Embed Size (px)

Citation preview

Report No. 1695a-PO

Manufacturing ExDort Industriesi n Portugaili' I btiree VOlHImSQ

Main ReportDecember 27, 1977

'l [ trtdi, II I H! I ( D1%iF,\ I 'Is

I ul -qw. 1I&CllAL '1(I \Urtl) AlONiY( Rt-non

0, '42,,l C F EF r C gq A L J ,r;, E C) I iF Y

lil I teg [laltXi a I t Ix" If IIl A III , II )II .IIe 1(1 ilr II,t Ir hs II"v( I h

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

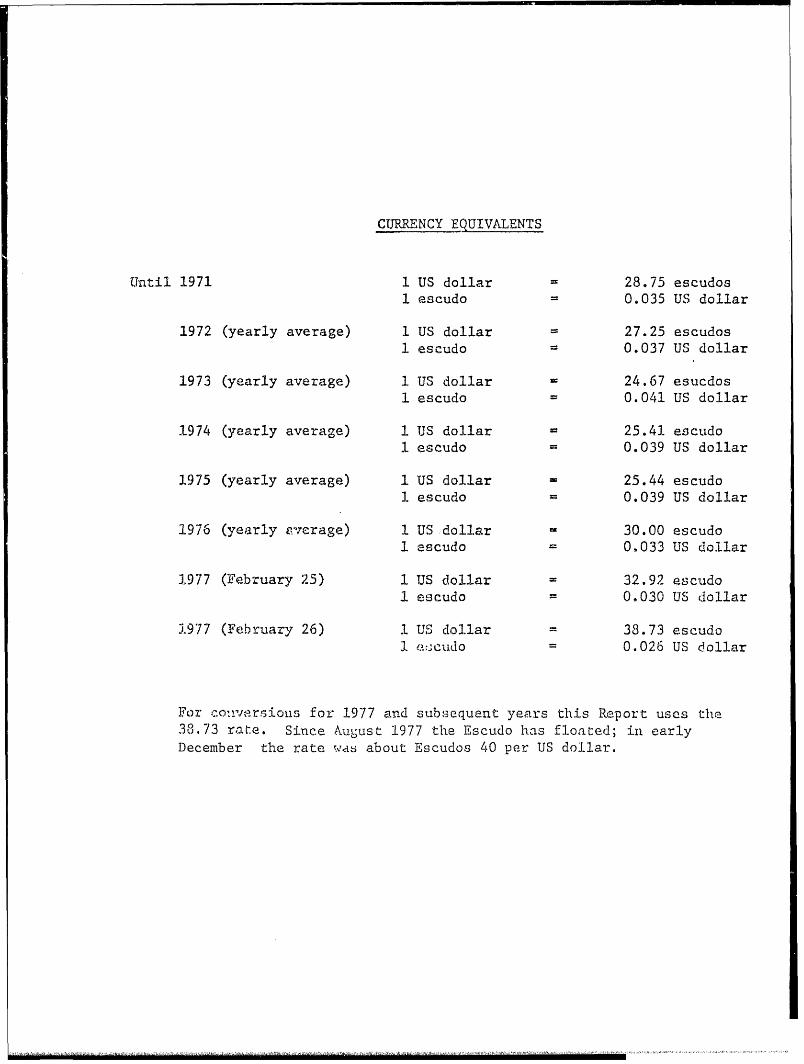

CTJRRENCY EQUIVALENTS

Until 1971 1 US dollar 28.75 escudos1 escudo 0.035 US dollar

1972 (yearly average) 1 US dollar 27.25 escudos1 escudo = 0.037 US dollar

1973 (yearly average) 1 US dollar 24.67 esucdos1 escudo 0.041 US dollar

1974 (yearly average) 1 US dollar 25.41 escudo1 escudo - 0.039 US dollar

1975 (yearly average) 1 US dollar - 25.44 escudo1 escudo 0.039 US dollar

1976 (yearly everage) 1 US dollar 30.00 escudo1 escudo 0.033 US dollar

1977 (February 25) 1 US dollar - 32.92 escuido1 escudo = 0.030 US dollar

1977 (February 26) 1 US dollar = 38.73 escudo1 c] ,lildo = 0.026 US dollar

For c0olv8rsious for 1977 and su-bsequent years this Report usCs thle38. 73 rat.e. Since August 1977 the Escudo has floated; in earlyDecember the rate rVas about Escudos 40 per UJS dollar.

FOR OFFl,YIL USE ONLY

PORTUGAL

MANUFACTURING EXPORT INDUSTRIES

TABLE OF CONTENTS

Page No.

BASIC DATA .................................... iii

GLOSSARY OF ABBREVIATIONS ...................... iv

PREFACE ........................................ v

CHAPTER I: AN OVERVIEW OF MANUFACTURING INDUSTRY ........ I

A. The Relative Roles of the Private and

Public Sectors .......................... . 1

B. Small and Medium Sized Industry ........... 2

C. Output and Growth ........................ 3

D. Employment ..... ........................... 4E. Exports: Performance, Markets and

Prospects 5 ................................. 5

CHAPTER II: INTERNATIONAL COMPETITIVENESS AND THE FOREIGN

TRADE INCENTIVE SYSTEM ......................... 9

A. Wages, Productivity and Competitiveness 9

B. Tariff Structure .......................... 11

C. Bias Towards Import Substitution ........... 14

D. Tariff Reform ............................. 15

E. Import Surcharges, Prior Import Deposits

and Quantitative Restrictions ..................... 16

F. Drawback .................................. 17

G. Credit Subsidies .......................... 19

H. Exemption of Indirect Taxes on Inputs 20

I. Income Taxes .............................. 20

J. Export Promotion Fund (Fundo de Fomento

de Exportacao - FFE) ...................... 21

K. Summary of the Effects of Trade

Incentives .............................. . 21

L. Recommendations ........................... 23

CHAPTEP. III: REVIEW OF MANUFACTURING INDUSTRIES .............. 26

A. General ................................... 26

B. 14Ietal Working Industry ..................... 29

C. The Textile and Clothing Industries 34

D. Other Industries ...................... .... 42

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

TABLE OF CONTENTS (Continued) Page No.

CHAPTER IV: FINANCING OF MANUFACTURING INDUSTRY ............. 44

A. General Financial Conditions ...................... 44B. Measures to Increase New Investment 44C. Resources to Finance Manufacturing,

1977-1980 .............................. . .46

CHAPTER V: FOREIGN INVESTMENT ............................. 52

A. The Role of Foreign Investors .............. 52B. General Background ......................... 52

C. The Investment Code and ProposedRevisions . .................................. 53

D. The Foreign Investment Institute ......... 54

- fit1 -

lanulfacturing Sector - Basic Data

Recent Years Annual Rate of Growth(%)1970 1976 (1970-76)

GDP (bln. esc., 1970 pr.ces) 158.7 212.3 5.0Mantifactur4ng Induscrv Output

(billion esctudos) 53.9 76.6 6.0

GFCF as % cf GDP1970 1975

Gross Fi;:ed Capital FormationTotal (bln. esc., 1970 prices) 31.1 28.0 (1975) 19.6 13.4% in Manufacturing 31.3 29.2 (1974)

Manu factLring Output Annual Rate of Growth (%)(bln. esc., 1970 prices) (1970-76)Foodstuffs, Beverages, Tobacco 6.3 11.3 10.2Textiles, Apparel, Footwear 10.0 16.4 8.6Chemicals & Related Activities 6.3 9.7 7.5Non-metal Minernil Products 3.9 6.8 9.721etal Products, Mechanical,and

Electrical tlachinery, Trans-portation Equipment 16.1 18.9 2.7

Emplc.ybeneTotal (000) 3,180.1 3,1.02.0 -0.5Manufacturing Industry (000) 828.9 336.9 0.15(% of Labor Force) (25.4) (23.4)

Employment in Main Industries(% of Total in Manufacturing)

Foodstuffs, Beverages, Tobacco 7.4 6.3Textiles, Apparel, Footwear 33.5 33.8Cheoica's & Related Activities 3.7 3.7Nori-wetdl Mineral Products 6.3 6.0Metal Products, Mechanical and

Elecrrical Maclhinery, Trans-portation Equipment 21.9 22.7

Annual Rate of Growth (%)(current prices)

Exports 1963 1968 1973 ]975 1968-73(mln. USS, current prices)Total. Manufactured Exports(SITC 5+6±7+8-68) 240 466 1,283 1,356 22.5

Total M'anufactured Exportsincl. processed food(03+05J-,6) and wine (1121) 343 639 1,578 -1,637 19.8

Total Exports 418 761 1,862 1,940 19.6Maini Manufactured Items

Textiles, Apparel, &Footwear 111 217 549 562 20.4Chemicals 39 56 124 141 17.2Metal Products, Mfechanical,Electrical & Transporta-tion Equipment 23 62 303 334 37.3

Processed Food 62 102 169 150 10.6Wine 31 59 12& 131 16.8

Direction of Exports 1976- - - - $ million % of Total

World 1,826 100EEC 940 51.5EFTA 294 16.1U.K. 335 18.3Getmany Fed. 197 10.8Frauce 153 8.4Sweden 141 7.7Italy 68 3.7USA 123 6.7USSR 55 3.0Angola 29 1.6Mozambique 27 1.5

-iv-

GLOSSARY OF ABBREVIATI.ONS

EFN 'Banco de Fomento NacionalCIP .Confederacao das Industrias Portuguesas

(Confederation bf Portuguesce Industries)CGD Caixa Geral de DepositosCOSEC Companhia Seguro de Creditos

(Credit Insurance Company)DEC Development Finance CompanyEEC European Economic CommunityEPPI * Empresa Publica de Parques Industrisis

(Public Enterprise for Industrial Parks)EFTA European Free Trade AssociationEIB European Investment BankFFE .Fundo de Fomento de Exportacao

(Export Development Fund)GEBEI General Studies Unit, Ministry of IndustryGFCF Gross Fixed Ca'pital FormationtAPfEI Instituto de Apoio as Pequenas e Medias Empresas

Industriais (Institute *for the Support of Smalland Medium Industrial Enterprises)

IPE Instituto das Participacoes do Estado(institute of the State Participation)

lIE1 Instituto dos Investmentos Estrangeiros(Institute of Foreign Investments)

lINE Instituto Nacional de Estatistica(National Institute of Statisti-cs)

HIT Ministry of Industry arLd TechnologyPISEE Programa de Investimentos do Sector Empresarial

do Estado (Investment Program for Public SectorEnterprises)

PIMEs Pequenas e Medias Empresas(Small and Medium Enterprises)

.

- v -

PREFACE

This Report is based on the findings of a Mission which visitedPortugal to review export manufacturing industries in April-May 1977. TheMission Report is in three parts, the Summary Report, the Main Report and theStatistical Appendix and Annexes. The Summary Report states the major find-ings and recommendations of the Mission and contains mainly those points whichshould be brought to the attention of the Government. Detailed background andanalyses are presented in the Main Report. Information on Portugal's policiesand industrial position of use primarily to readers outside the Government ofPortugal has been placed in Annexes of the Main Report. In preparing itsReport, the Mission has drawn on (and sought not to duplicate) information inother IBDR Reports on Portugal, in particular, "Portugal: An Economy inTransition", (Report No. 1408a-PO, March 16, 1977) and "Appraisal of Banco deFomento Nacional, Portugal" (Report No. 1462a-PO, May 9, 1977). Since theMission was in Portugal the Government, in August 1977, took a number ofeconomic measures; the Report notes these measures and the recommendationsmake allowance for them.

The Mission was composed as follows:

Barend A. de Vries Chief of MissionRichard L. Storch Private Investment and FinanceSurendra K. Agarwal General EconomistDavid Morawetz (Consultant) Economist (Trade Incentives)Wilson Suzigan (UNIDO Consultant) Industrial EconomistFederico Tubio (Consultant) Industrial Expert

(Textiles and Clothing)Walter Oettinger (UNIDO-Bank CP) Industrial Expert

(Metal-Working Industries)Jacob Levitsky Industrial Expert

(Other Industries, TechnicalAssistance)

In addition Mr. Francis Colaco participated in part of the Mission'sfield work. Messrs. S. Rangachar, C. Gomez and Mrs. S. Craigmile assisted inthe preparation of the Report.

Messrs. A. David Knox and M.G.S. Aiyer and mission members discussedthe draft Report with the Government in November 1977.

CHAPTER I

AN OVERVIEW OF MANUFACTURING INDUSTRY

A. The Relative Roles of the Private and Public Sectors

1.01 This Report deals with the prospects and problems of Portugal's

exoort industries and with the measures wlhich can be taken to accelerate the

growth of output and employment in these industries. The Report concentrates

on the textile and clothing, metal, mechanical and electronics industries, as

well as food processing, footwear, furniture, cork, and paper and pulp. These

industries, with the exception of paper and pulp, are largely in the private

sector. As a result of measures taken in 1974-76, the public sector has in-

creased its role in manufacturing, but despite these measures private firms in

the manufacturing industry continue to dominate aggregate output and to employ

the bulk of the industrial labor force.

1.02 The measures effecting manufacturing in 1974-76 included the nation-

alization of the banking system, insurance companies and the power sectGr, and

the takeover by the Government of some of the large industrial groups in indus-

tries such as steel, cement, petroleum and petrochemicals and tobacco as well

as most modes of public transport, radio and TV. The formal steps were com-

pleted by September 1975. The nationalization of financial institutions gave

the Government varying degrees of participation in private sector enterprises.

There are different types of public enterprises: those which were in the

public sector prior to 1974, those which were nationalized, and those in which

the State has acquired shareholder participations. In addition, there are

about 80 enterprises in the manufacturing industry in which the Government

intervened because of their financial difficulties or labor problems. In the

manufacturing industry of the 130 firms with State ownership, 30 were public

enterprises (100% ownership), 55 were State controlled enterprises (more than

50% ownership), and 45 were enterprises with 20-50% State participation. These

enterprises now account for about 17% of value added, 34% of gross fixed cap-

ital formation and 12% of the labor force in the manufacturing industry.

1.03 Nationalization and Government intervention created uncertainties

for investors and industrialists. The Government has now taken a number of

measures to remove their uncertainties. First, the Government has announced

that there will be no more nationalizations. Second, the "disintervention"

process has started and is to be completed by July, 1977; however, due to the

complicated and serious difficulties of many intervened companies, this pro-

cess will probably take longer than planned. Third, the law concerning com-

pensation for nationalized assets has been approved and financial measures to

set troubled enterprises back on their feet have been instituted (see Chapter

IV).

1.04 The Republican Assembly in May 1977 agreed on the delineation of the

public and private sector and the principles to be followed in their opera-

tions. All public utilities, post and telecommunications, banking, insurance,

and transport will be public sector. In the manufacturing industry, the public

sector will include the armaments, oil refining, petrochemical, fertilizer,

- 2 -

iron and steel, and cement industries. For these industries joint venturescould be authorized when the need justifies it, although the State wouldretain a majority interest. According to the law, the Government may handover to the private sector the small and medium size firms which were national-ized indirectly and are not in the above sectors, provided the workers do notopt for self-management or cooperatives.

1.05 With the implementation of all the measures mentioned above, businessconfidence, which has recently improved, will be given a further boost. Also,investment by the private sector should revive and is the essential key toincreased production and exports. The public sector will, however, remainimportant: the medium-term plan envisages that more than half of total produc-tive investment during 1977-80 is to be in the public sectors.

B. Small and Medium Sized Industry

1.06 Portugal's industrial structure is characterized by a large numberof very small enterprises. Of the 14,900 enterprises in manufacturing, in1974, 90% were small and medium sized firms (Pequenas e medias empresas orPMEs) employing up to 100 workers; 33.1% of all firms employed up to 10workers and 80.7% up to 50 workers. The predominance of PMEs is a markedfeature of all manufacturing subsectors as shown in Table I-1 below,

Table I-1: SIZE OF ENTERPRISES IN THE MANUFACTURING INDUSTRY(Number of Enterprises with Five or More Workers, January 1974)

101- 501- OverNumber of Workers 5 - 10 11 - 20 21 - 50 51 - 100 500 1000 1000 Total

Manufacturing Industry 4,931 3,781 3,314 1,388 1,268 148 70 14,900X of Total 33.1 25.4 22.2 9.3 8.5 1.0 0.5 100

of whichFood 446 364 321 156 199 10 2 1,498Textiles 250 276 402 217 286 44 25 1,500Clothing 77 78 40 18 15 1 - 229Footwear 803 460 425 158 113 6 - 1,965Metal products 599 386 337 148 103 9 4 1,586Machinery 257 143 156 86 65 9 8 724Transport equipment 631 382 224 85 62 7 5 1,396Miscellaneous mfg. 188 107 106 35 31 3 - 470

Source; Table 5.1.

1.07 There were only 218 manufacturing enterprises with more than 500workers. They were concentrated in food industry, textiles, clothing, chem-icals, non-metallic minerals, basic metals, and metal manufacturing industries.Of these only 70 employed more than 1,000 workers.

- 3 -

1.08 Small scale enterprises are generally less capital intensive thanmedium and large scale firms. But many of them, in common with enterprisesof similar size in other countries, also have deficiencies in production,management, and marketing. These problems stem from the small size, familyownLership of most firms and limited access to finance. Until the revolutionin 1974 there was no Government agency to deal with the specific problems ofPMEs. These enterprises were, however, able to survive and remained profit-able often due to low laboc costs.

1.09 As a result of the establishment of a minimum wage, changes in laborconditions, and steep increases in raw material prices during 1974-76, PIMEstended to become trapped in lower profitability and losses and faced severeliquidity problems. To help PMEs overcome their problems, the Government in1975 set up IAPMEI (The Institute for Assistance to Small and Medium SizeEnterprises (see Annex III-4). Considering the short period of its operationsIAPI4EI has become an important organization which has helped PtlEs in overcomi-ing their liquidity crisis.

C. Output and Growth 1/

1.10 Manufacturing was a leading sector in Portuguese growth in 1963-73and exports were a key factor in this growth. Value added in manufacturinggrew at 10-11% p.a. and GDP at 7 percent. The metal products, machinery andtransport equipment industries increased their share in the total manufactur-ing output while textiles and clothing held their share and other traditionalsectors (food, beverages, wood and cork) declined. In 1973, manufacturingoutput contributed 35.5% to GDP.

1.11 Exports were particularly important in textiles, clothing, footwear,metal products, machinery and transport equipment. The dollar value of ex-ports increased relative to manufacturing value added in 1963-73 from 43.5%to 46.1%.

1.12 Portugal has become increasingly integrated with the world economy.The share of manufactured imports in domestic supply increased from 50.7% in1963 to 56% in 1973. The import content of manufacturing is relatively highwith imports accounting (directly and indirectly) for 25% of export production.Likewise, a relatively high proportion of intermediate inputs is imported,e.g., textiles (50.9%) and non-electrical machinery (54.1%). 2/ (Annex I-1,Table 4).

1/ For details, see Annex I-1.

2/ These percentages will now be much higher because of the worldwideincrease in prices and the loss of former colonies as chief suppliersof cheaper raw materials. No new recent data is available on the importcontent of Portugal's exports but it could be anywhere between 34-45%.

-4-

1.13 The design of trade incentive policies must necessarily allow for

the open character of the Portuguese economy. Given the high import content

of manufacturing output, restrictions on imports will quickly have a restrain-

ing effect on productivity and competitiveness. Moreover, t'ie importance of

exports in manufacturing output means that acceleration of export growth is

essential for future growth of manufacturing output and employment.

1.14 In recent years social and economic changes caused a decline in

growth with manufacturing growth decelerating to 2% in 1974 and output falling

by 5.6% in 1975. In 1976 output increased by 5.5 - 6% and once again surpassed

the 1974 level. The wood and cork, textile and machinery industries suffered

most, while pulp and paper, metal products and chemicals faired best. Capacity

utilization fell to less than 70% in 1976 compared with more than 80% in 1972-

74 (Table 4.1). Capacity utilization is particularly low in the textile and

clothing, wood and cork and metal manufacturing industries.

D. Employment 1/

1.15 Unemployment presents the country's economic management with problems

to which there are no quick solutions. In total some 452,000 or 12.7% of the

labor force is unemployed, and moreover there is considerable underutilization

of labor in the manufacturing industry. Of the total unemployed 137,000 are

looking for new jobs, 189,000 are looking for their first jobs and 126,000 are

returnees from the former colonies. Most of the unemployed are unskilled and

white collar workers. Only 25,473 out of a total of 207,545 unemployed regis-

tered with the National Employment Service stated their preference to work in

the manufacturing industry.

1.16 At the end of 1976 the manufacture industry employed 836,900 or 27%

of the labor force. "Export industries" 2/ play an important iole in employ-

ment. They provide employment for 710,500 persons, i.e., 84.9% of the total

employment in manufacturing and 22.9% of total employment in the economy.

About 250,000 persons are employed in the textiles and clothing industries

alone. Export industries are generally more labor intensive than industries

producing mainly for the home market (as chemicals, cement, fertilizer, and

basic metals); exceptions are the pulp and paper and certain mechanical indus-

tries. The former have a higher employment coefficient (number of workers per

value of output) and lower capital investment per worker than the latter (see

Annex I-1, Table 4 and Annex I-2, Table 4).

1.17 The Government's draft medium-term Plan for 1977-80 gives high

priority to improvement in employment. It envisages that 203,000 new jobs will

be created of which 34,000 would be In the manufacturing industry, i.e., 17%

1/ For details see Annex I-2.

2/ "'Export industries" in this Report include: food, beverages, tobacco,

textiles, clothing, footwear, wood and cork, furniture, paper and print-

ing, leather, metal products, non-electrical machinery, electricalmachinery, transport equipment, and miscellaneous manufacturing. Most of

the industries export more than 25% of their share added (Table 2.3).

-5-

of the total new jobs. Thus industry would be a minor provider of new employ-ment and, in fact, the Plan appears to expect that most new manufacturingemployment will be created in capital intensive industries. According to thePlan construction, services and trade sectors will be a principal force forcreating new jobs during 1977-80.

1.18 At present, capacity utilization in manufacturing is low and thereis excess labor in most firms. These factors and the restructuring of thetextile, clothing and shoe industries, will tend to limit new job creationin the years immediately ahead. Many of the less economic smaller mills willneed to be consolidated through mergers or absorbed by the largest expandingfirms.

1.19 The total employment impact of the manufacturing industry will dependon several critical decisions ahead. Improvement and stability of labor condi-tions are crucial to create new jobs. Recognizing this, the Government hastaken a number of measures affecting labor rules. The assembly recently passedlaws concerning workers' committees, dismissals and strikes. Their implementa-tion should enhance certainty about work rules in Portugal. Discipline isapparently improving and labor conditions in general are better compared withwhat they have been dtiring 1974-76.

1.20 An accelerated export-led industrial growth with emphasis on laborintensive industries, which is well within Portugal's potential, would addnew jobs in 1979-80 and subsequent years well above those now in sight espe-cially when indirect employment benefits associated with such a strategy areincluded in the analysis. Employment and growth prospects are particularlypromising in clothing, footwear, wood, cork, furniture, glass and glassproducts, metal products, machinery, ship construction and ship repair 1/.

E. Exports: Performance, Markets and Prospects 2/

1.21 Exports (particularly of manufactured goods) expanded rapidly during1963 and 1973. Manufactured exports grew by 12% in real terms and some 45% ofthe manufactured output was exported. The leading export industries were tex-tiles, clothing, machinery, wine, fruits and vegetables (mainly tomato paste),fish, wood and cork, non-metallic minerals and chemicals. The industriesstudied by the mission account for about 80% of manufactured exports (includ-ing wine and processed food) and were 69% of total exports in 1973.

1/ Investment in the manufacturing industry will lead to a significantdemand for construction materials and thus create a large number ofjobs in construction materials industry.

2/ For details see Annex I-3.

-6-

1.22 Portugal's membership in EFTA was an important factor in exportgrowth. Together with EEC countries, EFTA countries accounted for 68% of theexpansion of exports in 1963-73. Exports to EFTA countries accounted for 38%of the increase in the clothing exports in 1903-73 and 27% of the textileexports. Until 1974, the former African colonies provided sheltered marketsfor Portugal's exports. Angola and Mozambique accounted for 21% of Portugal'stotal exports in 1963 and 12% in 1973.

1.23 Exports declined sharply, however, following the events in 1974 dueto the loss of markets in the former African colonies, the unstable situationin Portugal, and the recession in the OECD countries to which Portugal exported78% of its total exports in 1973. Exports in constant dollar terms in 1976were 35% lower than in 1973. Exports to Angola and Mozambique declined to only3% of total exports in 1976.

1.24 The importance of manufactured exports to the Balance of Paymentsis illustrated by the difference between actual performance in 1976 and levelswhich could have been achieved on a "normal" trend. In 1976 manufactured ex-ports were, in current dollars, about $1.4 billion or slightly above the 1973level of $1.28 billion. Had Portugal kept pace with manufactured exports ofLDC's to OECD countries they would have increased by 40-50% or some $530 mil-lion more than was actually achieved. This would have constituted a netimprovement (after allowing for raw material imports) of some $400 millionover actual performance.

1.25 Prospects. Portuguese manufactured exports can be increased througha combination of cost reduction, productivity improvement and strengtheningof management and marketing (Chapter III). In several industrial branchesproduct quality and mix will need to be improved. The increase in exportvolume will make possible better utilization of labor and will tend to improvelabor productivity significantly. At the same time an increase in exports willhelp improve capacity utilization.

1.26 The medium term Plan (1977-80) projects growth of traditional exportsat 8.8% (textiles, clothing, wood, cork and paper and pulp) and 15.9% formachinery and basic metal products. Overall exports are projected to grow 12-13% p.a. The mission feels that if adequate incentive measures are providedand industrial management is improved as recommended in Chapter III, Portugalshould be able to expand exports of several manufactured items at a higherrate than those given in the Plan particularly in the later years of theperiod and after 1980. There are good possibilities to expand exports ofprocessed fishery products, fruits and vegetables, paper and pulp, clothing,footwear, furniture, metal manufacturing and machinery, consumer electronics(color TV sets), glass and glassware, and plastic products. Relatively favor-able growth rates estimated by the mission include textiles and clothing (11%for 1976-80), footwear (22% in 1974-81), cork (11.6% in 1977-81), pulp andpaper (23% in 1976-78), furniture (26% in 1976-80). In metal manufacturingand machinery Portugal's prospects for expanding exports are also particularlypromising (see Chapter III).

1.27 Portugal's export prospects are enhanced by the fact that at pre-sent its most promising products have only a minor share in its major markets.(Its share in the imports of the EEC and EFTA countries was only 0.7% in 1973.)This is true e-ven though for some of its exports it is subject to quota re-strictions. According to the 1976 Agreement between the EEC and Portugal,ceilings had been established on the quantities of several products whichPortugal can export to the EEC member countries. These restrictions refer tothe articles of natural cork, cotton yarn, woven fabric of synthetic fibers,twine ropes and cables, undergarments, and outergarments. There are also"voluntary" quotas on a number of -extiles and clothing items which Portugalcan export to the United Kingdom. However, the ceilings are set in metric tonswhich means that by upgrading products it should be possible to increase sig-nificantly the value of exports of these items. The Portuguese are clearlycorrect in anticipating that membership in the EEC will be advantageous totheir export growth. Such membership will, however, also imply that importrestrictions be kept low and trade incentives generally conform to the Europeanstandards.

1.28 With aggressive marketing efforts, Portugal could also exportto North Africa and the Middle-East, and East-European countries such asCzechoslovakia (metal-manufactures), Hungary (cork) and Romania (ship repair,cork, batteries). Portugal has already been successful in exporting footwearto USSR and prospects for textiles appear good; exports to USSR were 3% ofPortugal's total exports in 1976. There are also indications that Portugal'sexports to its former colonies (Angola and Mozambique) could improve in thenear future. Countries in Latin America could also be potential markets forPortuguese exports.

1.29 The Plan's growth rate of 7.9% p.a. for manufacturing output is wellbelow Portugal's potential and would be exceeded if Portugal takes appropriatemeasures and accelerates its export growth. The Plan's projected growth ratesappear low for the metal products, machinery and transport equipment industriesas well as the traditional export sectors. These are the sectors in whichPortugal should be able to utilize its comparative advantage and substantiallyexpand exports. Furthermore, these sectors have relatively low capital-laborratios and, therefore, a rapid export-led growth in their output can make asignificant impact on Portugal's present high unemployment rate. If appro-priate policies to expand exports, as discussed in Chapter II of the Report,were followed, manufacturing output could increase at a rate above that indi-cated in the Plan.

1.30 Investment. As discussed in Annex I-4, investment in manufacturingdeclined to Escudo 15.3 billion ($601 million) in 1975 and Escudo 16.5 billion($550 million) in 1976 compared with Escudo 19.6 billion ($767 million) in1974. In 1977 prices, investment in manufacturing in 1974 was around $1 bil-lion. Assuming that the Government is successful in reviving investment, 1978investment in manufacturing could reach once again the 1974 level, i.e., $1billion.

- 8 -

1.31 The Mission has not made detailed projections of investment in themanufacturing sector. It seems possible, however, that accelerated export-ledgrowth could involve output growth for the sector as a whole of at least 10%per year and investment growth of 25% (see Annex I-4). Sustained export growthwill require the construction of new facilities after an initial period ofimproving capacity utilization. However, from the start significant investmentwill need to be made in plant modernization, re-equipping and restructuring.Investments by 1979 could rise to $1,265 million and in 1980 to $1,400 million(in 1976 prices). During 1977-80 the total investment in the manufacturingindustry would amount to some $4,400 million. The actual amount would, ofcourse, depend among other factors on the realization of plans for the steel,cement, and chemical industries.

1.32 In the early seventies, approximately 68% of the manufacturinginvestment took place in the "export industries" (see Table 3.1). This ratioimplies that out of a total of $4.5 billion some $3 billion investment shouldbe in export industries in 1977-80, leaving around $1.5 billion for otherindustries. The latter figure could be significantly exceeded if presentplans for heavy industry were to materialize. The substantial increases inmanufacturing investment will make necessary new planning and resource alloca-tion procedures so as to assure that sufficient resources are available tohigh priority export industries identified in this Report as well as projectsin heavy industry with a high economic return (paragraphs 4.09 and 4.10).

-9-

CHAPTER II

INTERNATIONAL COMPETITIVENESS AND

THE FOREIGN TRADE INCENTIVE SYSTEM

2.01 This chapter analyzes the explicit and implicit incentives and dis-

incentives which currently influence the production of exports and import

substitutes in Portugal.

2.02 Portugal is suffering from a severe balance of payments deficit.

To reduce import demand and stem the deficit, the Government has taken a

number of measures:, import surcharge, prior import deposits and quantitative

restrictions. It has taken further steps directly to stimulate exports, e.g.

interest rate subsidies and tax exemptions. The mission has sought to analyze

the impact of these various measures on the allocation of resources and in

particular on the profitability of export industries. It has done so by

studying the incentive system as a whole and by reviewing ,ne system's impact

on individual export manufacturers, usually through interviews with firms.

2.03 The incentive measures must, of course, be seen against the back-

ground of increases in wage costs and changes in exchange rates and in produc-

tivity, both in Portugal and abroad. After discussing the changes in the com-

petitiveness of manufacturing industry since 1973, this Chapter analyzes the

incentive effects of the customs tariff; of the surcharges, restrictions and

advance import deposits and, finally, of other measures such as credit subsi-

dies and tax rebates.

A. Wages, Productivity and Competitiveness 1/

2.04 In examining Portugal's competitiveness it seems appropriate to com-

pare wage cost and productivity trends in Portugal with those in Portugal's

main trade partners and competitors since 1973. In 1973 the exchange rate for

the Escudo seems to have been adequate to maintain balance of payments equi-

librium at least in the short to medium term. (See Annex II-1 for details).

2.05 Data for Portugal on the one hand, and France, Germany, the U.K.

and the U.S. on the other, indicate that annual earnings in Portugal (adj'lsted

for exchange rate changes) increased in total about 4% more than wage earnings

1/ The analysis is relative to prices and exchange rates as of February 1977.

The floating of the Escudo since August 1977 has partly corrected for

domestic inflation since February.

- 10 -

in its trading partners between 1973 and early 1977 1/. In addition, fringebenefits in Portugal have at least kept pace with, and may have been morerapid than those in Portugal's trade partners during 1973-77. Social securitycontributions by employers increased from 17% of wages in 1972-76 to 19% fromend-1976 onwards, while employers' contributions to the unemployment fund in-creased from 1.5% in 1973 to 3% in 1975. To the extent that these increaseswere more rapid than in the rest of Europe, the difference in the increase(at most 3.5%) should be added to the relative wage increase of 4%, makingPortugal's wage disadvantage (compared with its 1973 position) 7.5% in total.

2.06 Similar comparisons can be made between Portugal and its Europeancompetitors, e.g. Italy, Greece and Turkey. (See Annex II-1, paragraph 11).Since 1973, Portuguese wages have increased somewhat relative to those inItaly, (including an allowance for fringe benefits). Italy is an important"tcompetitor", particulaLly in exports of clothing and footwear. As discussedin Chapter III, Portugal has to improve its product quality and compete in thesame markets as Italy.

2.07 For the manufacturing sector as a whole, i.e. including both"export" and "heavy" industries, Portugal's wage disadvantage may be offset,in part, by a relative improvement in productivity. In 1973-76 total manu-facturing output improved somewhat (2%), while employment declined by 3.6%.Hence productivity measured as output per man-year improved by 5.8%. Thiscompared with an improvement in productivity in the U.S. and leading European"trade partners" of 3.4% on average (weighted by their shares in Portugal'sexports). Portugal's productivity improved by 2.3% in relative terms. Hence,after allowing for productivity changes the wage disadvantage for the manu-facturing sector as a whole, is 5.1%.

2.08 The improvement in Portugal's productivity in 1973-76 was caused,principally, by a decline in the work force and a completion of investmentsand an associated increase in output in certain industries, mainly the "heavyindustries" (e.g. pulp and paper, chemicals, oil and coal products). In 1973there were indications of excess labor in some industries and a decline inthe work force since then (and a decrease of 12.6% in total hours worked peryear) did not adversely affect output in all cases. However, the improvementin productivity is spread unevenly over the different industries. In manyexport industries, and especially the textile and clothing industries, outputdeclined more than employmeint, and productivity fell an average by 2.7% (AnnexII-1, Tables 2 and 3). According to available statistics the most severeproductivity declines occurred in non-electrical machinery (36%) and wood andcork (12%) and textiles and clothing (12%). The Mission's observations basedon plant interviews confirm that productivity (output per man-year) has

1/ This figure includes allowance for the fact that Portuguese salaries arenow naid for 14 months instead of 13 1/2 as previously. The wage-costdisadvantage is calculated relative to 1973 and should not be interpretedas an absolute wage disadvantage. Portugal's wages are well below thoseof the U.S. and the main European countries (e.g. see Chapter III, para-graphs 3.42 and 3.43).

- 11 -

declined in certain export industries, with output per man-hour (allowing for

the decline in hours worked) having at best recovered to 1973 levels. (Annex

II-1, paragraph 10).

2.09 Thus for the export industries the effect of the wage disadvantage(7.5%) is enhanced by the deterioration in productivity - to an average of

10% for the export sector as a wiole and more for certain key industries:e.g. close to 20% for the textile and clothing industries.

2.10 The deterioration since 1973 in the relative competitive positionof Portugal's export industries will have to be overcome by a combinationof measures aiming at a reduction in costs and improvement in productivity.It is unlikely that real wages will decline and hence, other cost reducingmeasures will be necessary. Improvements in productivity will have to be

associated with an increase in output and exports and a number of measures

discussed in Chapter III, particularly improvements in management, the lay-out of plants, modernization of machinery and new plant investment.

B. Tariff Structure

2.11 From the viewpoint of the incentive system, two main features ofthe current Portuguese tariff structure should be noticed:

(a) Protection varies significantly and arbitrarily from sectorto sector; the uneveness of the tariff structure is worsenedby differentiation according to country of origin, (e.g.lowering of tariffs on imports from EFTA countries);

(b) The use of tariffs without offsetting export subsidies biasesthe allocation of resources away from exporting towards importsubstitution.

2.12 S -ctoral Variation of Protection. The Portuguese tariff scheduleis currently set out mainly in "specific" rather then "ad valorem" terms.This means that without months of detailed analysis it is not possible todiscover even nominal let alone effective rates of protection.

2.13 The General Studies Unit (GEBEI) of the Ministry of Industry isputting together the available data to examine the 1977 pattern of effectiveprotection insofar as it can be ascertained. The results of this work are notyet available. In the meantime, GEBEI has produced an analysis of protection

based on 1970 tariff rates with the addition of the 1976 and 1977 surcharges(but excltuding prior import deposits and quantitative restrictions). These

data are summarized in Table II-1. In November 1977, when the report wasdiscussed with the Government, GEBEI, presented similar data based on the 1974tariff which are summarized in Table II-la.

Page 12

Table II-1 NOMINAL AND EFFECTIVE PROTECTION FROM TARIFFS AND SURCHARGES, 1977(IN PRACTICE, AFTER EXEMPTIONS - PERCENT)

Nominal ProtectionTariff 1970 Effectiveplus Protection

Tariff 1970 (Balassa Method)plus derived from

Input-Output Sector Tariff 1970 a/ 1976 Surcharge b/ 1977 Surcharge b/ Column 3 c/

1. Agriculture 9.5 16.6 19.1 232. Forestry 1.8 28.6 28.6 29

3. Livestock 2.2 2.7 2.8 0

4. Fishing and conserves 8.7 19.4 19.4 20

5. Mining - metallic 0.5 0.6 0.6 -5

6. Mining - non metallic 0.2 27.0 27.0 33

7. Meat and conserves 10.7 11.2 11.2 423

8. Milk products 63.6 83.3 83.3 4,453

9. Fruit conserves 13.5 43.0 43.0 39

10. Edible oils 12.5 12.5 12.5 -305

11. Animal feed 1.7 2.8 2.8 -38

12. Other food products 27.8 36.5 37.3 292

13. Beverages 329.2 355.0 355.0 278

14. Tobacco 66.9 106.0 106.0 133

15. Textiles - wool 19.8 39.1 39.1 118

16. Textiles - cotton 20.1 50.0 50.0 10517. Textiles - synthetic fibers 22.5 51.3 52.4 341

18. Clothing 24.4 54.9 54.9 65

19. Footwear 18.3 48.3 48.3 6320. Leather and products 17.8 49.3 49.3 173

21. Wood 4.5 35.5 36.2 60

22. Cork 8.6 33.5 47.8 13023. Furniture and upholstery 24.4 79.9 79.9 14824. Paper paste (pulp) 0.1 25.4 25.4 65

25. Paper, carton and products 10.6 31.0 31.7 39

26. Printing 16.5 28.2 28.7 45

27. Rubber and products 33.0 62.7 62.7 153

28. Plastic products 43.7 73.2 82.9 194

29. Basic chemicals 7.3 21.9 21.9 58

30. Resins 8.4 22.8 22.8 14531. Inedible oils; pesticides 15.3 15.3 15.3 -95

32. Paints, varnishes, lacquers 19.8 48.4 48.4 116

33. Other chemical products 21.1 44.7 44.7 123

34. Derivatives of petroleum and coal 7.8 7.8 7.8 54

35. Glass and products 32.3 56.4 62.7 119

36. Cement 11.4 41.4 41.4 65

37. Other non-metallic min. products 14.5 43.2 46.9 60

38. Iron and steel 16.4 24.9 24.9 67

39. Non-ferrous metals 2.7 15.1 15.1 5840. Metal products 19.0 45.6 47.7 75

41. Non-electrical machinery 9.0 26.2 26.5 2242. Electrical machinery and equip. 15.8 43.6 44.0 71

43. Shipping repairs and construction 11.7 39.5 39.5 5144. Tranbport equipment 22.3 30.7 31.0 135

45. Other manufacturing 13.2 38.8 41.5 72

Notes:

a! Calculated as: customs duty collections as percent of value of imports.

b/ Assumes that goods exempted from regular tariff are also exempted from surcharge.

c/ Based on input-output table for 1970 when wages, and hence value added were much lower than in 1977.No price comparisons' available.

Source: Unpublished data, GEBEI, Ministry of Industry

- 12a -

Table II-la NOMINAL AND EFFECTIVE PROTECTION FROM TARIFFS AND SURCHARGES, 1977(IN PRACTICE, AFTER EXEMPTIONS - PERCENT)

Nominal ProtectionEffectiveProtection

Tariff 1970 Tariff 1974 (Balassa Method)plus 1976 plus ln77 derived from

Input-Output Sector Tariff 1974a/ Surchargeb/ Surchargeb/ Column 3 c/

1. Agriculture 7 13 15 202. Forestry 00 00 00 - L3. Livestock 1 1 1 - 114. Fishing & Conserves 1 63 23 305. Mining - metallic 00 00 00 - 46. Mining - non metallic 00 24 24 297. Meat & Conserves 2 2 2 18. Milk products 23 43 43 44079. Fruit conserves 9 28 28 15

10. Edible oils 8 8 8 -10311. Animal feed 1 2 2 - 2412. Other food products 10 13 13 13113. Beverages 65 94 94 84514. Tobacco 104 104 104 174015. Textiles - wool 10 30 30 5516. Textiles - cotton 15 42 42 9217. Textiles - synthetic fibers 8 38 39 12018. Clothing 6 36 36 2119. Footwear 19 50 50 13520. Leather & products 6 28 28 10421. Wood 3 33 36 7422. Cork 1 2 4 1023. Furniture & upholstery 14 68 68 13424. Paper paste (pulp) 00 00 00 - 325. Paper, carton & products 6 26 27 4026. Printing 7 19 19 2727. Rubber & products 15 37 37 8628. Plastic products 13 39 48 11529. Basic chemicals 1 8 8 1330. Resins 00 15 15 14231. Inedible oils; pesticides 00 00 00 -23432. Paints, varnishes, lacquers 8 37 37 9133. Other chemical products 3 9 9 - 334. Derivatives of petroleum & coal 7 7 7 192835. Glass & products 12 38 47 7736. Cement 9 58 58 17437. Other non-metallic min. products 7 39 42 5938. Iron & steel 1 5 5 1039. Non-ferrous metals 1 13 13 6040. Metal products 8 34 37 8941. Non-electrical machinery 3 15 15 1142. Electrical machinery & equip. 8 31 31 4843. Shipping repairs & construction 1 29 29 4744. Transport equipment 2 17 18 2245. Other manufacturing 6 24 27 33

NOTES:

a/ Calculated as: customs duty collections as Dercent of value of imDorts.b/ Assumes that goods exempted from. regular tariff are also exempted from surcharge.

cf Based on input-output table for 1074.

Source: Unpublished data, GEBEI, Ministry of Industry.

- 13 -

2.14 The average nominal tariff rate for each sector has been estimatedby taking customs duty collections as a percent of the value of imports. Onthis basis, the average tariff rate for all industry (excluding surcharges)is about 22%. However, this method of calculation tends to underestimate theprotective effect of the tariff, in part because goods not produced inPortugal tend to bear low tariffs, and in part because goods with high tariffprotection are imported in small quantities.

2.15 Before the Revolution, tariff protection was generally granted toindustrialists on a tailor-made ad hoc basis, with little regard to the over-all pattern of effective protection that emerged. The results may be seenin the final column of Table 1: effective protection varies widely, from over200% in milk products, meat and conserves, synthetic fibers, other food prod-ucts and beverages to below zero for edible oils, inedible oils and pesticides,animal feed and mining (metallic). It should be emphasized that these effec-tive protection figures are built up on a number of simplified assumptions.For example, in the absence of hard data, it had to be assumed that goodsexempted from tariffs are also exempted from the surcharges. Equally impor-tant, the effective protection figures make use of the 1970 input-output table;but the pattern of wgages (and hence percent domestic value added) has alteredsignificantly since then.

2.16 Nevertheless, even if only the nominal tariff and surcharge figuresare used (Table II-1, columns 1-3), the essential arbitrariness of the currenttariff structure may be seen. For example, the average tariff rate on goodsin which Portugal has a comparative advantage varies from relatively low (non-electrical machinery: 9% or 27% including surcharge) to high (glass and glassproducts: 32% or 63% including surcharges). Similarly, there exist a numberof cases of raw materials and semi-finished goods bearing higher tariffs thanthe final product in which they are used. One of the most striking examplesconcerns the clothing industry: imports of "textiles used in producing cloth-ing" pay tarirfs of 30% (sub-sector not shown in Table II-1), which is greaterthan the protection for finished garments (24%).

2.17 The protection data based on the 1974 tariff (Table II-la) calcu-lated with the same method as those for 1970 show a number of changes. The(unweighted) average nominal tariff fell from 22% in 1970 to 9.6% in 1974.Reductions in nominal tariffs and nominal protection including the surclarge,took place in such items as non-electrical and electrical machinery, leatherand products, garments; but no reduction took place in footwear. Iitcludingthe 1977 surcharge (column 3) the (unweighted) average fell from 44.9% (TableII-1) to 28% (Table II-la). The calculation of effective protection (column4) is based on the same assumptions as the earlier data and does not incor-porate price comparisons. It shows that there continues to be a considerablevariation. For 1974 there is a larger number of items with negative effec-tive protection (e.g. mining-metallic, edible and inedible oils, animal feed,forestry, livestock, pulp and other chemical products). Certain categoriesof special interest for export development also show a reduction in effec-tive protection, as for example garments (65% in 1970 to 21% in 1974), non-electrical machinery (22% to 11%) and electrical machinery (71% to 47%).

- 14 -

2.18 The unevenness and arbitrariness of the tariff structure is accen-

tuated further by the existence of differential tariff rates according to

the area of origin of the merchandise. Thus in 1970 goods originating in

the colonies and EFTA countries paid significantly lower tariffs than those

from other sources (see Table II-2). Portugal's increasing ties with the EEC

will further increase this source of variation.

Table II-2: NOMINAL PROTECTION FROM TARIFFS BY SOURCE

IMPORTS, 1970 (NOT INCLUDING SURCHARGES)

Theoretical tariff Tariff rate in practice,

rate, before exemptions after exemptions

Source of Imports (percent)- (percent)/

Overseas colonies 0.0 0.0

Mini-EFTA (Sweden,Austria, Switzerland,Finland) 7.7 6.5

"Adherents" (U.K.,Denmark, Norway) 13.6 10.8

EEC (thie original six) 18.8 13.1

Spain 17.5 15.1

Ireland 15.6 15.4

Other GATT 16.o 12.0

Other countries 1.4-17.4 1.2-15.9

TOTAL 12.9 9.7

/a Based on published tariff rates

/b Calculated as: customs duty collections as percent of value of imports

Source: Unpublished data, GEBEI, Ministry of Industry.

C. Bias Towards Import Substitution

2.19 The use of tariffs and other import restricting instruments without

complementary export subsidies has a tendency to bias new investments and

- 15 -

hence production towards import substitution rather than exporting 1/. It isimportant to minimize the protection granted to import-substituting producers(and to reduce it gradually over time) to insure that industry does not becomecluttered up with a large number of high-cost (or high-profit) producers, ashas happened in the past in domestic appliances in many other countries, andin automobile assembly in Portugal 2/.

D. Tariff Reform

2.20 The Government is planning a revision of the tariff code to convertit from "specific" to "ad valorem" terms. Wholesale overhauls of the tariffschedule come but rarely; advantage should be taken of this opportunity toreform and systematize the entire structure. The new tariff structure shouldbe systematically designed to grant low nominal and effective rates of protec-tion, relatively equal across and within all sectors. There should not be toomuch "cascading", i.e. increasing rates of protection progressively as onegoes from capital goods and raw materials to intermediate and final goods.This would penalize the domestic intermediate and capital goods industries(e.g. metal manufacturing) and make for unduly high effective protection offinal products. At the sarte time, domestic intermediate and capital goodsproducers should not receive too much protection, otherwise users of theirproducts will be penalized. The surcharges should be excluded from the tariffstructure, and it should be emphasized that they are temporary measures only.

2.21 Portugal's increasing ties with the EEC make such a tariff reformespecially urgent at this time. The currently strong domestic demand iscausing resources to be diverted to import substitution. It is important thatthis should be efficient (not highly protected) import substitution, so thatonce the demand backlog has been fulfilled, the industries will be able to usetheir newly installed and expanded equipment to export, instead of being leftwith high costs and excess capacity.

1/ High tariff protection for import-substituting activities has attracteda number of investments by multinational corporations, as well as somefootloose industries.

2/ The way in which reducing tariff protection may be expected to stimulateexports is suggested by the following snippet of an interview which wehad with a Portuguese clothing manufacturer. This enterprise is currentlvemploying 250 persons and produces no fewer than 250 varieties of shirtsin cramped and poorly organized quarters in Lisbon. The firm is currentlycopying a shirt bought in a store in Switzerland for $21. The Lisbonall included production cost for this shirt is $6, and the quality of theproduct seems identical to the Swiss one. But the firm is not exportingthis or any other shirt because it can sell all its output comfortably inthe protected domestic market. When asked what he would do if he had toface competition from abroad, the entrepreneur answered that he would haveto specialize and start exporting to Europe.

- 16 -

E. Import Surcharges, Prior Import Deposits, and Quantitative Restrictions

2.22 These measures all have the same effect as tariffs, the main

difference between the three being that for surcharges the percentage rates

are easily seen.

Table II-3: COVERAGE OF THE SURCHARGE, IMPORT DEPOSITS AND

QUANTITATIVE RESTRICTIONS (NOTIONAL, BEFORE EXEMPTIONS)

Structure of Percent of value of imports subject to:

Imports Import Quantitative

Type (percent) Surcharges Deposits /1 Restrictions /1

Consumption goods 14 80

Intermediate goods 56 22

Capital goods 15 58

Petroleum products 16 - - -

All Industry 100 31 10 5

/1 No breakdown available.

Source: Unpublished data, Ministry of Commerce.

2.23 About 31% of all imports of industrial products are subject to the

30% surcharge, while about 2.3% of such imports are subject to the 60% sur-

charge. Over half of the goods subject to surcharge are intermediate products

(see Table II-3), many of which are inputs into export industries; and many of

these and/or other finished goods are potentially exportable. For example,

the 30% list includes important inputs into the textiles, clothing, and foot-

wear industries (e.g. yarns, fibers, woven fabrics, leather, buttons, fasten-

ers) also chemicals, pig iron, copper foil, bearings, capital goods, stoves,

boilers, tools, machine tools for working wood and cork, utensils. The 60%

list includes mostly finished "luxury goods", bult some are products which

co'ild be exported (e.g. canned fish and shellfish, flowers, some wines, travel

goods, bags, glass products, wood manufactures, clothing, motor cycles).

2.24 Import deposits apply to about 10% of all industrial imports. They

are required mostly for finished products, but again many are exportable or

are used as inputs into exports (e.g. textile fibers, clothing, footwear,

furniture, glassware, jewelry, locks, safes, domestic appliances, motorcycles).

The cost-raising effect of the import deposits is about 3.5% of the value of

the finished product. (The deposit represents 50% of the c.i.f. import value

in non-interest bearing notes for six months, while the interest forgone is

14% per annum.)

2,25 Quantitative Restrictions which cover 5% of all industrial imports,

apply mostly to "luxury goods" like coffee, floor coverings and childrens'

mechanical toys. However, the list also includes a wide range of potentially

exportable domestic electrical and electronic appliances such as washing

- 17 -

machines, stoves, refrigerators, radio and TV receivers and domestic sewingmachines 1/.

2.26 It is believed that, as of May 15, 1977, no licenses had yet beengranted to import goods which appear on the February 28, 1977 list of productssubject to quantitative restrictions. This is apparently because of bureau-cratic problems and delays involved in administering the system, and alsobecause of the discovery that some parts and pieces for machinery had uninten-tionally appeared on the list of goods subject to quantitative restrictions.

2.27 As is the case with tariffs, surcharges, prior deposits, and quanti-tative restrictions attract resources away from exporting and into import sub-stitution. Under Portugal's agreement with the EEC such restrictive measureswill not be permitted to remain for long, and all tariffs on industrial goodswill have to be substantially reduced by 1985. It would be useful to putindustrialists on notice that these changes are going to have to occur.

2.28 To the extent that the various types of import restrictions areintenided to limit consumption of luxury items rather then just import, theymight be converted to consumption taxes to avoid encouraging domestic produc-tion of the same goods. For imports, the consumption tax could be collectedat the point of entry into Portugal.

F. Drawback

2.29 The drawback system, to the extent that it is in fact used, servesto remove one of the distortions - high costs of raw materials and intermediateinputs - introduced by the, use of tariffs and other import restrictions withoutcompensating export subsidies. However, the drawback itself does nothing tooffset the second tariff - induced distortion - the fact that protected linesof production become more attractive; nor does it compensate for the cost -disadvantage of Portuguese manufacturers vis-a-vis competitors.

2.30 The drawback system as currently operated suffers from a number ofdefects. Judging from the comments of some plant managers, the drawback pro-cedure tends to be rather cumbersome in practice, involving excessive datarequirements, discretionary decision-making and long delays, and hence is notalways used 2/. Even drawback users often have to pay the customs duty in

1/ When originating in the EEC and EFTA imports of non-liberalized industrialprodtucts are free of quantitative restrictions, except for certain pro-tected products such as steel and automobiles.

2/ Decree Law No. 75-L/77 of February 28, 1977 goes part of the way to solvethis problem by increasing the length of time during which a drawback canbe claimed, but much of the red tape remains. A series of detailed sug-gestions on simplifying custom procedures, were made by a working groupof 27 firms in Northern Portugal. (Braga, Report of Working Group ofIndustries in the North, February 1977).

- 18 -

advance, and the duty is sometimes returned only after 12-24 months instead ofthe 6 laid down in the law.

2.31 Furthermore, the drawback system as currently operated discriminatesagainst small firms and in favor of large ones. Small firms do not alwayshave the detailed cost informLation required by the drawback administration,and their managers cannot always afford to spend the time required to negotiateand shepherd the drawback application through the various official channels.

2.32 The drawback as currently operated also discriminates in favor of in-tegrated and against horizontally specialized enterprises. Thus an integratedspinning-weaving-garment-making firm which exports its final products can claimthe drawback on raw materials or intermediate inputs imported at any stage ofthe production process; whereas an otherwise identical spinning and weavingfirm which sells its output to an otherwise identical garment manufacturer (whoexports his final product) cannot claim the drawback 1/. A possible solutionto this problem which has been used successfully in other countries (e.g.Israel) is to allow the drawback for indirect exports too. For example, a firmmanufacturing metal cans which are sold to food processing plants and used intheir exports would be eligible for drawback benefits.

2.33 The OECD apparently currently permits Portugal to apply a drawbacksystem - permission was initially granted for a year and has since beenrenewed. The drawback is permitted under the GATT. But the EEC and similarlyEFTA, is prepared to accept such a system only if it is operated in a "bonafide" manner. In practice this means that it is acceptable if (a) the rawmaterials and intermediate inputs exempted from duty come from EEC countries;or (b) if they come from other countries (especially including Japan) domesticPortuguese value added must be "relatively high". Hence, beyond certain limits(depending on the commodity), duty-free importation of components from coun-tries other than those in EEC (EFTA) for use in exports to EEC (EFTA) countriesis generally not permitted.

2.34 Drawback schemes may encourage the use of imported inputs in placeof domestically produced items. In Portugal this is avoided by the ruling thatthe inputs must be bought in Portugal if local supplies "of satisfactory priceand quality" are available 2/. But this ruling, in turn, introduces problems.Government bureaucrats are not well equipped to judge a producer's claim thatthis or that raw material or intermediate product is not exactly what it needsto be able to export. And the addition of an element of judgment makes theprocess of applying for drawbacks slow and cumbersome. It would be preferableto raise the exchange rate, lower tariffs (which would be that much lessneeded) and grant to exporters automatic drawbacks of the by-now low tariffs.

1/ This discrimination is especially serious now that the 30% surcharge isin force on many textile inputs.

2/ See e.g. Article 17 of Decree Law No. 288/76 on Export DevelopmentContracts.

- 19 -

This would minimize the difference in incentives to different firms created bythe variation in applicability of the drawback system, lighten the governmentsalready-too-heavy administrative burden, and speed up and simplify the wholeprocedure, thus increasing the likelihood that it would be used.

G. Credit Subsidies

2.35 The interest rate structure in Portugal fixed by the Government hasbeen at a level below the rate of inflation over the past five years or more.In 1977 inflation is projected at approximately 30%, but hopefully it willsubside to about 20% in 1978. The highest interest rate currently chargedfor a short-term loan is 16.5%, while for a term loan it is about 18.5%.Thus, during 1977, borrowers were paying zero interest and, in addition, werereceiving a subsidy on capital of at least 12%. If a real positive interestrate of 5% is used as the point of comparison, (that is, a 35% nominal ratewhen, inflation is 30%), then the actual subsidy is at least 17%.

2.36 In addition, the Government has introduced interest rate rebatesrunning from 2 to 9%, for one to four years, to be available on the following:export credit, investment credit for agriculture, forestry, livestock, fish-eries, tourism, mining and manufacturing; and credit for the restructuirng ofviable enterprises currently in difficulty. 1/ This raises the actual subsidyanother step, to the 19 to 26% range. Furthermore, it is necessary to dis-count to present value the subsidy on term loans (negative interest rate plusrebate); this comes to 3 to 5%. Total actual subsidy is now 22 to 31% on bor-rowings, assuming credit is evenly split between short and long-term.

2.37 If the inflation subsidy is omitted, the net incentive is 5 to 14%.The amount of this subsidy has to be adjusted in accordance with the incre-mental capital-output ratio (ICOR). If the ICOR is 0.5, the interest ratesubsidy (inflation adjustment excluded) becomes 2.5 to 7%. If, as in heavyindustry, the ICOR is 2.0, then the value of the subsidy quadruples to10 to 28% 2/.

1/ In the range from 2 to 9%, there is a cost per jobs cut-off point ofEsc. 750,000 ($18,750). This is quite high in the Portuguese contextand ways to circumvent it are being found by loan applicants.

2/ Initial investment = 100; annual production = 200; interest savings = 21to 27% p.a. Effective output subsidy - (21 to 27%)/200 = 10.5 to 13.5%.Estimated direct capital-output ratios in industry at about Portugal'slevel of development vary from 0.5 (printing and furniture) to 1.9(fertilizer). Total (direct and indirect) capital-output ratios vary from1.0 (shipbuilding) to 3.4 (fertilizer). Total capital-output ratios forthe export industries are 1.29 (Lextiles and clothing), 1.41 (furniture),1.26 (shipbuilding), 1.35 (machinery), 1.63 (wood and cork), 1.67 (metalproducts), 1.83 (food processing), and 1.85 (paper). Joseph J. Stern,"The Employment Impact of Industrial Investment", World Bank Staff WorkingPaper No. 255.

- 20 -

2.38 A credit subsidy of the magnitude indicated above provides a strongincentive for capital-intensive labor-saving investment, even though thisis contrary to Portuguiese policy to encourage employment creation.

2.39 Exporters can get an interest rate subsidy of 5% to finance sales orproduction for up to two years. This is not very significant in view of theoverall interest rate structure and the relatively short period for which thesubsidy applies. The discrimination of the interest rate regime in favor ofCxports is rather negligible, and the main effect of the set of implicit andexplicit credit subsidies is to lower the cost of capital quite substantiallyacross the board, regardless of whether manufacture is export oriented or not.

H. Exemption of Indirect Taxes on Inputs

2.40 As in most countries, Portuguese exporters are exempted from payingindirect taxes on inputs used in production. In the absence of detailedinformation, the mission assumed that this exemption guarantees equal treat-ment with foreign firms rather than granting any net advantage to exporters.It may of course, put export firms in a better position vis-a-vis importsubstitution firms.

I. Income Taxes

2.41 The current Export Development Contract law permits discretionaryreduction or temporary abolition of corporate income tax payments (Article 13).This may be challenged by Portugal's trading partners in Europe - GATT rulesare ambiguous on the point 1/. More likely to be acceptable are the existingprovisions which relate to accelerated depreciation allowances, which in theend have a similar effect (Articles 13, 15). Again, these should be madeautomatic rather than discretionary. Further, the industrial corporation taxcan' be reduced by an amount up to 5% of export value (see para. 4.06 (g)).

2.42 Depending on exemptions, loopholes, etc., the rate of corporateincome tax is approximately 20-30% on income. If income taxes are waived,firms earning 2% on sales (assuming all sales are value added), would receivebenefits equivalent to an output subsidy of 0.4 to 0.6%; for a firm earning

1/ Ireland regarded by the EEC as a less developed region, has been allowedto retain such tax exemptions. But the U.S. may impose countervailingduties.

- 21 -

as much as 15% on sales the output subsidy would be 3 to 4.5%. 1/ If valueadded is 50% sales, the percentage (subsidies) would be doubled.

J. Export Development Fund (Fundo de Fomento de Exportacao - FFE) i

2.43 The FFE provides a number of useful services to exporters describedin Annex III-5. It has 130 representatives at various strategic locationsabroad, organizes participation in trade fairs, finances missions and trips byprospective buyers and sellers, hires and finances consultants to do marketresearch, and is in charge of signing and implementing the Export DevelopmentContracts discussed in Annex III-5.

2.44 Although these are useful services it has not been attempted to cal-culate what "percentage incentive" they represent for exporting firms. TheFFE has been useful in opening up new markets, and in the future it is expectedto play a key role in providing marketing and other export development assis-tance (paragraph 2.52).

K. Summary of the Effects of Trade Incentives

2.45 The effects of the various trade incentive measures on productionfor export on the one hand and production of import-substitutes on the otherare summarized in Table II-4. The table does not include credit subsidieswhich apply to both export and import substitution industries. In the absenceof the necessary detailed calculations the Table does not present averages butinstead ranges of price incentives.

2.46 Two conclusions may be drawn from the table:

(a) Export firms receive subsidies well below those received byfirms producing import substitutes. The former receive asubsidy averaging 2% (or 0.5% - 5%) of output value (andwhen the drawback does not operate, an additional penalty of10% as against a protection of 13 - 80% for import substitu-tion firms. According to mission calculations for individualfirms, the calculations showing the incentive effect as a per-centage of value added would show a similar bias in favor ofimport substitution and against exports. Thus, the observa-tions made about the import substitution bias in paragraph2.19 above is true generally for the incentive system as a

1/ The top corporations in the U.S. earned an average of 4.6% net on sales(after tax) in 1976. (Fortune, in Time, May 16, 1977, p. 52). The taxadvantages are spelled out in detail in the new draft export incentivebill. (Law No. 42177 of June 18, 1977 specifies that the industrialcorporative tax liability can be reduced by up to 5% of export value.)The law also permits acceleration of depreciation and other tax benefitswhich the Mission did not discuss with the authorities.

2/ Recently renamed "Portuguese Institute for Export Probiotion".

- 22 -

whole. Between 1970 and 1974 there was a reduction in tarifflevels (cf. para4 2.17), but since then several instrumentswere added which in effect intensified the imports substitutionDias.

(b) Moreover, the subsidy element received by the export manu-facturer [averaging 2%, and 10 percentage points less whenthe drawback is not operating] is insufficient to overcomethe deterioration since 1973 in competitive advantage (causedby changes in wages, productivity and exchange rates) vis-a-vis producers in Portugal's OECD trade partners. As discussedin paragraph 2.09 this deterioration was at least 10% on aver-age and substantially more for certain industries.

2.47 It is true that in the short-run there may be quite a deal of scopefor import substitution, especially because of the effects of the post-1974income redistribution and the arrival of the retornados. However, in themedium to long term the small size of the Portuguese market and the tariffreductions required by Portugal's agreement with the EEC limit the amount ofimport substitution that may profitably be done. Therefore, it is importantto ensure that the current catch-up phase of import substitution is efficient,so that once it is spent the capacity built up will be useable for export.

Table II-4: SUMMARY OF THE PORTUGUESE FOREIGN TRADE INCENTIVE SYSTEM

Incentive for:Measure Exports Import Substitutes

--------- (% of value of output)-------

/a1. Tariffs Average of +10%

or more with widevariation

/a2a. Surcharges +30% for 31% of

imported goods;+60% for 2.3% ofimported goods /b

/a2b. Prior import deposits +3.5% for 10% of

imported goods /b

2c. Quantitative import Strongly positiverestrictions for 5% of imported

goods /b

3. Drawback /a Net effect zero(it simply removesdisincentives fromtariffs, surcharges,etc. on imported inputs)

- 23-

Incentive for:Measure Exports Import Substitutes

--------- (% of value of output)-------

4. Exemption of indirecttaxes on inputs (Simply equalizes tax

treatment with thatof foreign firms)

5. Income taxes +0.5% to +4% increasingwith the rate of profit

6. Export Development Small positiveFund

TOTAL 0.5% to 5% Varies widely from13% to 80% andhigher (see TableII-la, column 3)

CONCLUSION: There is a clear bias in favor of import substitution and againstexports.

/a See drawback below. When the drawback does not operate (e.g. for smallfirms), tariffs and/or surcharges and/or prior deposits have to be paid,and the subsidy to exporters is lowered correspondingly. E.g. a 10%penalty results when imported inputs are subject to the 30% surcharge andaccount for a third of total cost. The penalty will be even greater than10% if there are tariffs and prior import deposits to be paid.

/b The positive incentive is lower to the extent that exemptions are granted.;

L. Recommendations

2.48 The steps to be taken fall into three categories: (a) have a generalreduction in the cost structure of Portuguese industries to overcome the deter-ioration in competitive advantage since 1973 and lay the basis for accelerationof exports of manufactures; (D) remove the present import substitution bias ofthe incentive system; and (c) improve the effectiveness or remaining elementsof the system, e.g. the tariff, the drawback and the operations of the ExportDevelopment Fund. Once the measures have been taken and a program of actionhas been agreed, it is essential that the system will be maintained in a stablemanner so as to give full opportunity to export manufacturers to make thenecessary investments, develop products and enter new markets.

2.49 Improvement in cost-competitiveness. The mission stresses the needfor across-the-board measures, in particular a general reduction in relativecost which has an even effect on all industries. Portugal is faced with asituation of crucial structural adjustment in which it is extremely difficultto determine a priori precisely which export industries and products will do

- 24 -

well in foreign markets and which existing production lines must be adopted tonew conditions and markets. Estimates for the necessary improvement in cost-competitiveness of export industries range between 10 and 20% and higher (para

2.09). These estimates however, probably are less than the over-all cost re-ductions required when account is taken of the adjustments which industry mustmake if it is to contribute sufficiently to Portugal's balance of payments. Asa result of structural changes affecting the balance of payments, manufacturedexports will have to make a substantially larger contribution to Portugal'sforeign exchange earnings than they did before 1973. Thus, even if on a 1973basis Portuguese export industry would have been fully cost-competitive inFebruary 1977, further cost reductions would have been necessary if exportgrowth is to speed up sufficiently. The manner and timing of the necessaryacross-the-board cost reducing measures will very much depend on the progresstoward achieving domestic price and wage stability and improvements in produc-tivity. The measures called for will have to be part of a broad program ofdomestic price-cost stabilization, and improvements in industrial management,efficiency and productivity discussed in Chapter III.

2.50 A sufficient general reduction in relative cost-levels will makepossible removal of the import substitution bias of the present restrictivesystem. This will require dismantling - or setting up a timetable for theelimination, of the system of surcharges, prior deposits and quantitativerestrictions, as well as a reduction in tariffs. This is necessary in orderto avoid attracting resources away from exports into high cost import substi-tution industries which will be a burden once Porgual's EEC agreement forcesimport restrictions to be lowered.

2.51 The Mission also recommends that the Government consider additionaldirect export subsidies. P6rtugal already has various means of assistingexport industries and the Mission is recommending improvements in them, espe-cially in the operations of the Export Development Fund. Failing adequategeneral measures to reduce relative costs (and accompanying reduction in importsurcharges and tariffs) there would be a case for subsidies to overcome thedeterioration in competitive position and remove the import substitutica biasof the present incentive system. The subsidies should preferably be based ondomestic value added, be simple to administer and be confined to a transitionalperiod pending more basic measures and a strengthening of manufactured exports.Portugal would need approval of the EEC and EFTA for such subsidies, presumablyfor a limited period.

2.52 Further steps are:

(i) Take advantage of the present unlikely-to-be-repeatedopportunity to rationalize the entire tariff structureduring its conversion from "specific" to "ad valorem"terms. In general protection should be relatively lowand tend to have similar levels of effective rates acrossand within all sectors.

(ii) Simplify and speed up procedures involved in the draw-back.

- 25 -

(iii) Extend the drawback to apply to indirect exports (e.g.exempt from duty yarn used to weave cloth whtich is soldto a garment-maker who exports his products).

2.53 A special role is to be played by the Export Development Fund:

(a) Rationalize the operations of the Export Development Fund, andespecially attempt to increase its degree of contact withPortuguese industry. The Fund would make sure that exportfirms receive all the benefits available, and follow-up on thevaricus phases of development of new export projects.

(b) Have the Export Development Fund issue the firms which exportmore than a minimum percentage of output (say 30%) with theequivalent of an Exporters' Card - this may be the revampedExport Development Contract - which would automatically andquickly entitle him to exporters' privileges - drawback taxreductions, etc.

(c) Simplify and speed up the procedures for signing of theExport Development Contract as suggested in Annex III-5.

2.54 The effects of the incentive system should be kept under review.Once economic recovery gets under way the entire system might profitably bestudied with a view to rationalizing it further.

- 26 -

CHAPTER III

REVIEW OF MANUFACTURING INDUSTRIES

A. General

3.01 Portugal's comparative advantage in manufactured exports rests onits natural resources, its labor and engineering skills and its location.