Embed Size (px)

Citation preview

i

MANAGEMENT OF FRAUD IN NIGERIA COMMERCIAL BANKS

BY

UKPAFE KINGSLEY UZUAJEME PG/MBA/07/46910

DEPARTMENT OF MANAGEMENT FACULTY OF BUSINESS ADMINISTRATION

SCHOOL OF POST GRADUATE STUDIES UNIVERSITY OF NIGERIA

ENUGU CAMPUS

AUGUST, 2009.

ii

TITLE PAGE

MANAGEMENT OF FRAUD IN NIGERIA

COMMERCIAL BANKS

(A CASE STUDY OF SELECTED COMMERCIAL BANKS)

BY

UKPAFE KINGSLEY UZUAJEME PG/MBA/07/46910

SUBMITTED TO THE DEPARTMENT OF MANAGEMENT IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR THE

AWARD OF MASTER OF BUSINESS ADMINISTRATION

(MBA) IN MANAGEMENT

DEPARTMENT OF MANAGEMENT FACULTY OF BUSINESS ADMINISTRATION

SCHOOL OF POST GRADUATE STUDIES UNIVERSITY OF NIGERIA

ENUGU CAMPUS

SUPERVISOR

DR C.A EZIGBO

AUGUST, 2009.

iii

CERTIFICATION

This is to certify that this project was carried out by Ukpafe

Kingsley U with Registration Number PG/MBA/46910, in the

Department of Management Faculty of Business Administration,

University of Nigeria, Enugu Campus (UNEC).

The work embodied in this research is original and has not

been submitted in part or full for any other degree of this or any

other university.

………………………………………. ………………………. Dr. C.A Ezigbo Date Supervisor ………………………………………. ………………………. Mr. C.O Chukwu Date Head of Department

iv

DEDICATION

This research work is dedicated to God Almighty for his infinite

mercy and love upon me throughout my stay in the university.

v

ACKNOWLEDGMENT

I wish to use this medium to express my profound gratitude to

a number of people who assisted me in various ways during the

course of my studies. I am grateful to God Almighty for his guidance,

mercies, protection and ever abiding presence, which made it

possible for me to cope with the programme.

I am indebted to my humble supervisor Dr. C.A Ezigbo, for her

immeasurable support and patience with me throughout this

research.

I am equally grateful to the Head of Department of

Management, Mr. C.O Chukwu for his stimulating academic

leadership. I cannot forget some of my Lecturers in the Department

of Management, for the knowledge they imparted in me. They

include Chief J.A Eze, Dr. U.J.F Ewurum and Dr. J.U.J Onwumere.

I am grateful to my family, my lovely and precious wife Mrs

Mabel Ukpafe, my children Marvelous, Dora and Divine Ukpafe and

my respectful sister Rosemary Ukpafe for their support and prayers

for me throughout my stay in the university.

I am particularly grateful to the management and staff of Union

Bank, Diamond Bank and Stanbic IBTC Bank for readily providing

vi

some of the data used in this research. Their unequalled

cooperation and assistance quickened the completion of this study.

May God, the rewarder of every good deed bless them abundantly.

Ukpafe Kingsley U. PG/MBA/07/46910

vii

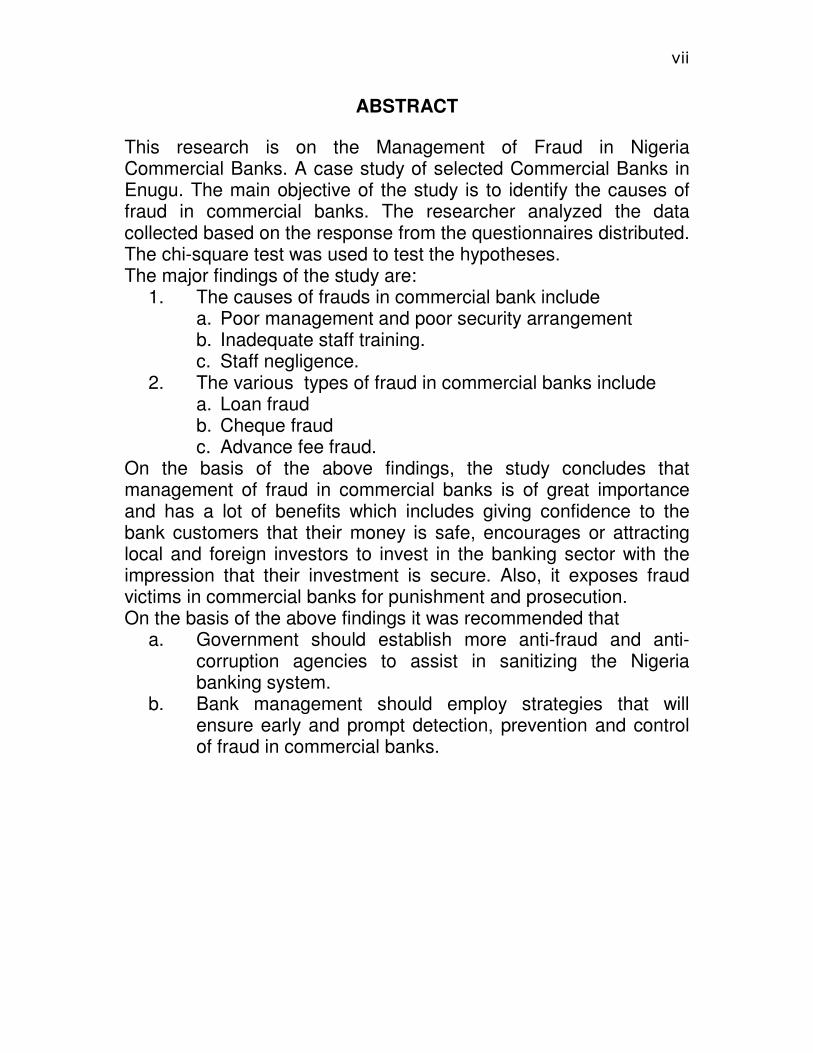

ABSTRACT

This research is on the Management of Fraud in Nigeria Commercial Banks. A case study of selected Commercial Banks in Enugu. The main objective of the study is to identify the causes of fraud in commercial banks. The researcher analyzed the data collected based on the response from the questionnaires distributed. The chi-square test was used to test the hypotheses. The major findings of the study are:

1. The causes of frauds in commercial bank include a. Poor management and poor security arrangement b. Inadequate staff training. c. Staff negligence.

2. The various types of fraud in commercial banks include a. Loan fraud b. Cheque fraud c. Advance fee fraud.

On the basis of the above findings, the study concludes that management of fraud in commercial banks is of great importance and has a lot of benefits which includes giving confidence to the bank customers that their money is safe, encourages or attracting local and foreign investors to invest in the banking sector with the impression that their investment is secure. Also, it exposes fraud victims in commercial banks for punishment and prosecution. On the basis of the above findings it was recommended that

a. Government should establish more anti-fraud and anti-corruption agencies to assist in sanitizing the Nigeria banking system.

b. Bank management should employ strategies that will ensure early and prompt detection, prevention and control of fraud in commercial banks.

viii

ix

TABLE OF CONTENTS

Cover Page

Title Page - - - - - - - - - i

Certification - - - - - - - - ii

Dedication - - - - - - - - - iii

Acknowledgement - - - - - - - iv

Abstract - - - - - - - - - v

Table of Contents - - - - - - - vi

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study - - - - - 1

1.2 Statement of the Problem - - - - - 3

1.3 Objectives of the Study - - - - - 4

1.4 Research Questions - - - - - - 4

1.5 Research Hypotheses - - - - - - 5

1.6 Significance of the Study - - - - - 6

1.7 Scope and Limitations of the Study - - - 6

1.8 Definition of Terms - - - - - - 7

References - - - - - - - - 10

x

CHAPTER TWO

REVIEW OF RELATED LITERATURE

2.0 Origin of Fraud - - - - - - - 11

2.1 What is Fraud? - - - - - - - 12

2.2 What is Bank Fraud? - - - - - - 14

2.3 Major Causes of Fraud in the Commercial Banks - 26

2.4 Implications of Fraud on the Bank and Entire Economy of

Nigeria - - - - - - - - 35

2.5 Punishment and Penalties to Fraud Perpetrators - 39

2.6 Fraud Detection, Prevention and Control - - 42

2.7 Government Effort towards Fraud Control - - 60

2.8 CBN and NDIC Effort to Fraud Control - - - 62

2.9 Extent of Fraud in Banks - - - - - 62

References - - - - - - - - 65

CHAPTER THREE

RESEARCH METHODOLOGY

3.0 Introduction - - - - - - - 66

3.1 Area of the Study - - - - - - 66

3.2 Source of Data - - - - - - - 66

3.3 Population and Sample Size Determination - - 67

xi

3.4 Instrument Used For Data Collection - - - 70

3.5 Method of Data Analysis - - - - - 71

3.6 Validity and Reliability of Data - - - - 73

References - - - - - - - - 74

CHAPTER FOUR

DATA PRESENTATION, ANALYSIS AND INTERPRETATION

4.0 Data Presentation and Analysis - - - - 75

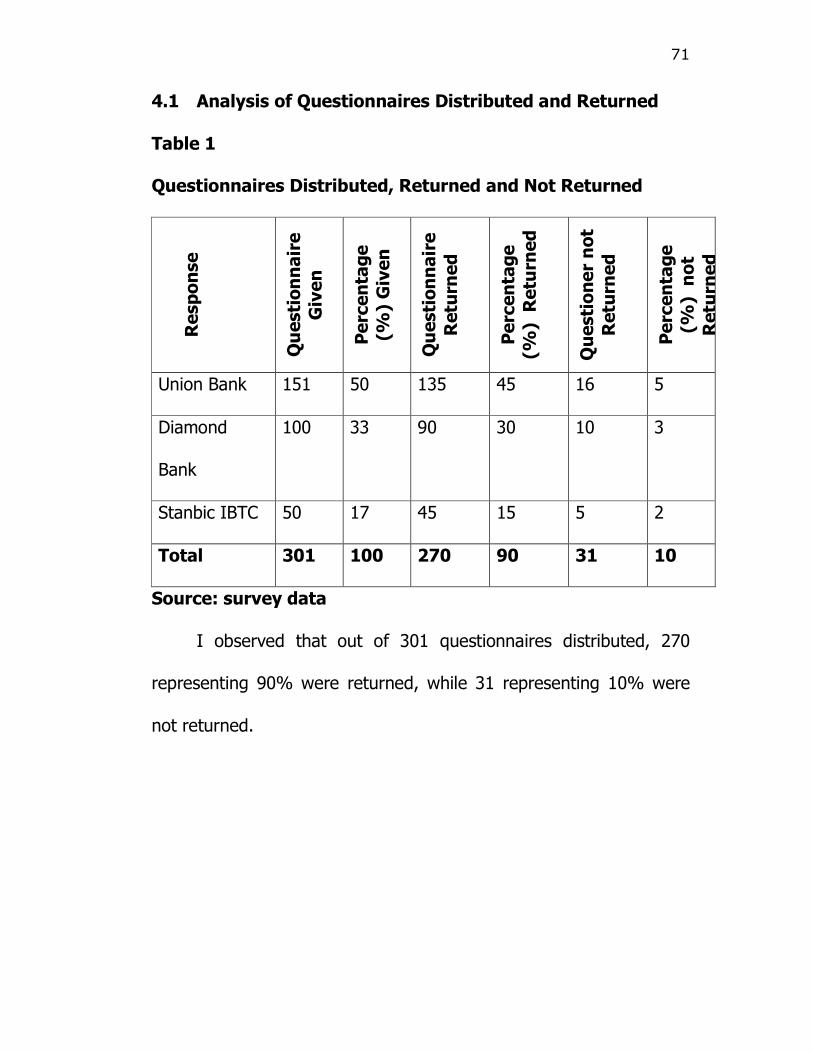

4.1 Analysis of Questionnaires Distributed and Returned 88

4.2 Testing of Hypotheses - - - - - - 88

CHAPTER FIVE

SUMMARY OF FINDINGS, CONCLUSION & RECOMMENDATIONS

5.1 Major Findings - - - - - - - 100

5.2 Conclusion - - - - - - - - 101

5.3 Recommendations - - - - - - 101

Bibliography - - - - - - - - 103

Appendix A - - - - - - - - - 106

1

2

CHAPTER ONE

1.0 INTRODUCTION

1.1 BACKGROUND OF THE STUDY

The term irregularities are used to refer to intentional distortion

of financial statements, for whatever purpose and to

misappropriations of assets, whether or not accompanied by

distortions of financial statements. Fraud is one type of irregularity.

In auditing guideline, the word fraud is used to refer to irregularities

involving the use of criminal deception to obtain an unjust or illegal

advantage.

Fraud may entail that proper accounting record have not been

maintained, it may also indicate that some internal controls are not

effective and that the auditor cannot rely on these internal controls.

Existence of Fraud in financial statements could jeopardize the

statements from showing true and fair view and complying with the

companies and Allied Matter Acts (CAMA) 1990.

Therefore, fraud in banks must be looked at generally as “acts

that involve the loss of assets by banks through deceitful and

dishonest means. The intention of the fraudster is to dishonestly

benefit himself to detriment of the bank or bank staff or bank

customer or any other member of the public via banking operations.

3

Fraud can be committed by bank customer, bank customer, bank

staff and customers or a third party that is non-customers. (Eze,

2004).

1.2 STATEMENT OF THE PROBLEM

Fraud in the Nigerian Commercial Banks has remained an

unavoidable problem and has also resisted all practicable treatment.

The incidence has not only become incessant but also been on the

increase in the recent past.

Although, it has assumed global dimension, the rate of growth

in Nigeria has been outstanding in sophistication from N1542.91

million in 1996, the amount involved in commercial banks alone rose

to N3590.31 million in 1997. Where as the actual/expected loss went

from N371.08 million to N224.54 million (NDIC). This has affected

the commercial banks profitability in no small measure.

The general confidence reposed in the banking institutions has

become eroded since the new concepts of distress, bank failures and

closures of 1990’s. From available records, out of about 115 financial

institutions operating in the country as at 1996, surprisingly 52 were

distressed while 6 were acquired. With the frequent of fraud, people

are no longer at ease keeping their monies in the commercial banks

4

but prefer to keep them in their houses or concretizes them in wares

(an uncivilized practice for underdeveloped economy).

The internal control measures in the commercial banks seem to

have faults. Such that, it has aided the perpetration of fraud. As a

result, the industry shares 90% of all cases of malpractices, forgeries

and frauds. (Wiki pedia 2007).

1.3 OBEJECTIVES OF THE STUDY

The specific objectives of the study include the following.

a. To identify the causes of fraud in commercial banks.

b. To identify the types of fraud in commercial banks.

c. To evaluate the extent of fraud in commercial banks.

d. To evaluate how fraud is detected and controlled in Nigeria

commercial banks.

1.4 RESEARCH QUESTIONS

The study poses the following research questions.

i. What are the causes of fraud in commercial banks?

ii. What are the various types of fraud in commercial banks?

iii. What is the extent of fraud in commercial banks?

5

iv. How is fraud detected and controlled in Nigeria commercial

banks.

1.5 RESEARCH HYPOTHESES

For the purpose of the study the following research hypotheses

will be formulated and tested.

1. Ho: Poor management and poor security arrangement in

commercial banks cannot cause fraud.

Hi: Poor management and poor security arrangement in

commercial banks can cause fraud.

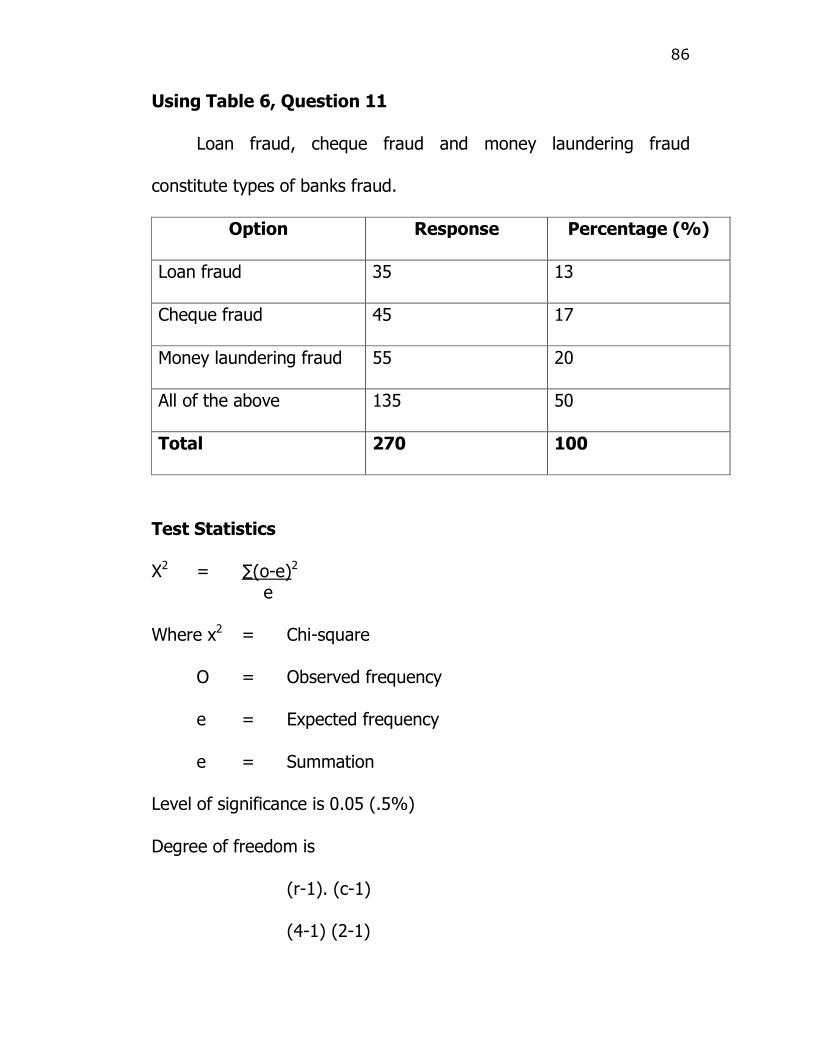

2. Ho: Loan fraud, cheque fraud and money laundering

fraud do not constitute types of banks fraud.

Hi: Loan fraud, cheque fraud and money laundering fraud

constitute types of banks fraud.

3. Ho: The extent of fraud in commercial banks is high.

Hi: The extent of fraud in commercial banks is low.

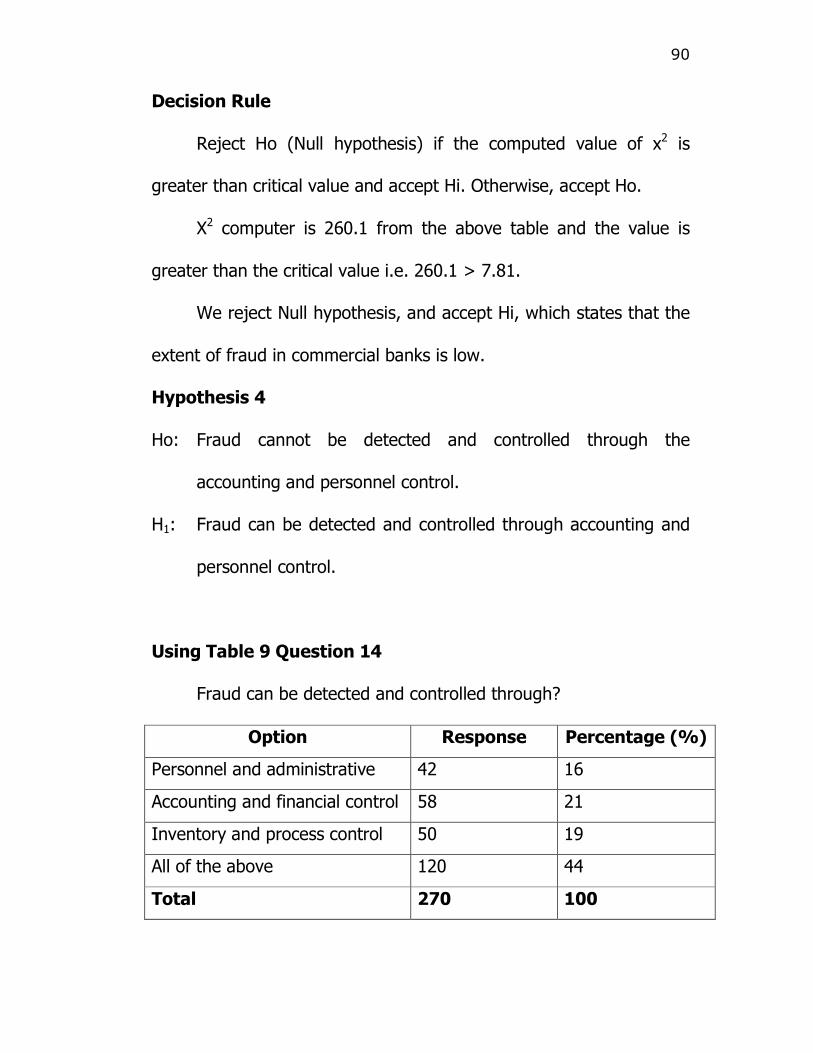

4. Ho: Fraud cannot be detected and controlled through the

accounting and personnel control.

Hi: Fraud can be detected and controlled through the

accounting and personnel control.

6

1.6 SIGNIFICANCE OF THE STUDY

The study of this nature is expedient as well as timely, coming

at a time when central bank of Nigeria and Nigerian deposit

insurance corporation (NDIC) and government and it’s agencies are

doing something to curb the menace of fraud in commercial banks.

The study will raise public awareness of the presence of fraud in

commercial banks it will also generate public awareness of the

existence of anti-fraud investigators; this will encourage and assist

those who witness or suspect fraud being committed by people to

report it and provide evidence.

This study will sensitize the public on the adverse effect of

fraud on commercial banks and the Nigerians economy at large. It

will equally serve as a reference Material for researchers in the same

field.

1.7 SCOPE AND LIMITATIONS OF THE STUDY

The study focuses on management of fraud in Nigeria

commercial banks. The main constraints of the study include.

Time Constraint:

Due to limited time given for the study, the researcher could

not get all the information needed for the study.

7

Financial Constraint:

The researcher has not got enough money to embark on the

study. Due to financial constraint, the researcher could not visit

places where information relevant to the study could be obtained.

Attitude of the Respondents.

Some of the respondents show negative attitude towards the

study because they felt that they have no financial benefit.

1.8 DEFINITION OF TERMS

Commercial Banks:

Commercial bank is any Bank whose business includes the

acceptance of deposits withdrawable by cheque or cash (Okeke,

1996).

Assets:

Assets is what a person or business owns. Castle and Owen (1992).

Fraud:

“Fraud” refers to an intentional act by one or more individuals among

management employees or third parties which results in a

misrepresentation of financial statement. (Adeniyi, 2004).

8

Auditor:

Auditor is an independent person or body charged with the

responsibilities of preventing, detecting financial irregularities (Fraud)

which might impair the truth and fairness of the view given by the

financial statements. (Eze, 2001).

Auditing:

Auditing is the process carried out by the independent examination

of and expression of opinion on the financial statements of an

enterprises by an appointed auditor in pursuance of that

appointment and in compliance with any relevant statutory

obligation. (Adeniyi, 2004).

CBN:

Central Bank of Nigeria.

NDIC:

Nigeria Deposit Insurance Corporation.

Capital Base:

Capital base is the amount contributed by the powers of a business

which gives them right to enjoy all the future earnings

(Anyanwokoro, 1996).

9

Shareholders Funds:

Shareholders Funds are paid up capital, share premium, statutory

reserves, retained earning (Undistributed profit) general reserves,

minority interests and other subsidiary reserves excluding preference

shares and revaluation reserves (Iganiga and Anyanwokoro, 1996).

10

REFERENCES

Adeninyi, A. (2004): Auditing and investigations, Lagos El- Toda Venture limited.

Castle, E.F. and Owens P.N. (1992): Elements of Banking 2nd Edition.

New York, Pretince Hall. Eze, J.C. (2004): Principle and Techniques of Auditing Volume II,

Enugu, Computer Edge Publishers. Johnson, U.O (2007) Introduction to project writing, Enugu. New

Dimension Publishers.

11

CHAPTER TWO

2.0 REVIEW OF RELATED LITERATURE

2.1 Origin of Fraud

It is very difficult to trace the origin of fraud however, in the

case of fraud perpetration, Adewole, 1990, opines that any minor

mistakes by an individual which is not detected in time or at all

makes such an individual to think that the success of such mistakes

may be taken advantage of and may proceed to enact more

mistakes, this time, deliberately so as to test the system’s check and

balance. He stresses that where a deliberate mistake is made and is

successful, the individual takes benefit of it for selfish end. He refers

to this behaviour as fraud, since it is now a deliberate action aimed

at dishonestly enriching the individual. The next logical step for such

an individual is definitely to continue with such errors until he

eventually graduates to a hardened fraudster.

It can therefore be deduced that the genesis of fraud is

traceable to the committal of minor, undetected mistakes, which are

consequently capitalized upon by individual intending to defraud.

(Adewole, 1990).

12

2.2 What is Fraud?

Fraud has been variously defined in the literature. Most

developing countries of the world regard fraud as criminal act. In

Nigeria, it is equally recognized as a crime too, this promoted the

promulgation of decree on fraud and other fraud related matters/

structures namely “the failed Banks and recovery of public debts

decree 18 of (1994), Banks and other financial institution decree

(BOFID) 1991, money laundering Act No 3 of 1995 Federal

Intelligence Investigation Bureau (FIIB), Independence Corrupt

Practices Commission (ICPC) and Economic and Financial Crime

Commission (EFCC).

According to Oxford Advance Learners Dictionary of Current

English “Fraud” is defined as “a criminal act/ deception. According to

Udok (1992) Fraud is concerned with the activities of those who seek

to divert to their pockets the fruits of others hard work. Adeniyi

(2004) sees Fraud as an intentional act by one or more individuals,

among management, employees or third parties which results in a

misrepresentation, of financial statements which involve.

1. Manipulation falsification or alteration of records or

documents.

2. Misappropriation of Assets.

13

3. Suppression or omission of the effect of transactions from

records or documents.

4. Recording of transaction without substance.

5. Misapplication of accounting policies.

According to Adekanye (1983) “Fraud” is an act of falsifying or

altering of a writing document for the purpose of doing injury to

another person. He therefore, continued by saying any alteration of a

writing document made with intention to defraud is therefore

forgery”.

According to Wiki pedia (2007) fraud is any insidious, sneaky

crime that ruins individuals and families, causes corporation to go

under. Eze (2004) refers to fraud as irregularities involving the use

of criminal deception to obtain an unjust or illegal advantage.

Another definition of fraud put it that, it is an act by which one

person intends to gain a dishonest advantage over another person.

2.3 What is Bank Fraud?

Frauds in the banks are not new they are as old as the industry

itself. Bank fraud can be defined as a conscious or deliberate effort

aimed at obtaining unlawful financial advantage at the detriment of

another person who is the rightful owner of the fund. Orjih (1998).

14

Bank fraud must be looked at generally as acts that involve the loss

of assets by banks through deceitful and dishonest means. The

intention of the fraudster is to dishonestly benefit himself to the

detriment of the bank or bank staff or bank customer or any member

of the public via banking operations. Fraud can be committed by

bank customers, bank staff or a combination of staff and customer or

third parties that is non-customers.

Also, bank fraud as a canker worm has eaten deep gradually

into our social fabric and a concerted effort by individual,

government, bank staff and authorities concerned will be required to

minimize its occurrence. Unfortunately, bank managements are

generally unwilling to release details of frauds that may have been

perpetrated in their banks for fear of loosing their corporate image.

Eze (2004).

2.4 Nature and Types of Bank Frauds

Frauds in banks vary widely in nature, character and methods

of operation. In general, fraud perpetrators, using different methods

of fraud perpetration, can commit bank fraud. On the basis of

perpetrators, bank fraud may be categorized into three groups

(Shogotola, 1994).

15

a. Internal Fraud

b. External Fraud

c. Mixed Fraud.

a. Internal Perpetrators of Fraud: This relate to members of staff

(insiders) Accountant, Executives Assistants, supervisors, clerk

(cashier), typist/ stenographers, Technicians, Drivers, Cleaners

etc.

b. External Fraud: are fraud related to those committed by

persons not connected with the bank. A typical example was

that of the armed robbery attack either during the banking

hours or during special movement of cash in transit). More so,

some external fraud could result through carelessness and

recklessness or negligence on the part of some customers.

Often times, it comes through corporate accounts in which a

dishonest staff may have access to the company’s cheque

book.

c. Mixed Fraud: These are fraud committed by collusion between

the insider staff and outsiders customers. It is general belief

that no successful fraud is perpetrated without the aid of an

insider staff, for instance, in one of the outrageous armed

robbery incident in 1986 against Union Bank Plc, Nnewi. The

16

staff dispositions charts recovered from the bandits was alleged

to have been designed by a number of staff (insider) that is

why Shongotola cautions that the banking industry has become

not just a battle front with a clear-cut firing line between banks

and the fraudster but a veritable minefield on which some

banks and their top management staff are in secret league

with the enemy.

Categorization on the basis of methods of perpetration is the

most common form of classification employed by banks. Here, the

list of types of fraud is inexhaustible as new methods are devised

with time. However, shongotola identify the following.

• Outright theft and embezzlement.

• Defalcation.

• Forgeries and insider abuse.

• Suppression.

• Fraudulent substitution.

• Tampering with reserve.

• Payment against uncleared effects.

• Unauthorized lending.

• Lending to “Ghost” borrowers.

• Kite flying and cross firing.

17

• Unofficial borrowing.

• Foreign Exchange Malpractices.

• Impersonation.

• Teaming and lending.

• Fake payments.

• False proceeds of collections.

• Influence of evil forces.

• False declaration of cash shortages.

• Ficticious accounts.

• Ledger cards manipulation.

• Misuse of suspense accounts.

• Manipulation of vouchers.

• Dry posting.

• Over invoicing.

• Over/ under valuation of properties.

• Inflation of statistical data.

• Duplication of cheque books, drafts, stamps etc.

• Interception of clearing cheques.

• Interception and switching of telex messages

• Ficticious contracts.

• Laundering.

18

• Computer frauds.

However, the bank administration institutes identify the

following as the most important and common types of bank fraud:

i. Advance Fee Fraud (419).

ii. Cheque kiting.

iii. Account opening fraud.

iv. Letter of credit fraud.

v. Money transfer fraud.

vi. Loan fraud.

vii. Counterfeit securities.

viii. Cheque fraud.

ix. Money laundering fraud.

x. Clearing fraud.

xi. Computer fraud and

xii. Telex fraud.

i. Advanced Fee Fraud (419):

Fee may involved an agent approaching a bank, a company or

an individual with an offer to access large funds at below market

interest rate often for long term. The purported source of such funds

is not specifically identified as the only way to have access to it is

through the agent who must receive fee or commission “in advance”

19

as soon as the agent collects the fee, he disappears into the air and

the facility never comes through. Any bank desperate for funds

especially the distressed banks and banks needing huge funds to

bid for foreign exchange can easily fall victim to this type of fraud

when the deal fails and the fees paid in advance is lost, these victims

are not likely to report the losses to the police or to the authorities.

ii. Cheque Kiting:

Kiting is defined by the United States Controller of the

currency’s policy, guidelines for national bank directors as “a method

whereby a depositors utilizes the time required for cheque to clear to

obtain an unauthorized loan without interest charge”. The aim of the

cheque kiter is to use these uncollected funds interest free for a

short time to overcome a temporary cash shortage or to withdraw

the funds permanently for personal use.

iii. Account Opening Fraud:

This involves the deposit and subsequent cashing of

fraudulent cheques. It usually starts when a person not known to the

bank asks to open a transaction account such as current and saving

account with false identification but unknown to the bank.

20

iv. Letters of Credit Fraud:

Letters of credit generally arise out of international trade and

commerce. They stimulate trade across national boarders by

providing a vehicle for ensuring prompt payment by financially sound

commercial banks. However, in some areas of the world, fraud has

historically been a problem. In Nigeria (Nnewi) in particular, letter of

credit (L/C) Fraud rate is statistically high as a result of importation

of motor parts and other machines.

v. Money Transfer Fraud:

Money transfer services are means of moving fund to or from a

bank to a beneficiary account at any banking point worldwide in

accordance with the institution from the banks customers. Some

common means of money transfers are mail, telephone, cheques-

over the counter, telegraphic, electronic process, telex and bill of

exchange. Fraudulent money transfer may result from a request

created solely for the purpose of committing a fraud or the alteration

of a genuine funds request by changing the beneficiary’s name or

account number or changing the amount off the transfer.

vi. Loans Frauds:

Loan and other form of credit extensions to business and

individual customers constitute traditional function of commercial

21

banks. In process of credit extension fraud may occur at any stage

from the first interaction between the customers and the bank to the

final payment of the loan. Loan fraud occurs when credit is extended

to non-borrowing customer or to a borrowing customer who has

exceeded his credit ceiling. The fraudulent aspect of this class is that,

there is intent to conceal it from the head office (inspectorate) staff

on routine check to deceive them with plausible but falsified

statements, documents etc. advanced perpetrators of credit fraud to

the extent to applying credit facility approved for one customer to

credit another who is often unrelated to be first customer, that is to

say a credit facility for a customer “A” yet to be drawn is directed to

the use of customer “B” (Anaeto, 1996).

vii. Counterfeit Security Fraud:

Like counterfeiting of money, counterfeiting of commercial

financial instrument is one of the oldest forms of crime. Modern

photographic and printing equipment has greatly aided criminals in

reproducing good quality forged instruments. According to Agba,

documents may be total counterfeit or may be genuine documents

that are copied, forged or altered an amount payment date, payee or

terms of payment. A common fraud is to present the counterfeit

stocks or bonds as collected to loan. Other counterfeit items such as

22

treasury notes, cashier cheque, bankers acceptances or certificates

of deposit in counterfeit or altered forms may be presented to a

commercial bank for redemption. The presenter would drawn out the

proceeds or disappear before the financial instruments are found

counterfeit.

viii. Cheque Fraud:

This is use as a means of payment or paying for financial

obligations is an essential features of modern economy. Cheque

fraud is now common involving millions of naira annually. Common

types of cheque are personal, business, government travelers,

certified drafts and counter cheque with each having its own

characteristics and vulnerabilities of fraudulent use. The most

common of cheque fraud involve cheques that are stolen, forged

counterfeit or altered.

ix. Money Laundering Fraud:

This is a means to conceal the existence source or use of

illegally obtained money by converting the cash into untraceable

transactions in banks. The cash is disguised to make the income

appear legitimate Commercial Banks as well as other banks should

be advised to avoid handling such funds (Umunna, 1989)

23

x. Clearing Fraud:

Most clearing fraud hinge on suppression of an instrument so

that at the expiration of the clearing period applicable to the

instrument the collecting bankss will give value as through the

paying bank has confirmed the instrument good for payment.

Clearing cheques can also assist fraudsters to complete a clearing

fraud. This is to say a local clearing item can be routed to an up

country branch. In the process of re-routing the instrument to the

proper branch, the delay entailed will give the collecting branch. The

impression that the paying bank has paid the instrument. (Ifeduba,

2002).

xi. Telex Fraud:

Transfer of funds from one location to another can be affected

through the telex. The message though often coded can be altered

(decoded) to enable diversion of the funds to an account not

originally. (Ifeduba, 2002).

xii. Computer Fraud:

Computer fraud can remain undetected for long time. It can

take the form of corruption of the program or application packages

and be ever breaking into the system via a remote sensor by a

24

computer specialist or a programmer. Diskettes can be tampered

with to gain access to unauthorized areas or even give credit to an

account for which the funds were not originally intended. Computer

fraud do rarely occur but when it happens, large sums of money are

lost. (Shongotla, 1994)

2.5 Major Causes of Fraud in the Commercial Banks

Many authors have analyzed in some write-ups different causes

of fraud in the commercial banks.

Shongola, 1994 grouped the major causes of fraud usually into

two classes:-

a. Institutional Factors

b. Environmental or societal factors.

The institutional factors are those traceable to the internal

environment of the financial institution while the environmental or

societal factors are those which result from the influence of the

environment or society of the banking industry.

Institutional Causes of Fraud

According to shongotola, institutional causes of fraud are

classified below;-

1. Volume of Work:

25

The amount of work done by officials could be heavy that

fraud could easily pass undetected by such officials.

2. Number of Staff:

Where an official supervises quite a large number of

staff, there is a high likelihood that fraud could go undetected.

3. Nature of Services:

Fraud may be caused where documents of value and

liquid assets (cash) are exposed to an indiscipline staff or

unauthorized persons, for example, customers.

4. Banking Experience of Staff:

Frauds in commercial banks occur with higher frequency

among staff with little experience and knowledge in financial

practice. The more the experience and knowledge of a staff,

the less the likelihood that fraud would pass such staff

undetected unless with the active support of the staff. Where

professionally qualified finances are involved in fraud, they are

more likely to swindle large chunks of money than less

qualified staff.

5. Inadequate Staff Training:

This could affect the morally weak as well as orally

robust staffs in various ways. Lack of knowledge of the ways of

26

dealing with fraudulent practices in commercial banks could

affect an otherwise honest staff in apprehending and avoiding

the tricks of bank fraudsters.

6. Poor Management:

Commercial banks with poor management record higher

incidence of all sorts of frauds than those with effective

management. Poor management give rise to in-effective and

poor control system, indiscipline among staff and this create an

environment for fraud to flourish.

7. Staff Negligence:

In certain cases, staff negligence could give rise to the

perpetration of fraud in commercial banks. Negligence itself is

a product of several factors including poor supervision, lack of

technical knowledge, apathy and pressure and lack of cognate

experience.

8. Recruitment System:

In the past, recruitment of staff into the banks was

strictly on merit. However, nowadays, poor recruitment and

selection system where cognate experience, relevant technical

knowledge, competence, character and other sterling qualities

are sacrificed on the alter of non performance related factors

27

such as connections and tribalism constitute important

facilitator of fraud in financial institution or commercial banks.

9. Poor Security Arrangement for Documents:

In commercial banks where security arrangements for

valuable documents are week, poor and vulnerable, it is easy

for fraudsters to have their way without detection.

10. Lack of Adequate Job Rotation:

The longer a staff stays in a particular job “ceteris

paribus” the more proficient he is likely to be however, when a

staff over stays her tenure on job, it can encourage fraud as

the perpetrator is assumed of the fact that no one is likely

unearth his fraud.

11. Use of Sophisticated Accounting Machine:

Where sophisticated accounting machines are in use are

manned by inadequately equipped staff, errors could arises and

thus lead to the production of unreliable records. In the hands

of dishonest staff, sophisticated accounting machines could be

employed to deliberately omit entries substitutes improper

calculation and posting, manipulating documents, substitute,

28

fictitous documents and alter genuine ones. All these are

different ways of perpetrating fraud in commercial bank.

12. Inadequate Motivation:

Management practices, when negative to the aspiration

and developmental needs of staff could result in the generality

of staff being frustrated. Frustration in turn can result to

fraudulent practices in commercial banks.

13. Inadequate Infrastructures:

Poor communication system, power failure and frequent

network failure or breakdown which result in backlog of

unbalanced postings congested office space etc. are some

factors which encourage the perpetration of fraud in

commercial banks.

14. Lapses in the Management Control System of Corporate

Customers:

This is classic example where frauds could be externally

hatched and executed. Fraudulent staff in both commercial

banks and in the employment of corporate customers could

collude to take undue advantage of lapses observed in the

management control systems of corporate customer.

15. Negligence by Customers:

29

Traditionally, it is the negligence on the part of

customers that provide ample opportunities to staff or

commercial banks perpetrate frauds. Negligence by customers

takes various forms, consisting errors that might have been

genuine but which are open to abuse, distortions and

defalcations unscrupulous staff both within and outside the

institution in the employment of customer.

Environmental /Societal Causes of Fraud

According to shongotola,1994 Environmental causes of fraud are

classified below:-

1. Personality profile of dramatize personnel:

Most individuals with inordinate ambitions without

qualms are prone to committing frauds. This kinds of individual

is bent on making money by hook or by crook. Such people

dismiss morality as an unnecessary or requisite for virtuous life.

To them the end justifies the means they are usually

unscrupulous and opportunistic.

2. Societal Value:

As for Fagbami, 1990 the value system in any society is

the sets of rules that prescribes what is right or wrong within

30

that society. When the possession of wealth determines the

reputation ascribed to a person, that society is bound to

witness unnecessary competition for acquisition of wealth. This

no doubt will lead to some people using dubious means to get

rich overnight. It can be argued that the main causes of fraud

in commercial banks are traceable to the general dishonest in

society where morality is thrown to the dogs. Misplacement of

society values, unquestioning attitudes of the society towards

the sources of wealth. The rising societal expectations from

staff of commercial banks and the subsequent desire by such

staff to live up to such expectations are also contributory

factors to fraud.

3. Slow and Tortuous Legal Process:

Delays in prosecution of fraud cases have a way of

frustrating the parties to the cases. A frustrated party can

abandon the case midway leading to miscarriage of justice.

The delays can be form of:

a. Lack of specialized manpower for the investigation of

fraud.

b. Late reporting of cases to police.

31

c. Lawyers and persecution witness absenting

themselves from court.

d. Undue delay in the investigation and charging of cases

to court and

e. Frequent adjournment by the court could frustrate

appellant and favour the defendant.

All these make fraudsters to have feeling that they are above

the law and as such can get away with any act of illegality.

(Adewole, 1990)

4. Lack of Effective Deterrence & Punishment:

Although this may be considered as a most point, it is

argued in some quarters that lacks of effective deterrent such

as heavy punishment could be factor that contributes to non-

abetting perpetration of fraud in commercial banks.

5. Fear of Negative Publicity in Reporting Fraud Cases:

Many commercial banks fail to report fraud cases to the

authorities. They believe that doing so will give unnecessary

negative publicity to their institutions, this attitudes encourages

individuals with inordinate to defraud in commercial banks.

They reason correctly that effected institution may not

prosecute them. It is even said to note that some staff whose

32

appointment have been terminated or retired prematurely are

still manage to secure appointments in other commercial

banks. (Shongotola 1994)

2.6 Implications of Fraud on the Bank and entire Economy

of Nigeria

According to Wikipedia, 2007 the following are the various

implications of fraud on the banks and the entire economy of Nigeria.

i. Down Turn in the Economy:

For the past 18 years or so our economic development

has witnessed a serious set-back with graduates roaming the

streets in search of employment which are not available.

Various government polices to revamp the economy though

appear laudable were all frustrated at the implementation

stage because some of the people responsible for

implementing them are fraudulent. Both the political and

economic situation declined from bad to worse with naira

witnessing an unprecedented devaluation of 1,300% within five

years. As at December 2008 and January 2009 the naira

exchange rate with the stood between N149 to N150 per

$1.Devil then found job as idle hands were meant to engage in

one kind of fraud or the other while "419, cocaine pushing,

33

billion naira bank frauds", becoming regular features of our

newspaper, Television and Radio headlines.

ii. Termination/Retirement of Staff:

As a result of this very serious economic crime, some

staff in the industry have either been dismissed, or have their

appointment terminated or prematurely retired. This means

that some experienced hands in the sectors are lost due to

their involvement in frauds and forgeries. During and after the

consolidation exercise that took place in the Nigerian banking

industry it was revealed by the central bank that some bank

directors and senior managers of those banks that couldn't

meet up the N25 billion minimum capital base gave themselves

unserviceable loans in hundreds of millions. The Nigerian

Deposit Insurance Corporation is still in court with those

involved in this unethical behavior. Our problem is that most of

those involved these economic crimes are highly placed or

senior politicians. We can't know their names simply because of

their positions in the country.

iii. Global Perception:

Nigeria has become synonymous with fraud as some of

its citizens use the boom in internet fraud and corruption has

34

become an unfortunate staple in Nigeria’s international

reputation. The country regularly features at the top of

international surveys measuring the part played by graft in

different economies. Successive dictatorships have extracted

billions from the exchequer, denuding the public purse of

revenues from Nigeria's rich oil reserves. Outside the country

Nigeria has become synonymous with fraud as some, of its

citizens use internet and the boom in of cafes to send "spam"

emails, promising millions in exchange for the gullible

recipient's bank details. This makes it difficult for genuine

business men from Nigeria to go into international business

with foreigners or secure credit overseas.

iv. Frauds deplete shareholders funds and lead to loss of money

belonging to customers. This loss invariably results in a

reduction of the available resources, which could lead to the

collapse of the affected bank. These banks are also deprived of

faithful and honest applicants who might be unwilling to apply

for fear of being associated with fraud. Fraud causes

termination, dismissals and retrenchment of staff who may not

be fraudsters, resulting in losing experience staff.

35

v. The welfare of staff may also be adversely affected in a bank

with persistent fraudulent practices. No worker or staff will

have the courage to fight for staff welfare matters such as

promotion, increased salaries, and improvement in general

working condition.

vi. Bank frauds erode public confidence in the banking system.

This constitute a serious set back to the efforts geared at

promoting bank habit in a country where numerous people

prefer to keep their money at home.

vii. Another effect of frauds on bank is that it destroyed the

nation economy and it sovereignty since banking sector help

to survive the economy of the nation through money in

circulation. We are all living witnesses to how Nigerian

sovereignty was called into question and its international

trade threatened when a foreign power issued an ultimatum

to its (Nigerian) National Assembly to pass a bill on financial

malpractice. Had the national assembly failed to pass the bill,

the country would have faced international sanctions.

36

2.7 Punishment and Penalties to Fraud Perpetrators

We appreciate the effort of the federal military government

towards fraud control as represented through the sub-structures set

up via security and exchange commission (SEC) for the capital

market operations. Federal Mortgages Institutions (FMI), National

Board for Community Banks (NBCB). For community Banks,

Insurance Supervisory Board (NISB), For Insurance Companies, the

Central Bank of Nigeria (CBN), decree, National Drug Law

Enforcement Agency (NDLEA), banks and other financial institution

decree (BOFID), Nigerian Deposit Insurance Corporation decree

(NDIC), Companies and Allied Matter Acts (CAMA), Money

Laundering Degree (ML) Economic Sabotage decree (ESD), Failed

Bank and Debt Recovery (FBDR), others are Justice, the police, the

judiciary and even the armed forces, economic and financial crime

commission (EFCC) and Independent Corrupt Practices Commission

(ICPC).

All these are reasonable pointers to the facts that our financial

system is riddle with fraud. Perhaps, the recent bank return to NDIC

on fraud and forgeries in commercial banks revealed that the

phenomenon has assumed an unimaginable level with this in mind

the monetary authorities (CBN), (NDIC) involved the Federal

37

Intelligence Investigation Bureau (FIIB) as well as the setting up of

tribunal. For example the federal intelligence investigation bureau

are empowered to arrest, detain, prosecute and even confiscate

property of persons accused of any fraudulent practices and the

promulgation of decree No. 18 of 1994 Failed Bank and Debt,

financial malpractices empowered to arrest, detain, prosecute and

even confiscate property of persons directly or indirectly connected

to the failure or distress of any financial institution even where the

person secured assets have been sold off by the banks.

So also, the provision of section 39 and 40 of NDIC decree 232

1988 stressed the need for returns or dismissed, terminated,

disengaged and Retire bank staffs involved in fraud and fraud related

offences

Within the bank, there are internal punishments. Staff who has

any action of fraudulent intentions/behaviors face disciplinary action

via suspension for indefinite period with half pay, denial of year

increment, bonus, demotion, inspection report.

Again, the money laundering decree No 3 of 1995 requires all

commercial banks to disclose to the National Drug Law Enforcement

Agency (NDLEA) and the CBN in writing within 7 days any single

38

lodgement (Cash or cheque in excess of N500,000 for an individual

and N2,000,000 for corporate body.

Furthermore, the banks and other financial institutions decrees

(BOFID) No25 of 1991 section (189) stipulates penalty for the

contravention of section 18 (a) an offences punishable of conviction

to a fine of N100,000 or to imprisonment of a term of 3 years and

forfeiture of gains and benefit to the federal Government section 19

(Prohibition of employment of certain persons interlocking

directorship) etc decree 25. Section 19 (1) provides that no bank

shall

a. Employ or continue the employment of any person who at

any time has been adjusted bankrupt or has compounded

with his creditors or who is or has been convicted by a

court for an offence involving fraud or dishonest or

professional misconduct (BOFID).

(Ribadu, 2004).

2.8 Fraud Detection, Prevention and Control

According to Eze (2004), the problem of fraud and forgeries

endemic in the banking sector, is unavoidable due to a variety of

reasons such as:

39

i. The vary nature of banking business which involves

human being, clients and staff of diverse background and

interest in a relationship trust.

ii. The convertible (i.e. cash or near cash) nature of most

banks assets.

iii. Wide network of branches. Some remotely located,

poorly staffed, ill-equipped and without adequate

communication facilities.

iv. Wide spread application of automated system which have

no finger print or handwriting evidence.

v. Common social misconceptions e.g. that bank have

limitless funds or that banks monies are an institutional loot or body

to be plundered by the able (Eze, 2004).

In this country Nigeria, commercial banks fraud has assumed a

frightened scale of sophistication consequent upon the general

economic depression of last decades and the continuiting travails of

the banking sector in the wake of government frantic policy

experimentation.

However, the unfortunate truth from empirical observation is

that majority of commercial banks fraud are never reported to the

police and (NDIC) in spite of the well known statutory requirement.

40

Some of the fraud actually passes undetected while some are

criminal covered up especially where no actual or significant loss is

sustained.

The common reason for such cover up is to avoid adverse

publicity, protracted police case, litigation and or black mail. Worse

still, some of the new generation banks have been known not only

the condone but actually commit and promote gross malpractices

e.g. kite flying and across firing as a matter of corporate deliberate

business strategy.

The Nigeria banking industry has become not just a battle front

with a clear-cut firing line between the bank and the bandits, but a

variable mine-field in which some banks and their top management

staff are in secret league with the enemy. Only the increased

alertness and collaboration of genuine banks together with improved

supervisory measures by the CBN and NDIC will terminate such

private organization.

Commercial banks must wake up to the concern of elements in

their operating environment and serious threats to their internal

security arising from internal and external factors (Eze, 2004).

41

Internal Factors

Internal factors are those factors that relate to the insiders or

members of staff such as

i. Absence of a tough, unambiguous corporate policy

committing top management to pursue the severest

sanctions including prosecution for act of dishonesty.

ii. Lack of clear procedural guidance or updated instruction

manual.

iii. Poor staff of vital functions and loss of experience

personnel.

iv. Low workers morale and employee frustration.

v. Staff dismissed or terminated for fraud be re-enaged in

other financial institution e.g. mortgage banks and

financial houses from where they could sneak attacks on

their erstwhile employers.

vi. Unplanned acquisition of new technologies e.g.

computerization.

External Factors

External factors relate to these factors that are not connected

with the bankers such as:

42

• Special degeneracy which promotes the get rich-quick

syndrome and workshop of materialism.

• Exploitable defects in the legal and panel system.

The essence of the categorization is to focus on the banks shop

floor i.e. (branches) with a view to highlighting controls for fraud

prevention in the first place and timely detection where unavoidable.

Branch Operation Control

In the context, branch is defined as a subordinate division of a

business subsidiary shop, office etc (chambers 20th century

dictionary).

Branches are common features of banking co-operations

(especially commercial banks their establishment being mostly

dictated by market imperatives such as proximity to prime clients.

The status of bank branches with head office is defined in the

case of prince vs. orient bank corporation where it was stated that

“in principle and in fact, branches are agencies of one principal

banking corporation or firm, notwithstanding that they may be

regarded as district for specially purpose”. It is important to mention

the common rule of agency that would normally apply such that any

notice served in the head office (principal) would be deemed to apply

43

to all its branches (the agent) allowing a reasonable time for

communication.

The agency relationship however, will aid a clear understanding

of the duties of branch management refers both of the function of

managing a branch and to the crops of personnel to whom that

responsibility is entrusted.

A holistic view of both the organization and the active

management process must therefore be adopted at every level of

decision making be it head office or branch level.

Branch management he continued must attain or surpress the

standard of efficiency and security prescribed by head office. To do

so, it must only function complementarily to the head office

management but take initiative in performing the five basic

managerial operations:

a. Setting fraud control objectives and goals.

b. Organizing fraud control activities and exercise.

c. Motivation and communicating effectively.

d. Measuring performance of teams and individuals.

e. Developing people.

Of course, branch work is a very demanding responsibility full

of unpredictable events and unanticipated situations which may

44

precipitate or facilitate frauds. Perhaps, no other position in a bank

carries as much risk exposure since every account and every

transaction is a potential for fraud. It has been indicated that large

branch network increases a banks vulnerability to fraud especially

where there is inferior quality of staff. An empirical fact is that the

massive expansion (Rural banking programme) of the commercial

banking network in Nigeria in the last few years resulted in an

unfortunate dilution of bank staff in key aspects of operation

including branch management be that as it may the branch ability to

prevent or detect and control fraud depends especially on the quality

of personnel assigned to it by the head office and the effectiveness

and adequacy of internal control in place (Eze, 2005).

Internal control is defined by the American Institute of certified

Public Accountant as “the plan of organization and all the co-ordinate

methods and measures adopted by a business to safeguard its

assets, check the accuracy and reliability of its accounting data,

promote operation and encourage adherence to prescribed

management policies. A second similarly definition is offered by the

Institute of Chartered Accountants of England and Wales who refers

to internal control as “the whole system of controls in financial and

otherwise established by management in order to carry on the

45

business of the company in an orderly manner to safeguard its

assets and secure as far as possible the accuracy and reliability of its

records.

Both the human resources and the internal control system in

which rest on the efficiency and security of the branch must be

closely monitored by the branch. The measures which ensure timely

detection and control of fraud are categorized by Shogotola (1994)

as the following:

a. Personnel control.

b. Administrative control.

c. Accounting control.

d. Financial control.

e. Inventory control.

f. Process control.

a. Personnel Control: Under this we have

i. Proper recruitment procedure: screening, referees sworn,

declaration certificates, photographs, permanent home

address.

46

ii. Proper Disengagements Procedure: Timely notification of

relevant department’s cancellation of rights and

privileges, withdrawal of staff identify cards.

iii. Posting and Placement: Properly documented posting

written job description with defined authority and

responsibility level. Others are:

• Job rotation.

• Attendance logs or register

• Enforced holidays and annual leave or absence training

programmes.

b. Administrative Control: under the administrative control

measure we have:

• Segregation of duties.

• Dual custody.

• Movement logs and registers.

• Access rights and restrictions.

• Security personnel.

• Franking machine.

• Archival system.

• Passwords.

• Regis cope and

47

• Cameras.

c. Accounting Control: Accounting control includes the following:

• Data validation.

• Prompt posting of transaction

• Balancing

• Reconciliation.

• Call over of posting entries.

• Signed authentication and approvals.

• Budgeting standards and projections.

• Variance analysts.

• Reviews and statistics.

• Returns.

d. Finance Control: This includes:

1. Cash limits.

2. Signing power

3. Specialized stationer (e.g. certified payment coupons)

e. Inventory Control: Inventory control identifies the following:

• Logs and listings.

• Physical checks and counts.

• Bin cards, stock receipts noted, stock issued vouchers.

• Locks and keys.

48

• Balancing stock, figures with the general ledger.

f. Process Control: This includes the:

• Input/output validation.

• Program.

• Key computer personnel (data processing manager, data

administrator, programmers, system analyst, operator,

librarian data, operators, computer operator). The various

principles and types of controls are rationally applied to every

aspect of branch operation as fraud antidotes or early

warning system. However, it has been accepted fact that

fraud at branch level focused on the following:

• Means of payments (cash cheques, bankers payment,

interbranch transfer) etc.

• Account (house ledgers impersonal accounts customers

accounts).

g. Petty Cash:

Cash payment for goods and services are usually reserved for

very small amounts and made through petty cash control centers on

a specified imprest limit. All expenses must be supported by duly

49

approved vouchers involves and cash receipts and properly entered

in the petty cash book.

Reimbursements to imprest should be covered by cheque

issued and not made directly from the till or vault. Petty cash

advance (IOU’s) must receive prior approval and be retired within a

specified period.

h. Main Cash:

A lot of controls are also exercise over the main cash. These

include dual custody of the vault and strict entry and exit

procedures. Insurance limits on premises and in- transit rules

fort cash movements within or without limits allowable with the

cashier and/ their staff in the banking hall, daily physical

checks and balancing as well as agreeing the vault book with

the bullion officer cash control book on daily basis. Daily

exchange of tills and till book and occasional surprise check on

cashiers are effective control techniques. The use of a control

register to monitor cash movements checks by receiving

cashier branch management should ensure that these controls

are established and adhere to.

50

i. None Cash Payment:

Most fraud in commercial banks involving none cash payment

mode includes:

Cheques (cheques on collection) bankers payments for

payment to other banks. Interbranch vouchers (for transfer between

sister branches. Cash cheques are negotiable free or equities in other

words, they are payable over the counter if regular on the face of it

i.e. drawn according to mandate and correct in particular. A branch

must however, exercise reasonable care to confirm that the cheque

is genuine and that payment is made to the genuine payee (use of

tally in some banks). This may involve measure like contacting the

drawer and using a photocopies camera. The branch internal control

unit (ICU) system would ensure that large payments are scrutinized

by two or more persons in the hierarchy.

j. None Cash Lodgement:

None cash cheques lodges into customers account are

processed for payment in two district ways if they are house cheques

i.e. if the drawers and payees accounts are dominated in the same

branch processing follows more of or less the same branch, the same

treatment as cash credit entry to the payee account. If they are

51

drawn on other banks (or branches) they are sent to them for

collection through the process of clearing. We have witnessed

majority of cheque frauds that involve clearing cheques. For this

reason, branch management must exercise extreme control here.

Caution notices must be sent to the paying branch/bank on any

unusual cheque lodgement received in any account.

This alert has proved quite effective in thwarting many fraud

attempts. Equally important is to ensure that only persons of

impeccable character are entrusted with clearing items which

clearing accounts are balanced and or reconciled daily. Again in

approving any cheques from payment, the branch management must

ensure that account is sufficiently funded or that drawings are within

the approved credit line (if any) attention must be paid to stop

orders in all cases and to caution notices in the cases of clearing

cheques.

k. Inter Bank Settlements:

Bank to bank payments are usually affected with special

instruments known as bankers payment. Similarly, there are pre-

printed as inter-branch voucher for the settlement and transfer

between branches of the same bank. Both sets of instruments are

safe custody items which should be closely controlled even when

52

blank. At issurance, stub or counter foil must signed by the

authorized issuing officers and retained for audit purposes. All serial

numbers must be well accounted for any lost instruments is a danger

signal.

L. Accounts (Current):

The second focal point of anti-fraud control must be

closely guarded from the time of account opening to eventual

closure. It must always be borne in mind that (apart from a

few incident of direct theft or defalcation) most frauds of nay

value are perpetrated on and or through an account. The

opening of an account must therefore be subjected to the

strictest care. For current account, satisfactory references from

reputable persons and precious bankers must be obtained, the

customers business address and other personal records

confirmed before he is issued with a cheque book. For a

corporate body or registered business, a prior search should be

conducted at the Corporate Affairs Commission and a clean

report should be held in the mandate file together with a

certified copy of the registration certificate and memorandum

and Article of Association, passport, photographs and photo

scope impression of account signatories are essential controls

53

and signed mandates (files and signatories cards) must be

securely preserved.

m. Impersonal Ledger Account:

In the case of impersonal ledger account only those on

the head office approved chart of account should be opened

and duplication must be scrupulously avoided (or in

computerized system precluded by program control. Periodic

review of personal accounts should be carried out by branch

management and appropriate precautionary actions being

taken on those not satisfactorily conducted e.g. long standing

credit balances should be transferred to dormant account

while abandoned merger accounts should be closed after due

notice to customers concerned. Closure of current account

must be preceded by a demand for unused cheque leaves.

Furthermore, it is be regularly checked importance that the

ledger balanced be regularly checked. A good computerized

system would provide branch management with the daily

detailing all ledger balanced thus a very important control and

managerial attention should be given to accounts with irregular

balances e.g. assets account with credit balances, liability

accounts with debit balances, rejection accounts and transit

54

accounts with balances. All suspense account (especially

receivables and payable/accreditives) should be kept under

close security with regular balancing and reconciliation while

dormant account and unclaimed balances should be

administrated on top security status.

n. Human Resources Control:

It has become a generally accepted truth that the

personality of the branch manager is perhaps the most

important signal factor in fraud prevention and control; the

best internal measures would be rendered ineffective, If human

agents for their implementation are ineffective. The buck

literally stops with the branch manager to see that controls are

put in place, that they are working that violating or exceptions

are promptly reported and corrective action is timely and

adequate. However, in order to perform these corrective

actions, the personality must posses the following qualities:

���� Knowledge Ability: the branch managers must be

knowledgeable enough not only to supervise but lead by

example both on the job and outside the office.

���� Technical Competence: On the job he must be technical

informed for only so can he succeed in inspiring confidence.

55

Ability to personally check paper work and ask intelligent

questions would discourage staffs from errors and fraud

attempts. It is therefore necessary that the branch manager

should posses appropriate educational qualification as well as

sound on the job training. He must be capable of developing

both himself and others. He must be receptive to new ideas

and responsive to innovation. He ought to adopt new

technologies (computerization) Okonkwo and Okoye (1984)

���� High Level of Self Discipline: He must posses and exhibit a high

level of self discipline and sound ethnical standards otherwise

he cannot provide the morale and leadership necessary for the

prevention of fraud and abuse. A manager who displays

divided locality or conflict of interest or who indulge in various

corrupt and unethical practices (such as bribery, extortion, kick

back contract inflation) cannot keep his subordinates in check “

he who preaches equity must come with clean hands” indeed,

since the position of a branch mangers is a core factor to fraud

detection, prevention and control, the appointment should be

crucial management decision which should not be subjected to

undue politics or extraneous considerations such as nepotism,

favoritism etc.

56

2.9 Government effort towards Fraud Control

The role of the federal government on prevention and control

of fraud is not only the commercial banks, but almost in all the

financial institutions (Adekanye 1986). The government is mainly

interested in ensure a discipline society, promulgation of appropriate

statutes, enforcement of various legal provisions.

The deduction is based on the realization that indiscipline and

corruption in the society created false value systems and tend to

encourage others to be like them (Joneses). In an attempt to be like

the Jones, people get involved in unorthodox means of making

wealth including fraudulent practices.

It is a common saying that where there is no law, there is no

offences. In recognition of this, the federal government put in place

relevant statutes to ensure safeguard and sound practices in Nigeria

financial system. According to Adeniji (1981), they include CBN

Decree, BOFID Decree, NDIC Decree, FMBN Decree, SEC Decree,

CAM Decree, Community Bank Decree, People Bank Decree. To

further give effects to its resolve to rid the financial institutions of

fraud, the government constituted the National Committee on

Malpractices in banks and other financial institutions in 1990. The

committee after deliberations recommended the promulgation of a

57

special law on fraud and malpractices banks. What is left is to

legislate appropriately so that the incidence of fraud and other

malpractices would be curtailed in the financial system. Again, the

Federal Government puts in place necessary infrastructure that will

ensure that incidence of fraud in commercial banks is abated. It is

for this and many other reasons that we have CBN, NDIC, SEC,

Police Judiciary, ICDC, CPC & EFCC of Olusegun Obasanjo regime.

These agencies in their various activities have been preventing

and controlling fraud. On the enforcement of the various legislation

to curb fraud in the banks, we have the ministry of justice, police

and the Judiciary. It will suffice to add that what is required mainly

from the judiciary is prompt, fair and evenly handled justice.

(Adeniji, 1981).

2.10 CBN and NDIC effort to Fraud Control

The subject of fraud in the commercial banks is of special

interest or concern to the monetary and supervisory authorities

particularly the CBN and NDIC. These government agencies are

concerned about the safety of individual’s institutions and the

soundness of the banking system. Most especially the NDIC is

specifically charge with the responsibility of protesting depositors.

58

The CBN on the hand is to specifically check the activities of

commercial banks operations in order to regulate and to make sure

that no banks operate without following the due process of rules and

regulations (CBN Annual Report, 2007).

2.11 Extent of Fraud in Banks

Bank fraud in Nigeria has increased and will continue to

increase because it is a part of everyday life. “The magnitude of

fraud is, of course, not known because much of is undiscovered or

undetected and not all that is detected is published” Nwankwo

(1991). In Nigeria, where the statistics are non-existent, it is put at

about-N-200 Million per annum of which about 15%-20% would be

successful. It is appropriate to have a feel of the extent of loss

through bank frauds in Nigeria in order to appreciate the havoc the

cankerworm has been wrecking on the economy.

The sum of =N=2.2 billion was involved in banks fraud in 3 year,

1991-1993, out of which commercial banks accounted for about 94.1

percent the actual/expected loss to the banking system within the

same period totaled about #0.3 Billion with commercial banks

accounting for about 95.7 percent thereof.

59

In 1998, the nation’s banking industry lost #3.196 Billion while in

1999, it lost a whopping sum of #7.404 Billion to fraud. Similarly, the

actual/expected loss stood at a higher level of #2.713 Billion relative

to #623.50 Million in 1998 (NDIC Annual report and statement of

account 1999).

Nigeria’s banks have seen almost $10m disappear through employee

fraud in 2002, a rise of more than 40% on the year before, a survey

by the country’s banking regulator has found.

The total amount stolen was 1.29bn naira, up from 906.3m in 2001,

the Nigerian Deposit insurance corporation reported. Ten times that

amount #12.91bn was recorded in attempted fraud, up from

11.24bn for a rise of 15%. Most of the thefts, NDIC said, were the

result of either forgeries or illegal withdrawals from customer’

accounts.

The figures may well be an understatement, though; as NDIC said it

believes financial institutions routinely underreport fraud losses for

fear of negative publicity. In may 2003 Nigerian bank fraud moved

up to 40%. The banking regulator says theft by bank employees

soared last year, but suspects that much more fraud may go

unreported.

60

It is not only Nigerian banks and citizens that are exposed to bank

frauds. Such frauds are also focused on foreign banks and their

citizens. Just how much has been stolen by such fraud is not clear.

But BBC news-business says that US citizens lose in 2004 move than

$100m (£63.4m) a year to Nigerian fraudsters. However, Nigerians

do indeed involve themselves in genuinely legal businesses apart

from the infamous banking scams (Nwankwo, 1991).

61

REFERENCES

Adeniyi, A.A (2004); Auditing and Investigation, Lagos. El-Toda

Ventures Limited.

Adewunmi, W. (1986); Data Processing and Management

Information System, Lagos. Macmillan Nigeria

Publisher Limited.

Alashi, S.O (1994); Fraud Prevention and Control, Role of

Government and its Agents Lagos. July- Dec,

2007.

Anyanwu, J.C (1993); Monetary, Economics Theory, Policy and

Institutions. Onitsha, Hybrid Publishers Ltd.

Eze, J.C (2004); Principles and Techniques of Auditing, Enugu.

Edge Publishers.

Castle, E.F and Owens P.N (1992); Elements of Banking 2nd Edition

New York. Pretince Hall Publishers.

Johnson, U.O (2007); Introduction to Project Writing, Enugu. New

Dimension Publisher.

62

CHAPTER THREE

3.0 RESEARCH METHODOLOGY

The aim of the chapter is to discuss the method adopted by the

researcher in carrying out this research work. The chapter contains,

Area of the study, source of data, population and sample size

determination, instrument used for data collection, method of data

analysis, validity and reliability of data.

3.1 Area of the Study

The study was carried out in the following selected commercial

banks in Enugu, Union bank, Diamond bank and Stanbic IBTC bank

plc.

3.2 Sources of Data

Data for this study was generated from both primary and

secondary sources.

Primary Data: The primary data is the original or first hand

information obtained by the researcher from the respondents directly

for the purpose of the study. To generate this data, the researcher

employed the use of questionnaire.

63

Secondary Data: Secondary data are facts that the researcher

collected from already existing sources. In this study, the secondary

sources were from Journals, text books, Newspapers magazines and

internet.

3.3 Population and Sample Size Determination

The target population of the study consists of senior staff of

selected commercial banks in Enugu.

According to the information received from the selected

commercial banks concerning their population.

Union Bank = 610

Diamond Bank = 407

Stanbic IBTC Bank = 203

Total = 1220

Base on the population of the selected commercial banks the

sample size was determined at 5% error tolerance and 95% degree

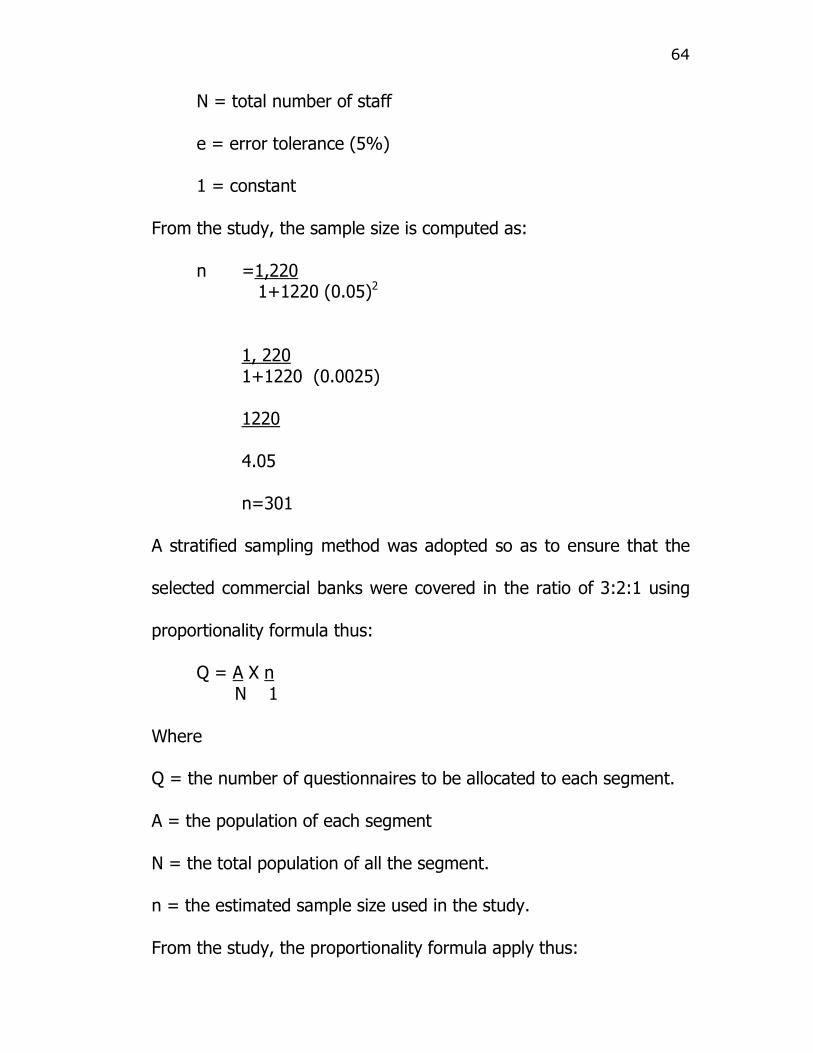

of confidence, using yamane’s formula

n = N 1+ne2

Where

n = population size

64

N = total number of staff

e = error tolerance (5%)

1 = constant

From the study, the sample size is computed as:

n =1,220 1+1220 (0.05)2

1, 220 1+1220 (0.0025)

1220

4.05

n=301

A stratified sampling method was adopted so as to ensure that the

selected commercial banks were covered in the ratio of 3:2:1 using

proportionality formula thus:

Q = A X n N 1

Where

Q = the number of questionnaires to be allocated to each segment.

A = the population of each segment

N = the total population of all the segment.

n = the estimated sample size used in the study.

From the study, the proportionality formula apply thus:

65

Union bank = 610

Diamond bank = 407

Stanbic IBTC = 203

Total 1220

Union bank plc = 610 x 301 =151 1,220 1

Diamond bank = 407 x 301 =100 1,220 1

Stanbic IBTC bank = 203 x 301 =50 1,220 1

Total = 301

Table 3.1

Organization A Q

Union bank Plc 610 151

Diamond bank 407 100

Stanbic IBTC bank 203 50

Total 1,220 301

66

3.4 Instrument used for Data Collection

Questionnaire

The questionnaire is made up of 17 questions consisting of

multiple choice and dichotomous questions.

(a) Dichotomous questions- These are close ended questions that

require respondents to answer yes or no.

(b) Multiple choice questions- This requires the respondents to

choose from a set of alternative options asked.

Interview

Interview gives an on the spot response from the respondents.

It provides complimentary data to the questionnaire.

3.5 Method of Data Analysis

The data collected were subjected to simple statistical

treatments. They were organized and presented in tables and

percentages.

Also, the chi-square (χ2) statistical method was used to test

the hypotheses.

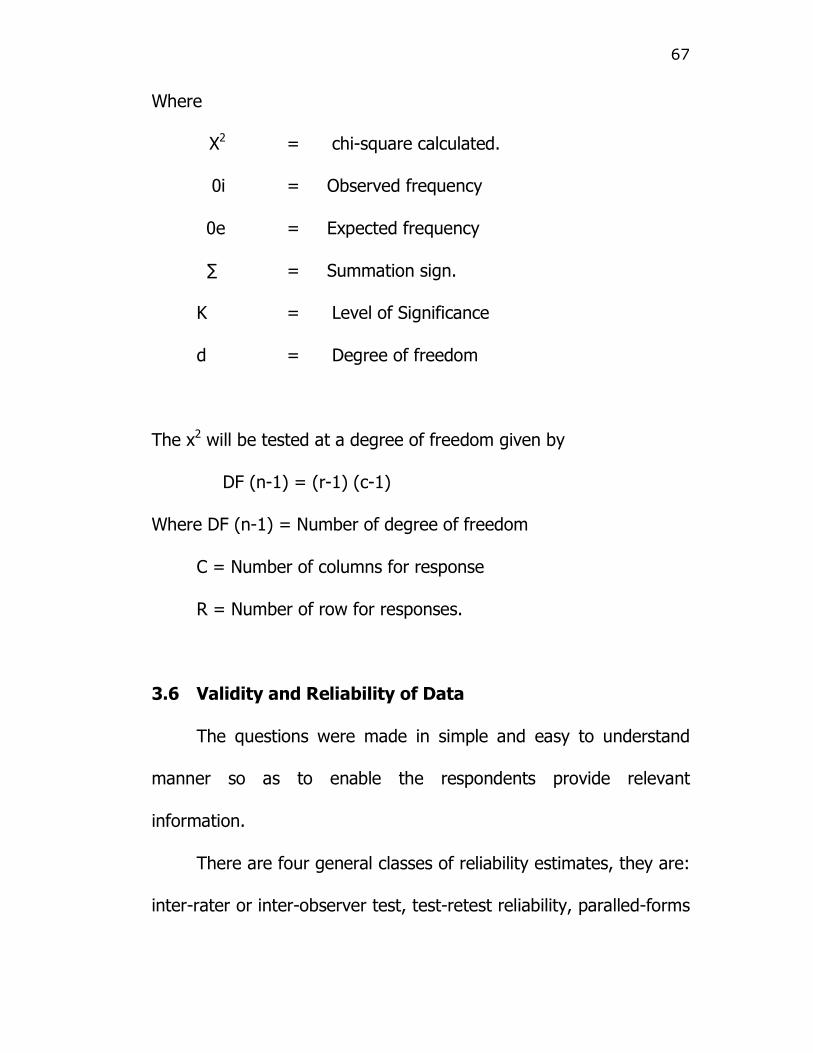

The chi-square formula is calculated as follows.

Х2 ∑(0-0e)2 0e

67

Where

Х2 = chi-square calculated.

0i = Observed frequency

0e = Expected frequency

∑ = Summation sign.

K = Level of Significance

d = Degree of freedom

The x2 will be tested at a degree of freedom given by

DF (n-1) = (r-1) (c-1)

Where DF (n-1) = Number of degree of freedom

C = Number of columns for response

R = Number of row for responses.

3.6 Validity and Reliability of Data