Embed Size (px)

Citation preview

Managing safe and efficient coal mining and processing operations in the Gloucester Basin

September 2008

ASX: GCL

September 2008Rob LordAustralian Coal Summit 2008

September 2008Australian Coal Summit 2008

Background on GCL

Operations overview

FY 2008 performance

Growth and development

Future outlook

Contents

2

DisclaimerStatements contained in this material, particularly those regarding the possible or assumed future performance, costs, dividends, returns, production levels or rates, prices, reserves, potential growth of Gloucester Coal Limited, industry growth or other trend projections and any estimated company earnings are or may be forward looking statements. Such statements relate to future events and expectations and as such involve known and unknown risks and uncertainties. Actual results, actions and developments may differ materially from those expressed or implied by these forward looking statements depending on a variety of factors.

September 2008Australian Coal Summit 2008

Gloucester Coal has been a publicly listed mining company since 1985, with the modern era for GCL starting when RJB sold its controlling stake in 2004

3

2008 Market capitalisation reaches A$1 billion

1999

First coal railed from Stratford

Company enters USD hedging transaction with NatwestRJB Mining (UK Coal) invests in Company

1996

2007 Xstrata attempts to buy the Company

Roseville Pit opened

2004 RJB sells its 97% stake in the Company, with an implied market capitalisation of A$54m

1995

1985 ASX listing as Centenary International Mining with exploration interests in a range of minerals excluding coal

Troubled hedging results in RJB takeover of the Company

1997

2003 Duralie and Bowen Road North mines commissioned

2006 Clareval seam confirmed at East Duralie

September 2008Australian Coal Summit 2008

‐

2

4

6

8

10

12

14

16

Jan‐03

Jul‐0

3

Dec

‐03

Jun‐04

Dec

‐04

Jun‐05

Dec

‐05

Jun‐06

Dec

‐06

Jun‐07

Dec

‐07

Jun‐08

GCL

sto

ck p

rice

(A$)

GCL ASX2004

April 2004RJB Australia sells 97% stake - allows liquidity

Since 2004 GCL has outperformed the ASX 200, initially on the strength of its operations and more recently, on the back of rising coal prices

September 2008Australian Coal Summit 2008

Listed independent NSW based coal producerc.1.8Mtpa of production from two 100% owned open cut mines:

• Stratford• Duralie

Product is semi-hard and thermal coal100% of coal is exported through Newcastle to Asian marketsMarket cap circa A$959 million (29/8/08)Coal is noted for its high fluidityFY08 net profit of A$23.4 million

GCL’s operations are in the Gloucester Basin, north east of the Hunter Valley and about three hours north of Sydney

5

Substantial shareholdersNoble Group 21.7%AMCI Investments 9.9%Itochu Minerals & Energy 5.1%

September 2008Australian Coal Summit 2008

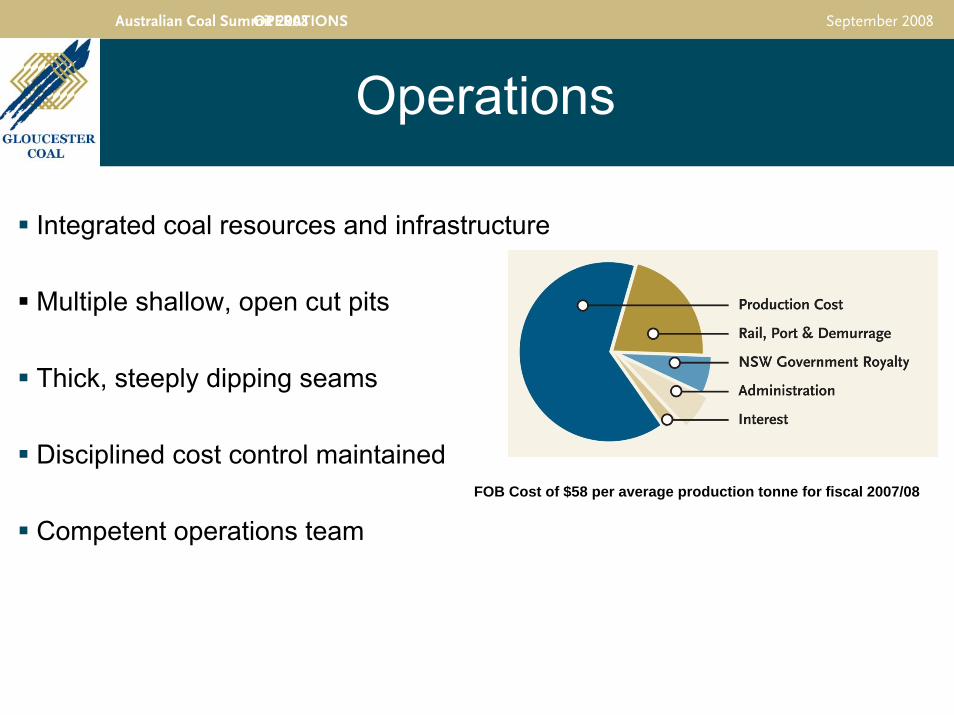

Operations

Integrated coal resources and infrastructure

Multiple shallow, open cut pits

Thick, steeply dipping seams

Disciplined cost control maintained

Competent operations team

OPERATIONS

FOB Cost of $58 per average production tonne for fiscal 2007/08

September 2008Australian Coal Summit 2008

StratfordOperation comprise of three open cut mines:− Bowens Road North: lower sulphur, low volatiles

thermal coal with very low strip ratio− Co-Disposal: high ash, lower sulphur thermal coal− Roseville: coking coal with low ash and high fluidity

Location of coal handling and preparation plantOperated by Ditchfield contracting

DuralieOperations comprise of the Weismantal Seam open cut, producing:− Top section: high energy, moderate sulphur thermal

coal− Bottom section: low ash, high fluidity coking

Shuttle train transports ROM coal to Stratford (20kms north) on main North Coast lineOperated by Leighton Mining 7

Stratford and Duralie are linked by the North Coast rail line, which reduces operating costs

September 2008Australian Coal Summit 2008

Despite relative complexity of geology at Duralie and Stratford, GCL’s operations are comparatively efficient

8

Raw production per employees FY07 NSW open cut mines

Source: 2008 NSW Coal Industry Profile, NSW Dept of Primary Industries

* Excludes CHPP staff

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000U

lan

Wes

tsid

eN

aram

aS

tratf

ord

Lidd

elW

ambo

Ben

galla

Dur

alie

Cul

len

Val

ley

Baa

l Bon

eW

hite

have

nC

umno

ck S

outh

Mou

nt A

rthur

Ope

ratio

nsTa

rraw

onga

Wer

ris C

reek

Bul

gaR

ix's

Cre

ekD

onal

dson

Mou

nt O

wen

Mou

nt T

horle

y …P

ine

dale

Blo

omfie

ldC

ambe

rwel

lD

rayt

onH

unte

r V

alle

y O

pera

tions

Ash

ton

Cha

rbon

Mus

wel

lbro

okLa

mbe

rt's

Gul

ly

Prod

uctio

n pe

r em

ploy

ee (t

onne

s)*

ROM

Saleable

September 2008Australian Coal Summit 2008

GCL’s safety performance has been strong. LTIFR is significantly under the industry average

9

Days since

last LTILTIFR1 MTIFR1

Gloucester Coal

- Mining operations 1,122 0.0 0.0

- CHPP 547 0.0 14.5

- Combined -- 0.0 11.1

Contractors

- Ditchfield (Stratford) 155 10.4 0.0

- Leighton (Duralie) 1,081 0.0 5.3

- Combined -- 7.0 3.5

GCL & contractors -- 2.7 8.0

Industry average2 -- 8.9 --

GCL statistics

1. Rolling 12 months2. Five year average for NSW open cut mines to June 30, 2007

Source: 2008 NSW Coal Industry Profile, NSW DPI

0

20

40

60

80

100

120

140

160

0

1

2

3

4

5

6

7

8

9

1990

-91

1991

-92

1992

-93

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

LTIF

R

Fata

litie

s

Fatalities - UG Fatalities - OC LTIFR - UG

LTIFR - OC LTIFR - total

NSW coal mine statistics

September 2008Australian Coal Summit 2008

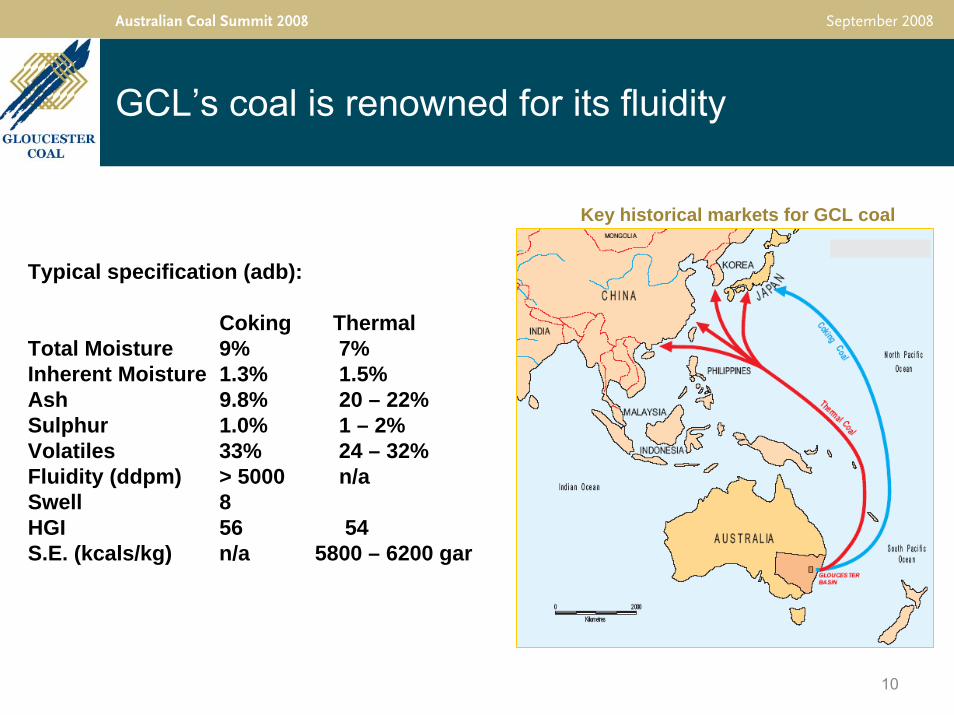

GCL’s coal is renowned for its fluidity

10

Key historical markets for GCL coal

Typical specification (adb):

Coking ThermalTotal Moisture 9% 7%Inherent Moisture 1.3% 1.5%Ash 9.8% 20 – 22%Sulphur 1.0% 1 – 2%Volatiles 33% 24 – 32%Fluidity (ddpm) > 5000 n/aSwell 8HGI 56 54S.E. (kcals/kg) n/a 5800 – 6200 gar

September 2008Australian Coal Summit 2008

Record revenue of $159.6 million - higher sales margins

NPAT of $23.4 million, 30% higher than previous year. EBITDA of $41.9 million.

Strong cash-flows facilitated loan repayments of $15.0 million. Net debt at $4.1 million.

Negotiated record coking coal pricing – up 270%.

Result impacted by stronger AUD and industry cost pressures

Coal chain infrastructure constraints offset - by increased coking coal sales.

2008 consolidated prior year’s financial performances and has laid a foundation for the Company’s future growth

11

September 2008Australian Coal Summit 2008

A continued focus on cost control and operations optimisation is reflected in the FY08 result

12

Year Ended 30 June 08A$ Millions

Year Ended 30 June 07A$ Millions

Revenue $M 159.6 151.9

EBITDA $M 41.9 34.2

EBITDA margin % 26% 23%

Net Profit After Tax $M 23.4 18.0

Earnings per Share 28.8 cents 23.0 cents

Coal Sales Mt 1.903 2.166

Cash & Cash Equivalents $M 5.6 16.5

Current Ratio 2.5 0.8

Interest Bearing Loans $M 9.7 24.8

Net Debt $M 4.1 8.3

Net Assets $M 101.7 73.2

September 2008Australian Coal Summit 2008

Positive trendsImproved pricing − JFY 2008/09 coking coal contract price

to rise 270% on 2007/08 price− Spot thermal prices continue to firm at

record levels− Not greater than 13% of sales volume for

the coming 08/09 year is at old contract prices

Improving mix of coking coalImproving quality of thermal coalIncreased capacityOngoing resource and reserve expansion

Historical constraintsInfrastructure access limiting volumesExchange rate of Aussie dollar vs US dollar

A number of trends point towards a positive future for GCL

13

-

20

40

60

80

100

120

140

160

180

FY05 FY06 FY7 FY08

Dollars (millions)

Revenue

EBITDA

NPAT

Note: FY05 comparative restated to 12 month period

September 2008Australian Coal Summit 2008

GCL is increasingly focused on developing the long term future for the Company through exploration and development both inside the Gloucester Basin and beyond

14

2 mines that are:Low costLow riskSafe

Ongoing additional finds in the Gloucester Basin extending mine life and improving coal quality

Clareval seamDuralie underground (longer term potential)

Actively drilling within the Gloucester Basin to identify additional satellite deposits to leverage existing infrastructure

Within Gloucester Basin Outside Gloucester Basin

New exploration tenements

Continuing to review partnerships, JV’s and acquisition opportunities

September 2008Australian Coal Summit 2008

Reserves (Mt)Proved & probable 28.5

Resources (Mt)Open cut 105Underground 100

JORC compliant reserves were increased by 30% in July and resources by 10%

More drilling is underway and further upgrades expected later in 2008

Reserves & resources

15

September 2008Australian Coal Summit 2008

Exploration

A priority > $2m pa next few years

Focus on potential for Clareval and Weismantel seams between Stratford and Duralie – East side of license area.

Confirmation in April 08 that thick Clareval is present at Stratford near coal processing plant and in Grant / Chainey area

Further exploration drilling is continuing to delineate the Clareval seam east of the Stratford coal processing plant

Over the next five months about 40 drill holes are planned to provide data that will enable JORC resources to be estimated over 4km of strike length of the seam subcrop and down to 100 meters of cover

September 2008Australian Coal Summit 2008

Significantly better product ash and sulfur specification for current and proposed pits - confirmed by drilling. Coking to thermal product split moving in favour of coking coal with introduction of Clareval into blends. Ability to produce better coking and thermal product specification than 2003 –2008 periodPotential to blend back thermal coal into coking cargosSignificant value attributed to better coal quality for next 10 years.

The properties of the coal found in the Clareval and other satellite seams is set to improve the quality of GCL’s product coal

17

September 2008Australian Coal Summit 2008

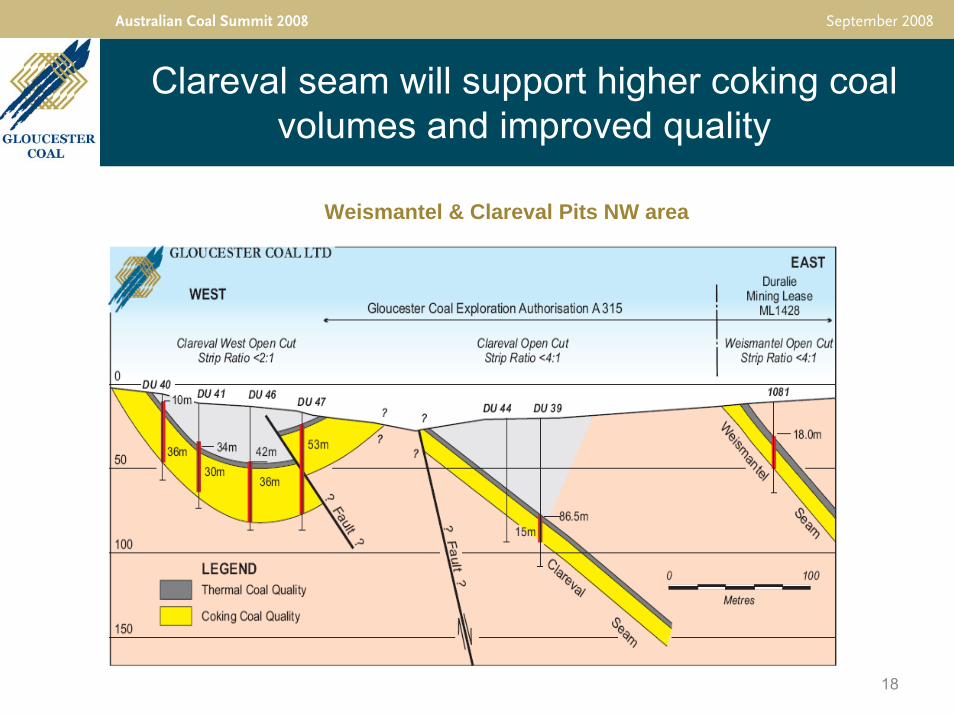

Weismantel & Clareval Pits NW area

Clareval seam will support higher coking coal volumes and improved quality

18

September 2008Australian Coal Summit 2008

Production capacity is being expanded through upgrades to the CHPP, stockpile and materials handling facilitiesUpgraded ROM processing capacity will be 4.0-4.5MtpaUpgraded product coal capacity will be:− 1.1 to 1.4 Mtpa coking coal − 1.4 to 1.7 Mtpa thermal/blend coal− 2.8 Mtpa total

Commissioning planned for 2009/10Capital Expenditure:− $18 M Stockpile/materials handling − $12 M CHPP upgrade

Note:

− (1) $20 M provides immediate benefit at current production rates and port allocation

− (2) Latest estimates suggest overall completion costs could increase by ~10%

Capacity at existing operations is being increased to coincide with the PWCS expansion…

19

September 2008Australian Coal Summit 2008

Stratford exploration and development4 key areas for development− Avon north− Roseville west− Bowen’s Road south− Avon South

Currently in 3A planning stageAbove would extend life of Stratford mine to at least 2017Recent Clareval discovery will extend this further

Stratford – towards 2020

20

September 2008Australian Coal Summit 2008

Weismantel seam ~1.8mt p.aHigh energy, moderate sulphurthermal (top section of seam)Low ash, high fluidity coking (bottom section)Strip ratio <4:1

Exploration and developmentExtend Weismantel seam to the north westOpen the Clareval seamPotential for underground development

Duralie – towards 2020

21

OPERATIONS

September 2008Australian Coal Summit 2008

Exploration, land acquisition and planning activity to secure and extend Gloucester Basin mining activityValue adding to our sales mix though continued focus on coking coal production and blending synergiesMaximizing available coal chain capacityUpgrading our production capability – product handling, stockpiling and processing capabilityInvestigating and securing growth opportunities outside Gloucester basin – including mergers / acquisitions / strategic alliances/JV’sHaving the right people, skills and tools to achieve our goalsContainment of costs in buoyant resources environment

FY09 is set to be a year for growth – our focus

22

September 2008Australian Coal Summit 2008

Company: Gloucester CoalASX code: GCLContacts:

Rob Lord – Chief Executive OfficerPeter Scott – Chief Financial Officer

Phone: +61 (0)2 9413 2028Website: www.gloucestercoal.com.auEmail: [email protected]

Media: Third PersonTelephone: +61 (0)403 527 755

Contacts

23