Embed Size (px)

Citation preview

Managerial Accounting2nd Edition

J. O'Callaghan

Managerial Accounting

by:J. O'Callaghan

Copyright © 2002 John Wiley & Sons, Inc. All rights reserved.

John Wiley & Sons, Inc.New York

0471413658

Due to electronic permissions issues, some material may have been removed from this chapter,though reference to it may occur in the text. The University of Phoenix has determined that thecontent presented herein satisfies the requirements for this course.

ii

Table of Contents

CHAPTER 1MANAGERIAL ACCOUNTING BASICS............................................................................. 5

COMPARING MANAGERIAL AND FINANCIAL ACCOUNTING........................... 6ETHICAL STANDARDS FOR MANAGERIAL ACCOUNTANTS............................... 7MANAGEMENT FUNCTIONS........................................................................................... 7

MANAGERIAL COST CONCEPTS....................................................................................... 9MANUFACTURING COSTS............................................................................................... 9PRODUCT VERSUS PERIOD COSTS............................................................................... 11

MANUFACTURING COSTS IN FINANCIAL STATEMENTS..................................... 13INCOME STATEMENT...................................................................................................... 13BALANCE SHEET............................................................................................................... 16COST CONCEPTS‐A REVIEW.......................................................................................... 18

CONTEMPORARY DEVELOPMENTS IN MANAGERIAL ACCOUNTING............. 20SERVICE INDUSTRY TRENDS......................................................................................... 20VALUE CHAIN MANAGEMENT.................................................................................... 22

APPENDIX 1A ACCOUNTING CYCLE FOR A MANUFACTURING COMPANY... 27WORK SHEET........................................................................................................................... 28CLOSING ENTRIES................................................................................................................ 30SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 1A............................................. 32GLOSSARYū 67

CHAPTER 2COST ACCOUNTING SYSTEMS......................................................................................... 72

JOB ORDER COST SYSTEM.............................................................................................. 73PROCESS COST SYSTEM................................................................................................... 73

JOB ORDER COST FLOW...................................................................................................... 75ACCUMULATING MANUFACTURING COSTS.......................................................... 76ASSIGNING MANUFACTURING COSTS TO WORK IN PROCESS......................... 78ASSIGNING COSTS TO FINISHED GOODS.................................................................. 89ASSIGNING COSTS TO COST OF GOODS SOLD........................................................ 90SUMMARY OF JOB ORDER COST FLOWS.................................................................... 90

REPORTING JOB COST DATA............................................................................................ 92UNDER‐ OR OVERAPPLIED MANUFACTURING OVERHEAD................................ 93

INTERIM BALANCES........................................................................................................ 93YEAR‐END BALANCE....................................................................................................... 94

GLOSSARY.............................................................................................................................. 130CHAPTER 3

THE NATURE OF PROCESS COST SYSTEMS............................................................... 136USES OF PROCESS COST SYSTEMS............................................................................. 136

Managerial AccountingTable of Contents

iii

SIMILARITIES AND DIFFERENCES BETWEEN JOB ORDER COST AND PROCESSCOST SYSTEMS................................................................................................................. 138PROCESS COST FLOW.................................................................................................... 140ASSIGNMENT OF MANUFACTURING COSTS—JOURNAL ENTRIES................ 140

EQUIVALENT UNITS........................................................................................................... 145WEIGHTED‐AVERAGE METHOD................................................................................ 145REFINEMENTS ON THE WEIGHTED‐AVERAGE METHOD.................................. 146PRODUCTION COST REPORT....................................................................................... 148

COMPREHENSIVE EXAMPLE OF PROCESS COSTING............................................. 149COMPUTE THE PHYSICAL UNIT FLOW (STEP 1).................................................... 149COMPUTE EQUIVALENT UNITS OF PRODUCTION (STEP 2).............................. 150COMPUTE UNIT PRODUCTION COSTS (STEP 3)..................................................... 151PREPARE A COST RECONCILIATION SCHEDULE (STEP 4)................................. 152PREPARING THE PRODUCTION COST REPORT..................................................... 153

FINAL COMMENTS.............................................................................................................. 155APPENDIX 3A FIFO METHOD........................................................................................... 162EQUIVALENT UNITS UNDERFIFO................................................................................. 162

ILLUSTRATION................................................................................................................. 163COMPREHENSIVE EXAMPLE........................................................................................... 164

COMPUTE THE PHYSICAL UNIT FLOW (STEP 1).................................................... 165COMPUTE EQUIVALENT UNITS OF PRODUCTION (STEP 2).............................. 166COMPUTE UNIT PRODUCTION COSTS (STEP 3)..................................................... 167PREPARE A COST RECONCILIATION SCHEDULE (STEP 4)................................. 168PREPARING THE PRODUCTION COST REPORT..................................................... 169

FIFO AND WEIGHTED‐AVERAGE................................................................................... 171SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 3A........................................... 171GLOSSARY.............................................................................................................................. 207

CHAPTER 4ACTIVITY‐BASED COSTING VERSUS TRADITIONAL COSTING........................ 213

TRADITIONAL COSTING SYSTEMS............................................................................ 213THE NEED FOR A NEW COSTING SYSTEM.............................................................. 214ACTIVITY‐BASED COSTING.......................................................................................... 215

ILLUSTRATION OF TRADITIONAL COSTING VERSUS ABC................................ 217UNIT COSTS UNDER TRADITIONAL COSTING...................................................... 217UNIT COSTS UNDER ABC.............................................................................................. 217COMPARING UNIT COSTS............................................................................................ 221

ACTIVITY‐BASED COSTING: A CLOSER LOOK......................................................... 224BENEFITS OF ABC............................................................................................................ 224LIMITATIONS OF ABC.................................................................................................... 225WHEN TO SWITCH TO ABC.......................................................................................... 226VALUE‐ADDED VERSUS NONVALUE‐ADDED ACTIVITIES................................ 226

ACTIVITY‐BASED COSTING IN SERVICE INDUSTRIES......................................... 228

Managerial AccountingTable of Contents

iv

TRADITIONAL COSTING EXAMPLE.......................................................................... 229ACTIVITY‐BASED COSTING EXAMPLE..................................................................... 230

JUST‐IN‐TIME PROCESSING............................................................................................ 232OBJECTIVE OF JIT PROCESSING.................................................................................. 233ELEMENTS OF JIT PROCESSING.................................................................................. 233BENEFITS OF JIT PROCESSING..................................................................................... 234

APPENDIX 4A HIERARCHY OF ACTIVITY LEVELS................................................... 238SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 4A........................................... 241GLOSSARY.............................................................................................................................. 280

CHAPTER 5COST BEHAVIOR ANALYSIS............................................................................................ 287

VARIABLE COSTS............................................................................................................ 288FIXED COSTS..................................................................................................................... 289RELEVANT RANGE......................................................................................................... 290MIXED COSTS.................................................................................................................... 292IMPORTANCE OF IDENTIFYING VARIABLE AND FIXED COSTS....................... 295

COST‐VOLUME‐PROFIT ANALYSIS............................................................................... 296BASIC COMPONENTS..................................................................................................... 297CVP INCOME STATEMENT........................................................................................... 297BREAK‐EVEN ANALYSIS............................................................................................... 301MARGIN OF SAFETY....................................................................................................... 307TARGET NET INCOME................................................................................................... 308CVP AND CHANGES IN THE BUSINESS ENVIRONMENT.................................... 310CVP INCOME STATEMENT REVISITED..................................................................... 313

APPENDIX 5A VARIABLE COSTING.............................................................................. 317EFFECTS OF VARIABLE COSTING ON INCOME........................................................ 318RATIONALE FOR VARIABLE COSTING....................................................................... 320SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 5A........................................... 321GLOSSARY.............................................................................................................................. 344

CHAPTER 6BUDGETING BASICS........................................................................................................... 350

BUDGETING AND ACCOUNTING.............................................................................. 351THE BENEFITS OF BUDGETING................................................................................... 351ESSENTIALS OF EFFECTIVE BUDGETING................................................................. 352LENGTH OF THE BUDGET PERIOD............................................................................ 352THE BUDGETING PROCESS.......................................................................................... 352BUDGETING AND HUMAN BEHAVIOR.................................................................... 353BUDGETING AND LONG‐RANGE PLANNING....................................................... 354THE MASTER BUDGET................................................................................................... 355

PREPARING THE OPERATING BUDGETS.................................................................... 356SALES BUDGET................................................................................................................. 356PRODUCTION BUDGET................................................................................................. 357

Managerial AccountingTable of Contents

v

DIRECT MATERIALS BUDGET...................................................................................... 358DIRECT LABOR BUDGET............................................................................................... 360MANUFACTURING OVERHEAD BUDGET............................................................... 360SELLING AND ADMINISTRATIVE EXPENSE BUDGET.......................................... 361BUDGETED INCOME STATEMENT............................................................................. 363

PREPARING THE FINANCIAL BUDGETS..................................................................... 364CASH BUDGET.................................................................................................................. 364BUDGETED BALANCE SHEET...................................................................................... 368

BUDGETING IN NONMANUFACTURING COMPANIES......................................... 370MERCHANDISERS........................................................................................................... 370SERVICE ENTERPRISES.................................................................................................. 372NOT‐FOR‐PROFIT ORGANIZATIONS......................................................................... 373

GLOSSARY.............................................................................................................................. 407CHAPTER 7

CONCEPT OF BUDGETARY CONTROL......................................................................... 413STATIC BUDGET REPORTS............................................................................................... 414

ILLUSTRATIONS.............................................................................................................. 415USES AND LIMITATIONS.............................................................................................. 416

FLEXIBLE BUDGETS............................................................................................................. 417WHY FLEXIBLE BUDGETS?............................................................................................ 418DEVELOPING THE FLEXIBLE BUDGET...................................................................... 421FLEXIBLE BUDGET—A CASE STUDY......................................................................... 421FLEXIBLE BUDGET REPORTS........................................................................................ 424MANAGEMENT BY EXCEPTION................................................................................. 425

THE CONCEPT OF RESPONSIBILITY ACCOUNTING............................................... 427CONTROLLABLE VERSUS NONCONTROLLABLE REVENUES AND COSTS.... 429RESPONSIBILITY REPORTING SYSTEM..................................................................... 430

TYPES OF RESPONSIBILITY CENTERS.......................................................................... 432RESPONSIBILITY ACCOUNTING FOR COST CENTERS......................................... 433RESPONSIBILITY ACCOUNTING FOR PROFIT CENTERS..................................... 434RESPONSIBILITY ACCOUNTING FOR INVESTMENT CENTERS......................... 437PRINCIPLES OF PERFORMANCE EVALUATION.................................................... 440

APPENDIX 7A RESIDUAL INCOME—ANOTHER PERFORMANCEMEASUREMENT.................................................................................................................... 446RESIDUAL INCOME COMPARED TOROI..................................................................... 447RESIDUAL INCOME WEAKNESS.................................................................................... 448SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 7A........................................... 449GLOSSARY.............................................................................................................................. 485

CHAPTER 8THE NEED FOR STANDARDS........................................................................................... 490

DISTINGUISHING BETWEEN STANDARDS AND BUDGETS............................... 491WHY STANDARD COSTS?............................................................................................. 491

Managerial AccountingTable of Contents

vi

SETTING STANDARD COSTS—A DIFFICULT TASK................................................ 492IDEAL VERSUS NORMAL STANDARDS.................................................................... 493A CASE STUDY................................................................................................................. 493

VARIANCES FROM STANDARDS................................................................................... 498ANALYZING VARIANCES............................................................................................. 499REPORTING VARIANCES.............................................................................................. 513STATEMENT PRESENTATION OF VARIANCES....................................................... 514

APPENDIX 8A STANDARD COST ACCOUNTING SYSTEM................................... 519JOURNAL ENTRIES.............................................................................................................. 520LEDGER ACCOUNTS........................................................................................................... 522SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 8A........................................... 523GLOSSARY.............................................................................................................................. 551

CHAPTER 9MANAGEMENT'S DECISION‐MAKING PROCESS.................................................... 557

INCREMENTAL ANALYSIS APPROACH................................................................... 557HOW INCREMENTAL ANALYSIS WORKS................................................................ 558

TYPES OF INCREMENTAL ANALYSIS........................................................................... 559ACCEPT AN ORDER AT A SPECIAL PRICE............................................................... 560MAKE OR BUY.................................................................................................................. 560SELL OR PROCESS FURTHER........................................................................................ 563RETAIN OR REPLACE EQUIPMENT........................................................................... 566ELIMINATE AN UNPROFITABLE SEGMENT............................................................ 567

SALES MIX.............................................................................................................................. 570BREAK‐EVEN SALES....................................................................................................... 570LIMITED RESOURCES..................................................................................................... 572

OTHER CONSIDERATIONS IN DECISION MAKING............................................... 574QUALITATIVE FACTORS............................................................................................... 574RELATIONSHIP OF INCREMENTAL ANALYSIS AND ACTIVITY‐BASED COSTING.5 7 5

GLOSSARY.............................................................................................................................. 604CHAPTER 10

THE CAPITAL BUDGETING EVALUATION PROCESS............................................. 611CASH FLOW INFORMATION....................................................................................... 612ILLUSTRATIVE DATA..................................................................................................... 613

CASH PAYBACK.................................................................................................................... 614NET PRESENT VALUE METHOD..................................................................................... 615

EQUAL ANNUAL CASH FLOWS.................................................................................. 616UNEQUAL ANNUAL CASH FLOWS........................................................................... 617CHOOSING A DISCOUNT RATE.................................................................................. 618SIMPLIFYING ASSUMPTIONS...................................................................................... 619COMPREHENSIVE EXAMPLE....................................................................................... 621

ADDITIONAL CONSIDERATIONS................................................................................. 622

Managerial AccountingTable of Contents

vii

INTANGIBLE BENEFITS................................................................................................. 622MUTUALLY EXCLUSIVE PROJECTS............................................................................ 624RISK ANALYSIS................................................................................................................ 626POST‐AUDIT OF INVESTMENT PROJECTS................................................................ 627

OTHER CAPITAL BUDGETING TECHNIQUES........................................................... 628INTERNAL RATE OF RETURN METHOD.................................................................. 628COMPARING DISCOUNTED CASH FLOW METHODS.......................................... 630ANNUAL RATE OF RETURN METHOD..................................................................... 631

GLOSSARY.............................................................................................................................. 660CHAPTER 11

SECTION 1 EXTERNAL SALES.......................................................................................... 666PRICING IN A COMPETITIVE MARKET....................................................................... 668COST‐PLUS PRICING.......................................................................................................... 669

LIMITATIONS OF COST‐PLUS PRICING.................................................................... 671TIME AND MATERIAL PRICING..................................................................................... 674SECTION 2 INTERNAL SALES.......................................................................................... 678NEGOTIATED TRANSFER PRICES.................................................................................. 680

NO EXCESS CAPACITY................................................................................................... 680EXCESS CAPACITY.......................................................................................................... 681VARIABLE COSTS............................................................................................................ 682SPECIAL ORDER............................................................................................................... 683SUMMARY OF NEGOTIATED TRANSFER PRICING APPROACH....................... 683

COST‐BASED TRANSFER PRICES................................................................................... 684MARKET‐BASED TRANSFER PRICES............................................................................. 685EFFECT OF OUTSOURCING ON TRANSFER PRICING............................................. 686TRANSFERS BETWEEN DIVISIONS IN DIFFERENT COUNTRIES........................ 686APPENDIX 11A OTHER COST APPROACHES TO PRICING.................................... 691ABSORPTION COST APPROACH.................................................................................... 691CONTRIBUTION (VARIABLE COST) APPROACH..................................................... 694SUMMARY OF STUDY OBJECTIVE FOR APPENDIX 11A......................................... 696COMPREHENSIVE PROBLEM: CHAPTERS 1–11.......................................................... 723GLOSSARY.............................................................................................................................. 730

CHAPTER 12THE STATEMENT OF CASH FLOWS: PURPOSE AND FORMAT............................ 735

PURPOSE OF THE STATEMENT OF CASH FLOWS................................................. 736MEANING OF “CASH FLOWS”.................................................................................... 736CLASSIFICATION OF CASH FLOWS........................................................................... 737SIGNIFICANT NONCASH ACTIVITIES....................................................................... 738FORMAT OF THE STATEMENT OF CASH FLOWS.................................................. 740THE CORPORATE LIFE CYCLE..................................................................................... 741USEFULNESS OF THE STATEMENT OF CASH FLOWS.......................................... 743PREPARING THE STATEMENT OF CASH FLOWS................................................... 744

Managerial AccountingTable of Contents

viii

INDIRECT AND DIRECT METHODS........................................................................... 745SECTION 1 STATEMENT OF CASH FLOWS—INDIRECT METHOD..................... 747FIRST YEAR OF OPERATIONS—2002.............................................................................. 747

STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 748STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 749STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 751STATEMENT OF CASH FLOWS—2002........................................................................ 752

SECOND YEAR OF OPERATIONS—2003........................................................................ 753STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 754STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 754STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 756STATEMENT OF CASH FLOWS—2003........................................................................ 758SUMMARY OF CONVERSION TO NET CASH PROVIDED BY OPERATINGACTIVITIES—INDIRECT METHOD............................................................................. 758

SECTION 1 STATEMENT OF CASH FLOWS—DIRECT METHOD.......................... 762FIRST YEAR OF OPERATIONS—2002.............................................................................. 762

STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 764STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 764STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 769STATEMENT OF CASH FLOWS—2002........................................................................ 770

SECOND YEAR OF OPERATIONS—2003........................................................................ 771STEP 1: DETERMINE THE NET INCREASE/DECREASE IN CASH........................ 772STEP 2: DETERMINE NET CASH PROVIDED/USED BY OPERATINGACTIVITIES........................................................................................................................ 772STEP 3: DETERMINE NET CASH PROVIDED/USED BY INVESTING ANDFINANCING ACTIVITIES............................................................................................... 775STATEMENT OF CASH FLOWS—2003........................................................................ 776

USING CASH FLOWS TO EVALUATE A COMPANY................................................. 779FREE CASH FLOW............................................................................................................ 779CAPITAL EXPENDITURE RATIO.................................................................................. 781ASSESSING LIQUIDITY, SOLVENCY, AND PROFITABILITY USINGCASH FLOWS.................................................................................................................... 782

GLOSSARY.............................................................................................................................. 836CHAPTER 13

EARNING POWER AND IRREGULAR ITEMS.............................................................. 842DISCONTINUED OPERATIONS.................................................................................... 843

Managerial AccountingTable of Contents

ix

EXTRAORDINARY ITEMS.............................................................................................. 844CHANGES IN ACCOUNTING PRINCIPLE................................................................. 847COMPREHENSIVE INCOME......................................................................................... 849

COMPARATIVE ANALYSIS............................................................................................... 849HORIZONTAL ANALYSIS.............................................................................................. 851VERTICAL ANALYSIS..................................................................................................... 855

RATIO ANALYSIS................................................................................................................. 859LIQUIDITY RATIOS.......................................................................................................... 862SOLVENCY RATIOS......................................................................................................... 867PROFITABILITY RATIOS................................................................................................. 870

LIMITATIONS OF FINANCIAL ANALYSIS................................................................... 878ESTIMATES........................................................................................................................ 878COST....ū 878ALTERNATIVE ACCOUNTING METHODS............................................................... 879ATYPICAL DATA............................................................................................................. 879DIVERSIFICATION........................................................................................................... 879

GLOSSARY.............................................................................................................................. 931APPENDIX A

THE ANNUAL REPORT....................................................................................................... 935FINANCIAL HIGHLIGHTS................................................................................................. 936

Corporate Principles ......................................................................................................... 936Corporate Profile ............................................................................................................... 937

LETTER TO THE STOCKHOLDERS................................................................................. 937To Our Shareholders ........................................................................................................ 937Operating Report .............................................................................................................. 939

MANAGEMENT DISCUSSION AND ANALYSIS........................................................ 942Management's Discussion and Analysis of Financial Condition and Results ofOperations .......................................................................................................................... 942

FINANCIAL STATEMENTS AND ACCOMPANYING NOTES................................. 948Notes to Consolidated Financial Statements ................................................................ 953

AUDITOR'S REPORT............................................................................................................ 966Report of Independent Accountants .............................................................................. 967

SUPPLEMENTARY FINANCIAL INFORMATION....................................................... 967APPENDIX BAPPENDIX C

NATURE OF INTEREST....................................................................................................... 977SIMPLE INTEREST............................................................................................................ 978COMPOUND INTEREST................................................................................................. 978

SECTION 1 FUTURE VALUE CONCEPTS....................................................................... 979FUTURE VALUE OF A SINGLE AMOUNT..................................................................... 979FUTURE VALUE OF AN ANNUITY.................................................................................. 982SECTION 2 PRESENT VALUE CONCEPTS..................................................................... 985

Managerial AccountingTable of Contents

x

PRESENT VALUE VARIABLES.......................................................................................... 985PRESENT VALUE OF A SINGLE AMOUNT................................................................... 985PRESENT VALUE OF AN ANNUITY................................................................................ 988TIME PERIODS AND DISCOUNTING............................................................................ 991COMPUTING THE PRESENT VALUES IN A CAPITAL BUDGETINGDECISIONū 991GLOSSARY............................................................................................................................ 1000

APPENDIX DETHICAL BEHAVIOR FOR PRACTITIONERS OF MANAGEMENT ACCOUNTINGAND FINANCIAL MANAGEMENT............................................................................... 1001STANDARDS OF ETHICAL CONDUCT FOR PRACTITIONERS OF MANAGEMENTACCOUNTING AND FINANCIAL MANAGEMENT................................................. 1002

COMPETENCE................................................................................................................ 1002CONFIDENTIALITY....................................................................................................... 1002INTEGRITY....................................................................................................................... 1003OBJECTIVITY................................................................................................................... 1003RESOLUTION OF ETHICAL CONFLICT................................................................... 1003

AFTERWORDCASE‐1....ū 1007CARD‐MART SWIMS IN THE DOT‐COM SEA: JOB ORDER COSTING............. 1007

THE BUSINESS SITUATION......................................................................................... 1007CASE‐2....ū 1010CARD‐MART SWIMS IN THE DOT‐COM SEA: ACTIVITY‐BASED COSTING.. 1010

THE BUSINESS SITUATION......................................................................................... 1011CASE‐3....ū 1016CARD‐MART SWIMS IN THE DOT‐COM SEA: CAPITAL BUDGETING............ 1016

THE BUSINESS SITUATION......................................................................................... 1016CASE‐4....ū 1019CARD‐MART SWIMS IN THE DOT‐COM SEA: TRANSFER PRICING ISSUES. 1019

THE BUSINESS SITUATION......................................................................................... 1019CASE‐5....ū 1022RICHLAND CIRCULAR CLUB PRO RODEO ROUNDUP......................................... 1022

THE BUSINESS SITUATION......................................................................................... 1022

Managerial AccountingTable of Contents

xi

Managerial AccountingTable of Contents

xii

Chapter 6

Budgetary Planning

Navigator

• Scan Study Objectives

• Read Feature Story

• Read Preview

• Read text and answer Before You Go On

p.235 □ p.246 □ p.249 □

• Work Using the Decision Toolkit

• Review Summary of Study Objectives

• Work Demonstration Problem

• Answer Self‐Study Questions

• Complete Assignments

Managerial AccountingChapter 6

Page 347

STUDY OBJECTIVES

After studying this chapter, you should be able to:

1. Indicate the benefits of budgeting.

2. State the essentials of effective budgeting.

3. Identify the budgets that comprise the master budget.

4. Describe the sources for preparing the budgeted income statement.

5. Explain the principal sections of a cash budget.

6. Indicate the applicability of budgeting in nonmanufacturing companies.

Managerial AccountingChapter 6

Page 348

Feature Story

THE NEXT AMAZON.COM? WELL, ALMOST

The bursting of the dot‐com bubble resulted in countless stories of dot‐com failures. Manyof these ventures were half‐baked, get‐rich‐quick schemes, rarely based on sound businesspractices. Initially they saw money flowing in faster than they knew what to do with—whichwas precisely the problem. Without proper planning and budgeting, much of the moneywent to waste. In some cases, failure was actually brought on by rapid, uncontrolled growth.

One such example was the Web site www. Positively‐You.com, an online discount bookseller.One of the co‐founders, Lyle Bowline, had never run a business. However, his experienceas an assistant director of an entrepreneurial center had provided him with knowledge aboutthe do's and don'ts of small business. To minimize costs, he started the company off smalland simple. He invested $5,000 in computer equipment and ran the business out of hisbasement. In the early months, even though sales were only about $2,000 a month, thecompany actually made a profit because it kept its costs low (a feat few other dot‐coms couldboast of).

Things changed dramatically when the company received national publicity in the financialpress. Suddenly the company's sales increased to $50,000 a month—fully 25 times the previouslevel. The “simple” little business suddenly needed a business plan, a strategic plan, and abudget. It needed to rent office space and to hire employees. Initially, members of a localbook club donated time to help meet the sudden demand. But quickly the number of paid

Managerial AccountingChapter 6

Page 349

employees ballooned. The sudden growth necessitated detailed planning and budgeting.The need for a proper budget was accentuated by the fact that the company's gross profitwas only 16 cents on each dollar of goods sold. This meant that after paying for its inventory,the company had only 16 cents of every dollar to cover its remaining operating costs.

Unfortunately, the company never got things under control. Within a few months, sales hadplummeted to $12,000 per month. At this level of sales the company could not meet themountain of monthly expenses that it had accumulated in trying to grow. Ironically, thecompany's sudden success, and the turmoil it created, appears to have been what eventuallycaused the company to fail.

PREVIEW OF CHAPTER 6

As the Feature Story about the Positively‐You.com indicates, budgeting is critical to financialwell‐being. As a student, you budget your study time and your money. Families budgetincome and expenses. Governmental agencies budget revenues and expenditures. Businessenterprises use budgets in planning and controlling their operations.

Our primary focus in this chapter is budgeting—specifically, how budgeting is used as aplanning tool by management. Through budgeting, it should be possible for managementto maintain enough cash to pay creditors, to have sufficient raw materials to meet productionrequirements, and to have adequate finished goods to meet expected sales.

The content and organization of Chapter 6 are as follows.

BUDGETING BASICS

One of management's major responsibilities is planning. As explained in Chapter 1, planning isthe process of establishing enterprise‐wide objectives. A successful organization makes both

Managerial AccountingChapter 6

Page 350

long‐term and short‐term plans. These plans set forth the objectives of the company and theproposed way of accomplishing them.

A budget is a formal written statement of management's plans for a specified future time period,expressed in financial terms. It normally represents the primary method of communicatingagreed‐upon objectives throughout the organization. Once adopted, a budget becomes animportant basis for evaluating performance. It promotes efficiency and serves as a deterrent towaste and inefficiency. We consider the role of budgeting as a control device in Chapter 7.

BUDGETING AND ACCOUNTING

Accounting information makes major contributions to the budgeting process. From the accountingrecords, historical data on revenues, costs, and expenses can be obtained. These data are helpfulin formulating future budget goals.

Normally, accountants have the responsibility for expressing management's budgeting goals infinancial terms. In this role, they translate management's plans and communicate the budget toall areas of responsibility. Accountants also prepare periodic budget reports that provide thebasis for measuring performance and comparing actual results with planned objectives. Thebudget itself, and the administration of the budget, however, are entirely managementresponsibilities.

THE BENEFITS OF BUDGETING

The primary benefits of budgeting are:

1. It requires all levels of management to plan ahead and to formalize their goals on arecurring basis.

2. It provides definite objectives for evaluating performance at each level of responsibility.

3. It creates an early warning system for potential problems. With early warning,management has time to make changes before things get out of hand.

4. It facilitates the coordination of activitieswithin the business. It does this by correlatingthe goals of each segment with overall company objectives. Thus, production and salespromotion can be integrated with expected sales.

5. It results in greater management awareness of the entity's overall operations and theimpact on operations of external factors, such as economic trends.

6. It motivates personnel throughout the organization to meet planned objectives.

A budget is an aid to management; it is not a substitute for management. A budget cannot operateor enforce itself. The benefits of budgeting will be realized only when budgets are carefullyprepared and properly administered by management.

Managerial AccountingChapter 6

Page 351

ESSENTIALS OF EFFECTIVE BUDGETING

Effective budgeting depends on a sound organizational structure. In such a structure, authorityand responsibility for all phases of operations are clearly defined. Budgets based on researchand analysis should result in realistic goals that will contribute to the growth and profitabilityof a company. And, the effectiveness of a budget program is directly related to its acceptance byall levels of management.

Once the budget has been adopted, it should be an important tool for evaluating performance.Variations between actual and expected results should be systematically and periodically reviewedto determine their cause(s). However, individuals should not be held responsible for variationsthat are beyond their control.

LENGTH OF THE BUDGET PERIOD

The budget period is not necessarily one year in length. A budget may be prepared for anyperiod of time. Various factors influence the length of the budget period. These factors includethe type of budget, the nature of the organization, the need for periodic appraisal, and prevailingbusiness conditions. For example, cash may be budgeted monthly, whereas a plant expansionbudget may cover a ten‐year period.

The budget period should be long enough to provide an attainable goal under normal businessconditions. Ideally, the time period should minimize the impact of seasonal or cyclical fluctuations.On the other hand, the budget period should not be so long that reliable estimates are impossible.

The most common budget period is one year. The annual budget, in turn, is often supplementedby monthly and quarterly budgets. Many companies use continuous twelve‐month budgets.These budgets drop the month just ended and add a future month. One advantage of continuousbudgeting is that it keeps management planning a full year ahead.

THE BUDGETING PROCESS

The development of the budget for the coming year generally starts several months before theend of the current year. The budgeting process usually begins with the collection of data fromeach organizational unit of the company. Past performance is often the starting point from whichfuture budget goals are formulated.

The budget is developed within the framework of a sales forecast. This forecast shows potentialsales for the industry and the company's expected share of such sales. Sales forecasting involvesa consideration of various factors: (1) general economic conditions, (2) industry trends, (3) marketresearch studies, (4) anticipated advertising and promotion, (5) previous market share, (6) changesin prices, and (7) technological developments. The input of sales personnel and top managementare essential to the sales forecast.

Managerial AccountingChapter 6

Page 352

In small companies like Positively‐You.com, the budgeting process is often informal. In largercompanies, responsibility for coordinating the preparation of the budget is assigned to a budgetcommittee. The committee ordinarily includes the president, treasurer, chief accountant(controller), and management personnel from each of the major areas of the company, such assales, production, and research. The budget committee serves as a review board where managerscan defend their budget goals and requests. Differences are reviewed, modified if necessary, andreconciled. The budget is then put in its final form by the budget committee, approved, anddistributed.

Management Perspective

A recent study by Willard & Shullman Group Ltd. found that fewer than 14 percent ofbusinesses with fewer than 500 employees do an annual budget or have a written businessplan. In all, nearly 60 percent of these businesses have no plans on paper at all. For manysmall businesses the basic assumption is that, “As long as I sell as much as I can, and keepmy employees paid, I'm doing OK.” A few small business owners even say that they see noneed for budgeting and planning. Most small business owners, though, say that theyunderstand that budgeting and planning is critical for survival and growth. But given thelong hours that they already work addressing day‐to‐day challenges, they also say that theyare “just too busy to plan for the future.”

BUDGETING AND HUMAN BEHAVIOR

A budget can have a significant impact on human behavior. It may inspire a manager to higherlevels of performance. Or, it may discourage additional effort and pull down the morale of amanager. Why do these diverse effects occur? The answer is found in how the budget is developedand administered.

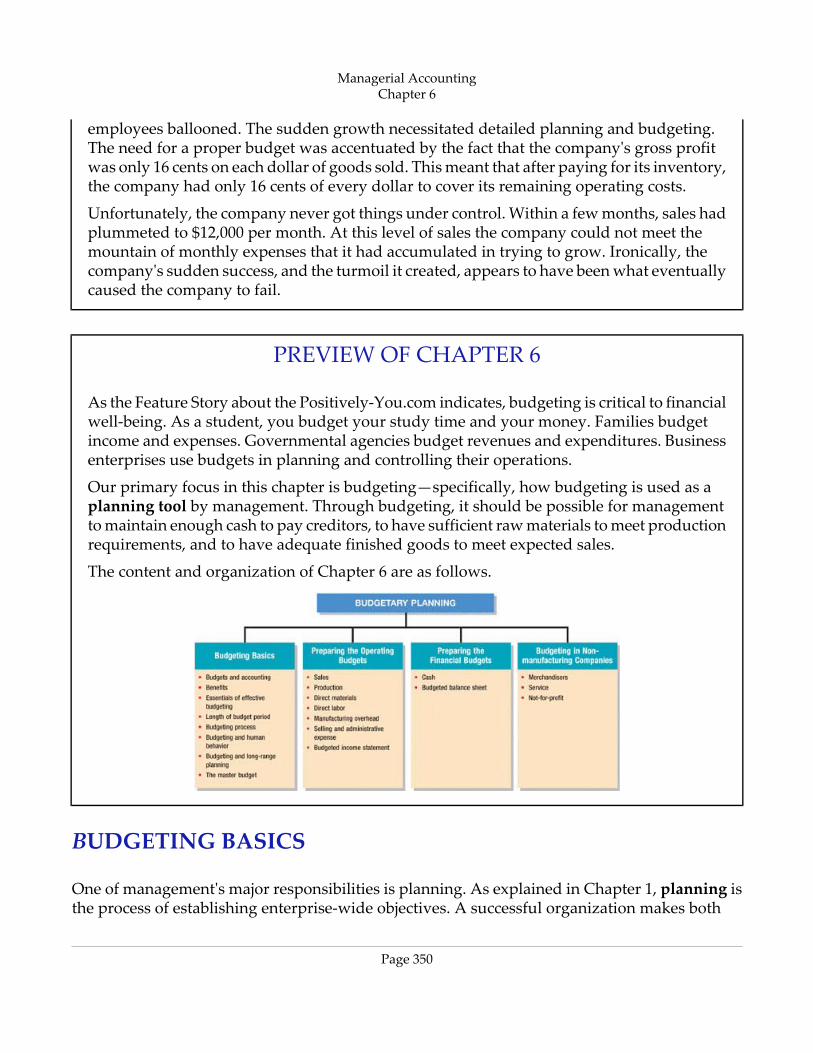

In developing the budget, each level of management should be invited to participate. The overallgoal is to reach agreement on a budget that the manager considers fair and achievable. Whenthis objective is met, the budget will have a positive effect on the manager. In contrast, if themanager views the budget as being unfair and unrealistic, he or she may feel discouraged anduncommitted to the budget goals. The risk of having unrealistic budgets is generally greaterwhen the budget is developed from top management down to lower management than viceversa. Illustration 1 graphically displays the appropriate flow of budget data from bottom to topin an organization.

Managerial AccountingChapter 6

Page 353

Flow of budget data from lower levels of management to top levels

Administering the budget relates to how the budget is used by top management. As explainedearlier, the budget should have the complete support of top management. The budget also shouldbe an important basis for evaluating performance. The effect of an evaluation will be positivewhen top management tempers criticism with advice and assistance. In contrast, a manager islikely to respond negatively if the budget is used exclusively to assess blame.

A budget may be used improperly as a pressure device to force improved performance. Or, itcan be used as a positive aid in achieving projected goals. In sum, a budget can become a manager'sfriend or a foe.

BUDGETING AND LONG-RANGE PLANNING

In business, you may hear talk about the need for long‐range planning. Budgeting and long‐rangeplanning are not the same. One important difference is the time period involved. The maximumlength of a budget is usually one year, and budgets are often prepared for shorter periods oftime, such as a month or a quarter. In contrast, long‐range planning usually encompasses a periodof at least five years.

A second significant difference is in emphasis. Budgeting focuses on achieving specific short‐termgoals, such as meeting annual profit objectives. Long‐range planning, on the other hand, identifieslong‐term goals, selects strategies to achieve those goals, and develops policies and plans toimplement the strategies. In long‐range planning, management also considers anticipated trendsin the economic and political environment and how the company should cope with them.

The final difference between budgeting and long‐range planning pertains to the amount of detailpresented. Budgets, as you will see in this chapter, can be very detailed. Long‐range plans containconsiderably less detail. The data in long‐range plans are intended more for a review of progresstoward long‐term goals than as a basis of control for achieving specific results. The primaryobjective of long‐range planning is to develop the best strategy to maximize the company'sperformance over an extended future period.

Managerial AccountingChapter 6

Page 354

THE MASTER BUDGET

The term “budget” is actually a shorthand term to describe a variety of budget documents. Allof these documents are combined into a master budget. The master budget is a set of interrelatedbudgets that constitutes a plan of action for a specified time period. The individual budgetsincluded in a master budget are pictured in Illustration 2.

Components of the master budget

As the illustration shows, the master budget contains two classes of budgets. Operating budgetsare the individual budgets that result in the preparation of the budgeted income statement. Thesebudgets establish goals for the company's sales and production personnel. In contrast, financialbudgets are the capital expenditure budget, the cash budget, and the budgeted balance sheet.These budgets focus primarily on the cash resources needed to fund expected operations andplanned capital expenditures.

The master budget is prepared in the sequence shown in Illustration 2. The operating budgetsare developed first, beginning with the sales budget. Then the financial budgets are prepared.

Managerial AccountingChapter 6

Page 355

We will explain and illustrate each budget shown in Illustration 2 except the capital expenditurebudget. This budget is discussed under the topic Capital Budgeting in Chapter 10.

Before You Go On...

Review It

1. What are the benefits of budgeting?

2. What are the factors essential to effective budgeting?

3. How does the budget process work?

4. How does budgeting differ from long‐range planning?

5. What is a master budget?

PREPARING THE OPERATING BUDGETS

A case study of Hayes Company will be used in preparing the operating budgets. Hayesmanufactures and sells a single product, Kitchen‐mate. The budgets will be prepared by quartersfor the year ending December 31, 2002. Hayes Company begins its annual budgeting process onSeptember 1, 2001, and it completes the budget for 2002 by December 1, 2001.

SALES BUDGET

As shown in the master budget in Illustration 2, the sales budget is the first budget prepared.Each of the other budgets depends on the sales budget. The sales budget is derived from thesales forecast. It represents management's best estimate of sales revenue for the budget period.An inaccurate sales budget may adversely affect net income. For example, an overly optimisticsales budget may result in excessive inventories that may have to be sold at reduced prices. Incontrast, an unduly conservative budget may result in loss of sales revenue due to inventoryshortages.

The sales budget is prepared by multiplying the expected unit sales volume for each product byits anticipated unit selling price. For Hayes Company, sales volume is expected to be 3,000 unitsin the first quarter, with 500‐unit increments in each succeeding quarter. Based on a sales priceof $60 per unit, the sales budget for the year, by quarters, is shown in Illustration 3. Somecompanies classify the anticipated sales revenue as cash or credit sales and by geographicalregions, territories, or salespersons.

Managerial AccountingChapter 6

Page 356

Sales budget

PRODUCTION BUDGET

The production budget shows the units that must be produced to meet anticipated sales.Production requirements are determined from the following formula.1

Production requirements formula

A realistic estimate of ending inventory is essential in scheduling production requirements.Excessive inventories in one quarter may lead to cutbacks in production and employee layoffsin a subsequent quarter. On the other hand, inadequate inventories may result either in addedcosts for overtime work or in lost sales. Hayes Company believes it can meet future salesrequirements by maintaining an ending inventory equal to 20 percent of the next quarter'sbudgeted sales volume. For example, the ending finished goods inventory for the first quarteris 700 units (20% × anticipated second‐quarter sales of 3,500 units). The production budget isshown in Illustration 5.

Managerial AccountingChapter 6

Page 357

Production budget

The production budget, in turn, provides the basis for determining the budgeted costs for eachmanufacturing cost element, as explained in the following pages.

Management Perspective

Wrong move, wrong time, poor planning. When Fruit of the Loom Inc. saw underwear andapparel sales slowing, it cut back production sharply. Too sharply, in fact: almost overnight,demand soared. Caught with its shorts down, the company hired back thousands of workersand frantically increased production. The mistimed production cuts contributed to a 43percent fall in first‐quarter profits. For the year, Fruit stood to lose $200 million in sales, andanalysts expected an 11 percent drop in profits for the year.

DIRECT MATERIALS BUDGET

The direct materials budget shows both the quantity and cost of direct materials to be purchased.The quantities of direct materials are derived from the following formula.

Managerial AccountingChapter 6

Page 358

Formula for direct materials quantities

The budgeted cost of direct materials to be purchased is then computed by multiplying therequired units of direct materials by the anticipated cost per unit.

The desired ending inventory is again a key component in the budgeting process. For example,inadequate inventories could result in temporary shutdowns of production. Because of its closeproximity to suppliers, Hayes Company has found that an ending inventory of raw materialsequal to 10 percent of the next quarter's production requirements is sufficient. The manufactureof each Kitchen‐mate requires 2 pounds of raw materials, and the expected cost per pound is $4.The direct materials budget is shown in Illustration 7.

Direct materials budget

Managerial AccountingChapter 6

Page 359

Management Perspective

The successful manufacturers of the twenty‐first century will be fully computerized. A crucialstep on the way is material requirements planning (MRP) systems. Early MRP systemsaccepted a sales forecast and computed how much materials, inventory, people, andmachinery a company needed to manufacture the product. Current MRP systems link thecompany's manufacturing resource planning with its financial management. This newcapability creates a powerful system of control over the entire business planning and operatingprocess. With MRP, management can make decisions on facts rather than on “hunches” and“instinct.”

DIRECT LABOR BUDGET

Like the direct materials budget, the direct labor budget contains the quantity (hours) and costof direct labor necessary to meet production requirements. Direct labor hours are determinedfrom the production budget. At Hayes Company, two hours of direct labor are required toproduce each unit of finished goods. The anticipated hourly wage rate is $10. These data areshown in Illustration 8. The direct labor budget is critical in maintaining a labor force that canmeet the expected levels of production.

Direct labor budget

MANUFACTURING OVERHEAD BUDGET

The manufacturing overhead budget shows the expected manufacturing overhead costs for thebudget period. As shown in Illustration 9, this budget distinguishes between variable and fixedoverhead costs.Hayes Company expects variable costs to fluctuate with production volume onthe basis of the following rates per direct labor hour: indirect materials $1.00, indirect labor $1.40,

Managerial AccountingChapter 6

Page 360

utilities $0.40, and maintenance $0.20. Thus, for 6,200 direct labor hours, budgeted indirectmaterials are $6,200 (6,200 × $1), and budgeted indirect labor is $8,680 (6,200 × $1.40). Hayes alsorecognizes that some maintenance is fixed. The amounts reported for fixed costs are assumed.

Manufacturing overhead budget

At Hayes Company, overhead is applied to production on the basis of direct labor hours. Thus,as shown in Illustration 9, the annual rate is $8 per hour ($246,400 ÷ 30,800).

SELLING AND ADMINISTRATIVE EXPENSE BUDGET

Hayes Company combines its operating expenses into one budget, the selling and administrativeexpense budget. This budget projects anticipated selling and administrative expenses for thebudget period. In this budget, as in the preceding one, expenses are classified as either variableor fixed. In this case, the variable expense rates per unit of sales are sales commissions $3.00 andfreightout $1.00. Variable expenses per quarter are based on the unit sales from the sales budget(Illustration 3). For example, sales in the first quarter are expected to be 3,000 units. Thus, SalesCommissions Expense is $9,000 (3,000 × $3), and Freight‐out is $3,000 (3,000 × $1). Fixed expensesare based on assumed data. The selling and administrative expense budget is shown in Illustration10.

Managerial AccountingChapter 6

Page 361

Selling and administrative expense budget

e‐Business Insight

Good budgeting depends on good information. And good information is what e‐businessis all about. As manufacturers, suppliers, and customers become electronically linked, eachbenefits by being better informed. Dell Computer not only is directly linked to Solectron,one of its main suppliers, but also to Texas Instruments, one of the main suppliers of partsto Solectron. This linking takes a lot of guesswork out of planning and budgeting for allthree companies.

To further improve planning and budgeting, Dell hopes that some day everyone in itsindustry will anonymously provide their up‐to‐the‐minute production and sales informationat a central, electronic exchange. A centralized database such as this would provide valuableinformation about the supply and demand of computer goods in the marketplace. Thisinformation might dramatically improve sales projections, leading to significantimprovements in the budgeting process.Source: “E‐Management,” The Economist, November 11, 2000.

Managerial AccountingChapter 6

Page 362

BUDGETED INCOME STATEMENT

The budgeted income statement is the important end‐product of the operating budgets. Thisbudget indicates the expected profitability of operations for the budget period. The budgetedincome statement provides the basis for evaluating company performance.

As you would expect, this budget is prepared from the various operating budgets. For example,to find the cost of goods sold, it is first necessary to determine the total unit cost of producingone Kitchen‐mate, as follows.

Computation of total unit cost

Cost of goods sold can then be determined by multiplying the units sold by the unit cost. ForHayes Company, budgeted cost of goods sold is $660,000 (15,000 × $44). All data for the statementare obtained from the individual operating budgets except the following: (1) interest expense isexpected to be $100, and (2) income taxes are estimated to be $12,000. The budgeted incomestatement is shown in Illustration 12.

Budgeted income statement

Managerial AccountingChapter 6

Page 363

PREPARING THE FINANCIAL BUDGETS

As shown in Illustration 2, the financial budgets consist of the capital expenditure budget, thecash budget, and the budgeted balance sheet. The capital expenditure budget is discussed inChapter 10; the other budgets are explained in the following sections.

CASH BUDGET

The cash budget shows anticipated cash flows. Because cash is so vital, this budget is consideredto be the most important output in preparing financial budgets. The cash budget contains threesections (cash receipts, cash disbursements, and financing) and the beginning and ending cashbalances, as shown in Illustration 13.

Basic form of a cash budget

The cash receipts section includes expected receipts from the company's principal source(s) ofrevenue. These are usually cash sales and collections from customers on credit sales. This sectionalso shows anticipated receipts of interest and dividends, and proceeds from planned sales ofinvestments, plant assets, and the company's capital stock.

The cash disbursements section shows expected cash payments. Such payments include directmaterials, direct labor, manufacturing overhead, and selling and administrative expenses. Thissection also includes projected payments for income taxes, dividends, investments, and plantassets.

Managerial AccountingChapter 6

Page 364

The financing section shows expected borrowings and the repayment of the borrowed fundsplus interest. This section is needed when there is a cash deficiency or when the cash balance isbelow management's minimum required balance.

Data in the cash budget must be prepared in sequence. The ending cash balance of one periodbecomes the beginning cash balance for the next period. Data for preparing the cash budget areobtained from other budgets and from information provided by management. In practice, cashbudgets are often prepared for the year on a monthly basis.

To minimize detail, we will assume that Hayes Company prepares an annual cash budget byquarters. The cash budget for Hayes Company is based on the following assumptions.

1. The January 1, 2002, cash balance is expected to be $38,000.

2. Sales (Illustration 3): 60 percent are collected in the quarter sold and 40 percent arecollected in the following quarter. Accounts receivable of $60,000 at December 31, 2001,are expected to be collected in full in the first quarter of 2002.

3. Short‐term investments are expected to be sold for $2,000 cash in the first quarter.

4. Direct materials (Illustration 7): 50 percent are paid in the quarter purchased and 50percent are paid in the following quarter. Accounts payable of $10,600 at December31, 2001, are expected to be paid in full in the first quarter of 2002.

5. Direct labor (Illustration 8): 100 percent is paid in the quarter incurred.

6. Manufacturing overhead (Illustration 9) and selling and administrative expenses(Illustration 10): All items except depreciation are paid in the quarter incurred.

7. Management plans to purchase a truck in the second quarter for $10,000 cash.

8. Hayes makes equal quarterly payments of its estimated annual income taxes.

9. Loans are repaid in the earliest quarter in which there is sufficient cash (i.e., when thecash on hand exceeds the $15,000 minimum required balance).

In preparing the cash budget, it is useful to prepare schedules for collections from customers(assumption No. 2, above) and cash payments for direct materials (assumption No. 4, above).The schedules are shown in Illustrations 14 and 15.

Managerial AccountingChapter 6

Page 365

Collections from customers

Payments for direct materials

The cash budget for Hayes Company is shown in Illustration 16. The budget indicates that $3,000of financing will be needed in the second quarter to maintain a minimum cash balance of $15,000.Since there is an excess of available cash over disbursements of $22,500 at the end of the thirdquarter, the borrowing, plus $100 interest, is repaid in this quarter.

Managerial AccountingChapter 6

Page 366

Cash budget

Management Perspective

Douglas Roberson, president of Atlantic Network, woke up one morning to find that hiscompany was out of cash. At that point, Roberson realized that managing cash flow isdifferent from simply accumulating sales. He says: “If you don't do serious projections abouthow much cash you will need to handle sales—and how long it will take to collect oninvoices—you can end up out of business no matter how fast you are growing.” In fact,Roberson says, fast growth makes cash flow problems worse because the company can bespending cash on supplies and payroll at an accelerated pace while waiting 45 days or longerto collect receivables.

A cash budget contributes to more effective cash management. It can show managers whenadditional financing will be necessary well before the actual need arises. And, it can indicatewhen excess cash will be available for investments or other purposes.

Managerial AccountingChapter 6

Page 367

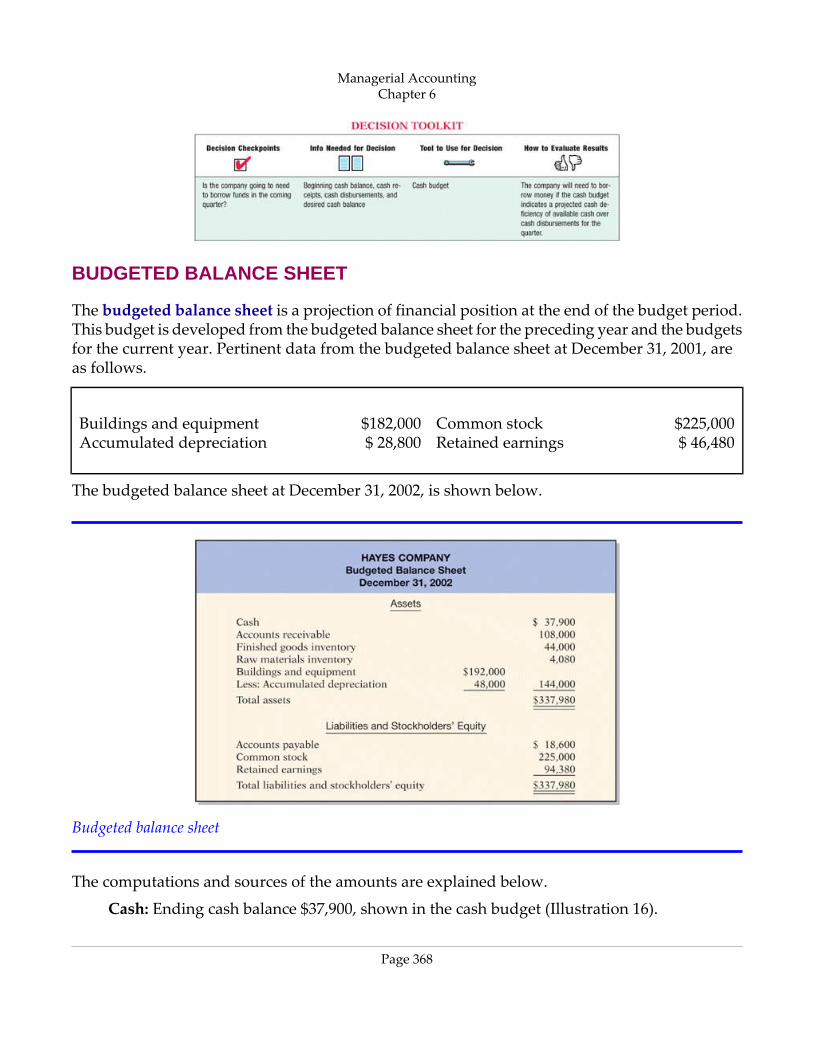

BUDGETED BALANCE SHEET

The budgeted balance sheet is a projection of financial position at the end of the budget period.This budget is developed from the budgeted balance sheet for the preceding year and the budgetsfor the current year. Pertinent data from the budgeted balance sheet at December 31, 2001, areas follows.

$225,000Common stock$182,000Buildings and equipment$ 46,480Retained earnings$ 28,800Accumulated depreciation

The budgeted balance sheet at December 31, 2002, is shown below.

Budgeted balance sheet

The computations and sources of the amounts are explained below.

Cash: Ending cash balance $37,900, shown in the cash budget (Illustration 16).

Managerial AccountingChapter 6

Page 368

Accounts receivable: 40 percent of fourth‐quarter sales $270,000, shown in the schedule ofexpected collections from customers (Illustration 14).

Finished goods inventory:Desired ending inventory 1,000 units, shown in the productionbudget (Illustration 5) times the total unit cost $44 (shown in Illustration 11).

Raw materials inventory:Desired ending inventory 1,020 pounds, times the cost per pound$4, shown in the direct materials budget (Illustration 7).

Buildings and equipment:December 31, 2001, balance $182,000, plus purchase of truck for$10,000.

Accumulated depreciation: December 31, 2001, balance $28,800, plus $15,200 depreciationshown in manufacturing overhead budget (Illustration 9) and $4,000 depreciation shownin selling and administrative expense budget (Illustration 10).

Accounts payable: 50 percent of fourth‐quarter purchases $37,200, shown in schedule ofexpected payments for direct materials (Illustration 15).

Common stock: Unchanged from the beginning of the year.

Retained earnings:December 31, 2001, balance $46,480, plus net income $47,900, shown inbudgeted income statement (Illustration 12).

Management Perspective

After the budgeting data are entered into the computer, the various budgets (sales, cash,etc.) can be prepared, as well as the budgeted financial statements. Management can alsomanipulate the budgets in “what if” (sensitivity) analyses based on different hypotheticalassumptions. For example, suppose that sales were budgeted to be 10 percent higher in thecoming quarter. What impact would the change have on the rest of the budgeting processand the financing needs of the business? The computer can quickly “play out” the impactof the various assumptions on the budgets. Armed with these analyses, management canmake more informed decisions about the impact of various projects. They also can anticipatefuture problems and business opportunities. Budgeting is one of the top uses of electronicspreadsheets. Template versions of every one of the Hayes Company budgets shown in thischapter could easily be prepared.

Managerial AccountingChapter 6

Page 369

Before You Go On...

Review It

1. What are the two classifications of the individual budgets in the master budget?

2. What is the sequence for preparing the budgets that comprise the operating budgets?

3. Identify some of the source documents that would be used in preparing each of theoperating budgets.

4. What are the three principal sections of the cash budget?

Do It

1. In Martian Company, management wants to maintain a minimum monthly cashbalance of $15,000. At the beginning of March, the cash balance is $16,500, expectedcash receipts for March are $210,000, and cash disbursements are expected to be$220,000. How much cash, if any, must be borrowed to maintain the desired minimummonthly balance?

Action Plan

• Write down the basic form of the cash budget, starting with the beginning cashbalance, adding cash receipts for the period, deducting cash disbursements,and identifying the needed financing to achieve the desired minimum endingcash balance.

• Insert the data given into the outlined form of the cash budget.

Related exercise material: BE6‐9 and E6‐9.

BUDGETING IN NONMANUFACTURING COMPANIES

Budgeting is not limited to manufacturers. Budgets may also be used by merchandisers, serviceenterprises, and not‐for‐profit organizations.

MERCHANDISERS

As in manufacturing operations, the sales budget for a merchandiser is both the starting pointand the key factor in the development of the master budget. The major differences between themaster budgets of a merchandiser and a manufacturer are these: (1) A merchandiser uses amerchandise purchases budget instead of a production budget. (2) A merchandiser does not

Managerial AccountingChapter 6

Page 370

use the manufacturing budgets (direct materials, direct labor, and manufacturing overhead).The merchandise purchases budget shows the estimated cost of goods to be purchased to meetexpected sales. The formula for determining budgeted merchandise purchases is:

Merchandise purchases formula

To illustrate, assume that the budget committee of Lima Company is preparing the merchandisepurchases budget for July. It estimates that budgeted sales will be $300,000 in July and $320,000in August. Cost of goods sold is expected to be 70 percent of sales. The company's desired endinginventory is 30 percent of the following month's cost of goods sold. Required merchandisepurchases for July are $214,200, computed as follows.

Computation of required merchandise purchases

Managerial AccountingChapter 6

Page 371

When a merchandiser is departmentalized, separate budgets are prepared for each department.For example, a grocery store may start by preparing sales budgets and purchases budgets foreach of its major departments, such as meats, dairy, and produce. These budgets are then combinedinto a master budget for the store. When a retailer has branch stores, separate master budgetsare prepared for each store. Then these budgets are incorporated into master budgets for thecompany as a whole.

SERVICE ENTERPRISES

In a service enterprise, such as a public accounting firm, a law office, or a medical practice, thecritical factor in budgeting is coordinating professional staff needs with anticipated services.If a firm is overstaffed, several problems may result: (1) Labor costs will be disproportionatelyhigh. (2) Profits will be lower because of the additional salaries. (3) Staff turnover may increasebecause of lack of challenging work. In contrast, if an enterprise is understaffed, revenue maybe lost because existing and prospective client needs for service cannot be met. Also, professionalstaff may seek other jobs because of excessive work loads.

Budget data for service revenue may be obtained from expected output or expected input. Whenoutput is used, it is necessary to determine the expected billings of clients for services rendered.In a public accounting firm, for example, output would be the sum of its billings in auditing, tax,and consulting services. When input data are used, each professional staff member is requiredto project his or her billable time. Billing rates are then applied to billable time to produce expectedservice revenue.

Managerial AccountingChapter 6

Page 372

Service Company Perspective

Lucy Carter, managing partner of a small CPA firm in Nashville, uses formal budgets as theprincipal tool for keeping cash flow on an even keel throughout the year. The firm budgetsannually for both revenues and expenses on a month‐by‐month basis. For example, therevenue budget is derived from chargeable‐hour goals set by the staff. The firm sets athreshold of 1,800 hours for each staff member and 1,700 hours for each manager. Eachmonth the budget is compared with the financial statements, and adjustments are made ifnecessary.

NOT-FOR-PROFIT ORGANIZATIONS

Budgeting is just as important for not‐for‐profit organizations as for profit‐oriented enterprises.The budget process, however, is significantly different. In most cases not‐for‐profit entities budgeton the basis of cash flows (expenditures and receipts), rather than on a revenue and expensebasis. Further, the starting point in the process is usually expenditures, not receipts. For thenot‐for‐profit entity, management's task generally is to find the receipts needed to support theplanned expenditures. The activity index is also likely to be significantly different. For example,in a not‐for‐profit entity, such as a university, budgeted faculty positions may be based on full‐timeequivalent students or credit hours expected to be taught in a department.

For some governmental units, the budget must be approved by voters. In other cases, such asstate governments and the federal government, legislative approval is required. After the budgetis adopted, it must be strictly followed. Overspending is often illegal. In governmental budgets,authorizations tend to be on a line‐by‐line basis. That is, the budget for a municipality may havea specified authorization for police and fire protection, garbage collection, street paving, and soon. The line‐item authorization of governmental budgets significantly limits the amount ofdiscretion management can exercise. The city manager often cannot use savings from one lineitem, such as street paving, to cover increased spending in another line item, such as snowremoval.

Before You Go On...

Review It

1. What is the formula for computing required merchandise purchases?

2. How does budgeting in service and not‐for‐profit organizations differ from budgetingfor manufacturers and merchandisers?

Managerial AccountingChapter 6

Page 373

USING THE DECISION TOOLKIT

The University of Wisconsin and its subunits must prepare budgets. One unique subunit ofthe University of Wisconsin is Babcock Ice Cream, a functioning producer of dairy products(and famous, at least on campus, for its delicious ice cream).

Assume that Babcock Ice Cream prepares monthly cash budgets. Relevant data from assumedoperating budgets for 2002 are:

FebruaryJanuary$412,000$460,000Sales210,000185,000Direct materials purchases85,00070,000Direct labor65,00050,000Manufacturing overhead95,00085,000Selling and administrative

expenses

Babcock sells 50% of its ice cream in its shops on campus, as well as selling to local stores.Collections from local stores are expected to be 50% in the month of sale, and 50% in themonth following sale. Sixty percent (60%) of direct materials purchases are paid in cash inthe month of purchase, and the balance due is paid in the month following the purchase.All other items above are paid in the month incurred. (Depreciation has been excluded frommanufacturing overhead and selling and administrative expenses.)

Other data:

1. Sales: November 2001, $370,000; December 2001, $320,000

2. Purchases of direct materials: December 2001, $175,000

3. Other receipts:

January—Donation received, $2,000

February—Sale of used equipment, $4,000

4. Other disbursements: February—Purchased equipment, $10,000

5. Repaid debt: January, $30,000