Embed Size (px)

Citation preview

47Annual Report 2013 | Encana Corporation

MA

NA

GE

ME

NT

RE

PO

RT

Management’s Responsibility for Consolidated Financial Statements

The accompanying Consolidated Financial Statements of Encana Corporation (the “Company”) are the responsibility of Management. The Consolidated Financial

Statements have been prepared by Management in United States dollars in accordance with generally accepted accounting principles in the United States and

include certain estimates that reflect Management’s best judgments.

The Company’s Board of Directors has approved the information contained in the Consolidated Financial Statements. The Board of Directors fulfills its responsibility

regarding the financial statements mainly through its Audit Committee, which has a written mandate that complies with the current requirements of Canadian

securities legislation and the United States Sarbanes-Oxley Act of 2002 and voluntarily complies, in principle, with the Audit Committee guidelines of the New York

Stock Exchange. The Audit Committee meets at least on a quarterly basis.

Management’s Assessment of Internal Control over Financial Reporting

Management is also responsible for establishing and maintaining adequate internal control over the Company’s financial reporting. The internal control system was

designed to provide reasonable assurance to the Company’s Management regarding the preparation and presentation of the Consolidated Financial Statements.

Internal control systems, no matter how well designed, have inherent limitations. Therefore, even those systems determined to be effective can provide only reasonable

assurance with respect to financial statement preparation and presentation. Also, projections of any evaluation of effectiveness to future periods are subject to the risk

that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Management has assessed the design and effectiveness of the Company’s internal control over financial reporting as at December 31, 2013. In making its

assessment, Management has used the Internal Control – Integrated Framework (1992) issued by the Committee of Sponsoring Organizations of the Treadway

Commission to evaluate the effectiveness of the Company’s internal control over financial reporting. Based on our evaluation, Management has concluded that

the Company’s internal control over financial reporting was effectively designed and operating effectively as at that date.

PricewaterhouseCoopers LLP, an independent firm of chartered accountants, was appointed by a vote of shareholders at the Company’s last annual meeting

to audit and provide independent opinions on both the Consolidated Financial Statements and the Company’s internal control over financial reporting

as at December 31, 2013, as stated in their Auditor’s Report. PricewaterhouseCoopers LLP has provided such opinions.

Douglas J. Suttles Sherri A. BrillonPresident & Chief Executive Officer Executive Vice-President & Chief Financial Officer

February 20, 2014

MANAGEMENT REPORT

47

48 Encana Corporation | Annual Report 2013

AU

DIT

OR

’S

RE

PO

RT

INDEPENDENT AUDITOR’S REPORT

To the Shareholders of Encana Corporation

We have completed an integrated audit of Encana Corporation’s 2013 and 2012 Consolidated Financial Statements and its internal control over financial reporting

as at December 31, 2013 and an audit of its 2011 Consolidated Financial Statements. Our opinions, based on our audits, are presented below.

Report on the Consolidated Financial Statements

We have audited the accompanying Consolidated Financial Statements of Encana Corporation, which comprise the Consolidated Balance Sheet as at December 31, 2013

and December 31, 2012 and the Consolidated Statements of Earnings, Comprehensive Income, Changes in Shareholders’ Equity and Cash Flows for each of the three

years in the period ended December 31, 2013, and the related notes, which comprise a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these Consolidated Financial Statements in accordance with accounting principles generally

accepted in the United States of America and for such internal control as management determines is necessary to enable the preparation of Consolidated Financial

Statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these Consolidated Financial Statements based on our audits. We conducted our audits as at December 31, 2013

and December 31, 2012 and for the years then ended in accordance with Canadian generally accepted auditing standards and the standards of the Public

Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether

the Consolidated Financial Statements are free from material misstatement. Canadian generally accepted auditing standards also require that we comply with

ethical requirements.

An audit involves performing procedures to obtain audit evidence, on a test basis, about the amounts and disclosures in the consolidated financial statements.

The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial

statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the company’s preparation

and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances. An audit also

includes evaluating the appropriateness of accounting principles and policies used and the reasonableness of accounting estimates made by management,

as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our audit opinion on the Consolidated

Financial Statements.

Opinion

In our opinion, the Consolidated Financial Statements present fairly, in all material respects, the financial position of Encana Corporation and its subsidiaries as at

December 31, 2013 and December 31, 2012 and the results of its operations and its cash flows for each of the three years in the period ended December 31, 2013

in accordance with accounting principles generally accepted in the United States of America.

AUDITOR’S REPORT

48

49Annual Report 2013 | Encana Corporation

AU

DIT

OR

’S

RE

PO

RT

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING

We have also audited Encana Corporation and its subsidiaries’ internal control over financial reporting as at December 31, 2013, based on criteria established

in Internal Control - Integrated Framework (1992), issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”).

Management’s Responsibility for Internal Control over Financial Reporting

Management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over

financial reporting included in the accompanying Management’s Assessment of Internal Control over Financial Reporting.

Auditor’s Responsibility

Our responsibility is to express an opinion on the company’s internal control over financial reporting based on our audit. We conducted our audit of internal control

over financial reporting in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan

and perform the audit to obtain reasonable assurance about whether effective internal control over financial reporting was maintained in all material respects.

An audit of internal control over financial reporting includes obtaining an understanding of internal control over financial reporting, assessing the risk that a material

weakness exists, testing and evaluating the design and operating effectiveness of internal control based on the assessed risk, and performing such other

procedures as we consider necessary in the circumstances.

We believe that our audit provides a reasonable basis for our audit opinion on the company’s internal control over financial reporting.

Definition of Internal Control over Financial Reporting

A company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the

preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company’s internal control over financial

reporting includes those policies and procedures that: (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions

and dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial

statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with

authorizations of management and directors of the company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition,

use, or disposition of the company’s assets that could have a material effect on the financial statements.

Inherent Limitations

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation

of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions or that the degree of compliance

with the policies or procedures may deteriorate.

Opinion

In our opinion, Encana Corporation and its subsidiaries maintained, in all material respects, effective internal control over financial reporting as at December 31, 2013,

based on criteria established in Internal Control - Integrated Framework (1992) issued by COSO.

PricewaterhouseCoopers LLPChartered AccountantsCalgary, Alberta, Canada

February 20, 2014

49

50 Encana Corporation | Annual Report 2013

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

CONSOLIDATED STATEMENT OF EARNINGS

For the years ended December 31 ($ millions, except per share amounts) 2013 2012 2011

Revenues, Net of Royalties (Note 2) $ 5,858 $ 5,160 $ 8,467

Expenses (Note 2)

Production and mineral taxes 134 105 198

Transportation and processing 1,476 1,231 1,193

Operating 859 794 866

Purchased product 441 349 635

Depreciation, depletion and amortization 1,565 1,956 2,282

Impairments (Note 8) 21 4,695 2,249

Accretion of asset retirement obligation (Note 14) 53 53 50

Administrative (Note 17) 439 392 350

Interest (Note 4) 563 522 468

Foreign exchange (gain) loss, net (Note 5) 325 (107) 133

Other (6) 1 21

5,870 9,991 8,445

Net Earnings (Loss) Before Income Tax (12) (4,831) 22

Income tax expense (recovery) (Note 6) (248) (2,037) 17

Net Earnings (Loss) $ 236 $ (2,794) $ 5

Net Earnings (Loss) per Common Share (Note 15)

Basic $ 0.32 $ (3.79) $ 0.01

Diluted $ 0.32 $ (3.79) $ 0.01

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOMEFor the years ended December 31 ($ millions) 2013 2012 2011

Net Earnings (Loss) $ 236 $ (2,794) $ 5

Other Comprehensive Income (Loss), Net of Tax

Foreign currency translation adjustment (Notes 16) (46) 81 (305)

Pension and other post-employment benefit plans (Notes 16, 19) 60 13 (34)

Other Comprehensive Income (Loss) 14 94 (339)

Comprehensive Income (Loss) $ 250 $ (2,700) $ (334)

See accompanying Notes to Consolidated Financial Statements

50

51Annual Report 2013 | Encana Corporation

CONSOLIDATED BALANCE SHEET

As at December 31 ($ millions) 2013 2012

AssetsCurrent Assets

Cash and cash equivalents $ 2,566 $ 3,179

Accounts receivable and accrued revenues (Note 7) 988 1,236

Risk management (Note 21) 56 479

Income tax receivable 562 560

Deferred income taxes (Note 6) 118 23

4,290 5,477 Property, Plant and Equipment, at cost: (Note 8)

Natural gas and oil properties, based on full cost accounting

Proved properties 51,603 50,953

Unproved properties 1,068 1,295

Other 3,148 3,379

Property, plant and equipment 55,819 55,627

Less: Accumulated depreciation, depletion and amortization (45,784) (45,876)

Property, plant and equipment, net (Note 2) 10,035 9,751

Cash in Reserve 10 54

Other Assets (Note 9) 526 466

Risk Management (Note 21) 204 111

Deferred Income Taxes (Note 6) 939 1,116

Goodwill (Notes 2, 10) 1,644 1,725

(Note 2) $ 17,648 $ 18,700

Liabilities and Shareholders’ EquityCurrent Liabilities

Accounts payable and accrued liabilities (Note 11) $ 1,895 $ 2,003

Income tax payable 29 45

Risk management (Note 21) 25 5

Current portion of long-term debt (Note 12) 1,000 500

Deferred income taxes (Note 6) 3 59

2,952 2,612

Long-Term Debt (Note 12) 6,124 7,175

Other Liabilities and Provisions (Note 13) 2,520 2,672

Risk Management (Note 21) 5 10

Asset Retirement Obligation (Note 14) 900 936

12,501 13,405

Commitments and Contingencies (Note 23)

Shareholders’ Equity

Share capital - authorized unlimited common shares, without par value

2013 issued and outstanding: 740.9 million shares (2012: 736.3 million shares) (Note 15) 2,445 2,354

Paid in surplus (Notes 15, 18) 15 10

Retained earnings 2,003 2,261

Accumulated other comprehensive income (Note 16) 684 670

Total Shareholders’ Equity 5,147 5,295

$ 17,648 $ 18,700

See accompanying Notes to Consolidated Financial Statements

Clayton H. Woitas Jane L. Peverett Director

Approved by the Board of Directors

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

Director51

52 Encana Corporation | Annual Report 2013

CONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

For the year ended December 31, 2013 ($ millions)

Share Capital

Paid in Surplus

Retained Earnings

Accumulated Other Comprehensive

Income

Total Shareholders’

Equity

Balance, December 31, 2012 $ 2,354 $ 10 $ 2,261 $ 670 $ 5,295

Share-Based Compensation (Note 18) - 3 - - 3

Net Earnings (Loss) - - 236 - 236

Common Shares Cancelled (Note 15) (2) 2 - - -

Dividends on Common Shares (Note 15) - - (494) - (494)Common Shares Issued Under

Dividend Reinvestment Plan (Note 15) 93 - - - 93

Other Comprehensive Income (Loss) (Note 16) - - - 14 14

Balance, December 31, 2013 $ 2,445 $ 15 $ 2,003 $ 684 $ 5,147

For the year ended December 31, 2012 ($ millions)

Share

Capital

Paid in

Surplus

Retained

Earnings

Accumulated Other

Comprehensive

Income

Total

Shareholders’

Equity

Balance, December 31, 2011 $ 2,354 $ 5 $ 5,643 $ 576 $ 8,578

Share-Based Compensation (Note 18) - 5 - - 5

Net Earnings (Loss) - - (2,794) - (2,794)

Dividends on Common Shares (Note 15) - - (588) - (588)

Other Comprehensive Income (Loss) (Note 16) - - - 94 94

Balance, December 31, 2012 $ 2,354 $ 10 $ 2,261 $ 670 $ 5,295

For the year ended December 31, 2011 ($ millions)

Share

Capital

Paid in

Surplus

Retained

Earnings

Accumulated Other

Comprehensive

Income

Total

Shareholders’

Equity

Balance, December 31, 2010 $ 2,352 $ - $ 6,226 $ 915 $ 9,493

Share-Based Compensation - 5 - - 5

Net Earnings (Loss) - - 5 - 5

Dividends on Common Shares (Note 15) - - (588) - (588)

Common Shares Issued Under Option Plans 2 - - - 2

Other Comprehensive Income (Loss) - - - (339) (339)

Balance, December 31, 2011 $ 2,354 $ 5 $ 5,643 $ 576 $ 8,578

See accompanying Notes to Consolidated Financial Statements

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

52

53Annual Report 2013 | Encana Corporation

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

CONSOLIDATED STATEMENT OF CASH FLOWS

For the years ended December 31 ($ millions) 2013 2012 2011

Operating Activities

Net earnings (loss) $ 236 $ (2,794) $ 5

Depreciation, depletion and amortization 1,565 1,956 2,282

Impairments (Note 8) 21 4,695 2,249

Accretion of asset retirement obligation (Note 14) 53 53 50

Deferred income taxes (Note 6) (57) (1,837) 212

Unrealized (gain) loss on risk management (Note 21) 345 1,465 (879)

Unrealized foreign exchange (gain) loss (Note 5) 330 (112) 96

Other 55 82 87

Net change in other assets and liabilities (80) (78) (160)

Net change in non-cash working capital (Note 22) (179) (323) (15)

Cash From (Used in) Operating Activities 2,289 3,107 3,927

Investing Activities

Capital expenditures (Note 2) (2,712) (3,476) (4,610)

Acquisitions (Note 3) (184) (379) (515)

Proceeds from divestitures (Note 3) 705 4,043 2,080

Cash in reserve 44 415 (383)

Net change in investments and other 252 (242) (203)

Cash From (Used in) Investing Activities (1,895) 361 (3,631)

Financing Activities

Issuance of revolving long-term debt - 1,721 13,606

Repayment of revolving long-term debt - (1,724) (13,556)

Issuance of long-term debt (Note 12) - - 997

Repayment of long-term debt (Note 12) (500) (503) (500)

Issuance of common shares - - 2

Dividends on common shares (Note 15) (401) (588) (588)

Capital lease payments (Note 8) (8) (17) (155)

Cash From (Used in) Financing Activities (909) (1,111) (194)

Foreign Exchange Gain (Loss) on Cash and Cash

Equivalents Held in Foreign Currency (98) 22 (1)

Increase (Decrease) in Cash and Cash Equivalents (613) 2,379 101

Cash and Cash Equivalents, Beginning of Year 3,179 800 699

Cash and Cash Equivalents, End of Year $ 2,566 $ 3,179 $ 800

Cash, End of Year $ 161 $ 92 $ 70

Cash Equivalents, End of Year 2,405 3,087 730

Cash and Cash Equivalents, End of Year $ 2,566 $ 3,179 $ 800

Supplementary Cash Flow Information (Note 22)

See accompanying Notes to Consolidated Financial Statements

53

Encana Corporation | Annual Report 2013

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

54

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A) NATURE OF OPERATIONS

Encana Corporation and its subsidiaries (“Encana” or the “Company”) are in the business of the exploration for, the development of, and the production

and marketing of natural gas, oil and natural gas liquids (“NGLs”). The term liquids is used to represent Encana’s oil, NGLs and condensate.

B) BASIS OF PRESENTATION

The Consolidated Financial Statements include the accounts of Encana and are presented in accordance with accounting principles generally accepted

in the United States (“U.S. GAAP”).

In these Consolidated Financial Statements, unless otherwise indicated, all dollar amounts are expressed in United States (“U.S.”) dollars. Encana’s financial results

are consolidated in Canadian dollars; however, the Company has adopted the U.S. dollar as its reporting currency to facilitate a more direct comparison to other

North American oil and gas companies. All references to US$ or to $ are to United States dollars and references to C$ are to Canadian dollars.

C) PRINCIPLES OF CONSOLIDATION

The Consolidated Financial Statements include the accounts of Encana and entities in which it holds a controlling interest. All intercompany balances and

transactions are eliminated on consolidation. For upstream joint interest operations where Encana retains an undivided interest in jointly owned property, the

Company records its proportionate share of assets, liabilities, revenues and expenses. Investments in non-controlled entities over which Encana has the ability

to exercise significant influence are accounted for using the equity method.

D) FOREIGN CURRENCY TRANSLATION

Monetary assets and liabilities of the Company that are denominated in foreign currencies are translated at the rates of exchange in effect at the period end date.

Any gains or losses are recorded in the Consolidated Statement of Earnings. Foreign currency revenues and expenses are translated at the rates of exchange

in effect at the time of the transaction.

For the accounts of foreign operations, assets and liabilities are translated at period end exchange rates, while revenues and expenses are translated using

average rates over the period. Translation gains and losses relating to the foreign operations are included in accumulated other comprehensive income (“AOCI”).

Recognition of Encana’s accumulated translation gains and losses into net earnings occurs upon complete or substantially complete liquidation of the Company’s

investment in the foreign operation.

For financial statement presentation, assets and liabilities are translated into the reporting currency at period end exchange rates, while revenues and expenses

are translated using average rates over the period. Gains and losses relating to the financial statement translation are included in AOCI.

E) USE OF ESTIMATES

The timely preparation of the Consolidated Financial Statements requires that Management make estimates and assumptions and use judgment regarding the

reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the Consolidated Financial Statements and the reported

amounts of revenues and expenses during the period. Such estimates primarily relate to unsettled transactions and events as of the date of the Consolidated

Financial Statements. Accordingly, actual results may differ from estimated amounts as future events occur.

Significant items subject to estimates and assumptions are:

Estimates of proved reserves and related future cash flows used for depletion and ceiling test impairment calculations

Estimated fair value of long-term assets used for impairment calculations

Fair value of reporting units used for the assessment of goodwill

Estimates of future taxable earnings used to assess the realizable value of deferred tax assets

Fair value of asset retirement obligations and costs

Fair value of derivative instruments

Tax interpretations, regulations and legislation in the various jurisdictions in which the Company and its subsidiaries operate

Accruals for long-term performance-based compensation arrangements, including whether or not the performance criteria will be met and measurement

of the ultimate payout amount

Recognized values of pension assets and obligations, as well as the pension costs charged to net earnings depend on certain actuarial and economic assumptions

Accruals for legal claims, environmental risks and exposures

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Annual Report 2013 | Encana Corporation

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

55

F) REVENUE RECOGNITION

Revenues associated with Encana’s natural gas and liquids are recognized when production is sold to a purchaser at a fixed or determinable price, delivery has

occurred, title has transferred and collectability of the revenue is probable. Realized gains and losses from the Company’s financial derivatives related to natural

gas and oil commodity prices are recognized in revenue when the contract is settled. Unrealized gains and losses related to these contracts are recognized

in revenue based on the changes in fair value of the contracts at the end of the respective periods.

Market optimization revenues and purchased product expenses are recorded on a gross basis when Encana takes title to the product and has the risks and

rewards of ownership. Purchases and sales of products that are entered into in contemplation of each other with the same counterparty are recorded on a net

basis. Revenues associated with the services provided where Encana acts as agent are recorded as the services are provided.

G) PRODUCTION AND MINERAL TAXES

Costs paid by Encana to certain mineral and non-mineral interest owners based on production of natural gas and liquids are recognized when the product is produced.

H) TRANSPORTATION AND PROCESSING

Costs paid by Encana for the transportation and processing of natural gas and liquids are recognized when the product is delivered and the services provided.

I) OPERATING

Operating costs paid by Encana for oil and gas properties in which the Company has a working interest. Expenses are net of amounts capitalized in accordance

with the full cost method of accounting.

J) EMPLOYEE BENEFIT PLANS

The Company sponsors defined contribution and defined benefit plans, providing pension and other post-employment benefits to its employees in Canada

and the U.S. As of January 1, 2003, the defined benefit pension plan was closed to new entrants.

Pension expense for the defined contribution pension plan is recorded as the benefits are earned by the employees covered by the plans. Encana accrues for

its obligations under its employee defined benefit plans, net of plan assets. The cost of defined benefit pensions and other post-employment benefits is actuarially

determined using the projected benefit method based on length of service and reflects Management’s best estimate of salary escalation, retirement ages

of employees and expected future health care costs. The expected return on plan assets is based on historical and projected rates of return for assets in the

investment plan portfolio. The actual return is based on the fair value of plan assets. The projected benefit obligation is discounted using the market interest

rate on high-quality corporate debt instruments as at the measurement date.

Pension expense for the defined benefit pension plan includes the cost of pension benefits earned during the current year, the interest cost on pension obligations,

the expected return on pension plan assets, the amortization of the net transitional obligation, the amortization of adjustments arising from pension plan

amendments, the amortization of prior service costs, and the amortization of the excess of the net actuarial gain or loss over 10 percent of the greater of the

benefit obligation and the fair value of plan assets. Amortization is done on a straight-line basis over a period covering the expected average remaining service

lives of employees covered by the plans. Actuarial gains and losses related to the change in the over-funded or under-funded status of the defined benefit pension

plan and other post-employment benefit plans are recognized in other comprehensive income.

K) INCOME TAXES

Encana follows the liability method of accounting for income taxes. Under this method, deferred income taxes are recorded for the effect of any temporary

difference between the accounting and income tax basis of an asset or liability, using the enacted income tax rates and laws expected to apply when the assets

are realized and liabilities are settled. Current income taxes are measured at the amount expected to be recoverable from or payable to the taxation authorities

based on the income tax rates and laws enacted at the end of the reporting period. The effect of a change in the enacted tax rates or laws is recognized in net

earnings in the period of enactment. Income taxes are recognized in net earnings except to the extent that they relate to items recognized directly in shareholders’

equity, in which case the income taxes are recognized directly in shareholders’ equity.

Deferred income tax assets are routinely assessed for realizability. If it is more likely than not that deferred tax assets will not be realized, a valuation allowance

is recorded to reduce the deferred tax assets. Encana considers available positive and negative evidence when assessing the realizability of deferred tax assets

including historic and expected future taxable earnings, available tax planning strategies and carry forward periods. The assumptions used in determining expected

future taxable earnings are consistent with those used in the goodwill impairment assessment.

Encana recognizes the financial statement effects of a tax position when it is more likely than not, based on the technical merits, that the position will be sustained upon

examination by a taxing authority. A recognized tax position is initially and subsequently measured as the largest amount of tax benefit that is greater than 50 percent

likely of being realized upon settlement with a taxing authority. Liabilities for unrecognized tax benefits that are not expected to be settled within the next 12 months

are included in other liabilities and provisions.

Encana Corporation | Annual Report 2013

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

56

L) EARNINGS PER SHARE AMOUNTS

Basic net earnings per common share is computed by dividing the net earnings by the weighted average number of common shares outstanding during the period.

Diluted net earnings per common share amounts are calculated giving effect to the potential dilution that would occur if stock options were exercised or other

contracts to issue common shares were exercised, fully vested, or converted to common shares. The treasury stock method is used to determine the dilutive effect

of stock options and other dilutive instruments. The treasury stock method assumes that proceeds received from the exercise of in-the-money stock options and

other dilutive instruments are used to repurchase common shares at the average market price.

M) CASH AND CASH EQUIVALENTS

Cash and cash equivalents include cash on hand and short-term investments, such as money market deposits or similar type instruments, with a maturity of three

months or less when purchased. Outstanding disbursements issued in excess of applicable bank account balances are excluded from cash and cash equivalents

and are recorded in accounts payable and accrued liabilities. Cash in reserve represents cash amounts segregated or held in escrow which are not available for

general operating use.

N) PROPERTY, PLANT AND EQUIPMENT

UPSTREAM

Encana uses the full cost method of accounting for its acquisition, exploration and development activities. Under this method, all costs directly associated with the

acquisition of, the exploration for, and the development of natural gas and liquids reserves are capitalized on a country-by-country cost centre basis. Capitalized

costs exclude costs relating to production, general overhead or similar activities.

Under the full cost method of accounting, the carrying amount of Encana’s natural gas and oil properties within each country cost centre is subject to a ceiling test

performed quarterly. A ceiling test impairment is recognized in net earnings when the carrying amount of a country cost centre exceeds the country cost centre

ceiling. The carrying amount of a cost centre includes capitalized costs of proved oil and gas properties, net of accumulated depletion and the related deferred

income taxes.

The cost centre ceiling is the sum of the estimated after-tax future net cash flows from proved reserves, using the 12-month average trailing prices and

unescalated future development and production costs, discounted at 10 percent, plus unproved property costs. The 12-month average trailing price is calculated

as the average of the price on the first day of each month within the trailing 12-month period. Any excess of the carrying amount over the calculated ceiling

amount is recognized as an impairment in net earnings.

Capitalized costs accumulated within each cost centre are depleted using the unit-of-production method based on proved reserves. Depletion is calculated using

the capitalized costs, including estimated retirement costs, plus the undiscounted future expenditures to be incurred in developing proved reserves.

Costs associated with unproved properties are excluded from the depletion calculation until it is determined that proved reserves are attributable or impairment

has occurred. Unproved properties are assessed separately for impairment on a quarterly basis. Costs that have been impaired are included in the costs subject

to depletion within the full cost pool.

Proceeds from the divestiture of properties are normally deducted from the full cost pool without recognition of gain or loss unless the deduction significantly alters

the relationship between capitalized costs and proved reserves in the cost centre, in which case a gain or loss is recognized in net earnings. Generally, a gain or

loss on a divestiture is not recognized unless more than 25 percent of the Company’s proved reserves quantities in a particular country are sold. For divestitures

that result in the recognition of a gain or loss on the sale and constitute a business, goodwill is allocated to the divestiture.

MARKET OPTIMIZATION

Midstream facilities, including power generation facilities, are carried at cost and depreciated on a straight-line basis over the estimated service lives of the assets,

which are 20 years.

CORPORATE

Costs associated with office furniture, fixtures, leasehold improvements, information technology and aircraft are carried at cost and depreciated on a straight-line basis

over the estimated service lives of the assets, which range from three to 25 years. Costs associated with The Bow office building are carried at cost and depreciated

on a straight-line basis over the 60-year estimated life of the building. Assets under construction are not subject to depreciation until put into use. Land is carried at cost.

O) CAPITALIZATION OF COSTS

Expenditures related to renewals or betterments that improve the productive capacity or extend the life of an asset are capitalized. Maintenance and repairs are

expensed as incurred. Interest is capitalized during the construction phase of major development projects.

Annual Report 2013 | Encana Corporation

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

57

P) BUSINESS COMBINATIONS

Business combinations are accounted for using the acquisition method. The acquired identifiable net assets are measured at their fair value at the date

of acquisition. Deferred taxes are recognized for any differences between the fair value of net assets acquired and their tax bases. Any excess of the purchase

price over the fair value of the net assets acquired is recognized as goodwill. Any deficiency of the purchase price below the fair value of the net assets acquired

is recorded as a gain in net earnings. Associated transaction costs are expensed when incurred.

Q) GOODWILL

Goodwill, which represents the excess of purchase price over fair value of net assets acquired, is assessed for impairment at least annually at December 31.

Goodwill and all other assets and liabilities are allocated to reporting units, which are Encana’s country cost centres. To assess impairment, the carrying amount

of each reporting unit is determined and compared to the fair value of the reporting unit. If the carrying amount of the reporting unit is higher than its related fair

value then goodwill is written down to the reporting unit’s implied fair value of goodwill. The implied fair value of goodwill is determined by deducting the fair value

of the reporting unit’s assets and liabilities from the fair value of the reporting unit as if the reporting entity had been acquired in a business combination. Any

excess of the carrying value of goodwill over the implied fair value of goodwill is recognized as an impairment and charged to net earnings. Subsequent

measurement of goodwill is at cost less any accumulated impairments.

R) IMPAIRMENT OF LONG-TERM ASSETS

The carrying value of long-term assets, excluding goodwill and upstream assets included in property, plant and equipment, are assessed for impairment when

indicators suggest that the carrying value of an asset or asset group may not be recoverable. If the carrying amount exceeds the sum of the undiscounted cash

flows expected to result from the continued use and eventual disposition of the asset or asset group, an impairment is recognized for the excess of the carrying

amount over its estimated fair value.

S) ASSET RETIREMENT OBLIGATION

Asset retirement obligations are those legal obligations where the Company will be required to retire tangible long-lived assets such as producing well sites,

offshore production platforms and natural gas processing plants. The fair value of estimated asset retirement obligations is recognized in the Consolidated Balance

Sheet when incurred and a reasonable estimate of fair value can be made. The asset retirement cost, equal to the initially estimated fair value of the asset

retirement obligation, is capitalized as part of the cost of the related long-lived asset. Changes in the estimated obligation resulting from revisions to estimated

timing or amount of future cash flows are recognized as a change in the asset retirement obligation and the related asset retirement cost.

Amortization of asset retirement costs is included in depreciation, depletion and amortization in the Consolidated Statement of Earnings. Increases in the asset

retirement obligations resulting from the passage of time are recorded as accretion of asset retirement obligation in the Consolidated Statement of Earnings.

Actual expenditures incurred are charged against the accumulated asset retirement obligation.

T) STOCK-BASED COMPENSATION

Obligations for payments of cash or common shares under Encana’s stock-based compensation plans are accrued over the vesting period, net of forfeitures,

using fair values. Fair values are determined using observable share prices and/or pricing models such as the Black-Scholes-Merton option-pricing model. For

equity-settled stock-based compensation plans, fair values are determined at the grant date and are recognized over the vesting period as compensation costs

with a corresponding credit to shareholders’ equity. For cash-settled stock-based compensation plans, fair values are determined at each reporting date and

periodic changes are recognized as compensation costs, with a corresponding change to liabilities.

Obligations for payments for share units of Cenovus Energy Inc. (“Cenovus”) held by Encana employees are accrued as compensation costs based on the fair

value of the financial liability.

U) LEASES

Leases entered into for the use of an asset are classified as either capital or operating leases. Capital leases transfer to the Company substantially all of the risks

and benefits incidental to ownership of the leased item. Capital leases are capitalized upon commencement of the lease term at the lower of the fair value of the

leased asset or the present value of the minimum lease payments. Capitalized leased assets are amortized over the estimated useful life of the asset if the lease

arrangement contains a bargain purchase option or ownership of the leased asset transfers at the end of the lease term. Otherwise, the leased assets are

amortized over the lease term. Amortization of capitalized leased assets is included in depreciation, depletion and amortization in the Consolidated Statement

of Earnings. All other leases are classified as operating leases and the payments are recognized on a straight-line basis over the lease term.

Encana Corporation | Annual Report 2013

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

58

V) FAIR VALUE MEASUREMENTS

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the

measurement date. Valuation techniques include the market, income, and cost approach. The market approach uses information generated by market transactions

involving identical or comparable assets or liabilities; the income approach converts estimated future amounts to a present value; and the cost approach is based

on the amount that currently would be required to replace an asset.

Inputs used in determining fair value are characterized according to a hierarchy that prioritizes those inputs based on the degree to which they are observable.

The three input levels of the fair value hierarchy are as follows:

Level 1 – Inputs represent quoted prices in active markets for identical assets or liabilities, such as exchange-traded commodity derivatives.

Level 2 – Inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly, such as quoted market

prices for similar assets or liabilities in active markets or other market corroborated inputs.

Level 3 – Inputs that are not observable from objective sources, such as forward prices supported by little or no market activity or internally developed estimates

of future cash flows used in a present value model.

In determining fair value, the Company utilizes the most observable inputs available. If a fair value measurement reflects inputs at multiple levels within the

hierarchy, the fair value measurement is characterized based on the lowest level of input that is significant to the fair value measurement.

Recurring fair value measurements are performed for risk management assets and liabilities and for share units issued as part of the Split Transaction,

as discussed in Notes 15 and 20. The carrying amount of cash and cash equivalents, accounts receivable and accounts payable reported on the Consolidated

Balance Sheet approximates fair value. The fair value of long-term debt is disclosed in Note 12. Fair value information related to pension plan assets is included

in Note 19.

Certain non-financial assets and liabilities are initially measured at fair value, such as asset retirement obligations and certain assets and liabilities acquired

in business combinations or through non-monetary exchange transactions.

W) RISK MANAGEMENT ASSETS AND LIABILITIES

Risk management assets and liabilities are derivative financial instruments used by Encana to manage economic exposure to market risks relating to commodity

prices, foreign currency exchange rates and interest rates. The use of these derivative instruments is governed under formal policies and is subject to limits

established by the Board of Directors (“Board”). The Company’s policy is not to utilize derivative financial instruments for speculative purposes.

Derivative instruments that do not qualify for the normal purchases and sales exemption are measured at fair value with changes in fair value recognized in

net earnings. The fair values recorded in the Consolidated Balance Sheet reflect netting the asset and liability positions where counterparty master netting

arrangements contain provisions for net settlement. Realized gains or losses from financial derivatives related to natural gas and oil commodity prices are

recognized in revenues as the contracts are settled. Realized gains or losses from financial derivatives related to power commodity prices are recognized in

transportation and processing expense as the related power contracts are settled. Unrealized gains and losses are recognized in revenues and transportation

and processing expense accordingly, at the end of each respective reporting period based on the changes in fair value of the contracts.

X) COMMITMENTS AND CONTINGENCIES

Liabilities for loss contingencies arising from claims, assessments, litigation, environmental and other sources are recorded when it is probable that a liability has

been incurred and the amount can be reasonably estimated. These accruals are adjusted as additional information becomes available or circumstances change.

Annual Report 2013 | Encana Corporation

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

59

Y) RECENT ACCOUNTING PRONOUNCEMENTS

CHANGES IN ACCOUNTING POLICIES AND PRACTICES

On January 1, 2013, Encana adopted the following accounting standards updates issued by the Financial Accounting Standards Board (“FASB”), which have

not had a material impact on the Company’s Consolidated Financial Statements:

Accounting Standards Update 2011-11, “Disclosures about Offsetting Assets and Liabilities”, and Accounting Standards Update 2013-01, “Clarifying the Scope

of Disclosures about Offsetting Assets and Liabilities”, require disclosure of both gross and net information about certain financial instruments eligible for offset

in the balance sheet and certain financial instruments subject to master netting arrangements. The amendments have been applied retrospectively.

Accounting Standards Update 2013-02, “Reporting of Amounts Reclassified Out of Accumulated Other Comprehensive Income”, requires enhanced disclosures

about amounts reclassified out of accumulated other comprehensive income. The amendments have been applied prospectively.

NEW STANDARDS ISSUED NOT YET ADOPTED

As of January 1, 2014, Encana will be required to adopt the following accounting standards updates issued by the FASB, which are not expected to have a material

impact on the Company’s Consolidated Financial Statements:

Accounting Standards Update 2013-04, “Obligations Resulting from Joint and Several Liability Arrangements for Which the Total Amount of the Obligation is Fixed at the

Reporting Date”, clarifies guidance for the recognition, measurement and disclosure of liabilities resulting from joint and several liability arrangements. The amendments

will be applied retrospectively.

Accounting Standards Update 2013-05, “Parent’s Accounting for the Cumulative Translation Adjustment upon Derecognition of Certain Subsidiaries or Groups of Assets

within a Foreign Entity or of an Investment in a Foreign Entity”, clarifies the applicable guidance for certain transactions that result in the release of the cumulative

translation adjustment into net earnings. The amendments will be applied prospectively.

Accounting Standards Update 2013-11, “Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit

Carryforward Exists”, clarifies that a liability related to an unrecognized tax benefit or portions thereof should be presented as a reduction to a deferred tax asset for

a net operating loss carryforward, a similar tax loss or a tax credit carryforward, except under specific situations. The amendments will be applied prospectively.

2. SEGMENTED INFORMATION

Encana’s reportable segments are determined based on the Company’s operations and geographic locations as follows:

Canadian Division includes the exploration for, development of, and production of natural gas, oil and NGLs and other related activities within the Canadian cost centre.

USA Division includes the exploration for, development of, and production of natural gas, oil and NGLs and other related activities within the U.S. cost centre.

Market Optimization is primarily responsible for the sale of the Company’s proprietary production. These results are included in the Canadian and USA Divisions.

Market optimization activities include third party purchases and sales of product that provide operational flexibility for transportation commitments, product type,

delivery points and customer diversification. These activities are reflected in the Market Optimization segment. Market Optimization sells substantially all of the

Company’s upstream production to third party customers. Transactions between segments are based on market values and are eliminated on consolidation.

Corporate and Other mainly includes unrealized gains or losses recorded on derivative financial instruments. Once the instruments are settled, the realized gains

and losses are recorded in the reporting segment to which the derivative instrument relates.

Encana Corporation | Annual Report 2013

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

60

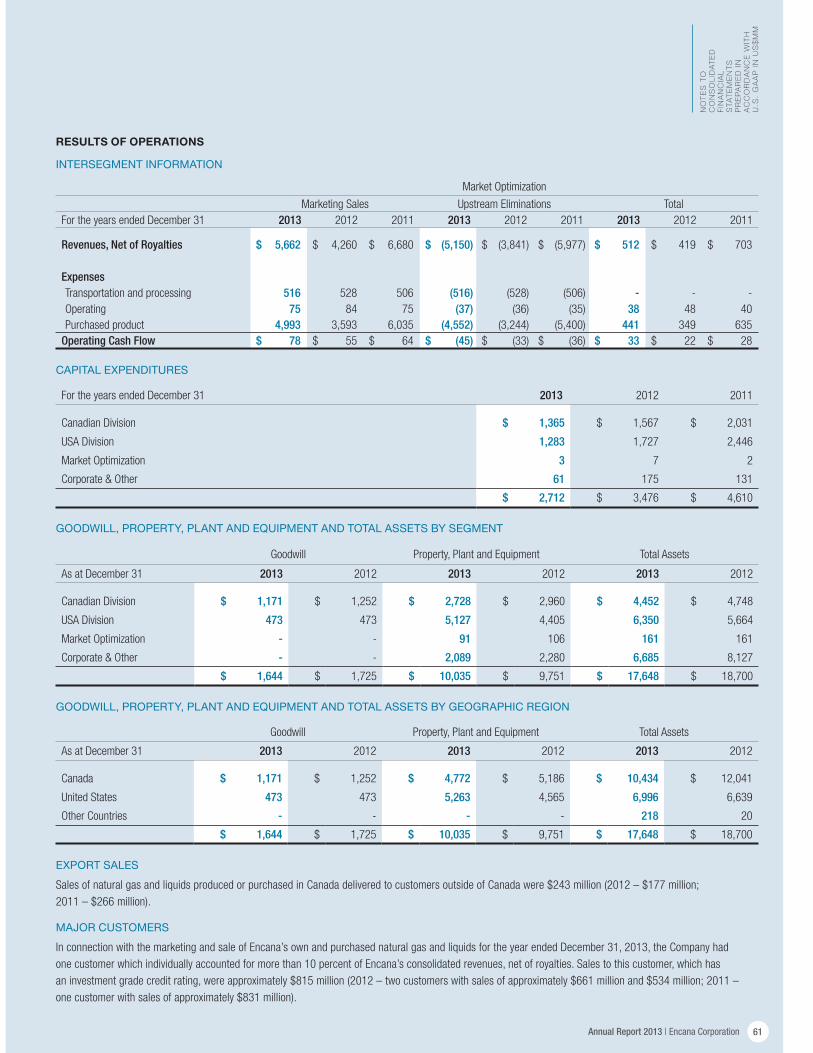

RESULTS OF OPERATIONS

SEGMENT AND GEOGRAPHIC INFORMATION

Canadian Division USA Division Market Optimization

For the years ended December 31 2013 2012 2011 2013 2012 2011 2013 2012 2011

Revenues, Net of Royalties $ 2,824 $ 2,760 $ 2,872 $ 2,763 $ 3,365 $ 4,022 $ 512 $ 419 $ 703

Expenses

Production and mineral taxes 15 9 15 119 96 183 - - -

Transportation and processing 756 555 490 722 652 728 - - -

Operating 372 352 380 411 377 444 38 48 40

Purchased product - - - - - - 441 349 635

1,681 1,844 1,987 1,511 2,240 2,667 33 22 28

Depreciation, depletion and amortization 601 748 966 818 1,102 1,226 12 12 12

Impairments - 1,822 2,249 - 2,842 - - - -

$ 1,080 $ (726) $ (1,228) $ 693 $ (1,704) $ 1,441 $ 21 $ 10 $ 16

Corporate & Other Consolidated

2013 2012 2011 2013 2012 2011

Revenues, Net of Royalties $ (241) $ (1,384) $ 870 $ 5,858 $ 5,160 $ 8,467

Expenses

Production and mineral taxes - - - 134 105 198

Transportation and processing (2) 24 (25) 1,476 1,231 1,193

Operating 38 17 2 859 794 866

Purchased product - - - 441 349 635

(277) (1,425) 893 2,948 2,681 5,575

Depreciation, depletion and amortization 134 94 78 1,565 1,956 2,282

Impairments 21 31 - 21 4,695 2,249

$ (432) $ (1,550) $ 815 1,362 (3,970) 1,044

Accretion of asset retirement obligation 53 53 50

Administrative 439 392 350

Interest 563 522 468

Foreign exchange (gain) loss, net 325 (107) 133

Other (6) 1 21

1,374 861 1,022

Net Earnings (Loss) Before Income Tax (12) (4,831) 22

Income tax expense (recovery) (248) (2,037) 17

Net Earnings (Loss) $ 236 $ (2,794) $ 5

Annual Report 2013 | Encana Corporation

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

61

RESULTS OF OPERATIONS

INTERSEGMENT INFORMATION

Market Optimization

Marketing Sales Upstream Eliminations Total

For the years ended December 31 2013 2012 2011 2013 2012 2011 2013 2012 2011

Revenues, Net of Royalties $ 5,662 $ 4,260 $ 6,680 $ (5,150) $ (3,841) $ (5,977) $ 512 $ 419 $ 703

Expenses Transportation and processing 516 528 506 (516) (528) (506) - - -

Operating 75 84 75 (37) (36) (35) 38 48 40

Purchased product 4,993 3,593 6,035 (4,552) (3,244) (5,400) 441 349 635

Operating Cash Flow $ 78 $ 55 $ 64 $ (45) $ (33) $ (36) $ 33 $ 22 $ 28

CAPITAL EXPENDITURES

For the years ended December 31 2013 2012 2011

Canadian Division $ 1,365 $ 1,567 $ 2,031

USA Division 1,283 1,727 2,446

Market Optimization 3 7 2

Corporate & Other 61 175 131

$ 2,712 $ 3,476 $ 4,610

GOODWILL, PROPERTY, PLANT AND EQUIPMENT AND TOTAL ASSETS BY SEGMENT

Goodwill Property, Plant and Equipment Total Assets

As at December 31 2013 2012 2013 2012 2013 2012

Canadian Division $ 1,171 $ 1,252 $ 2,728 $ 2,960 $ 4,452 $ 4,748

USA Division 473 473 5,127 4,405 6,350 5,664

Market Optimization - - 91 106 161 161

Corporate & Other - - 2,089 2,280 6,685 8,127

$ 1,644 $ 1,725 $ 10,035 $ 9,751 $ 17,648 $ 18,700

GOODWILL, PROPERTY, PLANT AND EQUIPMENT AND TOTAL ASSETS BY GEOGRAPHIC REGION

Goodwill Property, Plant and Equipment Total Assets

As at December 31 2013 2012 2013 2012 2013 2012

Canada $ 1,171 $ 1,252 $ 4,772 $ 5,186 $ 10,434 $ 12,041

United States 473 473 5,263 4,565 6,996 6,639

Other Countries - - - - 218 20

$ 1,644 $ 1,725 $ 10,035 $ 9,751 $ 17,648 $ 18,700

EXPORT SALES

Sales of natural gas and liquids produced or purchased in Canada delivered to customers outside of Canada were $243 million (2012 – $177 million;

2011 – $266 million).

MAJOR CUSTOMERS

In connection with the marketing and sale of Encana’s own and purchased natural gas and liquids for the year ended December 31, 2013, the Company had

one customer which individually accounted for more than 10 percent of Encana’s consolidated revenues, net of royalties. Sales to this customer, which has

an investment grade credit rating, were approximately $815 million (2012 – two customers with sales of approximately $661 million and $534 million; 2011 –

one customer with sales of approximately $831 million).

Encana Corporation | Annual Report 2013

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

62

3. ACQUISITIONS AND DIVESTITURES

For the years ended December 31 2013 2012 2011

Acquisitions

Canadian Division $ 28 $ 139 $ 410

USA Division 156 240 105

Total Acquisitions 184 379 515

Divestitures

Canadian Division (685) (3,770) (350)

USA Division (18) (271) (1,730)

Corporate & Other (2) (2) -

Total Divestitures (705) (4,043) (2,080)

Net Acquisitions and Divestitures $ (521) $ (3,664) $ (1,565)

ACQUISITIONS

For the year ended December 31, 2013, acquisitions totaled $184 million (2012 – $379 million; 2011 – $515 million), which primarily included land and property

purchases with oil and liquids rich natural gas production potential.

DIVESTITURES

For the year ended December 31, 2013, amounts received on the sale of assets were $705 million (2012 – $4,043 million; 2011 – $2,080 million). In 2013,

divestitures were $685 million in the Canadian Division and $18 million in the USA Division.

The Canadian Division and USA Division divestitures included the following transactions:

CANADIAN DIVISION

In 2013, divestitures in the Canadian Division included the sale of the Company’s Jean Marie natural gas assets in the Greater Sierra resource play in northeast

British Columbia and other assets.

In 2012, Encana entered into a partnership agreement with a Mitsubishi Corporation subsidiary (“Mitsubishi”) to jointly develop certain Cutbank Ridge lands

in British Columbia. Under the agreement, Encana owns 60 percent and Mitsubishi owns 40 percent of the partnership. Mitsubishi agreed to invest approximately

C$2.9 billion for its partnership interest, with C$1.45 billion received in February 2012. Mitsubishi agreed to invest the remaining amount of approximately

C$1.45 billion, in addition to its 40 percent of the partnership’s future capital investment, over an expected commitment period of five years, thereby reducing

Encana’s capital funding commitment to 30 percent of the total expected capital investment.

In 2012, the Company entered into an agreement with a PetroChina Company Limited subsidiary (“PetroChina”) to jointly explore and develop certain liquids

rich natural gas Duvernay lands in Alberta. PetroChina agreed to invest approximately C$2.18 billion for a 49.9 percent working interest in the lands. PetroChina

invested C$1.18 billion in December 2012 and agreed to further invest approximately C$1.0 billion which will be used to fund half of Encana’s capital funding

commitment over an expected commitment period of four years.

In 2012, Encana entered into an agreement with a Toyota Tsusho Corporation subsidiary (“Toyota Tsusho”) under which Toyota Tsusho agreed to invest approximately

C$600 million to acquire a 32.5 percent gross overriding royalty interest in natural gas production from a portion of Encana’s Clearwater resource play. Toyota Tsusho

invested C$100 million in April 2012 and agreed to further invest approximately C$500 million over an expected commitment period of seven years.

In 2012, the Company also closed the sale of two natural gas processing plants in British Columbia and Alberta for proceeds of approximately C$920 million.

USA DIVISION

In December 2011, the Company closed the majority of the North Texas asset sale for proceeds of $836 million. The remainder of the sale closed in March 2012

for proceeds of $114 million. During 2011, Encana also sold its Fort Lupton natural gas processing plant for proceeds of $296 million and its South Piceance

natural gas gathering assets for proceeds of $547 million.

Amounts received from these transactions have been deducted from the respective Canadian and U.S. full cost pools.

Annual Report 2013 | Encana Corporation

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

63

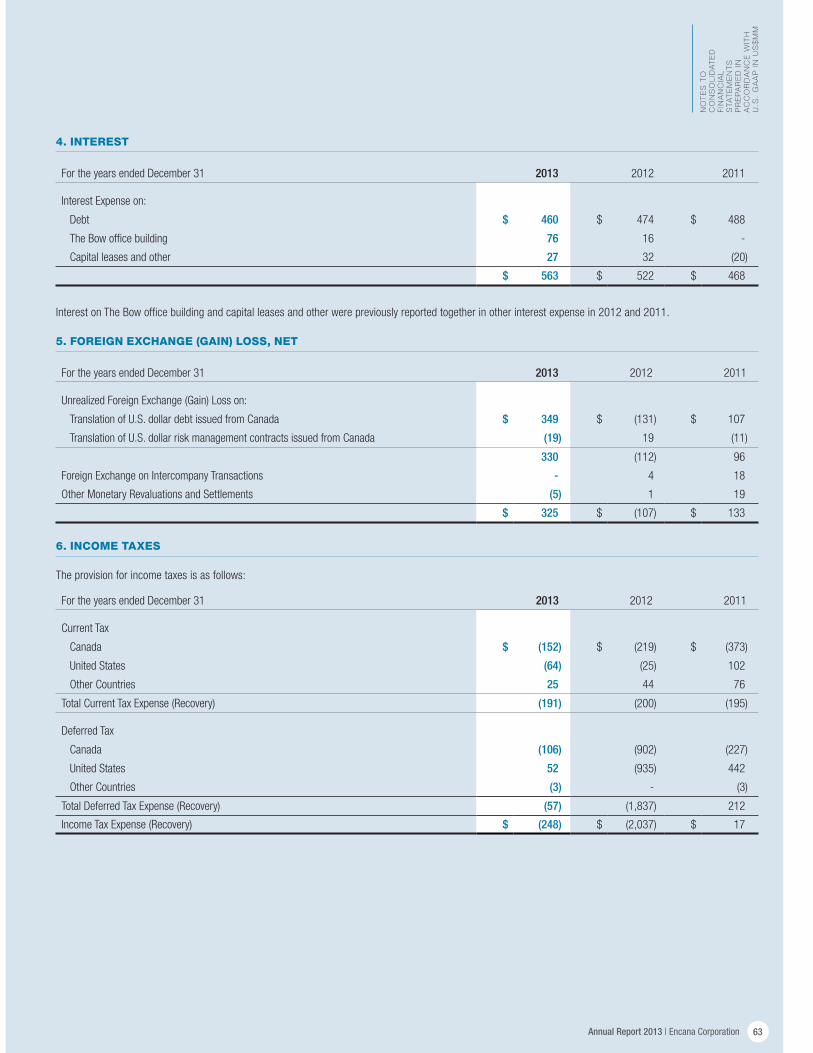

4. INTEREST

For the years ended December 31 2013 2012 2011

Interest Expense on:

Debt $ 460 $ 474 $ 488

The Bow office building 76 16 -

Capital leases and other 27 32 (20)

$ 563 $ 522 $ 468

Interest on The Bow office building and capital leases and other were previously reported together in other interest expense in 2012 and 2011.

5. FOREIGN EXCHANGE (GAIN) LOSS, NET

For the years ended December 31 2013 2012 2011

Unrealized Foreign Exchange (Gain) Loss on:

Translation of U.S. dollar debt issued from Canada $ 349 $ (131) $ 107

Translation of U.S. dollar risk management contracts issued from Canada (19) 19 (11)

330 (112) 96

Foreign Exchange on Intercompany Transactions - 4 18

Other Monetary Revaluations and Settlements (5) 1 19

$ 325 $ (107) $ 133

6. INCOME TAXES

The provision for income taxes is as follows:

For the years ended December 31 2013 2012 2011

Current Tax

Canada $ (152) $ (219) $ (373)

United States (64) (25) 102

Other Countries 25 44 76

Total Current Tax Expense (Recovery) (191) (200) (195)

Deferred Tax

Canada (106) (902) (227)

United States 52 (935) 442

Other Countries (3) - (3)

Total Deferred Tax Expense (Recovery) (57) (1,837) 212

Income Tax Expense (Recovery) $ (248) $ (2,037) $ 17

Encana Corporation | Annual Report 2013

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

64

The following table reconciles income taxes calculated at the Canadian statutory rate with the actual income taxes:

For the years ended December 31 2013 2012 2011

Net Earnings (Loss) Before Income Tax

Canada $ (316) $ (2,246) $ (1,973)

United States 46 (2,978) 1,477

Other Countries 258 393 518

Total Net Earnings (Loss) Before Income Tax (12) (4,831) 22

Canadian Statutory Rate 25.1% 25.0% 26.5%

Expected Income Tax (3) (1,208) 6

Effect on Taxes Resulting From:

Statutory rate and other foreign differences (42) (412) 53

Effect of legislative changes (70) - -

Non-taxable capital (gains) losses 48 (16) 20

Tax differences on divestitures and transactions (28) (307) -

Partnership tax allocations in excess of funding (41) (40) -

Amounts in respect of prior periods (103) (64) (60)

Other (9) 10 (2)

$ (248) $ (2,037) $ 17

Effective Tax Rate 2,066.7% 42.2% 77.3%

Statutory rate and other foreign differences above include statutory and other rate differences and international financing, which were previously reported

separately in 2012 and 2011.

The net deferred income tax asset (liability) consists of:

As at December 31 2013 2012

Deferred Income Tax Assets

Property, plant and equipment $ 786 $ 995

Compensation plans 109 113

Accrued and unpaid expense 61 65

Non-capital and net capital losses carried forward 429 119

Alternative minimum tax and foreign tax credits 199 122

Less valuation allowance (6) -

Other 95 61

Deferred Income Tax Liabilities

Property, plant and equipment (407) -

Risk management (63) (176)

Unrealized foreign exchange gains (120) (205)

Other (29) (14)

Net Deferred Income Tax Asset (Liability) $ 1,054 $ 1,080

The net deferred income tax asset (liability) is reflected in the Consolidated Balance Sheet as follows:

As at December 31 2013 2012

Current deferred income tax asset $ 118 $ 23

Non-current deferred income tax asset 939 1,116

Current deferred income tax liability (3) (59)

Net Deferred Income Tax Asset (Liability) $ 1,054 $ 1,080

Annual Report 2013 | Encana Corporation

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

65

Tax pools, loss carryforwards, charitable donations and tax credits that can be utilized in future years are as follows:

As at December 31 2013 Expiration Date

Canada

Tax pools $ 4,792 Indefinite

Net capital losses 269 Indefinite

Non-capital losses 505 2015 - 2033

Charitable donations 26 2015 - 2018

United States

Tax basis $ 3,642 Indefinite

Non-capital losses 647 2033

Charitable donations 6 2018

Alternative minimum tax credits 55 Indefinite

Foreign tax credits (net of valuation allowance) 138 2021 - 2023

As at December 31, 2013, approximately $2.6 billion of Encana’s unremitted earnings from its foreign subsidiaries were considered to be permanently reinvested

outside of Canada and, accordingly, Encana has not recognized a deferred tax liability for Canadian income taxes in respect of such earnings. If such earnings were

to be remitted to Canada, Encana may be subject to Canadian income taxes and foreign withholding taxes. However, determination of any potential amount of

unrecognized deferred income tax liabilities is not practicable.

The following table presents changes in the balance of Encana’s unrecognized tax benefits excluding interest:

For the years ended December 31 2013 2012

Balance, Beginning of Year $ 164 $ 165

Additions for tax positions taken in the current year - 2

Additions for tax positions of prior years - 3

Reductions for tax positions of prior years (2) (2)

Lapse of statute of limitations (4) (4)

Settlements (29) (4)

Foreign currency translation (10) 4

Balance, End of Year $ 119 $ 164

The unrecognized tax benefit is reflected in the Consolidated Balance Sheet as follows:

For the years ended December 31 2013 2012

Income tax receivable $ - $ 59

Other liabilities and provisions (See Note 13) 133 134

Current deferred income tax liability 2 5

Non-current deferred income tax asset (16) (34)

Balance, End of Year $ 119 $ 164

If recognized, all of Encana’s unrecognized tax benefits as at December 31, 2013 would affect Encana’s effective income tax rate. Encana does not anticipate

that the amount of unrecognized tax benefits will significantly change during the next 12 months.

Encana recognizes interest accrued in respect of unrecognized tax benefits in interest expense. During 2013, Encana recognized a recovery of $6 million

(2012 – $8 million; 2011 – $18 million) in interest expense. As at December 31, 2013, Encana had a liability of $1 million (2012 – $3 million) for interest

accrued in respect of unrecognized tax benefits.

Encana Corporation | Annual Report 2013

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

66

Included below is a summary of the tax years, by jurisdiction, that remain subject to examination by the taxation authorities.

Jurisdiction Taxation Year

Canada - Federal 2005 - 2013Canada - Provincial 2005 - 2013United States - Federal 2008 - 2013United States - State 2008 - 2013Other 2012 - 2013

Encana and its subsidiaries file income tax returns primarily in Canada and the United States. Issues in dispute for audited years and audits for subsequent years

are ongoing and in various stages of completion.

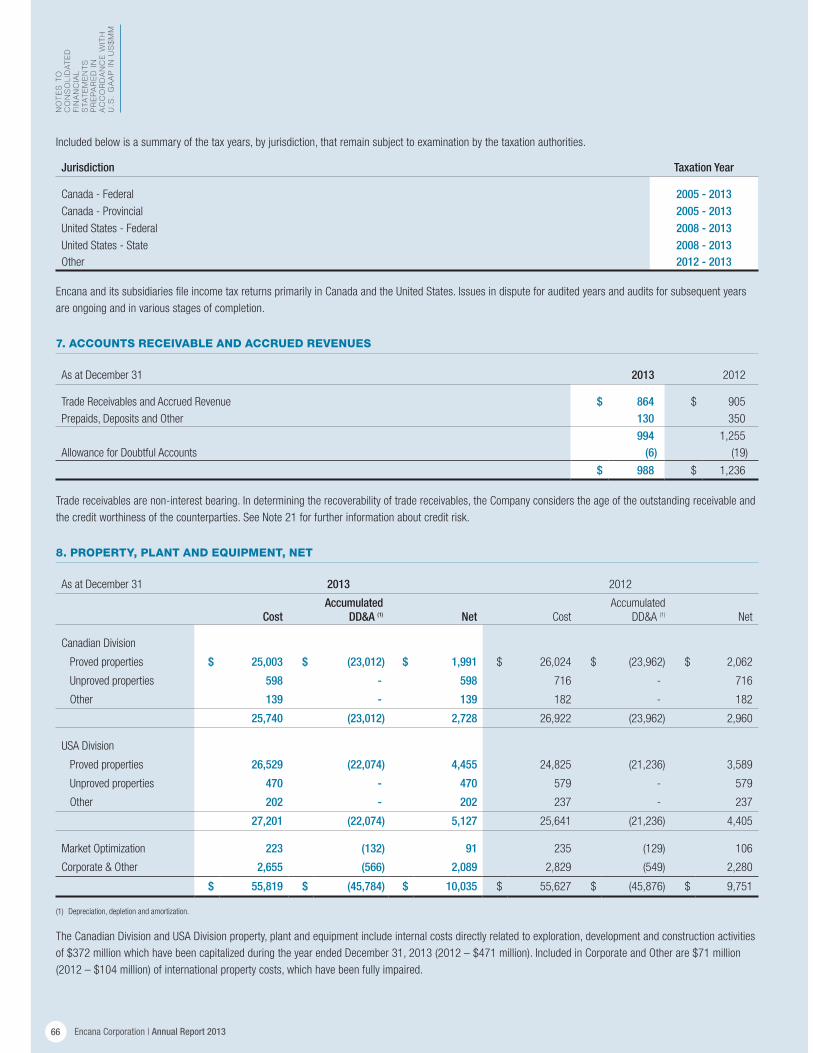

7. ACCOUNTS RECEIVABLE AND ACCRUED REVENUES

As at December 31 2013 2012

Trade Receivables and Accrued Revenue $ 864 $ 905

Prepaids, Deposits and Other 130 350

994 1,255

Allowance for Doubtful Accounts (6) (19)

$ 988 $ 1,236

Trade receivables are non-interest bearing. In determining the recoverability of trade receivables, the Company considers the age of the outstanding receivable and

the credit worthiness of the counterparties. See Note 21 for further information about credit risk.

8. PROPERTY, PLANT AND EQUIPMENT, NET

As at December 31 2013 2012

Cost Accumulated

DD&A (1) Net Cost

Accumulated

DD&A (1) Net

Canadian Division

Proved properties $ 25,003 $ (23,012) $ 1,991 $ 26,024 $ (23,962) $ 2,062

Unproved properties 598 - 598 716 - 716

Other 139 - 139 182 - 182

25,740 (23,012) 2,728 26,922 (23,962) 2,960

USA Division

Proved properties 26,529 (22,074) 4,455 24,825 (21,236) 3,589

Unproved properties 470 - 470 579 - 579

Other 202 - 202 237 - 237

27,201 (22,074) 5,127 25,641 (21,236) 4,405

Market Optimization 223 (132) 91 235 (129) 106

Corporate & Other 2,655 (566) 2,089 2,829 (549) 2,280

$ 55,819 $ (45,784) $ 10,035 $ 55,627 $ (45,876) $ 9,751

(1) Depreciation, depletion and amortization.

The Canadian Division and USA Division property, plant and equipment include internal costs directly related to exploration, development and construction activities

of $372 million which have been capitalized during the year ended December 31, 2013 (2012 – $471 million). Included in Corporate and Other are $71 million

(2012 – $104 million) of international property costs, which have been fully impaired.

Annual Report 2013 | Encana Corporation

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

67

For the year ended December 31, 2013, the Company recognized a ceiling test impairment of nil (2012 – $1,822 million; 2011 – $2,249 million) in the Canadian

cost centre and nil (2012 – $2,842 million; 2011 – nil) in the U.S. cost centre. The impairments resulted primarily from the decline in the 12-month average

trailing natural gas prices which reduced proved reserves volumes and values.

The 12-month average trailing prices used in the ceiling test calculations reflect benchmark prices adjusted for basis differentials to determine local reference

prices, transportation costs and tariffs, heat content and quality. The benchmark prices are disclosed in Note 24.

CAPITAL LEASE ARRANGEMENTS

The Company has several lease arrangements that are accounted for as capital leases, including an office building, equipment and an offshore production platform.

In December 2013, Encana commenced commercial operations at its Deep Panuke facility located offshore Nova Scotia following successful completion of the

Production Field Centre (“PFC”) and issuance of the Production Acceptance Notice. As at December 31, 2013, Canadian Division property, plant and equipment

and total assets include the PFC, which is under a capital lease totaling $536 million. As at December 31, 2012, $612 million in accumulated costs related to the

PFC were recorded as an asset under construction.

During 2011, the Company entered into a capital lease arrangement in the U.S. whereby the beneficial rights of ownership of specific equipment would

be conveyed to Encana over five years. The Company recorded an asset under capital lease with a corresponding capital lease obligation totaling $158 million,

which was subsequently paid by Encana.

As at December 31, 2013, the total carrying value of assets under capital lease was $683 million (2012 – $207 million).

OTHER ARRANGEMENT

As at December 31, 2013, Corporate and Other property, plant and equipment and total assets include Encana’s accumulated costs to date of $1,617 million

(2012 – $1,668 million) related to The Bow office building. In 2012, Encana assumed partial occupancy of The Bow office premises and commenced payments

to the third party developer under a 25-year lease agreement. As of March 31, 2013, Encana had assumed full occupancy of the building. The Bow asset is being

depreciated over the 60-year estimated life of the building. At the conclusion of the 25-year term, the remaining asset and corresponding liability are expected

to be derecognized as disclosed in Note 13.

Liabilities for the capital lease arrangements and The Bow office building are included in other liabilities and provisions in the Consolidated Balance Sheet and

are disclosed in Note 13.

9. OTHER ASSETS

As at December 31 2013 2012

Deferred Charges and Debt Transaction Costs $ 58 $ 61

Long-Term Receivables 184 180

Long-Term Investments and Other 284 225

$ 526 $ 466

10. GOODWILL

As at December 31 2013 2012

Canada $ 1,171 $ 1,252

United States 473 473

$ 1,644 $ 1,725

There have been no additions or dispositions of goodwill during 2013 or 2012 and the Company has not recognized any previous goodwill impairments.

The change in the Canada goodwill balance between December 31, 2013 and December 31, 2012 reflects movements due to foreign currency translation.

Goodwill was assessed for impairment as at December 31, 2013 and December 31, 2012. The fair values of the Canada and United States reporting units

were determined to be greater than the respective carrying values of the reporting units. Accordingly, no goodwill impairments were recognized.

Encana Corporation | Annual Report 2013

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO

RD

AN

CE

WIT

H

U.S

. G

AA

P I

N U

S$

MM

68

11. ACCOUNTS PAYABLE AND ACCRUED LIABILITIES

As at December 31 2013 2012

Trade Payables $ 265 $ 417

Capital Accruals 398 415

Royalty and Production Accruals 473 497

Other Accruals 514 490

Interest Payable 111 117

Outstanding Disbursements 2 27

Current Portion of Capital Lease Obligations (See Note 13) 66 7

Current Portion of Asset Retirement Obligation (See Note 14) 66 33

$ 1,895 $ 2,003

Payables and accruals are non-interest bearing. Interest payable represents amounts accrued related to Encana’s unsecured notes as disclosed in Note 12.

12. LONG-TERM DEBT

As at December 31 Note C$ Principal Amount 2013 2012

Canadian Dollar Denominated Debt

Revolving credit and term loan borrowings A $ - $ - $ -

Canadian Unsecured Notes: B

5.80% due January 18, 2018 750 705 754

$ 750 705 754

U.S. Dollar Denominated Debt

Revolving credit and term loan borrowings A - -

U.S. Unsecured Notes: B

4.75% due October 15, 2013 - 500

5.80% due May 1, 2014 1,000 1,000

5.90% due December 1, 2017 700 700

6.50% due May 15, 2019 500 500

3.90% due November 15, 2021 600 600

8.125% due September 15, 2030 300 300

7.20% due November 1, 2031 350 350

7.375% due November 1, 2031 500 500

6.50% due August 15, 2034 750 750

6.625% due August 15, 2037 500 500

6.50% due February 1, 2038 800 800

5.15% due November 15, 2041 400 400

6,400 6,900

Total Principal F 7,105 7,654

Increase in Value of Debt Acquired C 40 46

Debt Discounts D (21) (25)

Current Portion of Long-Term Debt E (1,000) (500)

$ 6,124 $ 7,175

Annual Report 2013 | Encana Corporation

NO

TE

S T

O

CO

NS

OL

IDA

TE

D

FIN

AN

CIA

L S

TAT

EM

EN

TS

P

RE

PA

RE

D I

N

AC

CO