Embed Size (px)

Citation preview

Formation Metals Inc.

Management’s Discussion and Analysis

For the Three Months Ended May 31, 2013

Unaudited

Date of Report: July 15, 2013

Suite 1810 – 999 West Hastings Street Vancouver, BC, Canada

V6C 2W2

Symbol: Toronto Stock Exchange - FCO

Table of Contents

1.1 Date .............................................................................................................................................................................. 1 1.2 Overview ..................................................................................................................................................................... 1 1.2.1 Summary ................................................................................................................................................................... 1 1.2.2 Highlights for the three months ended May 31, 2013 and subsequent events......................................................... 2 1.2.3 Risk Management ..................................................................................................................................................... 3 1.2.4 Basis of Analysis ....................................................................................................................................................... 4 1.2.5 Property Activities ..................................................................................................................................................... 4

(a) Idaho Cobalt Project – Idaho, USA .................................................................................................................... 4 (b) Big Creek Hydrometallurgical Complex (the “Complex”) – Idaho, USA ........................................................... 11 (c) Black Pine – Idaho, USA .................................................................................................................................. 11 (d) Badger Basin – Idaho, USA ............................................................................................................................. 11 (e) Morning Glory – Idaho, USA ............................................................................................................................ 11 (f) Queen of the Hills – Idaho, USA ...................................................................................................................... 12 (g) Wallace Creek – Idaho, USA ........................................................................................................................... 12 (h) El Milagro – Mexico .......................................................................................................................................... 12 (i) Kernaghan Lake / Bell – Saskatchewan, Canada ............................................................................................ 12 (j) Virgin River – Saskatchewan, Canada ............................................................................................................ 12 (k) Other Projects .................................................................................................................................................. 15

1.2.6 Outlook .................................................................................................................................................................... 15 1.3 Selected Annual Information .................................................................................................................................. 23 1.4 Results of Operations .............................................................................................................................................. 24 1.5 Summary of Quarterly Results ............................................................................................................................... 26 1.6 Liquidity .................................................................................................................................................................... 27 1.7 Capital Resources .................................................................................................................................................... 27 1.8 Off-Balance Sheet Arrangements ........................................................................................................................... 28 1.9 Transactions with Related Parties ......................................................................................................................... 28 1.10 Proposed Transactions ......................................................................................................................................... 28 1.11 Critical Accounting Estimates .............................................................................................................................. 28 1.13 Financial Instruments and Other Instruments .................................................................................................... 33 1.14 Other MD&A Requirements ................................................................................................................................... 34

(a) Disclosure of Outstanding Share Data ................................................................................................................ 34 (b) Internal Controls over Financial Reporting and Disclosure Controls .................................................................. 35 (c) Additional Information .......................................................................................................................................... 36

1

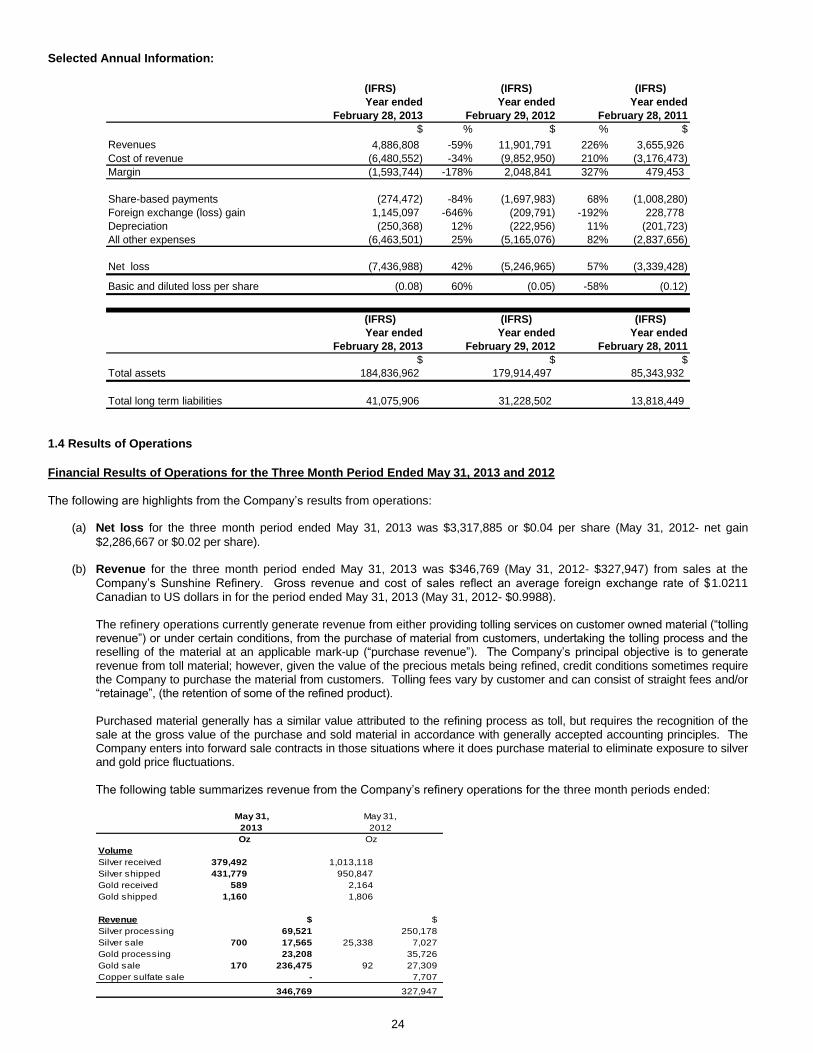

This Management’s Discussion and Analysis (“MD&A”) should be read in conjunction with the audited consolidated financial statements of Formation Metals Inc. (the “Company”) and the notes thereto, for the years ended February 28, 2013 and February 29, 2012 which have been prepared in accordance with International Financial Reporting Standards (“IFRS”) and are available through the internet on SEDAR at www.sedar.com. All dollar amounts herein are expressed in Canadian Dollars unless stated otherwise.

This MD&A includes certain statements that may be deemed “forward-looking statements” which the Company believes it has a reasonable basis for disclosing. All statements in this discussion, other than statements of historical facts, that address future production, reserve potential, exploration drilling, exploitation activities and events or developments that the Company expects are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, investors are cautioned such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include market prices, exploitation and exploration successes, continued availability of capital and financing and general economic, market or business conditions. The Company does not undertake to update any forward-looking statements that are contained herein, except in accordance with applicable securities laws. 1.1 Date

This MD&A is prepared as of July 15, 2013 1.2 Overview

1.2.1 Summary

Formation Metals Inc. (the “Company”) is a mineral exploration, development and refining company listed on the senior board of the Toronto Stock Exchange under the symbol FCO. The Company is engaged in the business of exploring minerals in Canada, the United States and Mexico either directly or indirectly through its wholly owned subsidiaries including:

(a) Formation Holdings Corp. (“Formation Holdings”), a British Columbia corporation; (b) Formation Capital Corporation, U.S (“Formation Capital”), a Nevada corporation. (c) Formation Holdings US, Inc.(“Formation Holdings US”), an Idaho corporation; (d) US Cobalt, Inc. (“US Cobalt”), an Idaho corporation; (e) Coronation Mines Ltd. (“Coronation”), a Saskatchewan company; (f) Minera Terranova S.A. de C.V. (“Minera Terranova”), a Mexican company; (g) Essential Metals Corporation® (“EMC”), an Idaho corporation; and (h) Formation Metals, U.S. (“FM US”) a Nevada corporation. (dba Sunshine Precious Metals Refinery).

The Company’s flagship project, the 100% owned Idaho Cobalt Project (the “ICP”), is comprised of the mine and mill site (“ICP Mine Site”) located in Lemhi County, Idaho, near the town of Salmon, and the current conceptual Cobalt Production Facility (“CPF”) located at the Big Creek Hydrometallurgical Refining Complex (the “Complex”) in Shoshone County, near the town of Kellogg, Idaho. The ICP is an environmentally permitted, primary cobalt deposit that will be capable of producing high purity cobalt (“HPC”) metal suitable for critical applications in the superalloy sector once fully financed and in production. If the ICP is put into production in the near-term, it is expected that the Company will become the United States’ sole integrated primary cobalt miner and refiner of superalloy grade HPC metal. Stage I Construction, completed in 2010, consisted primarily of clearing timber from the site in preparation for laying the foundation to be used for the ICP Mine Site structures. Over the course of the past fiscal year, efforts concentrated on completing detailed engineering at the ICP Mine Site and the CPF (95% complete) and accomplishing time critical tasks of Stage II construction to prepare the ICP for the commencement of underground development. At the ICP Mine Site, work concluded includes the mobilization and assembly of modular administration offices for permanent use, the completion of pad earthwork construction at the concentrator, crusher, tram discharge terminal and miner’s dry and the procurement of additional equipment. Portal bench excavation and geotechnical drilling was completed to assist in further evaluation of engineering for surface and underground work at the mine. At the Tailing Waste Storage Facility (“TWSF”), construction on all berms and the wetlands mitigation pond was completed and sufficient liner was installed preparing the TWSF to accept mine portal tailings once underground operations commence. Roadwork on the associated infrastructures to and from these facilities was also completed.

At the CPF, pouring of concrete for foundations of the new building was completed and refurbishment of existing regrind mill and copper circuits is ongoing. Additional concrete construction began in July 2012 and was completed in August 2012. This work was concentrated on the foundations for the cobalt electrowinning cells, crane structures, and constructing the oxygen tank pad. The cobalt electrowinning cells were placed on the CPF foundation beams and were covered for the winter months. Significant progress on beneficiation engineering analysis was completed and these studies demonstrated that in lieu of modifying existing autoclaves, the installation of a new autoclave would enhance efficiency at the CPF. Ongoing studies are considering the most favorable location for the CPF with a view to reducing estimated operating costs.

2

The Company announced on May 2, 2013 its decision to defer underground development at the ICP. This decision was made in light of weak cobalt prices during fiscal 2013 and enhanced adversity to risk by potential financiers in prevailing turbulent markets, which resulted in unattractive financing costs to complete development of the ICP. This decision allowed the Company to preserve working capital and delay extraction of cobalt and copper resources until market conditions improve to enhance the ICP’s economics. The Company fully intends to recommence construction of the ICP once markets improve and financing has been completed. Stage III of construction involves underground excavation to the ore face and the building of the required facilities such as the mill, concentrator and water treatment plant. Initial commercial production is expected to begin between 9 and 14 months from the commencement of Stage III construction. The Company’s Sunshine Precious Metals Refinery (the “Sunshine Refinery”) and copper refinery (“SX-EW”) are also located at the Complex. The SX-EW is a facility that could be shared by both the Sunshine Refinery and the CPF; however internal studies conducted in 2012 concluded that a standalone facility would be better suited to process concentrate from the ICP Mine Site rather than a retro-fit of the existing Complex. The standalone facility can be relocated within the general vicinity where the Company holds an additional 16 acres of industrial zoned private land. This also affords the opportunity for management to consider the relocation of the standalone facility to a location closer to the ICP Minesite, and/or a railhead, which would have a positive impact on future operational expenditures for the ICP. The Sunshine Refinery has been receiving silver doré from major silver producers and high grade silver products from silver users, mints and from other sources. On April 30, 2012, the Company’s Sunshine Refinery became an Approved Refiner and Brand on the official list of the COMEX (Commodity Exchange, Inc., a designated contract market of the CME Group Inc.). On June 6, 2013, the Company entered into a binding letter agreement (the “Letter Agreement”) to sell, for US$9.0 million in cash, 100% of its Sunshine Refinery, copper refinery and certain lands at the Complex (the “Refinery Assets”) to certain entities that are associated or affiliated with Waterton Global Resource Management, Inc. (“Waterton”). On June 26, 2013, the Company announced that the proposed sale of the Refinery Assets to Waterton had terminated, and on July 5, 2013 the Company announced the execution of a full and final mutual release with Waterton in respect of the Letter Agreement and the payment to Waterton of a break fee of US$1.0 million. A sale of this non-core asset continues to be pursued. In addition to cobalt, other minerals being explored for by the Company and its various subsidiaries include silver, gold, copper, lead, zinc, uranium, platinum group metals and rare earth elements (“REE’S”). 1.2.2 Highlights for the three months ended May 31, 2013 and subsequent events

ICP:

(a) On May 2, 2013, the Company announced its decision to defer underground development of the ICP due to weak cobalt

prices during fiscal 2013 and enhanced adversity to risk by potential financiers in prevailing markets, which resulted in

unattractive financing costs to complete development of the ICP. The Company fully intends to recommence construction

of the ICP once markets improve and financing has been completed; and

(b) During the three months ended May 31, 2013, the Company capitalized an additional $202,972 on the ICP, totalling

$56,701,323 spent on the ICP at May 31, 2013;

Sunshine Refinery:

(a) The Company announced on June 6, 2013 that it had entered into a binding Letter Agreement to sell, for US$9.0 million in cash, 100% of the Refinery Assets to Waterton;

(b) On June 13, 2013, Dundee Corporation (“Dundee”) filed a Petition in the Supreme Court of British Columbia against the Company, its directors and Waterton seeking to obtain a determination that the sale of the Refinery Assets to Waterton is a sale of all or substantially all of the Company’s undertaking subject to approval of the Company’s shareholders, under the Business Corporations Act (British Columbia), to obtain injunctions restraining the Company and Waterton from proceeding with the sale pending determination of that issue and seeking leave to commence a derivative proceeding against the directors of the Company based on allegations of breach of fiduciary duty;

(c) The Company announced on June 20, 2013 that the Supreme Court of British Columbia had dismissed Dundee’s

application for an injunction to halt the potential sale of the Refinery Assets to Waterton and that Dundee had sought only injunctive relief and did not proceed with its petition with respect to the issue of shareholder approval of any sale, nor leave to bring a derivative action;

(d) On June 26, 2013, the Company announced that the proposed sale of the Refinery Assets to Waterton had terminated;

and

(e) On July 5, 2013, the Company announced the execution of a full and final mutual release with Waterton in respect of the Letter Agreement and the payment to Waterton of a break fee of US$1.0 million. A sale of this non-core asset continues to be pursued. In the meantime, operations at the Complex are continuing.

3

Corporate:

(a) During the three months ended May 31, 2013, the Company reported a comprehensive loss of $3,533,680 and accumulated deficit of $46,047,422;

(b) As at May 31, 2013, the Company has working capital of $8,325,074;

(c) On May 9, 2013, the Company repaid the remaining US$43,600,000 of the Federal Stimulus Program Recovery Zone Facility Bonds (the “Bonds”) by using restricted cash from the Bank of Montreal (“BMO”) Letter of Credit (“LOC”). The balance of amounts requisitioned by the Company on redemption date was US$34,667,602 resulting in an unused balance of US$8,932,398. The Company also closed the LOC in conjunction with the Bond redemption and released net cash of US$9,569,439 or $9,595,277 from unused Bond proceeds and restricted cash to the Company’s treasury;

(d) On June 14, 2013, Dundee issued a letter and proxy circular soliciting the Company’s shareholders to vote for two nominees proposed by Dundee to be the two Class III directors elected at the Company’s Annual General and Special Meeting on June 21, 2013;

(e) On June 21, 2013, at the Annual General and Special Meeting, the Company’s shareholders voted to re-elect

managements’ director nominees, Mari-Ann Green and Scott Bending. The other resolutions considered at the Annual General and Special Meeting were also passed in accordance with the recommendations of management; and

(f) On July 9, 2013, pursuant to an initial recommendation of the Compensation, Nomination and Corporate Governance Committee of the Board, which was previously charged with undertaking a comprehensive review of the Company’s corporate governance practices, the roles of Chairman and CEO have been separated. Mr. Robert Quinn, previously Lead Director, has been appointed Chairman of the Board of Directors of the Company and Mari-Ann Green will continue in her role as director and Chief Executive Officer.

1.2.3 Risk Management Overview

The Company is an exploration, development, mining and refining company. Its activities subject the Company to a broad range of risks. These risks are managed within a company-wide risk management framework. The Company’s goal in managing risk is to strategically optimize risk taking and risk management to support long-term revenue, earnings and capital growth. Management seeks to achieve this by capitalizing on business opportunities that are aligned with the Company’s risk taking philosophy, risk appetite and return expectations; by identifying, measuring and monitoring key risks taken; and by executing risk control and mitigation programs. The Company’s risk management framework sets out policies and standards of practice related to risk governance, risk identification, risk measurement, risk monitoring, and risk control and mitigation. With an overall goal of effectively executing risk management activities, the Company continuously invests to build, acquire and maintain the necessary personnel, processes, tools and systems. The Company manages risk taking activities against an overall risk appetite, which defines the amount and type of risks we are willing to assume. The risk appetite reflects the Company’s financial condition, risk tolerance and business strategies. The quantitative component of our risk appetite establishes Company targets defined in relation to economic capital, and projected earnings sensitivity. Management has further established targets for each of the Company’s principal risks to assist management in maintaining appropriate levels of exposures and a risk profile that is well diversified across risk categories. Individual risk management programs are in place for each of the Company’s broad risk categories including strategic, market, liquidity, credit, insurance and operational. To ensure consistency, these programs incorporate policies and standards of practice covering:

(a) Assignment of risk management accountabilities across the organization;

(b) Delegation of authorities related to risk taking activities;

(c) Philosophy and appetite related to assuming risks;

(d) Establishment of specific risk targets or limits;

(e) Identification, measurement, assessment, monitoring, and reporting of risks; and

(f) Activities related to risk control and mitigation.

The Company cautions that the preceding discussion of risks that may affect future results is not exhaustive. When relying on forward-looking statements, investors and others should carefully consider the foregoing risks, as well as other uncertainties and potential events, and other external and Company specific risks that may adversely affect the future business, financial condition or results of operations of the Company.

4

1.2.4 Basis of Analysis

The sections that follow provide information about the important aspects of our operations and investments, on a consolidated basis, and include discussions of our results of operations, financial position and sources and uses of cash, as well as significant future commitments. In addition, we have highlighted key trends and uncertainties to the extent practical. The content and organization of the financial and non-financial data presented in these sections are consistent with information used by our chief operating decision makers for, among other purposes, evaluating performance and allocating resources. The following discussion should be read in conjunction with the Company’s audited annual consolidated financial statements for the fiscal year ended February 28, 2013 and February 29, 2012 and notes thereto. As part of our decision-making process we monitor many economic indicators, especially those most closely related to the demand, supply and pricing of metals, as well as the politico-economic situation in the main commodity supplier and consumer countries. Political developments affecting metal production can change quickly in some of the major cobalt producing countries such as the Democratic Republic of Congo, Zambia, Cuba, Russia, and in particular, those countries that are currently coping with armed conflicts. While most economic indicators impact our operations to some degree, we are especially sensitive to capital spending in cobalt intensive industries such as the re-chargeable battery sector, aerospace, high-tech, medical prosthetics, industrial, high-temperature steels and environmental applications such as gas and coal to liquids processes, oil desulphurization, wind turbine generators and hybrid-electric vehicles. We also monitor cobalt–related consumption expenditures on such items as computers, cell phones, paints and cutting steels. 1.2.5 Property Activities

The Company holds mineral exploration properties in Canada, the United States and Mexico. The Company’s 100% owned subsidiary, FM US, is engaged in the operation of a precious metals and concentrate refining business located in the State of Idaho. The Company conducts its exploration independently as well as through joint venture agreements with third parties. The following is a brief discussion of the Company’s major mineral exploration and development projects: (a) Idaho Cobalt Project – Idaho, USA

Background

The Company’s principal property is the 100% owned ICP Mine Site, a primary high grade cobalt deposit located in Lemhi County, Idaho, acquired through staking in 1994 and 1995. The property is held by the Company’s 100% owned subsidiary Formation Capital, and was extensively explored and developed to a bankable feasibility stage. All required environmental permits have been received from the various permitting agencies and construction of the project commenced with timber clearing in the spring of 2010. The project covers an area of approximately 4,080 acres and includes 241 mining claims. The Company now owns a 100% interest in these claims. This project is not subject to any royalty payments. Technical Results

A National Instrument 43-101 compliant technical report (the “Technical Report”), was completed September 14, 2007, revised May 19, 2008, amended and restated June 23, 2008 and SEDAR filed on July 15, 2008 and was derived from a more comprehensive Bankable Feasibility Study. The Technical Report is an engineering document designed to assess the mineral resources of the ICP and evaluate, among other things, the economic parameters of the deposit for potential financiers for the purpose of securing funds for mine development. The SEDAR filed Technical Report revealed the conservative base case scenario utilizing a 7.5% discount rate and utilizing a US$22.52 per lb. high purity cobalt metal price, returned a pre-tax Net Present Value (“NPV”) of US$87.29 million with an Internal Rate of Return (“IRR”) of 22.30%. Modifications to planned mining methods are being studied with the objective of reducing construction and operating costs and improve the NPV and IRR. Capital costs may be further reduced during detailed engineering and re-assessment of capital expenditures as the prices of several inputs have decreased since the Technical Report was completed prior to the onset of the world financial crisis. These optimization studies are ongoing. Prior to the completion of the Technical Report, an updated resource estimate was completed by Mine Development & Associates (MDA) in October of 2006 and is summarized in the following table.

5

Total Cobalt Project Resource utilizing 0.2% cut-off:

Category Tons % Cobalt % Copper Oz/ton Gold

Measured (“M”) 1,840,700 0.626 0.592 0.015

Indicated (“I”) 813,700 0.632 0.681 0.017

Total M&I 2,654,400 0.628 0.619 0.016

Inferred 1,121,600 0.585 0.794 0.017

Contained Metal Pounds Pounds Ounces

Measured and Indicated 33.3 million 32.9 million 41,000

Inferred 13.1 million 17.8 million 19,000

The resource estimate was prepared in conformance with the requirements set out in the Standards of Disclosure for Mineral Projects defined by National Instrument 43-101, under the direction of Mr. Neil Prenn, P.Eng., a Principal of MDA, who is an independent Qualified Person as defined by National Instrument 43-101. This report was SEDAR filed on November 3, 2006. The proven and probable mineral reserves outlined in the Technical Report are 2,636,200 tons with an average grade of 0.559% cobalt, 0.596% copper and 0.014 ounces per ton gold, based on a cut-off grade of 0.2% cobalt for a ten year mine life. The inferred resource for the ICP, not a part of this study, is 1,121,600 tons grading 0.585% cobalt, 0.794% copper and 0.017 ounces per ton gold as reported in the October 2006 MDA report mentioned above. Previous exploration and development drilling demonstrated that the permissive sequence for cobaltiferous mineralization in the Ram deposit remains open at both the north and south ends along strike and remains open down dip. This represents a currently defined strike length of approximately 3,200 feet. A 6,000 foot diamond drill program was initiated in late July 2010 in a previously untested area on the ICP and concluded in October 2010 with final assay results released in January 2011. Drill assays results confirmed economic ore grade mineralization in an additional 390 feet along strike to the south and 200 feet down dip, representing a 14% increase in the known strike extension of the Ram deposit to 3,200 feet. These results are expected to increase the reserve / resource base and mine life of the project, however, to date, no comprehensive NI 41-101 compliant studies have been conducted to confirm this expectation of resource base and mine life extension. An additional 5,727.5 feet were drilled in six holes in a previously untested area along the southern extension of the Ram deposit during this program. The data from this verification drill program has provided information needed to optimize mine design and production plans and has been used to maximize ore production as early in mine life as possible. Additional material for follow-up metallurgical testing on gold and REE’s known to occur on the property will be obtained once underground operations reach the ore face. Potential revenue from the production of gold and REE’s was not included in the Company’s Technical Report and no estimation of the potential economic viability of any such additional commodities currently exists. Financing

(i) Letters of Credit Arrangements

In September 2010, the Company received two Certificates of Allocation from the State of Idaho authorizing a total of US$46,700,000 in Bonds to the Company as ultimate beneficiary to be issued by the Industrial Development Corporation of Lemhi County, Idaho and the Industrial Development Corporation of Shoshone County, Idaho. In December 2010, the Company was issued revised Certificates of Allocation from the State of Idaho authorizing an additional US$31,000,000 in Bonds. As a result, the Company’s wholly owned subsidiaries, Formation Capital and EMC, were the sole beneficiaries of US$77,700,000 in Bonds. The interest rate on the Bonds is benchmarked with the Securities Industry and Financial Markets Association (“SIMFA”) Municipal Swap Index. These tax exempt industrial facility bonds were sold to the public prior to their December 31, 2010 expiry date and the funds were placed in a trust account. The terms of the Bonds require that the Company secure supporting letters of credit for the amounts to be drawn upon. Otherwise, the funds will be returned to the bondholders. The Company only record the liability at the time when funds are withdrawn from the Bonds. To provide letters of credit guarantees to back the Bonds, the Company mandated BNP Paribas (“BNPP”) to act as sole Mandated Lead Arranger and bookrunner for a senior secured debt facility (the “Facility”) for the construction and operation of the ICP. Based on an indicative term sheet negotiated between BNPP and the Company through its financial advisor, Auramet Trading, LLC, the Facility was expected to take the form of an amortizing construction / term loan or Letter of Credit supporting the issuance of the Bonds. In December 2010, Micon International Limited (“Micon”) was chosen through a selective bid process, to act as Independent Technical Engineer to provide the necessary due diligence technical reviews required for the Company’s ICP debt financing. Micon and JDS Energy and Mining Inc. (“JDS”), the Company’s Construction Manager, and in house engineers completed their due diligence during the second quarter of fiscal 2012 resulting in the receipt of the commitment from BNPP to provide a Facility to back the Bonds. On November 3, 2011, the commitment by BNPP to provide the Facility support of the Bonds was terminated without closing. On November 21, 2011, the Company secured a Letter of Credit (“LOC”) from BMO Bank of Montreal in support of US$43,600,000 of the US$77,700,000 raised from the sale of the Bonds. This LOC was cash

6

collateralized with $43,800,000 from the Company’s treasury. Although US$43,600,000 was secured, the full amount of the LOC was not used to draw down the Bond. An extension for the placement of letters of credit was made for the remaining US$34,100,000 of the US$77,700,000 Bonds until March 21, 2012. On February 7, 2012, the Company engaged Union Bank, N.A. (“UB”) as Lead Arranger to provide a credit facility supporting the Company’s US$77,700,000 Bonds. As UB was involved as one of the key syndicate members in the BNPP structured Facility, it was familiar with the Company’s ICP project. UB proposed to arrange a club of underwriters that would include themselves and at their discretion, additional lenders. On March 21, 2012, due to feedback from UB, other banks and the capital market, the Company repaid US$34,100,000 of the US$77,700,000 to Bond purchasers from cash originally held in trust. The Bonds added long term value with respect to their relatively low interest rates but they would have limited the Company’s flexibility with respect to the capital structure of project finance under current market conditions. On May 9, 2013, the Company repaid the remaining US$43,600,000 of Bonds by using restricted cash from the LOC. During the three months period ended May 31, 2013, the Company requisitioned $nil (February 28, 2013- US$11,130,229 or $11,479,718) for an aggregate requisitioned balance of US$34,667,602 or $35,756,165 prior to redemption of the Bonds. These funds were requisitioned from the ICP construction accounts to reimburse qualified ICP construction expenditures to the Company’s treasury since the inception of the Bonds. The unused balance of the Bonds on redemption date was US$8,932,398. In conjunction with the Bonds redemption, the Company closed the LOC and released net cash of US$9,569,439 or $9,595,277 from unused Bond proceeds and restricted cash to the Company’s treasury. As at May 31, 2013, amounts owed for Bonds proceed requisitioned is $nil (February 28, 2013- US$34,667,602 or $35,756,165). The Bonds repayment was made as a result of the Company’s decision to defer underground development of the ICP due to weak cobalt prices and enhanced adversity to risk by potential financiers in prevailing market conditions, which resulted in unattractive financing costs for further ICP development. The Company fully intends to recommence construction once market conditions improve and mine financing has been concluded.

(ii) Letters of Credit and Restricted Cash

Per the LOC, the Company was required to secure US$626,475 for finance and accrued interest for up to 106 days at 8% calculated on the principal of the Bonds, less US$800,000 for initial issuance costs. The total amount secured by the November 21, 2011 LOC was US$44,226,474. On March 21, 2012, the Company returned US$34,100,000 to bondholders. As a result, accrued interest for this portion of the Bond was collapsed reducing the LOC to US$44,163,958. The LOC for US$44,163,958 was made up of one set of Letters of Credit expiring November 21, 2013. As consideration, the Company agreed to pay the BMO interest of 0.375% per annum on the principal of the LOC and a quarterly fee of $200 for each LOC. The Company is required to pay BMO on demand in Canadian currency, at BMO’s prevailing US dollars selling rate, amounts drawn from the LOC and all other charges and expenses incurred by BMO relative to the LOC. The Company had converted all cash held in restricted cash account to US dollars since November 21, 2011. This eliminated foreign exchange risks as 100% of the US dollars Letters of Credit have been secured by US dollars held in restricted cash account. On May 9, 2013, the Company repaid the remaining US$43,600,000 of Bonds by using restricted cash from the LOC. The balance of amounts requisitioned by the Company on redemption date was US$34,667,602 resulting in an unused balance of US$8,932,398. The Company also closed the LOC in conjunction with the Bond redemption and released net cash of US$9,569,439 or $9,595,277 from unused Bond proceeds and restricted cash to the Company’s treasury. Due to the Bonds redemption and cancelation of the LOC, the Company collateralized $nil (February 28, 2013- $45,550,708) with cash from treasury to secure the LOC with BMO as at May 31, 2013. During the three months ended May 31, 2013, the Company paid $32,430 (May 31, 2012- $43,154) for interest and fees related to the LOC prior to the cancelation of the LOC.

7

As at May 31, 2013, the Bonds were recognized as follows:

Secured Secured with LOC

US$ US$ US$ CDN$

Bonds issued (USD) 77,700,000 - - -

LOC Cash security (USD) (43,600,000) 43,600,000 - -

Requisitions - (23,537,373) 23,537,373 23,290,231

Balance, February 29, 2012 34,100,000 20,062,627 23,537,373 23,290,231

Deferred financing cost - - - (1,476,058)

Accretion expense - - - 17,236

Foreign exchange loss - - - (38)

Balance, February 29, 2012 34,100,000 20,062,627 23,537,373 21,831,371

Bonds repaid (USD) (34,100,000) - - -

Requisitions - (11,130,229) 11,130,229 11,479,718

Foreign exchange loss - - - 986,216

Balance February 28, 2013 - 8,932,398 34,667,602 34,297,305

Deferred financing cost - - - (1,135,736)

Accretion expense - - - 98,113

Foreign exchange loss - - - (108,372)

Balance February 28, 2013 - 8,932,398 34,667,602 33,151,310

LOC Cash security (USD) 43,600,000 (43,600,000) - -

Bonds repaid (USD) (34,667,602) 34,667,602 (34,667,602) (34,761,205)

Return to treasury (8,932,398) - - -

Balance, May 9, 2013 - - - (1,609,895)

Deferred financing cost - - - 2,681,116

Accretion expense - - - 17,202

Foreign exchange loss - - - (1,088,423)

Balance, May 9, 2013 -$ -$ -$ -$

Bonds Issued ICP Construction Expenditure

Withdrawal

(iii) Convertible Debenture

On October 16, 2012, the Company issued a secured convertible debenture (the “Debenture”) in the principal amount of US$5,000,000 to an arm’s length party (the “Investor”). The interest cost of the Debenture is 8% per annum compounded quarterly. The Debenture matures one year from the date of issuance and is subject to acceleration in certain events and the Company retains the right to repay the Debenture in whole at any time, without premium or penalty. The principal of the Debenture is convertible, in whole or in part, at the option of the Investor into common shares of the Company at a conversion price of US$0.50 per share. The accrued interest of the Debenture is convertible, in whole or in part, at the option of the Investor at the greater of US$0.50 per share or the market price of the common shares at the time of conversion. The Investor may not convert amounts under the Debenture into more than 9.9% of the Company’s outstanding common shares. The Debenture is secured by certain assets of the Company and such security will be released upon repayment or conversion of all amounts due on the Debenture. The liability component of the Debenture has been calculated as the present value of the interest and principal payments of the Debenture at maturity, discounted at an interest rate of a similar liability without the conversion feature. The liability value of the Debenture was $4,665,195 based on an effective discount rate of 13.65% and the residual value of $232,924 was allocated to equity. The combined value from both liability and equity components were $4,898,119 or US$5,000,000 on October 16, 2012. The Company incurred net issue cost of $108,527 for the issuance of the Debenture of which $103,366 was netted against the liability component and will be charged to earnings using the effective interest method over the life of the bond and $5,161 was allocated to the equity component. The Company also recognized a deferred income tax liability of $28,470 to be allocated to the equity portion of the Debenture, resulting in a net equity effect of $199,293. During the three months period ended May 31, 2013, the Company accrued $106,079 (May 31, 2012- $nil) for interest expense, recorded accretion expense of $87,249 (May 31, 2012- $nil), and foreign exchange loss of $119,562 (May 31, 2012- $nil). The net liability balance of the Debenture at May 31, 2013 is $5,411,256.

(iv) Other Financing During the first fiscal quarter of 2011, the Company completed a fully subscribed equity financing (the "Financing") originally announced on January 27, 2011 for gross proceeds of $80,000,000. The Financing was sold in all of the provinces of Canada, except Québec, and certain offshore jurisdictions and consisted of Units priced at $1.50 per Unit. Each Unit was comprised of one common share in the capital of the Company (a "Common Share") and one half of one Common Share purchase warrant. Each whole Common Share purchase warrant (a "Warrant") entitles the holder to purchase one Common Share for 36 months at a price of $2.00. The Company's Common Shares currently trade on the Toronto Stock Exchange under the symbol "FCO" and the Warrants trade on the Toronto Stock Exchange under the symbol "FCO.WT". The Financing was conducted on a best efforts agency basis by a syndicate co-led by Byron Securities Limited and Cormark Securities Inc. and also included Jennings Capital Inc. (collectively, the "Agents"). The Agents were granted

8

an option, exercisable at any time for a period of 30 days, to purchase additional Units equal to 15% of the number of Units sold pursuant to the offering at the issue price of the Units, to cover over-allotments, if any and for market stabilization purposes. No portion of this option was exercised by the Agents. In consideration for the services rendered by the Agents under the offering, the Agents received a cash commission of 6% of the gross proceeds of the Offering and received broker warrants to purchase an aggregate number of Common Shares equal to 6% of the number of Units issued under the offering, at a purchase price of $1.50 for a period of 24 months. Concurrent with the close of the Financing, the Company repaid the balance owing of $7,000,000 on the $8,000,000 unsecured convertible debenture (the "Debenture") issued to Coalcorp Mining Inc. ("Coalcorp") on May 7, 2010. The Debenture was repaid through a mutually agreed cash and share settlement in the amount of $9,330,000 in cash for the unsecured debenture balance and any accrued and unpaid interest and 400,000 common shares issued at market value of $1.25 per share. The Company recorded a $2,737,588 loss from this settlement for the fiscal year ended February 29, 2012. The successful conclusion of the $80,000,000 equity financing allowed the Company to commence Stage II Construction of the ICP in the summer of 2011.

Construction of ICP Mine Site and Cobalt Production Facility

In December 2009, the Company and the United States Department of Agriculture Forest Service signed the “Forest Service Evaluation” which approved and finalized the Company’s Mine Plan of Operations for the ICP. The approval and finalization of the Company’s Mine Plan of Operations allowed the Company to commence Stage I Construction on the ICP Mine Site which consisted of timber clearing for the crusher and concentrator site, tailings and waste rock storage facility, topsoil stock pile area and road areas around the mill site. This was completed in the first quarter of the 2011 fiscal year. Additional approvals such as agreements on bonding continue to be negotiated. On June 17, 2011, the Company signed a Services Agreement with JDS for Project and Construction Management services for the ICP. JDS is working on a target based project risk/reward basis that includes an on-budget, on schedule and no harm execution accountability. Project development includes comprehensive overall project design and execution review to enhance the ICP (now completed), detailed design, procurement and contract execution and construction management through to commissioning and handover. Upon the successful conclusion of mine financing and completion of construction, the Company plans to use a mining contractor for the preproduction mine development and the first two years of mine production. Mine equipment will be required starting in Year 3 to continue development and to mine the stopes. According to the Company’s independent Technical Report completed in 2007, the amount of financing required to complete the ICP construction was estimated to be US$138.7 million. This figure did not include the post reclamation financial assurance (bonds) for both surface disturbance reclamation and long-term water treatment. More recent internal estimates by management in coordination with JDS places the estimated forecast at completion for construction and commissioning of the ICP at US$155,334,770 less cost to date, which takes into account the bonding requirements and additional facilities to increase precious metals recovery, and to increase autoclave leach capacity by 51%. This new cost estimation consists of US$93,318,852 for the mine concentrator, infrastructure and bonding, and US$62,015,913 for the retrofitting of the hydrometallurgical plant. These costs include mechanical and electrical equipment, construction materials, labor, labor supervision and contracted direct and indirect costs for these facilities. As at May 31, 2013 the Company spent $56,701,323 on the ICP. Of that, $202,972 was spent during the three months period ended May 31, 2013 (February 28, 2013- $13,176,084). Included in amounts spent to date, $16,498,912 previously spent on long lead items are not included in the current budget. Total to complete the project net of cost spent is currently estimated to be US$118,310,674. Since completion of the 2007 Technical Report, the Mine Plan has been re-engineered and optimized to maximize the extraction of the highest grade ore material in the shortest possible time frame in order to provide an optimized cash flow scenario in the early years of mine life. This resulted in a re-positioning of the portal bench and other engineering modifications associated with this re-positioning. This has not materially changed capital costs and is expected to assist in streamlining future mine operations. Review and optimization of the ICP Mine Site and the CPF is an ongoing process that incorporates new technology, new concepts, improved logistics and changing conditions. The approval of the Mine Plan of Operations for the ICP by the U.S. Forest Service outlines a 5-stage approach for posting the bonds that is coordinated with the development and operation of the ICP. Stages I and II pertain to all surface disturbance activities including Phase I of the tailings and waste rock storage facility expansion schedule (operational years approximately 1-6). The total bond requirement for Stages I and II is approximately US$6,379,617. To date, US$2,232,000 in cash was posted to secure a reclamation surety bond in the amount of approximately US$6,379,617, in conjunction with the commencement of Stage II Construction. Prior to the decision to defer mine financing and construction, mine development efforts concentrated on accomplishing time critical tasks of Stage II construction to prepare the ICP Mine Site for underground development and winterization of the construction site. These tasks included access road upgrades, portal bench construction and the preparation of the TWSF to accept waste rock from underground development. Underground excavation to the ore face will commence once the time critical construction tasks are completed and final mine finance is secured. The building of the required processing facilities such as the mill, concentrator and water treatment plant are expected to begin concurrently with underground development.

9

Initial production is expected to begin between 9 and 14 months from the commencement of underground development. Other tasks accomplished include the following:

(i) Modular administration offices were mobilized and assembled for permanent use at the mine site;

(ii) Construction of a new haul road resulted in eliminating the need to use the portion of Bucktail Road on the neighbouring property and shortening the haul distance from the portal bench by approximately two miles. This is expected to result in additional savings in mining costs and may eliminate the need to utilize an aerial tram system to haul ore and waste.;

(iii) Concurrent with the above roadwork, the installation of several extensive guardrails and berms on roads and gates to restricted areas were completed. These measures were implemented to reduce road maintenance and enhance the safety of the mine workers;

(iv) Placement of new surfacing material on all new and existing roads was conducted. In collaboration with the United States Department of Agriculture Forest Service and Lemhi County, maintenance of the transportation route to the project site was also conducted. This included blading, watering and rolling of approximately 10 miles of surface on Williams Creek Road for safety and road surface protection purposes;

(v) Drilling of water capture and monitoring wells was initiated and the installation of all monitoring wells required on the mine site and capture wells offsite was completed;

(vi) Excavation and sub-grade preparation and installation of the foundation-drain piping of the south half of the TWSF and the installation of a portion of the liners in the south half the TWSF was completed;

(vii) Excavation and sub-grade preparation of the WMP and the septic system drain field excavation was completed;

(viii) Installation of pipeline from Portal Bench to Big Deer Creek for treated water discharge, including the in-stream diffuser, air release valves and reclamation seeding and mulching of the completed right of way was conducted;

(ix) Construction on the portal access road, TWSF haul road, soil stockpile road and the WMP access road was completed; and

(x) Repairing of the 7900 level surface water diversion ditch and the installation of a security gate at the property boundary on the Big Flat area was completed.

Prior to the decision to defer mine financing, in addition to physical earthworks and other construction efforts, the Company’s development team of operations, process and outsourced engineers continued mine optimization studies. These studies were developed to demonstrate additional economic potential outside of the scope of the Bankable Feasibility Study, primarily for mine financing purposes. Construction efforts at the mine site will continue upon the successful conclusion of mine financing. Prior to and during the first fiscal quarter of 2013, JDS concentrated its efforts on finalizing budgets and engineering and procurement tasks involving several areas at the CPF. Engineering emphasis continued on flow sheet development and refinements to the heat and water balances and equipment layout specifications for the CPF were undertaken. The planned stand-alone CPF building and the adjacent existing refinery building collectively comprise the Complex. At the CPF, additional concrete construction began in July of 2012 and was completed in August 2012. This work concentrated on the foundations for the cobalt electrowinning cells, crane structures, and constructing the oxygen tank pad. Engineering and construction efforts at the refinery focused on the development of the P&ID’s and GA drawings at the CPF. In addition, modifications of the silver refinery progressed to accommodate the requisite modifications for third party copper / silver concentrates as well as cobalt concentrates from the ICP Mine Site. However internal studies concluded that a standalone facility would be better suited to process concentrate from the ICP Mine Site rather than a retro-fit of the existing Complex. P&ID’s show the connectivity of equipment, sensors, and valves in a control system. P&ID’s also provide the basis for the conceptual layout of the CPF. Other tasks accomplished include the following:

(i) The PHA of CPF designs were initiated;

(ii) Design of the Leach Residue Repository facility progressed, with the water management area were surveyed, and information on geo-tube layout design was received from one of the Company’s engineering consultants. Geo-tube requests for proposals were released to determine the recommended vendor;

(iii) The budget support documentation was reviewed and project execution strategy was conducted as part of ICP finance due diligence;

(iv) The cobalt electrowinning cells were placed on the CPF foundation beams and covered for the winter;

(v) An engineering schedule for completion of P&ID review and GA drawings was prepared;

(vi) A review of P&ID & Control Philosophy by the Company was initiated. Over half of P&ID’s and their related sections of control philosophy were finalized; and

10

Several photos have been posted on the Company's website documenting the above work and can be viewed at http://www.formationmetals.com/s/ConstructionGallery.asp. In addition, video updates of construction progress at both the mine site and at the refinery have been posted on the Company’s website at http://www.formationmetals.com/s/Presentations.asp documenting the work completed to date. Stage III Construction includes posting the bond for long-term water treatment prior to mine development below the water table. The amount of the Stage III bond was previously determined by the Forest Service at approximately US$20.60 million; however, the Company successfully appealed this decision and is working with the Forest Service to determine the appropriate discount rate for use in calculating the bond for Stage III Construction. Stage IV and Stage V Construction correspond with Phases II and III of the TWSF expansion schedule (operational years approximately 7-10) and amount to approximately US$1.90 million, and US$0.80 million, respectively. As a result of discussions with insurance brokers, the Company anticipates the actual cost for surface disturbance bonding will be approximately US$2.40 million. The long-term water treatment bonding will be determined when discount rate discussions with the Forest Service are concluded. Long lead time items that have not already been delivered to the mine site, are currently being stored in a company owned facility and in a nearby leased storage facility outside of the town of Salmon, Idaho. The 9,600 square foot company owned facility is located on a 3 acre lot on the outskirts of town. The facility will also act as a staging area for the transportation of mine employees to and from the mine site, as well as an offloading area for mine concentrate to be transported to the CPF. Mine equipment stored at the staging areas include ball mill components, flotation cells, power transformer, bridge crane, vibratory feeders, crusher and concentrator building components, the cyclone package, the aerial tram towers, cables, drive system, bucket and tram loading and discharge terminals. The equipment is for the processing of primary cobalt ore at a production rate of 800 tons per day at the cobalt mine site. Concentrate from the mine will be shipped to the CPF for processing into high purity, superalloy grade cobalt metal at a design rate of approximately 1,500 tons per year on average over a minimum 10 year mine life. The mine life is expected to be longer than the minimum ten years outlined in the Technical Report, as the primary deposit remains open along both strike directions and at depth. Including inferred resources would add an additional 4 years to the mine life. In addition, numerous other targets remain to be explored and developed on the property. To date, none of these additional resources or extensions of mine life have been verified through any studies or reports that are National Instrument 43-101 compliant. Several engineering companies were engaged and worked on finalizing different aspects of the engineering plans for the mine and the cobalt production facility. This included engineering work on site, roads, portal bench, tram layout revisions, power line layout, tailings and waste rock storage facility final design and concentrator site layout and design. Once construction of the ICP reaches a critical stage, an intensive hiring program will be involved for both the Mine Site and the CPF locations and includes professional recruitment campaigns for more senior positions and advertising with employment agencies and / or employment websites for staff positions. There is a local qualified workforce in both the Salmon and Kellogg areas to draw from and we expect to fill our labour needs without serious difficulty. Contingent upon financing of the construction of the ICP, the Company intends to continue ICP construction personnel hiring resulting in a total of 52 employees for the Salmon operation and an additional 41 employees for the Kellogg facility, totalling 93 new jobs in Lemhi and Shoshone Counties, Idaho. It is estimated that an additional 49 miners would be employed by a contract miner. These jobs are expected to have a positive impact on both local economies. If made operational in the near term, the ICP is expected to be the only primary cobalt producer in the Western Hemisphere, making Formation Metals Inc. the United States’ sole integrated cobalt miner and refiner of high purity, superalloy grade cobalt.

Once in full production, the project would create approximately 200 well-paying jobs in two Idaho counties.

Impairment Analysis

In order to assess the recoverability of the non-current assets recorded as part of the ICP, management has estimated the after tax future cash flows of the ICP and compared these results to the carrying value of the ICP. The after-tax cash flows have been determined based on the estimated life of mine and dates for operational commencement, production levels at current estimates of proven and probable reserves and inferred resources, future operating costs, non-expansionary capital expenditures and most significantly estimated metal selling prices for Cobalt. The projected cash flows are significantly affected by changes in assumptions of metal prices, future capital expenditures, production cost estimates, construction completion timelines and discount rates. Metal prices are estimated based on historical price volatility ranges. For their assessment as at the year-ended February 28, 2013, management used an estimated price assumption of US$19.83 per lb. for high purity cobalt (“HPC”) which is based on historical twenty year average price. HPC trades at a premium with greater expected demand than cobalt of lesser purity. The reasons are due primarily to this select class of material being the most difficult to produce, is not affected by African production, increase in demand in the super-alloy sector, a lack of substitution for premium material, and only a limited number of producers fall within this cobalt subsector. The ability to increase supply to meet demand growth is very limited. More information on HPC can be found in the section “1.2.6 Outlook”, under the subheading “High Purity Cobalt Market”.

11

Cash flow projections are discounted at a rate of 8.24% which represents management best estimate of its weighted average cost of capital. Management also estimated the time for commercial production at the mine to be one year from balance sheet date of February 28, 2013, pending successful financing. A decrease of 6.75% in cobalt pricing assumptions made by management, by itself, could have an adverse impact on the estimated recoverable amount of the project.

(b) Big Creek Hydrometallurgical Complex (the “Complex”) – Idaho, USA

The Company acquired the Complex in 2002 for the purpose of retrofitting the hydrometallurgical facility for cobalt production to meet the processing requirements of the ICP. In 2004, management restarted the precious metals refining section of the facility, known as the Sunshine Refinery, to help meet increasing North American demand for silver and gold refining. The Company’s Sunshine Refinery and SX-EW are located at the Complex. The SX-EW is a facility that can be shared by both the Sunshine Refinery and the CPF; however internal studies conducted in 2012 concluded that a standalone CPF would be better suited to process concentrate from the ICP Mine Site rather than a retro-fit of the existing Complex. The standalone CPF can be relocated within the general vicinity where the Company holds an additional 16 acres of industrial zoned private land. This also affords the opportunity for management to consider the relocation of the standalone facility to a location closer to the ICP Minesite, and/or a railhead, which would have a positive impact on future operational expenditures for the ICP. On March 29, 2012 the Company announced that after significant analysis, it would install a new autoclave in the CPF in lieu of modifying the existing autoclaves to process cobalt. This decision effectively separated the existing refinery operations from the proposed CPF and allows the existing autoclaves to be used to process third party precious and base metals concentrates. The Company proceeded to obtain expressions of interest letters, contracts, and testing of various materials from customers and potential customers. However, the Company determined that the successful development of that business will require substantial capital expenditures, sufficient working capital, a hedging program and the ability to provide provisional payments. Current unprecedented market turmoil has made it unlikely that the Company will obtain these capital requirements in the near future.

The Company announced on June 6, 2013 that it had entered the Letter Agreement to sell, for US$9.0 million in cash, 100% of the Refinery Assets to Waterton. The sale was subject to, among other things, confirmatory due diligence, the execution of a definitive acquisition agreement by June 20, 2013, unless mutually extended, and any required regulatory approvals. In addition, the Letter Agreement included an exclusivity provision in respect of the Company until its termination and required the Company to pay Waterton a break fee of US$1.0 million and a portion of Waterton’s costs in certain circumstances. Cormark Securities Inc. was engaged to provide a fairness opinion on the transaction.

On June 26, 2013, the Company announced that it had terminated the proposed sale of the Refinery Assets to Waterton, and on July 5, 2013 the Company announced the execution a full and final mutual release with Waterton in respect of the Letter Agreement and the payment to Waterton of a break fee of US$1.0 million.

The Sunshine Refinery continues to receive product from customers and the Company is continuing its efforts to expand this division of the business. The refinery is a zero liquid discharge operation and as such the Company ascertained through consultation with legal counsel and environmental experts that there are no legal requirements related to reclamation of real property upon any sale, temporary shut down or closure of the refinery.

The Company’s refinery operations currently generate revenue from both toll material and purchased material. The Company’s principal objective is to generate revenue from toll material; however, given the value of the precious metals being refined, credit conditions have on occasion required the Company to purchase the material from customers. Toll material fees vary by customer and can consist of straight fees and/or “retainage”, (the retention of some of the refined product). Purchased material generally has a similar value attributed to the refining process as toll but requires the recognition of the sale at the gross value in accordance with generally accepted accounting principles. From time to time the Company enters into forward sale contracts in those situations where it does purchase material to eliminate exposure to silver and gold price fluctuations. The Sunshine Refinery has been receiving silver doré from major silver producers, high grade silver products from silver users, mints and from other sources. On April 30, 2012, the Company’s Sunshine Refinery became an Approved Refiner and Brand on the official list of the COMEX (Commodity Exchange, Inc, a designated contract market of the CME Group Inc).

(c) Black Pine – Idaho, USA

The Company has a 100% interest in certain mineral claims with prospects for copper, cobalt and gold located in Lemhi County, Idaho. An option agreement is in effect until the year 2014 to share on a 50/50 basis with the option or any payments received from a joint venture partner.

(d) Badger Basin – Idaho, USA

The Company has a 100% interest in certain mineral claims acquired through staking with prospects for copper and cobalt located in Lemhi County, Idaho.

(e) Morning Glory – Idaho, USA

The Company has a 100% interest in certain mineral claims with prospects for gold and silver located in Lemhi County, Idaho. The Company also has a 100% lease option on certain additional mineral claims located in the same area. A total of

12

US$45,900 has been paid to date to the option or. To exercise the option, the Company must pay a total purchase price of US$1,000,000 including the advance annual minimum royalty payments. During fiscal 2013, the option and mineral claims were maintained in good standing. Confidentiality Agreements have been signed with parties interested in a possible joint venture.

(f) Queen of the Hills – Idaho, USA

The Company holds a lease option to purchase 100% of certain mineral claims with prospects for gold and silver located in Lemhi County, Idaho. A total of US$25,200 (2011 - US$25,200) has been paid to date to the option or. Total purchase price of US$1,000,000 including advance payments must be made to exercise the option. During the fiscal year ended February 28, 2013, the option and mineral claims were maintained in good standing. Confidentiality Agreements have been signed with parties interested in a possible joint venture.

(g) Wallace Creek – Idaho, USA

The Company has a 100% interest in certain mineral claims with prospects for gold and silver located in Lemhi County, Idaho. The Company also has a 100% lease option on certain additional mineral claims located in the same area. To exercise the option, the Company must pay a total purchase price of US$1,000,000 of which US$25,600 has been paid to date.

(h) El Milagro – Mexico

The Company entered into a purchase option agreement in 1998 that was completed at year end February 28, 2003. The Company now has a 100% interest in the prospective silver rich base metal property. The primary target defined within the Milagro Concessions is the Santa Maria Vein, a 1-4 meter wide tabular subvertical NNE trending breccias vein that has been mapped over a strike length of 450 meters, with a lead-rich polymetallic assemblage and bonanza silver grades. This vein, localized along the footwall contact of a sericite altered dike, is cemented by a fine grained intergrowth of galena, sphalerite, pyrite, barite and manganese oxides. Silver grades in the sulphitic vein material have been reported in the range of 1.5 to 5.5 kg per tonne (Tschauder, 1988). It has been reported to the Company that the Mexican Government intends to establish a Protected National Area in the general area that encompasses the Milagro project. The Company has been advised by its legal counsel that this new designation will involve additional environmental analysis by Mexican permitting authorities, but in no way precludes the exploration, development and mining of minerals from the property. The permitting of the project is not expected to be any more onerous than what the Company’s internal environmental standards and guidelines require and what it has already experienced and is familiar with during the exploration and development of its other mineral projects. The Company intends to further evaluate the mineral occurrences on the property and define targets for further development. Previously, the Company embarked on a strategic land acquisition program that has complemented the existing core land holdings of the El Milagro project. These additional holdings cover the extension of the Santa Maria Vein occurrence and it is management’s intention to further pursue exploration of this project once additional financial and personnel resources become available or through joint venture or other such partnerships. Subsequent to the end of the three months period ended May 31, 2013, a Confidentiality Agreement has been signed by a third party expressing possible interest in joint venturing the property.

(i) Kernaghan Lake / Bell – Saskatchewan, Canada

The Company granted an option whereby the optionee has earned 80% interest in certain mineral claims by making certain payments (received), and completing exploration work totaling $1,000,000 (deemed completed). The project area is located near the northeast rim of the Athabasca Basin approximately 42 km north of Points North Landing. The Kernaghan / Bell project currently consists of 13 mineral claims totaling 4,342 hectares. The target unconformity depth ranges from 160m to 290m. To date 38 diamond drill holes within the property outline totaling 10,051.4m have been drilled targeting the unconformity. The completed drilling for the 2009 program consisted of 8 drill holes, KB04 through KB11, totaling 2,683.4m. Geochemical analyses were received for basement systematic and selective samples collected for drill holes KB-04 to KB-11. These samples returned anomalous uranium intersections with a maximum partial uranium value returned from Ker A Conductor in drill hole KB-11 of 160 ppm and a maximum partial uranium value returned from K 1 Conductor in drill hole KB-07 of 34.2 ppm, none of the holes drilled in 2009 intersected significant uranium mineralization. A Geochemical Compilation Report was sent out to joint venture partners and filed for assessment credit. Approval of the assessment filing will keep the project land in good standing until 2017. There wasn’t a proposed budget for field work for the current period.

(j) Virgin River – Saskatchewan, Canada

In the year ended February 28, 1999, the Company entered into a joint exploration agreement with UEM Inc. UEM Inc. was a corporation owned 50% by Cameco Corporation ("Cameco") and 50% by AREVA on the Virgin River project located in the Athabasca Basin of northern Saskatchewan. Subsequently, UEM was dissolved and both Cameco and AREVA became equal partners (49% each) in the joint exploration agreement. Cameco is the operator of the project. The Company's wholly owned subsidiary, Coronation Mines Ltd. owns the remaining 2% of the project with the first right of offer to acquire up to 10% of the project and has been carried through to $10.0 million worth of exploration and development (vetted). As at February 28, 2013,

13

over $32.0 million has been spent on the project exploring for a large unconformity-type deposit that has resulted in the discovery of the Centennial Deposit. Cameco is the operator of the project. The Centennial Deposit was traced over 650 metres of strike length and has a minimum across strike width ranging from 10.0 metres to 52.5 metres. Approximately $14.0 million was reported by Cameco as having been spent on the 2009 - 2012 drill programs that were designed to follow up on the 2004 - 2008 drill results from the Centennial Zone. The joint venture approved a budget of $2.15 million for continued drilling on the Virgin River project for calendar 2012. The 2012 drill program concentrated on the evaluation of the off-conductor mineralization intersected in drill hole DDH VR-051 and evaluated the conductor responses from a proposed geophysical survey between L21N and L33N located to the north of the deposit. Several tests were also dedicated to upgrading mineralization on the Centennial Deposit by assessing the cross structural influence on uranium mineralization within the deposit. High grade U3O8 intersections of up to 298 GT have been intersected within the Centennial Deposit (33.9 metres grading 8.78% U3O8 -- see Company News release dated May 30, 2011). GT is defined as % grade U3O8 multiplied by thickness in metres. Assay results returned from diamond drill programs from 2004 to 2011 on the Centennial deposit have resulted in 39 significant primary uranium intersections returning results greater than 10.0 GT. Results from the 2011 drill program were discussed in the Company's news release dated January 12, 2012 with final results of the program released during the quarter ended May 31, 2012 in the Company’s news release dated April 4, 2012. All drill holes completed on or immediately surrounding the Centennial Deposit in 2011 displayed uranium enrichment throughout the basal sandstone in contact with the basement unconformity with elevated pathfinder elements such as lead, vanadium and nickel. Significant high grade uranium intercepts were intersected in 7 of the drill holes with GT's over 10. Diamond drill programs from 2004 to 2012 on the Centennial Zone have resulted in 39 significant primary uranium intersections returning results greater than 10.0 GT. Drilling during the 2012 program consisted of 6 diamond drill holes which included 4 pilot holes and 2 wedge holes, VR-051W1, 51W2, 52, 53, 54 and 55, totaling 4,487.9 m. These holes were drilled to evaluate a quartzite fault north of the Centennial Zone, and to investigate the geophysical conductors known as C1 and CF. Final assay results are pending as at the date of this report. Plans for the 2013 program are concentrated on environmental studies focused on the indigenous Woodland Caribou population, an evaluation of a permanent overland road to the Centennial Deposit for year round exploration and development access and the compilation of existing data to prepare the project area for renewed exploration activities in 2015 and beyond with a proposed 2013 budget of $450,000. Drilling was not planned for the fiscal year ended February 28, 2013.

14

Significant diamond drill results greater than 10.0 GT from the Centennial Deposit From 2004 - 2011:

Note: Inductively Coupled Plasma - Optical Emission Spectroscopy Split assay results with core recovery intervals of less than 75% were replaced by shielded probe results.

Cameco has indicated they are exploring for a McArthur River style uranium deposit, and the Company’s management is very encouraged with results to date. All uranium assays were carried out by the Saskatchewan Research Council (SRC) of Saskatoon, Saskatchewan. Delayed neutron counting (DNC) and / or X-ray fluorescence spectroscopy (XRF) U3O8 check assays were completed on all split assay samples returning greater than 1.0% U3O8. The average of the check assays and the ICP-OES results were used in the calculations of grade thicknesses. Mr. Eric (Rick) Honsinger, P.Geo., of Formation Metals Inc., is the Qualified Person who has reviewed and approved the information in this MD&A with respect to the Virgin River Project based on an examination of the data submitted to the Company by the project operator Cameco Corporation.

15

(k) Other Projects

The Company has varying other interests of up to 100% in certain mineral claims located in Idaho, Saskatchewan and Manitoba.

1.2.6 Outlook

Over the course of the next several months the Company expects to focus its activities on assessing the world financial markets for the opportunity to have a successful conclusion of ICP financing and recommencing the final Stages of construction of the ICP. The continued rise in cobalt prices from their lows in late 2012 are expected to assist in ICP financing efforts. In addition, any proceeds from a potential sale of the refinery will be used to enhance the Company’s working capital and allow for access to capital to further develop the Company’s assets and to take advantage of potential opportunities that may arise. Potential financing alternatives include bank debt financing, securing strategic partnerships, securing off-take, securing streaming arrangements for future by-product copper and gold production at the ICP, securing a high yield debt facility and/or other means deemed reasonable by management including joint ventures. The Company will also continue to seek opportunities to form additional exploration joint ventures in order to reduce shareholder risk. As a mineral exploration and development company, until such time as construction of the ICP re-commences, the future liquidity of the Company is expected to be affected principally by the level of exploration and development expenditures and by its ability to raise capital in the equity markets. The Company’s current cash position is not sufficient to fund construction of the ICP Mine Site and the CPF. During the three months ended May 31, 2013, the Company’s shares, trading on the TSX under the symbol FCO, attained a high of $0.23 in early March 2013 and reached a low of $0.06 in mid June 2013. Similarly, the Company’s warrants trading on the TSX under the symbol FCO.WT, sustained a low of $0.005 during the same period where they remain today. Prevailing weak and uncertain financial markets resulting from the European Union’s unresolved financial crisis, the weak economic recovery of the United States and a decline in a demand for commodities, particularly in Asia, continue to severely affect the resource sector and its ability to finance mining projects. The commodities and resource sector in general continued to decline to unprecedented levels. Following the Company’s May 2, 2013 announcement of the deferral of underground development for the ICP, the stock traded down to a historic low of $0.06 representing a market capitalization discounting the Company’s cash position. Figure 1: Formation Metals’ Share Price, March 1, 2013 – July 15, 2013

Outlook for the Cobalt Market

Cobalt markets have been less turbulent than in previous years. High purity cobalt rose to nearly US$52.00 per lb. in early 2008 and subsequently fell to a low of approximately US$17.00 per lb. During 2010 cobalt prices near the beginning of the year were around US$24.00 per lb., and subsequently softened to around US$19.50 per lb. in March 2010 then rose to close to US$25.00 per lb. in April 2010. Average prices then remained in a narrow trading range between US$21.00 per lb. and US$22.00 per lb. until late in 2010. Average prices for 99.8% purity cobalt during 2011 have traded in a range between US$15.50 and US$21.00 per lb. During the first nine months of 2012 high purity cobalt prices traded in a narrow range between US$12.00 and US$16.50 per lb. Prices softened during the last three months of 2012 to a multi-year low of between $10.20 and $11.80 per lb. (MetalBulletin)

16