Embed Size (px)

Citation preview

Page 1

UNITAID

Joint UNICEF, UNFPA & WHO Meeting with Manufacturers & Suppliers

Copenhagen, Denmark, 23 Nov. 2015

Malaria Medicines Market

Perspectives

Alexandra Cameron

Ambachew Yohannes

Page 2

Outline

• Gaps in access to antimalarial tools

• Malaria medicines & diagnostics market

overview

• Interventions needed to address challenges

• UNITAID catalytic interventions

Page 3Page 3

Gaps in Access to Key Antimalarial Tools Persist

Page 4

Malaria Medicines Landscape Anlysis Key Findings (1)

We need

• Improved demand & supply forecast,

• More products for severe malaria.

• Innovative market interventions.

ACTs Market Overview• High market growth (392m in 2013)• Increasing market share for FDCs

& generics• High volumes co-exist with low

access (public sector stock-outs)

Market Shortcoming (in brief) • Low market share of ACTs (private

sector) • High ACT retail prices compared to

older treatments (SP, CQ)• Low availability of prequalified

products for severe malaria

Page 5

Preventive Treatments (SP, SP+AQ) - Market Overview• Few prequalified products• Many generics, low-cost, • Limited incentives for quality-

assured supply• SP resistance threatens future

demand

Market Shortcomings (in Brief)• No alternative to SP for IPTp &

SMC • High quality control failure rates

for SP (28%)• No child-friendly presentations• Low coverage (SMC, IPTp)

Malaria Medicines Landscape Analysis Key Findings (2)

We need

• More quality assured products for SMC & IPTp.

• Child-friendly presentation for SMC, packaging for IPTp

Page 6

Market Overview• Rapid growth in RDT market (45million in

2008 to 319 million in 2013) • Declining prices • Market consolidation around a few

suppliers (90% RDTs from 2 suppliers)

Market Shortcomings (in Brief)• Challenges related to the quality of RDTs • Concentration of suppliers and

associated risk of market disruptions• limited uptake of RDTs • Lack of robust RDT tests for malaria

elimination settings

Malaria Diagnostics Landscape Analysis Key Findings (1)

We need

• Better quality control.

• Improved uptake of RDTs

• New dx for specific settings/groups

Page 7

Next UNITAID Landscape Reports

• Up to date data and information through 2015

• More data & evidence from

– ACT, Artemisinin and RDTs demand forecast

– API market intelligence

• Findings from the ACT Watch market research

– preliminary data shows some major improvements and challenges

Page 8

ACTwatch is a research project implemented by PSI and Ministries of Health in 13 countries

• 45 outlet surveys conducted between 2008-2015

• Most outlet surveys are conducted at national level

• Outlet surveys measure availability, price, and market share in the public and private sectors for malaria medicines and diagnostics

Selected results from ACTwatch

Page 9

• Quality-assured ACTs account for one-third to one-half of all antimalarials distributed in all survey countries, except DRC.

• Non quality-assured ACTs are distributed in some (but not all) countries with striking market share in DRC (~40%) and Zambia (~25%), and a growing problem in Kenya (~20%).

• SP accounts for ¼ to ½ of all private sector antimalarial distribution in each survey country, and 75% in Zambia.

Antimalarials Relative Market Share (1)

Page 10

• Distribution of other non-artemisinin therapies including chloroquineand quinine is declining but these still capture 20-30% of the total market share in Benin, DRC, Madagascar and Nigeria.

• Oral AMT is no longer distributed with the exception of relatively small market share in Nigeria. However, 1 in 4 private providers in Nigeria stock oral AMT.

• Non-oral AMT relative market share remains low with the notable exception of private sector market share in DRC (7%).

Antimalarials Relative Market Share (2)

Page 11

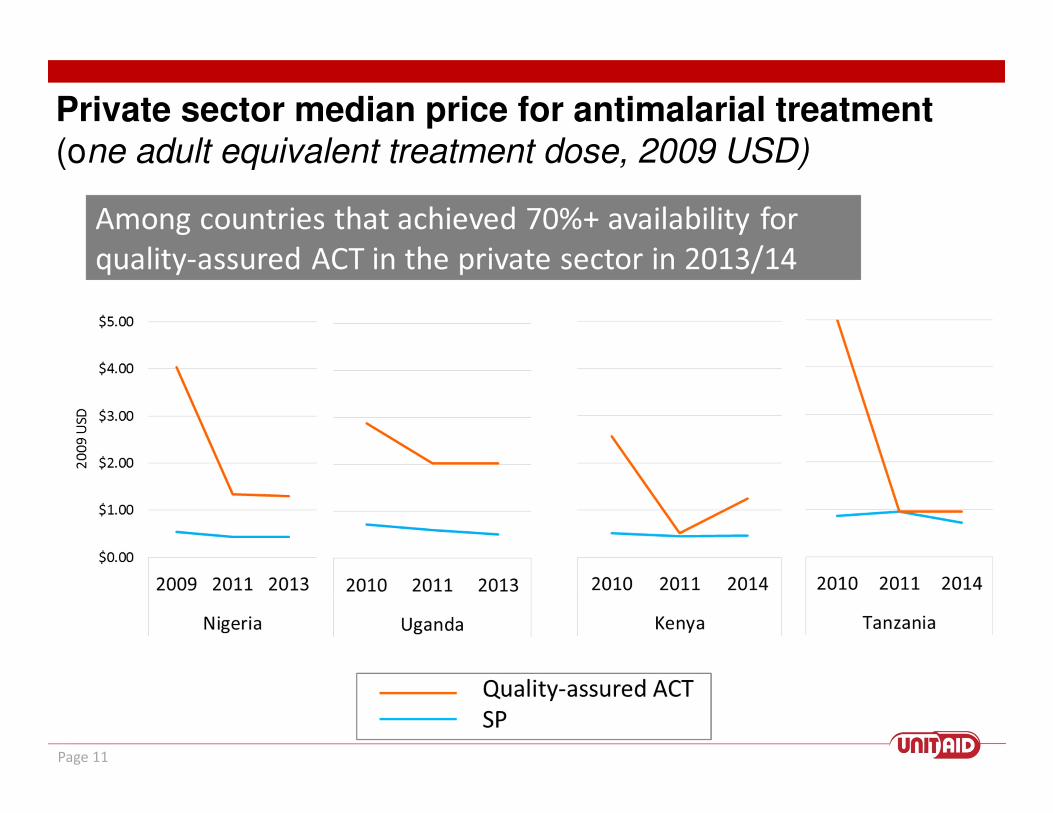

Private sector median price for antimalarial treatment(one adult equivalent treatment dose, 2009 USD)

Page 12

Malaria Diagnostics Market (1)

• Confirmatory testing is largely not available among private sector outlets providing antimalarial medicines.

• Limited availability of malaria testing in the private sector is a key barrier to appropriate case management given large market share of antimalarials in this sector.

• Most testing in the public sector by RDTs, except in DRC & Kenya where microscopy is more common.

• In most countries, more testing in the private sector by microscopy than by RDTs.

Page 13

UNITAID Catalytic Interventions

• ACTs, Artemisninin & RDT demand forecast.

• ACT market intelligence research

• API market intelligence

Market

Intelligence

Quality

Availability

• Artesunate injection & suppositories.

• Dispersible SP+AQ

• RDTs Quality Assurance

Demand

Creation &

uptake

• Private Sector RDTs

• Injectable Artesunate uptake

• Seasonal Malaria Chemoprevention

Page 14

UNITAID landscape & technical reportshttp://www.unitaid.eu/en/resources/publications/technical-reports

sawyerj9

Slide 14

sawyerj9 The most recent ACT forecasting report is Dec 2012, which seems a bit old.

If we have such a slide would be good to summarize the malaria reports/info available from a range of organizations/sources and not just UNITAID.SAWYER, Jacqueline K., 12/11/2015

Page 15

Thank you

UNITAID T: +41 22 791 55 03

F: +41 22 791 48 90

E-mail: [email protected]

http://www.unitaid.org