Embed Size (px)

Citation preview

MANAGERIAL ACCOUNTING TOOLS USED IN PUBLIC

INSTITUTIONS IN THE ROMANIAN HEALTH SYSTEM

PhD Thesis Abstract

Scientific adviser,

PhD Professor GEORGESCU Iuliana Eugenia

PhD Candidate,

GHEONEA Victoria

IAŞI

- 2012 -

1

Content of PhD Thesis Abstract

Key words........................................................................................................................................1

Structure of PhD Thesis...................................................................................................................2

Motivation and importance of research ...........................................................................................4

Synthetic presentation of thesis chapters.........................................................................................5

Conclusions, contributions and future research directions............................................................17

Selected references ........................................................................................................................23

Key words

Managerial accounting, health management, public sector, hospital services, health

system, cost, calculation methods, budget, Balanced Scorecard, Diagnosis Related Groups,

performance indicators

2

Structure of PhD Thesis

INTRODUCTION

Motivation and importance of research

The purpose and objectives of the research

State of knowledge in the use of management accounting tools in public sector

Research methodology

Chapter I. MANAGERIAL ACCOUNTING, A NECESSITY FOR THE SUCCESS OF ORGANIZATION

1.1. The relationship between management accounting and financial accounting

1.2. Objectives of management accounting and its role in management of organizations

1.3. Managerial accounting, information resource for management of health institutions

Chapter II. PARTICULARITIES OF HEALTH SYSTEM IN ROMANIA

2.1. Analysis of the Romanian healthcare system

2.1.1. Romanian health system analysis in European and global context

2.1.2. SWOT analysis of the health services in Romania

2.2. Financial management in the healthcare system

2.3. Analysis of performance indicators of public hospital management

2.4. Financing of health services

2.4.1. Models of health insurance financing used internationally

2.4.1.1. The British system - Beveridge

2.4.1.2. German system - Bismarck

2.4.1.3. Private insurance-based system used in the U.S.

2.4.2. Financing of hospital services in Romania

Chapter III. COSTS IN DECISION MAKING IN THE PUBLIC HEALTH SECTOR

3.1. Strategic Cost Management

3.2. The cost of healthcare quality

3.3. Models of cost-based decisions in the public sector

3.3.1. General considerations on cost-based decisions

3.3.2. "Produce or buy" decision. Outsourcing costs

3.3.3. Decision under limited resources. Opportunity cost

3.4. Methods of cost calculation of hospital services

3.4.1. Features of the calculation cost in terms of classical methods

3.4.2. Activity-based cost method

3.4.3. Comparative study on cost calculation in a public hospital: global method and activity based costing method

3

Chapter IV. MANAGEMENT TOOLS OF PERFORMANCE IN ROMANIAN HEALTH INSTITUTIONS

4.1. Planning and budgetary management

4.1.1. The budget, a tool for assessing the performance of public sector

4.1.1.1. Budgeting methods in the public sector

4.1.1.2. Programming the public budget

4.1.2. Control through budgets

4.2. Balanced Scorecard – strategic management tool of performance in public institutions

4.2.1. General considerations on Balanced Scorecard

4.2.2. The perspectives of Balanced Scorecard

4.2.2.1. Financial perspective

4.2.2.2. Customer perspective

4.2.2.3. Internal processes perspective

4.2.2.4. Learning & Growth perspective

4.2.3. Balanced Scorecard in Romania

4.2.4. Implementation of Balanced Scorecard in a public hospital

Chapter V. EMPIRICAL STUDY ON THE COSTING IN HEALTHCARE USING DIAGNOSIS RELATED GROUPS SYSTEM

5.1. Presentation of Diagnosis Related Groups System

5.1.1. DRG-based hospital financing system

5.1.2. SWOT analysis of DRG

5.2. Diagnosis Related Groups System, specific management tool to cost estimation of hospital services

5.2.1. Case study on example of "Gheorghe Buzoianu" Targu Bujor Hospital

5.2.2. Statistical analysis of hospitalized morbidity indicators according to diagnostic groups

5.2.2.1. Factorial analysis

5.2.2.2. Analysis of "cluster"

5.2.2.3. Conclusions statistical analysis

CONCLUSIONS, CONTRIBUTIONS AND FUTURE DIRECTIONS FOR RESEARCH

REFERENCES

ANNEXES

4

Motivation and importance of research

The thesis falls into a very current context: reforming the management of health units,

respectively the answer of managers to reform expectations. In this context, our research

approach is the extent to which managers succeed by applying and implementing new methods

and modern forms of management of accounts information, to obtain improved performance

health units, and develop advantages in the competition health market. In light of current trends,

especially future trends, of development of public sector in general, and the health system in

particular, it can be said that reform radical measures are needed.

Managerial accounting is often used, but the concept still arouses the interest of

researchers and practitioners in this field, they trying to highlight its delineation of management

accounting through advanced managerial accounting tools and complex information that it can

provide (Gupta & Gunasekaran, 2005; Kaplan & Atkinson, 1998; Roslender & Hart, 2003).

Decision making has become very complex and diverse due to various situations that

may occur in the activity of any organization, and therefore management accounting is a prime

source of information for managers, assisting them in making decisions, planning and control, a

context which confirms the topicality of investigated theme.

The main motivation for choosing the theme is the fact that, both in research and in

practice, study and use of management accounting are mainly in the private sector, public sector

management accounting tools are rarely addressed. Management of an organization is based on

the decisions that were taken from a good knowledge of internal and external factors which

could impact the organization activity. Complexity of the activity in a hospital needs usefulness

of managerial accounting tools, because the accurate determination of costs and their

implications in achieving the proposed performance is a constant imperative of decision making.

Thus, the scientific approach pursued, becomes a novelty and utility at the same time, both for

public sector accountants as well as academic, scientific novelty of the thesis is determined by

the goal and objectives of the research.

Through our approach, we aim to study and deepen the implementation of management

accounting tools in the public sector, the primary aim of our research.

5

Synthetic presentation of thesis chapters

In the introduction we defined the theoretical and methodological research, presenting the

theme, motivation and importance of research purpose and research objectives, level of

knowledge in the use of public sector management accounting tools and research methodology.

The first chapter entitled "Managerial accounting, a necessity for the success of

organization" we analyzed the role and objectives of management accounting, mainly in the

public sector in order to identify the information needs of the public manager from managerial

accounting and how it becomes the main tool in decision making process of the public

institution.

Managerial accounting is the most important source of information for planning and

control of resources and decision-making accordingly. Management accounting in public

institutions of the Romanian health system aims mainly to obtain information necessary for the

health unit management to base decisions. This information relates mainly to:

� financing mechanisms;

� costs of hospital services;

� performance of public hospitals, namely their monitoring by identifying

difficulties, irregularities and possible alternatives, in assessing the efficiency

ratio allocation / consumption and the development of strategies and plans.

On health care financing, management accounting provides valuable information, which

determines the viability of the financial institution and outlines the scope of services provided

action and size, quantifying financial resources being a key determinant for the organization.

This information relates to attracting and balanced managing of funds with a good foundation of

funding. A hospital is a public institution financed wholly from own revenues based on medical

service contracts with health insurance houses. Depending on the achievements and addressing

hospital patients, it can encounter two common situations in practice:

� The hospital performed more than the contracted amount (number of patients

treated is greater than the number of cases contracted with the house health); case there is a very

high addressability and the hospital is required to treat all patients who come to hospital. The

difference is a loss because the hospital treats patients either from its own resources saved, either

by reducing the quality of care for all patients. This situation is most common in hospitals in

Romania.

� Hospital achieved less than the contracted amount and the number of patients

treated is much smaller than the number of cases contracted. In this case, the house of health

adjusted the contract value to patients treated, and the hospital does not record deficit. Appear,

6

however, shortcomings in current and future planning: operational strategy is affected, it creates

a precedent unfavorable hospital for the next few years, which will affect the amounts to be

incurred in the future and are threatened the conditions of continuity of hospital activity, i.e. it

does not can continue operation and cannot meet its obligations for the foreseeable future.

In such cases, the information provided by managerial accounting support the manager by

warning and adjustment tools (e.g., determining beneficial activities and departments

"locomotive" of the hospital - which types of patients / diagnostic with benefit).

On the costs of hospital services, managerial accounting helps management of health

institutions to substantiate fair prices and tariffs, and precise control of centers of consumption

expenditure on activities or projects, thus helping to rigorous documentation of decisions

making. Information received in this case, are extremely useful in calculating costs of hospital

services to the level of procedure, patient and diagnostic group. They determine the real costs of

hospitalization knowledge, assessing their efficiency and financial decision making informed,

and manager having thus provided both clinical data and cost data at the patient level.

Managerial accounting can answer therefore to the question "how much costs this type of patient

/ diagnosis?"

The second chapter, "Particularities of the health system in Romania", aims to identify

and describe the current state of the Romanian health system performance, establishing precisely

the areas where managerial accounting can intervene and improve healthcare processes and

activities. Thus, we obtained an overview of the Romanian health system by which we identified

its particularities in financial terms by comparison with international financing patterns of

hospital care, by presenting the advantages and disadvantages of the current system, describing

resources and performances in relation to allocated resources, and description of existing

financial model.

Romanian health budget has decreased by over 40% in the last three years. It is obvious

that the public health system in Romania is really underfunded, given occidental standards

(where over 10% of GDP allocated to health) and that our health indicators look much worse

than those of other European countries, not only European Union.

7

Figure 1 Ranking of Euro Health Consumer Index for 2012

(Source: own achievement by Euro Health Consumer Index 2012 Report)

According to the Euro Health Consumer Index for 20121, the annual comparative

research of health systems in Europe relegated Romania ranked 32 (!) with 489 points, out of 34

European countries (Figure 1). Rank points out that states in top (Netherlands, Denmark,

Iceland) begin to use information about health and choice, to involve patients in decision

making, building bottom-up process to improve performance. At the end of the standings is a

group of countries (Romania, Bulgaria, and Serbia) stuck in the old health system, hierarchized

and lacking in transparency. This difference poses a challenge to the principles of equity and

solidarity of the European Union.

Recent data centralized by the National Health Insurance House2 (NHIH) shows that after

Romania joined the EU, 45% of the total NHIH's budget reaches to hospitals (Figure 2).

Figure 2 Composition of the National Unique Health Insurance Fund budget after EU accession

(Source: own achievement data by NHIH)

1 *** Euro Health Consumer Index 2012 Report, available at http://www.healthpowerhouse.com/files/Report-EHCI-2012.pdf (accessed 16 August 2012) 2 *** The National Health Insurance House (NHIH), The National Unique Health Insurance Fund Evolution, available at http://www.cnas.ro/informatii-publice/bugetul-fnuass/evolutia-fnuass (accessed 7 March 2012)

8

In addition to underfunding, we can talk about arbitrary use of resources: allocation of

resources between different regions, between different types of health services, between different

health institutions is inefficient and inequitable. Analyzing data from the Ministry of Health3, It

can be notice the inequitable of resource allocation by counties. Thus, in Figure 3 we notice that

28 counties (67% of all counties) receive less than 2% of the budget and 9 counties (21%)

receive between 2-3%. "Favorites" ranks are occupied by 4 counties (Cluj - 6% of the budget,

Iaşi 5%, Mureş and Timişoara 4%), in the top being Bucharest with funding over 23% of the

budget.

Figure 3 Hospitals financing by counties in 2010, in % of total budget

(Source: own achievement by the Ministry of Health)

Therefore, differences between regions and counties are too large to not suspect the

presence of unfair inequalities in resource allocation. Even if in our analysis we observed that in

some counties high level is determined by a certain factor that acts locally and regionally (the

concentration of a large number of medical institutions specialized in these areas where the entire

population migrates), which result in a sharp contrast with the low level of other districts, this

factor should be the subject of health policy interventions that aim to reduce unfair differences

found in the analysis.

The third chapter, entitled "Costs in decision making in the public health sector",

shows how hospital care in Romania can be modeled and improved based on actual cost data.

Thus, Chapter III focuses on the study of the relationship between costs and public sector

decision making through concrete analysis, comparisons between different decision models and

costing methods and an overview of managerial accounting tools currently used in the public

sector to identify their advantages and limitations. 3 *** Ministry of Health, Hospitals Financial Situation. 2010, available at http://www.ms.ro/?pag=210 (accessed 10 March 2012)

9

Strategic decision "to produce or buy” certain products or services is mandated to assess

and establish realistic, exactly, that alternative is more advantageous to the final economic

results of the organization. The criteria for analysis are not only economic, must be taken into

account certain technical reasons, organizational and even social: "produce" if we gets low cost

or if there is wrong suppliers or if used thus the surplus of staff and benefit increases, or to

obtain a desired quality; "buy" if there is more than one supplier or if there is no technical skills,

managerial and adequate capacities to produce, or if fast and costly technological changes occur.

Opportunity cost is the sacrifice that supports an economic subject when choosing

between several possible solutions. Opportunity cost is used only for limited resources, because

in these conditions, the sacrifice may occur in favor of other more efficient alternatives. The

public sector has always faced the problem of limited resources. Act of choice, especially in the

public sector, appears like a need for limiting resources. Resources are limited, especially in

public sector, which makes their use to compete: when you want to satisfy in a higher degree of

certain need (ensuring staff salaries, for example), must be accepted to satisfy other needs in a

lesser extent (investment in equipment). Limitation of resources forces the manager to be

effective in restoring public priorities. No matter how limited it is an action of a public

institution, it exerts an influence on resource allocation, because itself, inevitably involves

consumption of resources and so long as resources are limited, it involves an opportunity cost.

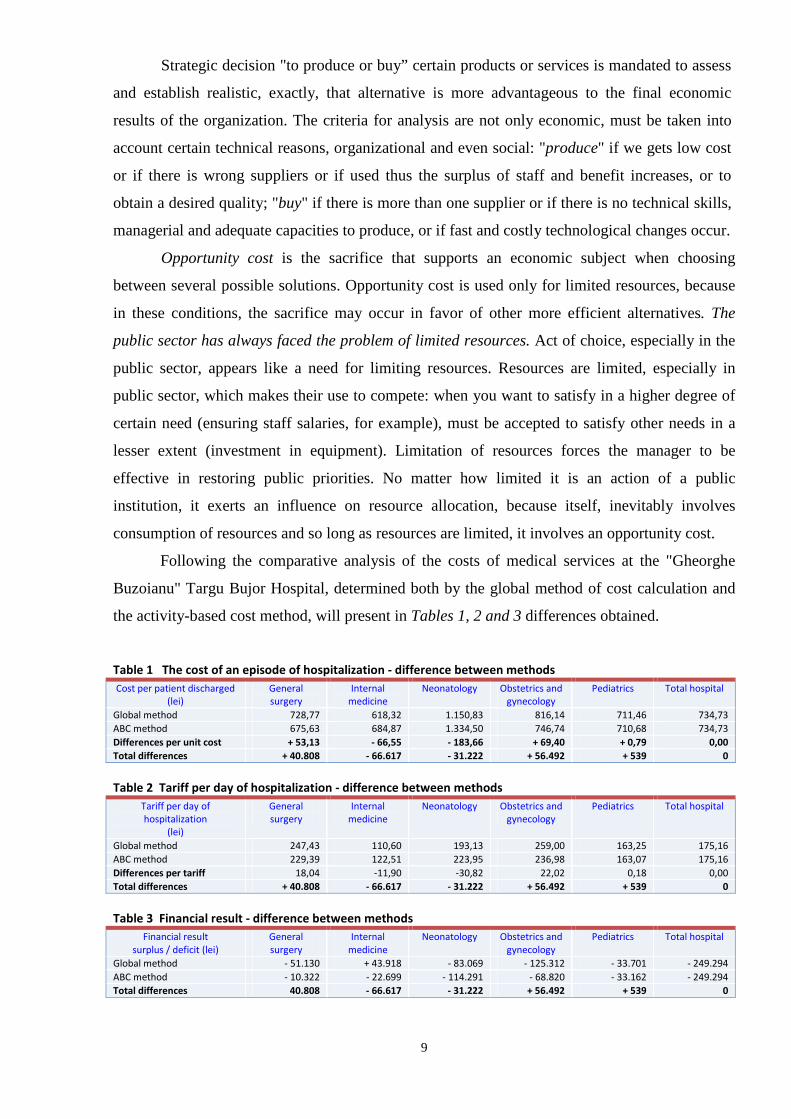

Following the comparative analysis of the costs of medical services at the "Gheorghe

Buzoianu" Targu Bujor Hospital, determined both by the global method of cost calculation and

the activity-based cost method, will present in Tables 1, 2 and 3 differences obtained.

Table 1 The cost of an episode of hospitalization - difference between methods

Cost per patient discharged

(lei)

General

surgery

Internal

medicine

Neonatology Obstetrics and

gynecology

Pediatrics Total hospital

Global method 728,77 618,32 1.150,83 816,14 711,46 734,73

ABC method 675,63 684,87 1.334,50 746,74 710,68 734,73

Differences per unit cost + 53,13 - 66,55 - 183,66 + 69,40 + 0,79 0,00

Total differences + 40.808 - 66.617 - 31.222 + 56.492 + 539 0

Table 2 Tariff per day of hospitalization - difference between methods

Tariff per day of

hospitalization

(lei)

General

surgery

Internal

medicine

Neonatology Obstetrics and

gynecology

Pediatrics Total hospital

Global method 247,43 110,60 193,13 259,00 163,25 175,16

ABC method 229,39 122,51 223,95 236,98 163,07 175,16

Differences per tariff 18,04 -11,90 -30,82 22,02 0,18 0,00

Total differences + 40.808 - 66.617 - 31.222 + 56.492 + 539 0

Table 3 Financial result - difference between methods

Financial result

surplus / deficit (lei)

General

surgery

Internal

medicine

Neonatology Obstetrics and

gynecology

Pediatrics Total hospital

Global method - 51.130 + 43.918 - 83.069 - 125.312 - 33.701 - 249.294

ABC method - 10.322 - 22.699 - 114.291 - 68.820 - 33.162 - 249.294

Total differences 40.808 - 66.617 - 31.222 + 56.492 + 539 0

10

It can notice from the three summary tables, that there is a significant difference between

the results obtained by the two methods of calculation, representing nearly 4% of total health

care costs. The explanation for the large differences reflected by ABC is the high complexity

diagnoses and long duration of hospitalization both specific to neonatology and internal

medicine departments. On the other hand, internal medicine department has the largest medical

addressability by nature of diseases treated, hospitalizing almost 30% of all patients in the

hospital. Also, these medical departments, through the specific diagnoses have the longest period

of hospitalization, per an episode of admission (about 6 days in one patient).

All these costs were not captured by the classical method, which calculated against ABC

a complete cost per patient and a charge per day of hospitalization by 11% lower in the

department of internal medicine, respectively 16% in neonatology. This lack of precision leads to

a considerable error of 97,839 lei: hospitalization in internal medicine is more expensive by

66,617 lei, and neonatology department with 31,222 lei. The sum of 97,839 lei is allocated

incorrectly by classical method to the costs of surgery and obstetrics-gynecology departments.

The only department where the two methods have achieved a similar result is pediatrics.

We appreciate the usefulness of ABC method, especially in a hospital where "final

product" - healthcare - can be decomposed into activities, which in turn can be quantified in

costs. In this sense, medical clinical protocols and guidelines are extremely useful, all medical

maneuvers and medical behavior takes place according to clear and detailed criteria, as they are

developed by international guidelines based on evidence of clinical effectiveness and at the same

time, economic and adapted to specialty and hospital competence. Using multiple cost drivers

and less arbitrary, ABC method led to obtaining a real cost and therefore produced a relevant

cost, identifying the exact origins of costs and factors that triggered the consumption of resources

on each medical department.

Given the conclusions of the previous chapters, in the following chapters we realized

empirical studies on the application of managerial accounting tools in public health sector and

the benefits they provide. Thus, in the fourth chapter we presented "Management tools of

performance in Romanian health institutions".

In a public institution, and not only, it is very important to ensure continuity of the

strategic process. Consequently, the budgeting process should not be isolated from the initial

stage (at start of year), but a continuous and ongoing process, trend in global strategic

management being "sliding forecasting". From this perspective, budgets must be able to adapt,

be flexible. Flexible budget is a budget designed to be modified according to the level of activity

achieved. It is known as variable budget or sliding scale budget4 or continuous budget5.

4 Vijayakumar, T., Accounting for Management, Tata McGraw Hill, New Delhi, 2010, p. 20.7

11

Sliding budgeting ensures that if the different achievements of planning, budget figures

be able to correct, of course after following certain rules. Sliding budgeting is to establish a

baseline budget version, from a year, and in its periodic update (recommended quarterly)

depending on achievements of the past period. Changing projections depending on the

circumstances, and thus using in the sliding budget the latest information on the development

and updating quarterly forecasts, it is an advantage of this budget. Sliding budgeting involves

quarterly review of the budget, and this means a higher volume of work and costs. But this

disadvantage is canceled by the fact that the sliding budget is designed for a long time (ideally to

be developed in the medium term of 3 years) and is updated constantly on the go, at

predetermined intervals on the achievements of past time periods and requirements of

foreseeable future. Premises and assumptions are continuously reviewed, as management learns

from experience. In this way, the latest information is included continuously in budgeting

process.

Some authors6 consider that the Balanced Scorecard was originally conceived as a

concept addressed to the need for performance measurement in the private sector and not fully

meet the needs of the public sector in this regard. Costs are high and lack of specialists

constitutes a real obstacle in implementing BSC in public institutions. BSC implementation in a

public hospital could lead to very valuable results. Basically, the Balanced Scorecard scheme for

a hospital is presented in Figure 4.

Figure 4 Balanced Scorecard scheme for hospital

(Source: own achievement after Albu & Albu, 2005, p. 221)

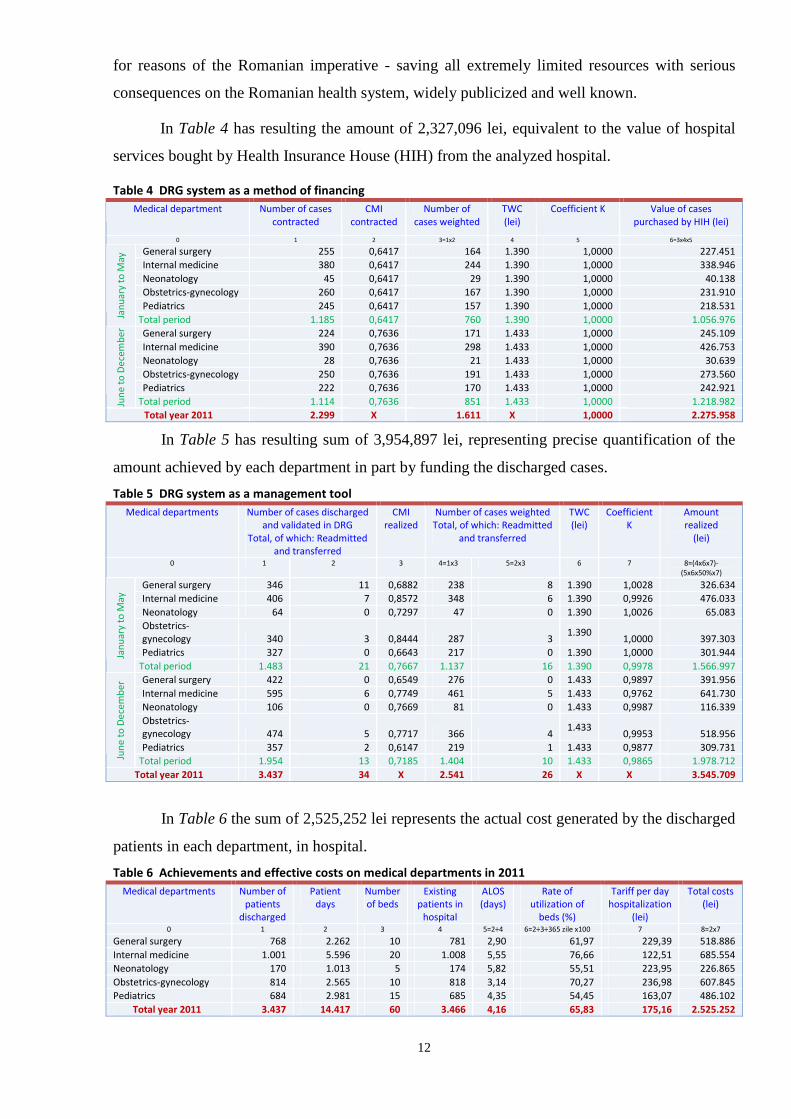

In the fifth chapter of the thesis, we developed an Empirical study on the costing in

healthcare using Diagnosis Related Groups System (DRG). As long as DRG System is used

in real mode with actual data from hospitals, it is really a management tool to estimate and

control costs of hospital services. In practice of the Romanian health sector, DRG system is used

only as a method of funding hospitals because it uses standard data, required by law, obviously

5 Ştefănescu, A., Ţurlea, E., Tănase, G.L., Meanings and controversies on economic entities budgets, in Review of Financial Audit, year X, no. 91, July 2012, p. 19, available at http://www.cafr.ro/uploads/AF%207%202012%20-%20Site-d6af.pdf (accessed 1 September 2012) 6 Wisniewski, M., Olafsson, S., Developing balanced scorecards în local authorities: a comparison of experience, in International Journal of Productivity and Performance Management, vol. 53, no. 7(2004), pp. 602-610

12

for reasons of the Romanian imperative - saving all extremely limited resources with serious

consequences on the Romanian health system, widely publicized and well known.

In Table 4 has resulting the amount of 2,327,096 lei, equivalent to the value of hospital

services bought by Health Insurance House (HIH) from the analyzed hospital.

Table 4 DRG system as a method of financing

Medical department Number of cases

contracted

CMI

contracted

Number of

cases weighted

TWC

(lei)

Coefficient K Value of cases

purchased by HIH (lei)

0 1 2 3=1x2 4 5 6=3x4x5

General surgery 255 0,6417 164 1.390 1,0000 227.451

Internal medicine 380 0,6417 244 1.390 1,0000 338.946

Neonatology 45 0,6417 29 1.390 1,0000 40.138

Obstetrics-gynecology 260 0,6417 167 1.390 1,0000 231.910

Pediatrics 245 0,6417 157 1.390 1,0000 218.531

Jan

ua

ry t

o M

ay

Total period 1.185 0,6417 760 1.390 1,0000 1.056.976

General surgery 224 0,7636 171 1.433 1,0000 245.109

Internal medicine 390 0,7636 298 1.433 1,0000 426.753

Neonatology 28 0,7636 21 1.433 1,0000 30.639

Obstetrics-gynecology 250 0,7636 191 1.433 1,0000 273.560

Pediatrics 222 0,7636 170 1.433 1,0000 242.921

Jun

e t

o D

ece

mb

er

Total period 1.114 0,7636 851 1.433 1,0000 1.218.982

Total year 2011 2.299 X 1.611 X 1,0000 2.275.958

In Table 5 has resulting sum of 3,954,897 lei, representing precise quantification of the

amount achieved by each department in part by funding the discharged cases.

Table 5 DRG system as a management tool

Medical departments Number of cases discharged

and validated in DRG

Total, of which: Readmitted

and transferred

CMI

realized

Number of cases weighted

Total, of which: Readmitted

and transferred

TWC

(lei)

Coefficient

K

Amount

realized

(lei)

0 1 2 3 4=1x3 5=2x3 6 7 8=(4x6x7)-

(5x6x50%x7)

General surgery 346 11 0,6882 238 8 1.390 1,0028 326.634

Internal medicine 406 7 0,8572 348 6 1.390 0,9926 476.033

Neonatology 64 0 0,7297 47 0 1.390 1,0026 65.083

Obstetrics-

gynecology 340 3 0,8444 287 3 1.390

1,0000 397.303

Pediatrics 327 0 0,6643 217 0 1.390 1,0000 301.944 Jan

ua

ry t

o M

ay

Total period 1.483 21 0,7667 1.137 16 1.390 0,9978 1.566.997

General surgery 422 0 0,6549 276 0 1.433 0,9897 391.956

Internal medicine 595 6 0,7749 461 5 1.433 0,9762 641.730

Neonatology 106 0 0,7669 81 0 1.433 0,9987 116.339

Obstetrics-

gynecology 474 5 0,7717 366 4 1.433

0,9953 518.956

Pediatrics 357 2 0,6147 219 1 1.433 0,9877 309.731

Jun

e t

o D

ece

mb

er

Total period 1.954 13 0,7185 1.404 10 1.433 0,9865 1.978.712

Total year 2011 3.437 34 X 2.541 26 X X 3.545.709

In Table 6 the sum of 2,525,252 lei represents the actual cost generated by the discharged

patients in each department, in hospital.

Table 6 Achievements and effective costs on medical departments in 2011

Medical departments Number of

patients

discharged

Patient

days

Number

of beds

Existing

patients in

hospital

ALOS

(days)

Rate of

utilization of

beds (%)

Tariff per day

hospitalization

(lei)

Total costs

(lei)

0 1 2 3 4 5=2÷4 6=2÷3÷365 zile x100 7 8=2x7

General surgery 768 2.262 10 781 2,90 61,97 229,39 518.886

Internal medicine 1.001 5.596 20 1.008 5,55 76,66 122,51 685.554

Neonatology 170 1.013 5 174 5,82 55,51 223,95 226.865

Obstetrics-gynecology 814 2.565 10 818 3,14 70,27 236,98 607.845

Pediatrics 684 2.981 15 685 4,35 54,45 163,07 486.102

Total year 2011 3.437 14.417 60 3.466 4,16 65,83 175,16 2.525.252

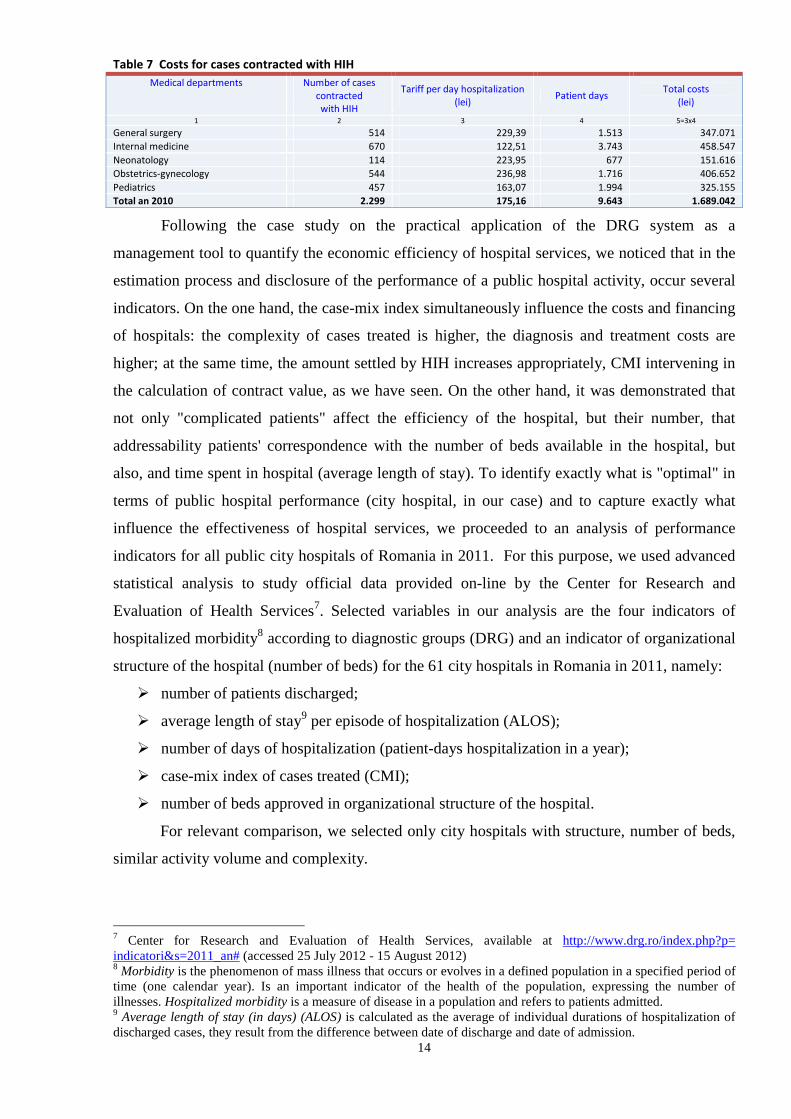

13

The difference between the amount realized theoretically and the amount contracted with

HIH is clearly positive (+1,269,751 lei) and represents the amount that the hospital would be

required to collect in addition to the contracted budget, because, regardless of the resources

consumed by patients discharged, the amount of 3,545,709 lei reflect actual funding for

discharged cases, according to DRG mechanism. By comparing the actual value of cases

discharged (3,545,709 lei) with costs to treat patients (2,525,252 lei) results a surplus of

1,020,457 lei - savings that could be kept in the hospital for investment.

The difference between the contracted budget (2,275,958 lei) and costs incurred to

resolve all cases (2,525,252 lei) is negative (– 249,294 lei), representing a deficit resulting from

the fact that the hospital has treated a total of 3,466 patients and received only the equivalent of

2,299 cases. In concrete terms, although the hospital activity is profitable, so economically

efficient, performing with 50.76% more, the hospital receive 9.87% less than spent and 35.81%

less than realized. The situation is almost unrealistic unfair, as follows: hospital has treated 3,466

patients of whom only 3,437 cases was DRG validated and HIH has paid only 2,299 cases (!)

Therefore, it results a number of 1167 cases discharged from hospital, for which there was no

"leu" returned from the National Unique Health Insurance Fund (NUHIF), patients being treated

from the hospital savings.

If the HIH, as a customer of the hospital, would have bought all medical services

performed by the hospital, we can say with conviction that healthcare, led by a management

team well prepared, is a very profitable activity: the value of all cases discharged and validated

in 2011 i.e. 3,437 cases, mean revenues totaling 3,545,709 lei, plus the 29 cases invalidated by

DRG (3,466 realized cases minus 3,437 validated).

To obtain at least fictional this revenue, the hospital performed the actual expenditures

2,525,252 lei, resulting in a surplus of 1,020,457 lei, amount absolute sufficient to purchase

modern medical equipment, for example, a chapter that most hospitals in Romania are very

poorly. In fact, although the hospital has spent 2,525,252 lei for 3,437 discharged cases, the

revenue from HIH, under contract, were 2,275,958 lei cashed for only 2,299 cases.

Extrapolating, if the hospital would be treated only 2,299 patients (cases reimbursed by

HIH), according to Table 7, the costs were worth 1,689,042 lei, and the surplus would have been

586,916 lei (2,275,958 lei received for the 2,299 patients minus 1,689,042 lei spent on the same

2,299 patients). Instead, the hospital not only achieved a surplus of 586,916 lei, but more, it

spent extra 836,211 lei for unsettled patients (difference between effective expenditures of

2,525,252 lei and HIH reimbursed expenditures for patients of 1,689,042 lei).

14

Table 7 Costs for cases contracted with HIH

Medical departments Number of cases

contracted

with HIH

Tariff per day hospitalization

(lei) Patient days

Total costs

(lei)

1 2 3 4 5=3x4

General surgery 514 229,39 1.513 347.071

Internal medicine 670 122,51 3.743 458.547

Neonatology 114 223,95 677 151.616

Obstetrics-gynecology 544 236,98 1.716 406.652

Pediatrics 457 163,07 1.994 325.155

Total an 2010 2.299 175,16 9.643 1.689.042

Following the case study on the practical application of the DRG system as a

management tool to quantify the economic efficiency of hospital services, we noticed that in the

estimation process and disclosure of the performance of a public hospital activity, occur several

indicators. On the one hand, the case-mix index simultaneously influence the costs and financing

of hospitals: the complexity of cases treated is higher, the diagnosis and treatment costs are

higher; at the same time, the amount settled by HIH increases appropriately, CMI intervening in

the calculation of contract value, as we have seen. On the other hand, it was demonstrated that

not only "complicated patients" affect the efficiency of the hospital, but their number, that

addressability patients' correspondence with the number of beds available in the hospital, but

also, and time spent in hospital (average length of stay). To identify exactly what is "optimal" in

terms of public hospital performance (city hospital, in our case) and to capture exactly what

influence the effectiveness of hospital services, we proceeded to an analysis of performance

indicators for all public city hospitals of Romania in 2011. For this purpose, we used advanced

statistical analysis to study official data provided on-line by the Center for Research and

Evaluation of Health Services7. Selected variables in our analysis are the four indicators of

hospitalized morbidity8 according to diagnostic groups (DRG) and an indicator of organizational

structure of the hospital (number of beds) for the 61 city hospitals in Romania in 2011, namely:

� number of patients discharged;

� average length of stay9 per episode of hospitalization (ALOS);

� number of days of hospitalization (patient-days hospitalization in a year);

� case-mix index of cases treated (CMI);

� number of beds approved in organizational structure of the hospital.

For relevant comparison, we selected only city hospitals with structure, number of beds,

similar activity volume and complexity.

7 Center for Research and Evaluation of Health Services, available at http://www.drg.ro/index.php?p= indicatori&s=2011_an# (accessed 25 July 2012 - 15 August 2012) 8 Morbidity is the phenomenon of mass illness that occurs or evolves in a defined population in a specified period of time (one calendar year). Is an important indicator of the health of the population, expressing the number of illnesses. Hospitalized morbidity is a measure of disease in a population and refers to patients admitted. 9 Average length of stay (in days) (ALOS) is calculated as the average of individual durations of hospitalization of discharged cases, they result from the difference between date of discharge and date of admission.

15

In order to get a more precise classification of city hospitals in Romania in terms of

efficiency, in our approach we use factor analysis and cluster analysis. Following the analysis,

we observed that the five individual variables are characterized by high levels of volatility, but

some are highly correlated with each other (as was the case indicators "Number of patients

discharged" and "Number of hospitalization days"), which means that in addition to the intrinsic

information content of each variable, there is a significant amount of information directly

dissipated in unobserved connections between variables. In this context, principal components

analysis has proven to be a useful tool to study because managed both synthesizing information

and information redundancy elimination.

Applying principal components method on our data set, we obtained two components

which summarizes approximately 77.880% of the information contained in the original data.

Thus, halving variables was performed under conditions of minimal information loss of 22.12%.

Therefore, we concluded that the indicator "Number of patients discharged" is not really

necessary in a city hospital efficiency analysis as long as the indicator "Number of

hospitalization days" provides more relevant information. Depending on the complexity and

pathology of disease, an episode of hospitalization may take 2-3 until 10-15 days for acute

patients or even up to 40-50 days (or more) for patients with chronic diseases. Thus, there may

be 10 patients who accumulate 20 days of hospitalization and only one admitted for 20 days and

the costs, at least hotelier ones (food, utilities, clothes, personal hygiene products, cleaning) are

identical for a patient or 10 patients. The first component can be analyzed in terms of morbidity

hospitalized at the admission capacity, because we noticed that there is a strong correlation

between the total number of patients discharged in a year, patient-days hospitalization per year

and the number of hospital beds. A second component can be analyzed in terms of the

complexity of cases treated or hospitalization period, statistical analysis capturing well close

correlation between the two indicators. We see therefore that there is no determining factor

between the complexity of the disease and greater or smaller number of patients discharged, but

obviously hospital beds are constantly crowded (day hospitalization) due to high turnover on a

bed (discharged patients).

In terms of hospital performance, it is difficult to assess which hospital is economically

efficient: a hospital with more patients (indicator "Number of patients discharged" is high) or a

hospital with patients "complicated" (indicator "Case-mix index" is high), a hospital with patients

"complicated" due to prolonged hospitalization (indicator "Average length of stay" is high) or an

increased complexity of diagnosis etc. Statistical analysis reached its intended purpose and was

able to clarify these issues: information redundancies were eliminated (Targu Carbunesti

Hospital is atypical for our analysis), we obtained a homogeneous mass of most city hospitals

(class 2) and we identified a benchmark of economic efficiency (Costesti Hospital). "Performing

16

supplier" recorded the best values of efficiency indicators. Although CMI increased, compared

with other providers, the hospital was able to make adequate values, which led placing first in

ranking. In other words, the optimum efficiency is the obvious, that hospital that manages to

quickly treat a number of patients appropriate for hospital capacity, but at the same time with a

high complexity of diagnostics. Accordingly, such a hospital will receive funding from HIH

sufficient to cover the costs of medical services provided and will be able to use resources in an

economical manner.

At the other extreme are the hospitals which forces length of stay, artificial - to get more

funding or wrongly - because there are doctors that hospitalized those patients who are not

suitable for continuous hospitalization (many hospitals still treating patients in continuous

hospitalization, even if the diseases can be treated in one day hospitalization). These ways of

increasing the length of stay determines implicitly equally artificial increase of the complexity of

cases treated, but much less than the costs involved, fact reflected in insufficient funding to cover

high costs, not always justified.

Statistical analysis performed identified thus some correlation between hospital

performance indicators. Thus, at the level of correlation between the number of cases discharged

and complexity index, we see that increasing the number of patients treated implicitly determines

an increase in costs, and in this respect we believe that increasing complexity index of cases

(DRG's complexity) must ensure an optimal level of hospital resources, in accordance with

treated patients. Statistical analysis performed reinforces the idea that, in time, at the level of

hospitals has formed a gap increasing in terms of funding. Thus, given that theoretically, the cost

of a weighted case is the same, we consider that, in terms of required resources, should not

register significant differences between healthcare providers.

17

Conclusions, contributions and future research directions

Managing a public hospital has a special place, because involves management of

complex activities with a high consumption of resources, so that leads to health services of high

quality. These activities begin with the treatment provided to patients (clinical activity) and

continue with hotel services (accommodation and food), effective stock management (medicines,

medical supplies, laboratory reagents, etc.) and extremely limited financial resources, but also

strategies to improve the quality of medical care (training, investment in medical equipment

performance, quality management standards). For this reason, a hospital management is based on

decisions from knowledge of all the factors that could influence activity and strategic objectives.

In this regard, accurate determination of costs and their implications in achieving established

performance is a constant imperative in decision making. There is no doubt that in a public

institution, a well established managerial accounting and dynamic, flexible, is a powerful tool

available to managers as a valuable source of information in decision-making relevant to

planning, financing costs and strategies. But it is absolutely necessary to establish and develop a

new mentality among managers about cost strategy and the importance of its use.

We observed in our approach, also studying current trends in research, that the

organizations themselves, private and especially public, and normalizers and professional

accountants, show no interest and seem not to understand the importance of managerial

accounting. Managers and even accountants identifies managerial accounting with simple cost

calculation, ignoring modern and advanced methods that can enhance value and improve

organization performance and its internal processes. Also, the lack of methodological rigor of

normalizers, who are not concerned with the development of more specific and severe

regulations on managerial accounting, and also the lack of a specialized professional body, leads

practitioners not be concerned with this area, known the fact that they are turning their attention

rather to what is highly regulated, standardized and obligatory (financial accounting, taxation,

financial statements). Precisely for these reasons, also observed in practice, we join the experts

who believe that academic environment understand the importance and need for managerial

accounting and advanced cost calculation, having the power to facilitate the process of

knowledge through its experts, demonstrated by research concerns more frequent and more

advanced in this field in recent years.

Making parallels between financial and managerial accounting, between classical and

modern methods of budgeting, costing methods, analyzing the particularities of the health system

in Romania, we can formulate the following conclusions and proposals regarding the application

of modern tools of management accounting in the public sector, namely the public health system.

18

Financial accounting has its well-defined role in an organization, but its information is

intended for external environment. Managerial accounting uses some of this information, but

with the help of advanced tools and with increased and informed interest from the management,

with concern and dedication of the professionals, with the cooperation and effective

communication between all hierarchical levels in the organization, can create a strong system of

information necessary for the future of the organization, an adviser to management decision

making. Managerial accounting has evolved from a system of financial information to a set of

tools oriented outwards, towards strategy and future, by changing over time, the orientation of

the calculation and identifies problems, to reduce waste and using the resources for value

creation and support for act of management and decision.

Specialists and many healthcare organizations have attempted to provide a valid response

to those who wonder to what extent the health system is better than another. Each national health

system has a number of objectives. Essentially, any healthcare system aims to provide a high

level of health and equitable distribution of health services. Meanwhile, a healthcare system has

to comply with people's expectations, which implies respect for the individual (autonomy and

confidentiality) and client orientation (prompt service and quality medical act). The conclusion

after analyzing the Romanian healthcare system in the European and international context is that

all these objectives should be related to the absolute level of responsiveness to the demands of

patients and the distribution of health care, and the health system reform has to take into account

the national specificities and must be based on a solid knowledge of system problems, on

available resources and clearly defined goals.

Our analysis at national level surprised that although the hospital financing system takes

into account the principle of "money follows the patient", in reality this applies only partially,

and transfers of funds are not made on the basis of clearly defined criteria. In this respect, it is

necessary to separate the funding system unlike system health care providers to ensure those who

pay greater autonomy in spending and unequivocal adoption of the idea that the health sector

resources should be directed to the patient needs (e.g. DRG codes).

Cost data can be used mainly in strategic decisions, because at the time when information

is presented to the management, production processes were consumed, and interventions that

occur are late. This is why the best cost for the organization is not necessarily the lowest, but one

that occurs in the place and at the right time and gives to user (the manager) the desired

precision. If costs involved are not taken into account, a decision is made difficult because the

main objective of the organization is to achieve performance, a goal that can be achieved only

under conditions of correlation decisions with costs.

Strategic cost management is articulated with managerial accounting rather it is an

integral part of it. In essence, the role of strategic cost management is "the establishment of

19

budgets, standard costs and actual costs of operations, processes, activities or products and

employees analysis, profitability on the use of funds" (Lucey, 2002), representing a

"cornerstone" for accounting information system in an organization.

By testing practical example of a public hospital of the ABC method compared to the

classical method allocation of costs, we identified a competitive tool that offers more relevant

costs to management. ABC method is the most used approach, recognized and appreciated

internationally to improve system cost, since it is based on understanding how resources are

consumed to create value. We have noticed that in the public sector the situation becomes more

complicated, as the management of costs is much affected by budgetary constraints. Therefore,

cost allocation based on resource consuming activities is the most accurate method of

quantifying the indirect costs of a hospital. Given the complexity of hospital care, which

involves many types of resources and services provided, the percentage of indirect costs is very

high and thus causes inaccurate estimates costing (cost per episode of hospitalization or

discharged patient, tariff per day of hospitalization, etc). In this respect, the ABC method is a

solution to identify activities inefficient and resource consuming activities in terms of cost /

benefit, thereby facilitating their effective costs control. Also, the cost information obtained by

the ABC method, i.e. activity costs, allowing to the hospital management to better and more

accurately estimate future costs with the same type of patient or diagnosis, and compare medical

costs with the level of funding. Relevance of the information provided by the ABC method

allows the hospital to identify and expand profitable services or to reorganize and restrict

inefficient activities.

In the public sector, especially for public institutions financed from own revenues (such

as public hospitals), it is imperative a more flexible mechanism of the budgetary process based

on procedures and rules focused on evaluation, results, efficiency, performance. Availability of

flexible budgets means for a manager the ability to handle information and resources and lead

the change. Ideally, a flexible budget should be built based on several scenarios depending on the

overall context of the internal and external environment of public institution, and its ability to

adapt: pessimistic, realistic (balanced) or optimistic, in conjunction with what happens in its field

and at the macroeconomic level, but with the real possibilities of public institution. Both the Law

no. 95/2006 on healthcare reform and the project of new health law, in the "Hospitals funding"

section, the first article reads: "Hospitals are organized as public institutions fully financed from

own revenues, and operates on the principle of financial autonomy". Under article 16, paragraph

(1) of Law no. 273/2006 on local public finance, the principle of financial autonomy means that

"administrative-territorial units are entitled to sufficient financial resources...". As such, hospitals

need flexible budgets, funded by achievements and not depending on the HIH budget, or local

councils and directorates of public finance restrictions.

20

A public hospital, works only if produces services: receives funds from HIH if it treating

patients, unlike public institutions financed from the state budget (such as the ministries,

National House of Pension, National Health Insurance House, National Agency for

Employment), which regardless of achievements receive funds. For this reason, the hospital

needs a sliding budget to enable comparisons between the reality of budget execution and initial

budgetary projections, based on patient addressability size - i.e., what has received from HIH and

what actually performed (as we presented empirical study on DRG system). With a flexible

budget, fixed costs should remain constant and variable costs should be modified according to

sales (HIH settled patients) if they were higher or less than were projected. Flexible budget is

then compared with reality, and the differences between planned and realized are calculated and

designed to be favorable or unfavorable (surplus or deficit). Health institution prepare flexible

budget taking account of changing consumption according to their achievements, this

representing a dynamic basis for comparing actual results with budget indicators. A flexible

budget is a detailed plan implemented in order to control indirect costs and which is available for

a significant period. It helps to control certain expenditure for which consumptions are not easy

to standardized, because they are not in each final product (such as laboratory investigations, for

example, which are not found in all medical services provided). It is required where possible

(and in a public hospital is possible) that budgets must be flexible, meaning adjustable, adaptable

so that their contents may change as the activity is changing and should be reviewed taking into

account the changes in the organization. Sliding budget proposed by us, obliges the financial

manager to set achievable goals and identify the key factor or limiting factor that will impose

constraints on current and future activities of the institution. This is because a budget that

includes unrealized indicators is totally ineffective.

We identified in our approach a strategic tool for measurement and performance

management, which helps the entity to accommodate long-term strategies with short-term

actions, using both financial indicators and non-financial: Balanced Scorecard. Performance

measurement, the main function of the BSC, divided these indicators of outcome indicators that

indicate past efforts and pilot indicators that indicate future performance, intervening to identify

opportunities and prevent errors. These indicators help finally to building the organization's

performance through the balance and interaction of the four forces (financial, customer

satisfaction by pursuing their perceived value, the efficiency of internal processes and its

capacity for growth and development). Balanced Scorecard is a tool designed to align actions

and strategic plans into a coherent control system. Since the BSC philosophy is to learn from its

actions, teamwork and follow-up strategy, this tool puts a strong emphasis on clear

communication of objectives and priorities. In short, being a flexible and dynamic instrument,

the BSC shows what needs to be done. According to its authors, Kaplan and Norton Balanced

21

Scorecard is a management system that translates strategy into action (The Balanced Scorecard:

Translating Strategy into Action, 1996). If a strategy for success has never been an easy task,

surely its practical application is crucial. Kaplan and Norton summarized this very well: "The

formulation of great strategies is an art, and it will always remain so. But the description of

strategy should not be an art. If people can describe strategy in a more disciplined way, they will

increase the likelihood of its successful implementation"10. Specifically, the Balanced Scorecard

approach helps public managers in the implementation of the ideas contained in the management

plans and development strategy. In the Balanced Scorecard the indicators of the four perspectives

(financial, customer, internal processes and learning & growth) are derived from vision and

strategy of organization. Developing the prospective board (balanced scorecard) implies that for

each of these perspectives to establish in a first stage: targets (what we aim), priorities (what

trying to achieve) and strategic objectives (what key elements should rectify to achieve the

objectives). Subsequently, for each key objective it will identify the sources of information and

performance indicators related to objectives (how do we measure), which are disaggregated by

organizational levels, responsible persons, optimum values and possibly on terms. And finally,

we set up measures to achieve the objectives (how do we know if we got to where we plan), BSC

placing great emphasis on performance measurement feedback. Of course, the Balanced

Scorecard is accompanied by an implementation plan on how the objectives will be achieved.

In Romania, where organizational climate is quite precarious, there is every chance that

such a system may be regarded only as an additional form of control of staff, so be sabotaged by

employees. On the other hand, the interest of managers of public institutions not often goes to

performance, at least not in the terms set by the Balanced Scorecard. Too few public institutions

are concerned with customer satisfaction of accountability to citizens, and efficiency (Şandor &

Raboca, 2004). We ensure that academic environment, for which performance is a real concern,

will also be able to guide organizational climate to these concerns essential to success of

organization, we appreciate.

The results of our research revealed many shortcomings of the current system of

financing and costing of public sector health and showed how it could be modeled and improved

by advanced methods of modern managerial accounting based on actual costs hospital care in

Romania. By recourse to the particularities of the health system in Romania, we presented a

model costing hospital services based on classification diagnosis-related groups system (DRGs).

The study, based on practical experience, is an element of novelty and utility, as we consider that

case-mix board made through the Diagnosis-Related Group provides hospital management

10 Kaplan, R.S., Norton, D.P., Having Trouble with Your Strategy? Then Map it, in Harvard Business Review, September-October 2000, pp. 167-176, available at http://www.bscol.se/_wcm/documents/Having%20trouble% 20with%20your%20stategy%20then%20map%20it%20%282%29.pdf (accessed 7 June 2012)

22

information on effectiveness of the financial mechanism, and at the same time, is a management

tool to estimate and control costs of hospital services.

From the idea that "you'll get only what you pay", using this funding mechanism based on

complexity of diagnoses treated, stimulates the hospital to treat patients more quickly and in the

best conditions. This is because the amount received from HIH depends on the types of patients

treated (volume and complexity of diagnosis), and not arbitrary factors such as structure and

hospital capacity (number of beds, number of medical departments, or degree of medical

equipment) or other process indicators (number of days of hospitalization, average length of stay

per type of departments). In this way resource allocation to hospitals becomes more objective,

transparent and fair: a hospital with a small number of patients, or patients with less severe

diseases will have lower financing.

In the DRG-based financing mechanism, were developed rates per weighted case, ie

"standard" cases, adjusted by complexity pathology. Using this mechanism manifests differently

in terms advantage / disadvantage to its three beneficiaries. Thus, on the one hand, hospitals

know exactly how much they receive from HIH for a patient, but do not know the cost to the

patient concerned. On the other hand, health insurance houses know what types of patients

contracted services with hospitals, but do not know the package of medical services actually

provided to patients, covered by amount. Third, patients know (or should know) what medical

services are entitled as insured persons, but in reality they do not know what services they will

actually receive from public health system (Haraga & Ţurlea, 2009). ICM-DRG board allows

clear and consistent measure of the types of patients treated, control costs incurred by them and

therefore efficient use of resources and disclosure of medical performance achieved by each

department individually. For these reasons, our study demonstrated how the DRG system

stimulates the calculation and control of hospital costs at department level and at the patient

level, helping to reduce patient costs and on DRG, and average length of stay on groups of

diseases or medical specialties, especially at DRG's which "allows" these things. In addition,

following the application mechanism DRG, the hospital has developed a highly complex

database that can provide useful information to hospital management. In fact, data DRG helps

the management team to know better the hospital, with its weaknesses and strengths, and act

accordingly, based on the evidence in the process of increasing the quality and efficiency of

services.

Finally, we consider that our research has achieved its purpose and meet the information

needs of academics, specialists and practitioners in particular, giving them more modern and

efficient methods of managerial accounting, solutions and proposals which they can apply in

practice of public healthcare institutions.

23

Selected references

Specialized books

1. Albu, N., Albu, C. - Instrumente de management al performanţei. Contabilitate de gestiune, Volumul I , Editura Economică, Bucureşti, 2003

2. Albu, N., Albu, C. - Instrumente de management al performanţei. Control de gestiune, Volumul II, Editura Economică, Bucureşti, 2003

3. Albu, N., Albu, C. - Soluţii practice de eficientizare a activităţilor şi de creştere a peformanţei organizaţionale. Gestiunea dezvoltării durabile prin Balanced Scorecard, Editura CECCAR, Bucureşti, 2005

4. Andrei, T., Matei, A., Stancu I., Andrei C. L.

- Socioperformanţa reformei sistemului public de sănătate, Editura Economică, Bucureşti, 2009

5. Androniceanu, A. - Management public - Studii de caz din instituţii şi autorităţi ale administraţiei publice, Editura Universitară, Bucureşti, 2008

6. Anica - Popa L.E. - Conducerea întreprinderii prin costuri. Recursul la modelele contabilităţii manageriale, Editura Economică, Bucureşti, 2005

7. Bouquin, H. - Contabilitate de gestiune, traducere Prof. dr. Tabără N., Editura TipoMoldova, Iaşi, 2004

8. Braga, V.F. - Contabilitate managerială, Editura Fundaţiei România de Mâine, Bucureşti, 2009

9. Briciu, S. - Contabilitatea managerială. Aspecte teoretice şi practice, Editura Economică, Bucureşti, 2006

10. Briciu, S., Căpuşneanu, S., Rof, M.L., Topor, D.

- Contabilitatea şi controlul de gestiune, instrumente pentru evaluarea performanţei entităţii, Editura Aeternitas, Alba Iulia, 2010, p. 12

11. Budugan, D., Georgescu, I., Berheci, I., Beţianu, L.

- Contabilitate de gestiune, Editura CECCAR, Bucureşti, 2007

12. Butuc, C., Dragomirişteanu, A., Fărcăşanu, A.

- Managementul serviciilor de sănătate, Editura C.N.I. Coresi, Bucureşti, 2000

13. Cardoş, I. R. - Contabilitate managerială şi calculaţia costurilor. Trecut, prezent şi viitor, Editura Alma Mater, Cluj-Napoca, 2010

14. Călin, O. (coord.), Man, M., Nedelcu, M.V.

- Contabilitate managerială, Editura Didactică şi Pedagogică, Bucureşti, 2008

15. Călin, O., Călin, C. - Contabilitate managerială, Editura Tribuna Economică, Bucureşti, 2007

16. Căpuşneanu, S. - Elemente de management al costurilor, Editura Economică, Bucureşti, 2008

17. Chadwick, L. - The Essence of Management Accounting, traducere Criste D., Contabilitate de gestiune, Editura Teora, Bucureşti, 1998

18. Diaconu, P. - Contabilitate managerială & Planuri de afaceri, Editura Economică, Bucureşti, 2006

19. Diaconu, P., Albu, N., Mihai S., Albu, C., Guinea F.

- Contabilitate managerială aprofundată, Editura Economică, Bucureşti, 2003

20. Dragomirişteanu A., Radu P., Mihăescu C., Brutu C.

- Economie sanitară şi management sanitar, Editura Rao, Bucureşti, 2003

21. Dumitru, M., Calu, D.A.

- Contabilitatea de gestiune şi calculaţia costurilor, Editura Contaplus, Ploieşti, 2008

22. Farkas, E. - Elemente de sănătate publică şi management sanitar, Editura University Press, Târgu-Mureş, 2006

23. Fătăcean, G. - Contabilitate managerială, Editura Alma Mater, Cluj-Napoca, 2005

24. Garrison, R., Noreen, E., Brewer, P.

- Managerial Accounting, McGraw-Hill Irwin, New York, 2008

25. Gisberto-Chiţu, A., Tudorache, S., Pitulice, C.

- Contabilitatea şi gestiunea instituţiilor publice, Editura CECCAR, Bucureşti, 2003

26. Glynn J.J., Murphy M., Perrin J., Abraham A.

- Accounting for Managers, Third Edition, Thompson Learning, 2003

27. Gray, S.J., Salter S.B., Radebaugh L.H.

- Global Accounting and Control. A managerial Emphasis, John Wiley & Sons, New York, 2001

28. Ham, C. - Health Policy in Britain, 5th edition, Palgrave McMillan, Hampshire, 2004

29. Heisinger, K. - Essentials of Managerial Accounting, South-Western Cengage Learning Publisher, USA, 2010

30. Hoffmeyer, U.,K., McCarthy T., R.

- Financing Health Care, vol. I, Kluwer Academic Publishers, Dordrecht, 1994

31. Hopwood, A.G., Chapman, C.S.

- Handbook of Management Accounting Research, vol. 3, Elsevier Ltd., Oxford, 2009

32. Horngren, C.T., Srikant, M.D., Foster, G.

- Contabilitatea costurilor, o abordare managerială, traducere Leviţchi, R., Leviţchi, V., Stanciu, D., Ediţia a XI-a, Editura Arc Chişinău, 2008

24

33. Horngren, C.T., Sundem, G.L., Stratton, W.O.

- Introduction to Management Accounting, 14th edition, Prentice Hall International Press, Upper Saddle River, 2005

34. Iacob C., Firescu V., Băluţă A., Popescu L., Mihai D. , Marinică D.

- Costurile: calculaţie, contabilizare, previziune, Editura Fundaţiei România de Mâine, Bucureşti, 2002

35. Ionescu, L. - Reforma bugetului public şi a contabilităţii publice în România, Editura Economică, Bucuresti, 2005

36. Ionescu, L. (coord.), Diaconu, E., Şuiu, I.

- Contabilitate publică, Editura Fundaţiei România de Mâine, Bucureşti, 2008

37. Johnson, H.T., Kaplan, R.S.

- Relevance Lost: The Rise and Fall of Management Accounting, Harvard Business Press, Business & Economics, 1991

38. Kaplan, R.S., Atkinson, A.A.

- Advanced Management Acconting, Third Edition, Prentice Hall International Press, 1998

39. Kaplan, R.S., Norton, D.P.

- The Strategy-Focused Organization: How BalancedScorecard Companies Thrive in the New Business Environment, Harvard Business School Press, Boston, 2001

40. Kumar, R., Goel, S.L. - Hospital Administration And Management: Theory And Practice, Deep & Deep Publications Ltd, New Delhi, 2007

41. Lock, D. (coord.) - Manualul Gower de Management, Editura Codecs, Bucureşti, 2001

42. Lucey, T. - Costing, 6th edition, Thomson Learning, Continuum, Londra, 2002

43. Mincă, D. - Sănătate publică şi management sanitar, Editura Universitară Carol Davila, Bucureşti, 2005

44. Muţiu, A., Mureşan, M. - Contabilitate managerială, Editura Risoprint, Cluj-Napoca, 2006

45. Nicolescu, O., Verboncu, I.

- Metodologii manageriale, Editura Universitară, Bucureşti, 2008

46. Nistor, C.S. - Trecut, prezent şi perspective în contabilitatea publică românească, Editura Casa Cărţii de Ştiinţă, Cluj Napoca, 2009

47. Niven, P.R. - Balanced Scorecard Step-by-step for Government and Nonprofit Agencies, 2nd Edition, John Wiley & Sons, New Jersey, 2008

48. Nowicki, M. - The Financial Management of Hospitals and Healthcare Organizations, Health Administration Press, Chicago, 2008

49. Olteanu, M. (coord.) - Renaşterea sistemului sanitar printr-o reformă bazată pe dovezi, I.D. International Technoprint, Bucureşti, 2005

50. Opincaru., C., Imbri, E., Gălăţescu, E.

- Managementul calităţii serviciilor în unităţile sanitare, Editura C.N.I. Coresi, Bucureşti, 2004

51. Oprea, C., Man, M., Nedelcu, M.V.

- Contabilitate managerială, Editura Didactică şi Pedagogică, Bucureşti, 2008

52. Pârvu, F. - Costuri şi fundamentarea deciziilor, Editura Economică, Bucureşti, 1999

53. Păunescu, M. (coord.) - Management public în România, Editura Polirom, Iaşi, 2008

54. Proctor, R. - Managerial Accounting for Business Decisions, 2nd Edition, Pearson Education Ltd., Edinburgh, 2006

55. Rampersad, H.K. - Total Performance Scorecard: Fundamente, traducere Turmac C., Editura Didactică şi Pedagogică, Bucureşti, 2005

56. Sarant, P.C. - Zero Base Budgeting in the Public Sector: A Pragmatic Approach, Addison - Westley Publishing, Massachusetts, 1978

57. Simionescu, A., Buşe, F., Bud, N., Purcaru Stamin, I.

- Control Managerial, Editura Economică, Bucureşti, 2006

58. Tabără, N. - Contabilitate şi control de gestiune. Studii şi cercetări , Editura Tipo Moldova, Iaşi, 2004

59. Tabără, N. - Modernizarea contabilităţii şi controlului de gestiune, Editura Tipo Moldova, Iaşi, 2006

60. Tabără, N. - Control de gestiune, Editura TipoMoldova, Iaşi, 2009

61. Tabără, N., Briciu, S. (coord.)

- Cercetări privind modernizarea în contabilitate şi control de gestiune, Editura Tipo Moldova, Iaşi, 2011

62. Tănăsescu, P. - Managementul financiar al activităţii sanitare, Editura Tribuna Economică, Bucureşti, 2001

63. Tănăsescu, P. - Economia sanitară şi management financiar, Editura Rao, Bucureşti, 2003

64. Tiron Tudor, A., Gherasim, I.

- Contabilitatea instituţiilor publice, Editura Dacia, 2002, Cluj Napoca

65. Vijayakumar, T. - Accounting for Management, Tata McGraw Hill, New Delhi, 2010

66. Vlădescu, C. - Managementul serviciilor de sănătate, Editura Expert, Bucureşti, 2000

67. Vlădescu, C. (coord.) - Sănătate publică şi management sanitar. Sisteme de sănătate, Editura Cartea Universitară, Bucureşti, 2004

68. Warren, C.S., Reeve, J.M., Duchac, J.

- Financial and Managerial Accounting, South-Western Cengage Learning Publisher, USA, 2009

69. Webster, W. - Accounting for managers, McGraw-Hill Irwin, 2004

70. Weygandt, J.J., Kimmel, P.D., Kieso, D.E.

- Managerial Accounting: Tools for Business Decision Making, 5th Edition, John Wiley & Sons, New Jersey, 2010

71. Young, D.W. - Management Accounting in Health Care Organizations, Jossey-Bass Publisher, San Francisco, 2003

72. *** - Şcoala Naţională de Sănătate Publică şi Management Sanitar, Managementul spitalului, Editura Public H Press, Bucureşti, 2006

25

Scientific articles published in journals or volume of national and international conferences

73. Abernethy, M.A., Chua, W.F., Luckett, P.F., Selto, F.H.

- Research in managerial accounting: Learning from others’ experiences, în Accounting and Finance, no. 39(1999), pp. 1-27

74. Albu, C., Albu, N. - Bugetele - între tradiţie şi reformă: o tipologie a funcţiilor şi formelor procesului bugetar, în Contabilitatea, Expetiza şi Auditul Afacerilor, nr.11/2006, pp. 48-53

75. Albu, N. - O investigaţie asupra naturii şi întinderii atribuţiilor de contabilitate managerială în România, la Congresul al XVI-lea al profesiei contabile din România, Bucureşti, 15-16 septembrie 2006, pp. 27-48

76. Albu, N., Albu, C. - Fenomenul de convergenţă în contabilitatea managerială: între discurs şi realitate, în Expertiza şi Auditul Afacerilor, nr. 3 (2008), pp. 44-49

77. Aldea, A. - Ghid privind efectuarea analizei diagnostic în unităţile sanitare, în Revista Administraţie şi Management Public, nr. 3 (2004), Editura ASE Bucureşti

78. Armean, P. - Analiza sistemelor de sănătate din perspectiva calităţii, în Revista Management în Sănătate, nr. 3 (2002)

79. Bârliba, I., Siniţchi, G. - Sisteme de sănătate europene, în Revista Practica Medicală, Empire Publishing, vol. 3/2008, nr. 3(11), pp. 116-121

80. Berheci, I., Budugan, D.

- Contabilitatea şi exigenţele manageriale în contextul economiei de piaţă, în Buletinul Ştiinţific al Universităţii George Bacovia Bacău, 1998, pp. 47-48

81. Bigliardi, B., Alberto Ivo Dormio, Galati, F.

- Balanced Scorecard for the Public Administration: Issues from a Case Study, în International Journal of Business, Management and Social Sciences, vol. 2, no. 5, 2011, pp. 1-16, disponibil la http://www.ijbmss-ng.com/ijbmss-ng-vol2-no5-pp1-16.pdf (accesat 30 aprilie 2012)

82. Briciu, S., Căpuşneanu, S.

- Aspecte ale normalizării contabilităţii manageriale din România la nivel microeconomic, în Revista Economie Teoretică şi Aplicată, vol. XVIII (2011), nr. 3 (556), pp. 57-68, disponibil la http://store.ectap.ro/articole/573_ro.pdf (accesat 3 septembrie 2011)

83. Briciu, S., Teiuşan, S.C.

- Sistemul informaţional al contabilităţii de gestiune, în Revista Annales Universitatis Apulensis Series Oeconomica, Universitatea 1 Decembrie 1918 Alba Iulia, nr. 8/2006, vol. 1, pp. 17-23, disponibil la http://oeconomica.uab.ro/upload/lucrari/820061/3.pdf (accesat12 iunie 2011)

84. Budugan, D., Georgescu, I.

- Decizii pe bază de costuri în condiţii de incertitudine, în Analele Ştiinţifice ale Universităţii Alexandru Ioan Cuza Iaşi, Seria Ştiinţe Economice, Tom LII/LIII, 2005/2006, pp. 9-13, disponibil la http://anale.feaa.uaic.ro/anale/resurse/01_Budugan_D,_Georgescu_I_-_Decizii_pe_baza_de_costuri_in_conditii_de_incertitudine.pdf (accesat 11 iunie 2011)

85. Budugan, D., Georgescu, I., Creţu, L.

- Relaţia cost-valoare în contabilitatea managerială, la Congresul al XVIII-a al profesiei contabile din România: «Pentru o nouă cultură în profesia contabilă», 3-4 septembrie 2010, Bucureşti, Editura CECCAR, 2010, pp. 55-72

86. Capps, C., Dranove, D., Lindrooth, R.C.

- Hospital closure and economic efficiency, în Journal of Health Economics, vol. 29 (2010), pp. 87-109, disponibil la http://www.sciencedirect.com/ (accesat 19 iulie 2012)

87. Cardinaels, E., Roodhooft, F., van Herck, G.

- Drivers of cost system development in hospitals: results of a survey, în Health Policy, vol. 69 (2004), pp. 239-252, disponibil la http://www.sciencedirect.com/ (accesat 19 iulie 2012)

88. Căpuşneanu. S. - Metoda ABC (Activity-Based Costing). Principiile gestiunii pe activităţi, în Revista Economie Teoretică şi Aplicată, nr. 432/2005

89. Căpuşneanu. S., Martinescu, D.M.

- Convergenţa principiilor ABC şi ABM - garanţia unui management performant, în Revista Economie Teoretică şi Aplicată, vol. XVII (2010), nr. 10 (551), pp. 51-61, disponibil la http://store.ectap.ro/articole/180.pdf (accesat 18 septembrie 2011)

90. Cokins, G., Căpuşneanu, S.

- Menţinerea în funcţiune a unui sistem eficient ABC/ABM, în Revista Economie Teoretică şi Aplicată, Vo.l XVIII (2011), nr. 2 (555), pp. 46-57, diponibil la http://store.ectap.ro/articole/555_ro.pdf (accesat 14 august 2011)

91. Constantin, C., Gănescu, R.

- Sistemul de sănătate: concept şi importanţă, în Jurnalul Cercetării Doctorale în Ştiinţe Economice, vol. I, nr. 3, Editura ASE Bucureşti, 2009

92. Dascălu, C., Caraiani, C., Dumitrana, M.

- Bugetarea şi controlul bugetar - o provocare pentru economia românească, în Analele Universităţii Orade, Seria Ştiinţe Economice, tom XV, vol. 2, 2006, pp. 468-472, disponibil la http://steconomice.uoradea.ro/anale/vol./2006/finante-contabilitate-si-banci/21.pdf (accesat 4 iunie 2011)

93. Daum, J.H. - Beyond Budgeting: A Model for Performance Management and Controlling in the 21st Century?, în Controlling & Finance, July 2002 issue, pp. 1-3, disponibil la http://www.juergendaum.de/articles/beyond_budgeting.en.pdf (accesat 2 septembrie 2012)

94. Dirsmith, M.W., Jablonsky, S.F., Luzi, A.D.

- Planning and Control in the US Federal Government: a Critical Analysis of PPB, MBO and ZBB, în Strategic Management Journal, vol. I, no. 4, 1980, publicat on-line 17 august 2006, pp. 303-329, disponibil la http://onlinelibrary.wiley.com/doi/10.1002/smj.4250010403/abstract (accesat 8 mai 2010)

95. Doboş, C. - Finanţarea sistemelor de sănătate în ţările Uniunii Europene. România în context european, în Revista Calitatea Vieţii , vol. XIX, nr. 1-2, Editura Academiei Române, 2008, pp. 107-123, disponibil la http://www.revistacalitateavietii.ro/2008/CV-1-2-2008/06.pdf (accesat 26 august 2010)

96. Donaldson, C., Magnussen, J.

- DRGs: the road to hospital efficiency, în Health Policy, vol. 21(1), May 1992, pp. 47-64, disponibil la http://www.sciencedirect.com/ (accesat 19 iulie 2012)

97. Dothan, M.U., Thompson, F.

- A Better Budget Rule, în Journal of Policy Analysis and Management, vol. 28, no. 3 (2009), pp. 463-478, disponibil la http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1077555 (accesat 2 septembrie 2012)

98. Drăgoi, C.M., Ionescu, E., Iamandi, I.E., Chiciudean, A., Constantin, L.G.

- An economic analysis of the romanian healthcare system based on an european comparative approach, în WSEAS Transactions on Business and Economics, vol. 5, issue 6, June 2008, pp. 330-340, disponibil la adresa: http://www.wseas.us/e-library/transactions/economics/2008/27-578.pdf (accesat 30 aprilie 2011)

99. Florea, G. - Consideraţii privind obiectivele informaţiei contabile în sectorul public, în Analele Universităţii din Oradea, Fascicula Ştiinţe Economice, tom XV, vol. II, 2006, pp. 643-646

26

100. Fragidis, L., Chatzis, V. - Modeling Hospital Expenses for a Patient Accounting System, în International Scientific Conference Computer Science, vol. 2 (2008), pp. 449-455, disponibil la http://csconf.org/vol.2/page449.pdf (accesat 12 septembrie 2011)