Embed Size (px)

DESCRIPTION

Management Report: The effect of management practices on productivity.Governments can have impact in empowering the take-up of good management conduct. Doing as such may be the absolute most practical method for enhancing the performance of their economies. Solid rivalry and adaptable work markets both lead straightforwardly to enhanced management performance. Multinational organizations have an in number constructive outcome as well, and their impact is felt all through the locales in which they work.

Citation preview

IISB – Assignment B Kumar Mayank - 14609038

Item - 24 (Management Report)

8/16/2015

Jaypee Business School

Constituent of Jaypee Institute of Technology

A-10, Sector-6, Noida-201307 (U.P)

Tel: 91-120-2400973-975 Fax: 91-120-2400986

1 | P a g e

Management Report: The effect of management

practices on productivity

Kumar Mayank, Jaypee Business School, NOIDA, India

Abstract

The reason for the paper is to discover new approach for the powerful estimation of an

organization's management works on, permitting them to be contrasted specifically and genuine

business performance. This paper is taking into account the article

http://cep.lse.ac.uk/management/Management_Practice_and_Productivity.pdf distributed in

November 2007 by Nick Bloom (Stanford University), Stephen Dorgan and John Dowdy (McKinsey &

Company), John Van Reenen (Center for Economic Performance, London School of Economics).

Multinational organizations have been compelled to take an efficient way to deal with management.

Just by having solid, viable management rehearses set up have they possessed the capacity to imitate

the same norms of execution crosswise over distinctive areas, societies and markets. Today, they are

procuring the advantages of this exertion as far as higher profitability, better profits for capital and

more strong development.

Governments can have impact in empowering the take-up of good management conduct. Doing as

such may be the absolute most practical method for enhancing the performance of their economies.

Solid rivalry and adaptable work markets both lead straightforwardly to enhanced management

performance. Multinational organizations have an in number constructive outcome as well, and their

impact is felt all through the locales in which they work.

Constant change in instructive benchmarks is likewise crucial. Better-oversaw firms require all the

more exceedingly talented laborers and they improve utilization of them, while better instructed

chiefs will be a key part of the execution change that both built up and rising economies must

attempt on the off chance that they are to keep up and enhance their worldwide focused position.

Keywords: Management Reports, Management Practices, Management Productivity

2 | P a g e

Introduction

Management reporting is the process of providing agency management with timely, accurate and

relevant information that is designed to assist in the strategic and operational management of an

agency.

Under proper management, the high risk, hazard and fluffy property privileges of intangibles can be

influences into extensive quality.

The achievement of any business undertaking depends essentially on procuring income that would

produce adequate assets for sound development. To accomplish this goal, the management ought to

release its capacities proficiently and successfully. The reporting frameworks are profoundly valuable

to the management for successful arranging and control. A standard arrangement of reporting is

considered as a superior direction for brief choice making. Subsequently, it is important to have a

decent management reporting framework.

Objectives of Management Reporting

(1) To obtain the required information relating to the business to discharge its managerial functions

of planning, organizing, controlling, directing, and decision making etc. efficiently and effectively.

(2) To ensure the operational efficiency of the concern.

(3) To facilitate the maximum utilization of resources.

(4) To secure industrial understanding among people who are engaged in various aspects of work of

enterprise.

(5) To motivate for improving discipline and morale.

(6) To help the management for effective decision making.

Essentials of Good Reporting System

The accompanying are the essentials of a decent management reporting framework:

(1) Proper Form: A great report ought to have a thorough structure with suggestive title, heading,

sub heading and number of sections as and where essential for simple and fast reference.

(2) Contents: Simplicity is one of the essentials of reporting in connection to the substance of a

report. Further the substance ought to take after a consistent grouping. Wherever important the

substance ought to be spoken to as visual guides, for example, graphs and outlines and so forth.

3 | P a g e

(3) Promptness: It implies that the framework ought to guarantee the planning and accommodation

of report at the best possible time. It encourages business officials to settle on suitable choices in

view of speedy reports as soon as possible.

(4) Accuracy: Information passed on ought to be exact. This implies that the individual in charge of

reporting ought to have adequate consideration in setting up the report as accurately as could be

allowed inside of the parameters of feasible precision in such manner.

(5) Comparability: With a specific end goal to guarantee that the outfitted data is helpful, it is vital

that reports are likewise implied for examination. The report ought to give data about both the

genuine and the planned execution of the monetary allowance period. So that significant

examination can be made to discover the deviations and to start fitting activity.

(6) Consistency: keeping in mind the end goal to make a significant and valuable correlation,

uniform bookkeeping standards and techniques ought to be taken after on steady premise over a

stretch of time for gathering, characterization and presentation of bookkeeping data.

(7) Relevancy: The report ought to be given significant information to uncover the certainty in

unambiguous terms. Consideration of both the applicable and the unimportant information in the

administration reports may bring about flawed choices.

(8) Simplicity: The report ought to be beyond what many would consider possible in basic structure.

As it were, the report ought to stay away from specialized languages, duplication of work and

exhibited in a basic style.

(9) Flexibility: The framework ought to be fit for being balanced by prerequisite of the clients.

(10) Cost-Benefit Analysis: Cost-Benefit Analysis ought to be made and the expense of reporting

ought to comparable with the consumption included.

(11) Principle of Exception: Since the time and exertion of administrative work force are valuable,

the rule of administration by exemption has turned into the standard of the day rather than special

case. It is important along these lines to draw the consideration of administration, through reports,

just towards outstanding matters.

(12) Controllability: It is essential that each report ought to be tended to an obligation focus and

investigated the elements into controllable and wild independently. So that the leader of the

obligation focus can be considered mindful just for controllable fluctuation however not for changes

which are outside his ability to control.

4 | P a g e

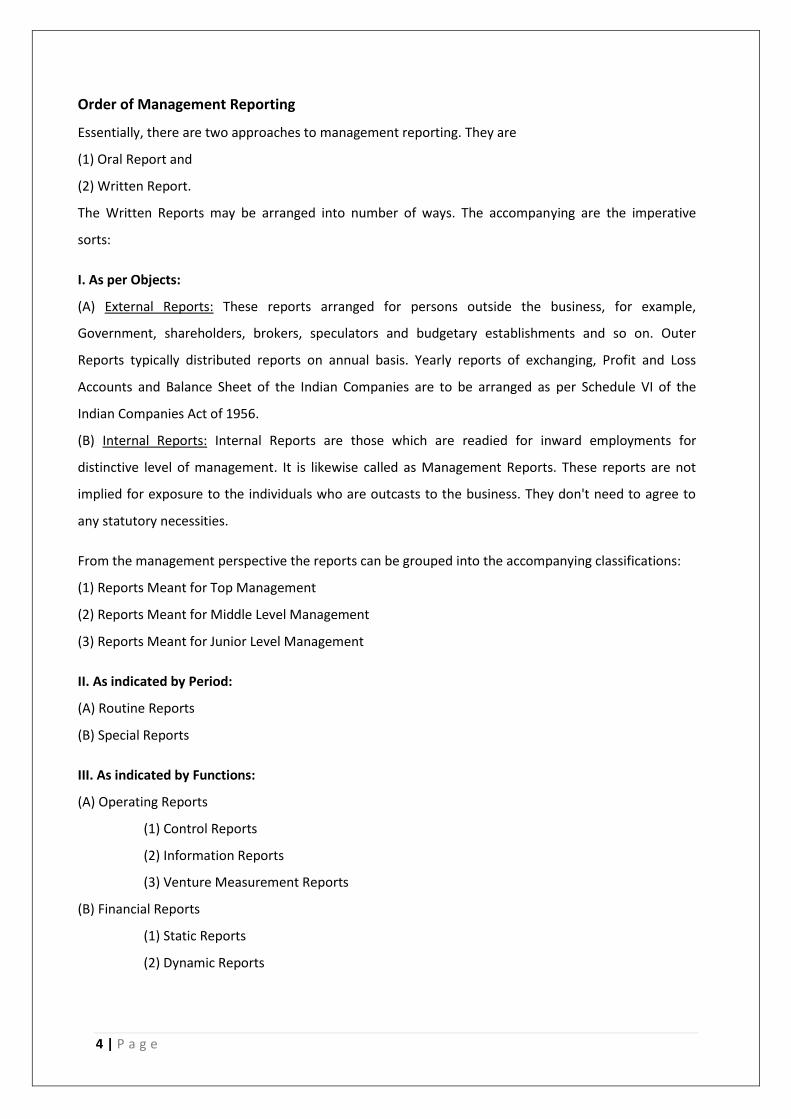

Order of Management Reporting

Essentially, there are two approaches to management reporting. They are

(1) Oral Report and

(2) Written Report.

The Written Reports may be arranged into number of ways. The accompanying are the imperative

sorts:

I. As per Objects:

(A) External Reports: These reports arranged for persons outside the business, for example,

Government, shareholders, brokers, speculators and budgetary establishments and so on. Outer

Reports typically distributed reports on annual basis. Yearly reports of exchanging, Profit and Loss

Accounts and Balance Sheet of the Indian Companies are to be arranged as per Schedule VI of the

Indian Companies Act of 1956.

(B) Internal Reports: Internal Reports are those which are readied for inward employments for

distinctive level of management. It is likewise called as Management Reports. These reports are not

implied for exposure to the individuals who are outcasts to the business. They don't need to agree to

any statutory necessities.

From the management perspective the reports can be grouped into the accompanying classifications:

(1) Reports Meant for Top Management

(2) Reports Meant for Middle Level Management

(3) Reports Meant for Junior Level Management

II. As indicated by Period:

(A) Routine Reports

(B) Special Reports

III. As indicated by Functions:

(A) Operating Reports

(1) Control Reports

(2) Information Reports

(3) Venture Measurement Reports

(B) Financial Reports

(1) Static Reports

(2) Dynamic Reports

5 | P a g e

The accompanying diagram clarifies this more about the sorts of reporting:

Figure 1: Types of Management Reporting

Why do management practices differ across firms and countries?

There is huge difference in productivity across countries for a substantial fraction of the difference in

average per capita income. Difference in productivity are typically calculated as a residual – that is,

productivity is inferred as the gap between output and inputs that cannot be accounted for by

conventionally measured inputs.

Differences in productivity to management practices has long been popular for television shows,

business schools and policymakers, it has been less popular among economists for two broad reasons:

1. Most of management literature is based on case studies rather than on systematic empirical data

across firms and countries.

2. Economists have tended to shy away from management based explanations for productivity

differences is a sense that changing management seems a relatively straightforward process. A

deep study reveals that the combination of imperfectly competitive markets, family ownerships of

firms, regulations restricting management practices and informational barriers allow bad

management to persist.

6 | P a g e

Figure 2: Management scores across countries

How can management practices be measured?

Bloom and Van Reenan (2007) has utilized meeting based instrument that characterizes and scores 1

("most exceedingly awful practices") to 5 ("best practices") upon eighteen fundamental management

practices. In that approach, a high score speaks to a best practice as in a firm that has embraced the

practice will, all things considered, build their profitability. The mix of a large number of these markers

reflects "great management" as it is plainly portrayed from the normal scores of 18 management

practices.

What causes differences in management practices?

Management practices vary substantially across countries and across firms, which raises different

questions. If improved management offers profitability gains, why would firms not adopt better

management practices?

The elements which cause difference in management practices are:

1. Product market competition: when product market competition is not very intense, some low

productivity firms will be able to survive. Syverson (2007b) showed that in a very homogenous

industry in US (ready mix concrete), more competitive geographic markets has a smaller tail of less

productivity plants.

7 | P a g e

2. Labor market regulations: Labor market regulations that constrain the ability of managers to hire,

fire, pay and promote employees could reduce the quality of management practices. Tough labor

market regulations are significantly negatively correlated with the management scores on

incentives. In contrast, more restrictive labor market regulations are not significantly correlated

with the management practices in other dimensions like monitoring and targets.

3. Ownership and meritocratic selection of the Chief Executive Officer: Since family firms typically

have less debt, product market competition may not be as effective in during then out of business if

they are badly managed. Firms owned by private equity appear to be well managed, in particular

when compared to family and government owned firms.

4. Multinationals and Exporters: Foreign multinationals are better managed firms than domestics

ones, presumably reflecting the selection effect that better managed firms are more likely to

become multinationals. Foreign multinationals seems able to partially “transport” their better

practices abroad despite after difficult local circumstances (Burstein and Monge-Noranjo (2009)).

5. Human Capital: Education is strongly correlated with high management scores, whether one looks

at the education level of managers or of workers.

Measuring Management Practices

To investigate these issues we first have to construct a robust measure of management practices

overcoming three hurdles: scoring management practices, collecting accurate responses, and obtaining

interviews with managers. We discuss these issues in turn.

Scoring Management Practices

To quantify management obliges arranging the idea of "good" and "awful" management into a

measure pertinent to distinctive firms over the assembling area. This is a hard undertaking as great

management is difficult to characterize, and is frequently dependent upon an association's situation.

Our beginning theory was that while some management practices are too unforeseen to be in any way

assessed as "great" to "awful", others can possibly be characterized in these terms, and it is these

practices we attempted to concentrate on in the overview.

To do this we utilized a practice assessment apparatus created by a main universal management

consultancy firm. So as to keep any view of predisposition with our study we decided to get no

budgetary backing from this firm.

The practice assessment device characterizes and scores from one (most exceedingly terrible practice)

to five (best practice) over eighteen key management practices utilized by modern firms. These

8 | P a g e

practices can be gathered into four regions: operations (3 works on), checking (5 practices), focuses on

(5 practices) and motivating forces (5 practices). The operations management area concentrates on the

presentation of incline assembling strategies, the documentation of procedures enhancements and the

basis behind presentations of upgrades. The observing area concentrates on the following elements of

performance of people, checking on performance (e.g. through general evaluations and occupation

arrangements), and outcome management (e.g. verifying that arranges are kept and proper endorses

and prizes are set up). The objectives area analyzes the kind of targets (whether objectives are just

monetary or operational or more comprehensive), the authenticity of the objectives (extending,

improbable or non-tying), the straightforwardness of targets (basic or complex) and the extent and

interconnection of targets (e.g. whether they are given reliably all through the association). At long last,

the motivating forces area incorporates advancement criteria (e.g. simply residency based or including

a component connected to individual performance), pay and rewards, and settling or terminating awful

entertainers, where best practice is regarded the methodology that gives solid prizes for those with

both capacity and exertion. A subset of the practices has likenesses with those utilized as a part of

studies on HRM practices.

Since the scaling may change crosswise over practices in the econometric estimation, we change over

the scores (from the 1 to 5 scale) to z-scores by normalizing by practice to mean zero and standard

deviation one. In our principle econometric details, we take the unweighted normal over all z-scores as

our essential measure of general administrative practice; however we additionally try different things

with different weightings plans taking into account variable investigative methodologies.

There is degree for true blue difference about whether these measures truly constitute "great

practice". In this way, an imperative approach to analyze the externality legitimacy of the measures is

to inspect whether they are related with information on firm performance developed from organization

records and money markets. We additionally look at whether the relationship between management

practices and efficiency is weaker in the Continental European countries to check for any "Somewhat

English Saxon" inclination in our management scores.

Gathering Accurate Responses

With this assessment apparatus we can, on a fundamental level, give some measurement of firms'

management rehearses. In any case, a critical issue is the degree to which we can acquire unprejudiced

reactions to our inquiries from firms. Specifically, will respondents give precise reactions? As is

understood in the studying writing (see, for instance, Bertrand and Mullainathan, 2001) a respondent's

response to study inquiries is normally one-sided by the scoring lattice, secured towards those answers

9 | P a g e

that they expect the questioner believes is "right". Also, questioners might themselves have

assumptions about the performance of the organizations they are talking and predisposition their

scores in view of their ex-risk observations. All the for the most part, a scope of foundation attributes,

conceivably connected with great and awful chiefs, may create a few sorts of efficient inclination in the

study information.

Lack of insight, loss of opportunity

Great management has all the earmarks of being so ardently connected with great performance that it

may be sensible to anticipate that all organizations will improve rehearses a need. The strategies of

good practice are, all things considered, accessible in people in general space in an extensive variety of

effectively available structures. Yet numerous organizations are still ineffectively overseen.

To look at conceivable reasons for this distinction, the most recent round of examination tried to assess

organizations' view they could call their own performance. As the last question in the meeting, subjects

were requested that survey the general management performance of their firm on a size of one to five.

To dodge false humility they were requested that avoid their own performance from the count.

Subjects' responses to this inquiry were not very much connected with either our management practice

score, or their own business performance. This circumstance connected in all districts, and improved or

all the more inadequately oversaw firms.

We discovered this absence of mindfulness striking. It proposes to us that the greater part of firms are

making no endeavor to contrast their own management conduct and acknowledged practices or even

with that of different firms in their segment. As a result, numerous associations are most likely passing

up a great opportunity for an opportunity for noteworthy change in light of the fact that they

essentially don't perceive that their own management practices are so poor.

Government action could help

A mixed bag of strategy components has an impact on organizations' adoption of good management

practices. Most critical among these were their focused surroundings and the adaptability of the nearby

work market.

Organizations in the overview were solicited to appraise the number from contenders working in their

business sector. The more contenders and organization reported, the higher its management practice

scores. This could be as a consequence of two impacts:

10 | P a g e

1) Great practice spreads rapidly in very focused situations, and

2) Poor practice is wiped out by normal choice as poorer performing organizations are expelled from

the commercial center.

Adaptable work markets ought to urge organizations to embrace better individuals’ management

practices so as to draw in and hold the best representatives. The bigger number of nations included in

the most recent examination, with broadly diverse work market environments, permitted this

speculation to be investigated inside and out.

The connection turned out to be an in number one. Organizations working in nations with more

adaptable work polices (measured utilizing the World Bank's measure of occupation law unbending

nature record) scored notably better in individuals management rehearses. The US, with its amazingly

adaptable occupation laws, had by a long shot the best individuals’ management record, a component

which contributed firmly to its general top position among reviewed organizations.

The accessibility of talented individuals, both in management and among the workforce when all is said

in done, is another essential distinction between better oversaw firms and the rest. 84 percent of

administrators in the most astounding scoring firms were taught to degree level or higher, similar to a

quarter of the non-management work power. Among the most minimal scoring firms, by difference,

just 53 percent of chiefs and just 5 percent of the more extensive workforce had degrees.

Conclusion

Based on the studies conducted by Nicholas Bloom and John Van Reenen published in The Journal of

Economic Perspectives Vol. 24, No. 1 (Winter 2010), pp. 203-224, ten conclusions had been discussed

based on management data.

1. Firms with “better” management practices tend to have better performance on a wide range of

dimensions: they are larger, more productive, grow faster, and have higher survival rates.

2. Management practices vary tremendously across firms and countries. Most of the differences are

the average management score of a country is due to the size of the “long tail” of very badly

managed firms.

3. Countries and firms specialize in different styles of management.

4. Strong product market competition appears to boost average management practices through a

combination of eliminating the tail of badly managed firms and pushing incumbents to improve

their practices.

5. Multinationals are generally well managed. They also transplant their management styles abroad.

11 | P a g e

6. Firms that exports (but do no manufacture) overseas are better managed than domestic non

exporters, but are worse managed than multinationals.

7. Inherited family owned firms who appoint a family member as Chief Executive Officer are very

badly managed on average.

8. Government owned firms are typically managed extremely badly.

9. Firms that more intensively use human capital, as measured by more educated workers, tend to

have much better management practices.

10. At the country level, a relatively light touch in labor market regulation is associated with better use

of incentives by management.

For companies

Multinational organizations have been compelled to take an efficient way to deal with management.

Just by having solid, compelling management rehearses set up have they possessed the capacity to

reproduce the same norms of performance crosswise over diverse districts, societies and markets.

Today, they are procuring the advantages of this exertion as far as higher efficiency, better profits for

capital and more powerful development.

The same advantages are effortlessly open to different associations, wherever they work. Yet

shockingly few organizations have made any endeavor to pick up knowledge into the nature of their

management practices. Those that do as such give themselves the chance to get to quick, savvy and

practical game changer.

For policymakers

Governments can play their part in encouraging the take-up of good management behaviour. Doing so

may be the single most cost-effective way of improving the performance of their economies. Strong

competition and flexible labor markets both lead directly to improved management performance.

Multinational companies have a strong positive effect too, and their influence is felt throughout the

regions in which they operate.

Relentless improvement in educational standards is also essential. Better-managed firms need more

highly skilled workers and they make better use of them, while better educated managers will be a key

component of the performance transformation that both established and emerging economies must

undertake if they are to maintain and improve their global competitive position.

12 | P a g e

Plagiarism Check Report:

For plagiarism check I have referred 3 online portals –

1. http://smallseotools.com/plagiarism-checker/

2. https://www.thepensters.com/free-plagiarism-checker-

report.html?id=4e15360419bd681add5a88ddd1fe4fce_1440180432:6663710

13 | P a g e

3. https://academichelp.net/plagiarism-

report/?id=625d43e58fad25e816a39ab1fc5f0d4a_1440180495:6663719