 21 22 C Topic 4: Managed Futures Chapter 18 23 A Topic 5: Real Estate Chapter 23 24 A Topic 5: Real Estate Chapter 24 25 A Topic 5: Real Estate Chapter 25 26 C Topic 5: Real Estate Chapter 27 27 D Topic 5: Real Estate Chapter 28 28 C Topic 6: Hedge Funds Chapter 32 29 B Topic 6: Hedge Funds Chapter 32 30 B Topic 6: Hedge Funds Chapter 32 31 A Topic 6: Hedge Funds Reading C 32 C Topic 6: Hedge Funds Reading A 33 B Topic 8: Asset Allocation Reading A 34 A Topic 8: Asset Allocation Reading A 35 C Topic 7: Structured Products, New

Products, and New Strategies Reading 1-A

36 D Topic 7: Structured Products, New Products, and New Strategies

Reading 1-A

37 C Topic 7: Structured Products, New Products, and New Strategies

Reading 1-A

38 C Topic 7: Structured Products, New Products, and New Strategies

Reading 1-A

39 A Topic 8: Asset Allocation Reading C

Copyright 2009, CAIA AssociationSM. All rights reserved. 18

Question Number

Key Topic

Chapter Reference

40 A Topic 8: Asset Allocation Reading C 41 B Topic 7: Structured Products, New

Products, and New Strategies Reading 1

42 C Topic 7: Structured Products, New Products, and New Strategies

Reading 1

43 B Topic 7: Structured Products, New Products, and New Strategies

Reading 1

44 C Topic 7: Structured Products, New Products, and New Strategies

Reading 1

45 A Topic 7: Structured Products, New Products, and New Strategies

Reading 1

46 C Topic 7: Structured Products, New Products, and New Strategies

Reading 1

47 C Topic 7: Structured Products, New Products, and New Strategies

Reading 1

48 C Topic 10: Portfolio and Risk Management Reading 1 49 D Topic 10: Portfolio and Risk Management Reading 1 50 B Topic 10: Portfolio and Risk Management Reading 1

Copyright 2009, CAIA AssociationSM. All rights reserved. 19

Guideline Answers: Essay Questions Question 1 Level II Study Guide: Topic 1: Professional Standards and Ethics Purpose: To test candidates’ ability to understand the Standards of Professional Conduct as published by the CFA Institute. Learning Objectives: Apply Standard V with respect to Diligence and Reasonable Basis. (p. 99-103) Rui Gomes holds a professional designation that requires all members to adhere to the Code and Standards. He has created a website and discussion room in order to attract new clients to the firm with which he is employed and to publish his recommendations. In a recent forum he placed a buy recommendation on a particular merger arbitrage fund based upon a study of the performance of the targets of three large takeovers between September and November of 2006. A. Describe the violation of the Code and Standards. You need not quote the number

and/or letter of the standard, but must provide an explicit description as it applies to this situation.

(3 Points)

Standard V: Investment Analysis, Recommendations, and Actions (A) Diligence and Reasonable Basis The application of Standard V(A) is dependent on the investment philosophy followed, the role of the member or candidate in the investment decision making process, and the support and resources provided by the member or candidate’s employer. These factors will dictate the nature of the diligence, thoroughness of the research, and the level of investigation required by Standard V(A). The requirements for issuing conclusions on research will vary based on the member of candidate’s role in the investment making process, but the member or candidate must make reasonable efforts to cover all pertinent issues when arriving at the recommendation. Members and candidates enhance transparency by providing or offering to provide supporting information to clients when recommending a purchase or sale or when changing a recommendation. Given this standard, it is clear that Rui did not exercise the level of thoroughness required to recommend investment into a hedge fund. Note that the standard does not require the use of secondary or third-party research, only that the recommendations are based upon reasonable and diligent efforts to determine that the research is sound.

Copyright 2009, CAIA AssociationSM. All rights reserved. 20

B. Provide two recommended procedures for compliance to support the principles of

the standard that was violated.

(2 Points)

Recommended Procedures for Compliance Members and candidates should encourage their firms to consider the following policies and procedures to support the principles of Standard V(A): 1. Establish a policy requiring that research reports and recommendations have a

basis that can be substantiated as reasonable and adequate. An individual employee (supervisory analyst) or a group of employees (review committee) should be appointed to review all research reports and recommendations prior to external circulation to determine whether they meet the criteria established in the policy.

2. Develop detailed, written guidance for research analysts, supervisory analysts, and review committees that establish due-diligence procedures for judging whether a particular recommendation has a reasonable and adequate basis.

3. Develop measurable criteria for assessing the quality of research, including the reasonableness and adequacy of the basis for any recommendation and the accuracy of the recommendations over time, and implement compensation arrangements that depend on these measurable criteria that are applied consistently to all research analysts.

Copyright 2009, CAIA AssociationSM. All rights reserved. 21

Question 2 Level II Study Guide: Topic 9: Current Topics Till, H. "Amaranth Lessons Thus Far.” The Journal of Alternative Investments. Spring 2008, p. 82-98. (155-171) Purpose: To provide a historical analysis on the failure of a hedge fund; to introduce candidates to a commodities trading strategy. Keywords: Backwardation, calendar spread trading, contango Learning Objectives: The candidate should be able to:

1. Understand what is meant by the “term structure of a commodity futures curve” and

the terms “backwardation” and “contango.” 2. Understand the derivation of the futures curve for natural gas and the association

between the curve and potential determinants including anticipated production, consumption, and seasonal factors.

3. Explain a futures calendar spread trading and the sources of potential profits, potential losses and risk from this type of strategy.

4. Describe the type of calendar spread trading Amaranth employed and explain the rationale for this strategy as it relates to natural gas pricing.

5. Discuss the magnitude of Amaranth’s calendar spread positions: explain how this hedge fund was able to accumulate such large positions (including the role of position limits) and describe the effects of the magnitude of the positions on daily profits and losses.

6. Discuss the causes for increased volatility on the natural gas commodity futures market prior to Amaranth’s liquidation in September 2006.

7. Discuss how sophisticated storage operators can manage their storage facilities as a set of options on calendar spreads.

8. Describe how daily volatility as measured by standard deviation can underestimate potential risk (where risk is defined as the likelihood of experiencing severe loss), and explain how scenario analysis can be used to better indicate the risk of a fund’s structural position in such circumstances.

9. Describe what is meant by “nodal” or “one-way” liquidity in the commodity markets and how the lack of “two-way” liquidity adversely affected Amaranth.

10. Understand how forced liquidations can affect market prices and why changes in market prices can be correlated with the size and direction of the liquidation.

Copyright 2009, CAIA AssociationSM. All rights reserved. 22

Question In September of 2006, a large hedge fund named Amaranth collapsed. Ensuing research and investigations indicated that Amaranth had massive positions in energy derivatives, particularly natural gas. The dominant Amaranth trading strategy involved taking short positions in natural gas futures contracts with delivery in non-winter months and long positions in natural gas futures contracts with delivery in winter months. A. Common positions involving multiple derivatives are often referred to with specific

terminology such as “straddles,” “strangles,” or “bull call spreads.”

i. Identify the name of the main strategy that Amaranth employed (described above).

ii. State the name of the relationship wherein nearby futures prices are lower than more distant futures prices.

(2 Points) Guideline Response The trading strategy was a calendar spread (also known as a “time spread” or a “horizontal spread”). A calendar spread is the difference in price between two different delivery months for a given futures contract. Amaranth’s trading strategy involved taking short positions in non-winter months and long positions in subsequent winter months. When a nearby futures contract trades at a discount to more deferred contracts, one says the forward curve is said to be in contango. B. It is believed that natural gas storage operators took futures positions offsetting

many of the positions held by Amaranth (described above). These storage operators have been described as holding a position in real options.

i. Describe the options that the storage operators hold. ii. Describe the mechanics of how storage operators would use futures contracts

with their decision to exercise or not to exercise these options. iii. Discuss whether these storage operators would prefer high or low volatility in

natural gas prices and why.

(3 Points)

Copyright 2009, CAIA AssociationSM. All rights reserved. 23

Guideline Response Recall that Amaranth’s strategy was to take short positions in natural gas contracts with delivery in non-winter months (e.g., summer) and long positions in natural gas futures contracts with delivery in winter months (e.g., January). As counterparty to these positions, the owner of the storage facility has the option of buying summer gas and storing it until the winter for delivery, or liquidating their futures positions (and leaving their storage facilities empty). The operators can choose to lock in the purchase and sales prices using futures contracts if the calendar spread is attractive. By being long summer gas futures and short subsequent winter gas futures, the storage operator can “exercise” their option to buy natural gas in the summer, store it in their facilities, and then sell it in the winter. If the spread narrows prior to delivery, the storage operators can close their futures positions at a profit and elect not to store natural gas. Further, operators would then have the option of re-establishing the futures positions should the spread return to being attractive again. As option holders, the storage operators prefer high volatility since large spreads can create large profit opportunities, while the downside risk is limited to having idle facilities. This is an illustration of the asymmetrical payoff to options such that volatility can push profits higher but losses are capped at the premium. C. It is believed that Amaranth relied principally upon the historical volatility of the

natural gas futures prices in analyzing the risks of its positions. Till (Amaranth Lessons Thus Far, 2008) suggested a risk measurement technique that may have better captured the true likelihood of incurring large losses.

i. Name and describe the risk measurement approach recommended by Till. ii. Provide an explanation of how that methodology may have more accurately

reflected the true risks assumed by Amaranth.

(2 Points)

Guideline Response The volatilities of the prices and the spreads did not reflect the extent to which the levels of spreads or the levels of prices had departed from their historic levels. Till suggests that scenario analysis could have been used to better indicate the likelihood that prices and/or spreads would return to their previous levels. A scenario analysis would delineate possible outcomes and would likely recognize a reasonable probability that pricing relationships could return to previously experienced levels (or perhaps could reach extreme values). A traditional historic volatility approach may vastly underestimate the probability that a market will experience a massive one directional change.

Copyright 2009, CAIA AssociationSM. All rights reserved. 24

D. As Amaranth collapsed, it was forced to liquidate its major positions due to margin

calls.

i. In addition to using the traditional markets, Amaranth employed another method to exit its final positions. Describe this method.

ii. Describe how this exit strategy affected their profitability. iii. Explain “nodal liquidity” and how this concept relates to the success or failure

of the second exit strategy employed by Amaranth.

(3 Points)

Guideline Response Faced with mounting losses, declining equity, and the resulting margin calls, Amaranth had no choice but to unwind existing positions. In a perfectly liquid market, one should be able to liquidate positions at market prices. Given the size of these positions however, Amaranth was unable to liquidate them in organized markets without affecting market prices. So, Amaranth exited many of their major positions by paying a few major financial institutions to remove those positions. Thus, Amaranth experienced liquidation losses in excess of those resulting from adverse price movements. The concept of “nodal liquidity” is the idea that major positions may be more easily liquidated in one trading direction versus another based on the potential supply of willing counterparties. In the case of Amaranth, while many storage operators might take offsetting positions to Amaranth, few entities were willing to assume the existing positions.